september 2021 ‘21 summary summary summary summary

TRANSCRIPT

Field of Study: Accounting Employee stock purchase plans, often known as ESPPs, are programs that enable employees to purchase company stock via elective payroll deductions. Typically, those deductions will accrue over a set period of time, often six months. At the end of that period, the accumulated money is then used to buy stock and a new six-month period starts. ESPPs are a great incentive for employees, but how are they different from any other kind of equity compensation like options or restricted stock? David Outlaw, director of Valuation and HR Advisory Services at Equity Methods, provides us with details on the different types of ESPPs, reasons companies offer them, common structures and tax qualifications.

Field of Study: Accounting Special purpose acquisition companies, SPACs, also known as “blank check companies” raise money but are listed on an exchange before they even own any assets. Their goal is to acquire a privately held company within two years. These are both good enough reasons to be on the SEC’s radar. The SEC not only looks closely at filings and disclosures by SPACs in an effort to protect the public interest, but also, in April 2021, issued new guidance on the treatment of SPAC warrants with neither previously issued proposals nor a comment period. This was an uncharacteristic move that caught financial professionals by surprise. Zac McGinnis, managing director at Riveron Consulting and Josh Schaeffer, director at Equity Methods, provide a more in-depth discussion on SPACs and their execution.

Field of Study: Accounting Related party transactions seem to be a recurring issue, and the reason is primarily two-fold. One, there's been a significant amount of related party frauds that were discovered only after the fact. And two, there's been criticism of related party disclosures in that they don't provide an accurate view of the related party activity that took place within the reporting entity. Identifying related party relationships and related transactions is not as straightforward as one might think. John Fleming, CPA, discussion leader at Kaplan Financial Education, focuses on the importance of such transactions and their impact on the fair representation of financial statements.

Field of Study: Taxes Subsequent to the March 2020 emergency declaration issued by President Trump in response to the coronavirus pandemic, there have been several major disaster relief declarations. As the pandemic seems like it’s never ending, the IRS has to plan accordingly and extend most of its tax treatments with respect to COVID-19 and/or provide additional guidance where necessary. Barbara Weltman, president of Big Ideas for Small Business, gives us COVID-19 related IRS updates, discusses the tax treatment of recent tax cases, and explores ways tax professionals can boost their data security and better protect client information.

SEPT

. ‘2

1

sum

mar

y su

mm

ary

sum

mar

y su

mm

ary

1. Employee Stock Purchase Plans – Why Offer One?

2. Accounting & Valuation of SPACs

3. Related Party Transactions – A Recurring Issue

4. IRS Updates

CPA REPORT SUBSCRIBER GUIDE

SEPTEMBER 2021 Summary Page i [p. 1]

CPE Requirements iii [pp. 3–5]

Segment One 1–1 [pp. 7–39]

Segment Two 2–1 [pp. 41–70]

Segment Three 3–1 [pp. 71–101]

Segment Four 4–1 [pp. 103–133]

Sememt Five 5–1 [pp. 135–158]

Evaluation Form A–1 [pp. 159–160]

Index B–1 [pp. 161–164]

Group Live Attendance Form C–1 [p.165]

68]

CPA Report is a product of www.kaplanfinancial.com

Note: CPA Report now includes one Government/Not-for-Profit segment.

Information regarding COVID-19 changes rapidly; further updates will be in upcoming segments.

ii

gove

rnm

ent

/ not

-for

-pro

fit

sum

mar

y

Field of Study: Accounting (NFP) The regulators have been busy providing guidance and not-for-profit accountants have been even busier preparing for the slew of new standards coming out. Kaplan Financial Education discussion leader Allen Fetterman provides an update on where things stand with revenue recognition, leases, CECL, goodwill and intangible assets, gifts in kind, accounting for pandemic-related issues, and other topics impacting not-for-profit organizations.

5. Revenue Recognition, Leases and Other Accounting Updates for NFPs

Summary Page (continued)

CP

AR

/ SEP

T. ‘2

1

iiiiii

cpe

requ

irem

ents

and

gro

up

liv

e CPE Requirements and Group Live

1. Select discussion leaders who have the appropriate education and/or experience both to teach the segment subject and conduct the subsequent group discussion.

2. Have each discussion leader review the video segment and the written materials in the Subscriber Guide prior to the presentation of the segment.

3. Make sure that each discussion leader certifies the attendance at his/her discussion group by signing and dating the Group Live Attendance Form.

4. (Individuals) View the video segment (30 to 35 minutes).

5. (Individuals) Discuss the segment materials as they relate to his/her own work and/or organization (20 to 25 minutes).

6. (Individuals) Evaluate the instructor using the criteria listed on the Evaluation Form.

7. Check with your State Board of Accountancy for specific details, including group live sponsorship registration requirements.

Group Live Format

When taking a CPA Report segment on a group live basis, individuals earn CPE credits when they (or their organization) do the following:

CPE RequirementsWhen properly administered, the CPA Report educational program meets the requirements for group live and self-study participation as defined in the Statement for Standards in CPE Reporting.

Please note:

l You cannot earn additional credits by taking the same course in group live format and online self-study format.

l CPE requirements vary from state to state. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. CPAs should contact their state board regarding specific CPE requirements.

iv

cpe

requ

irem

ents

and

gro

up

liv

e The following information will help you plan and implement the CPA Report program within your firm:

How to Implement the CPA Report

1. Each quarter, you may receive by email a CPA Report Summary Page in advance of the video segment notifying you of the upcoming Continuing Professional Education topics that will be covered.

2. The CPAR DVD is expected to arrive the month following the end of the quarter. If you do not have a standard day and time each quarter designated as CPE day, issue a memo with the date of your upcoming seminar. (If attendance is not required, please provide plenty of advance notice for optimum participation).

3. Select the topic(s) you wish to cover in your session when the CPAR Summary Page or the actual program arrives.

4. It is best for an organization to have its CPE classes on a regular and consistent basis, so it is easy for the staff to remember when scheduling clients.

5. You may wish to provide each group live attendee a “Certificate of Completion” noting the hours earned and the topic areas.

6. Always check with your State Board of Accountancy for specific details, including group live sponsorship registration requirements.

If you need more information or have any questions, please contact Customer Service at [email protected] or 914-517-1177.

Note: CPE requirements vary from state to state. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. CPAs should contact their state board regarding specific CPE requirements.

CP

AR

/ SEP

T. ‘2

1

v

CPA Report Update

onli

ne s

elf-

stud

y on

line

sel

f-st

udy

Please note: This issue of CPA Report Online Self-Study is scheduled to go live online on September 24, 2021.

If you need more information or have any questions, please contact Customer Service at [email protected] or 914-517-1177.

Online Self-Study

Kaplan Financial Education, powered by Smartpros is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.nasbaregistry.org.

Self-Study Format

Participants can gain self-study credit by enrolling in the CPA Report Online Self-Study library of courses. All components of the program will be hosted online, including the video, interactive review questions, required reading, and final exam.

In order to ensure adherence to NASBA guidelines regarding self-study, the CPA Report and CPA Report Government/Not-for-Profit Self-Study Professional Education Centers are no longer available. Customers should contact their company administrators for information on taking course exams and receiving CPE credit for the courses.

Customers may contact Kaplan Financial Education at [email protected] to obtain certificates previously earned through the CPA Report Self-Study and CPA Report Government/Not-for-Profit Self-Study Professional Education Centers.

Customers interested in the self-study format of the CPA Report can find information on Kaplan Financial Education’s self-study libraries at Online Accounting CPE Courses.

segm

ent

one

segm

ent

one

segm

ent

one

Segment 1

CP

AR

/ SEP

T. ‘2

1

1–1

segm

ent

one

segm

ent

one

segm

ent

one

1. Employee Stock Purchase Plans – Why Offer One?Learning Objectives:

Segment Overview:

Recommended Accreditation:Reading (Optional for Group Study):

Running Time:

Video Transcript:

Course Level:

Course Prerequisites:

Advance Preparation:

Expiration Date: November 6, 2022

Work experience in financial reporting or accounting, or an introductory course in accounting.

None

1 hour group live 2 hours self-study online

Update

“ESPPs that Work for You: Top Five Lessons Learned.“ “Case Study: ESPP Performance Across Economic Cycles” “The Key to Engagement: Designing an ESPP to Drive Your People Strategy” “ESPPs: Financial Reporting Complexity”

See page 1–12.

See page 1–22.

34 minutes

Employee stock purchase plans, often known as ESPPs, are programs that enable employees to purchase company stock via elective payroll deductions. Typically, those deductions will accrue over a set period of time, often six months. At the end of that period, the accumulated money is then used to buy stock and a new six-month period starts. ESPPs are a great incentive for employees, but how are they different from any other kind of equity compensation like options or restricted stock? David Outlaw, director of Valuation and HR Advisory Services at Equity Methods, provides us with details on the different types of ESPPs, reasons companies offer them, common structures and tax qualifications.

Upon successful completion of this segment, you should be able to: l Understand the distinct differences of ESPPs vs.other stock

compensation plans and restricted stock, l Identify the different design levers of ESPPs and the ways

they differ, l Recognize the accounting treatment of ESPPs based on their

features, and l Understand the remeasurement triggers and common

modification drivers.

