sept 2015 - bnktrinity.files.wordpress.com gujarat 2010 1.25 satara, maharashtra 2011 2.0 sangli,...

TRANSCRIPT

Management Presentation Sept 2015

Safe Harbour

2

This presentation and the accompanying slides (the “Presentation”), which have been prepared by Sarla Performance Fibers Ltd. (the “Company”), have been prepared solely for information purposes and do not constitute any offer, recommendation or invitation to purchase or subscribe for any securities, and shall not form the basis or be relied on in connection with any contract or binding commitment whatsoever. No offering of securities of the Company will be made except by means of a statutory offering document containing detailed information about the Company.

This Presentation has been prepared by the Company based on information and data which the Company considers reliable, but the Company makes no representation or warranty, express or implied, whatsoever, and no reliance shall be placed on, the truth, accuracy, completeness, fairness and reasonableness of the contents of this Presentation. This Presentation may not be all inclusive and may not contain all of the information that you may consider material. Any liability in respect of the contents of, or any omission from, this Presentation is expressly excluded.

Certain matters discussed in this Presentation may contain statements regarding the Company’s market opportunity and business prospects that are individually and collectively forward-looking statements. Such forward-looking statements are not guarantees of future performance and are subject to known and unknown risks, uncertainties and assumptions that are difficult to predict. These risks and uncertainties include, but are not limited to, the performance of the Indian economy and of the economies of various international markets, the performance of the tire industry in India and world-wide, competition, the company’s ability to successfully implement its strategy, the Company’s future levels of growth and expansion, technological implementation, changes and advancements, changes in revenue, income or cash flows, the Company’s market preferences and its exposure to market risks, as well as other risks. The Company’s actual results, levels of activity, performance or achievements could differ materially and adversely from results expressed in or implied by this Presentation. The Company assumes no obligation to update any forward-looking information contained in this Presentation. Any forward-looking statements and projections made by third parties included in this Presentation are not adopted by the Company and the Company is not responsible for such third party statements and projections.

Table Of Contents

Company Overview

India Operations

Overseas Operations

Growth Plans

Financials

3

Table Of Contents

Company Overview

India Operations

Overseas Operations

Growth Plans

Financials

4

Background

Brief Highlights

5

Presence Financials

Commenced operations in 1995 as a manufacturer of commodity yarns

Progressed to specialized and higher value added yarns

100% EOU:

Focus on high margin specialty polyester & nylon yarns

Products application:

Narrow Fabrics, Hosiery, Innerwear & Sportswear

Threads

Industrial Yarns

Nylon 66:

Pilot plant set up at Silvassa facility

India:

Silvassa: 2 manufacturing facilities; capacity 11,900 TPA

Vapi: In-house dyeing plant Capacity 3,200 TPA

Wind mills with capacities in Satara (2MW), Sangli (4MW) & Vapi (1.25 MW)

USA:

Plant set up in South Carolina in 2013; capacity 30 tons per day

Europe & South America:

Marketing offices in Portugal commenced in 2009

Last 10 years CAGR:

Revenue: 13%

EBITDA: 15%

PAT: 15%

~18% EBITDA margin consistently

Operating cash flows prudently deployed back into the business

For enhanced productivity and efficiency

Key Milestones

6

1997

2004

2007

2013

2009

2006

1999

1996

2016

Setup 100% US subsidiary - SarlaFlex LLC,(South Carolina) for the markets of USA and neighbouring countries Pilot Plant for Nylon 66 high tenacity yarn

Established an in-house dyeing plant in Vapi broadening the product offering to dyed yarns.

Started with value added products : Air Covered, Rubber/Spandex Yarns

1st overseas JV Savitex S.A. de C.V. in Honduras, Central America

Established Marketing subsidiary in Portugal, Sarla Europe LDA

SarlaFlex LLC commenced operations

Expanded Capacity by adding 2 new building units at Silvassa

Started as a 100% Export Oriented Unit (EOU) & Manufacturing unit at Silvassa for Polyester Textured, Twisted Yarn

Established 2nd manufacturing unit in Silvassa to house increasing production capacities

