service tax on intellectual property rights and related ... · service tax on intellectual property...

TRANSCRIPT

1 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

SERVICE TAX ON INTELLECTUAL PROPERTY RIGHTS AND RELATED TRANSACTIONS

(Please refer this note in conjunction with the discussions during the presentation at the session)

Background

Generally, the term Intellectual Property means any product of human intellect that is intangible but has value in the market. Under the current provisions of service tax regime, IPR has not been defined. However, as per erstwhile section 66(55a) of the Finance Act, 1994 (‘Act’), intellectual property right had been defined as under:

“means any right to intangible property, namely, trade marks, designs, patents or any other similar intangible property, under any law for the time being in force, but does not include copyright.”

Additionally, erstwhile Section 66(55b) of the Act defined ‘intellectual property service’ as

► transferring, temporarily; or

► permitting the use or enjoyment

► of, any intellectual property right;

Major types of IPRs

► Patents

As per Section 2(m) of the The Patents Act, 1970 (‘Patents Act’), patent means a patent for any

invention granted under the Patents Act. Invention has been defined under Section 2(j) of the

Patents Act as a new product or process involving an inventive step and capable of industrial

application.

► Copyrights

Copyright means the exclusive right to do or authorize the doing of any of the acts specified under

Section 14 of the Indian Copyright Act, 1957.

► Trademarks

As per Section 2 (zb) of the Trade Marks Act, 1999, trade mark means a mark capable of being

represented graphically and which is capable of distinguishing the goods or services of one

person from those of others and may include shape of goods, their packaging and combination of

colours.

2 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Legislative History

Date Particulars

Pre-negative List regime

1 July 2003- Introduction of Franchisee service

1 July 2003 to 15 June 2005

► As per Section 65(47), "franchise" means an agreement by which-

(i) franchisee is granted representational right to sell or manufacture goods

or to provide service or undertake any process identified with franchisor,

whether or not a trade mark, service mark, trade name or logo or any such

symbol, as the case may be, is involved;

(ii) the franchisor provides concepts of business operation to franchisee,

including know how, method of operation, managerial expertise,

marketing technique or training and standards of quality control except

passing on the ownership of all know how to franchisee;

(iii) the franchisee is required to pay to the franchisor, directly or indirectly, a

fee; and

(iv) the franchisee is under an obligation not to engage in selling or

providing similar goods or services or process, identified with any other

person

► Circular No.59/8/2003 dated 20 June 2003 clarified that all four criteria should

be satisfiedfor levy of service tax.

16 June 2005 onwards

► As per Section 65(47) as amended, "franchise" means

an agreement by which the franchisee is granted representational right to sell

or manufacture goods or to provide service or undertake any process

identified with franchisor, whether or not a trade mark, service mark, trade

name or logo or any such symbol, as the case may be, is involved;

► In order to expand the coverage of franchisee services, the conditions specified

under the earlier definition were removed.

Clarification issued vide Letter F.No. B1/6/2005-TRU, dated 27-7-2005

► License to produce or sell under brand name became taxable because of

change in the definition.

► Granting of rights for rendering services identified by the principal became

taxable.

10 September 2004 Introduction of

Intellectual

► Section 65(55a) defines IPR “as any right to intangible property, namely, trade

marks, designs, patents or any other similar intangible property, under any law

for the time being in force, but does not include copyright”.

3 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Property

Services

Definition of Intellectual Property Services as per Section 65(55b) of the Act during

the relevant period:

10 September 2004 to 15 June 2005

► “means transferring, whether permanently or otherwise; or permitting the

use or enjoyment of any intellectual property service.”

' 16 June 2005 onwards

► “means transferring, temporarily, or permitting the use of or enjoyment of any

intellectual property right”.

► The word ‘whether permanently or otherwise were replaced by ‘temporarily’

Clarifications issued vide Circular No. 80/10/2004-S.T., dated 17 September

2004

► Definition of IPR excludes ‘copyrights’.

► IPR covered under Indian law are chargeable to service tax and IPRs like

integrated circuits or undisclosed information (not covered by Indian law) would

not be covered under taxable services e

► No service tax on permanent transfer of IPR. This clarification has been further

made clear by amendment to Section 65(55b) of the Act to provide that only

temporary transfer of IPR will be subject to service tax.

