september quarter 2016 market update - reiwa · perth housing and land market perth region...

TRANSCRIPT

September Quarter 2016

market updateQuarterly review of the WA residential property market

SAMPLE

2 MARKET UPDATE | SEPTEMBER QUARTER 2016

Contents REIWA MARKET UPDATE

WA Real Estate Indicators 3

Perth Housing and Land Market 4

Perth Overview 6

Perth Central Sub-Region 8

Perth North-West Sub-Region 16

Perth North East Sub-Region 20

Perth South East Sub-Region 24

Perth South West Sub-Region 28

Perth Rental Report 32

Dwellilng Sales Overview 34

Land Sales Overview 35

Regional WA Real Estate Report 36

Lifestyle Living Summary 46

Macro Growth Rates 50

Economic Overview 51Statistical Concepts and

House Price Measurement 51

Centre SpreadLift-out colour maps

Perth House PricesMedian prices of established house sales for 12 months to September 2016

Regional House PricesMedian prices of established house sales (land less than 1Ha) in major regional centres for12 months to September 2016

EDITOR & ANALYST Lisa Kazalac | Ronak Bhimjiani | Dillon Kanbi COVER PHOTO iStock: Dirk Tacke

PRODUCTION & DESIGN Jan Burt PRINTING Printforce CONTACT REIWA PO Box 8099, Subiaco East 6008 TEL (08) 9380 8222 FAX (08) 9380 8289

SUBSCRIPTION [email protected]

About the REIWA Market UpdateThe Market Update is a quarterly review of the property market in Western Australia and is published by the Real Estate Institute of WA.

While REIWA has full confidence in the data contained in this document, no warranty, guarantee or holding out, either expressed or implied is given and persons or companies who pursue real estate investment or otherwise and act on the basis of this data do so at their own risk.

Issue 102 | © REIWA 2016 | This publication is copyright. Only REIWA members may copy or reproduce any part of this publication without authorisation.

unlocking opportunities Proudly supported by llestpac

The key to real estate is spotting value. Our real estate specialists have

expert industry knowledge to help you with anything from a simple and secure rent

collection system, to the purchase of rent rolls (thanks to our tailored rent roll funding).

So you can spend more time growing your business.

Talk to our WA Real Estate Relationship Manager

about how we can support you:

Aamna Bhatia on 0438 997 675

Or visit http://www.westpac.com.au/business

banking/industries/real-estate/

UI

SAMPLE

SEPTEMBER QUARTER 2016 | MARKET UPDATE 3

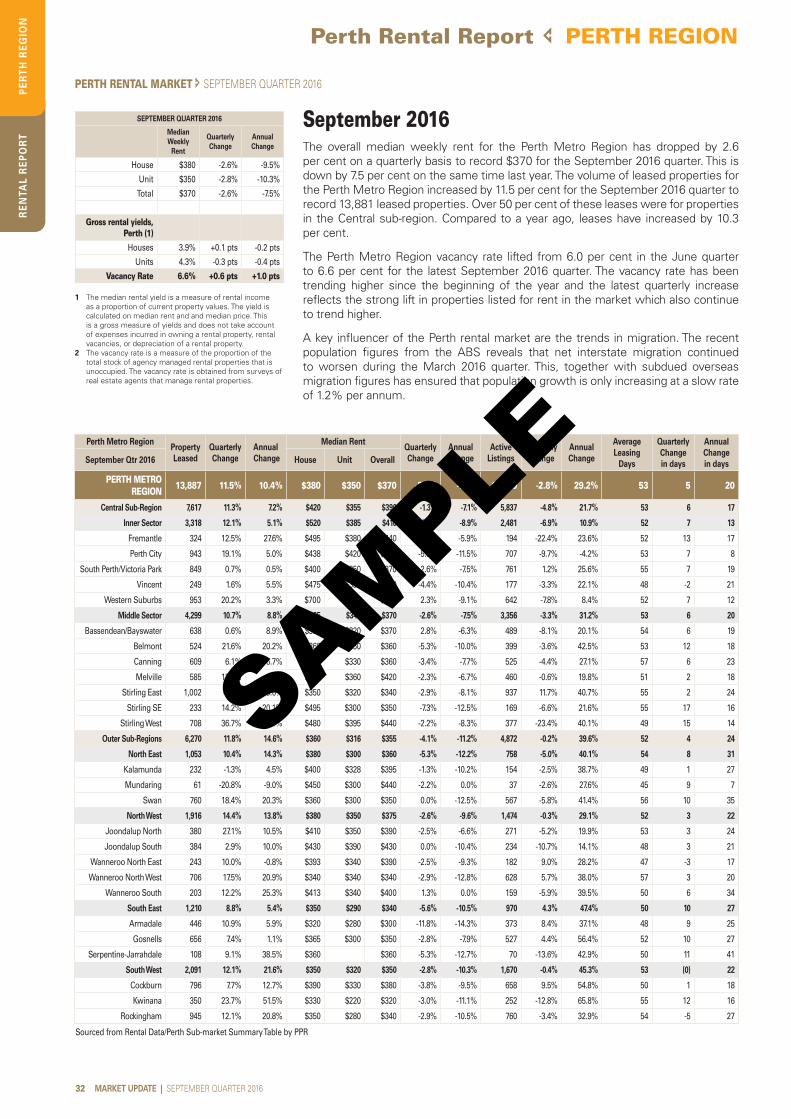

Western Australia’s Consumer Sentiment Index has fallen a significant 14.2 per cent in September to 89.2 - the lowest level of the five major states. The decline comes on the back of solid improvements in consumer sentiment in August with WA consumers now concerned about current and near future economic conditions. Economic conditions over the next 12 months was the main reason for the consumer pessimism, although economic conditions over the next five years has seen a boost in confidence. Compared to consumer sentiment levels a year ago, Western Australia is up 2.0 per cent but remains the lowest amongst the states.

According to the latest figures from the Australian Bureau of Statistics (ABS), domestic demand in Western Australia fell 2.5 per cent in the June quarter to $49.6 billion, its lowest level since June quarter 2011 in seasonally adjusted terms. The main factor of the fall is the decline in private capital investment, which was down by 4.9 per cent to $39.2 billion. The good news is household consumption in the state is still growing at a moderate pace at $25.2 billion. Public capital investment also had its strongest quarter on record, up 7.4 per cent to $10.3 billion. State final demand excludes exports and imports, which is Western Australia’s main commodity in international trade, but remains the best representation of the state’s economy. Overall Australia’s economy increased 3.3 per cent at the end of the 2016 financial year, led by Australian Capital Territory (3.8 per cent) and Northern Territory (2.4 per cent).

REIWA MARKET UPDATE WA Real Estate Indicators

WA consumer sentiment moderates in September

WESTERN AUSTRALIA REAL ESTATE INDICATORS - SEPTEMBER QUARTER 2016September Qtr 2016

PreliminaryJune Qtr 2016

Revised% change from

previous quarter% change

from previous year

Median sale price 1Preliminary median house and unit prices and estimated sales volume for current quarter based on a dataset of approximately 70-75% of transactions for the quarter. Median house & land prices for sales less than 1 Ha. Land sales estimates based on approximately 50% of expected transactions for the quarter. Figures are therefore subject to revision.1 Median sales prices are

derived from Landgate sales information & includes sales on lots less than 1 Ha Dwelling Sales for current quarter based on assumption that analysis conducted on 70% sample of data. Land Sales for current & past quarters based on assumption that only ~50% of sales have settled. Due to pre-selling & settlement lags, - final Land Sales figures not available for up to 12 months. Average selling time and sales to listing ratio are taken from REIWA.COM.

2 Buyer type information from the Australian Bereau of Statistics

3 Rental market data from REIWA.COM and member surveys.

4 Building approvals data from the Australian Bureau of Statistics.

5 Finance approvals data from the Australian Bureau of Statistics - latest figure may average for last month of quarter.

6 Interest rate data from Reserve Bank.

7 CPI data from Australian Bureau of Statistics.

* Data as of 3 months to Aug 2016

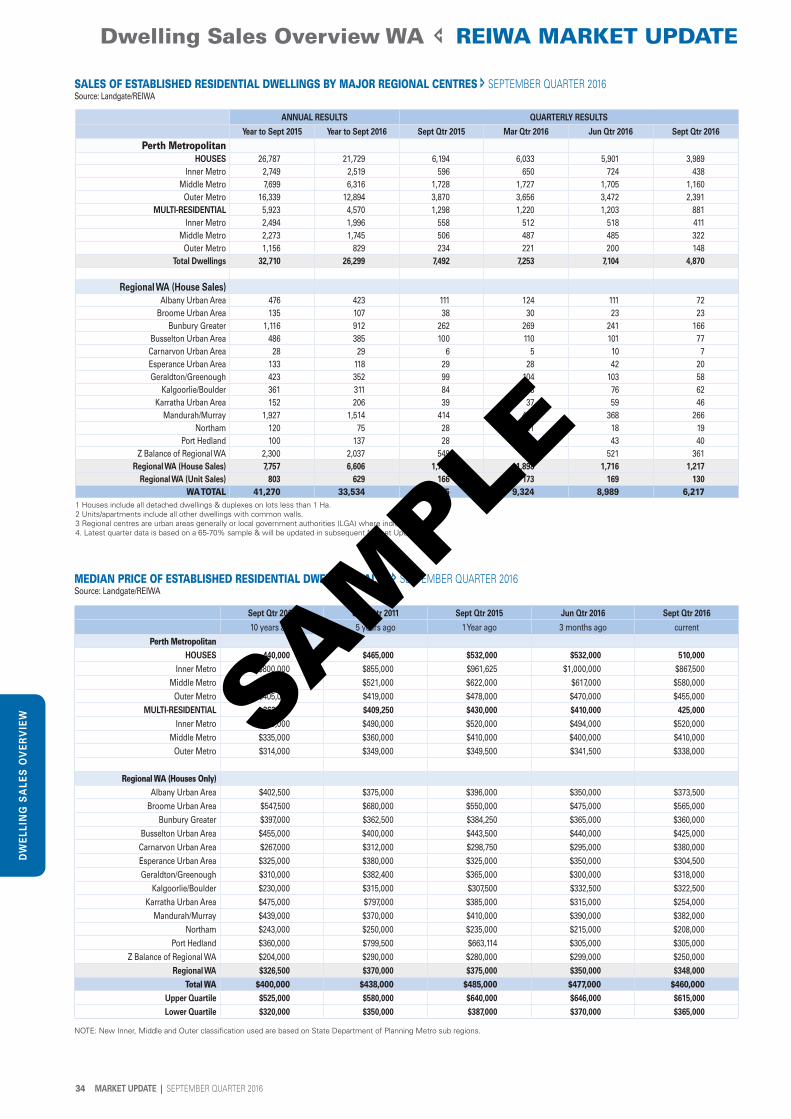

Houses, Perth $510,000 $532,000 -4.1% -4.1%Houses, Regional WA $348,000 $350,000 -0.6% -7.2%

Units/apartments, Perth $425,000 $410,000 3.7% -1.2%Units/apartments, Regional WA $273,500 $300,000 -8.8% -13.2%

All Dwellings, Perth $495,000 $515,000 -3.9% -4.1%All Dwellings, Regional WA $340,000 $350,000 -2.9% -8.1%

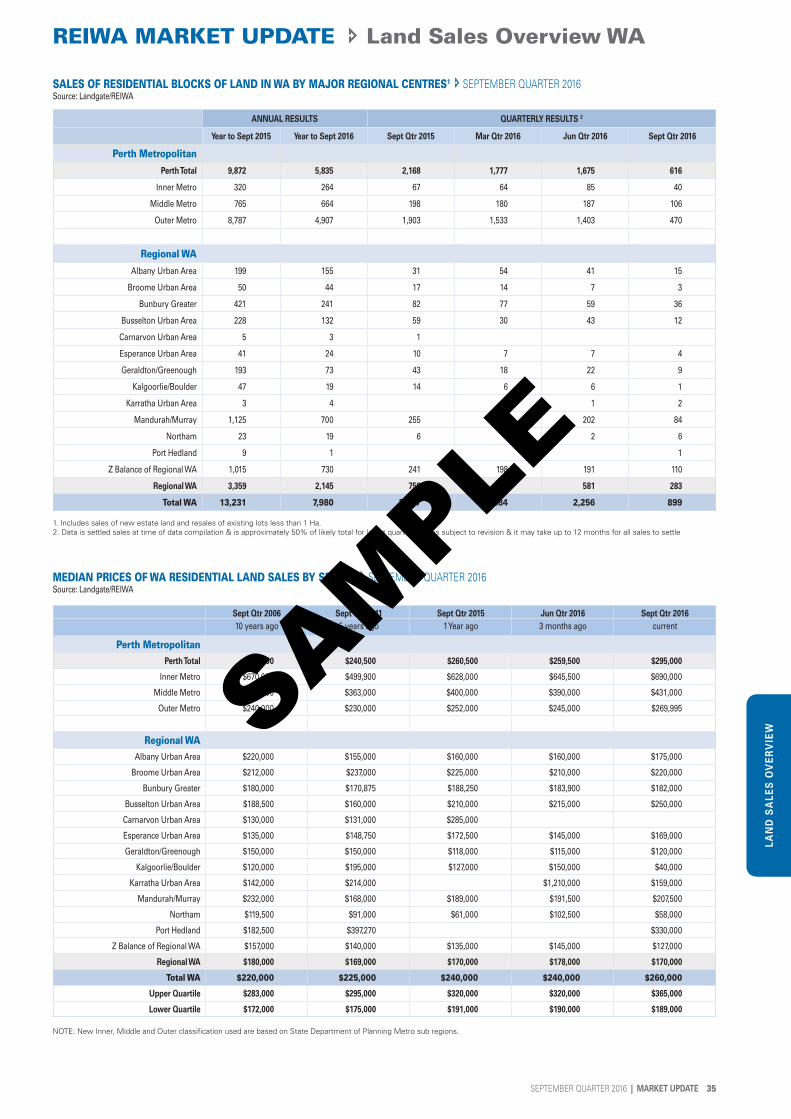

Land, Perth $295,000 $259,500 13.7% 13.2%Land, Regional WA $170,000 $178,000 -4.5% 0.0%

Buyer type 2 (% of total dwellings sold in WA)First home buyer 20.1%* 19.9% 0.2% pts -2.0% ptsTrade-up Buyers 63.4% 61.5% 1.9% pts -2.8% pts

Investor 16.5%* 18.6% -2.1% pts 4.8% pts

Sales 1

Houses, WA 5,206 7,617 -31.7% -34.8%Units/apartments, WA 1,011 1,372 -26.3% -30.9%

Total dwellings WA 6,217 8,989 -30.8% -34.2%Land, WA 899 2,256 -60.2% -69.3%

Average selling days residential property, Perth 69 67 2 days 5 daysSales to listings ratio, Perth 38.7% 62.1% -23.4% pts -26.2% pts

Properties for sale (end of qtr), Perth 14,164 14,134 0.2% -4.9%

Rental Market 3 Vacancy rate, Perth 6.6% 6.0% 0.6% pts 1.0% pts

Median weekly rent $370 $380 -2.6% -7.5%

Construction 4

Building approvals, all dwellings WA 5,219* 5,220 0.0% -26.5%

Finance 5

Home loan approvals, WA (includes refinancing) 20,239* 19,019 6.4% 7.9%

Interest Rates 6 (at quarters end)Official Cash Rate 1.50% 1.75% -0.25% pts -0.5% pts

Standard Variable Bank Home Loan Rate 5.25% 5.40% -0.15% pts -0.2% pts

Consumer Price Index 7

Perth 108.6 108.2 0.4% 0.5%Weighted Average - Eight Capital Cities 109.4 108.6 0.7% 1.3%

65

75

85

95

105

115

125

135

Jan-11M

ar-11M

ay-11Jul-11Sep-11N

ov-11Jan-12M

ar-12M

ay-12Jul-12Sep-12N

ov-12Jan-13M

ar-13M

ay-13Jul-13Sep-13N

ov-13Jan-14M

ar-14M

ay-14Jul-14Sep-14N

ov-14Jan-15M

ar-15M

ay-15Jul-15Sep-15N

ov-15Jan-16M

ar-16M

ay-16Jul-16Sep-16

Index (no.) Consumer Sentiment Index, Western Australia v National

Western Australia National

Source: Westpac-Melbourne Institute

Index WA National

Current month Sep-16 89.2 101.4

Previous month Aug-16 103.9 101.0

Previous year Sep-15 87.5 93.9

Five years ago Sep-11 108.0 96.9

Month Change -14.1% 0.4%

Year Change 1.9% 8.0%

SAMPLE

OV

ER

VIE

WP

ER

TH

RE

GIO

N

4 MARKET UPDATE | JUNE QUARTER 2016

Perth Housing and Land Market PERTH REGION

Multi-residential Dwelling Market The preliminary sales volumes for the multi-residential market for the September quarter are showing sales at 881, compared to a revised June 2016 quarterly figure of 1,203. At the time of publication of the June edition of Market Update, sales volumes were only at 878. This demonstrates a further lift in volumes of around 37 per cent. It can be expected that sales in the multi-residential market will also lift once figures are revised in the next quarter.

