session+1+value+framework

DESCRIPTION

Strategy NotesTRANSCRIPT

Introduction

Stern School at New York University Strategy Core J.P. Eggers

Agenda for Session 1

• Introduce the subject of strategy • Introduce this course (and a little about me) • Talk about Performance Indicator & golf balls • Discuss value creation & capture perspective

But first… A LITTLE INTERACTION

• Contestants are appointed CEOs of average firms in different industries

• Each quarter the CEO with the lowest profitability is fired

• Pilot: 3 contestants – VOLUNTEERS?

Pilot industry lineup

• Average firm in the following industries – U.S. airline carriers

• i.e. Southwest, US Airways, JetBlue

– U.S. pharmaceuticals • i.e. Johnson & Johnson, Eli Lilly, Pfizer

– U.S. personal computers and peripherals • i.e. Dell, Apple, Hewlett-Packard

Variation in performance across industries Average economic profits of U.S. industries (ROE/cost of capital spread)

Reproduced from Ghemawat (2004), Strategy and the Business Landscape

Avg. Spread (1984-2002)

Avg. Equity ($B) (1984-2002)

(20%)

(10%)

0%

10%

20%

30%

40%

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000

Tele ServiceSemiconduct

Air TransportTextile

Steel

Railroad

Paper & For.

For El/Ent.

For Telecom

PowerEntertain

Toiletry & Cosmetic

Soft DrinksPharmaceutical

Med SuppliesComputer Software

Tobacco

PublishingFinancial Services

BankRetail Store

Petro-Integergrated

Aerospace/Defense

Computers & PeripheralsAuto Parts

Building MaterialsInsurance Property & Casualty

Auto & Truck

Avg. Spread (1984-2002)

Avg. Equity ($B) (1984-2002)

(20%)

(10%)

0%

10%

20%

30%

40%

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000

Tele ServiceSemiconduct

Air TransportTextile

Steel

Railroad

Paper & For.

For El/Ent.

For Telecom

PowerEntertain

Toiletry & Cosmetic

Soft DrinksPharmaceutical

Med SuppliesComputer Software

Tobacco

PublishingFinancial Services

BankRetail Store

Petro-Integergrated

Aerospace/Defense

Computers & PeripheralsAuto Parts

Building MaterialsInsurance Property & Casualty

Auto & Truck

Variation in profitability across three industries N

et P

rofit

Mar

gin

in 2

009 13.6%

8.8%

-3.1%

Pharma Computers Airlines

Let’s try again…

• Different format for reality TV show – “Average CEO by Market Position within Industry”? – “Competing CEOs in a Particular Market Position”?

• All pharmaceuticals! – Proprietary drug manufacturers

• i.e. Eli Lilly, Pfizer – Generic drug manufacturers

• i.e. Teva, Ivax – Biotech firms

• i.e. Amgen, Biogen

Variation in Performance within Industries: Market Position

Wei

ghte

d N

et P

rofit

Mar

gin

in 2

009

All Pharma

Proprietary Generic Biotech

13.6%

16.4%

-0.4% 0.4%

Variation in Performance within Market Position: Proprietary Manufacturers

Net

Pro

fit M

argi

n in

200

9

Glaxo Eli Lilly Pfizer Bristol-Myers

19.8% 16.9%

24.8%

17.6%

Some Firms Seem to Have an Enduring Advantage

Firms Achieving 20 or More Years of Persistent Superior Performance (ROA significantly above industry average), 1974-1997

Pharma: American Home Products, Lilly Publishing: Plenum Computing: Hewlett Packard Medical Instr. Stryker Trucking: UPS Paper and Board: 3M Grocery: Albertsons, Brunos, Winn Dixie, Weis, Publix Restaurants: Bob Evans, Luby’s, McDonalds, Ruby Tuesday

Firms Achieving 50 Years of Persistent Superior Performance: American Home Products, Lilly, 3M

adapted from Wiggins and Ruefli, Organization Science, 2002.

from McGahan & Porter, Strategic Mgmt Journal, 1997

So, what really matters, and how much?

4%

32%

2%19%

43%Business Unit

Year

Corporate Parent

Industry

Unexplained Variation

Drivers of variation in firm profits (ROA) over time (1981-1994)

Industry?