16 May 2008 Introduction of Information Technology Software Services (ITSS)

16 May 2008 to 31 August 2009

► As per Section 65(105)(zzzze), ITSS has been defined as any service provided

or to be provided to any person, by any other person in relation to any person,

by any other person in relation to information technology software for use in the

course, or furtherance, of business or commerce, including,-

(i) development of information technology software,

(ii) study, analysis, design and programming of information technology

software,

(iii) adaptation, upgradation, enhancement, implementation and other similar

services related to information technology software,

(iv) providing advice, consultancy and assistance on matters related to

information technology software, including conducting feasibility studies on

implementation of a system, specifications for a database design, guidance and

assistance during the startup phase of a new system, specifications to secure

a database, advice on proprietary information technology software,

(v) acquiring the right to use information technology software for commercial

exploitation including right to reproduce, distribute and sell information

technology software and right to use software components for the creation of

and inclusion in other information technology software products,

4 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

(vi) acquiring the right to use information technology software supplied

electronically;

1 September 2009 to 30 June 2010

► The words ‘acquiring’ in sub-clauses (v) and (vi) above were replaced by the

word ‘providing’.

1 July 2010 onwards

► The words ‘for use in the course, or furtherance, of business or commerce’ has

been deleted from the definition of information technology software services.

Clarifications

► Circular 334/13/2009-TRU, dated 6-7-2009 clarifies following for amendment

under sub clause (v) and (vi) of the definition.

A correction has been carried out in the definition of the taxable service by

replacing the word ‘acquiring’ by the word ‘providing’, considering the fact

that it is the providing of ‘right to use’ and not the acquiring of ‘right to

use’ is a taxable service. This amendment would have retrospective effect

from 16-5-2008, when the service came into effect.

► Circular No. 334/1/2010-TRU, dated 26 February 2010 clarifies that scope of

ITSS services w.e.f. 1 July 2010 has been expanded to cover services even if

not used for business or commerce.

1 July 2010 Introduction of Copyright services

► As per Section 65(105) (zzzzt) of the Act, copyright service means any service

provided, to any person, by any other person, for transferring temporarily or

permitting the use or enjoyment of any copyright defined in the Copyright Act,

1957 (14 of 1957), except the rights covered under sub clause (a) of clause (1)

of section 13 of the said Act;

Clarification vide Circular No. D.O.F. No. 334/1/2010-TRU, dated 26 February

2010

► The right to temporarily transfer or permit the use of Intellectual Property Rights

(IPR), namely, trademarks, designs and patents was brought under tax net in

2004. However, one of the IPR, i.e. copyright has been specifically kept out of

the purview of the tax with an intent to encourage authors and artists, as it

involves creative works, such as literary work, musical work and artistic work.

► Copyright for Original literary, dramatic, musical and artistic works has been

kept out of service tax (sub clause (a) of clause (1) of section 13 of the said

Act).

5 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Post-negative List regime

1 July 2012 ► Under negative list regime, value of all services provided or agreed to be

provided in the taxable territory other than those service specified in the

negative list are chargeable to service tax.

► The term ‘service’ has been defined under section 65B (44) of the Act to mean

any activity carried out by a person for another for consideration, and includes

a declared service, but shall not include-

(a) an activity which constitutes merely,-

(ii) such transfer, delivery or supply of any goods which is deemed to be sale within the meaning of clause (29A) of article 366 of the Constitution;

► So, when there is transfer of right to use goods (tangible or intangible goods)

which is considered as deemed sale within the meaning of article 366 (29A) of

the Constitution, then the same is excluded from the definition of service.

► However, it is important to note that "temporary transfer or permitting the use or

enjoyment of any intellectual property right" is a declared service under Section

66E(c) of the Act and liable to service tax. Also “transfer of goods by way of

hiring, leasing, licensing or in any such manner without transfer of right to use

such goods” is a declared service under Section 66E(f) of the Act.

► From perusal of para 6 of the Educational Guide issued by CBEC, it seems that

the Central Government seems to be of the view that, while a temporary transfer

of intellectual property is a service, a permanent transfer of the intellectual

property is a deemed sale.

► Additionally, it is pertinent to note exemption has been provided for services

provided by way of temporary transfer or permitting use or enjoyment of a

copyright

(i). relating to original literary, dramatic, music or artistic works (covered by

Section 13(1)(a) of the Copyright Act), or

(ii). of cinematograph films for exhibition in a cinema hall or cinema theatre.

6 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

KEY COURT RULINGS:

Principles emerging from various judicial precedents for determining taxability under

service tax and VAT

► As per various judicial precedents, transfer of right to use goods has been held to attract VAT

whereas a mere right or license to use goods has been held to attract service tax.