The drop off in sales continues to exist for the sixth quarter running and has been on an overall downward trend since the early part of 2013. Sales have decreased in all but one of the sub-regions for the September quarter, with the largest decline coming from the North West sub-region, down approximately 36 per cent against revised June 2016 quarter results.

As was the case until June 2015, the multi-residential median price moved in a tight band of $440-$450,000. However, between the quarters ending March 2016 and June 2016, median prices showed signs of decreasing. For the latest quarter ending September 2016, preliminary multi-residential median prices have lifted by approximately four

per cent to $425,000. The revised June 2016 quarter median is slightly higher at $410,000 from the initially reported $405,500.

The larger Central sub-region has seen median prices increase by around five per cent this quarter. However, the greatest change in multi-residential median prices has occurred in the South East sub-region where the median price has climbed from $247,000 in June 2016 to $285,500 (preliminary September 2016 quarter).

Housing Market A decline in sales activity can be seen within the overall Perth Metro Region as sales turnover has dropped by 32 per cent in the September 2016 quarter compared to revised turnover for the June 2016 quarter. The latest preliminary data continues to show sales volumes retracing further away from the fifteen year long-term average. It is important to note however, that settlements take time to come through, and whilst volumes are low for the September quarter, it can be observed that revised June 2016 quarter data show an increase of approximately 40 per cent in sales activity on preliminary figures.

Looking at the Perth monthly sales chart which uses reiwa.com data (reported sales by REIWA members), it can be seen that sales volumes are continuing to trend downwards on a monthly basis since February 2016. The reiwa.com monthly sales data provides a leading indicator on sales volumes given the nature of the data being reported rather than settled.

Preliminary house sales data shows that all of the sub-regions are lower at the end of the September quarter compared to the June 2016 quarter. The drop-off in volume figures as a whole may be explained by the general sentiment of consumers towards the local economy as well as a recent shift in population trends, with net interstate migration trends reversing and net overseas migration declining from the peaks experienced in 2013.

In the June 2016 Market Update report, the preliminary house median was reported at $520,000, which, as more settlements filtered through, has now been revised to $532,000 on a quarterly basis. The preliminary median house price for the quarter ending September 2016 is $510,000, and it is expected that this will lift as further house sales transactions settle. From a sub-regional perspective,

$425,000

$450,000

$475,000

$500,000

$525,000

$550,000

$575,000

$600,000

0

500

1000

1500

2000

2500

3000

3500

Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

PERTH MONTHLY HOUSE SALES

House SalesMedian House Price

Source: reiwa.com (C)

all have experienced medians decreasing by between one and seven per cent on a quarterly basis. However, on an annual basis (which is more stable measure of the market), medians have fallen by varying amounts between 2.8 and 5.4 per cent.

SAMPLE

OV

ER

VIE

WP

ER

TH

RE

GIO

N

SEPTEMBER QUARTER 2016 | MARKET UPDATE 5

PERTH REGION Perth Housing and Land Market

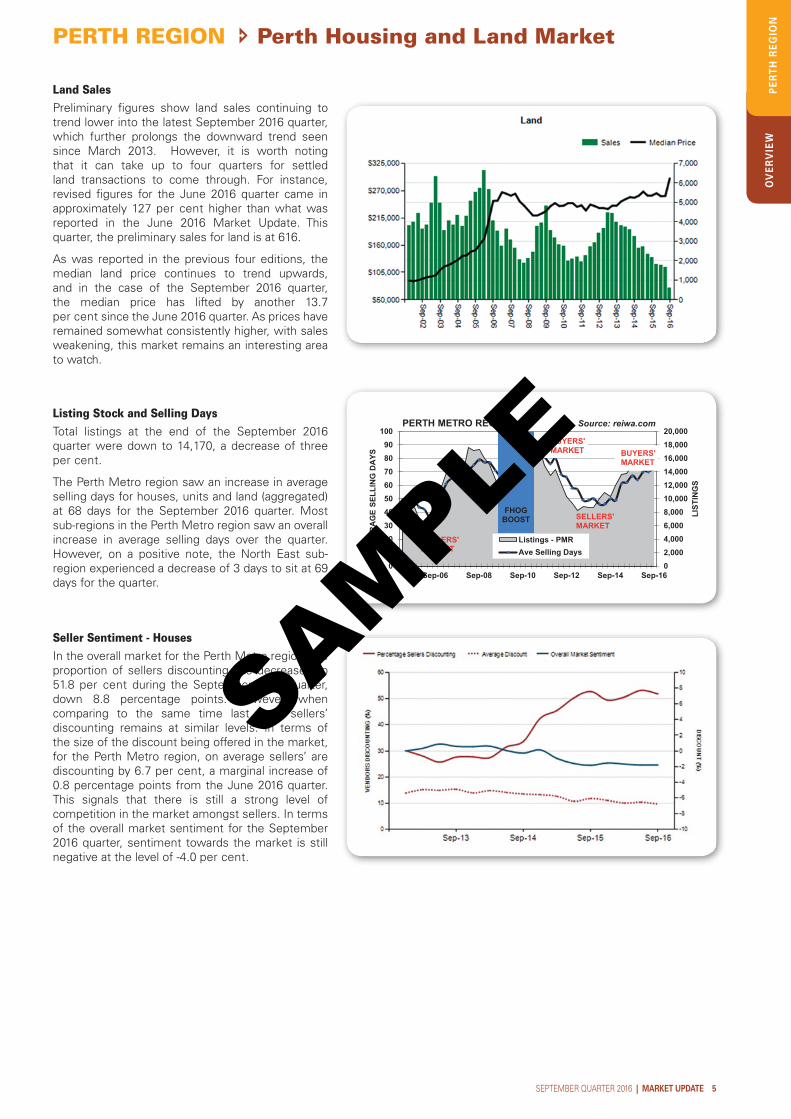

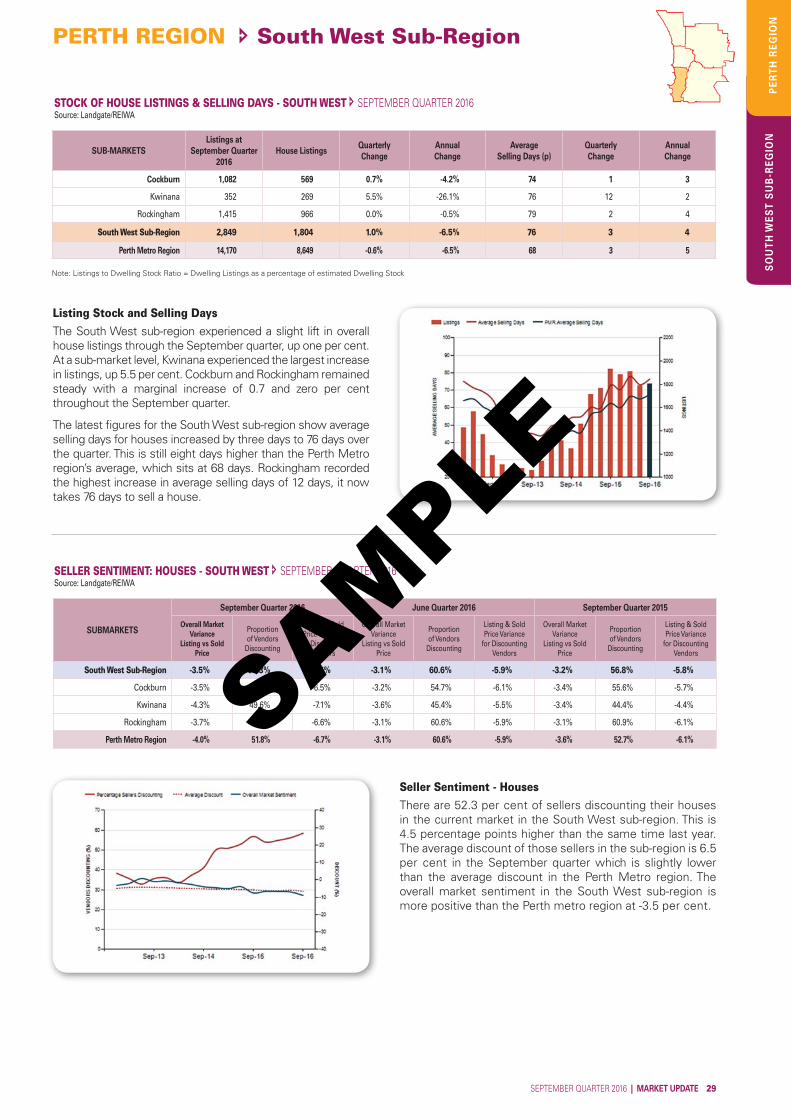

Seller Sentiment - HousesIn the overall market for the Perth Metro region, the proportion of sellers discounting has decreased to 51.8 per cent during the September 2016 quarter, down 8.8 percentage points. However, when comparing to the same time last year, sellers’ discounting remains at similar levels. In terms of the size of the discount being offered in the market, for the Perth Metro region, on average sellers’ are discounting by 6.7 per cent, a marginal increase of 0.8 percentage points from the June 2016 quarter. This signals that there is still a strong level of competition in the market amongst sellers. In terms of the overall market sentiment for the September 2016 quarter, sentiment towards the market is still negative at the level of -4.0 per cent.

Listing Stock and Selling Days Total listings at the end of the September 2016 quarter were down to 14,170, a decrease of three per cent.

The Perth Metro region saw an increase in average selling days for houses, units and land (aggregated) at 68 days for the September 2016 quarter. Most sub-regions in the Perth Metro region saw an overall increase in average selling days over the quarter. However, on a positive note, the North East sub-region experienced a decrease of 3 days to sit at 69 days for the quarter.

0102030405060708090

100

02,0004,0006,0008,00010,00012,00014,00016,00018,00020,000

Sep-16Sep-14Sep-12Sep-10Sep-08Sep-06

AVE

RA

GE

SELL

ING

DA

YS

LIST

ING

S

Listings - PMRAve Selling Days

FHOGBOOST

PERTH METRO REGION Source: reiwa.com

BUYERS' MARKET

SELLERS'MARKET

SELLERS'MARKET

BUYERS' MARKET

Land SalesPreliminary figures show land sales continuing to trend lower into the latest September 2016 quarter, which further prolongs the downward trend seen since March 2013. However, it is worth noting that it can take up to four quarters for settled land transactions to come through. For instance, revised figures for the June 2016 quarter came in approximately 127 per cent higher than what was reported in the June 2016 Market Update. This quarter, the preliminary sales for land is at 616.

As was reported in the previous four editions, the median land price continues to trend upwards, and in the case of the September 2016 quarter, the median price has lifted by another 13.7 per cent since the June 2016 quarter. As prices have remained somewhat consistently higher, with sales weakening, this market remains an interesting area to watch.

SAMPLE

OV

ER

VIE

WP

ER

TH

RE

GIO

N

Perth Overview PERTH REGION

6 MARKET UPDATE | JUNE QUARTER 2016

SUB-REGIONAL ANALYSISPERTH RESIDENTIAL MARKET YEAR TO SEPTEMBER 2016ANNUAL SALES, MEDIAN & QUARTILE PRICESSource: Landgate/REIWA

Data is for settled and pending sales data for the Year to June 2016 as at 24th October 2016 and may vary from other tables in this publication.Annual volumes are estimates based on 70% dwelling sales sample & 30-35% land sales sample for latest quarter. The Upper Quartile is the value of the bottom of the top 25% of the market - 25% of sales occurred above this price. The Median is the middle value of all sales placed in ascending order fom the cheapest to the most expensive. The Lower Quartile is the value of the top of the bottom 25% of the market - 25% of sales occurred below this price. 50% of sales fall within the values of the Upper and Lower Quartiles.

NORTH WEST

House Sales 4,292

Multi-Res Sales 214

Land Sales 1,257

Upper Quartile $650k $445k $340k

Median $520k $380k $258k

Lower Quartile $440k $340k $215k

Quarterly Change in Annual Median -1.0% -1.3% -0.8%

NORTH EAST

House Sales 2,555

Multi-Res Sales 130

Land Sales 1,031

Upper Quartile $554k $392k $294k

Median $460k $340k $247k

Lower Quartile $407k $310k $212k

Quarterly Change in Annual Median -1.1% n.c. -2.2%

PERTH METRO

House Sales 21,793

Multi-Res Sales 4,591

Land Sales 5,864

Upper Quartile $710k $565k $345k

Median $530k $425k $265k

Lower Quartile $427k $345k $215k

Quarterly Change in Annual Median -0.9% -0.7% 1.9%

CENTRAL

House Sales 8,861

Multi-Res Sales 3,758

Land Sales 932

Upper Quartile $940k $595k $635k

Median $681k $455k $460k

Lower Quartile $515k $365k $330k

Quarterly Change in Annual Median -1.3% n.c. 1.5%

SOUTH WEST

House Sales 3,400

Multi-Res Sales 382

Land Sales 1,441

Upper Quartile $535k $400k $310k

Median $445k $350k $243k

Lower Quartile $370k $270k $196k

Quarterly Change in Annual Median -1.1% 0.3% 1.3%

SOUTH EAST

House Sales 2,685

Multi-Res Sales 107

Land Sales 1,203

Upper Quartile $540k $345k $295k

Median $435k $300k $240k

Lower Quartile $360k $249k $205k

Quarterly Change in Annual Median -1.1% -3.2% n.c.