Field of Study: Accounting

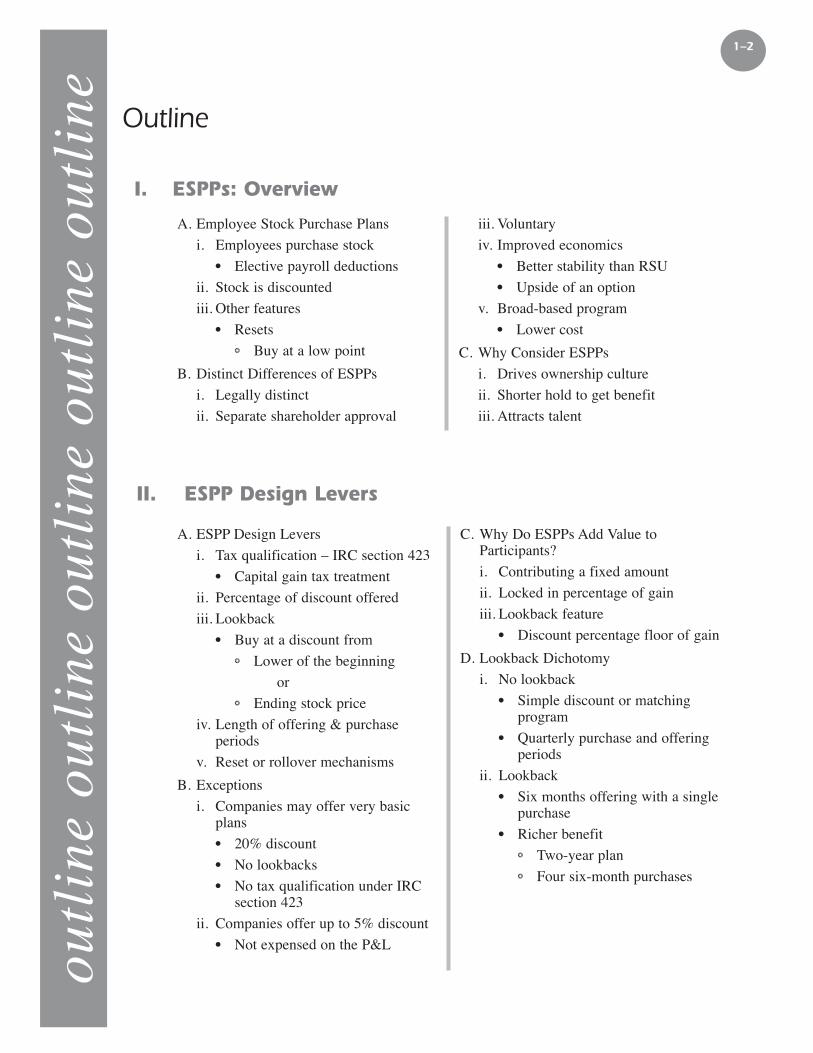

A. Employee Stock Purchase Plans

i. Employees purchase stock l Elective payroll deductions

ii. Stock is discounted

iii. Other features l Resets

b Buy at a low point

B. Distinct Differences of ESPPs

i. Legally distinct

ii. Separate shareholder approval

iii. Voluntary

iv. Improved economics l Better stability than RSU l Upside of an option

v. Broad-based program l Lower cost

C. Why Consider ESPPs

i. Drives ownership culture

ii. Shorter hold to get benefit

iii. Attracts talent

1–2

outl

ine

outl

ine

outl

ine

outl

ine

outl

ine

Outline

I. ESPPs: Overview

A. ESPP Design Levers

i. Tax qualification – IRC section 423 l Capital gain tax treatment

ii. Percentage of discount offered

iii. Lookback l Buy at a discount from

b Lower of the beginning

or b Ending stock price

iv. Length of offering & purchase periods

v. Reset or rollover mechanisms

B. Exceptions

i. Companies may offer very basic plans l 20% discount l No lookbacks l No tax qualification under IRC

section 423

ii. Companies offer up to 5% discount l Not expensed on the P&L

C. Why Do ESPPs Add Value to Participants?

i. Contributing a fixed amount

ii. Locked in percentage of gain

iii. Lookback feature l Discount percentage floor of gain

D. Lookback Dichotomy

i. No lookback l Simple discount or matching

program l Quarterly purchase and offering

periods

ii. Lookback l Six months offering with a single

purchase l Richer benefit

b Two-year plan b Four six-month purchases

II. ESPP Design Levers

CP

AR

/ SEP

T. ‘2

1

1–31–3

outl

ine

outl

ine

outl

ine

outl

ine

outl

ine Outline (continued)

A. Switching ESPPs

i. Shareholder approval

ii. Latitude with new plan

iii. Understand costs involved

iv. Roll out new plan at the end of an offering period

B. ESPPs Differences

i. Participation rules

ii. Define what falls under compensation

iii. Ability to change participation

iv. Beware of accounting ramifications

v. Cash infusions

vi. Auto enrollment

vii. International differences

C. Qualifications for Favorable Tax Treatment

i. Open to employees only

ii. Not transferable

iii. Approved by shareholders

iv. Eligibility l Broad based and non-

discriminatory

v. Discount can't be higher than 15%

vi. Term can't be more than l 27 months – lookback l 5 years – no lookback

vii. $25,000 cap

D. If Tax Qualified

i. Hold stock without selling for at least l 2 years from offering date l 1 year from purchase date l Tax on sale is capital gains

ii. Selling before that point l Disqualified disposition l Tax on sale is ordinary income l Capital gains for any subsequent

movement

III. ESPP Options and Tax Treatment

A. Estimating Fair Value

i. Simple discount plan l Discount Percentage x Stock

Price

ii. Lookback feature l Akin to an option

B. Put Option

i. Price goes down

ii. Payout remains flat

“The question we often get is what actually drives the resulting value then. And the main thing honestly is the terms of the plan.”

— David Outlaw

IV. Valuing ESPP Components

1–4

outl

ine

outl

ine

outl

ine

outl

ine

outl

ine

Outline (continued)

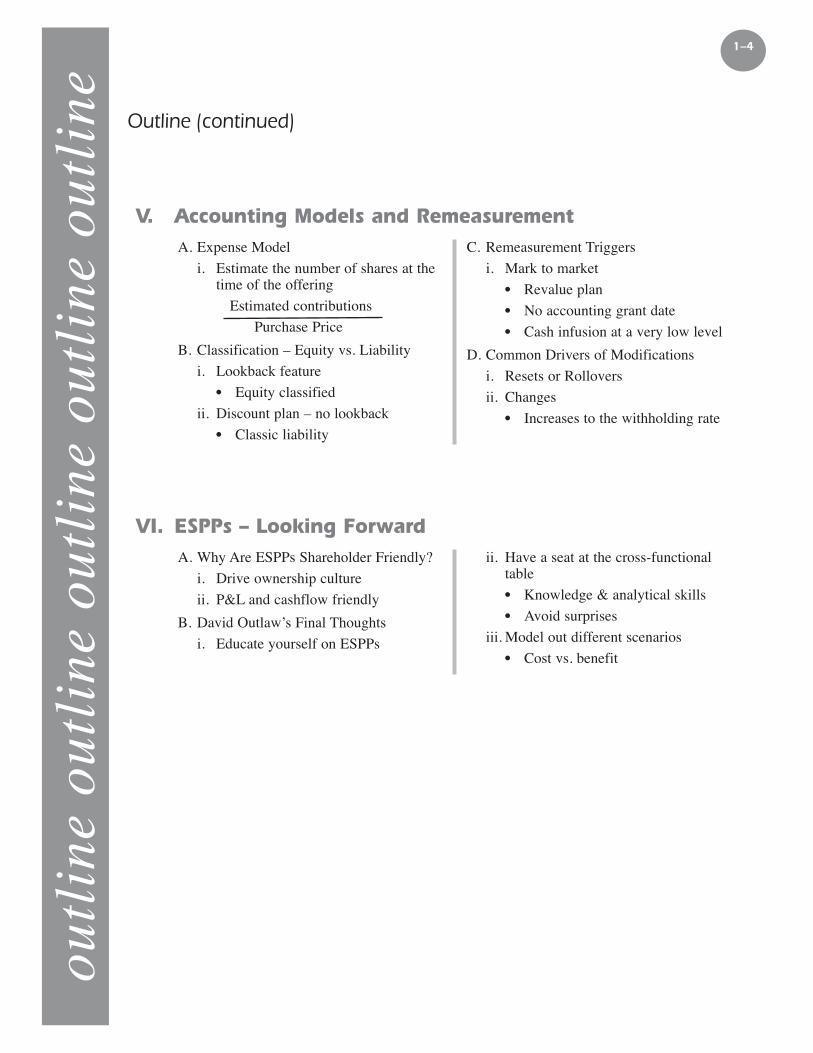

V. Accounting Models and RemeasurementA. Expense Model

i. Estimate the number of shares at the time of the offering

Estimated contributions

Purchase Price

B. Classification – Equity vs. Liability

i. Lookback feature l Equity classified

ii. Discount plan – no lookback l Classic liability

C. Remeasurement Triggers

i. Mark to market l Revalue plan l No accounting grant date l Cash infusion at a very low level

D. Common Drivers of Modifications

i. Resets or Rollovers

ii. Changes l Increases to the withholding rate

VI. ESPPs – Looking ForwardA. Why Are ESPPs Shareholder Friendly?

i. Drive ownership culture

ii. P&L and cashflow friendly

B. David Outlaw’s Final Thoughts

i. Educate yourself on ESPPs

ii. Have a seat at the cross-functional table l Knowledge & analytical skills l Avoid surprises

iii. Model out different scenarios l Cost vs. benefit

CP

AR

/ SEP

T. ‘2

1

1–5

Discussion Questions

1–5

1. Employee Stock Purchase Plans – Why Offer One?

l As the Discussion Leader, you should introduce this video segment with words similar to the following:

“In this segment, David Outlaw provides us with details on the different types of ESPPs, reasons companies offer them, common structures and tax qualifications.”

l Show Segment 1. The transcript of this video starts on page 1–22 of this guide.

l After playing the video, use the questions provided or ones you have developed to generate discussion. The answers to our discussion questions are on pages 1–7 to 1-9. Additional objective questions are on pages 1–10 and 1–11.

l After the discussion, complete the evaluation form on page A–1.

