session three: trial balance reports

TRANSCRIPT

Fiscal Training for Board Members2015-16

Session Three: Trial Balance Reports

and Treasurer’s Report

Session Three:Trial Balance Reports and Treasurer’s Report

• Last training – budget and revenue status reports

• This training - Taking the next step up to Trial Balance• Budget and revenue gives current picture – surplus/deficit • Trial Balance gives overall picture

• Then onto the Treasurer’s Report • Show how it links back to the Trial Balance

Session Three:Trial Balance Reports

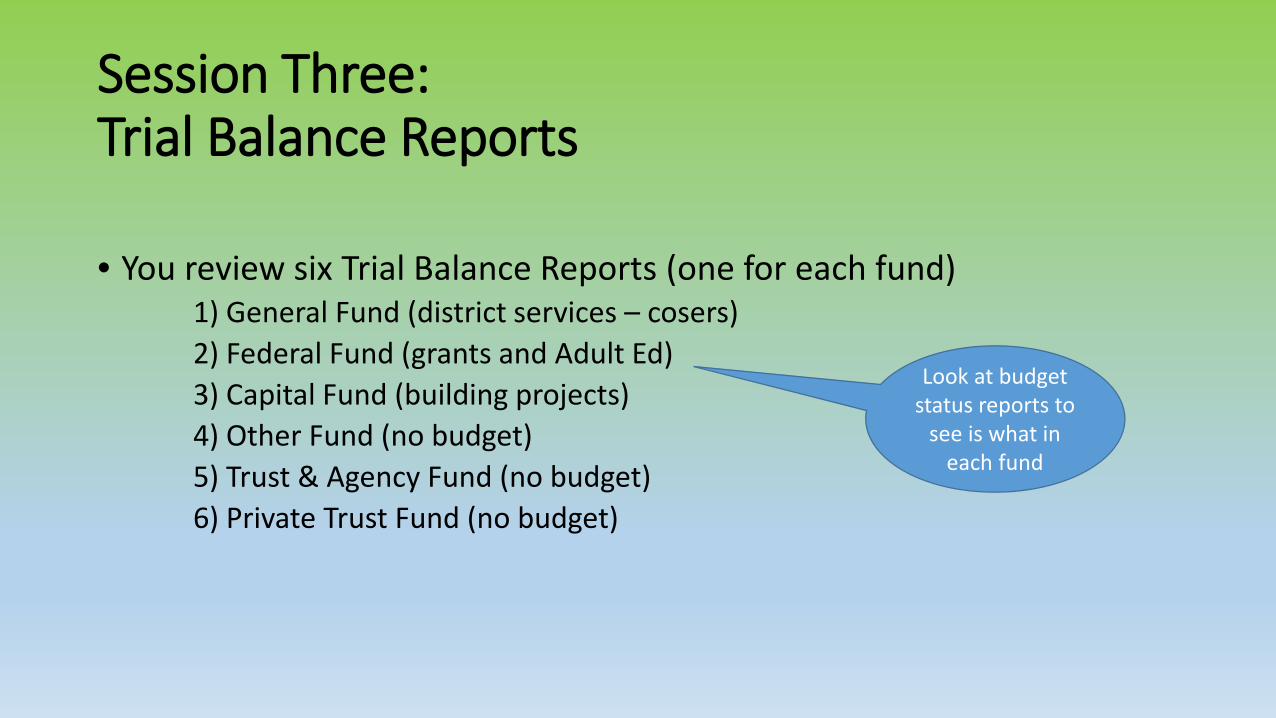

• You review six Trial Balance Reports (one for each fund)1) General Fund (district services – cosers)2) Federal Fund (grants and Adult Ed)3) Capital Fund (building projects)4) Other Fund (no budget)5) Trust & Agency Fund (no budget)6) Private Trust Fund (no budget)