Business Unit?

Something else important?

Now we know that there are significant differences between firms (both at any moment and over time). But, what is the “X Factor,” that secret ingredient that makes one firm more successful than another in the same business?

Is it luck? Is it a brilliant idea? Is it hard work? Is it good people working together?

We will admit to the possibility of all of these things

The Elements of Strategy?

• There are many definitions of strategy, but here are a good one-and-a-half: – Strategy is “the determination of the long-run goals and objectives of an

enterprise, and the adoption of courses of action and the allocation of resources necessary for carrying out these goals.”

• Alfred Chandler, Strategy and Structure – “Strategy is the … plan that integrates an organization’s major goals.”

• James Brian Quinn, Strategies for Change

• The goal of strategy is sustainable competitive advantage: – Firms to do well when they continue to create value and continue to

attract participants, even when other firms are making efforts to attract the same participants. We’ll call this a firm’s “sustainable competitive advantage.”

Course Overview

Stern School at New York University Strategy Core J.P. Eggers

Motivation for this class

This course is motivated by a simple question:

“What allows certain firms in certain industries to earn positive economic profits while others deliver negative returns?”

We will investigate five “types” of answers: • Structural answer – the external environment • Organizational answer – the activities and resources of the firm • Scope answer – the vertical and horizontal boundaries of the firm • Growth answer – the ways in which the firm grows over time • Managerial answer – decision-making

Things to know about strategy – Namely, that is very messy

• No single answer – Context-specific – Firm-specific

• No single framework – Multiple tools to consider – Lots of overlap

• Our goals here are: – Build a “toolkit” of frameworks, tools, and perspectives – Help you understand when some tools work better than others – Help you understand the limitations of these tools – Build “strategic thinking” perspective on business problems

Learning components

• Readings – Normally 0-2 readings per 3 hour class block – Posted on NYU Classes (some in coursepack)

• Video lectures – Developing a series of short (15-25 minute) video lectures that replace some

readings and some in-class lectures – Ensures that we have more time for discussion – Some will help to wrap the previous week, some will lead into the coming

week • Lecturettes

– Some remaining short (<30 minute) content-driven sessions, each covering a specific topic

– Slides will be available on NYU Classes before class (though censored in some cases)

• Cases – Primary learning mechanism – Effectively one case per 3 hour class block

Case preparation

• Things to do: – Read the case closely – Read it again – Sketch out short answers to study questions on syllabus – Be creative, but try to work with concepts from readings

• Things NOT to do: – Look for outside information – deal with the cases as they are presented – Rely on former students – honor code violation, limits learning, disrupts

the class, annoys me, etc. – Think there is only one “right” answer – or that there are no wrong

answers

Grading

• Course grading is based on the following: – Participation, attendance, in-class activities 25% – Small group short assignments 20% – Group project I 15% – Group project II 15% – Individual final assignment 25%

Current events assignments

• Once per semester, each group will be responsible for one 15 minute class segment

• Build a short (1-3 slides, ~5 minutes) presentation based on a current news article related to strategy: – Describe the company – Describe the specific event/issue – Identify relevance to strategy – End with a question to prompt discussion

• Then lead a ~10 minute discussion on the topic • None this week (Session 1), but from there they are ordered by your

group number (so Group 1 goes in Session 2) – Free market – feel free to trade if you can find a partner group & make a

deal

Other expectations

• No open laptops in class, except during group exercise or breaks • No cell phones, smart phones, iPhones, etc.

• We will take 10 minute breaks during each session

• Stay in the same general space for the first few weeks, and bring your name cards

• Office hours: Wednesdays, 10-12, or by appointment – Email ([email protected]) is best way to get me – Office is Tisch 715

Obligatory little bit about me…

• Education: – BA, Amherst College (History) – MBA, Emory University (Strategy) – PhD, Wharton / UPenn (Strategy)

• Work experience – Pre-MBA spent 4 years in political consulting – MBA internship at J&J (ETHICON) in New Brunswick – Post-MBA spent 4 years in strategy consulting

• Kurt Salmon Associates (retail and consumer products) • Viant Inc. (defunct .com consulting) • Clients: Levis, Nordstrom, Brooks Brothers, YKK, Coca-Cola, NASCAR,

Turner Broadcasting, Burger King

Obligatory little bit about me…

• Research interests – Strategy, specifically technology strategy and managerial decision-

making – Work on how managers deal with the uncertainty posed by new

technologies – Example: Implications for firms that speculate on a new technology, but

that technology fails to be a success – what do these firms do?