1. Employee stock purchase plans (ESPPs) allow employees to purchase stock in the companies they work for. What are the main features of such plans? Does your organization offer an ESPP to employees?

2. ESPPs can come in many different forms. What are the different types of ESPPs and how do they differ? Which form of ESPP does your organization prefer?

3. Even outside the design, ESPPs may be different. What are some of the ways ESPPs are different in terms? How does your organization treat such differences?

4. As long as they meet certain qualifications, ESPPs can get preferential tax treatment. What are the requirements for ESPPs to get favorable tax treatment? How does your organization seek to maintain compliance to achieve favorable tax treatment?

5. A key issue related to ESPPs is their valuation. How can the fair value of an ESPP be estimated? How do you or your organization measure fair value of your ESPPs?

You may want to assign these discussion questions to individual participants before viewing the video segment.

Instructions for Segment

Group Live Optiondi

scus

sion

que

stio

ns d

iscu

ssio

n qu

esti

ons

For additional information concerning CPE requirements, see page vi of this guide.

1–51–51–5

1–6

Discussion Questions (continued)di

scus

sion

que

stio

ns d

iscu

ssio

n qu

esti

ons

6. Accounting guidance for ESPPs is provided by ASC-718 Compensation—Stock Compensation. What are the main provisions of ASC-718? How does your company maintain compliance with ASC-718’s requirements?

7. Certain events may trigger remeasurements of ESPPs. What are some of the events that may cause ESPPs to be remeasured or revalued? How does your organization handle such events?

CP

AR

/ SEP

T. ‘2

1

1–71–71–71–7

sugg

este

d an

swer

s to

dis

cuss

ion

ques

tion

s1. Employee stock purchase plans (ESPPs)

allow employees to purchase stock in the companies they work for. What are the main features of such plans? Does your organization offer an ESPP to employees? l Employees purchase stock at

discounted prices through elective payroll deductions.

l Other features b Resets allow employees to buy at

a low point l Purchase price is based on any

price declines that happen over the offering period

b Employees get to buy stock with different types of discounts, which makes it a great intersection of compensation and benefit.

l Distinct Differences of ESPPs b Legally distinct b Separate shareholder approval b Voluntary b Improved economics over

traditional equity compensation plans l Better stability than RSU l Upside of an option

b Broad-based program l Participant response based on

personal/organizational experience

2. ESPPs can come in many different forms. What are the different types of ESPPs and how do they differ? Which form of ESPP does your organization prefer? l Different in ways that are unique to

ESPPs l Differences in design

b Tax qualification – IRC section 423 l Capital gain tax treatment

b Percentage of discount offered

b Companies offer up to 5% discount l Exceptions

v Companies may offer very basic plans k 20% discount k No lookbacks k No tax qualification

under IRC section 423 b Lookback

l Buy at a discount from v Lower of beginning or v Ending stock price

l Lookback dichotomy v No lookback

k Simple discount or matching program

k Quarterly purchase and offering periods

v Lookback k Six months offering

with a single purchase k Richer benefit

j Two-year plan j Four six-month

purchases b Length of offering & purchase

periods b Reset or rollover mechanisms

l Participant response based on personal/organizational experience

3. Even outside the design, ESPPs may be different. What are some of the ways ESPPs are different in terms? How does your organization treat such differences? l ESPPs Differences

b Participation rules b Define what falls under

compensation b Ability to change participation b Beware of accounting

ramifications

Suggested Answers to Discussion Questions

1. Employee Stock Purchase Plans – Why Offer One?

1–8

sugg

este

d an

swer

s to

dis

cuss

ion

ques

tion

sb Cash infusions b Auto enrollment b International differences

l Participant response based on personal/organizational experience

4. As long as they meet certain qualifications, ESPPs can get preferential tax treatment. What are the requirements for ESPPs to get favorable tax treatment? How does your organization seek to maintain compliance to achieve favorable tax treatment? l Qualifications for Favorable Tax

Treatment b Open to employees only and not

transferable b Approved by shareholders b Eligibility must be broad based

and non-discriminatory b Discount can't be higher than 15% b Term can't be more than

l 27 months – lookback l 5 years – no lookback

b $25,000 cap on stock purchases l If ESPP is Tax Qualified:

b Employees receive tax treatment similar to IPOs

b Hold stock without selling for at least l 2 years from offering date, and l 1 year from purchase date l Tax on sale is capital gains

b Selling before that point l Disqualified disposition l Tax on sale is ordinary income

l Participant response based on personal/organizational experience

5. A key issue related to ESPPs is their valuation. How can the fair value of an ESPP be estimated? How do you or your organization measure fair value of your ESPPs? l Estimating Fair Value

b Simple discount plan – (Discount Percentage x Stock Price)

b Lookback feature allowing employees to buy at the lower of the beginning or ending price l Akin to an option

v If the price goes up, employees can still buy it at today's price

l Put option v Price goes down v Payout remains flat

l Participant response based on personal/organizational experience

6. Accounting guidance for ESPPs is provided by ASC-718 Compensation—Stock Compensation. What are the main provisions of ASC-718? How does your company maintain compliance with ASC-718’s requirements? l Per ASC-718, entity must have a fair

value at the offering date. b Fair value amount is expensed

over the purchase period. l Expense Model

b Determine total estimated number of shares at time of offering:

b Estimated contributions divided by Purchase price if purchased today

b Apply computed fair value to estimated total number of shares and make necessary adjustments.

l Classification of ESPP b Equity or liability?

l Lookback feature v Equity classified

l Discount plan – no lookback v Classic liability

l Participant response based on personal/organizational experience

Suggested Answers to Discussion Questions (continued)

CP

AR

/ SEP

T. ‘2

1

1–9

sugg

este

d an

swer

s to

dis

cuss

ion

ques

tion

s7. Certain events may trigger

remeasurements of ESPPs. What are some of the events that may cause ESPPs to be remeasured or revalued? How does your organization handle such events? l Remeasurement Triggers

b Mark to market accounting – requires revaluation of ESPP each reporting period

b Revaluation occurs if there is no accounting grant date

b Cash infusion at a very low level l Common Drivers of Modifications

b Resets or Rollovers b Changes

l Increases to employee withholding rates

l Participant response based on personal/organizational experience

Suggested Answers to Discussion Questions (continued)

1–10

obje

ctiv

e qu

esti

ons

obje

ctiv

e qu

esti

ons

1. One of the features of an employee stock purchase plan (ESPP) is:

a) employees purchase stock via payroll deductions

b) employees purchase stock at a small premium but pay no tax on any gains from the sale of the stock

c) a lookback feature which allows employees to buy stock at the lowest possible historical price

d) all of the above

2. When compared to other forms of compensation, an ESPP is:

a) not legally distinct but voluntary

b) legally distinct but involuntary

c) legally distinct and voluntary

d) not legally distinct and involuntary

3. If an ESPP is considered ______ under the IRC, then employees ______.

a) qualified, receive ordinary income tax treatment

b) not qualified, get capital gains tax treatment

c) qualified, get capital gains tax treatment

d) not qualified, are not taxed on their ESPP transactions

4. A lookback period in an ESPP allows an employee to purchase a stock at a discount from the ______ of the purchase period.

a) beginning stock price at the beginning

b) lower of the beginning or ending stock price at the end

c) higher of the beginning or ending stock price at the end

d) ending stock price at the end

5. The most common lookback is a:

a) 6 month offering with a single purchase

b) 12 month offering with a single purchase

c) 24 month offering with two 12 month purchases

d) 12 month offering with two 6 month purchases

6. In order to get favorable tax treatment under the IRC an ESPP:

a) may not contain any caps

b) must have a discount of at least 15%

c) must be approved by the Board of Directors only

d) must not be transferable by employees

7. In order to get capital gains treatment, an employee of a tax qualified ESPP must hold the stock for at least ______ from the offering date and ______ from the purchase date.

a) 2 years; 2 years

b) 2 years; 1 year

c) 1 year; 1 year

d) 1 year; 1 year

8. According to ASC-718, an ESPP should be recorded as:

a) equity in all cases

b) a liability if there is a pure discount with a lookback

c) equity if there are look back features

d) a liability in all cases

You may want to use these objective questions to test knowledge and/or to generate further discussion; these questions are only for group live purposes. Most of these questions are based on the video segment; a few may be based on the reading that starts on page 1–12.

