service tax rules 1994_final

TRANSCRIPT

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 1/29

Compliance

Number

Type Category Law

Time

Based

Indirect

Taxation

Service Tax Rules, 1994

Time

Based

Indirect

Taxation

Service Tax Rules, 1994

Time

Based

Indirect

Taxation

Service Tax Rules, 1994

Time

Based

Indirect

Taxation

Service Tax Rules, 1994

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 2/29

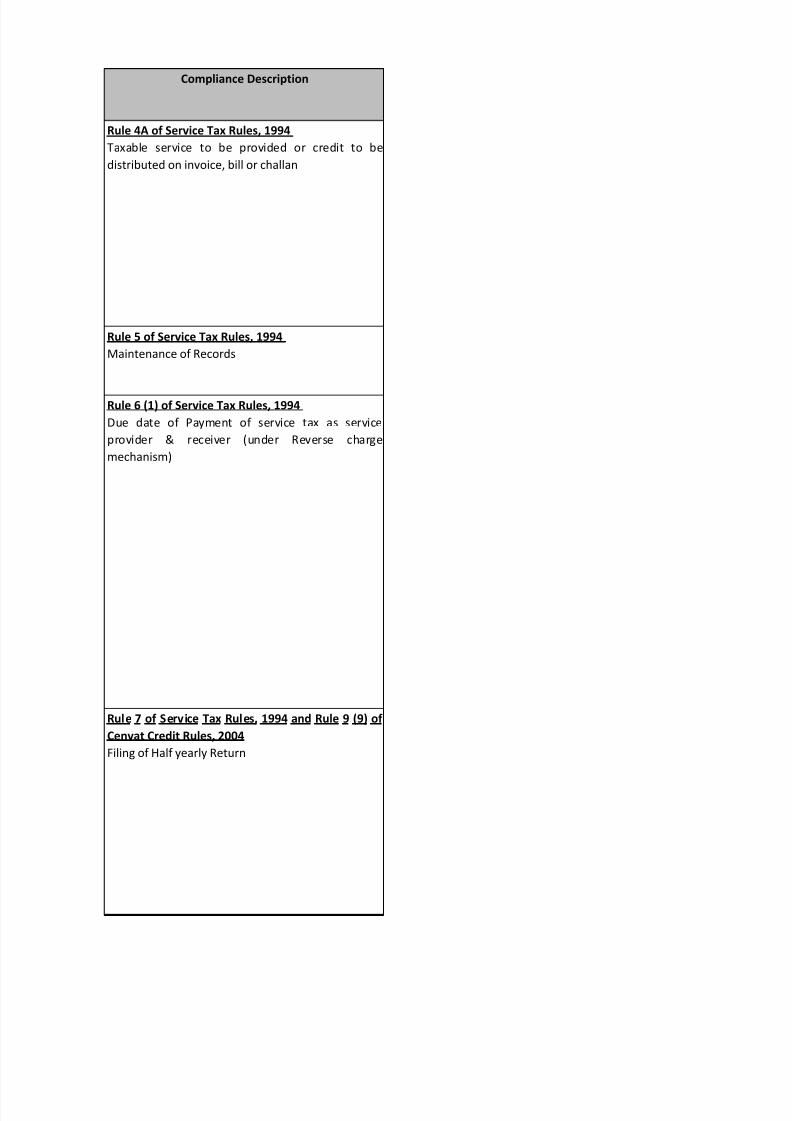

Compliance Description

Rule 4A of Service Tax Rules, 1994

Taxable service to be provided or credit to be

distributed on invoice, bill or challan

Rule 5 of Service Tax Rules, 1994

Maintenance of Records

Rule 7 of Service Tax Rules, 1994 and Rule 9 (9) of

Cenvat Credit Rules, 2004

Filing of Half yearly Return

Rule 6 (1) of Service Tax Rules, 1994

Due date of Payment of service tax as service

provider & receiver (under Reverse charge

mechanism)