Introduced 2nd core product : Nylon Textured, Twisted and Dyed Yarn

1995

2005 High Tenacity Yarn Nylon 6 manufacturing unit started in Silvassa

2015 Raised Rs. 466.9 mn by Placing Equity Shares at premium of Qualified Institutional Buyers (QIBs)

2014

Liquid Assets of the Company crossed Rs. 1 bn Mark

Management Team

7

Mr. Mahendra Sheth CFO & Company Secretary

FCA, ACS, B Com and LLB from University of Mumbai 35 years of experience in the field of Accounts, Finance & Secretarial

Ms. Neha Jhunjhunwala Director

BMS from University of Mumbai & Master’s in Marketing & Strategy from University of Warwick, London

Currently involved in managing Business Development, Operations & HRD

Commerce graduate with more than 50 years of experience in cotton trading

Has been president of Bombay Cotton Merchants and Muccadams Association, Western Indian Chambers of Commerce and also the director of East India Cotton Association

Commerce Graduate from University of Mumbai with more than 25 years of experience in textile industry

Engaged in all aspects of Production, Planning, Marketing & Operations

Actively participates in the key financial decisions of the Company

Madhusudan Jhunjhunwala

Chairman & Whole Time

Director

Krishnakumar Jhunjhunwala

Managing Director & CEO

Shareholding Pattern

Shareholding as at September 2015

8

Promoters, 55.20% FII, 1.16%

DIIs, 15.87%

Public & Others, 27.77%

Organisation Structure

9

Board of Directors

Plant Head VP

(Sales) VP (Purchases) Admin/Legal CFO

HR Manager

Others*

MD/CEO

Heads Quality Control

Asst. Manager

Export Manager

Excise and Other

Manager Accounts

Manager Secretarial

Dispatch & Store Head

Dyeing Head, Twisting Head, Texturizing Head

Sales Manager

In charge of Overseas Subsidiaries

Overview Of Key Subsidiaries

10

SARLA PERFORMANCE

FIBERS LTD.

Sarla Overseas Holdings Ltd.

(SOHL) Sarla Flex INC, USA

Sarla Flex LLC

Sarla Europe LDA

Sarla Tekstil Filament Sanayi Ve Tic

MRK S.A. De C.V.

M/S Savitex S.A. De C.V.

Manufacturing POY from polyester chips, texturising & twisting

Manufacture of Dyed Yarn

Manufacturer of Nylon & Polyester Rubber / Lycra / Spandex Covered Yarn

Marketing Operations for Europe & South America Markets

Manufacturer of Polyester Textured Yarn, Twisted Yarn & Dyed Yarn

Note:- Management is in the process of winding up the JVs present in Honduras * Sarla’s share of the business

100% 100%

100% 60% *

45%*

40%*

33%*

Key Products

11

Bulklon

Sewing Thread, Furniture

Upholstery, Automotive

Upholstery, Narrow Fabrics and Tapes, Circular and Flat Knitted products

Narrow Fabrics and

Hosiery applications

Active Wear, Swim Wear, Narrow Fabrics, Tapes,

Hosiery, Undergarments,

Furniture Upholstery, Automotive Upholstery

Apparel, Swim wear, Lingerie, Fleece Goods,

Towels & Washcloths, Table Cloths,

Placemats, Sheets & Pillow Cases

POY (Partially Oriented Yarn) Lycra Spandex Rubber

Chips FDY (Fully

Drawn Yarn)

Silvassa South Carolina, USA

Narrow tapes, Hosiery, Lingerie,

Seamless Knit wear, Medical

Bandages, Knitted and Denim

fabrics

Automotive seat belts & trims,

air bags, upholstery, dress, casual &

athletic footwear, leather

goods, soft luggage

Key Raw Material

Location

End User

Industry

Textured Nylon Stretch Yarns

Textured Polyester Yarn

Textured Sewing Thread

Covered Yarn High Tenacity

Yarn

Covered Yarn 7%

High Tenacity Nylon, 8%

High Tenacity Polyester, 2%

Texturised Nylon, 15%

Twisted Nylon, 4%

Texturised Polyester 49%

Twisted Polyester, 15%

Fully Drawn Yarn, 0%

Product Mix (By Value)

Revenue Mix

Covered Yarn 11%

High Tenacity Nylon 9%

High Tenacity Polyester, 1%

Texturised Nylon 18% Twisted

Nylon 7%

Texturised Polyester

34%

Twisted Polyester

20%

Product Mix (By Volume)

Figures in INR 2013 2014 2015

Texturised Nylon 315 328 322

Twisted Nylon 375 425 392

Texturised Polyester 184 192 197

Fully Drawn Yarn - 368 370

Covered Yarn 7% High Tenacity

Nylon, 6%

High Tenacity Polyester, 1%

Texturised Nylon, 15%

Twisted Nylon, 4%

Texturised Polyester

46%

Twisted Polyester,

21%

Fully Drawn Yarn, 0%

2014 2015

The product mix has moved in favour of products (Texturised & Twisted Polyester and Nylon),

having higher realisation

Realisation per Kg.