• Finding me – Tisch 715, Wed 10-12 – [email protected] – @jpeggers – www.linkedin.com/in/jpeggers/

Four types of golf balls

Damage to golf balls

• Water and golf balls – Takes 12 hours to penetrate the core

• Unauthorized “refinishing” – Adds layer of coating that affects dimple size &

shape – Has implications for aerodynamics

• Unauthorized “refurbishing”

– Coating sandblasted off, then a new coating is reapplied totally different from original purpose of the ball

Sources of support

• Chemistry and engineering professors at leading universities • Past president of the PGA of America • Multiple media outlets

• Why has PI found it so hard to get golf ball manufacturers to adopt its own technology? – Commercializing this innovation looks like an easy

putt with the green funneling down towards the cup. – But it has proved to be a par 10 hole. – Why?

Value Based Perspective (Creation & Capture)

Stern School at New York University Strategy Core J.P. Eggers

VALUE CREATION AND CAPTURE

The Value Creation and Capture framework links profit outcomes to strategic decisions firms make

units sold

$/unit

Benefit of product to customer; willingness-‐to-‐pay

WTP

Q Units sold, or number of customers who purchase

Average (per unit) cost of producOon

C

VALUE CREATION AND CAPTURE

The Value Creation and Capture framework links profit outcomes to strategic decisions firms make

units sold

$/unit

Benefit of product to customer; willingness-‐to-‐pay

WTP

Q Units sold, or number of customers who purchase

Average (per unit) cost of producOon

C

Value created

VALUE CREATION AND CAPTURE

The Value Creation and Capture framework links profit outcomes to strategic decisions firms make

units sold

$/unit

Benefit of product to customer; willingness-‐to-‐pay

WTP

Q Units sold, or number of customers who purchase

Average (per unit) cost of producOon

C

Value created Price customer pays for product in the market

P

Value that goes to customers as CONSUMER SURPLUS

Value that goes to firms as PROFITS

“In the news”

-‐ “Chipotle finds soluOon to grow pay increase for tomato pickers”

-‐ “Chipotle highlights food philosophy in new ads”

-‐ QuesOon: -‐ How does Chipotle’s commitment to pay tomato growers an addiOonal penny a pound affect value creaOon & capture?

An example of Value Creation and Capture: Florida tomato growers, fast food, and “fair” food

- Farm worker alliance promoOng “fair food” labor pracOces

- Has been working to get Taco Bell, McDonald’s, Burger King, and others to agree to a “penny-‐per-‐pound” raise for tomato pickers

- Would be implemented as a surcharge that growers would pass directly to pickers

COALITION OF IMMOKALEE WORKERS

TOMATO PICKERS - Earn 50 cents per 32-‐pound bucket of tomatoes picked ($10,000 -‐ 12,000 per year)

- Rate has risen only 5 cents per bucket since 1980

- Represents 90% of Florida tomato growers (major source of winter tomatoes in U.S.)

- Opposes “penny-‐per-‐pound” increase - Has threatened its growers with $100,000 fine if they pay surcharge

FLORIDA TOMATO GROWERS EXCHANGE

An example of Value Creation and Capture, continued: Chipotle and East Coast Growers and Packers

AN AGREEMENT

- In September 2009, Chipotle Mexican Grill and East Coast Growers made a sourcing agreement incorporaOng the “penny-‐per-‐pound” surcharge

- Chipotle already has a policy of using naturally raised meats and organic and local produce