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 3/29

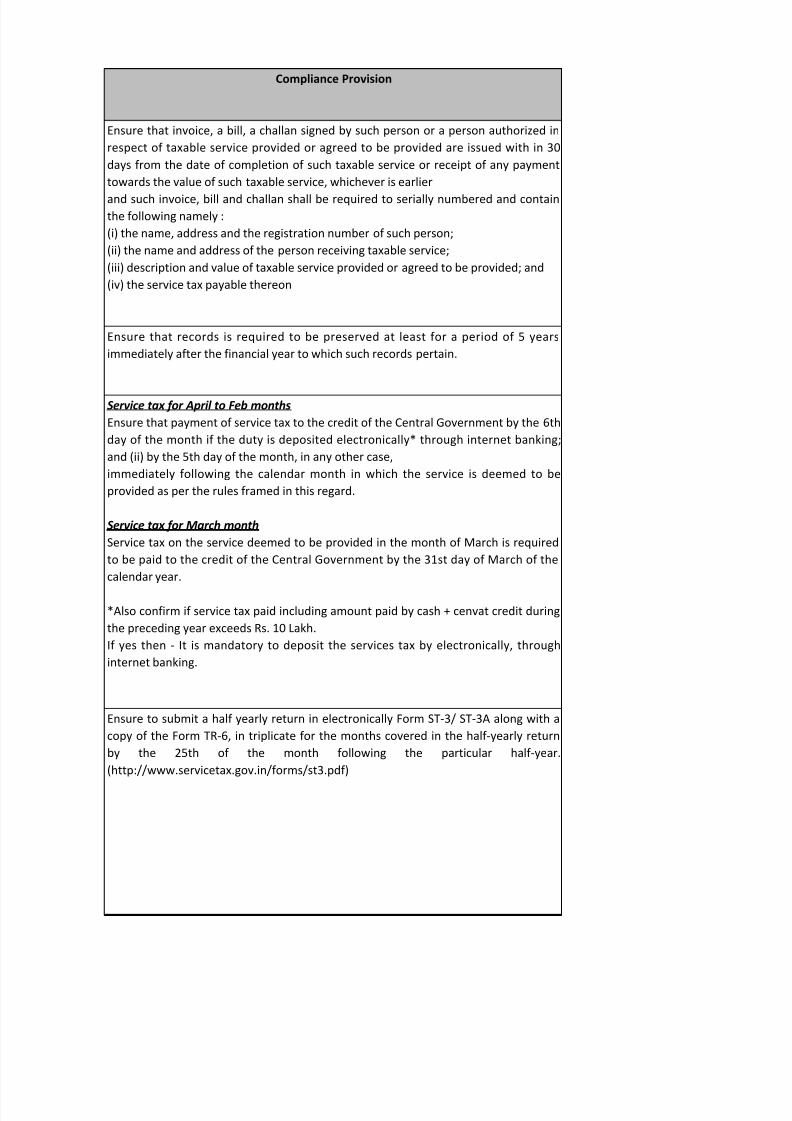

Compliance Provision

Ensure that invoice, a bill, a challan signed by such person or a person authorized in

respect of taxable service provided or agreed to be provided are issued with in 30

days from the date of completion of such taxable service or receipt of any payment

towards the value of such taxable service, whichever is earlier

and such invoice, bill and challan shall be required to serially numbered and containthe following namely :

(i) the name, address and the registration number of such person;

(ii) the name and address of the person receiving taxable service;

(iii) description and value of taxable service provided or agreed to be provided; and

(iv) the service tax payable thereon

Ensure that records is required to be preserved at least for a period of 5 years

immediately after the financial year to which such records pertain.

Ensure to submit a half yearly return in electronically Form ST-3/ ST-3A along with a

copy of the Form TR-6, in triplicate for the months covered in the half-yearly return

by the 25th of the month following the particular half-year.

(http://www.servicetax.gov.in/forms/st3.pdf)

Service tax for April to Feb months

Ensure that payment of service tax to the credit of the Central Government by the 6th

day of the month if the duty is deposited electronically* through internet banking;

and (ii) by the 5th day of the month, in any other case,

immediately following the calendar month in which the service is deemed to be

provided as per the rules framed in this regard.

Service tax for March month

Service tax on the service deemed to be provided in the month of March is required

to be paid to the credit of the Central Government by the 31st day of March of the

calendar year.

*Also confirm if service tax paid including amount paid by cash + cenvat credit during

the preceding year exceeds Rs. 10 Lakh.

If yes then - It is mandatory to deposit the services tax by electronically, through

internet banking.