Look at budget status reports to

see is what in each fund

Session Three:Trial Balance Reports

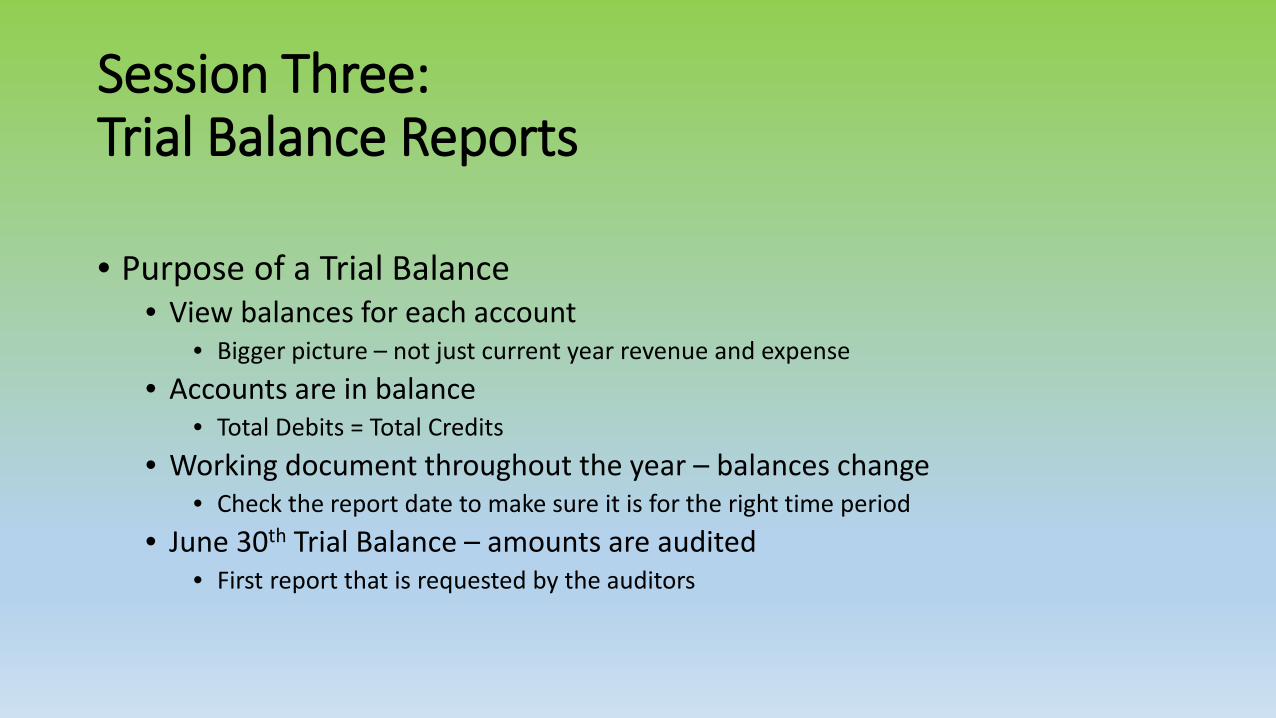

• Purpose of a Trial Balance• View balances for each account

• Bigger picture – not just current year revenue and expense• Accounts are in balance

• Total Debits = Total Credits• Working document throughout the year – balances change

• Check the report date to make sure it is for the right time period• June 30th Trial Balance – amounts are audited