12

Manufacturing Facility – India

Facility

2 Manufacturing facilities located in Silvassa, next to each other

Total Installed capacity – 11,900 TPA

Highlights

Product Offerings

Textured Polyester Yarns

Bulkon

Textured Nylon Stretch Yarns

Textured Sewing Thread

Covered Yarns

High Tenacity Yarns

In-house Dyeing facility at Vapi

Installed capacity – 3,200 TPA

Manufacturing Dyeing

Increased product offering to Dyed yarns

Large scale expansion, upgradation & modernisation undertaken in 2010

Being only 12 km from Silvassa facilitates movement of goods to quickly cater to customer orders

13

India Facility – Silvassa

External View of the Plant

Plant & Machinery

14

India Facility – Vapi

External View of the Plant

Plant & Machinery

15

Manufacturing Facility – Overseas

Manufacturing –South Carolina, USA

Manufacturing unit in Charleston, South Carolina which manufactures POY (Partially Oriented Yarn), Textured Polyester Yarn and Twisted Yarn

Total Installed capacity – POY and Textured Polyester Yarn 9,900 TPA each and Twisted Yarn 4,400 TPA

Phase I of project completed in December 2013 with a capital investment of USD 13.8 million

First Indian Textile company to set up a facility in the US

Product offering expanded into furnishings, automotive and industrial markets

This move is taken on the motive of CAFTA/NAFTA laws which are in favour of companies having manufacturing units set up in the region

Exporting to North and Central American countries is viable only for companies manufacturing in the region as they are waived off duties to the extent of 32%

H1FY15 H1 FY16

Production (lbs.)

Partially Oriented Yarn* 2,895,480 2,982,194

Textured Polyester Yarn 3,159,657 2,862,071

Twisted Yarn 2,165,158 929,555

Sales (lbs.)

Partially Oriented Yarn 204,651 50,083

Textured Polyester Yarn 1,009,070 1,285,941

Twisted Yarn 1,610,851 1,360,434

Sales (INR million)

Partially Oriented Yarn 0.01 0.01

Textured Polyester Yarn 14 18

Twisted Yarn 14 24

Charleston South Carolina

16

US Facility

External View of the Plant

Plant & Machinery

17

Table Of Contents

Company Overview

India Operations

Overseas Operations

Growth Plans

Financials

18

High-End Application products produced in India

19

Raw Materials Processes & Products Applications

Polyster POY

Nylon POY

Nylon Chips

High Tenacity Polyester Nylon 6

Texturising

Twisting

Extrusion

Twisting

Texturised Yarn

Twisted Yarn

Fully Drawn Yarn

Nylon 6 & Nylon 66

High Tenacity Nylon & Polyester

Lycra/ Spandex/ Rubber, Texturised Polyester / Nylon

Covering Covered Yarn

Threads, Hosiery, Elastics, Medical Bandages

Parachutes, Shoes, Seat Belts and Car Airbags

Fishing Nets, Twines ,Filter Fabrics & Industrial

Applications

Socks, Hosiery, Elastics, Innerwears

Facility Highlights • 2 facilities next to each other • Installed Capacity of 11,900 TPA • Can produce 250 different

varieties of Polyester & Nylon Yarn

Product Offering • Textured Polyester Yarn • Bulklon • Textured Nylon Stretch Yarns • Covered Yarns • High Tenacity Yarns

Manufacturing Facility - India

20

Silvassa Vapi

Facility Highlights • In-house dyeing facility • Installed Capacity of 3,200 TPA • State of the art technology • Computer shading matching and

developing new colours

Highlights • Increased product offering to

Dyed Yarn • Expansion, upgradation &

modernisation undertaken in 2010

12 KM distance between facilities

Wind Power Business

21

Efficient Wind Power Operations

Place Year Of

Commissioning Capacity (in MW)