► Transactions involving transfer of right to use goods includes lease or hire purchase of machinery

or equipment, software licensing, transfer of right to use trademarks, copyrights, patents, designs,

etc. as goods include both tangible and intangible goods. (Transfer of right to use goods was

brought to tax by virtue of Article 366 (29A) (d) of the Indian Constitution as a deemed sales.)

► State VAT provisions also include transfer of right to use goods in the definition of sales.

However, there are no provisions to explain what constitutes transfer of right to use goods. Thus,

reliance is placed on judicial precedents.

► The principles to determine whether a transaction qualifies as transfer of right to use have been

primarily emerged from the decision of Hon’ble Supreme Court in the case of Bharat Sanchar

Nigam Ltd. v. Union of India [2006 (2) S.T.R. 161 (SC)] and State of Andhra Pradesh v.

Rashtriya Ispat Nigam Ltd. [2002-ST 2-GJX-0050-SC].

► The facts of the case and principle emerging from the above decisions are summarised below:

Decision of Supreme Court in the case of State of Andhra Pradesh v. Rashtriya Ispat Nigam

Ltd. [2002-ST 2-GJX-0050-SC]

Facts of the

case

► The assessee supplied sophisticated and valuable imported machinery to the

contractor for the purpose of being used in execution of the contracted works

and received hire charges for the same.

► The issue before the SC was whether there was a transfer of right to use the

machinery by the assessee in favour of the contractors by collecting hire

charges and whether the assessee was liable to sales tax.

Observation

and

Decision

► On a careful reading and analysis of the various clauses contained in the

agreement, SC held that since the effective control of the machinery even

while it was in use by the contractor, was that with the assessee.

► The contractor was not free to make use of the machinery for the works other

than the project work or move it out during the period machinery was in his

custody.

► The condition that the contractor would be responsible for the custody of the

machinery while it was at the site did not militate against assessee's

possession and control of the machinery.

► Thus, SC held that the transaction did not involve transfer of right to use the

machinery in favour of contractor.

7 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Principle

emerging

from the

decision

► One of the determinants to constitute a transaction to be transfer of right to

use tangible goods is transfer of effective control and possession in the goods

to the exclusion of the lessor

Decision of Supreme Court in the case of Bharat Sanchar Nigam Ltd. v. Union of India [2006

(2) S.T.R. 161 (SC)]

Facts of the

case

► Assessee was engaged in providing telecom services.

► The issue before the SC was whether electromagnetic waves were goods and

whether transaction of providing access or telephone connection by BSNL

was a deemed sale liable to VAT.

► The assessee contented that there was neither the transfer of any legal right

to use goods nor any delivery of goods. On the other hand, the Revenue

contended that the transaction was a deemed sale under Article 366 (29A) (d)

of the Constitution read with the charging sections in their various sales tax

enactments and therefore they are competent to levy sales tax on the

transactions..

Observation

and

Decision

► SC observed that, the electromagnetic waves are neither abstracted nor are

they consumed in the sense that they are not extinguished by their user. They

are not delivered, stored or possessed. Nor are they marketable. They are

merely the medium of communication.

► Further, a subscriber to a telephone service could not reasonably be taken to

have intended to purchase or obtain any right to use electromagnetic waves or

radio frequencies when a telephone connection is given. Nor does the

subscriber intend to use any portion of the wiring, the cable, the satellite, the

telephone exchange etc.

► As far as the subscriber is concerned, no right to the use of any other goods,

incorporeal or corporeal, is given to him with the telephone connection.

Therefore, an electro-magnetic wave (or radio frequency), does not fulfil the

parameters applied by the SC in Tata Consultancy case for determining

whether they are goods, right to use of which would be a sale for the purpose

of Article 366(29-A).

► SC further held that it would depend upon the intention of the parties. If the

parties intended that the SIM card would be a separate object of sale, it would

be open to the Sales Tax Authorities to levy sales tax thereon.

► SC also laid down certain attributes to determine what will constitute transfer

of right to use goods. It was held that none of such attributes were present in

the relationship between telecom service provider and a consumer of such

services. Hence, it was held that there was no transfer of right to use.