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 4/29

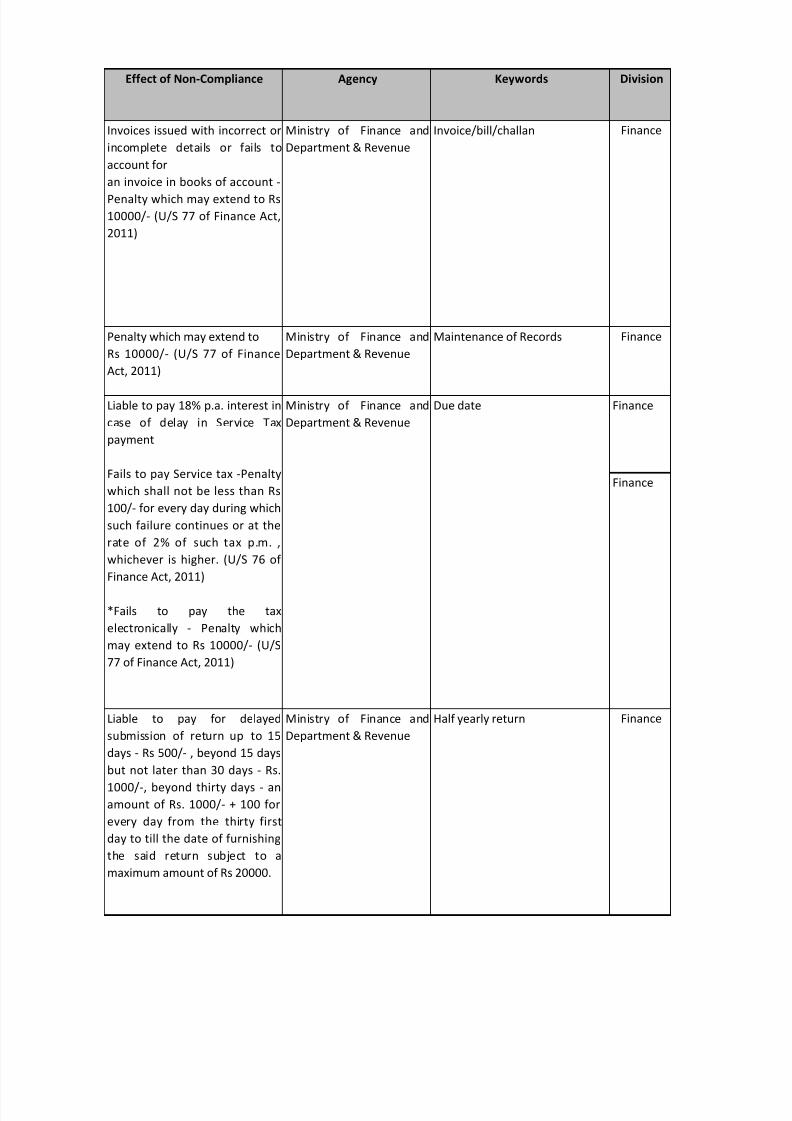

Effect of Non-Compliance Agency Keywords Division

Invoices issued with incorrect or

incomplete details or fails to

account for

an invoice in books of account -

Penalty which may extend to Rs10000/- (U/S 77 of Finance Act,

2011)

Ministry of Finance and

Department & Revenue

Invoice/bill/challan Finance

Penalty which may extend to

Rs 10000/- (U/S 77 of Finance

Act, 2011)

Ministry of Finance and

Department & Revenue

Maintenance of Records Finance

Finance

Finance

Liable to pay for delayed

submission of return up to 15

days - Rs 500/- , beyond 15 days

but not later than 30 days - Rs.

1000/-, beyond thirty days - anamount of Rs. 1000/- + 100 for

every day from the thirty first

day to till the date of furnishing

the said return subject to a

maximum amount of Rs 20000.

Ministry of Finance and

Department & Revenue

Half yearly return Finance

Liable to pay 18% p.a. interest in

case of delay in Service Tax

payment

Fails to pay Service tax -Penalty

which shall not be less than Rs

100/- for every day during which

such failure continues or at the

rate of 2% of such tax p.m. ,

whichever is higher. (U/S 76 of

Finance Act, 2011)

*Fails to pay the tax

electronically - Penalty which

may extend to Rs 10000/- (U/S

77 of Finance Act, 2011)