Objective Questions

1. Employee Stock Purchase Plans – Why Offer One?

1–10

CP

AR

/ SEP

T. ‘2

1

1–11

obje

ctiv

e qu

esti

ons

obje

ctiv

e qu

esti

ons

9. Recent statistics show ______ in the number of 15% discount plans and ______ in the number of 5% discount ESPPs.

a) an increase; a decrease

b) an increase; an increase

c) a decrease; a decrease

d) a decrease; an increase

10. A non-qualified tax ESPP can give discounts:

a) only less than 15%

b) greater than 5%

c) between 5% and 10%

d) greater than 15%

Objective Questions (continued)

1–121–121–121–12

By David Outlaw Source: https://www.equitymethods.com/articles/espp-plans-work-top-five-lessons-learned/

We’ve spent a lot of time over the last year or two talking to companies and industry friends about employee stock purchase plans (ESPPs). It’s hard to shake the feeling that the pendulum is swinging back toward ESPPs in a big way. With traditional equity programs focusing more on the executive suite, it’s harder for many companies to make broad-based equity grants meaningful to employees. ESPPs are a great way to fill that void, especially since they can scale to employees’ preferred participation levels and come with a built-in profit for participants.

These conversations culminated this month at the WorldatWork Total Rewards

conference, where I presented on the topic with Brit Wittman of Intel, Julie Mrozek of Leidos, and Cherie Curry of Hilton. Between the insights from that panel and the conversations in the hallways of the conference, there were some recurring points about how to make an ESPP suit your specific needs. Here are five key takeaways:

1. ESPPs are becoming more generous (again).

We all know the basic story: Everyone had great ESPPs in place 10-15 years ago before the accounting rules changed. But when FAS 123R went live in 2006, a lot of companies dialed back to “noncompensatory” plans with a 5% discount and no lookback in order to avoid any expense hit.

1–12

Self-Study Option

Reading (Optional for Group Study)

ESPPS THAT WORK FOR YOU: TOP FIVE LESSONS LEARNED

rea

ding

rea

ding

rea

ding

rea

ding

l In order to ensure adherence to NASBA guidelines regarding self-study, the CPA Report and CPA Report Government/Not-for-Profit Self-Study Professional Education Centers are no longer available. Customers should contact their company administrators for information on taking course exams and receiving CPE credit for the courses.

l Customers may contact Kaplan Financial Education at [email protected] to obtain certificates previously earned through the CPA Report Self-Study and CPA Report Government/Not-for-Profit Self-Study Professional Education Centers.

l Customers interested in the self-study format of the CPA Report can find information on Kaplan Financial Education's self-study libraries at Online Accounting CPE Courses.

CPA Report Update

CP

AR

/ SEP

T. ‘2

1

1–131–131–13

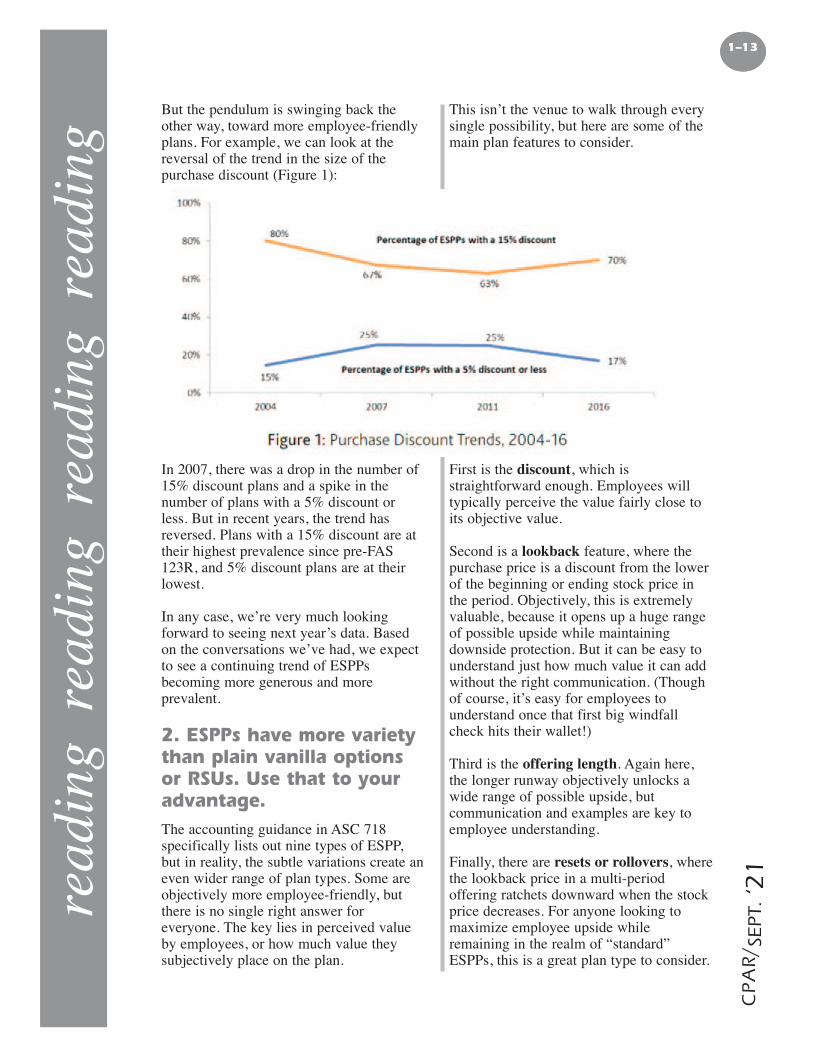

But the pendulum is swinging back the other way, toward more employee-friendly plans. For example, we can look at the reversal of the trend in the size of the purchase discount (Figure 1):

In 2007, there was a drop in the number of 15% discount plans and a spike in the number of plans with a 5% discount or less. But in recent years, the trend has reversed. Plans with a 15% discount are at their highest prevalence since pre-FAS 123R, and 5% discount plans are at their lowest.

In any case, we’re very much looking forward to seeing next year’s data. Based on the conversations we’ve had, we expect to see a continuing trend of ESPPs becoming more generous and more prevalent.

2. ESPPs have more variety than plain vanilla options or RSUs. Use that to your advantage. The accounting guidance in ASC 718 specifically lists out nine types of ESPP, but in reality, the subtle variations create an even wider range of plan types. Some are objectively more employee-friendly, but there is no single right answer for everyone. The key lies in perceived value by employees, or how much value they subjectively place on the plan.

This isn’t the venue to walk through every single possibility, but here are some of the main plan features to consider.

First is the discount, which is straightforward enough. Employees will typically perceive the value fairly close to its objective value.

Second is a lookback feature, where the purchase price is a discount from the lower of the beginning or ending stock price in the period. Objectively, this is extremely valuable, because it opens up a huge range of possible upside while maintaining downside protection. But it can be easy to understand just how much value it can add without the right communication. (Though of course, it’s easy for employees to understand once that first big windfall check hits their wallet!)

Third is the offering length. Again here, the longer runway objectively unlocks a wide range of possible upside, but communication and examples are key to employee understanding.

Finally, there are resets or rollovers, where the lookback price in a multi-period offering ratchets downward when the stock price decreases. For anyone looking to maximize employee upside while remaining in the realm of “standard” ESPPs, this is a great plan type to consider.

rea

ding

rea

ding

rea

ding

rea

ding

1–14

3. “Non-standard” plans may not be for everyone, but they’re the right answer for some.

There’s more reason than ever today to explore beyond the standard plans. If your employee base is unlikely to hold shares long enough to qualify for IRC §423 tax treatment—which is true for many companies—then the value in offering a qualified plan is limited. And if you don’t need your plan to qualify under IRC §423, then the design handcuffs are gone.

Without binding qualification criteria, a plan can give discounts greater than 15%, provide offerings longer than 27 months, or limit eligibility to a smaller employee population. Plus, a non-qualified plan always gives the company a tax deduction at settlement.

One of the more interesting features that’s come up lately is an auto-enrollment feature along the lines of what many companies do with 401(k) plans. Most often, we see these in companies that expect minimal withdrawals and who are undergoing a transition like an IPO. An auto-enrolling ESPP lets employees get in on the ground floor and helps kick-start an ownership culture.

4. Communication and education drive engagement and employee value. Perhaps the biggest takeaway from the experience of my co-panelists at WorldatWork was the importance of communication. Regardless of the plan terms, they all reiterated the importance of being proactive in driving employee engagement.

We all know that just handing a prospectus to an employee isn’t sufficient, but what are some other avenues? Plain-English FAQs or reference slides are one, as is including ESPP information in annual total rewards statements. Town hall meetings or webinars are another, especially if they coincide with enrollment periods. And

sometimes, going even bigger is necessary, such as a roadshow to support the launch of a new plan or the onboarding of new employees through a merger.

Intrigued by Intel’s astronomical participation rates (over 70% worldwide, and nearly 80% in the US), one audience member asked Brit how they managed to have such wide involvement. His answer was to embed the plan in the culture as much as possible. For example, splash purchase information onto the Intranet site and common area screens to reach as many people as possible. And once the plan really is part of the culture, fellow employees become the best salespeople for getting new folks to participate.