SAMPLE

OV

ER

VIE

WP

ER

TH

RE

GIO

N

PERTH REGION Perth Overview

SEPTEMBER QUARTER 2016 | MARKET UPDATE 7

PERTH METRO REGION

Year to June 2015

Year to June 2016

March Qtr 2016

June Qtr 2016

Sales% of total sales

Sales% of total sales

Sales% of total sales

Sales% of total sales

HOUSE

Up to $200,000 28 0.1% 49 0.2% 15 0.2% 20 0.5%

$200 - $300,000 562 1.8% 475 1.7% 201 3.3% 173 4.3%

$300 - $350,000 1472 4.6% 1204 4.4% 344 5.7% 266 6.6%

$350 - $400,000 2431 7.6% 2317 8.5% 614 10.2% 435 10.7%

$400 - $450,000 3718 11.7% 3521 12.9% 724 12.1% 574 14.2%

$450 - $500,000 3850 12.1% 3248 11.9% 684 11.4% 487 12.0%

$500 - $550,000 3608 11.3% 2857 10.5% 612 10.2% 426 10.5%

$550 - $600,000 3035 9.5% 2388 8.8% 481 8.0% 283 7.0%

$600 - $650,000 2339 7.3% 1854 6.8% 404 6.7% 259 6.4%

$650 - $700,000 1737 5.5% 1524 5.6% 296 4.9% 201 5.0%

$700 - $800,000 2592 8.1% 2268 8.3% 449 7.5% 303 7.5%

$800 - $900,000 1927 6.1% 1623 6.0% 336 5.6% 194 4.8%

$900 - $1 million 1123 3.5% 920 3.4% 169 2.8% 102 2.5%

$1 - $1.5 million 2251 7.1% 1998 7.3% 446 7.4% 233 5.8%

Over $1.5 million 1155 3.6% 965 3.5% 229 3.8% 94 2.3%

UNIT

Up to $200,000 62 0.8% 54 0.9% 31 2.6% 21 2.4%

$200 - $250,000 224 3.0% 220 3.7% 61 5.1% 40 4.5%

$250 - $300,000 511 6.7% 426 7.2% 102 8.5% 74 8.4%

$300 - $350,000 824 10.9% 768 13.0% 172 14.3% 106 12.0%

$350 - $400,000 1039 13.7% 813 13.7% 204 17.0% 126 14.3%

$400 - $450,000 1123 14.8% 931 15.7% 144 12.0% 129 14.6%

$450 - $500,000 867 11.4% 605 10.2% 109 9.1% 78 8.9%

$500 - $550,000 708 9.3% 484 8.2% 87 7.2% 69 7.8%

$550 - $600,000 556 7.3% 352 5.9% 62 5.2% 56 6.4%

$600 - $700,000 672 8.9% 506 8.5% 84 7.0% 70 7.9%

$700 - $850,000 473 6.2% 329 5.6% 55 4.6% 56 6.4%

$850 - $1 million 207 2.7% 159 2.7% 29 2.4% 21 2.4%

Over $1 million 313 4.1% 276 4.7% 63 5.2% 35 4.0%

VACANT LAND

Up to $150,000 433 3.0% 138 1.4% 41 2.4% 16 2.6%

$150 - $175,000 1033 7.2% 496 5.0% 101 6.0% 25 4.0%

$175 - $200,000 1606 11.2% 1049 10.6% 219 13.0% 61 9.8%

$200 - $225,000 1948 13.5% 1344 13.5% 206 12.2% 59 9.5%

$225 - $250,000 2006 13.9% 1237 12.5% 211 12.5% 56 9.0%

$250 - $275,000 1525 10.6% 1223 12.3% 172 10.2% 49 7.9%

$275 - $300,000 1280 8.9% 1056 10.6% 154 9.2% 66 10.6%

$300 - $350,000 1666 11.6% 1345 13.6% 194 11.5% 74 11.9%

$350 - $400,000 952 6.6% 652 6.6% 95 5.6% 55 8.8%

$400 - $500,000 871 6.1% 502 5.1% 110 6.5% 65 10.4%

$500 - $750,000 728 5.1% 629 6.3% 120 7.1% 73 11.7%

$750 - $1 million 158 1.1% 128 1.3% 22 1.3% 15 2.4%

Over $1 million 185 1.3% 120 1.2% 38 2.3% 10 1.6%

Analysis includes all sales transactions including houses and land on lots > 1 Ha

RESIDENTIAL REAL ESTATE SALES BY PRICE RANGE SEPTEMBER QUARTER 2016Source : Landgate/REIWA

Housing MarketThe preliminary median house price for the September 2016 quarter is $510,000, with the majority of house sales for the quarter sitting within the price range of $400-$500,000. In comparison to the June 2016 quarter, the percentage of transactions within the higher price ranges of $800,000 to greater than $1.5 million are at lower levels for the latest quarter. The $550-$650,000 price range also observed a marginal decline in percentage of sales transactions in comparison to the June 2016 quarter. On the other hand, a greater number of transactions are evident in the lower priced market ($200-$550,000).The higher transactions at the lower end of the market explains the decline of 4.1 per cent in the preliminary median house price for the September quarter.

Land Sales There continues to be a clear positive shift in the percentage of land sales between the $275,000 - $1 Million price ranges. The chart also indicates softening in most of the markets below $275,000. The shift in sales towards the higher end of the market explains the 13.7 per cent increase in the preliminary median land price for the September 2016 quarter.

Multi-residential MarketThe preliminary median unit price is $425,000 for the latest quarter ending September 2016. During this latest quarter, the $400-$450,000 price range saw the most action in terms of sales. On the other hand, during the June 2016 quarter, most sales occurred within the $350-$400,000 price range. The higher end of the market ($500-850,000) also recorded an increase in percentage sales activity in comparison to the June 2016 quarter. In contrast, the lower end of the market below $400,000 recorded a decrease in percentage sales activity in the September 2016 quarter compared to the June 2016 quarter. This explains the improvement of 3.6 per cent in the preliminary median unit price for the September 2016 quarter.SAMPLE

CE

NT

RA

L S

UB

-RE

GIO

N

8 MARKET UPDATE | SEPTEMBER QUARTER 2016

Central Sub-Region PERTH REGIONP

ER

TH

RE

GIO

N

Housing MarketPreliminary data for the September 2016 quarter, show early indications the volume of house sales in the Central sub-region is down by approximately 34 per cent in comparison to the previous quarter. Whilst this decline is more than the June 2016 quarter, REIWA expects revised September quarter data to lift in coming months as more transactions settle. The preliminary figures shows sub-markets including Western Suburbs (down 48 per cent), Vincent/Stirling SE (down 47 per cent), Belmont (down 41 per cent), Stirling West (down 33 per cent), Fremantle (down 32 per cent) and South Perth/Victoria Park (down 32 per cent), all experienced falls in the number of sales by greater than 30 per cent for the September quarter.

Preliminary data has the overall Central sub-region quarterly median for the September quarter down by 6.5 per cent to $645,000 over the revised June quarter median of $690,000. At a sub-market level, the preliminary medians were mixed across the board with drops ranging from -1.9 per cent in Bassendean/Bayswater to -12.8 per cent in South Perth/Victoria Park. The better performing sub-market included: Canning (-0.5 per cent), Stirling West (-2.4 per cent), Belmont (-3.0 per cent) and Melville (-3.9 per cent).

In terms of the change in annual medians, all sub-markets in the Central sub-region have recorded a negative change, with drops recorded from -2.7 per cent in the Western Suburbs to -12.8 per cent in Perth City sub-market. There are a few suburbs in the sub-region that shone a positive light including: Burswood (+16.7 per cent), Swanbourne (+14.8 per cent) and Trigg (+12.9 per cent).

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

$650,000

$700,000

$750,000

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

HOUSE SALES - CENTRALHOUSE MEDIAN - CENTRALPMR HOUSE MEDIAN

Source: Landgate/REIWAPERTH CENTRAL SUB-REGION

10 Year Ave

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

500

1,000

1,500

2,000

2,500

3,000

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

HOUSE SALES - MIDDLEHOUSE MEDIAN - MIDDLEPMR HOUSE MEDIAN

Source: Landgate/REIWAPERTH MIDDLE SUB-REGION

10 Year Ave

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

0

200

400

600

800

1,000

1,200

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

HOUSE SALES - INNERHOUSE MEDIAN - INNERPMR HOUSE MEDIAN

Source: Landgate/REIWAPERTH INNER SUB-REGION

10 Year Ave

TOP 10 SUBURBS BY QUARTERLY CHANGE IN PRICE Source: Landgate/REIWA

CENTRAL

Year to September 2016 Quarterly Change

in Annual Median %

House Sales

Median Price Highest Price

Riverton 64 $690,000 $1,900,000 8.9%

Attadale 74 $1,066,250 $4,130,000 7.4%

Bentley 51 $550,000 $750,000 5.3%

East Cannington 67 $520,000 $980,000 4.0%

Alfred Cove 44 $884,000 $1,730,000 3.5%

Woodlands 46 $875,000 $2,100,000 2.9%

Fremantle 62 $846,500 $2,050,000 2.9%

Wilson 81 $550,000 $988,000 2.8%

South Perth 73 $1,225,000 $4,300,000 2.1%

Ascot 31 $770,000 $1,850,000 2.0%

Excludes suburbs with less than 30 sales for the year & dwellings on lots greater than 1 Ha.

The suburbs with the greatest decline in annual change in annual medians include: O’Connor (-28.0 per cent), Waterford (-25.5 per cent), Coolbinia (-19.0 per cent) and Joondanna (-18.0 per cent).

The top three performing suburbs based on quarterly change in annual median include: Riverton (+8.9 per cent) with a median of $690,000, Attadale (+7.4 per cent) with a median of $1,066,250 and Bentley (+5.3 per cent) with a median of $550,000.

SAMPLE

SEPTEMBER QUARTER 2016 | MARKET UPDATE 9

PERTH REGION Central Sub-Region

CE

NT

RA

L S

UB

-RE

GIO

NP

ER

TH

RE

GIO

N

Listing Stock and Selling DaysThe overall stock of house listings in the Central sub-region declined in the September 2016 quarter by 2.1 per cent to 2,573. The middle sub-region contributed the most to the drop in house listings, decreasing by 2.3 per cent over the quarter. The Perth Metro region also saw a decline in house listings but by a smaller magnitude of 0.6 per cent for the quarter.

Average selling days for houses increased in the Central sub-region by three days to 63 days for the quarter and is seven days higher than last year. The only sub-market to record a reduction in average selling days was Canning which now only takes 53 days to sell a house. The Perth Metro Region saw an increase in days on market to 68 days for the quarter.

STOCK OF HOUSE LISTINGS & SELLING DAYS SEPTEMBER QUARTER 2016

SUB-MARKETS & SUBURBSListings at Sept

Quarter 2016House Listings

Quarterly Change

Annual Change

Average Selling Days (p)

Quarterly Change

Annual Change

Inner 1,971 728 -1.5% -13.9% 62 0 2Fremantle 261 121 -6.2% -14.8% 61 -12 5Perth City 473 41 5.1% -10.9% 42 -36 -29

South Perth/Victoria Park 573 257 2.8% -3.0% 68 2 4Vincent 146 51 24.4% -1.9% 53 -2 3

Western Suburbs 518 258 -7.9% -24.3% 62 7 3Middle 3,304 1,845 -2.3% -1.0% 64 4 9

Bassendean/Bayswater 523 297 -2.3% -7.8% 61 3 13Belmont 358 149 -15.3% -5.1% 70 11 12Canning 446 289 -2.7% 5.5% 53 -6 6Melville 558 399 -4.3% -5.9% 73 9 13

Stirling East 821 440 10.0% 7.8% 66 4 6Stirling SE 132 60 7.1% -14.3% 68 3 10Stirling West 466 211 -11.3% 1.0% 59 7 3

Central Sub-Region 5,275 2,573 -2.1% -5.1% 63 3 7Perth Metro Region 14,170 8,649 -0.6% -6.5% 68 3 5

Source: reiwa.com

SUBMARKETS

September Quarter 2016 June Quarter 2016 September Quarter 2015Overall Market

Variance Listing vs Sold

Price

Proportion of Vendors

Discounting

Listing & Sold Price Variance for Discounting

Vendors

Overall Market Variance

Listing vs Sold Price

Proportion of Vendors

Discounting

Listing & Sold Price Variance

for Discounting Vendors

Overall Market Variance

Listing vs Sold Price

Proportion of Vendors

Discounting

Listing & Sold Price Variance for Discounting

Vendors

Central Sub-Region -4.5% 45.3% -7.2% -4.8% 34.8% -7.8% -4.0% 49.0% -6.6%Bassendean/Bayswater -3.5% 53.8% -6.4% -3.6% 58.9% -6.4% -4.0% 46.3% -5.6%

Belmont -4.0% 47.0% -7.4% -3.2% 49.2% -6.0% -4.9% 44.7% -8.3%Canning -3.7% 51.9% -6.2% -4.3% 56.0% -6.7% -3.6% 48.4% -5.5%

Fremantle -3.1% 41.1% -6.0% -3.6% 47.0% -7.3% -3.9% 38.5% -4.5%Melville -4.6% 50.8% -7.9% -5.2% 58.9% -7.2% -3.9% 56.7% -5.9%

Perth City -4.2% 30.0% -4.7% -6.6% 34.8% -10.5% -4.1% 73.9% -5.0%South Perth/Victoria Park -4.6% 39.2% -7.4% -4.5% 47.3% -8.4% -4.1% 51.1% -7.9%

Stirling East -3.6% 51.6% -7.0% -3.6% 52.9% -6.8% -3.6% 56.1% -6.2%Stirling West -3.8% 42.9% -5.5% -4.5% 34.8% -6.5% -3.5% 42.0% -5.7%

Vincent/Stirling SE -3.7% 34.0% -6.0% -3.9% 52.2% -5.6% -4.1% 48.0% -7.4%Western Suburbs -6.5% 33.5% -9.0% -4.8% 34.8% -7.8% -4.9% 44.2% -8.4%Perth Metro Region -4.0% 51.8% -6.7% -3.1% 60.6% -5.9% -3.6% 52.7% -6.1%

SELLER SENTIMENT: HOUSES SEPTEMBER QUARTER 2016 Source: reiwa.com

Seller Sentiment - HousesThe proportion of sellers discounting in the Central sub-region house market has increased again in the September quarter with 45.3 per cent of sellers discounting compared to 34.8 per cent in June quarter (revised) 2016. The sub-markets with the most sellers discounting in the September quarter are Bassendean/Bayswater at 53.8 per cent and Canning at 51.9 per cent. In the Perth Metro Region, the number of sellers discounting has declined to 51.8 per cent from 60.6 per cent (revised) June quarter 2016.

The discount offered by sellers in the Central sub-region is 7.2 per cent for the September quarter, declining from 7.8 per cent in the June 2016 quarter. So whilst there has been an increase in the proportion of sellers discounting, the discount offered has reduced. This may signal, sellers are meeting the market at the time of listing and not having to adjust their prices significantly in order to sell.