Ministry of Finance and

Department & Revenue

Due date

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 5/29

Location Function Compliance Owner Other Owner

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 6/29

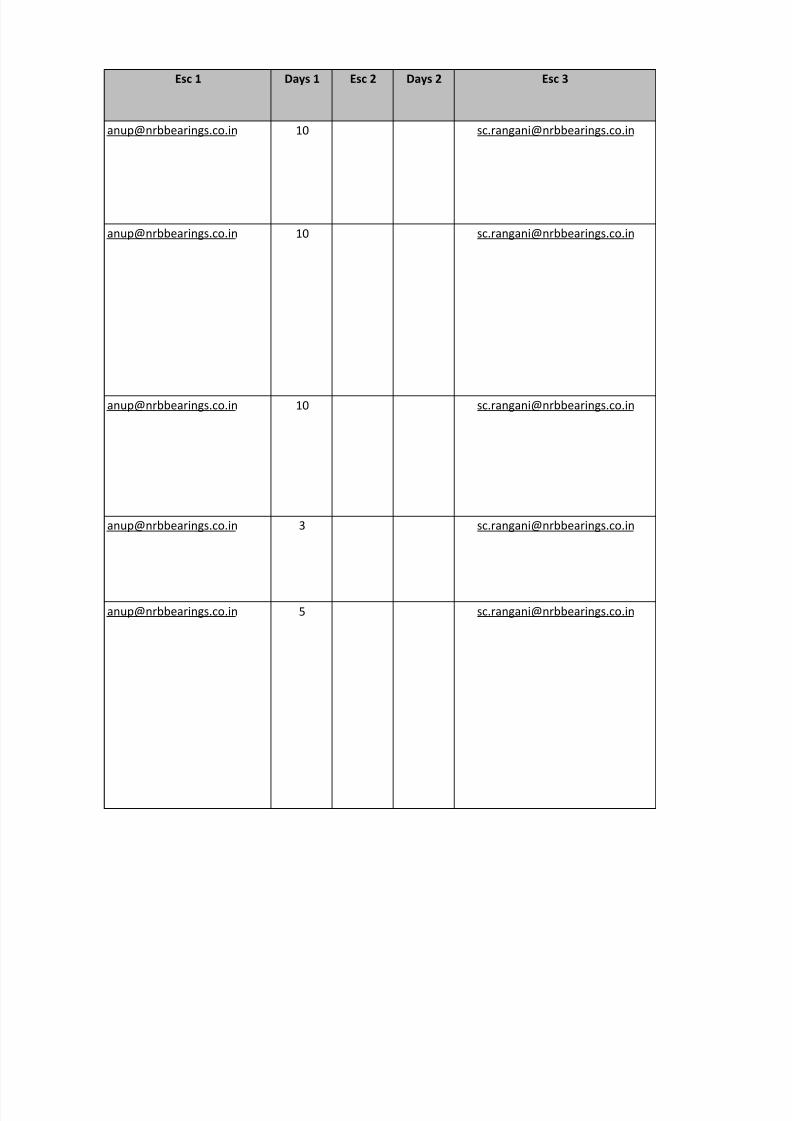

Esc 1 Days 1 Esc 2 Days 2 Esc 3

[email protected] 3 [email protected]

[email protected] 5 [email protected]