5. Use data and scenario modeling to inform your decisions.

It’s almost a cliché at this point, but data-driven decision-making is really important in this day and age.

Fortunately, ESPPs lend themselves very well to modeling. Sometimes, this is simple: What would our expense be if the stock price were $X, $Y, or $Z? And the participation rate were A, B, or C? And how would employee payouts compare to that expense?

Some of our clients even go as far as to simulate the whole range of potential payoffs to get a clearer idea of costs and benefits (Figure 2):

This level of detail can give you solid estimates on questions like “what’s my average expected employee gain?” and “how likely is an employee to have a gain higher than our accounting cost?” (For our curious readers, the answers in the case shown here are $1,354 and 60%, respectively.)

While this level of sophistication isn’t needed in every case, some amount of quantitative modeling is table stakes in the world today. We recommend at least starting with A) scenario modeling high/medium/low stock price cases and B) backtesting the numbers over the last few

rea

ding

rea

ding

rea

ding

rea

ding

CP

AR

/ SEP

T. ‘2

1

1–15

rea

ding

rea

ding

rea

ding

rea

ding

years of actuals as a baseline for real-world outcomes.

A major side benefit of modeling and visualization is building the case for senior management that your ESPP recommendation is well-grounded. There are a lot of opinions about ESPP designs, some more insightful than others, and our encouragement is to analyze the data before you make your decisions.

Parting thoughts All in all, this underscores the importance of being thoughtful. ESPPs are not one-size-fits-all, and there’s not a single answer that works best for every company and every culture. But by weighing a few alternatives, modeling out the possibilities, and communicating clearly to your employees, you can have a plan that works best for you.

1–16

rea

ding

rea

ding

rea

ding

rea

ding

By David Outlaw and Nick Faris Source: https://www.equitymethods.com/articles/case-study-espp-performance-across-economic-cycles/

The recent market volatility has put employee stock purchase plans (ESPPs) at the front of our mind a lot this year. While much of the compensation focus has been on restoring incentives for performance awards, we see ESPPs as a sort of bellwether for a company’s employee sentiment.

For most companies, ESPP participation has remained steady or even ticked up. After all, ESPPs are a powerful engagement tool that delivers excellent value across business cycles (as we’ll illustrate in our case below). The data supports this view, too: In recent polling of webcast participants, about 64% of respondents with ESPPs observed behavior roughly similar to the past, and a further 22% observed more interest or participation than normal.

At other firms, employee participation has declined, perhaps due to pay cut or furlough concerns. Among our client base (where we have detailed participation data), a substantial number of firms saw withdrawals increase by 40% or more. At

some companies in hard-hit industries, withdrawals rose more than tenfold.

There’s no compensation plan that can avoid the painful realities of economic distress. But as some companies look forward to building a future amidst volatility and uncertainty, we’re reminded that ESPPs are an excellent equity vehicle to help employees ride out this volatility. In this blog post, we’ll explore some of the costs and benefits that different ESPP types can deliver.

Note that we assume for the case study below that readers have a basic understanding of ESPP mechanics and features. If you’d like to brush up, we recommend the following articles:

The Key to Engagement: Designing an ESPP to Drive Your People Strategy (Workspan article)

ESPPs that Work for You: Top Five Lessons Learned (blog)

Five Ways that West Coast Companies Design ESPPs (blog)

ESPPs: Financial Reporting Complexity (issue brief)

CASE STUDY: ESPP PERFORMANCE ACROSS ECONOMIC CYCLES

CP

AR

/ SEP

T. ‘2

1

1–17

The Case

We selected a firm to study that we felt was fairly representative of a middle-of-the-road case over the last decade, with performance that roughly tracked the broader economy without unusual spikes or crashes in stock price. We’ll refer to them as Company XYZ (names have been changed to protect the innocent). The company is a Fortune 500 consumer staples firm, and our analysis is entirely at arm’s length—they’re not a client and we have no insight into any ESPP plan they may have.

For this case study, we did what we often do for our clients who are considering an ESPP: We ask, “What if this company had issued this plan over the past several years? What would have been the company costs and employee benefits?” So, in our never-ending quest to analyze as much data as possible, we simulated an employee contributing $5,000 during each purchase period in three enrollment designs, starting in May 2012 and running through April 2020. Here are the relevant plan attributes:

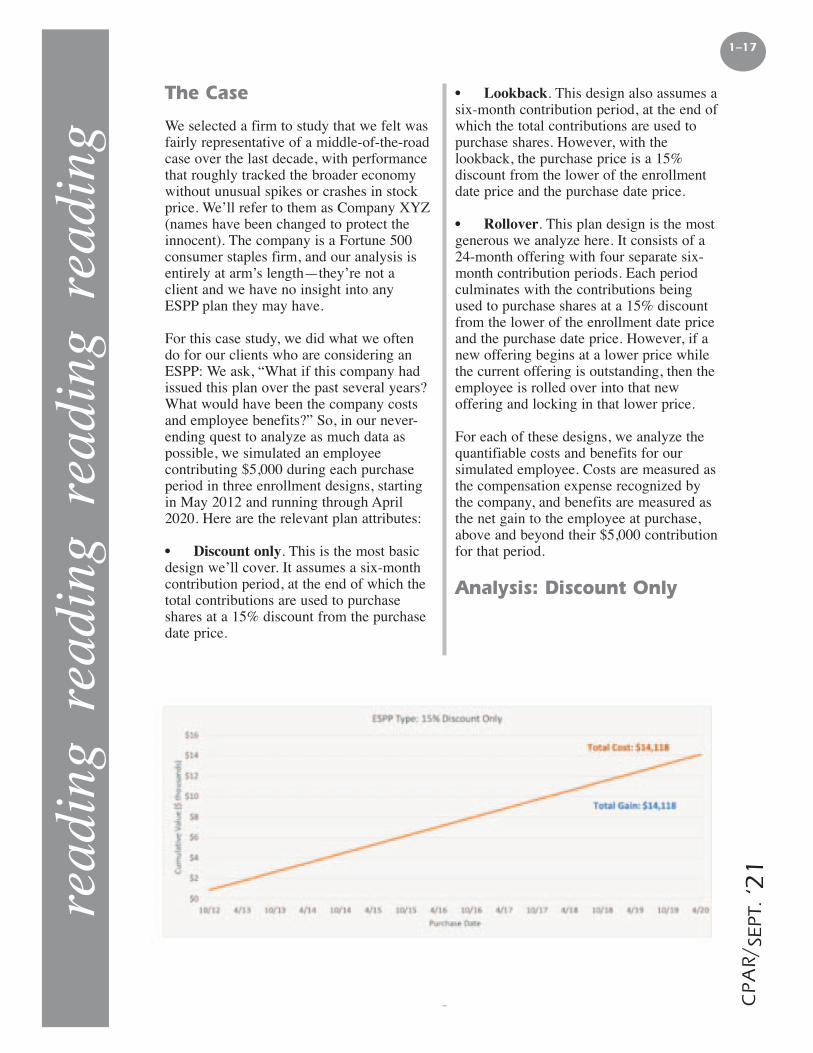

l Discount only. This is the most basic design we’ll cover. It assumes a six-month contribution period, at the end of which the total contributions are used to purchase shares at a 15% discount from the purchase date price.

l Lookback. This design also assumes a six-month contribution period, at the end of which the total contributions are used to purchase shares. However, with the lookback, the purchase price is a 15% discount from the lower of the enrollment date price and the purchase date price.

l Rollover. This plan design is the most generous we analyze here. It consists of a 24-month offering with four separate six-month contribution periods. Each period culminates with the contributions being used to purchase shares at a 15% discount from the lower of the enrollment date price and the purchase date price. However, if a new offering begins at a lower price while the current offering is outstanding, then the employee is rolled over into that new offering and locking in that lower price.

For each of these designs, we analyze the quantifiable costs and benefits for our simulated employee. Costs are measured as the compensation expense recognized by the company, and benefits are measured as the net gain to the employee at purchase, above and beyond their $5,000 contribution for that period.

Analysis: Discount Only

rea

ding

rea

ding

rea

ding

rea

ding

1–18

rea

ding

rea

ding

rea

ding

rea

ding

First, let’s analyze a plan with only a 15% discount. The way these plans work, the cost and benefit will necessarily track almost identically to one another—the only small differences you might see are due to things like share rounding and particular systems conventions.

This makes discount-only plans relatively unexciting as a benefit offering. It’s certainly nice for the employee to gain access to that 15% discount, but it comes as cost straight out of the company’s pocket. It’s effectively a straightforward compensation arrangement with no further upside or downside.