Baradiya, Gujarat 2010 1.25

Satara, Maharashtra 2011 2.0

Sangli, Maharashtra 2012 4.0

Total Installed Capacity 7.25

Captive Use for Dyeing facility in Vapi

Agreement for Power Procurement with

private entities

• Increased utilization of wind turbines & sale of renewable energy certificates benefiting Power income

• Limited CAPEX requirement makes it a cash positive business

• CAPEX per MW ~Rs.6 crores

• Current plant load factor at ~23-25%

Profitable Wind Power Business

The Company has taken ECB loans for windmill projects. Exclusive charge of the windmill to the lending banks.

Funding

Table Of Contents

Company Overview

India Operations

Overseas Operations

Growth Plans

Financials

22

Overseas Subsidiaries

23

Entered in joint venture in 2009

Operates as a marketing subsidiary in Portugal

Services the customer requirements of European & South American Region

Entered in joint venture in 2010

Located at gateway to Europe catering to Turkish & European Markets

Subsidiary of the company -Sarla Performance Fibers Ltd

In 2013, SPFL entered US markets through SarlaFlex LLC

Installed capacity of 9,900 TPA for POY and 4,400 TPA for Twisted Yarn

Duty free benefits on goods manufactured inside the US as per NAFTA & CAFTA

Sarla Europe LDA, Portugal

Sarla Tekstil, Turkey

SarlaFlex LLC, USA Sarla Overseas Holdings Ltd. (SOHL)

60% 45% 100%

Manufacturing Facility - USA

24

Charleston, South Carolina

Highlights

Benefits

Current Capacity of 9,900 TPA

Commenced Production in Dec 2013

Products: Partially Oriented Yarn (POY) & Textured Polyester Yarn

First POY plant in USA since 1998

NAFTA & CAFTA treaties, allows waiver of duties upto 32% on synthetic garments manufactured in North or Central American region using US origin yarn when exported back into the United States

Proximity & Visibility to customers

Lower Logistics & Power

Lower Cost of Borrowing

Facility Details:

Land Cost of Rs 4 Crores to be paid over 7 years

Spread over 42 acres

Constructed area of 3.3 lakh sqft

USA: Strategic Location

~99% of the decision makers of textile industry with global brand presence are in the USA

Presence in USA builds confidence & helps develop business with large customers

Sarla is the only player in this sector to have manufacturing presence in USA & India