8 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Principle

emerging

from the

decision

► Attributes to determine what will constitute transfer of right to use goods are as

follows:

(i) First and foremost, there must be goods available for delivery;

(ii) There must be a consensus ad-idem as to the identity of the goods;

(iii) The transferee should have a legal right to use the goods- as a result, all

legal consequences of such use including any permissions or licenses

required thereof should be available to the transferee;

(iv) For the period during which the transferee has such legal right, it has to be

to the exclusion to the transferor - this is the necessary concomitant of the

plain language of the statute - viz. a "transfer of the right to use" and not

merely a licence to use the goods;

(v) And lastly, having transferred the right to use the goods during the period

for which it is to be transferred, the owner cannot again transfer the same

rights to others.

► Apart from above attributes, the other two determinants to constitute a

transaction as transfer of right to use goods are the intention of the parties and

the fact that the subject matter of the transaction qualifies as goods.

► Para 6.6.1 of the Education Guide provides that whether a transaction amounts to transfer of right

or not cannot be determined with reference to a particular word or clause in the agreement. The

agreement has to be read as a whole, to determine the nature of the transaction.

IPR SPECIFIC COURT RULINGS:

Judicial precedents & Controversy

1. Trademarks

Decision of Bombay High Court in the case of Tata Sons Ltd [and Another v. The State of

Maharashtra and Another [TS-33-HC-2015 (Bom)-VAT

Facts of

the case

► Tata Sons, the holding company of Tata group had entered into ‘Tata Brand

Equity and Business Promotion Agreement’ with its subsidiaries to

systematically develop, promote and enhance the equity in the word TATA as

well as to legally protect the same.

► Tata Sons was discharging service tax on consideration received from its group

companies

► The issue before the HC was whether the consideration received by Tata Sons

from its group subsidiary companies for use of the brand name can be said to

9 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

be ‘deemed sale’ to attract sales tax under Transfer of Right to use any Goods

for any Purpose Act, 1985?

Decision ► On perusal of the agreement and provisions, HC observed that in case of

intangible goods, the right to use them is capable of being transferred and if

transferred it may be subject to VAT.

► The Act does not give any indication that the right to use incorporeal goods

should be exclusively transferred in favour of the transferee.

► The Act does not envisage exclusive and unconditional transfer of the right to

use goods. HC also observed that decision in case of BSNL’s case wherein it

was held that in order to attract levy under the transfer of right to use goods, the

transfer has to be to the exclusion of the transferor and once the right is

transferred the owner cannot again transfer the right to others is not applicable

in the instant case.

► Bombay HC held that even when there is transfer of right to use goods to

multiple users, it would attract VAT.

Current

Status

► Tata Sons has filed an appeal before the SC. Hearing for stay of demand took

place on 23 November 2015.

► SC has granted stay for penalty amount. However, for tax and interest, the SC

has directed Tata Sons to pay tax along with interest within 4 weeks if not

already paid

Circular

issued

after the

judgment

► Pursuant to ruling of Bombay HC, Trade Circular No. 11T of 2015 dated 13 July

2015 was issued by the Commissioner of Sales Tax, Maharashtra.

► The Circular elucidates Bombay High Court’s decision in the case of Tata Sons

Limited and concludes that VAT can be levied on transfer of right to use goods

of intangible nature i.e. trademark, technical know-how, copyright and other

intangibles, etc. even if it is transferred to multiple users.

► Relevant extract has been reproduced below:

“The High Court distinguished the remarks of the Supreme Court in the case of BSNL. The observation of one of the three judges bench of the Supreme Court in the case of BSNL was that in order to attract levy under transfer of right to use goods, the transfer has to be to the exclusion of the transferer and once the right to use the goods is transferred the owner again cannot transfer the right to others. This observation led to the conclusion that there cannot be transfer of right to use trade mark, copy rights and technical know how and other intangibles to multiple users. However, the High Court has put to rest the controversy and has comprehensively held that even when there is transfer of right to use goods to multiple users it would attract tax under the MVAT Act It further held that Bombay High Court judgment in the case of Dukes and Sons Ltd is still good law. The law is therefore now settled that VAT can be levied on transfer of right to use goods of intangible nature i.e. trade mark, technical know how, copy right and other intangibles etc even if it is transfered to multiple users.”

10 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Principle

emerging

from the

decision

► There could be transfer of the right to use these goods even though it is not

exclusive and unconditional, and VAT could be levied even if there were

multiple transferees.