SAMPLE

CE

NT

RA

L S

UB

-RE

GIO

N

10 MARKET UPDATE | SEPTEMBER QUARTER 2016

Central Sub-Region PERTH REGIONP

ER

TH

RE

GIO

N

MEDIAN PRICE OF ESTABLISHED HOUSE SALES - PERTH CENTRAL SUBURBS SEPTEMBER QUARTER 2016Source: Landgate/REIWA

SUB-MARKETS& SUBURBS

Year to September 2016 %Change Quarterly Sales Price

House Sales

Lower Quartile

Median Price

Upper Quartile

Highest Price

Quarterly Change Annual

Median %

Annual Change Annual

Median %

September Qtr 2015

June Qtr 2016 September Qtr 2016 (P)

Prelim Qtly

Change

June Qtr 2016

Sales

Sept Qtr 2016

Sales

House Rent per

week

House Average Selling Days

Central Sub-Region 8,835 $515,000 $681,000 $940,000 $14,130,000 -1.3% -5.4% $685,000 $690,000 $645,000 -6.5% 2,429 1,598 $420 63Bassendean/Bayswater 1,010 $480,000 $550,000 $640,000 $2,550,000 -1.5% -8.3% $589,404 $550,000 $539,500 -1.9% 284 192 $395 61

Ashfield 18 $480,000 $500,000 $547,000 $850,000 0.0% 0.0% $526,250 $536,000 $530,000 -1.1% 8 3 $320 19Bassendean 160 $460,000 $515,000 $595,000 $1,500,000 -2.7% -11.2% $580,000 $490,000 $535,000 9.2% 36 25 $380 43

Bayswater 203 $529,500 $600,000 $680,000 $1,245,000 -3.2% -6.3% $670,000 $597,500 $560,000 -6.3% 66 37 $420 55Bedford 70 $530,000 $636,000 $750,000 $1,050,000 -0.2% -2.9% $629,500 $662,500 $579,995 -12.5% 16 14 $370 57

Eden Hill 40 $400,000 $434,750 $485,000 $736,500 -1.2% -8.5% $479,500 $428,750 $450,000 5.0% 12 9 $380 67Embleton 56 $447,500 $506,250 $555,000 $670,000 -0.3% -10.4% $508,000 $520,000 $527,500 1.4% 15 12 $400 61Maylands 95 $548,500 $652,500 $775,000 $2,550,000 -3.2% -6.8% $673,000 $702,500 $601,000 -14.4% 26 17 $400 52

Morley 293 $464,500 $522,500 $580,000 $780,000 -1.4% -6.7% $535,000 $532,500 $520,000 -2.3% 88 59 $390 80Noranda 75 $507,500 $590,000 $638,250 $765,000 -2.5% -6.3% $615,000 $580,000 $560,000 -3.4% 17 16 $420 44

Belmont 501 $440,000 $507,000 $615,000 $1,850,000 -2.5% -7.8% $541,000 $495,000 $480,000 -3.0% 151 89 $360 70Ascot 31 $519,000 $770,000 $930,000 $1,850,000 2.0% -4.3% $695,000 $816,550 $770,000 -5.7% 8 5 $418 79

Belmont 83 $423,500 $485,000 $595,000 $1,008,000 -2.0% -9.3% $519,000 $445,000 $473,750 6.5% 21 14 $360 55Cloverdale 122 $438,000 $480,000 $540,000 $980,000 -3.7% -7.7% $507,500 $496,000 $455,000 -8.3% 38 31 $350 82

Kewdale 90 $455,000 $510,000 $600,000 $950,000 1.0% 1.6% $501,250 $532,000 $506,250 -4.8% 29 14 $360 53Redcliffe 87 $380,000 $473,500 $592,500 $990,000 -5.3% -5.3% $540,000 $423,750 $455,000 7.4% 26 11 $348 79

Rivervale 88 $500,000 $592,500 $668,000 $1,352,500 0.4% -3.7% $561,500 $559,000 $590,000 5.5% 29 14 $397 66

Canning 944 $455,000 $550,000 $692,500 $2,900,000 -0.5% -3.9% $563,000 $552,500 $550,000 -0.5% 256 181 $380 53Bentley 51 $472,750 $550,000 $617,500 $750,000 5.3% 3.3% $498,000 $585,000 $505,000 -13.7% 10 13 $375 62

Cannington 58 $390,000 $430,000 $486,000 $975,000 -1.1% -10.4% $460,000 $430,000 $429,000 -0.2% 21 9 $350 48East Cannington 67 $432,500 $520,000 $610,000 $980,000 4.0% 1.5% $463,000 $511,000 $455,000 -11.0% 18 18 $380 55

Ferndale 54 $420,000 $465,000 $520,000 $625,000 -2.1% -3.9% $500,000 $490,000 $475,000 -3.1% 18 11 $325 45Lynwood 58 $420,000 $450,000 $470,000 $520,000 -0.4% -8.3% $470,000 $450,000 $432,500 -3.9% 17 12 $360 43

Parkwood 70 $400,000 $480,000 $562,000 $760,000 -4.2% -5.9% $524,500 $515,000 $472,500 -8.3% 20 12 $380 47Queens Park 84 $434,500 $467,500 $532,500 $1,100,000 1.0% -2.5% $455,000 $468,000 $489,000 4.5% 21 12 $373 44

Riverton 64 $555,000 $690,000 $778,000 $1,900,000 8.9% 1.8% $618,500 $652,000 $702,500 7.7% 19 14 $370 59Rossmoyne 31 $893,500 $1,140,000 $1,311,500 $2,900,000 -0.5% 0.4% $1,110,000 $1,305,000 $980,000 -24.9% 7 7 $475 53

Shelley 41 $630,000 $825,000 $1,002,500 $2,850,000 -5.5% -4.1% $885,000 $845,000 $704,500 -16.6% 13 10 $390 57St James 74 $455,000 $537,500 $620,000 $1,300,000 -3.2% -9.8% $610,000 $517,500 $535,000 3.4% 17 11 $375 70Willetton 211 $623,700 $700,000 $781,500 $1,180,000 0.0% -4.1% $710,000 $661,000 $739,444 11.9% 57 34 $420 50

Wilson 81 $440,000 $550,000 $640,500 $988,000 2.8% -5.6% $530,000 $612,500 $543,000 -11.3% 18 18 $383 57Fremantle 398 $584,000 $742,500 $1,000,000 $3,070,000 -1.0% -7.2% $760,000 $727,500 $697,500 -4.1% 114 78 $495 61

Beaconsfield 75 $620,000 $705,000 $838,500 $1,600,000 -2.1% -8.4% $795,000 $727,500 $700,000 -3.8% 24 16 $425 57East Fremantle 68 $821,500 $1,085,000 $1,385,000 $3,070,000 -5.7% -10.5% $1,220,000 $1,120,000 $1,060,000 -5.4% 16 13 $563 68

Fremantle 62 $675,000 $846,500 $950,000 $2,050,000 2.9% 5.5% $786,250 $847,500 $787,500 -7.1% 18 8 $495 69Hilton 71 $510,000 $549,500 $605,000 $770,000 -0.1% -4.4% $560,000 $535,000 $541,500 1.2% 23 16 $350 76

North Fremantle 25 $789,500 $975,000 $1,362,500 $2,600,000 0.8% -4.9% $750,000 $960,000 $960,000 0.0% 7 1 $650 59O'Connor 5 $460,000 $475,000 $582,500 $615,000 -7.3% -28.0% $397,500 1 $335 214

Samson 15 $503,500 $566,000 $647,500 $715,000 -8.7% -16.1% $690,500 $620,000 $560,000 -9.7% 3 4 20South Fremantle 38 $780,000 $1,035,000 $1,290,000 $1,750,000 -0.5% 3.9% $1,150,000 $1,045,000 $1,015,000 -2.9% 12 8 $560 57

White Gum Valley 39 $625,000 $700,000 $830,000 $1,200,000 -1.4% -3.4% $702,500 $725,000 $675,000 -6.9% 11 11 $550 33

Melville 1,182 $640,000 $780,000 $995,000 $6,800,000 0.0% -4.3% $760,000 $775,000 $745,000 -3.9% 291 211 $450 73Alfred Cove 44 $675,000 $884,000 $1,075,000 $1,730,000 3.5% 4.0% $712,500 $675,000 $675,000 0.0% 9 5 $600 55Applecross 79 $1,020,000 $1,490,000 $2,137,500 $6,800,000 -0.7% 7.2% $1,407,500 $1,175,000 $1,265,000 7.7% 16 16 $597 102

Ardross 77 $802,000 $960,000 $1,232,500 $2,075,000 -8.6% -0.7% $1,132,500 $1,070,000 $900,000 -15.9% 17 14 $535 70Attadale 74 $772,500 $1,066,250 $1,384,000 $4,130,000 7.4% 4.0% $850,000 $980,000 $1,195,000 21.9% 21 7 $550 69

Bateman 35 $710,000 $778,000 $826,500 $1,270,000 0.0% -4.6% $750,000 $740,000 $710,000 -4.1% 9 5 $450 39Bicton 56 $725,000 $915,000 $1,412,500 $3,500,000 -3.7% -8.3% $965,500 $952,500 $807,500 -15.2% 14 6 $398 49

Booragoon 80 $747,500 $880,500 $988,000 $1,600,000 1.8% 0.5% $807,500 $895,000 $875,000 -2.2% 28 15 $495 37Brentwood 16 $559,500 $684,500 $886,000 $1,200,000 -0.8% 2.9% $650,000 $780,000 $620,000 -20.5% 4 3 $373 28Bull Creek 65 $645,000 $750,000 $870,000 $1,450,000 0.0% -0.7% $683,000 $760,000 $685,500 -9.8% 13 12 $400 70Kardinya 95 $582,500 $653,000 $733,500 $1,200,000 0.2% -4.1% $589,000 $670,000 $607,500 -9.3% 21 20 $400 73Leeming 110 $620,000 $699,000 $780,000 $1,125,000 -0.1% -6.0% $710,000 $722,500 $738,000 2.1% 24 27 $425 85Melville 90 $690,000 $785,000 $900,000 $2,500,000 0.0% -1.9% $760,000 $785,000 $770,000 -1.9% 27 13 $470 85

Mount Pleasant 74 $855,000 $1,128,250 $1,700,000 $5,500,000 -2.7% -1.0% $1,195,000 $1,172,000 $1,110,000 -5.3% 18 15 $480 110Murdoch 24 $649,000 $765,000 $802,500 $950,000 0.0% -0.6% $655,000 $765,000 $760,000 -0.7% 9 5 $290 78

Myaree 26 $635,000 $684,250 $770,000 $1,125,000 -4.4% -9.4% $740,000 $680,000 $640,000 -5.9% 5 5 $438 27Palmyra 102 $545,000 $660,000 $795,000 $1,200,000 -7.0% -7.7% $702,500 $703,500 $650,000 -7.6% 22 21 $405 57Willagee 82 $500,000 $560,000 $630,000 $870,000 -1.5% -8.2% $586,250 $555,000 $548,000 -1.3% 20 13 $380 66

Winthrop 53 $781,500 $850,000 $1,007,500 $1,900,000 0.0% -2.0% $827,500 $865,000 $800,000 -7.5% 14 9 $565 105

Perth City 52 $660,000 $806,250 $980,000 $2,665,000 3.7% -12.8% $770,000 $632,000 $830,000 31.3% 13 11 $438 42East Perth 10 $1,100,000 $1,395,000 $1,800,000 $2,665,000 8.6% 3.7% $1,175,000 $1,800,000 3 $450 41

Perth 30 $665,000 $777,500 $880,000 $1,090,000 1.6% -12.6% $855,000 $710,000 $830,000 16.9% 9 7 $450 40West Perth 12 $538,500 $696,500 $847,500 $1,075,000 1.2% -4.3% $707,000 $538,500 $725,000 34.6% 4 1 $410 15

SAMPLE

SEPTEMBER QUARTER 2016 | MARKET UPDATE 11

PERTH REGION Central Sub-Region

CE

NT

RA

L S

UB

-RE

GIO

NP

ER

TH

RE

GIO

N

MEDIAN PRICE OF ESTABLISHED HOUSE SALES - PERTH CENTRAL SUBURBS SEPTEMBER QUARTER 2016Source: Landgate/REIWA

Excludes suburbs with less than 5 sales for the year & dwellings on lots greater than 1 Ha. All figures are preliminary for up to 4 months after end of quarter.© REIWA - For the exclusive use of REIWA Subscribers. Unauthorised distribution, reproduction or sale of the data will breach REIWA’s copyright

SUB-MARKETS& SUBURBS

Year to September 2016 %Change Quarterly Sales Price

House Sales

Lower Quartile

Median Price

Upper Quartile

Highest Price

Quarterly Change Annual

Median %

Annual Change Annual

Median %

September Qtr 2015

June Qtr 2016 September Qtr 2016 (P)

Prelim Qtly

Change

June Qtr 2016

Sales

Sept Qtr 2016

Sales

House Rent per

week

House Average Selling Days

South Perth/Victoria Park 724 $601,750 $764,500 $960,000 $4,300,000 -2.0% -2.8% $790,000 $782,500 $682,500 -12.8% 200 137 $400 68Burswood 17 $741,500 $1,050,000 $1,420,000 $1,700,000 -7.1% 16.7% $1,235,500 $1,130,000 $962,500 -14.8% 3 4 $450 68

Carlisle 103 $450,000 $530,000 $600,000 $900,000 -1.9% -9.0% $594,250 $445,000 $547,500 23.0% 28 28 $390 58Como 123 $740,000 $855,000 $1,117,500 $1,900,000 -4.5% -8.1% $965,000 $835,000 $802,500 -3.9% 33 22 $428 51

East Victoria Park 131 $566,000 $647,500 $777,500 $1,215,000 -0.4% -0.5% $652,000 $643,750 $645,000 0.2% 34 20 $380 82Karawara 9 $775,000 $810,000 $958,750 $967,500 -0.2% 5.2% $1,275,000 $812,000 $800,000 -1.5% 1 3 $395 82

Kensington 58 $750,000 $855,000 $955,000 $1,385,000 0.0% -2.0% $812,500 $860,000 $855,000 -0.6% 20 9 $475 100Lathlain 34 $570,000 $717,500 $905,000 $1,030,000 -16.1% -13.6% $900,000 $760,000 $601,000 -20.9% 8 9 $445 85

Manning 58 $650,000 $790,000 $950,000 $1,350,000 -1.3% -8.0% $730,000 $820,500 $567,500 -30.8% 18 6 $550 31Salter Point 36 $890,000 $1,015,000 $1,325,000 $2,060,000 -1.5% -9.8% $1,125,000 $960,000 $1,060,000 10.4% 9 4 $648 53South Perth 73 $949,000 $1,225,000 $1,587,500 $4,300,000 2.1% -2.0% $1,250,000 $1,120,000 $1,427,500 27.5% 25 10 $495 80

Victoria Park 52 $567,500 $652,500 $753,750 $1,550,000 -2.6% -6.5% $709,000 $642,500 $620,000 -3.5% 14 9 $390 37Waterford 30 $705,000 $845,750 $1,090,000 $1,700,000 -16.6% -25.5% $1,380,000 $842,500 $705,000 -16.3% 7 13 $455 97

Stirling East 1,499 $410,000 $493,800 $645,000 $1,650,000 -1.2% -3.2% $500,000 $512,500 $466,000 -9.1% 388 278 $350 66Balcatta 129 $450,000 $540,000 $615,000 $1,030,000 -1.8% -1.5% $570,000 $567,500 $550,000 -3.1% 24 27 $380 71

Balga 260 $356,000 $385,000 $417,000 $550,000 -1.3% -6.1% $405,000 $377,500 $360,000 -4.6% 57 42 $325 70Dianella 259 $510,000 $620,000 $755,000 $1,610,000 0.0% -6.1% $615,000 $645,000 $595,000 -7.8% 76 48 $350 70

Glendalough 7 $509,000 $535,000 $625,000 $670,000 -4.5% 3.5% $578,500 $655,000 $535,000 -18.3% 1 3 $308 20Hamersley 86 $499,000 $549,500 $615,000 $901,000 -0.5% -2.7% $563,500 $535,000 $512,000 -4.3% 25 10 $370 47Joondanna 49 $550,000 $660,000 $821,944 $1,155,000 -5.7% -18.0% $850,000 $655,000 $535,000 -18.3% 16 10 $398 121Mirrabooka 60 $395,000 $415,000 $437,500 $530,000 -2.4% -3.5% $430,000 $417,500 $372,000 -10.9% 20 11 $355 39Nollamara 190 $411,000 $440,000 $480,000 $780,000 -2.2% -5.4% $460,000 $429,000 $433,194 1.0% 44 44 $360 71