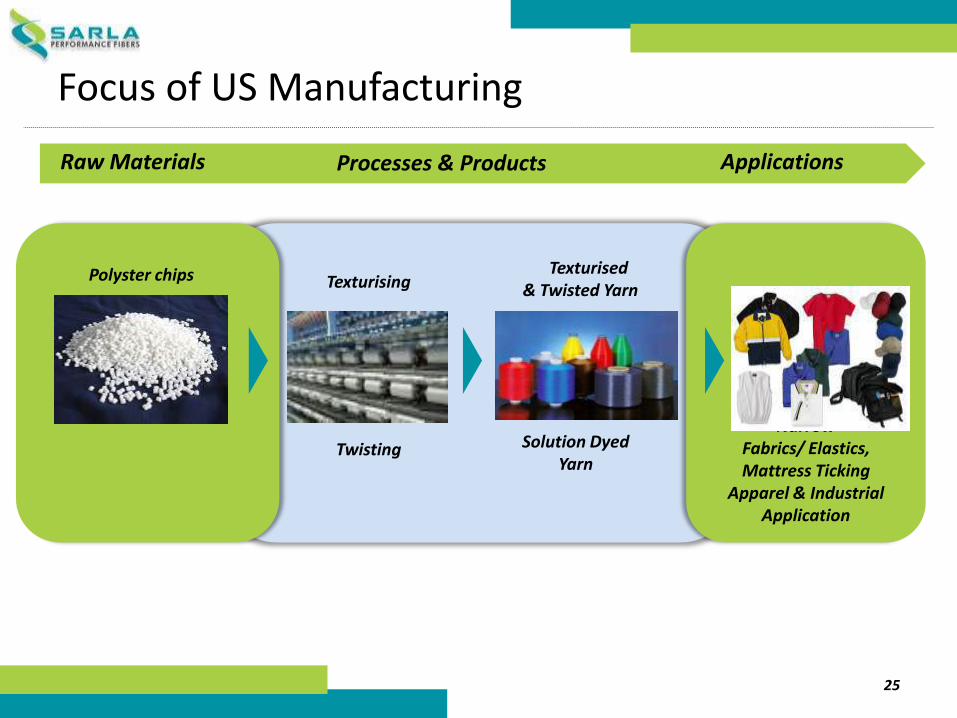

Threads, Hosiery , Narrow

Fabrics/ Elastics, Mattress Ticking

Apparel & Industrial Application

Focus of US Manufacturing

25

Polyster chips Texturising

Twisting

Texturised & Twisted Yarn

Solution Dyed Yarn

Raw Materials Processes & Products Applications

Opportunity in US Market

26

Higher realization

Greater visibility

Duty waiver

Demand boost

Competitive edge in the US

Legal restrictions As per NAFTA & CAFTA laws, American apparel companies can source

goods from US based manufacturers if they want their garment to have duty free access in the US market

Exporting to North and Central American countries is viable only for companies manufacturing locally in the regions as they are waved off duties to the extent of 35%

Sarla expects to gain tremendous impetus after operations stabilize and with a strong demand & marketing initiatives in place

Proximity and visibility to customer is expected to contribute significantly towards expanding and deepening customer relationships

Exporting low duty goods from India and manufacturing high duty goods in the US giving them a competitive edge

1 2 3 4 5

US Prices are 55 -70% higher than in Asia / Far East which enhances the profitability margins 6

Fiber Prices

Figures in Cents/ Kg. Jul-13 Sep-14 Sep-15

Polyester Fiber Prices

Asia / Far East

75 den textured 188-196 178-182 132-143

150 den textured 165-170 156-161 115-125

USA

70 den textured 322-366 140-163 127-151

150 den textured 282-317 122-141 112-130

West Europe

167 dtex texured 215-263 204-245 171-199

Nylon Fiber Prices

Asia / Far East

70 den 340-355 320-333 245-250

USA

40 den 785-807 365-380 365-380

70-200 den 597-762 260-340 245-315

For Polyester, the realisations in US and Europe are ~ 50 -70% higher than in India

For Nylon, the realisations in US and Europe are ~ 80-120% higher than in India

Source : PCI Fibres Report July 2014 27

Favourable Cost Structure in the US

Cost Component Unit India US Remarks

Raw Material % of Sales > 60% < 50% Raw Material cost as a % of sales is

lower in the US than in India

Labour $ / hr 1.5 15 Labour costs are higher in the US

than in India *

Electricity Rs. / Kwh 5 2.5 Electricity costs in the US are 50%

of the cost in India

Borrowing Cost % 13-15% p.a. 3-5%p.a. Borrowing cost in the US is one-

third of the cost in India

* Although labor costs are higher in the US, the high level of automation in the US facility will reduce the intensity of labour by over 30%

The savings in cost of raw materials, electricity and borrowing cost along with higher realisations in the US would result in higher profitability and return ratios. This will in turn be the key driver of the overall

profitability going forward

Source : Company 28

Global Presence

29

Table Of Contents

Company Overview

India Operations

Overseas Operations

Growth Plans

Financials

30

Growth Drivers

Optimization of US facility by increasing current capacity utilisation from the ~30% to

100% going forward

Expand the Installed capacity of the Partially Oriented Yarn from the current 9,900 TPA to

18,150 TPA by 2017

Set up manufacturing capability of Fully Drawn Yarn with an initial installed capacity of

1,980 TPA and gradually increase it to 3,960 TPA by 2017

Expansion of the Nylon 66 capacity at Silvassa from the current 1.5 TPD to 6 TPD with an

incremental capex of ~ INR 100 million

Cater to sectors like Automobiles which requires enhanced applications of specialised

yarn in headliners and others

Targeting an increased wallet share from the existing customers

31

Nylon 6,6 in India – to breakthorugh with existing key customers and replace

current imports into India

Uniquely positioned to gain market share in both Polyester and Nylon fibers

through its global business strategy and product offering

Growing opportunity in the South American market through Portugal

subsidiary

Investments made to manufacture new products in India and US to cater to

the growing demand

With the prevalence of Technical Textiles for Industrial applications in India, the

demand drivers for company’s product would get further strengthened in next

few years

Opportunity in Other markets & India

32

US Facility – Expansion Plan

33

Further Expansion Of South Carolina Facility

Current capacity Capacity by 2017

Facility will directly cater to clients in North, South & Central American markets

POY

• The total cost of the project is USD~ 25 mn

• Cost of Phase I already incurred

9,900 TPA ~18,000 TPA

Expansion

Total

~11

Phase I

~25

Phase II

~14

Cost of Project (USD Million)

New Product addition – Flat Yarn

Any Further Update?