Decision of Karnataka High Court in the case of State of Karnataka Vs M/s United Breweries

(UB) Limited 2015-VIL-479-KAR

Facts of

the case

► UB had entered into an agreement with a Contract Bottling Unit (‘CBU’) for

brewing and distribution of beer. The CBU manufactured beer under brand

name and as per specifications of UB. Further the CBU was permitted to sell

the output to UB’s specified distributors only. After allowing for the production

cost from the sale proceeds, UB collected the excess amounts from the CBU as

a fixed “brand franchise fee” of INR 10 per bottle and balance as surplus profits.

► UB had also provided a license to use its trademark “Kingfisher” on packaged

drinking water to certain manufacturers. While, UB collected a royalty for the

license, in contrast to the agreement with CBU, the manufacturers were free to

sell the output to their own customers.

Decision ► In the first instance, the High Court drew reference to the landmark judgement

of Supreme Court in the case of Rashtriya Ispat and observed that, to constitute

as “transfer to right to use”, the licensee must get an effective control to

commercially exploit the brand/ trademark. Further, such transfer of right

should be without any restriction.

► With respect to the second instance, the High Court distinguished the facts with

the first instance and observed that the effective control to commercially exploit

UB’s trademark was transferred to the manufacturers of ‘packaged drinking

water’.

► Thus, demand of VAT in the first instance was dropped and demand of VAT in

the second instance was confirmed.

Current

Status

► The issue is settled.

Principle

emerging

from the

decision

► Effective control should be transferred to constitute transfer of right to use.

Decision of Allahabad High Court in the case of The Commissioner, Commercial Tax v.

Seagram India Pvt. Ltd [2014-VIL-30 ALH]

Facts of

the case

► The assesse is manufacturing and selling Indian made foreign liquor. The

assesee had transferred trademarks to certain companies in return of valuable

consideration.

11 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Decision ► The High Court of Allahabad relying on the case of BSNL held that the

permission granted for the use of the trade mark to multiple users would only be

treated as licence and not as transfer of right to use the trade mark.

Current

Status

► The issue is settled.

Principle

emerging

from the

decision

► Grant of rights for multiple users for the use of trade mark would only be treated

as license.

Decision of Delhi CESTAT in the case of Eicher Good Earth Ltd v CST [2012-TIOL-579-

CESTAT-DEL]

Facts of

the case

► The assessee owned the trademark “EICHER” registered in India in respect of

Tractors. The assesse transferred the trademark Eicher to other company and

received consideration for the same.

► The issue in the instant case was whether transfer of trademark is a sale or

service.

Decision ► Contract is not in nature of transfer of right to use and is more in the nature of

permission to use the trademark which continues to be the property of the

licensor.

► The right to use is assigned subject to certain conditions. Accordingly, it was

held that the transaction is not a sale transaction but a service transaction.

Current

Status

► No Appeal has been filed before High Court or Supreme Court against the

Order of Delhi CESTAT. .

Principle

emerging

from the

decision

► Contract should be read as a whole and its nature should not be determined by

the words “perpetual” or “exclusive” used in the title or some clauses of the

contract.

12 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

2. Software

Decision of Madras High Court in the case of Infotech Software Dealers Association Versus

Union of India reported in 2010(20) STR 289

Facts of

the case

► Infotech Software Dealers Association (‘ISODA’) had filed a writ petition before

the Madras High Court challenging the constitutional validity of service tax on

Information Technology Software Service (‘ITSS’). Additionally, following

questions were raised before the High Court:

a) Whether software is goods?

b) Whether software supplied to the customer pursuant to end user license

agreement would qualify as sale or service?

Decision ► Levy of service tax under ITSS in constitutionally valid.

► In view of various judicial precedents, it has been held that software is goods.

► The copyright in software is protected and always remains the property of the

creator and what is transferred is the right to use the software with copyright

protection. The sale is coupled with a condition for exclusive use of the software

by the customer at the exclusion of others and it gives absolute possession and

control to the user of the right to use the software.

► When the developer does not sell the software as such, transaction would not

qualify as sale.

► If the software is sold through the medium of internet in downloadable form, it

would not qualify as goods.

► The terms and conditions of End user license agreement is material to

determine whether there is an element of sale involved when software is

delivered to the customer.

Current

Status

► The issue is settled.

Principle

emerging

form the

decision

► In order to determine whether software would qualify as sale or service would

depend on the terms and conditions of the End user license agreement and

medium on which software is transferred.

Decision of Maharashtra Sales Tax Tribunal in the case of M/s Atos Origin India (P) Ltd Vs

The State of Maharashtra [2015-VIL-12-MSTT]

Facts of

the case

► QAD USA is the owner of standard software MFG/PRO. The owner licensed

the said software to QAD India (‘QAD’).