Osborne Park 19 $450,000 $515,000 $666,000 $1,000,000 -1.9% -7.2% $546,000 $448,750 $505,000 12.5% 2 4 $400 52Stirling 112 $644,000 $817,500 $972,500 $1,650,000 1.7% 2.2% $737,500 $817,500 $741,000 -9.4% 34 20 $508 63

Tuart Hill 58 $500,000 $573,000 $643,000 $1,000,000 -1.8% -5.3% $620,000 $576,000 $532,500 -7.6% 17 9 $380 54Westminster 117 $392,500 $429,000 $468,000 $650,000 -2.1% -4.2% $454,500 $420,000 $400,000 -4.8% 37 26 $340 77

Yokine 153 $525,000 $655,000 $750,000 $1,500,000 0.0% -2.7% $716,250 $623,000 $667,500 7.1% 35 24 $450 60

Stirling West 983 $637,500 $775,000 $966,500 $6,125,000 -0.6% -4.6% $777,500 $780,000 $761,000 -2.4% 268 180 $480 59Carine 71 $662,500 $785,000 $850,000 $1,200,000 1.0% 0.6% $827,500 $792,500 $850,000 7.3% 16 16 $400 72

Churchlands 35 $1,185,000 $1,370,000 $1,495,000 $1,980,000 -0.9% 3.8% $1,485,000 $1,300,000 $1,482,500 14.0% 9 4 $750 39Doubleview 139 $587,000 $717,000 $810,000 $2,300,000 -0.4% -6.9% $740,000 $745,000 $705,000 -5.4% 43 31 $473 52

Gwelup 53 $755,000 $835,000 $955,000 $1,500,000 0.0% -2.7% $830,000 $815,000 $775,000 -4.9% 14 6 $675 69Innaloo 146 $515,000 $569,500 $660,000 $968,000 -3.5% -7.4% $605,000 $634,000 $553,500 -12.7% 39 30 $450 62

Karrinyup 139 $700,000 $815,000 $957,500 $1,800,000 -1.2% -3.3% $842,500 $780,000 $745,000 -4.5% 31 32 $493 75North Beach 42 $801,000 $860,000 $1,200,000 $6,125,000 -1.7% -5.6% $955,000 $930,000 $1,035,000 11.3% 14 7 $623 62

Scarborough 161 $646,250 $747,000 $834,250 $1,927,000 -1.1% -5.1% $785,000 $750,000 $725,000 -3.3% 50 23 $490 57Trigg 39 $935,000 $1,135,000 $1,300,000 $4,575,000 0.0% 12.9% $925,000 $1,201,000 $975,000 -18.8% 7 7 $400 73

Watermans Bay 22 $885,000 $1,187,500 $1,300,000 $2,400,000 -7.0% -7.6% $1,730,000 $1,165,000 $670,000 -42.5% 8 3 $475 15Wembley Downs 90 $720,000 $1,042,000 $1,210,000 $1,800,000 0.0% 2.2% $1,050,000 $1,060,000 $1,090,000 2.8% 22 14 $460 46

Woodlands 46 $670,000 $875,000 $1,140,000 $2,100,000 2.9% -6.4% $882,000 $900,000 $950,000 5.6% 15 7 $480 36

Vincent/Stirling SE 430 $740,000 $860,000 $1,081,000 $3,000,000 -1.9% -5.8% $878,750 $882,000 $795,000 -9.9% 131 69 $475 59Coolbinia 22 $715,000 $855,000 $1,185,000 $2,250,000 -0.8% -19.0% $864,000 $823,500 $802,500 -2.6% 10 3 $375 257Highgate 19 $722,500 $810,000 $1,001,250 $1,304,250 -6.5% -9.7% $665,000 $862,500 $767,500 -11.0% 6 4 $480 83

Inglewood 79 $672,500 $785,000 $905,000 $1,750,000 1.9% -2.8% $770,000 $814,125 $810,000 -0.5% 24 11 $445 73Leederville 34 $740,000 $850,000 $1,045,000 $2,250,000 0.0% -5.3% $1,005,000 $920,000 $687,000 -25.3% 11 3 $490 47

Menora 19 $816,000 $1,130,000 $1,600,000 $2,000,000 -1.7% 6.6% $1,000,000 $822,000 -17.8% 7 1 $498 24Mount Hawthorn 95 $776,250 $880,000 $1,057,663 $1,570,000 0.5% 2.2% $760,000 $925,000 $800,000 -13.5% 30 12 $490 42

Mount Lawley 77 $805,000 $975,000 $1,325,000 $3,000,000 -3.5% -7.1% $983,750 $917,500 $912,500 -0.5% 26 14 $530 58North Perth 85 $718,750 $820,000 $997,500 $2,500,000 -6.6% -8.9% $855,000 $766,000 $740,000 -3.4% 17 21 $450 53

Western Suburbs 1,112 $1,050,000 $1,362,500 $1,800,000 $14,130,000 -2.0% -2.7% $1,400,000 $1,385,000 $1,275,000 -7.9% 333 172 $700 62City Beach 84 $1,435,500 $1,672,500 $2,037,500 $3,600,000 -2.3% -7.9% $1,900,000 $1,930,000 $1,480,000 -23.3% 25 9 $950 107Claremont 89 $1,042,500 $1,250,000 $1,540,000 $7,500,000 -5.7% -13.3% $1,625,000 $1,217,500 $1,200,000 -1.4% 28 19 $675 40Cottesloe 101 $1,400,000 $1,700,000 $2,540,000 $5,010,000 0.0% -8.1% $1,830,000 $1,565,000 $1,800,000 15.0% 30 15 $750 78

Daglish 10 $865,000 $1,057,500 $1,200,000 $1,475,000 4.7% 3.7% $895,000 $865,000 $1,100,000 27.2% 3 3 $445 58Dalkeith 62 $1,800,000 $2,175,000 $3,300,000 $14,130,000 -7.4% -9.8% $2,400,000 $2,437,500 $1,850,000 -24.1% 24 8 $795 43Floreat 108 $1,000,000 $1,204,200 $1,445,000 $2,800,000 -0.4% -8.1% $1,200,000 $1,290,000 $1,135,000 -12.0% 25 19 $720 37

Jolimont 9 $939,250 $1,125,000 $1,225,000 $1,550,000 9.8% 11.9% $995,000 $1,045,500 -100.0% 4 $695Mosman Park 105 $1,000,000 $1,280,000 $2,025,000 $6,750,000 -1.5% -7.6% $1,311,500 $1,280,000 $1,270,000 -0.8% 33 17 $850 92

Mount Claremont 67 $1,049,000 $1,300,000 $1,495,000 $3,100,000 -1.1% -5.6% $1,400,000 $1,315,000 $1,287,500 -2.1% 24 14 $750 51Nedlands 125 $1,175,000 $1,500,000 $1,850,000 $4,150,000 0.0% -3.2% $1,490,000 $1,505,000 $1,181,000 -21.5% 38 20 $713 48

Peppermint Grove 15 $2,375,000 $2,850,000 $4,050,000 $7,700,000 -10.9% -18.6% $4,200,000 $3,200,000 $3,300,000 3.1% 2 4 $775 102Shenton Park 47 $1,037,500 $1,200,000 $1,430,000 $2,820,000 -1.6% 2.1% $1,247,500 $1,260,000 $1,198,750 -4.9% 9 8 $650 22

Subiaco 63 $955,000 $1,270,000 $1,500,000 $2,200,000 -1.7% 1.8% $1,220,000 $1,215,000 $1,000,000 -17.7% 19 9 $745 58Swanbourne 54 $1,335,000 $1,710,000 $2,120,000 $5,250,000 0.6% 14.8% $1,925,000 $1,720,000 $1,855,000 7.8% 17 6 $975 79

Wembley 115 $827,500 $970,000 $1,265,000 $1,960,000 -2.5% -9.1% $1,060,000 $1,070,000 $910,000 -15.0% 32 14 $575 62West Leederville 56 $927,500 $1,117,500 $1,347,500 $2,600,000 0.0% -2.4% $1,100,000 $1,110,000 $1,015,000 -8.6% 19 7 $600 43

Perth Metro Region 21,729 $427,000 $530,000 $710,000 $14,130,000 -0.9% -3.6% $532,000 $532,000 $510,000 -4.1% 5,901 3,989 $380 68

SAMPLE

CE

NT

RA

L S

UB

-RE

GIO

N

12 MARKET UPDATE | SEPTEMBER QUARTER 2016

Central Sub-Region PERTH REGIONP

ER

TH

RE

GIO

N

Multi-Residential Market

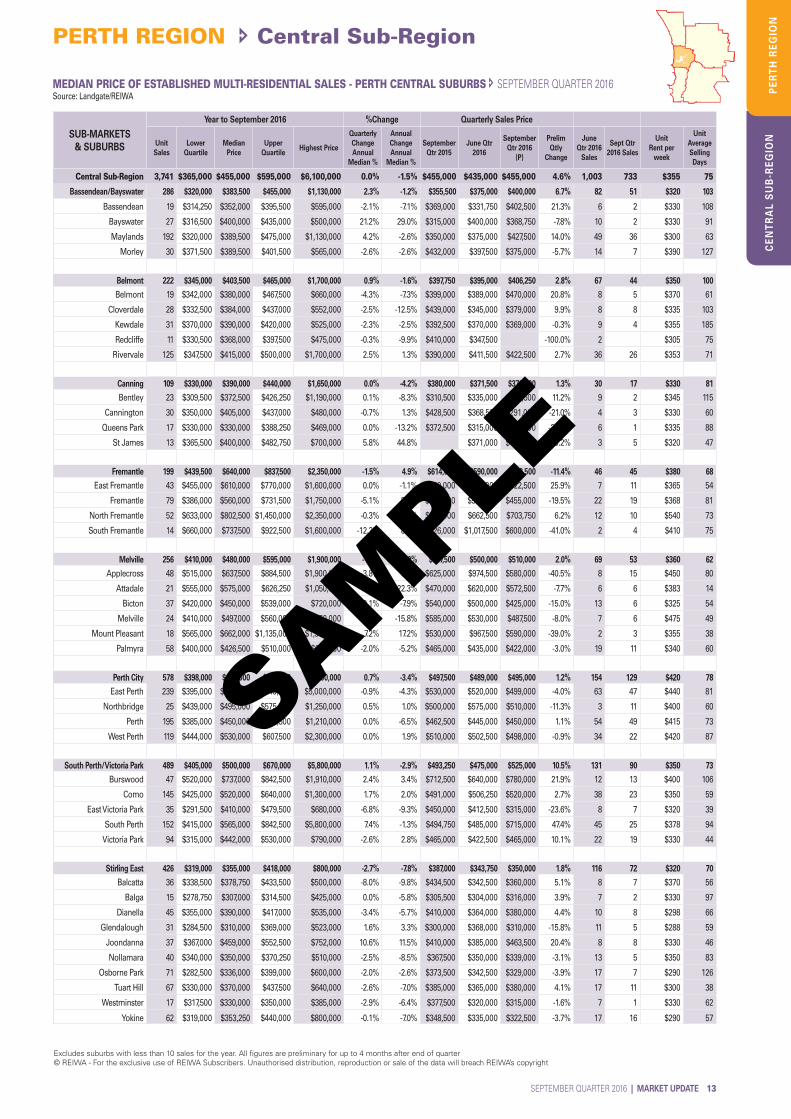

In the September quarter, preliminary sales volumes have decreased by similar levels to the preliminary June quarter results, recording a 27 per cent drop in the Central sub-region. A decline in preliminary sales activity has been observed across all sub-markets in the Central sub-region. There are a few suburbs in the Central sub-region which actually recorded an increase in sales activity, these suburbs include: East Fremantle (up 57 per cent), Applecross (up 88 per cent) and Mount Pleasant (up 50 per cent).

For the September quarter, the preliminary quarterly change in the median price was up 4.6 per cent to $455,000 after a revised June quarter quarterly median of $435,000. At a sub-market level, South Perth/Victoria Park was up 10.5 per cent and the Western Suburbs was up 11.3 per cent for the quarter.

The picture looks different though for the Central sub-region’s multi-residential market when considering changes in annual medians. There appears to be a bit more stability in the sub-markets in terms of changes in annual medians with positive growth recorded in the Fremantle sub-market at 4.9 per cent, Vincent/Stirling SE at 1.1 per cent and Western Suburbs at 6.0 per cent. The remaining sub-markets had negative growth. The overall performance of the Central sub-region in the annual change in annual median was -1.5 per cent.

Top performers with more than 30 sales for the quarterly change in the annual median for the September quarter include: Joondanna up 10.6 per cent at $459,000, South Perth up 7.4 per cent at 565,000 and Maylands up 4.2 per cent at $389,500.

TOP 10 SUBURBS BY QUARTERLY CHANGE IN PRICE Source: Landgate/REIWA

CENTRAL

Year to September 2016 Quarterly Change

in Annual Median %

Unit Sales Median Price Highest Price

Joondanna 37 $459,000 $752,000 10.6%

South Perth 152 $565,000 $5,800,000 7.4%

Maylands 192 $389,500 $1,130,000 4.2%

Rivervale 125 $415,000 $1,700,000 2.5%

Burswood 47 $737,000 $1,910,000 2.4%

Como 145 $520,000 $1,300,000 1.7%

Glendalough 31 $310,000 $523,000 1.6%

East Fremantle 43 $610,000 $1,600,000 0.0%

Perth 195 $450,000 $1,210,000 0.0%

West Perth 119 $530,000 $2,300,000 0.0%

Highgate 38 $415,000 $625,000 0.0%

Mount Lawley 93 $410,000 $881,020 0.0%

Excludes suburbs with less than 30 sales for the year & dwellings on lots greater than 1 Ha.

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

02004006008001,0001,2001,4001,6001,8002,000

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

MULTI-RES SALES - CENTRAL

MULTI-RES MEDIAN - CENTRAL

PMR MULTI-RES MEDIAN

PERTH CENTRAL SUB-REGION Source: Landgate/REIWA

10 Year Ave

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

01002003004005006007008009001,000

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

MULTI-RES SALES - MIDDLE

MULTI-RES MEDIAN - MIDDLE

PMR MULTI-RES MEDIAN

PERTH MIDDLE SUB-REGION Source: Landgate/REIWA

10 Year Ave

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

$600,000

0

200

400

600

800

1,000

1,200

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

MULTI-RES SALES - INNER

MULTI-RES MEDIAN - INNER

PMR MULTI-RES MEDIAN

PERTH INNER SUB-REGION Source: Landgate/REIWA

Listings for the multi-residential market in the Central sub-region lifted in the September quarter to total 2,337, up 2.6 per cent. The stock of unit listings in the Perth Metro Region increased by 1.4 per cent to 3,087 for the quarter.

Average selling days improved for the unit market in the Central sub-region. It now takes 75 days to sell which is an improvement of two days over the quarter.