New Products – Nylon 66

Commenced trials production of Nylon 66 yarn at Silvassa in 2013 on pilot basis

Nylon 66 is high tenacity and lower shrinkage yarn product

Being a niche product on its own, extremely specialized hence margins are substantially higher

Product applications:

Parachutes, Shoes, Seat Belts & Car Airbags, Specialized Sewing Applications in Automotive, Shoes, Leather, Industrial Filters, Hoses

Installed Capacity of 450 TPA at a pilot stage in Silvassa

34

Only company in India to “manufacture” Nylon 66

End User Industries

Seat Belts

Parachutes

Filter Fabric

Air Bags

Sports Shoes

Entry Barriers

35

Yarn constitutes ~5% to total cost of final product; however a very crucial product, hence Premium paid for Quality & Consistency desired by Large Global Customers

Over 150 varieties of moulds

Moulds form an integral part of the final product

These are designed as per clients specifications to fit the varied machinery used by them in their plants in different geographies

Clients Stickiness towards Quality & Goodwill

Global brands demand consistent quality products across markets

Major overseas clients with long standing relationship built over the years

Multi Geography Presence

Only Indian company in the sector to have manufacturing presence in NAFTA & CAFTA regions

Manufacturing operations in US & India and Marketing offices in South America & Europe

Key Strengths

36

Consistent quality & wide range of products provided to customers across the geographies

Over 150 moulds based on specifications provided by customers

Focused on High Margin value added products: Specialised Polyester and Nylon Yarns

Amongst a few players globally catering to Specialised Yarns – Used in a variety of niche applications

One of the Largest Manufacturers of Covered Yarn in India

Effectively positioned to be a preferred supplier to global manufacturers in Eastern and Western Hemisphere

Only Indian company in this sector to have manufacturing presence in NAFTA and CAFTA regions

Manufacturing & Distribution hub in close proximity to demand centres globally

Extremely low leverage – India Textile business has ‘Zero‘ Long Term Debt

QIP raised 46.7 crores in 2014

Liquid Assets of Over Rs. 100 crores

Strong Balance Sheet

Product Innovations & Quality

Relationships with brands like Hanes Brands, Gildan, Renfro, American & Efird, Delta Galil, Coats & Jockey

Manufacturing presence in USA gives confidence to most of the major customers based out of USA

Strong Relationship with Worlds Largest Brands globally

Table Of Contents

Company Overview

India Operations

Overseas Operations

Growth Plans

Financials

37

38

Q2 FY2016 Highlights

Revenue of Rs. 816 mn, YoY growth of 2%

Revenue excluding US Operations were at Rs. 681 mn

Gross Profit of Rs. 518 mn, margin 65%

EBITDA of Rs. 234 mn, margin of 28%, impacted due to:

Capacity Utilization for the US Operations in the range of 30-35%

PAT of Rs.132 mn, YoY growth of 31%

PAT excluding US Operations at Rs. 210 mn

Cash PAT of Rs. 171 mn margin of 21%

Profitability Statement

39

Rs. In Millions Q2 FY16 Q2 FY15 YoY H1FY16 H1FY15 YoY

Revenues 816 801 1.82% 1616 1622 -0.43%

Raw Material 330 410 701 870

Manpower Cost 56 64 109 131

Other Operating Expenses 227 198 430 389

EBITDA 234 133 76% 422 272 55%

EBITDA Margin 29% 17% 26% 17%

Other Income 31 52 46 68

Depreciation 39 40 77 80

Interest 14 11 28 22

PBT 182 81 124% 316 171 84%

Tax 50 34 84 60

PAT 132 47 180% 232 111 109%

PAT Margin 16% 6% 14% 7%

Cash PAT 171 88 94% 310 191 62%

Cash PAT Margin 21% 11% 19% 11%

Consolidated Performance Highlights H1 FY16

40

801 816

Q2FY2016 Q2FY2015

+1.82%

Revenue EBITDA Cash PAT

Rs. in Million

133

234

Q2FY2015 Q2FY2016

+76.00%

88 171

+94.0%

Q2FY2016 Q2FY2015

1,622 1,616

2016 2015

-0.43%

Revenue EBITDA Cash PAT

237 422

+55.00%

2015 2016

191 310

2015

2016

+61.73%

Performance of US Operations H1 FY16

41

110 160

+46%

Q2FY2016 Q2FY2015

Revenue EBITDA Cash PAT

Rs. in Million

22

Q2FY2016 Q2FY2015

20

Q2FY2015 Q2FY2016

219 309

2016 2015

+40.60%

Revenue EBITDA Cash PAT

44

2016 2015

40

2016 2015

Consolidated P&L Statement

Figures in INR million FY11 FY12 FY13 FY14 FY15 1HFY16

Net Sales / Income from Operations 1,930 2,336 2,587 2,618 3,120 1,616

Growth 24.3% 21.0% 10.7% 1.2% 19.2% -0.4%*

EBITDA 359 345 476 467 496 376

EBITDA Margin (%) 16.1% 14.8% 18.4% 17.8% 15.9% 23.2%

Finance Charges (Net) 19 30 43 69 64 29

Depreciation 66 80 82 110 145 77

Profit Before Tax (PBT) 274 235 350 323 404 316

PBT Margin (%) 14.2% 10.5% 13.5% 12.3% 12.9% 19.6%

Provision for Taxes 49 46 71 100 123 84

Profit After Tax (PAT) 225 189 280 223 280 232

PAT (%) 11.7% 8.4% 10.8% 9.1% 9.0% 14.4%

Earning Per Share 32.42 27.22 40.25 39.93 36.93 27.84

Rounded off to the nearest million *over 1HFY15 42

Consolidated Balance Sheet

Figures in INR million FY11 FY12 FY13 FY14 FY15 1HFY16

(A) LIABILITIES

Shareholder’s funds

a) Capital 70 70 70 70 84 84

b) Reserves & Surplus 1,013 1,175 1,355 1,622 2,214 2,384

Shareholder's Funds 1,083 1,244 1,425 1,692 2,298 2,468

Loan Funds 457 624 1,048 2,033 2,375 2,524

Deferred Tax Liability 92 113 140 151 142 142

TOTAL LIABILITIES 1,632 1,981 2,612 3,876 4,815 5,134

(B) ASSETS

Fixed Assets 779 823 1,287 1,970 1,893 1,903

Investments - 15 28 548 576 769

Total Current Assets 1,270 1,566 1,768 2,116 3,108 3,402

Less : Current Liabilities 416 423 471 758 762 940

Net Current Assets 853 1,143 1,297 1,358 2,346 2,462

TOTAL ASSETS 1,632 1,981 2,612 3,876 4,815 5,134

43 Rounded off to the nearest million

Ratio Analysis

44

Key Ratios FY12 FY13 FY14 FY15 1HFY16

Debt-Equity Ratio 0.52 0.80 1.38 1.13 1.11

Long Term Debt-Equity Ratio 0.08 0.31 0.94 0.60 0.72

Current Ratio 1.56 1.53 1.50 1.49 1.70

Fixed Assets Ratio * 1.87 1.86 1.27 1.19 1.19

Inventory Ratio * 4.31 4.47 3.37 4.18 3.53

Debtors Ratio * 3.7 4.43 3.91 4.16 3.77

Interest Cover Ratio 7.9 8.06 6.50 7.35 12.10

PBIDTM (%) 14.77 18.40 20.54 18.94 26.10

PBITM (%) 11.33 15.22 16.48 14.46 21.32

PBDTM (%) 13.5 16.72 18.01 16.95 24.33

ROCE (%) * 15.72 17.47 13.53 10.51 10.31

RONW (%) * 16.25 20.96 17.81 14.00 19.45

Debtors Velocity (Days) * 99 80 93 88 97

Creditors Velocity (Days) * 78 40 67 73 85

* Annualised for FY16

Financials – Growth Story

45

2,227 2,587 2,629

3,168 3,231

+13%

2015 2014 2013 2012 2016*

332

468 478 544 843

2014 2012 2013

+15%

2015 2016*

189

280 321 209

463

2012 2015 2014

2013

1,244 1,425 1,692