[email protected] 2 [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 7/29

Days 3 Frequency Reminder

Days

Day Month Start year Start month No. of years

1 Monthly 5 5

2 Annually 30 30 March

1 Monthly 5 6 April to Feb

1 Monthly 3 31th March March

3 Half yearly 25 25 April

Oct

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 8/29

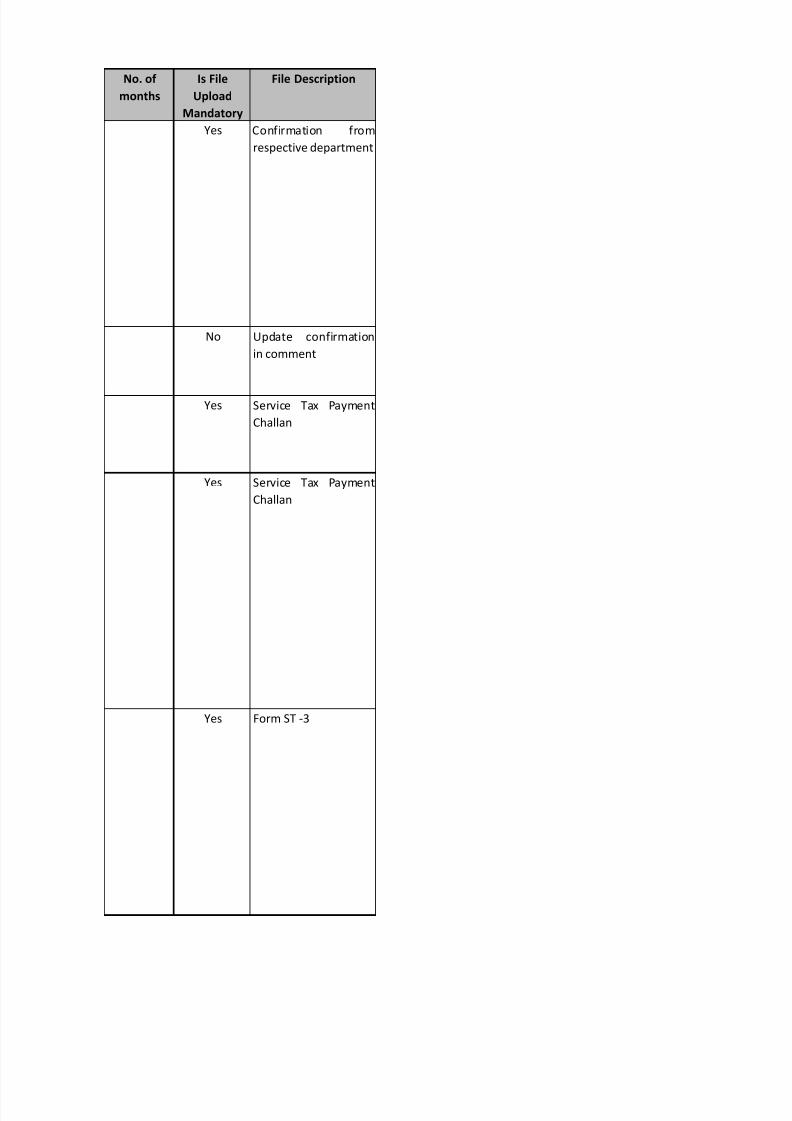

No. of

months

Is File

Upload

Mandatory

File Description

Yes Confirmation from

respective department

No Update confirmation

in comment

Yes Service Tax Payment

Challan

Yes Service Tax Payment

Challan

Yes Form ST -3

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 9/29

Compliance

Number

Type Category Law

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 10/29

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 11/29

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

Event

Based

Indirect

Taxation

Service Tax Rules, 1994

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 12/29

Compliance Description

Rule 5 of Service Tax Rules, 1994

Access to a registered premises

Rule 4 of Service Tax Rules, 1994

Registration

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 13/29

Rule 6 (1A) of Service Tax Rules, 1994

Payment of Service Tax in Advance

Rule 8 of Service Tax Rules, 1994

Appeals to Commissioner of Central Excise

Rule 9 of Service Tax Rules, 1994

Appeals to Appellate Tribunal

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 14/29

Rule 7A of Service Tax Rules, 1994

Revision of Return

Rule 10 of Service Tax Rules, 1994

Procedure and facilities for large taxpayer

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 15/29

Compliance Provision

Confirm whether are services are liable under service tax :

If yes then - Shall make an application for registration to the designated

superintendent of Central Excise in Form ST-1 for registration within a period of 30

days from the date on which the service tax is levied.(http://www.servicetax.gov.in/forms/st1.pdf)

Obtain the Confirmation that whether we provides the taxable service from more

than one premises or offices, and have any centralized billing systems or centralized

accounting systems.

If yes then - may apply to register such premises or offices from where centralised

billing or centralised accounting systems are located.

If No then - Shall make separate applications for registration in respect of each of

such premises or offices to the jurisdictional Superintendent of Central Excise.

Confirm whether there is a change in any information or details furnished in Original

Form ST-1 at the time of obtaining registration or intends to furnish any additional

information or detail :

If yes then - It is required to intimate the change or information or detail, in writing to

the jurisdictional Assistant Commissioner or Deputy Commissioner of Central Excise

within a period of 30 days of such change.

Obtain confirmation if any taxable services are cease to provide for which we are

registered.

If yes then - It is required to surrender the registration certificate immediately.

Obtain confirmation that if any demand form the officer authorised under sub-rule(1)

or the audit party deputed by the Commissioner or the Comptroller and Auditor

General of India :

If yes then - It is required to make available the below records for the scrutiny of the

officer or audit party within a reasonable time not exceeding 15 working days from

the day when such demand is made, or such further period as may be allowed by

such officer or the audit party.

(i) the records as mentioned in Rule 5(2)

(ii) trial balance or its equivalent; and

(iii) the income-tax audit report, if any, under section 44AB of the Income-tax Act,1961.

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 16/29

Obtain confirmation from the respective department that whether any service tax is

paid in advance to the credit of Central Government.

If yes then - It is required to intimate the details of the amount of service tax paid in

advance, to the jurisdictional Superintendent within a period of 15 days from the date

of such payment; and indicate the details of the advance payment made, and its

adjustment, if any in the subsequent return to be filed.

Obtain the confirmation that whether aggrieved by any decision or order passed by

an adjudicating authority subordinate to the Commissioner of Central Excise

If yes then - An appeal under Section 85 of the Act to the Commissioner of Central

Excise (Appeals) is required to filled in Form ST-4 in duplicate and accompanied by a

copy of order appealed against.

An appeal shall be presented within three months from the date of receipt of the

decision or order of such adjudicating authority relating to service tax, interest or

penalty made before the date on which the Finance Bill, 2012 receives the assent of

the President.

Provided that the Commissioner of Central Excise (Appeals) may, if he is satisfied that

the appellant was prevented by sufficient cause from presenting the appeal withinthe aforesaid period of three months, allow it to be presented within a further period

of three months.

Obtain the confirmation that whether aggrieved by an order passed by a

Commissioner of Central Excise section 73 (1)

If yes then - Appeal to the Appellate Tribunal against such order is required to filled

within three months of the date of receipt of the order in Form ST-5 in quadruplicate

and accompanied by a copy of the Order appealed against (one of which shall be a

certified copy).

An appeal U/S 86 (2) of the Act to the Appellate Tribunal shall be made in Form ST-7

in quadruplicate and accompanied by a copy of the order of the Commissioner of

Central Excise (one of which shall be a certified copy) and a copy of the order passed

by the Central Board of Excise and Customs directing the Commissioner of Central

Excise to apply to the Appellate

Tribunal.