• First report that is requested by the auditors

Session Three:Trial Balance Reports

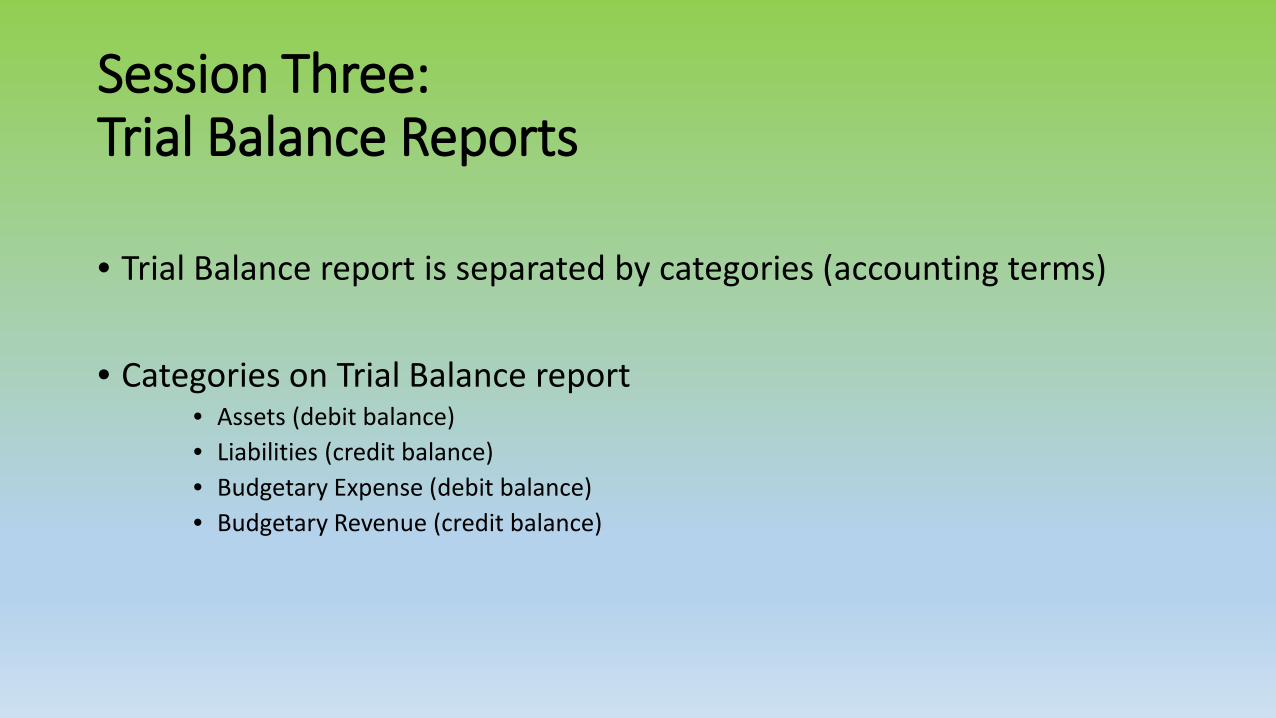

• Trial Balance report is separated by categories (accounting terms)

• Categories on Trial Balance report• Assets (debit balance)• Liabilities (credit balance)• Budgetary Expense (debit balance) • Budgetary Revenue (credit balance)

Trial Balance Report :General FundAssets = should have debit balance• Cash (operating, investments,

reserves) • Receivables ($ due to BOCES)• Prepaid Expenses

Liabilities & Reserves = should have credit balance• Surplus to Districts• Accounts Payable – current

payment to vendors• Due To & Accrued = pulling from

budgets to pay invoices• Overpayment/Collection in

Advance = contract obligations/retiree health ins

• Reserve balances

Current year – should match budget status report and revenue status report for the month

Trial Balance Report :Federal Fund (also called Special Aid Fund)Assets = should have debit balance• Cash (operating, investments,

reserves) • Receivables ($ due to BOCES),

Liabilities = should have credit balance“what we owe”• Accounts Payable – current

payment to vendors• Due to Other Funds

Current year – should match budget status report and revenue status report for the month

Trial Balance Report :Capital FundAssets = should have debit balance• Cash (operating, investments)

Liabilities = should have credit balance• Accounts Payable – current

payment to vendors• FB = Fund Balance as of 7/1

Current year – should match budget status report and revenue status report for the month