SAMPLE

SEPTEMBER QUARTER 2016 | MARKET UPDATE 13

PERTH REGION Central Sub-Region

CE

NT

RA

L S

UB

-RE

GIO

NP

ER

TH

RE

GIO

N

MEDIAN PRICE OF ESTABLISHED MULTI-RESIDENTIAL SALES - PERTH CENTRAL SUBURBS SEPTEMBER QUARTER 2016Source: Landgate/REIWA

SUB-MARKETS& SUBURBS

Year to September 2016 %Change Quarterly Sales Price

Unit Sales

Lower Quartile

Median Price

Upper Quartile

Highest Price

Quarterly Change Annual

Median %

Annual Change Annual

Median %

September Qtr 2015

June Qtr 2016

September Qtr 2016

(P)

Prelim Qtly

Change

June Qtr 2016

Sales

Sept Qtr 2016 Sales

Unit Rent per

week

Unit Average Selling Days

Central Sub-Region 3,741 $365,000 $455,000 $595,000 $6,100,000 0.0% -1.5% $455,000 $435,000 $455,000 4.6% 1,003 733 $355 75

Bassendean/Bayswater 286 $320,000 $383,500 $455,000 $1,130,000 2.3% -1.2% $355,500 $375,000 $400,000 6.7% 82 51 $320 103

Bassendean 19 $314,250 $352,000 $395,500 $595,000 -2.1% -7.1% $369,000 $331,750 $402,500 21.3% 6 2 $330 108

Bayswater 27 $316,500 $400,000 $435,000 $500,000 21.2% 29.0% $315,000 $400,000 $368,750 -7.8% 10 2 $330 91

Maylands 192 $320,000 $389,500 $475,000 $1,130,000 4.2% -2.6% $350,000 $375,000 $427,500 14.0% 49 36 $300 63

Morley 30 $371,500 $389,500 $401,500 $565,000 -2.6% -2.6% $432,000 $397,500 $375,000 -5.7% 14 7 $390 127

Belmont 222 $345,000 $403,500 $465,000 $1,700,000 0.9% -1.6% $397,750 $395,000 $406,250 2.8% 67 44 $350 100

Belmont 19 $342,000 $380,000 $467,500 $660,000 -4.3% -7.3% $399,000 $389,000 $470,000 20.8% 8 5 $370 61

Cloverdale 28 $332,500 $384,000 $437,000 $552,000 -2.5% -12.5% $439,000 $345,000 $379,000 9.9% 8 8 $335 103

Kewdale 31 $370,000 $390,000 $420,000 $525,000 -2.3% -2.5% $392,500 $370,000 $369,000 -0.3% 9 4 $355 185

Redcliffe 11 $330,500 $368,000 $397,500 $475,000 -0.3% -9.9% $410,000 $347,500 -100.0% 2 $305 75

Rivervale 125 $347,500 $415,000 $500,000 $1,700,000 2.5% 1.3% $390,000 $411,500 $422,500 2.7% 36 26 $353 71

Canning 109 $330,000 $390,000 $440,000 $1,650,000 0.0% -4.2% $380,000 $371,500 $376,500 1.3% 30 17 $330 81

Bentley 23 $309,500 $372,500 $426,250 $1,190,000 0.1% -8.3% $310,500 $335,000 $372,500 11.2% 9 2 $345 115

Cannington 30 $350,000 $405,000 $437,000 $480,000 -0.7% 1.3% $428,500 $368,500 $291,000 -21.0% 4 3 $330 60

Queens Park 17 $330,000 $330,000 $388,250 $469,000 0.0% -13.2% $372,500 $315,000 $240,000 -23.8% 6 1 $335 88

St James 13 $365,500 $400,000 $482,750 $700,000 5.8% 44.8% $371,000 $405,000 9.2% 3 5 $320 47

Fremantle 199 $439,500 $640,000 $837,500 $2,350,000 -1.5% 4.9% $614,000 $590,000 $522,500 -11.4% 46 45 $380 68

East Fremantle 43 $455,000 $610,000 $770,000 $1,600,000 0.0% -1.1% $560,000 $415,000 $522,500 25.9% 7 11 $365 54

Fremantle 79 $386,000 $560,000 $731,500 $1,750,000 -5.1% 5.3% $563,000 $565,000 $455,000 -19.5% 22 19 $368 81

North Fremantle 52 $633,000 $802,500 $1,450,000 $2,350,000 -0.3% -1.5% $805,000 $662,500 $703,750 6.2% 12 10 $540 73

South Fremantle 14 $660,000 $737,500 $922,500 $1,600,000 -12.3% 8.5% $926,000 $1,017,500 $600,000 -41.0% 2 4 $410 75

Melville 256 $410,000 $480,000 $595,000 $1,900,000 -1.8% -1.0% $517,500 $500,000 $510,000 2.0% 69 53 $360 62

Applecross 48 $515,000 $637,500 $884,500 $1,900,000 -3.8% 6.7% $625,000 $974,500 $580,000 -40.5% 8 15 $450 80

Attadale 21 $555,000 $575,000 $626,250 $1,050,000 1.3% 22.3% $470,000 $620,000 $572,500 -7.7% 6 6 $383 14

Bicton 37 $420,000 $450,000 $539,000 $720,000 -9.1% -7.9% $540,000 $500,000 $425,000 -15.0% 13 6 $325 54

Melville 24 $410,000 $497,000 $560,000 $750,000 -4.2% -15.8% $585,000 $530,000 $487,500 -8.0% 7 6 $475 49

Mount Pleasant 18 $565,000 $662,000 $1,135,000 $1,500,000 7.2% 17.2% $530,000 $967,500 $590,000 -39.0% 2 3 $355 38

Palmyra 58 $400,000 $426,500 $510,000 $640,000 -2.0% -5.2% $465,000 $435,000 $422,000 -3.0% 19 11 $340 60

Perth City 578 $398,000 $495,000 $620,000 $5,000,000 0.7% -3.4% $497,500 $489,000 $495,000 1.2% 154 129 $420 78

East Perth 239 $395,000 $515,000 $740,000 $5,000,000 -0.9% -4.3% $530,000 $520,000 $499,000 -4.0% 63 47 $440 81

Northbridge 25 $439,000 $495,000 $575,000 $1,250,000 0.5% 1.0% $500,000 $575,000 $510,000 -11.3% 3 11 $400 60

Perth 195 $385,000 $450,000 $557,500 $1,210,000 0.0% -6.5% $462,500 $445,000 $450,000 1.1% 54 49 $415 73

West Perth 119 $444,000 $530,000 $607,500 $2,300,000 0.0% 1.9% $510,000 $502,500 $498,000 -0.9% 34 22 $420 87

South Perth/Victoria Park 489 $405,000 $500,000 $670,000 $5,800,000 1.1% -2.9% $493,250 $475,000 $525,000 10.5% 131 90 $350 73

Burswood 47 $520,000 $737,000 $842,500 $1,910,000 2.4% 3.4% $712,500 $640,000 $780,000 21.9% 12 13 $400 106

Como 145 $425,000 $520,000 $640,000 $1,300,000 1.7% 2.0% $491,000 $506,250 $520,000 2.7% 38 23 $350 59

East Victoria Park 35 $291,500 $410,000 $479,500 $680,000 -6.8% -9.3% $450,000 $412,500 $315,000 -23.6% 8 7 $320 39

South Perth 152 $415,000 $565,000 $842,500 $5,800,000 7.4% -1.3% $494,750 $485,000 $715,000 47.4% 45 25 $378 94

Victoria Park 94 $315,000 $442,000 $530,000 $790,000 -2.6% 2.8% $465,000 $422,500 $465,000 10.1% 22 19 $330 44

Stirling East 426 $319,000 $355,000 $418,000 $800,000 -2.7% -7.8% $387,000 $343,750 $350,000 1.8% 116 72 $320 70

Balcatta 36 $338,500 $378,750 $433,500 $500,000 -8.0% -9.8% $434,500 $342,500 $360,000 5.1% 8 7 $370 56

Balga 15 $278,750 $307,000 $314,500 $425,000 0.0% -5.8% $305,500 $304,000 $316,000 3.9% 7 2 $330 97

Dianella 45 $355,000 $390,000 $417,000 $535,000 -3.4% -5.7% $410,000 $364,000 $380,000 4.4% 10 8 $298 66

Glendalough 31 $284,500 $310,000 $369,000 $523,000 1.6% 3.3% $300,000 $368,000 $310,000 -15.8% 11 5 $288 59

Joondanna 37 $367,000 $459,000 $552,500 $752,000 10.6% 11.5% $410,000 $385,000 $463,500 20.4% 8 8 $330 46

Nollamara 40 $340,000 $350,000 $370,250 $510,000 -2.5% -8.5% $367,500 $350,000 $339,000 -3.1% 13 5 $350 83

Osborne Park 71 $282,500 $336,000 $399,000 $600,000 -2.0% -2.6% $373,500 $342,500 $329,000 -3.9% 17 7 $290 126

Tuart Hill 67 $330,000 $370,000 $437,500 $640,000 -2.6% -7.0% $385,000 $365,000 $380,000 4.1% 17 11 $300 38

Westminster 17 $317,500 $330,000 $350,000 $385,000 -2.9% -6.4% $377,500 $320,000 $315,000 -1.6% 7 1 $330 62

Yokine 62 $319,000 $353,250 $440,000 $800,000 -0.1% -7.0% $348,500 $335,000 $322,500 -3.7% 17 16 $290 57

Excludes suburbs with less than 10 sales for the year. All figures are preliminary for up to 4 months after end of quarter© REIWA - For the exclusive use of REIWA Subscribers. Unauthorised distribution, reproduction or sale of the data will breach REIWA’s copyright

SAMPLE

CE

NT

RA

L S

UB

-RE

GIO

N

14 MARKET UPDATE | SEPTEMBER QUARTER 2016

Central Sub-Region PERTH REGIONP

ER

TH

RE

GIO

N

SUB-MARKETS& SUBURBS

Year to September 2016 %Change Quarterly Sales Price

Unit Sales

Lower Quartile

Median Price

Upper Quartile

Highest Price

Quarterly Change Annual

Median %

Annual Change Annual

Median %

September Qtr 2015

June Qtr 2016

September Qtr 2016

(P)

Prelim Qtly

Change

June Qtr 2016

Sales

Sept Qtr 2016 Sales

Unit Rent per

week

Unit Average Selling Days

Stirling West 325 $410,000 $480,000 $585,000 $3,500,000 -2.0% -5.7% $490,000 $489,500 $445,500 -9.0% 96 64 $395 68

Churchlands 21 $377,500 $390,000 $426,000 $1,035,001 -1.3% -8.8% $360,000 $375,000 $385,000 2.7% 3 6 $325 42

Doubleview 23 $352,500 $510,000 $590,750 $649,000 -4.2% -1.9% $502,500 $550,000 $373,000 -32.2% 9 4 $460 99

Innaloo 51 $449,000 $479,000 $511,000 $600,000 -2.0% -4.2% $490,000 $475,000 $440,000 -7.4% 15 15 $425 65

Scarborough 185 $401,500 $490,000 $634,500 $3,500,000 -2.0% -6.7% $500,000 $470,000 $515,000 9.6% 53 32 $380 57

Trigg 11 $467,500 $491,500 $740,000 $781,000 0.0% 5.0% $610,750 $612,500 0.3% 2 2 $435 55

Vincent/Stirling SE 262 $389,000 $455,000 $569,000 $3,550,000 -1.1% 1.1% $445,000 $435,000 $425,000 -2.3% 63 54 $350 64

Highgate 38 $325,000 $415,000 $545,000 $625,000 0.0% -7.6% $455,000 $330,000 $417,500 26.5% 8 10 $385 48

Inglewood 22 $359,000 $442,500 $618,000 $3,550,000 -7.8% 11.0% $407,500 $564,000 $406,000 -28.0% 4 5 $343 68

Leederville 35 $436,000 $513,000 $680,000 $1,250,000 -1.3% -10.0% $545,000 $462,500 $500,000 8.1% 11 9 $395 48

Mount Hawthorn 18 $499,000 $537,000 $572,000 $770,000 -0.9% -1.5% $580,000 $514,500 $539,000 4.8% 4 3 $425 90

Mount Lawley 93 $360,000 $410,000 $502,500 $881,020 0.0% -2.4% $406,200 $392,500 $397,000 1.1% 20 14 $300 57

North Perth 50 $400,000 $480,000 $580,000 $915,000 -1.0% -4.7% $465,000 $435,000 $462,000 6.2% 15 11 $385 88

Western Suburbs 589 $398,750 $580,000 $795,000 $6,100,000 1.8% 6.0% $560,000 $539,000 $600,000 11.3% 149 114 $350 77

Claremont 81 $505,000 $650,000 $840,000 $1,820,000 -2.6% -4.1% $735,000 $620,000 $530,000 -14.5% 18 13 $445 99

Cottesloe 49 $585,000 $785,000 $972,500 $3,570,000 -1.6% -3.2% $928,000 $736,000 $730,000 -0.8% 8 3 $450 107

Crawley 52 $442,500 $792,500 $1,175,000 $4,800,000 -7.3% -0.3% $1,100,000 $787,500 $800,000 1.6% 18 11 $370 40

Daglish 11 $424,000 $622,000 $675,000 $1,351,777 -0.2% 46.4% $557,500 $622,000 $423,000 -32.0% 3 3 $223 55

Floreat 16 $725,000 $978,750 $1,062,500 $1,150,000 -2.1% -12.8% $1,250,000 $690,000 $966,250 40.0% 5 4 $650 122

Jolimont 22 $312,000 $378,000 $535,000 $2,500,000 -1.2% -12.6% $350,000 $375,000 $375,250 0.1% 6 5 $290 67

Mosman Park 29 $312,500 $380,000 $482,000 $1,230,000 1.0% -8.4% $370,000 $382,500 $367,500 -3.9% 10 2 $290 105

Nedlands 23 $475,000 $575,000 $743,000 $2,275,000 1.4% -7.3% $565,000 $572,500 $450,500 -21.3% 6 5 $350 101

Shenton Park 19 $460,000 $535,000 $750,017 $1,300,000 0.0% 24.4% $535,000 $800,000 $300,000 -62.5% 5 1 $390 91

Subiaco 135 $494,000 $600,000 $737,500 $6,100,000 -1.6% -6.3% $654,000 $505,000 $600,000 18.8% 25 31 $418 73

Swanbourne 14 $535,000 $657,500 $930,000 $1,810,000 44.2% -48.2% $456,000 $657,500 14 $800

Wembley 87 $271,000 $320,000 $480,000 $900,000 -1.5% -4.5% $335,000 $315,000 $327,500 4.0% 27 12 $250 64

West Leederville 26 $265,000 $425,000 $635,000 $1,400,000 -5.6% -18.7% $568,500 $425,000 $630,000 48.2% 8 6 $330 44

Perth Metro Region 4,570 $345,000 $425,000 $565,000 $6,100,000 -0.7% -3.2% $430,000 $410,000 $425,000 3.7% 1,203 881 $350 80

Excludes suburbs with less than 10 sales for the year. All figures are preliminary for up to 4 months after end of quarter© REIWA - For the exclusive use of REIWA Subscribers. Unauthorised distribution, reproduction or sale of the data will breach REIWA’s copyright

MEDIAN PRICE OF ESTABLISHED MULTI-RESIDENTIAL SALES - PERTH CENTRAL SUBURBS SEPTEMBER QUARTER 2016Source: Landgate/REIWA

Land MarketThe land market in the Central sub-region is very mixed. Preliminary data for median price in the September quarter indicates an increase of nine per cent to $500,000 from $458,750 on the revised June quarter. Preliminary land sales for the September quarter are currently 146. The June quarter preliminary volumes have increased over the quarter to a revised figure of 272 from the initial 160. So, it is expected a further lift in land sales will occur in coming months. Most of the land sales in the Central sub-region can be found in the sub-markets of Bayswater/Bassendean, Western Suburbs and Stirling East.