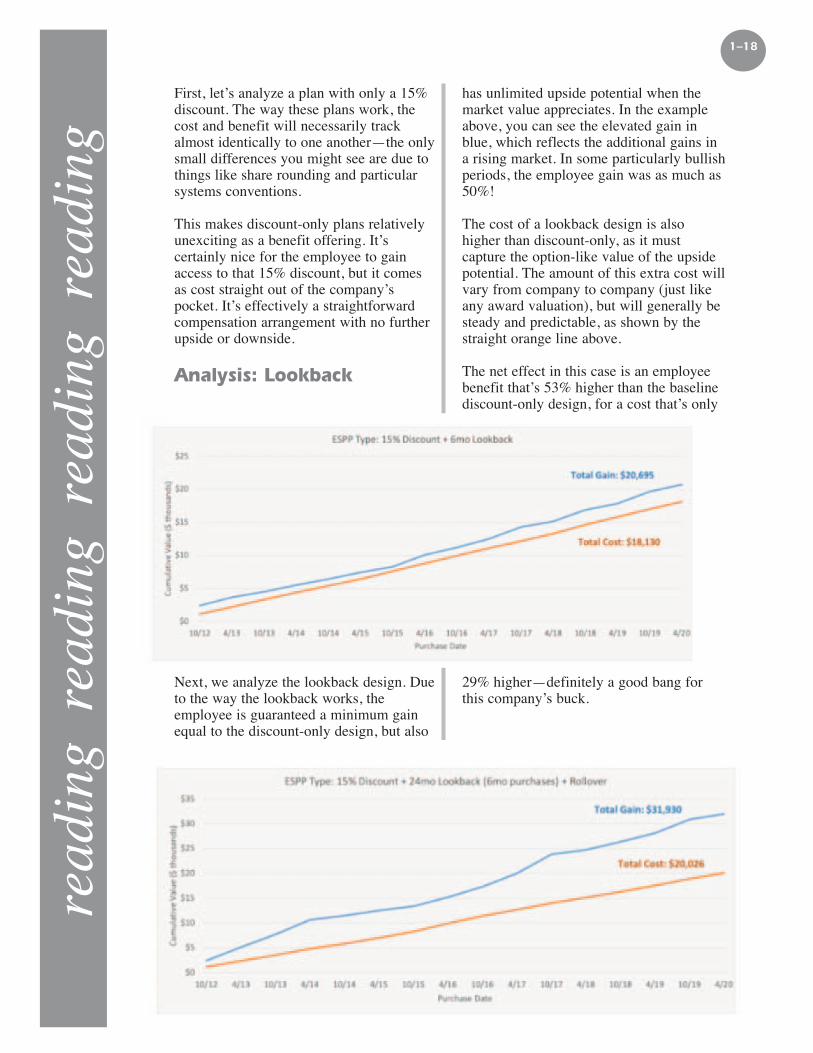

Analysis: Lookback

Next, we analyze the lookback design. Due to the way the lookback works, the employee is guaranteed a minimum gain equal to the discount-only design, but also

has unlimited upside potential when the market value appreciates. In the example above, you can see the elevated gain in blue, which reflects the additional gains in a rising market. In some particularly bullish periods, the employee gain was as much as 50%!

The cost of a lookback design is also higher than discount-only, as it must capture the option-like value of the upside potential. The amount of this extra cost will vary from company to company (just like any award valuation), but will generally be steady and predictable, as shown by the straight orange line above.

The net effect in this case is an employee benefit that’s 53% higher than the baseline discount-only design, for a cost that’s only

29% higher—definitely a good bang for this company’s buck.

CP

AR

/ SEP

T. ‘2

1

1–19

Analysis: Rollover

Next up is the rollover design. This design incorporates both the lookback and discount features, as well as having four purchases in one offering. The longer runway afforded by multiple purchases per offering adds a lot of value on its own: Since the lookback feature allows the participant to purchase at the lower of the purchase or enrollment date price, it gives the market price more time to climb without the lookback price ratcheting upward.

The other feature that adds a lot of value is the rollover itself, which helps further protect participants from decreases in the market price. If the price declines, which in this case occurs for the April 2015 purchase, the employee rolls over into the new offering at the lower price. This ensures that every employee can always buy at the most favorable price available, and leads to the steep gains seen above in 2016.

On the cost side of the ledger, two features of this design lead to higher expense for the company. One is the longer offering period to accommodate the four purchases. Because of the longer option term embedded in these purchases, the value is higher—just like Black-Scholes with a longer expected term. The other is that any time a rollover is triggered, it triggers an accounting modification and associated incremental expense.

On the whole, this is again a substantial value for the employee at a favorable cost. The employee sees a 136% gain over a discount-only plan—that’s more than twice the value—at only a 43% cost increase to the company. We caution that these results won’t be of the same magnitude for every company. This company had a lower volatility than others might, which leads to lower costs, and of course the last eight years have been a very positive period for stock performance. That said, we do consistently see good ROI for our clients’ money in implementing generous ESPPs like these.

Reviewing the Last Recession

Another angle we want to explore given the current economic uncertainty is what happened in the last recession, and what that can tell us about how ESPPs might behave in a future recession. With the above examples only running from 2012 to 2020, we also tested the period 2007 to 2011 on these same plan designs.

For a discount-only plan, we found again that the costs and benefits (by definition) are approximately equal, albeit with less value delivered in a down market. Keep in mind that this is already more favorable than a traditional equity plan—if you issue an RSU before a market decline, you’re stuck with the higher expense even when low value is actually delivered.

rea

ding

rea

ding

rea

ding

rea

ding

1–20

For a lookback plan, the lookback optionality provides less value to the employee when the price is declining. Employees will still be at least as well off as a discount-only plan, but can start benefiting from the recovery (and potentially from any volatility during the down period) immediately. For this company, we see that costs and benefits roughly align for this plan type.

Finally, we see that rollover plans significantly outperform in periods of recession and volatility. The longer lookback gives employees more time to ride out the down period and benefit from the recovery, while the rollover keeps their purchase price as low as possible if that recovery doesn’t happen smoothly.

Conclusion We’ve always seen ESPPs as a cost-effective way to drive a lot of value to employees, both monetarily and in softer ways like

creating engagement and encouraging an ownership culture. We see these advantages as especially true in uncertain times, where the unique combination of guaranteed gain and windfall upside opportunity can produce a truly differentiated employee benefit without breaking the bank.

Every company is unique, and the fact pattern shown in this case study is just one example that wouldn’t look the same for

everyone. But the cost effectiveness of generous ESPPs, either as a supplement or a replacement for traditional equity plans, has driven a resurgence in their use that we expect to continue in the coming months and years.

If you have any questions about ESPPs, whether you currently have one or are just considering it, please reach out to us or your Equity Methods consultant.

1–20

rea

ding

rea

ding

rea

ding

rea

ding

1–20

CP

AR

/ SEP

T. ‘2

1

1–21

rea

ding

rea

ding

rea

ding

rea

ding

THE KEY TO ENGAGEMENT: DESIGNING AN ESPP TO DRIVE YOUR PEOPLE STRATEGY

By Takis Makridis and Therese Sebastian Source: https://www.equitymethods.com/articles/the-key-to-engagement-designing-an-espp-to-drive-your-people-strategy/

Employee stock purchase plans (ESPPs) are more than just compensation. They’re an important tool for creating an ownership culture while potentially delivering outsized financial gains at a (usually) modest cost. In some industries, an ESPP is table stakes for competing in a tight labor market. In others, it can be a genuine strategic differentiator.

But ESPPs are not created equal. Even in industries where they’re common, it’s possible to design a program that stands out and delivers greater impact. In this article from the February 2019 issue of Workspan, we discuss the different flavors of ESPPs and ways to help you determine which type is right for your organization. Along the way, we’ll show why ESPPs just might be the most versatile—and underutilized—compensation and employee engagement instrument.

See the story online or get a PDF via the “download” button on this page.

by David Outlaw and Nick Faris Source: https://www.equitymethods.com/articles/espp-financial-reporting-complexity/

Across the country, employee stock purchase plans (ESPPs) are on the rise. In addition, more ESPPs have exotic provisions, such as features allowing for contribution rate changes and reset or rollover provisions.

With this growth in ESPP popularity, there is increasing scrutiny surrounding the financial reporting for these programs. Traditional “pool-based” approaches are running into trouble with external auditors, who are concerned that the imprecision may have material consequences on the final results.

This issue brief, originally published in 2016 and newly updated for 2018, details the rise in popularity of ESPPs. It also looks at exotic design features that are intended to deliver more value, as well as financial reporting best practices.

THE KEY TO ENGAGEMENT: DESIGNING AN ESPP TO DRIVE YOUR PEOPLE STRATEGY

1–221–221–221–221–221–221–221–221–221–221–221–221–221–221–221–221–221–221–221–22

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t

SURRAN: Employee stock purchase plans, often known as ESPPs are programs available to employees that enable them to purchase company stock via elective payroll deductions. Typically, those deductions will accrue over a set period of time, often six months. At the end of that period, the accumulated money is then used to buy stock and a new six month period starts. It is a continuous process of deducting from payroll and buying stock.

Where it gets really interesting is in the economics of exactly how that happens for employees. It is almost always happening at a discount, which is beneficial for employees and it is also possible to have features like lookbacks, which are the ability to buy the stock at the lower of the price at the beginning or end of that six-month purchase period. So there are some options and upside potential.

There are some other exotic features, such as resets, that allow employees to buy at the low point, which means that the purchase price is based on any price declines that happen over the offering period. Employees get to buy stock with different types of discounts which makes it a great intersection of compensation and benefit.

MORIARTY: Employee stock purchase plans sound like a great incentive for employees, but how are they different from any other kind of equity compensation like options or restricted stock? David Outlaw, director of Valuation and HR Advisory Services at Equity Methods, provides us with the distinct differences.