An appeal U/S 86 (2A) of Section 86 of the Act to the Appellate Tribunal shall be made

in from ST-7 in quadruplicate and shall be accompanied by a copy of the order of the

Commissioner of Central Excise (Appeals) (one of which shall be a certified copy) and

a copy of the order passed by the Commissioner of Central Excise directing the

Assistant Commissioner of Central Excise or as the case may be, the Deputy

Commissioner of Central Excise to apply to the

Appellate Tribunal.A memorandum of cross-objections U/S 86(4) of the Act, is required to be made in

form ST-6 in quadruplicate.

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 17/29

Obtain confirmation that whether is require to correct a mistake or omission made in

original return submitted under Rule 7.

If yes than - It is required to submit a revised return in Form ST-3, in triplicate copy

within a period of 90 days from the date of submission of the return.

(http://www.servicetax.gov.in/forms/st3A.pdf)

Obtain confirmation from the respective departments that whether we are large tax

payer :

If yes then - It is required to comply with followings :

(1) A large taxpayer shall submit the returns, as prescribed under these rules, for each

of the registered premises.

In case of centralized registration under rule 4 (2), submit a consolidated return for allsuch premises.

(2) A large taxpayer, on demand, may be required to make available the financial,

stores and CENVAT credit records in electronic media, such as, compact disc or tape

for the purposes of carrying out any scrutiny and verification, as may be necessary.

(3) May with intimation of at least 30 days in advance, opt out to be a large

taxpayer from the first day of the following financial year.

Note :- “large tax payer” means a person who (i) has one or more registered premises

under the Central Excise Act, 1944 (1 of 1944); or (ii) has one or more registered

premises under Chapter V of the Finance Act, 1994 (32 of 1994) and is an assessee

under the Income-Tax Act, 1961 (43 of 1961), who holds a PAN and satisfies the

conditions and observes the procedures as notified by the Central Government in this

regard.

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 18/29

Effect of Non-Compliance Agency Keywords Division

Penalty which may extend to

Rs 10000/- (U/S 77 of Finance

Act, 2011)

Ministry of Finance and

Department & Revenue

Registration Finance

Penalty which may extend to

Rs 10000/- (U/S 77 of Finance

Act, 2011)

Ministry of Finance and

Department & Revenue

Premises registration Finance

Penalty which may extend to

Rs 10000/- (U/S 77 of Finance

Act, 2011)

Ministry of Finance and

Department & Revenue

Changes in Registration details Finance

Penalty which may extend to

Rs 10000/- (U/S 77 of Finance

Act, 2011)

Ministry of Finance and

Department & Revenue

Surrender of Registration

Certificate

Finance

Penalty which may extend to

Rs 10000/- or Rs. 200/- for every

day during which such failure

continues, whichever is higher

(U/S 77 of Finance Act, 2011)