In the year to September 2016 the annual change in annual medians is still mixed. The Central sub-region recorded zero growth, with better performers found in Fremantle (up 1.3 per cent), Stirling East (up 6.3 per cent) and Stirling West (up 1.6 per cent).

It is important to note that land sales can take up to 12 months to settle and that the most recent figures provided for the September 2016 quarter will adjust in the future.

TOP 5 SUBURBS BY VOLUMESource: Landgate/REIWA

Year to September 2016 Land Sales Median PriceQuarterly Change in Annual Median

%

Perth Metro Region 5,835 $265,000 1.9%

Central Sub-Region 928 $460,000 1.5%Bayswater 59 $335,000 -2.2%

Dianella 47 $480,000 3.2%

Mount Claremont 44 $685,000 1.9%

East Cannington 39 $322,000 -0.3%

Morley 38 $300,000 -2.3%

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

$550,000

0

100

200

300

400

500

600

700

800

900

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

LAND SALES - CENTRALLAND MEDIAN - CENTRALPMR LAND MEDIAN

PERTH CENTRAL SUB-REGION Source: Landgate/REIWASAMPLE

SEPTEMBER QUARTER 2016 | MARKET UPDATE 15

PERTH REGION Central Sub-Region

CE

NT

RA

L S

UB

-RE

GIO

NP

ER

TH

RE

GIO

N

SUB-MARKETS& SUBURBS

Year to Sep 2016 Year to Sep 2015 Quarterly Sales Price

Land Sales

Median Price

Land Sales

Median Price

Quarterly Change Annual

Median %

Annual Change Annual

Median %

Sept Qtr 2015 June Qtr 2016 Sept Qtr 2016 (P)

Prelim Qtly Change

June Qtr 2016 Sales

Sept Qtr 2016 Sales

Central Sub-Region 928 $460,000 1,085 $460,000 1.5% 0.0% $440,000 $458,750 $500,000 9.0% 272 146

Bassendean/Bayswater 168 $327,500 183 $337,000 -2.8% -2.8% $345,000 $340,000 $310,000 -8.8% 56 22

Bassendean 18 $351,250 24 $404,000 -15.4% -13.1% $527,500 $430,000 $350,000 -18.6% 5 3

Bayswater 59 $335,000 34 $385,500 -2.2% -13.1% $384,500 $340,000 $295,000 -13.2% 19 5

Bedford 10 $400,000 10 $396,000 -0.6% 1.0% $400,000 $405,000 $390,000 -3.7% 5 1

Embleton 15 $271,000 8 $323,500 -1.5% -16.2% $325,000 $271,000 $270,000 -0.4% 5 3

Morley 38 $300,000 52 $320,000 -2.3% -6.3% $317,500 $300,000 $275,000 -8.3% 12 5

Belmont 42 $322,000 60 $389,500 -6.7% -17.3% $369,500 $335,000 $335,000 0.0% 16 9

Cloverdale 15 $295,000 15 $335,000 0.0% -11.9% $282,500 $305,000 $288,000 -5.6% 6 3

Canning 98 $328,500 123 $335,000 -0.5% -1.9% $355,000 $322,500 $460,000 42.6% 28 12

East Cannington 39 $322,000 42 $335,000 -0.3% -3.9% $332,500 $322,500 $259,000 -19.7% 12 3

Fremantle 67 $395,000 79 $390,000 -1.3% 1.3% $553,500 $379,767 $404,000 6.4% 9 10

Beaconsfield 13 $385,000 41 $390,000 -12.0% -1.3% $616,000 $325,000 $320,000 -1.5% 2 1

Hilton 10 $325,000 13 $300,000 0.0% 8.3% $365,000 $305,000 $355,000 16.4% 3 1

White Gum Valley 24 $385,000 6 $418,500 -1.3% -8.0% $455,000 $394,000 4

Melville 104 $568,750 87 $590,000 -0.2% -3.6% $580,000 $511,000 $584,000 14.3% 30 15

Kardinya 11 $425,000 14 $380,000 8.3% 11.8% $352,500 $390,000 $745,000 91.0% 5 3

Melville 18 $515,000 15 $590,000 -8.0% -12.7% $580,000 $460,000 $510,000 10.9% 4 2

Mount Pleasant 10 $745,000 12 $715,000 0.0% 4.2% $648,000 $815,000 $590,000 -27.6% 3 1

Perth City 2 $800,000 2 $2,310,000 0.0% -65.4%

South Perth/Victoria Park 65 $550,000 116 $559,444 6.3% -1.7% $556,944 $495,000 $880,000 77.8% 24 8

Carlisle 14 $362,500 18 $377,750 -1.5% -4.0% $372,500 $365,000 $850,000 132.9% 5 1

Como 19 $625,000 16 $634,000 0.0% -1.4% $719,000 $637,500 $1,353,750 112.4% 8 2

Stirling East 133 $425,000 134 $400,000 0.0% 6.3% $395,000 $395,000 $330,000 -16.5% 28 23

Balga 11 $200,000 36 $235,000 -11.1% -14.9% $298,500 $200,000 $8,333 -95.8% 3 1

Dianella 47 $480,000 22 $427,605 3.2% 12.3% $416,538 $453,000 $517,500 14.2% 7 6

Stirling 21 $500,000 14 $589,500 -13.0% -15.2% $579,000 $526,500 $330,000 -37.3% 6 7

Westminster 11 $240,000 11 $240,000 11.6% 0.0% $197,500 $217,500 2

Yokine 14 $452,500 14 $502,500 1.7% -10.0% $480,000 $460,000 $460,000 0.0% 6 1

Stirling West 113 $523,000 165 $552,000 1.6% -5.3% $555,000 $471,000 $580,000 23.1% 26 25

Doubleview 24 $428,500 15 $445,000 0.8% -3.7% $400,000 $339,000 $620,000 82.9% 9 5

Gwelup 24 $550,000 45 $545,000 -0.4% 0.9% $570,000 $538,500 $580,000 7.7% 4 7

Karrinyup 19 $480,000 27 $521,000 9.1% -7.9% $435,000 $480,000 $775,000 61.5% 5 3

Scarborough 18 $407,500 21 $476,000 -1.8% -14.4% $456,500 $460,000 $419,500 -8.8% 3 4

Vincent/Stirling SE 27 $485,000 27 $525,000 -7.6% -7.6% $548,750 $530,000 $547,500 3.3% 9 4

North Perth 12 $452,500 6 $536,250 -5.7% -15.6% $658,250 $675,000 $445,000 -34.1% 3 1

Western Suburbs 109 $740,000 109 $740,000 -4.2% 0.0% $755,000 $715,000 $705,000 -1.4% 46 18

Cottesloe 18 $1,355,000 14 $1,402,925 -4.4% -3.4% $1,425,000 $5,185,000 $825,000 -84.1% 3 1

Mosman Park 15 $710,000 19 $750,000 0.0% -5.3% $870,000 $672,500 -100.0% 4

Mount Claremont 44 $685,000 2 $1,025,000 1.9% -33.2% $685,000 $697,500 1.8% 27 14

Perth Metro Region 5,835 $265,000 9,872 $263,000 1.9% 0.8% $260,500 $259,500 $295,000 13.7% 1,675 616

Excludes suburbs with less than 10 sales for the year. All figures are preliminary for up to 4 months after end of quarter© REIWA - For the exclusive use of REIWA Subscribers. Unauthorised distribution, reproduction or sale of the data will breach REIWA’s copyright

MEDIAN PRICE OF LAND SALES - PERTH CENTRAL SUBURBS SEPTEMBER QUARTER 2016Source: Landgate/REIWA

SAMPLE

NO

RT

H W

ES

T S

UB

-RE

GIO

N

16 MARKET UPDATE | SEPTEMBER QUARTER 2016

North West Sub-Region PERTH REGIONP

ER

TH

RE

GIO

N

TOP 5 SUBURBS BY VOLUMESource: Landgate/REIWA

Year to September 2016 Land Sales Median PriceQuarterly Change in Annual Median %

Perth Metro Region 5,835 $265,000 1.9%

North West Sub-Region 1,246 $258,000 -0.8%Alkimos 186 $229,000 -0.2%

Landsdale 133 $325,000 -1.5%

Yanchep 124 $208,500 -3.0%

Eglinton 105 $215,000 -1.8%

Clarkson 81 $261,000 0.0%

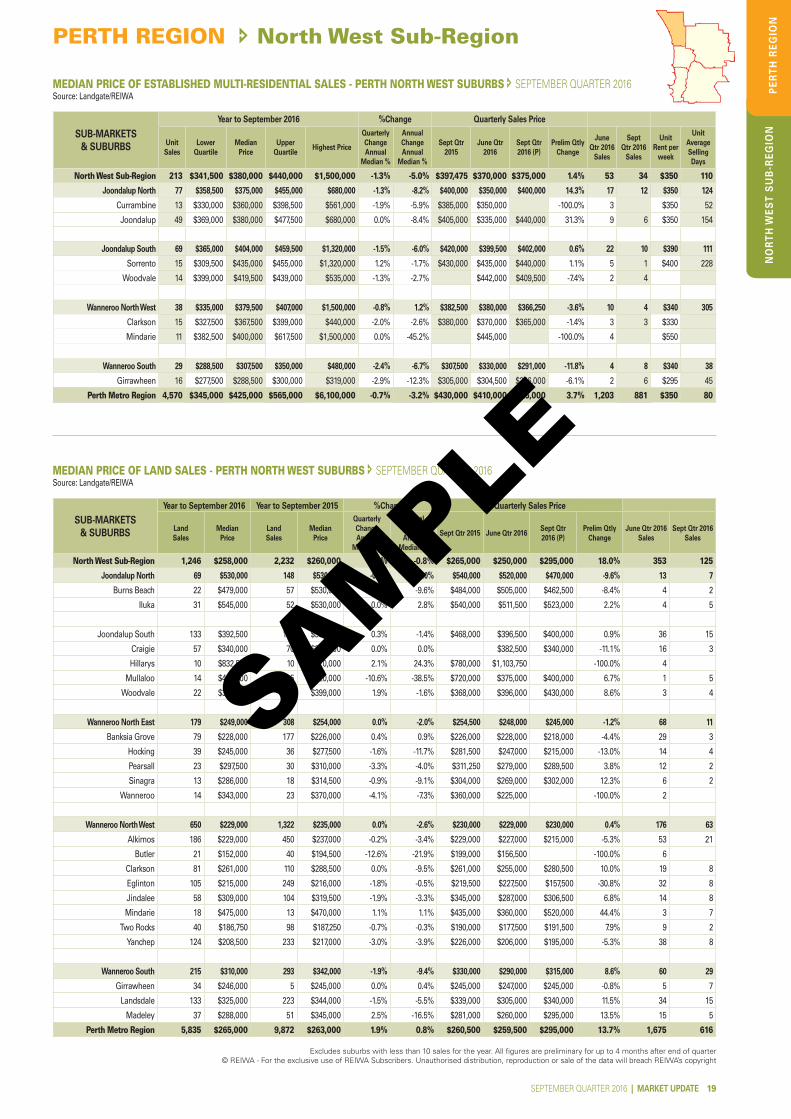

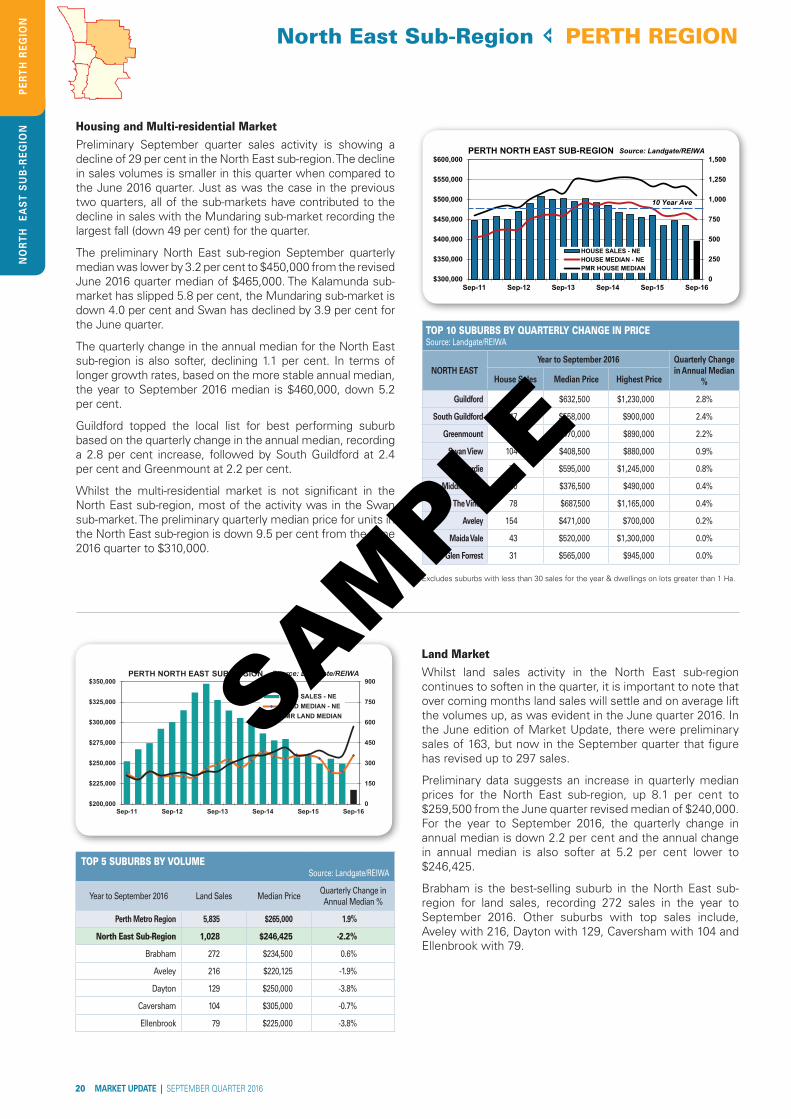

Land Market Whilst land sales activity in the North West sub-region continues to soften in the quarter, it is important to note that as more transactions settle in the coming months, volumes will lift. After revision, June quarter sales transactions more than doubled to reach 353 from a preliminary 163.

Preliminary data suggests an increase in quarterly median prices for the North West sub-region, up 18 per cent to $295,000 from the June quarter revised median of $250,000. For the year to September 2016, the quarterly change in annual median dropped slightly by 0.8 per cent with the annual change in annual median also slipping 0.8 per cent to $260,000.

Alkimos remains the bestselling suburb in the North West sub-region, recording 186 sales during the year to June 2016. Lansdale recorded 133 sales and Yanchep, Eglinton and Clarkson continue to feature in the top five.

$375,000

$400,000

$425,000

$450,000

$475,000

$500,000

$525,000

$550,000

$575,000

0

250

500

750

1,000

1,250

1,500

1,750

2,000

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

HOUSE SALES - NWHOUSE MEDIAN - NWPMR HOUSE MEDIAN

Source: Landgate/REIWAPERTH NORTH WEST SUB-REGION

10 Year Ave

$200,000

$225,000

$250,000

$275,000

$300,000

$325,000

$350,000

0

250

500

750

1,000

1,250

1,500

Sep-16Sep-15Sep-14Sep-13Sep-12Sep-11

LAND SALES - NWLAND MEDIAN - NWPMR LAND MEDIAN

PERTH NORTH WEST SUB-REGION Source: Landgate/REIWA

TOP 10 SUBURBS BY QUARTERLY CHANGE IN PRICE Source: Landgate/REIWA

NORTH WEST

Year to September 2016 Quarterly Change in

Annual Median %

House Sales

Median Price Highest Price

Warwick 47 $578,000 $865,000 3.2%Sinagra 37 $475,000 $575,000 2.3%Beldon 60 $502,000 $870,000 2.2%

Joondalup 85 $540,000 $1,180,000 1.9%Marmion 34 $931,000 $3,750,000 1.7%Kallaroo 67 $785,000 $2,195,000 1.6%

Burns Beach 41 $930,000 $1,500,000 0.8%Duncraig 200 $715,000 $1,680,000 0.7%

Marangaroo 100 $460,000 $735,000 0.4%Padbury 112 $529,750 $1,015,000 0.4%

Excludes suburbs with less than 30 sales for the year & dwellings on lots greater than 1 Ha.