OUTLAW: We tend to think of it as its own category of benefit. It's not quite stock compensation, it's certainly not based on a bonus, and it's really not a health plan or tuition reimbursement or anything. But it is its own important part of the overall portfolio. And in fact, it is legally distinct as well. It's an entirely separate shareholder approval and legal plan than the rest of the equity comp. So it is actually important to think about it distinctly. As far as some of the key really true differences.

First and foremost, it's voluntary. And so employees can choose to participate if they want to participate. They can participate a little bit, they can participate a lot. And so that gets around some of the concerns that companies might have with, for example, issuing equity lower in the organization where those people might prefer to have more cash, more liquidity in the paycheck in terms of paying their bills month to month.

It also has improved economics in many ways over a traditional equity compensation plan. So, you have essentially better downside stability than even a Restricted Stock Unit or RSU would have. But then you have the upside of an option, and so it's the best of both worlds there.

On the flip side, some things that make it a little bit less advantageous is it really is a best fit as a broad-based program. If it's tax qualified, which we'll talk about later, that does mean it has to be non-discriminatory and available to everyone. And it would have a $25,000 purchase cap, which means that it doesn't necessarily scale to executive compensation levels in the way that a traditional equity program would do fairly well.

Video Transcript

1. Employee Stock Purchase Plans – Why Offer One?

1–22

CP

AR

/ SEP

T. ‘2

1

1–23

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t All of that aside though, in terms of a broad-based program, it often is something that is lower cost to the company both in terms of the expense on the books as well as cash burn given that employees are actually contributing to the program itself instead of being given stock outright.

MORIARTY: David touched upon some of the reasons companies offer ESPPs. He further elaborates.

OUTLAW: I think that the main reasons are really two-pronged. So first is that it helps drive an ownership culture because people are actually buying the stock. So therefore, they have an interest in how that stock performs, which is good from an incentive alignment perspective. That's something that makes it very shareholder friendly.

Now, one knock that we sometimes hear on ESPPs is that if people are selling the shares pretty quickly after they purchase them that it detracts from the ownership culture. And that's partially true to some degree. But in my opinion, it misses the point because if you have one purchase leading right into the next, then the employee always has skin in the game. So it might not be compounding in the way that it would if they were to hold every single share, but they always have a reason to be paying attention to the stock price and driving performance.

In another sense, it can actually be beneficial that they don't have to hold on to it long-term to get the benefit of it. Because for example, if you have long-time employees who might already hold a lot of stock, that you're not playing against their need to diversify their wealth, for example. So the ownership culture is one of the key reasons to issue an ESPP.

The other one is simply that it makes a really attractive compensation and benefits package in this war for, that I think all companies are really seeing and feeling right now.

MORIARTY: David discusses the types of companies that usually offer ESPPs and if they are industry specific.

OUTLAW: Lots of different kinds of companies issue ESPPs. Most acutely, that is technology companies, usually on the West Coast where pretty much every company has any ESPP of some sort.

But even within that group, we see diversity, we see different types of companies that are issuing their ESPPs for different sorts of reasons. It's something where when a new employee comes on board, yes, HR gives them some sort of walkthrough of the ESPP.

But more importantly, it's something that their new colleagues are going to be talking to them about and encouraging them to participate in. And so it can be a part of the culture of a more mature company. But at the other end of the maturity spectrum, we very often see companies who are IPOing and decide to launch an ESPP alongside their IPO in order to give employees a chance to participate in that IPO price in a way that they might not otherwise have access to given various blackouts and restrictions and things like that. So we see diversity even within the technology space. But as I mentioned, it can be a really exciting part of the portfolio even for companies outside of that space. So for example, energy is another one that we see where ESPPs are a compensation tool that is resilient across the up and down cycles.

MORIARTY: David just discussed ESPPs in relation to IPOs, but can they also apply to SPACs?

1–241–241–24

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t OUTLAW: I guess I should be a little bit less specific in using the phrase IPO. I should say going public because between IPOs, direct listings, and SPACs these days, there seem to be a lot of roads that are leading to Rome. And with any of them, you can implement an ESPP that essentially kicks in on that first day of trading for the lookback price.

MORIARTY: David Outlaw discusses the different types of ESPPs and the way they differ.

OUTLAW: ESPPs are actually shockingly diverse, I think much so more in practice than stock options, for example. They're just different in ways that are unique to ESPP. So it's a little bit of its own language. So we can talk about five main levers with the design.

First is tax qualification under Internal Revenue Code section 423. If you're familiar with incentive stock options, that's IRC 422, so it's very similar guidance in that regard. Essentially, what it does is it says, if you design a plan within this fairly reasonable and broad set of boundaries, then your plan can be qualified. And if so, then your employees can get a capital gains tax treatment rather than ordinary income provided that they meet certain holding requirements.

Many, many U.S. plans are 423 qualified because it's a fairly easy way to increase the benefit of the ESPP, unless you're trying to do something sort of unique and potentially special with the design. So that's usually the first node in the decision tree of designing a plan.

From there, we go into our second design lever, which is how much of a discount you buy the stock for. So for a 423 qualified plan, that maxes out at a 15% discount that you're allowed to have. And indeed, 15% is the most common discount that we see in the market. And it's one of those probably path dependent things where because that was what the tax code allowed when it was written back in the 80s that many companies gravitated toward that. And so it's very much become the norm in that regard.

MORIARTY: Are there any exceptions?

OUTLAW: There are a couple of exceptions to that, that I should probably note. One is that some companies have a less exotic plan that is really just a matching stock purchase plan where they might say you're going to put some money in, we're going to match 25% of it, and then you're going to buy stock with that. Of course, a 25% match is effectively a 20% discount. That kind of a plan wouldn't have lookbacks, it wouldn't be 423 qualified, but we do see some plans that are just outside of this discount world entirely.

Then there is another category of practices around discounts where we see companies with just a 5% discount. Really that's another historical accident due to regulatory changes. So back in 2004 when FAS 123R was introduced that changed the accounting for stock options and by extension ESPPs as well, there was an exception that ESPPs would not have to be expensed on the P&L if the discount was 5% or less, and there were no lookbacks or other lucrative features.

The idea basically being that if a company wanted to just issue stock the traditional way with bankers that they would be paying at least 5% anyway, so it's not really compensatory to give that small of a discount. Now, those plans aren't very good benefit plans, they don't tend to have very high participation. But that is something that you do see; a lot of companies out there that have this semi dormant plan with just a 5% discount. But among companies who are trying to make a differentiated

CP

AR

/ SEP

T. ‘2

1

1–25

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t play in their compensation and benefits package, 15% is far and away the norm.

Now, the third design lever is what's called a lookback. I've mentioned this a couple of times, it's that ability to buy at a discount from the lower of the beginning or the ending stock price at the end of the purchase period. And essentially what that is then is a call option. Now, not every plan has this certainly. But in technology, they generally do. It's in some of the other industries where we see a little more variation on this. This is a feature that adds a little bit of expense because you do have this optionality, but it adds a ton of value to participants.

MORIARTY: So what is the reason it adds so much value to participants?

OUTLAW: If you have no lookback, then you have a guaranteed gain of whatever your discount is. So let's say it's 15%. It can't go lower, but it also can't go higher. Because you're contributing a fixed amount of money, if the price goes up, you buy fewer shares, and you lock in 15% of your contribution as your gain no matter what. So even that's not a bad deal at all, right?

But the lookback is where it starts to get super fun and really a unique deal for employees. Because with the lookback that 15%, it's now simply the floor on your gain, and it can go up from there. So if the price stays flat or if it goes down, then you stick that 15% in the bank or your brokerage account, I suppose. But if it goes up, then you keep your original 15% and then you start stacking on top of it dollar for dollar for every increase in the stock price.

Now, the fourth main design lever is the length of the offering period and the purchase periods. So the purchase period, to go through some terminology here, is the length of time where you are having money deducted from your paycheck and set aside before a purchase occurs. So in the example that I've been using so far, that would be a six-month purchase period. Now, the offering period is something that can either be the same as the purchase period or it can be longer. And the reason that the offering period length matters is if you have more than one purchase per offering, you can have a longer runway for your lookback feature.

MORIARTY: David discusses another common design.

OUTLAW: Another common design is to have a two-year offering period with four, six-month purchases occurring during it. And again, that advantage is that run-up ability in the lookback feature. So by the time you get to that two year mark, you're 24 months in, you are looking back not six months, but 24 months all the way to the start.

There's the ability for the stock price to have increased very dramatically and therefore made a very, very lucrative benefit for employees. In terms of what is common with purchase periods and offering periods, this is another place where we do see something of a dichotomy.

So for companies where there is no lookback and it is just more of a simple discount or a match program, then more frequent is common, like quarterly or something like that. There's no real upside or downside one way or the other, so it's mostly balancing the administrative burden of frequent purchases against the liquidity for the employees.

Now, if there is a lookback, the most common is to have six months offering with a single purchase. But that two-year plan with the four, six-month purchases is increasingly common where companies are trying to differentiate their ESPP and make it a richer benefit.

1–261–261–26

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t That's actually a good segue since those longer offerings often pair with our fifth design lever, which is reset or rollover mechanisms. And this is what companies use when they're trying to make their plan as advantageous and differentiated as possible.