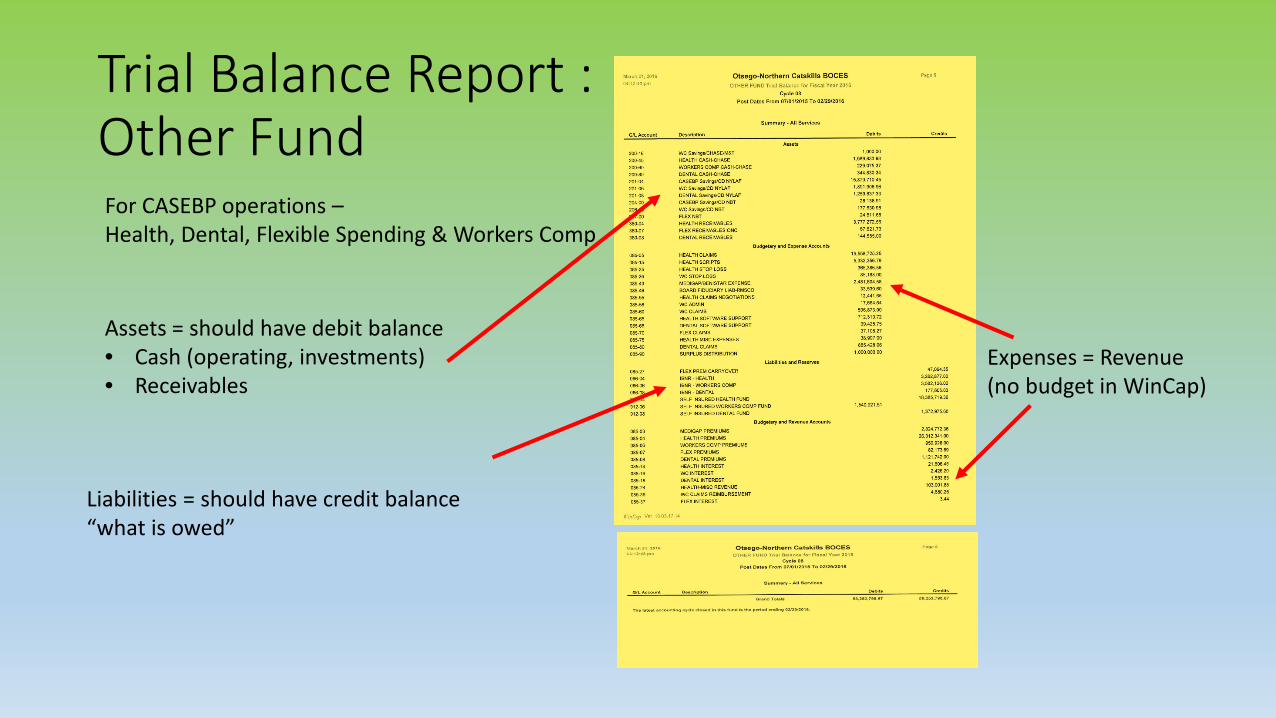

Trial Balance Report :Other Fund

Assets = should have debit balance• Cash (operating, investments) • Receivables

Liabilities = should have credit balance“what is owed”

Expenses = Revenue (no budget in WinCap)

For CASEBP operations –Health, Dental, Flexible Spending & Workers Comp

Trial Balance Report :Trust & Agency Fund

Assets = should have debit balance• Cash• Accounts Receivable – retirees owe

Liabilities – due on behalf of employee, retiree, student or Extra Class

Fund used for payroll, retiree health, student deposits and Extra Class Activity Fund– “not BOCES money”