Ministry of Finance and

Department & Revenue

Access to a registered premises Finance

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 19/29

Non adjustment of advance Ministry of Finance and

Department & Revenue

Payment of Service tax in

advance

Finance

Ministry of Finance and

Department & Revenue

Appeals to Commissioner of

Central Excise

Finance

Ministry of Finance and

Department & Revenue

Appeals to Commissioner of

Central Excise

Finance

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 20/29

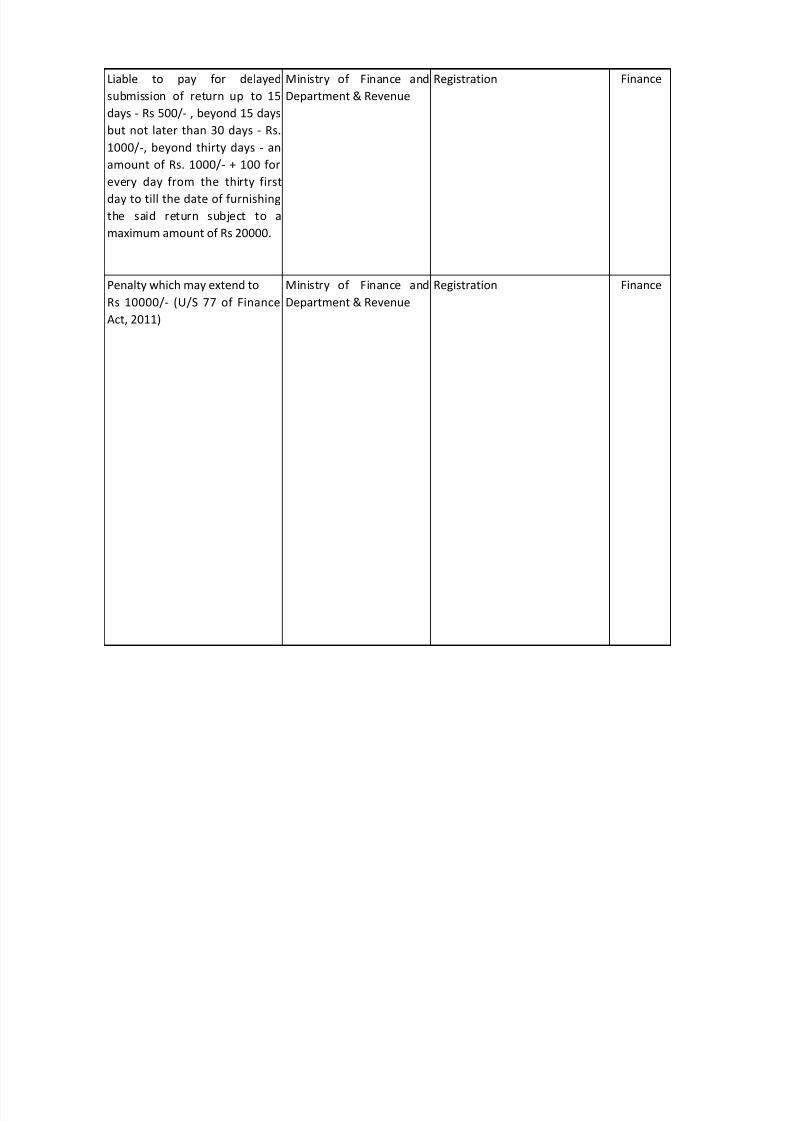

Liable to pay for delayed

submission of return up to 15

days - Rs 500/- , beyond 15 days

but not later than 30 days - Rs.

1000/-, beyond thirty days - an

amount of Rs. 1000/- + 100 for

every day from the thirty first

day to till the date of furnishingthe said return subject to a

maximum amount of Rs 20000.

Ministry of Finance and

Department & Revenue

Registration Finance

Penalty which may extend to

Rs 10000/- (U/S 77 of Finance

Act, 2011)

Ministry of Finance and

Department & Revenue

Registration Finance

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 21/29

Location Function Compliance Owner Other Owner

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 22/29

Mumbai Finance [email protected]

Mumbai Finance [email protected]

Mumbai Finance [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 23/29

Mumbai Finance [email protected]