So to explain these features, let's dive a little bit deeper into those two-year plans. The advantage again is clear, you have a longer runway for the price to increase, and your lookback is still anchored back to the price at the very beginning of the offering. But what about the downside, right? If the price drops in the first six months, it wouldn't be hard to take advantage of the lookback unless there's a quick recovery or you're stuck underwater. And that's where the reset comes in. It says that, okay, if the purchase price dips below the offering price, you make that lower of purchase like you normally would. But right after that, the offering price that's your anchor for the lookback, it resets to that now lower stock price for the remainder of the offering. And that way it's like a downward ratchet that always keeps employees in the most advantageous position.

MORIARTY: David gives us his insights as to available options when a company initially chooses a design plan and then several years later a more advantageous plan comes along that could attract talent even more. Can a company switch and would that be a burden for the company? How would employees be affected?

OUTLAW: It actually is in line with a lot of what we've been seeing over the last five years or so, which is ESPPs have historically been on sort of a pendulum where if you go back to the 90s, these very, very rich plans, even with resets and things like that were fairly common.

Then when the accounting rules changed in the early 2000s, a lot of companies dialed it back because they were afraid of the P&L hit.

And then after the financial crisis when the economy started booming again and the war for talent got more and more acute, companies started re-investing, they started seeing their ESPP as something that they could use as a differentiator. And so what we saw was a lot of companies starting to go from a less lucrative plan to a more lucrative plan.

It's actually a fairly easy thing to do. Most ESPPs, the actual legal plan documents, first of all, they're very easy to have shareholder approved. We'll talk about that a little bit more later.

But second of all, they usually give the company pretty good latitude in terms of what specifically they do with the plan that they decide to implement. There's this umbrella that allows the company to make decisions, and the company can then make those decisions. So that process, you want to model out what the cost differences would be, of course. But that's the main challenge for the company is making sure that they understand what it's going to do from a cost perspective.

Then from the employee perspective, you can't change an offering midstream typically, but they're always rolling off. What you can do is you can just once the next offering ends, roll them into the new plan.

And really, it's an employee communication and education question like so many things are just to make sure that they understand the benefit that they're getting with the switch.

MORIARTY: There is certainly a lot of design variety but outside the main terms, David discusses other ways the plans are different.

CP

AR

/ SEP

T. ‘2

1

1–271–27

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t OUTLAW: One common category of ways that plans are going to differ from one another is participation rules. For example, how much of somebody's pay are they allowed to contribute to the ESPP? Is that capped at 5% or 10% or 15% of somebody's compensation? That's a decision companies have to make.

There's also a related decision of what kind of compensation counts. So base pay is always there, but what about bonuses? What about commissions? Things like that are variable. You see more variation with companies there. The ability of people to change the degree to which they're participating is another way that it varies.

So for example, increasing or decreasing how much of your paycheck you're having deducted is something where we see variation. And the reason we see variation there is because of the accounting ramifications, which we'll talk about a little bit later.

But increasing your contributions is something that is actually a modification for accounting. So companies try to limit people's ability to do that either by prohibiting entirely, except for between offerings, of course, or by limiting it maybe to one time that it can happen mid period of a certain offering. Decreases, sometimes it's just as limited, sometimes you see more ability to do that because there is no onerous accounting or administrative burden to that. In a similar vein, we have withdrawals. And so can somebody either reduce their contributions down to zero and/or withdraw from the plan entirely and get their money back? Obviously, in case of termination, that's something that's universal. But outside of that, it's something that companies have to weigh the pros and cons of the administrative burden there again.

And then other things like cash infusion. So does somebody only have to prospectively have pay deducted from their paycheck or can they write a check to fill up their account for the ESPP contribution? That's where we see some variation there. That latter one is a little more rare, and we'll talk about why in a little bit when we talk about the accounting.

On a related note, auto enrollment is another common feature that we see these days, especially when companies are going public where they will automatically enroll employees in the ESPP and then give them the opportunity to opt out. But that way nobody misses the opportunity due to whatever reason to participate in that initial offering that's happening.

Then outside of that, we see international differences quite a lot, of course. And obviously, you'll need to talk to international securities counsel because it's driven by different global laws. But for example, you'll very often see sub-plans for places where the types of plans are more limited than what are allowed in the U.S.

MORIARTY: David Outlaw mentioned certain tax qualifications. He further elaborates.

OUTLAW: The basic gist is that as long as you stay within some basic design bounds, employees can get favorable tax treatment. And the design bounds are pretty easy to meet for the most part.

As I mentioned, only being open to employees, not being transferable. The plan has to be approved by shareholders, which is usually pretty noncontroversial.

Then eligibility, basically it has to be broad based and non-discriminatory. You have to exclude anyone who owns more than 5% of the company. If you want, you can exclude new hires, part-timers, seasonal workers, and highly compensated employees. And then anyone who is eligible for the plan has to have equal rights and privileges under the plan.

1–28

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t Then on the economics of the plan itself, essentially the discount can't be higher than 15%. The term can't be more than 27 months for an offering if there's a lookback or five years if there's no lookback. Then there's a $25,000 cap on how much stock can be purchased per person.

So assuming you meet those, the plan is tax qualified. What that means is the employee basically gets tax treatment similar to ISOs, Incentive Stock Options, if you're familiar with those.

So if they hold the stock without selling for at least two years from the offering date and one year from the purchase date, then the tax upon sale is entirely capital gains. If they sell before that point, it's a disqualifying disposition.

They get taxed then at ordinary income for the spread at purchase, the difference between what they paid and what the stock was worth. Then its capital gains or losses for any subsequent movement from there.

And then of course, there's a need for the company to track all of this as well, just like with ISOs. If the employee has a qualifying disposition, so they've held it for the two years, then there's no income ever recognized, no ordinary income on their tax return. And therefore, the company doesn't get to deduct anything on its own taxes for compensation costs because there was no compensation or no income, I should say. But if the employee has a disqualifying disposition, then that spread does get recognized as ordinary income by the employee, and therefore the company gets a deduction in that amount.

MORIARTY: The key principle with ESPPs is to value each component part. David discusses how fair value is estimated.

OUTLAW: If it's a simple discount plan, then the value is going to be simple. It's your percent discount multiplied by the stock price. So if the price is $100 and the discount is 15%, then the fair value is $15.

And the employee, they're contributing the other $85 themselves, so that's not compensation and not something that you therefore need to expense. Now, if you pay a dividend, there's a small wrinkle to add in there to slightly haircut for the dividends that are missed during the purchase period. You might pay two dividends during the six months, for example.

Now, the next piece to look at is if you have a lookback feature allowing you to buy at the lower of the beginning or ending price. So there, as you might guess, it is akin to an option.

Basically, if the price goes up, I can still buy it at today's price. So there's an at the money call option, and you can just use Black-Scholes for that. And fortunately, you have a fixed term.

Everything else from stock-based compensation accounting applies in terms of the way that you use Black-Scholes. But there's also a put option for most plans, which is a little less intuitive. And it's because if your price goes down, you can actually buy more shares with your fixed contribution so that your dollar gains are maintained.

In other words, if the price goes down, your payout stays flat, and that's a put option. So putting those pieces together, let's say for illustration, it's a 15% discount again. So you've got one, the discount valued at 15% of the stock price, two, an adjustment for forgone dividends, three, 85% of a Black-Scholes call option. And four, it is 15% of a Black-Scholes put option.

CP

AR

/ SEP

T. ‘2

1

1–29

vide

o tr

ansc

ript

vi

deo

tra

nsc

rip

t So you sum those four pieces together, and that's your value. So the question we often get is what actually drives the resulting value then. And the main thing honestly is the terms of the plan.

SURRAN: ASC-718 Compensation-Stock Compensation has a section that specifically discusses Employee Stock Purchase Plans that provides clear authoritative accounting guidance.

It offers several examples covering different features and how they are accounted for.

According to the guidance, you have a fair value at the offering date and you expense that over the purchase period. Similar to other stock-based compensation, you can analogize the grant date to the offering date and the vesting period or requisite service period over the purchase period.

MORIARTY: David Outlaw discusses in further detail the expense model and how it works.

OUTLAW: The first piece of it is fundamentally how many shares do you apply that fair value to that we just talked about? That's because this isn't like an RSU or a stock option where the number of units is actually a part of the contract, and you don't actually know at the beginning how many shares are actually going to be purchased.

Capital so what you need to do at the time of the offering is to estimate the number of shares at that point. And the way that you do that, it's going to be a division problem. So your numerator is your estimated contributions.

The specific way that you might come to this is going to vary a little bit from company to company, but you want to have a process that's set that is auditable, that is controlled and repeatable. Essentially what you want to do is say the percentage that somebody is contributing and then what their expected pay is over the length of the purchase period. And that will give you an estimated total dollar value that you expect to see in their account when the purchase actually occurs.

And then the denominator of that is the purchase price if it happened today. So continuing our example, that would be 85% of the stock price at the time of the offering.

That will be our estimated number of shares. We'll apply the fair value that we computed to that, and then there'll be some true-ups at the end and potentially some adjustments along the way that we'll talk about here. The next upfront consideration though is the classification, is this an equity or a liability? And that's actually something that depends on the design.