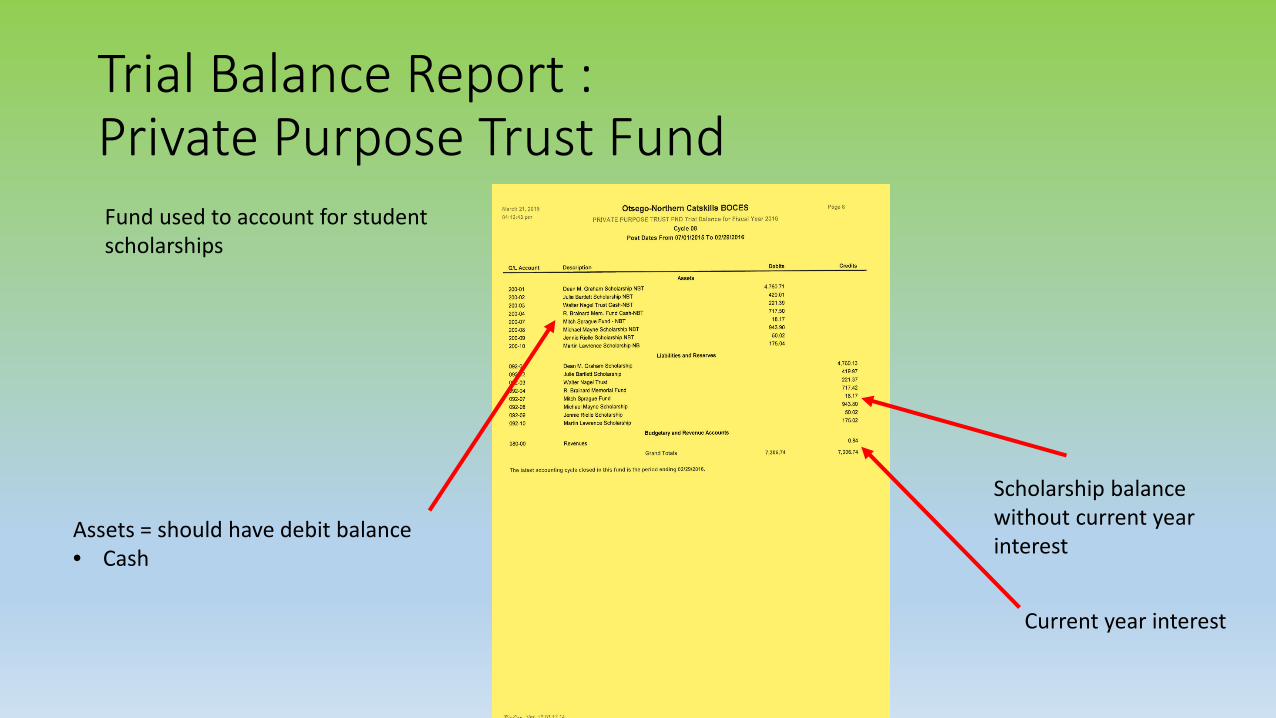

Trial Balance Report :Private Purpose Trust Fund

Assets = should have debit balance• Cash

Scholarship balance without current year interest

Fund used to account for student scholarships

Current year interest

Session Three:Trial Balance Reports

• Any questions on the Trial Balance reports?

• Moving onto the Treasurer’s Report

Session Three:Treasurer’s Report

• On each Trial Balance, there is cash.• How do we know that cash balance is correct?• Trace it to the Treasurer’s Report

• Purpose of Treasurer’s Report• Reconcile cash to bank statements• Need proper segregation of duties to ensure integrity of report

Session Three:Treasurer’s ReportMatches trial balance (our books)

Bank statement balance with outstanding deposits/checks

Shows each fund

Should match!

Treasurer

Treasurer verifies collateralizationApproved funding

of reserves

Session Three:Trial Balance Reports and Treasurer’s Report Conclusion• Things to look for…..

• Do the debits and credits look right on the Trial Balance?

• Do the balances on the Trial Balance seem in align with the operation?

• Is the Treasurer’s Report balanced?

• If you have any questions, please feel free to contact• Lynn Chase, Director of Management Services ([email protected]) (607) 588-6291 ext. 172

• Next month: • Session Four: Investment Report and Extra-Classroom Activity Fund Reports