13 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

► QAD entered into an agreement with Atos where Atos would provide service for

modification, development, enhancement and customization of the standard

software, which is supplied by QAD to its customers.

► The payment to Atos is based on the number of employees for the said activity

Decision ► The development, enhancement and customization would convert the standard

software into customized software satisfying the requirement of the end user.

► The terms of the agreement reveal that QAD is availing the intelligence of

Atos’s employees for creating software programme as per the end user

requirement. The dominant intention is to get the software and not a mere

service.

► The software programme for modification, development, enhancement and

customization of software has all the three attributes as contemplated in TCS

case to qualify as goods.

Current

Status

► The issue is settled.

Principle

emerging

from the

decision

► Levy of service tax or vat would depend upon the contractual terms mentioned

in the agreement and intention of the parties to the contract.

3. Franchisee Services

Decision of Kerala High Court in the case of Malabar Gold v CTO (2013) 40 STT 319

Facts of

the case

► The assessee company was engaged in marketing, trading, export and import

of jewellery under the brand name of 'Malabar Gold’

► It entered into franchisee agreements for use of their logo or brand name.

► The franchisee agreement do not confer any permanent right or interest to the

franchisee in any trade mark, trade name, service mark, design, logo or the

name of Malabar Gold.

► The assessee paid service tax on the royalty amount received by it under the

category of franchisee service.

Decision ► Kerala HC in this case held that the judgement of the SC in case of BSNL is

squarely applicable in the present case as there are no goods deliverable at

any stage and there is no transfer of right to franchisee at all as per the

agreement entered with them.

► The franchisee agreement show that the franchisor retains the right, effective

control and possession and it is not a case of transfer of possession to the

exclusion of the transferor.

14 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

► Franchisee has no right to sub-let or sub-lease or in any way sell, transfer,

discharge or distribute or delegate or assign the rights under the agreement in

favour of any third party.

Accordingly, it was held that franchisee service are liable to service tax and not VAT.

Current

Status

► Special leave petition filed by the department is pending before the SC.

Principle

emerging

from the

decision

► Franchisee service is not transfer of right to use goods and hence not deemed

sale.

Decision of Madras High Court in the case of Vitan Departmental Stores & Industries Ltd. v.

The State of Tamil Nadu Joint Commissioner (JT), Chennai [2013-TIOL-897-HC-MAD-CT]

Facts of

the case

► The assessee is engaged in the business of operating supermarket under the

name and style of 'VITAN A/C Supermarket.

► It entered into a franchisee agreement wherein, the franchisee was given

exclusive right to operate the supermarket in one of the location taken on lease.

► Whether consideration received pursuant to a franchisee agreement is liable to

sales tax?

Decision ► There was an exclusive right given to the transferee by the assessee in respect

of a particular store and consequently a transfer of right to use and not merely a

licence to use the goods.

► During the period when the agreement was in force, the assessee as the

transferor could not transfer such goods with particular reference to the

exclusive right given in respect of a particular store to any other party.

► All the attributes to constitute transfer of right to use the goods have been

fulfilled and accordingly the right given by the assessee is undoubtedly a

transfer of right to use incorporeal or intangible goods and therefore, exigible to

sales-tax

Current

Status

► The issue is settled.

Principle

emerging

from the

decision

► Exclusive transfer of incorporeal rights would be subject to sales tax.

15 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Other Important Case Laws:

► Oracle India Pvt Ltd Versus Commissioner of Service Tax, Bangalore reported in 2014 (36)

STR 1184 (Tri-Bang)

► Directi Internet Solutions P Ltd Versus Commissioner of Service Tax, Mumbai reported in

2014 (36) STR 849 (Tri-Mumbai)

► Skol Breweries Ltd Versus Commissioner of C.Ex. & S.T, Aurangabad reported in 2014(35)

STR 570 (Tri-Mumbai)

► Delhi Public School Society Versus Commissioner of Service Tax, New Delhi reported in 2013

(32) STR 179 (Tri-Del)

► SAP India (P) Ltd Versus Commissioner of Central Excise, Bangalore reported in 2013 (13)

STR 346 (Tri-Bang)

16 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

Other Issues

Copyright versus Copyrighted Article

► Copyright is an intangible incorporeal right in the nature of privilege, quite independent of any

material substance.

► Copyright is distinguishable from the sale consideration paid for a copyrighted article. A

transfer of copyrighted article may or may not involve transfer of Copyright.