Mumbai Finance [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 24/29

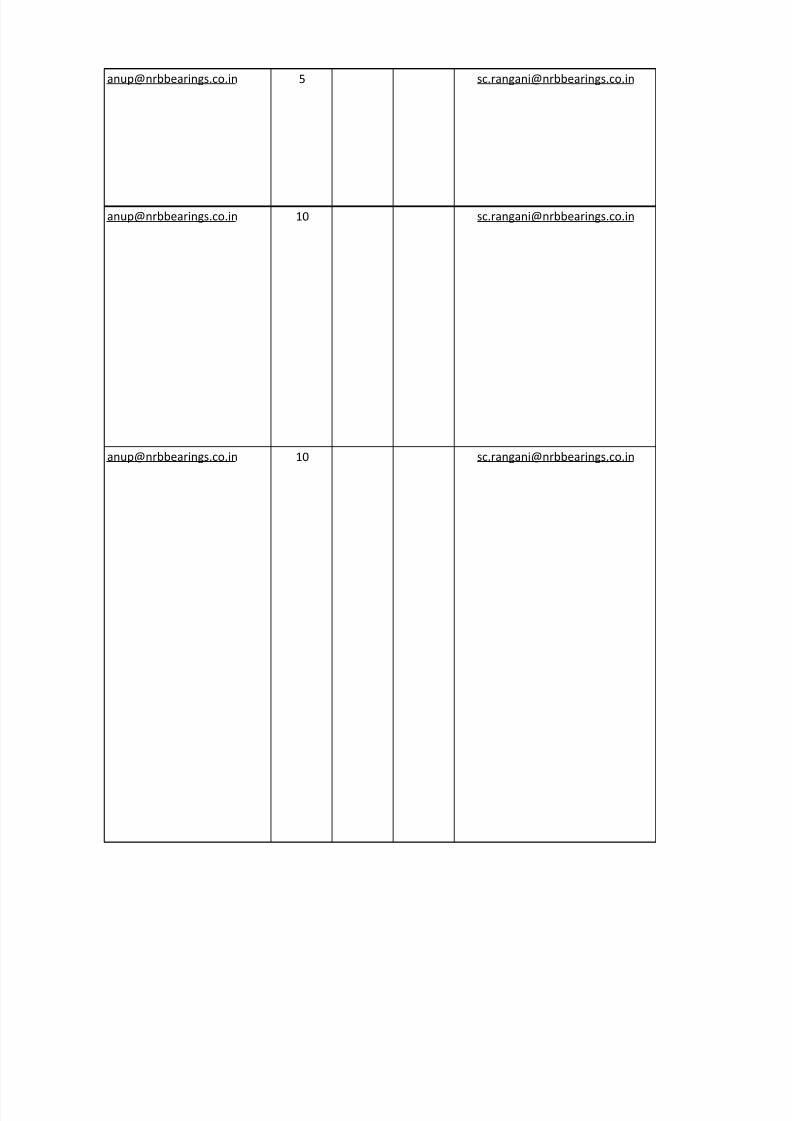

Esc 1 Days 1 Esc 2 Days 2 Esc 3

[email protected] 10 [email protected]

[email protected] 10 [email protected]

[email protected] 10 [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 25/29

[email protected] 5 [email protected]

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 26/29

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 27/29

Days 3 Frequency Reminder

Days

Day Is File

Upload

Mandatory

File Description

5 One time 30 30 Yes ST 1

5 Yearly 30 30 Yes ST 1

5 Yearly 30 30 Yes ST 1

1 Yearly 10 10 Yes Application for

surrender of

Registration certificate

2 Yearly 15 15 Yes Demand / Update

confirmation in

comment

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 28/29

2 Yearly 15 15 Yes Intimation for Service

Tax advance

5 Half yearly 90 3 months Yes ST 4

5 Half yearly 90 3 months Yes ST 5/ ST 6/ ST 7

8/10/2019 Service Tax Rules 1994_Final

http://slidepdf.com/reader/full/service-tax-rules-1994final 29/29

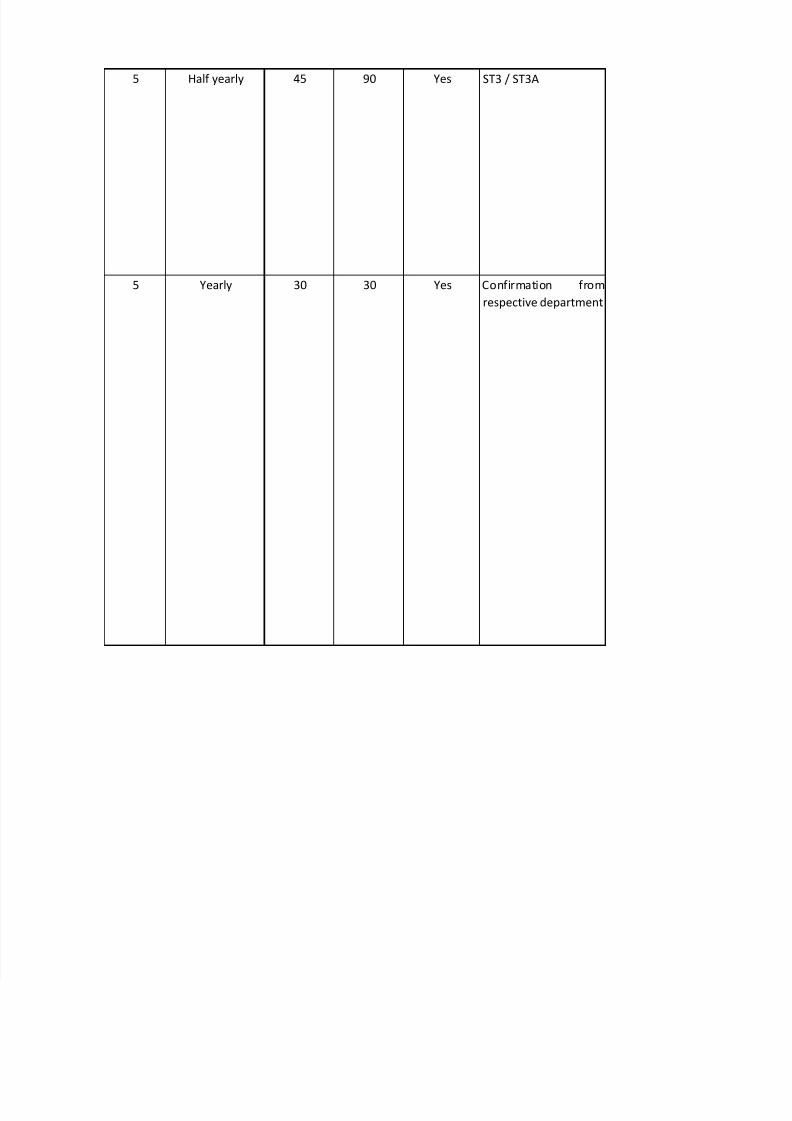

5 Half yearly 45 90 Yes ST3 / ST3A

5 Yearly 30 30 Yes Confirmation from

respective department