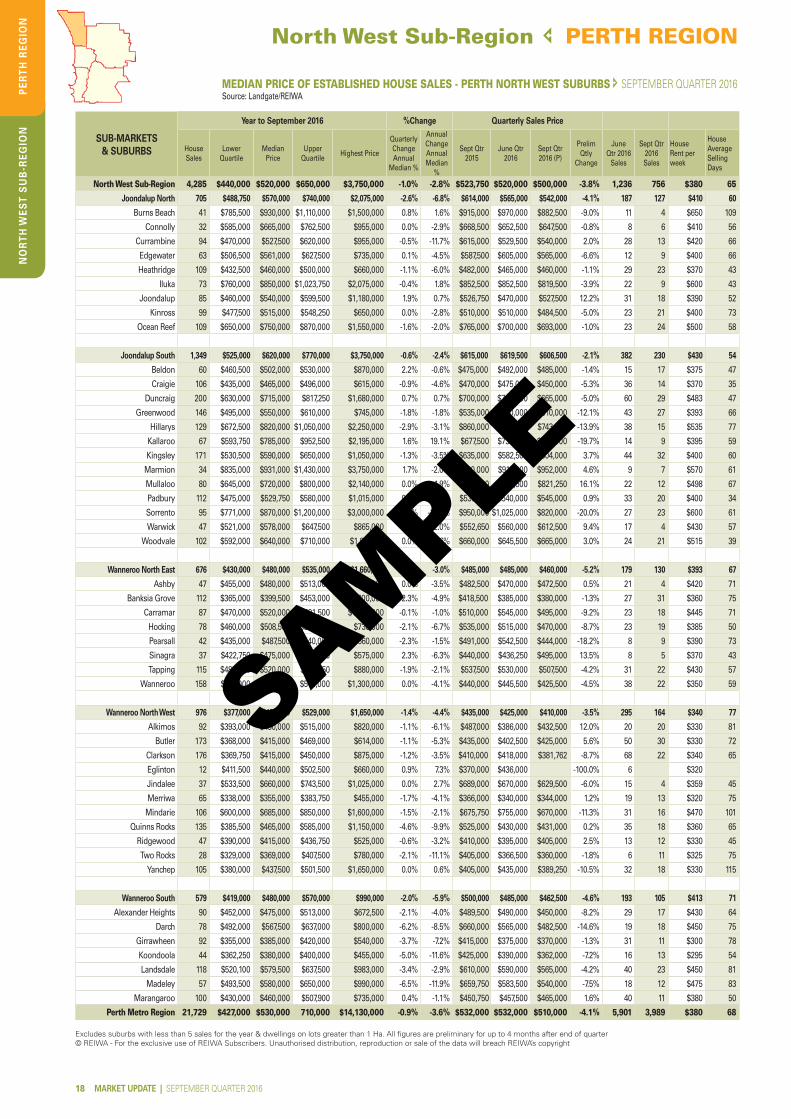

Housing and Multi-residential Markets

Preliminary Sales volumes for the housing market in the North West sub-region have continued their decline throughout the September quarter. Sub-markets that are experiencing the greatest decline in sales activity include Wanneroo South (down 46 per cent), Wanneroo North West (down 45 per cent) and Joondalup South (down 40 per cent).

The lower levels of sales transactions have also impacted the preliminary quarterly change in median price. The sub-region has recorded a drop of 3.8 per cent to $500,000 compared to a revised June quarter median of $520,000.

When considering the annual change in the annual median for the North West sub-region, the market is also experiencing some softening in price levels. The sub-region is down 2.8 per cent and all sub-markets have declined as well.

Turning to performance based on the quarterly change in the annual median, Warwick is on top with a lift of 3.2 per cent to $552,650, followed by Sinagra at 2.3 per cent with $440,000.

Multi-residential sales have followed a similar trend as the housing market, with preliminary sales for the September quarter falling by 36 per cent. The preliminary quarterly change in the median unit price is down marginally by one per cent to $375,000 compared to a revised June quarter median of $370,000. The best performing suburb in the North West sub-region for units is Joondalup with a quarterly change in annual median of 14 per cent.

SAMPLE

NO

RT

H W

ES

T S

UB

-RE

GIO

N

SEPTEMBER QUARTER 2016 | MARKET UPDATE 17

PERTH REGION North West Sub-Region

PE

RT

H R

EG

ION

SUB-MARKETS Listings at

September Quarter 2016

House ListingsQuarterly Change

Annual Change

Average Selling Days (p)

Quarterly Change

Annual Change

Joondalup North 291 223 -4.3% -7.9% 60 -4 -3Joondalup South 368 301 -4.7% -3.2% 54 3 2

Wanneroo North East 332 255 -15.8% -17.5% 67 0 5Wanneroo North West 888 674 0.0% -0.4% 77 0 1

Wanneroo South 321 231 -2.5% -6.5% 71 5 10

North West Sub-Region 2,200 1,684 -4.5% -5.7% 65 1 2Perth Metro Region 14,170 8,649 -0.6% -6.5% 68 3 5

Note: Listings to Dwelling Stock Ratio = Dwelling Listings as a percentage of estimated Dwelling Stock

SUBMARKETS

September Quarter 2016 June Quarter 2016 September Quarter 2015

Overall Market Variance

Listing vs Sold Price

Proportion of Vendors

Discounting

Listing & Sold Price Variance

for Discounting Vendors

Overall Market Variance

Listing vs Sold Price

Proportion of Vendors

Discounting

Listing & Sold Price Variance

for Discounting Vendors

Overall Market Variance

Listing vs Sold Price

Proportion of Vendors

Discounting

Listing & Sold Price Variance

for Discounting Vendors

North West Sub-Region -3.4% 50.7% -5.7% -3.0% 61.4% -5.8% -3.0% 50.3% -5.6%Joondalup North -3.6% 53.2% -6.1% -2.9% 49.7% -5.8% -2.5% 48.4% -5.6%Joondalup South -2.7% 39.2% -5.7% -3.8% 44.7% -5.2% -3.1% 48.8% -5.3%

Wanneroo North East -4.3% 58.9% -5.6% -2.8% 42.5% -7.5% -3.6% 50.0% -5.7%Wanneroo North West -3.0% 55.5% -5.3% -3.2% 59.8% -5.6% -3.1% 56.0% -6.4%

Wanneroo South -3.1% 53.2% -5.6% -3.0% 61.4% -5.8% -2.8% 46.7% -5.3%

Perth Metro Region -4.0% 51.8% -6.7% -3.1% 60.6% -5.9% -3.6% 52.7% -6.1%

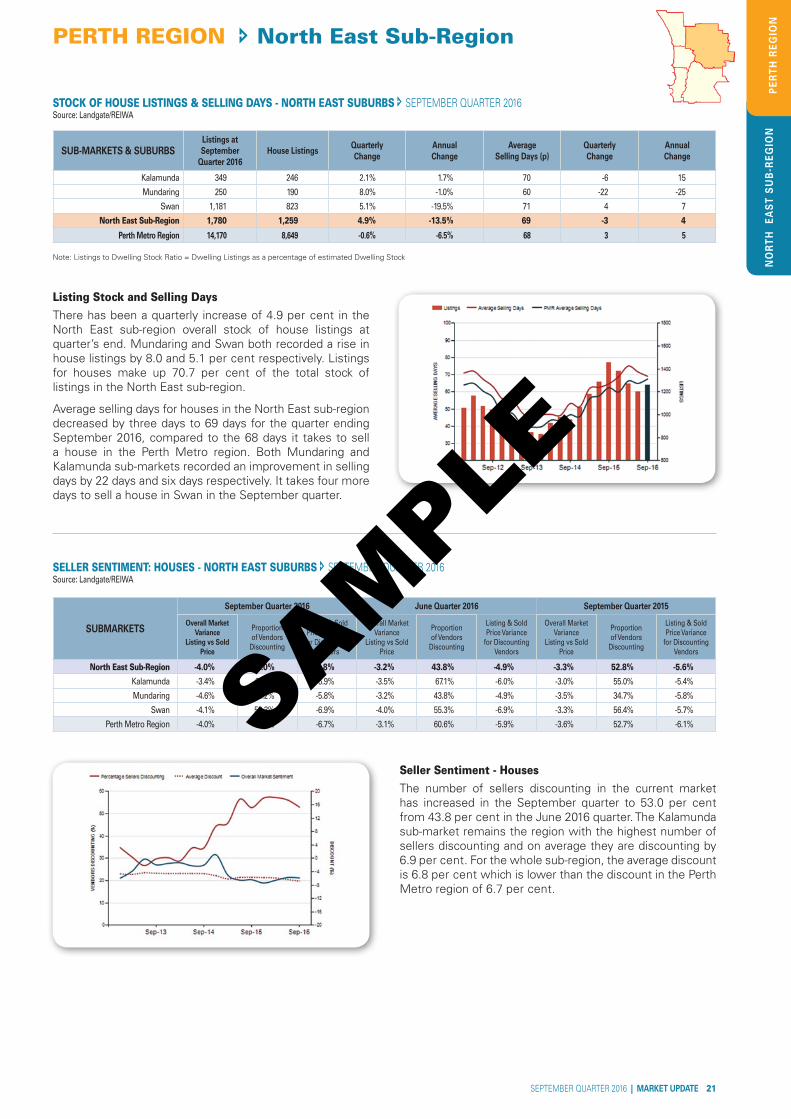

Listing Stock and Selling Days Total stock of house listings in the North West sub-region is down by 4.5 per cent for the quarter and 5.7 per cent lower than the same time last year.

All of the sub-markets except Wanneroo North West have shown a drop in the stock of listings for houses. The greatest decline in house listings was in Wanneroo North East down 15.8 per cent for the quarter.

In the North West sub-region, it is still taking more than 60 days to sell a house. The September quarter figure is 65 days for the sub-region and 77 days in the Wanneroo North West sub-market. Compared to the Perth Metro region, the sub-region is on slightly better against a 68 day average.

Seller Sentiment - HousesIn the North West sub-region, the number of sellers discounting their house has decreased to 50.7 per cent in the September quarter, from 61.4 per cent in the June quarter. The North West sub-region has fewer sellers discounting than the Perth Metro region as a whole.

It can be seen that the sub-market in the North West sub-region with the highest number of sellers discounting is Wanneroo North East, with 58.9 per cent of sellers discounting. The average discount that sellers are offering in the sub-region has remained stable at 5.7 per cent in September. The overall sentiment towards the housing market in the sub-region is still pessimistic at -3.4 per cent, however this is more positive than the general Perth metro market at -4.0 per cent.

SELLER SENTIMENT: HOUSES SEPTEMBER QUARTER 2016Source: Landgate/REIWA

STOCK OF HOUSE LISTINGS & SELLING DAYS - NORTH WEST SEPTEMBER QUARTER 2016Source: Landgate/REIWA

SAMPLE

NO

RT

H W

ES

T S

UB

-RE

GIO

N

18 MARKET UPDATE | SEPTEMBER QUARTER 2016

North West Sub-Region PERTH REGIONP

ER

TH

RE

GIO

N

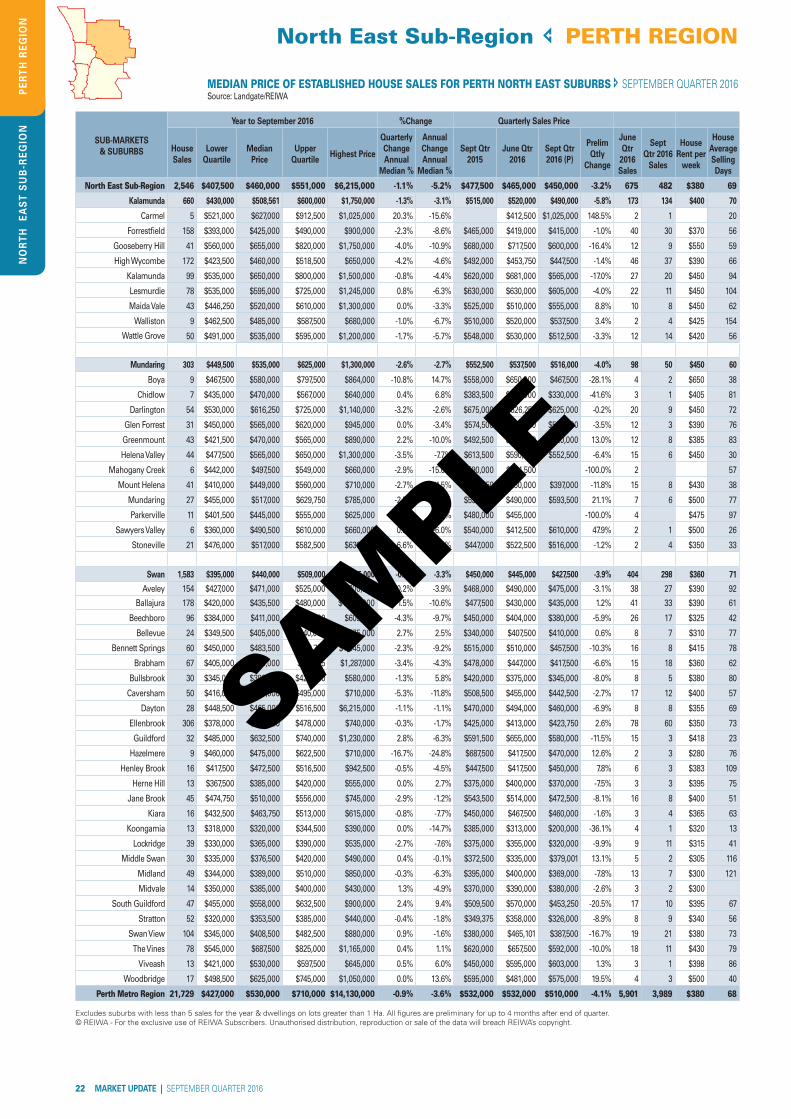

SUB-MARKETS& SUBURBS

Year to September 2016 %Change Quarterly Sales Price

House Sales

Lower Quartile

Median Price

Upper Quartile

Highest Price

Quarterly Change Annual

Median %

Annual Change Annual Median

%

Sept Qtr 2015

June Qtr 2016

Sept Qtr 2016 (P)

Prelim Qtly

Change

June Qtr 2016

Sales

Sept Qtr 2016 Sales

House Rent per week

House Average Selling Days

North West Sub-Region 4,285 $440,000 $520,000 $650,000 $3,750,000 -1.0% -2.8% $523,750 $520,000 $500,000 -3.8% 1,236 756 $380 65Joondalup North 705 $488,750 $570,000 $740,000 $2,075,000 -2.6% -6.8% $614,000 $565,000 $542,000 -4.1% 187 127 $410 60

Burns Beach 41 $785,500 $930,000 $1,110,000 $1,500,000 0.8% 1.6% $915,000 $970,000 $882,500 -9.0% 11 4 $650 109