- East Cost Growers withdrew from the Florida Tomato Growers Exchange

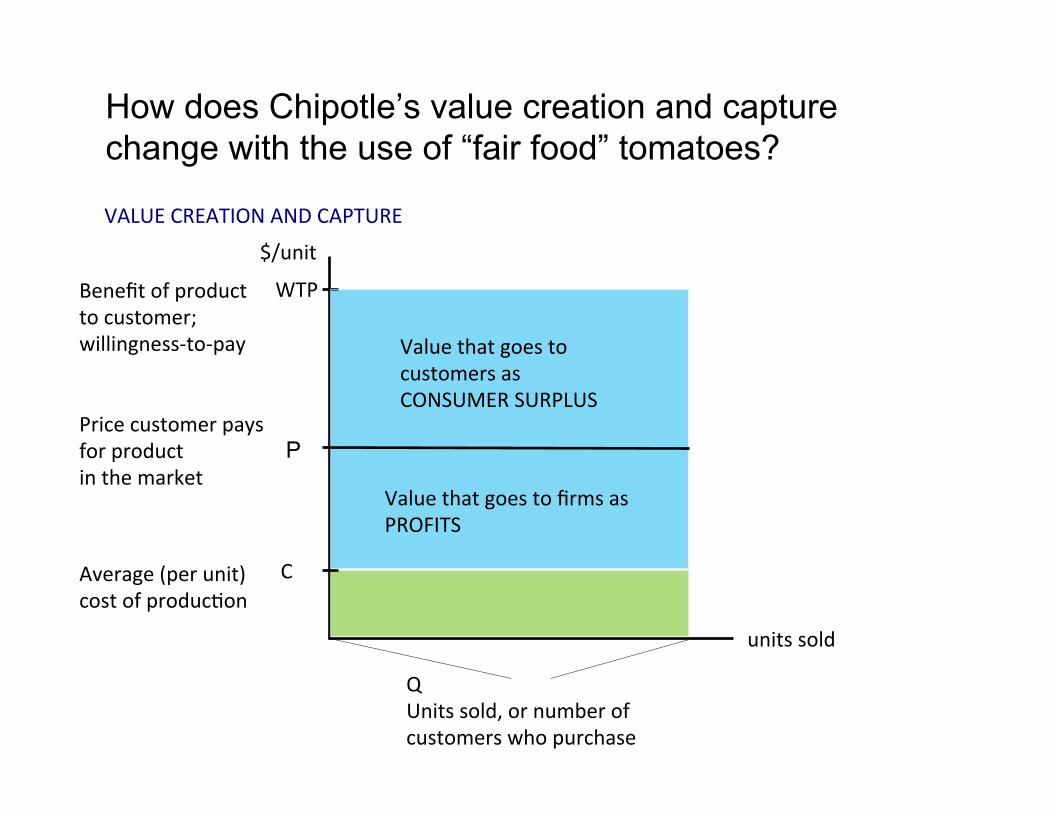

How will this affect Chipotle’s value creaOon and capture?

VALUE CREATION AND CAPTURE

How does Chipotle’s value creation and capture change with the use of “fair food” tomatoes?

units sold

$/unit

Benefit of product to customer; willingness-‐to-‐pay

WTP

Q Units sold, or number of customers who purchase

Average (per unit) cost of producOon

C

Price customer pays for product in the market

P

Value that goes to customers as CONSUMER SURPLUS

Value that goes to firms as PROFITS

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

WTP

C

P

Consumer surplus

Profits

units sold

$/unit

WTP

C

P

Consumer surplus

Profits

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

C

P

Consumer surplus

Profits

units sold

$/unit

C

P

Consumer surplus

Profits

WTP WTP

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

C

P

Consumer surplus

Profits

units sold

$/unit

C

P

Consumer surplus

Profits

WTP WTP

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

C

P

Consumer surplus

Profits

units sold

$/unit

C

P

Consumer surplus

Profits

Costs go up a lot, benefits only a lijle Difficult to increase price and profits

WTP WTP

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

C

P

Consumer surplus

Profits

units sold

$/unit

C

P

Consumer surplus

Profits

Costs go up a lot, benefits only a lijle Difficult to increase price and profits

WTP WTP

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

C

P

Consumer surplus

Profits

units sold

$/unit

C

P

Consumer surplus

Profits

Costs go up a lot, benefits only a lijle Difficult to increase price and profits

WTP WTP

VALUE CREATION AND CAPTURE

Will the use of “fair food” tomatoes increase Chipotle’s profits?