► The Special Bench of the Delhi Tribunal in case of Motorola Inc v. Dy. CIT [(2005) 147

Taxmann 39 (Del)] noted that the transfer of the ownership of a physical thing in which the

copyright exists gives to the purchaser the right to do with it (the physical thing) whatever the

purchaser pleases, except the right to make copies and issue them to the public. Just because

one has the copyrighted article, it does not follow that one has also the copyright in it.

Dual levy of VAT or service tax

► Dual taxation takes place when on the same amount both service tax and VAT are levied. The

issue of dual taxation arises because of complex nature of transaction which falls under both

Central List and State List of the Seventh Schedule of the Constitution. In this regard, it may be

noted that there are judgments both for and against the applicability of dual levy of tax on one

transaction:

► In this regard, it may be noted that the Hon’ble Supreme Court in the case of Federation of Hotel

& Restaurant Association of India v. Union of India reported in 2002-TIOL-699-SC-Misc has

held that more than one tax can be levied on different aspects of the same transaction.

► In the case of Escotel Mobile Communication Limited Versus Union of India reported in

2006(2) STR 567 (Ker), while deciding about the applicability of service tax and VAT had

observed that applying the concept of aspect theory, same transaction can be subject to both

service tax and VAT. Further, the Kerala High Court at para 36 observed that nothing can be said

to be a double taxation, unless two or more taxes have been levied on the same property or

subject-matter by the same Government or authority during the same taxing period, and for the

purpose.

► The above decision of Kerala High Court was revered by SC. The SC has held that aspect theory

would not apply to enable the value of the services to be included in the sale of goods or the price

of goods in the value of the service.

► Further, the SC in the case of Imagic Creative Pvt Ltd vs Commissioner of Commercial Tax

2008-TIOL-04-SC-VAT has held that service tax and sales are mutually exclusive.

17 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

► However, in case of Federation of Hotels & Restaurant Association of India v. Union of India

(1989 3 SCC 634), the SC upheld the multiple levy of taxes on the same transaction. Following

extract from the decision is relevant:

“The same transaction may involve two or more taxable events in its different aspects. But the

fact that there is an overlapping does not detract from the distinctiveness of the aspects.” [para

31]

► Further, the Delhi HC in case of Bharti Telemedia Ltd v. Government of NCT of Delhi (WPC

2194/2010) upheld the levy of entertainment tax on DTH services provided by the appellant

despite the fact that service tax was also applicable on provision of DTH services. Similar view

was taken by High Court of Madras in the case of Tata Sky Ltd Versus State of Tamil Nadu

(W.P.Nos.25721, 27070 to 27072, 25986, 25987, 28978, 28979, 25872, 25873 and 25927 to

25929 of 2011)

► Additionally, it may be noted that the Bombay HC admitted a writ petition (WP) of Mayhco

Monsanto Biotech (India) Pvt. Ltd. on the issue of dual levy of service tax as well as sales tax on

transfer of technical know-how. Earlier, HC had admitted WP of Subway, challenging similar dual

levy on franchisee fee.

Refund of Wrongly paid tax

Decision of Punjab and Haryana High Court in the case of M/s Idea Cellular Ltd (Idea) Versus

Union of India and Other]

Facts of

the case

► Idea had paid VAT on activation of SIM cards in the State of Haryana.

► The Hon’ble Supreme Court in the case of Idea had held that activation of SIM

cards is a service and not sale.

► Consequently, Idea approached State of Haryana for refund of the amount of

VAT paid as the same has been collected without authority of law.

► It was argued by the department that VAT was deposited in the accordance of

interpretation of law and there are no provisions under Haryana VAT for refund

of such wrongly paid tax

Decision ► The High Court in the case of Idea (supra) observed that when the tax has

been collected in absence of authority of law, the High Court is empowered to

issue writ directing refund. The High Court directed that the amount of VAT

paid to be transferred to the Service department of the Union as an adjustment

of service tax liability.