2,297 2,699

2015 2013 2012 2014

+18%

Revenues EBITDA

Profit After Tax Networth

Rs. in Million *2016 Figures are Annualised

+15%

2016* 2016*

Working Capital Profile for H1 FY16

46

87 103

2015 2016

73 85

2015 2016

88 97

2015 2016

Inventory Days Creditor Days

Debtor Days Net Working Capital Days

102 115

2015 2016

Future Box

Cost of Project USD million Phase I Phase II Total Land 0.80 - 0.80 Building 1.00 1.00 2.00 Plant & Machinery 9.40 9.25 18.65 Total Plant & Machinery 11.20 10.25 21.45 Pre-Operative Expenses 1.10 2.00 3.10 Working Capital 1.50 5.00 6.50 Total Current Assets 2.60 7.00 9.60 Total Cost of Project 13.80 17.25 31.05

The Company plans to expand the Installed capacity of the Partially Oriented Yarn from the current 9,900 TPA to 18,150 TPA by 2017

It plans to set up manufacturing capability of Fully Drawn Yarn with an initial installed capacity of 1,980 TPA and gradually increase it to 3,960 TPA by 2017

Planned capex cost (revised) of Phase 2 is USD 17.25 million

Plant will directly cater to our clients in the North, South and Central America markets

Phase 2 - Expansion of Manufacturing facility – South Carolina, USA

The total cost projected is USD 31 million.

Cost for Phase 1 has already been incurred

Source : Annual Reports 47

Clientele

Customers

48

Figures in INR million Mar-13 % Mar-14 % Mar-15 % Relationship

179 7% 221 8% 234 8% 5 to 10 Years

180 7% 189 7% 198 7% > 10 Years

105 4% 153 6% 182 6% > 10 Years

127 5% 117 4% 107 4% < 5 Years

70 3% 108 4% 105 3.5% 5 to 10 Years

Total Contribution to Revenue 787 26% 787 29% 826 26%

Client Concentration & Tenor (1/2)

Revenue contribution by the TOP 5 customers in 2014

49

Client Concentration & Tenor (2/2)

Figures in INR million FY13 % FY14 % FY15 % Relationship

179 7% 221 8% 234 8% 5 to 10 Years

180 7% 189 7% 198 7% > 10 Years

105 4% 153 6% 182 6% > 10 Years

127 5% 117 4% 108 4% < 5 Years

70 3% 108 4% 105 4% 5 to 10 Years

299 12% 93 3% 78 3% 5 to 10 Years

29 1% 73 3% 104 3% < 5 Years

Regal Elastics 62 2% 62 2% 50 2% 5 to 10 Years

38 1% 59 2% 44 2% > 10 Years

31 1% 54 2% 42 1% < 5 Years

Total Contribution to Revenue 1,120 43% 1,128 42% 1,145 37%

Revenue contribution by the TOP 10 customers for 2014

50

Case Study – Renfro Corporation

Sarla has been the only supplier for Renfro India since 1995

Revenue contributed by Renfro India has been increasing year on year for Sarla

SarlaFlex Inc. plans to sell its products from the US facility to the parent company, the Renfro Corporation

Despite its track record in serving Renfro Corporation’s Indian subsidiary, Sarla has to follow the regular process for empanelment as it’s preferred supplier

Revenue Contribution ( INR Mn)

Mar-13 Mar-14 Mar-15

105 153 182

Getting empanelment / approvals from Global Customers like Renfro Corporation is a Huge Barrier to entry

India Success Story for Sarla….

…..has little correlation with credentials for supplying to US parent, Renfro Corporation

51

Quality Standards & Environment Consciousness

QUALITY POLICY Sarla Performance Fibers Ltd is committed to a policy of continuous improvement and shall strive for excellence in all its endeavours. Each individual and the whole team shall work towards total quality culture aiming for customer satisfaction to remain competitive in business.

OEKO TEX CERTIFIED

ENVIRONMENT CONSCIOUSNESS SPFL Green Policy

Wind Power as a source of Energy

52

53

For further information, please contact:

Company :

Sarla Performance Fibers Limited CIN: L31909DN1993PLC0000562596 Mr. Mahendra Sheth, CFO & Company Secretary [email protected] www.sarlafibers.com