units sold

$/unit

C

P

Consumer surplus

Profits

units sold

$/unit

C

P

Consumer surplus

Profits

Costs go up a lot, benefits only a lijle Difficult to increase price and profits

Costs go up a lijle, benefits a lot Easier to increase price and profits

WTP WTP

Wrap-Up

Stern School at New York University Strategy Core J.P. Eggers

Update

• Performance Indicator has still not been able to get golf ball makers to use its technology

• Is trying to market its technology to different industries, including permanent yet reversible tattoo ink, paint for airport runways, cross walks, and medical devices

General lessons from Performance Indicator

• Spillover problems can create a disincentive to invest, even if it creates value for the firm itself

• Coordination challenges – where firms need to move together to create the most value – are difficult to count on for adopting a new innovation

• Innovations that simply redistribute value – instead of creating new value – are typically much harder to get adopted

• Value creation is not the same as value capture. Without a good way to do the latter, you can’t make money

• A customer-by-customer analysis can be very powerful. Put yourself in the customer’s shoes, since they adopt on their own and not with others

• Beware the dangers of the false analogy! (How is a golf ball not like a toothbrush?!?!)

For a strategy to be profitable it must • increase price, or • decrease average cost, or • increase quanOty sold

The overarching question for strategy: “How can firms make & sustain profits in the long run?”

= -‐ x QuanOty Average cost ) ( Price

) ( x Unit sales Cost per unit

Revenue per unit -‐ =

Profit Cost Revenue -‐ =

VALUE CREATION AND CAPTURE

The Value Creation and Capture framework links profit outcomes to strategic decisions firms make

units sold

$/unit

Benefit of product to customer; willingness-‐to-‐pay

WTP

Q Units sold, or number of customers who purchase

Average (per unit) cost of producOon

C

Value created Price customer pays for product in the market

P

Value that goes to customers as CONSUMER SURPLUS

Value that goes to firms as PROFITS

Value-based approach takeaways

• In order to be successful, strategies have to affect one or both of the following: – Drive up willingness to pay (WTP)

• May increase price • May increase sales volume

– Drive down costs – This gap is the “wedge” that firms try to drive

• Strategies also need to take into account value capture – How does the firm capture the benefits of its strategies, typically in

terms of price – We’ll discuss this in more detail in the coming sessions

Coming up next…

• (Group Project I information in a moment)

• Session 2 – CASE: Apple Computers in 2006 – READ: Porter, “Five Forces” (Classes) – VIDEO: Value Creation & Value Capture (Classes) – ASSIGNMENT: Small group (2-3 students)

• Use Porter’s Five Forces to analyze the personal computer industry in the mid-1980s based on information in the case. One page (single spaced, on side) max write up to be turned in at the start of Session 2

– Current events for Group 1

• Lunches (sign-up schedule pending, 100% optional) – Block leaders (if already elected) see me for 2 seconds after class

Industry, Positioning & Resources Group Assignment

• Assignment: As a team, select one leading firm (or SBU) in a single industry. Can be product-based or service-based. Ones you know are OK (or even advised). Use other online resources.

• Note: Industries on which we focus in class (case or discussion) are generally bad ideas for project topics. If you are at all uncertain whether your choice may qualify, please contact me.

• Deliverable: Prepare <=7 slides (as written memo) with – Basic info on the chosen company, including identification and

assessment of their strategy and how it creates & captures value – Strategic group map with 3+ other competitors – Discussion of four important activities and/or resources that the firm

uses to support its strategy – Discussion of ability of one such activity/resource to provide sustainable

competitive advantage – 2+ key takeaways (i.e. “What did I learn from doing this analysis?”)

• Due: Deposit on Blackboard before start of Session 7

Some ideas on resources for information

• NYU Virtual Business Library – http://library.nyu.edu/vbl/ – Under “Company and Financial Information”

• D&B Million Dollar DBase and Hoovers Online have basic information • Factiva provides ability to search news stories • Investext and ValueLine provide analyst reports on companies, industries • Mergent Online provides info on products, partners, etc. • Datamonitor Reports (available via EBSCO Business Source Premier) provide detailed

data and analysis on a limited set of companies • Other resources:

– Company websites (mission statements, organization structure, etc.) – Newspaper reports (often find one with detailed, inside access

• NOTE: I don’t expect “real” citations, but I want to be able to tell what YOU came up with, versus what you borrowed from somewhere (with a note on where it came from)