18 | P a g e Prepared by Divyesh Lapsiwala December 2015 All rights reserved

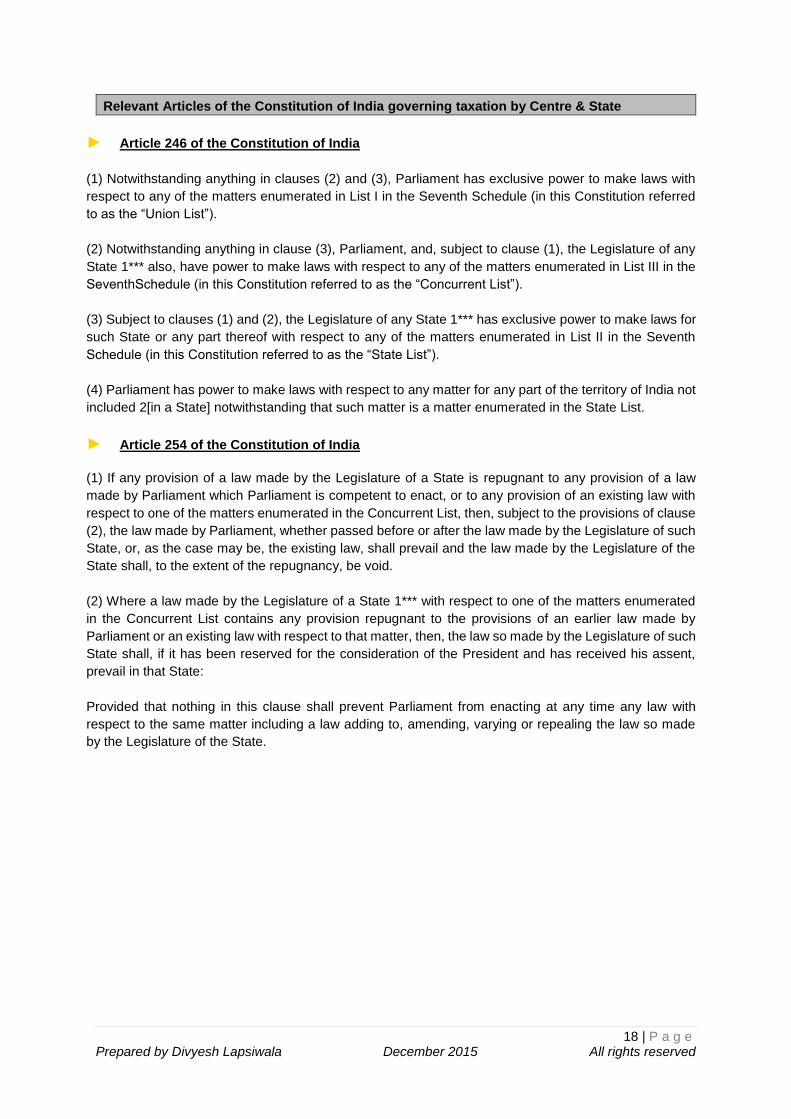

Relevant Articles of the Constitution of India governing taxation by Centre & State

► Article 246 of the Constitution of India

(1) Notwithstanding anything in clauses (2) and (3), Parliament has exclusive power to make laws with

respect to any of the matters enumerated in List I in the Seventh Schedule (in this Constitution referred

to as the “Union List”).

(2) Notwithstanding anything in clause (3), Parliament, and, subject to clause (1), the Legislature of any

State 1*** also, have power to make laws with respect to any of the matters enumerated in List III in the

SeventhSchedule (in this Constitution referred to as the “Concurrent List”).

(3) Subject to clauses (1) and (2), the Legislature of any State 1*** has exclusive power to make laws for

such State or any part thereof with respect to any of the matters enumerated in List II in the Seventh

Schedule (in this Constitution referred to as the “State List”).

(4) Parliament has power to make laws with respect to any matter for any part of the territory of India not

included 2[in a State] notwithstanding that such matter is a matter enumerated in the State List.

► Article 254 of the Constitution of India

(1) If any provision of a law made by the Legislature of a State is repugnant to any provision of a law

made by Parliament which Parliament is competent to enact, or to any provision of an existing law with

respect to one of the matters enumerated in the Concurrent List, then, subject to the provisions of clause

(2), the law made by Parliament, whether passed before or after the law made by the Legislature of such

State, or, as the case may be, the existing law, shall prevail and the law made by the Legislature of the

State shall, to the extent of the repugnancy, be void.

(2) Where a law made by the Legislature of a State 1*** with respect to one of the matters enumerated

in the Concurrent List contains any provision repugnant to the provisions of an earlier law made by

Parliament or an existing law with respect to that matter, then, the law so made by the Legislature of such

State shall, if it has been reserved for the consideration of the President and has received his assent,

prevail in that State:

Provided that nothing in this clause shall prevent Parliament from enacting at any time any law with

respect to the same matter including a law adding to, amending, varying or repealing the law so made

by the Legislature of the State.