sepmonitor iceland a-growing-ecosystem-full-of-potential...

TRANSCRIPT

SEP MONITORJUNE 2016

ICELAND: A GROWING ECOSYSTEM FULL OF POTENTIAL

SEP MONITORJUNE 2016

ICELAND:A GROWING ECOSYSTEM FULL OF POTENTIAL

SEP Monitor is published by Startup Europe Partnership (SEP)

About Startup Europe Partnership (SEP)

Established by the European Commission in January 2014 at the World Economic Forum in Davos, SEP is the first pan-European platform dedicated to transforming European startups into scaleups by linking them with global corporations. By participating in the SEP program, global companies can help this process via business partnerships and strategic and venture corporate investments, providing them with access to the best technologies and talents through procurement of services or products, corporate acquisition or “acqui-hiring”.

SEP is led by Mind the Bridge Foundation, a global organization based in Europe and United States, with the support of Nesta (the UK’s innovation foundation), Factory (an acceleration program and campus for tech companies of any stage, originating from Berlin), and Bisite Accelerator (Madrid/Salamanca).SEP is a Startup Europe initiative. Partners include Telefónica, Orange, BBVA (Founding), and Telecom Italia, Unipol Group, Microsoft and Enel (SEP Corporate Member), with the institutional support of the European Investment Fund/ European Investment Bank Group, London Stock Exchange Group, Cambridge University, IE Business School and Alexander von Humboldt Institute for Internet and Society.

For more info:

http://startupeuropepartnership.eu | @sep_eu

ICELANDA GROWING ECOSYSTEM FULL OF POTENTIAL

SEP MONITOR

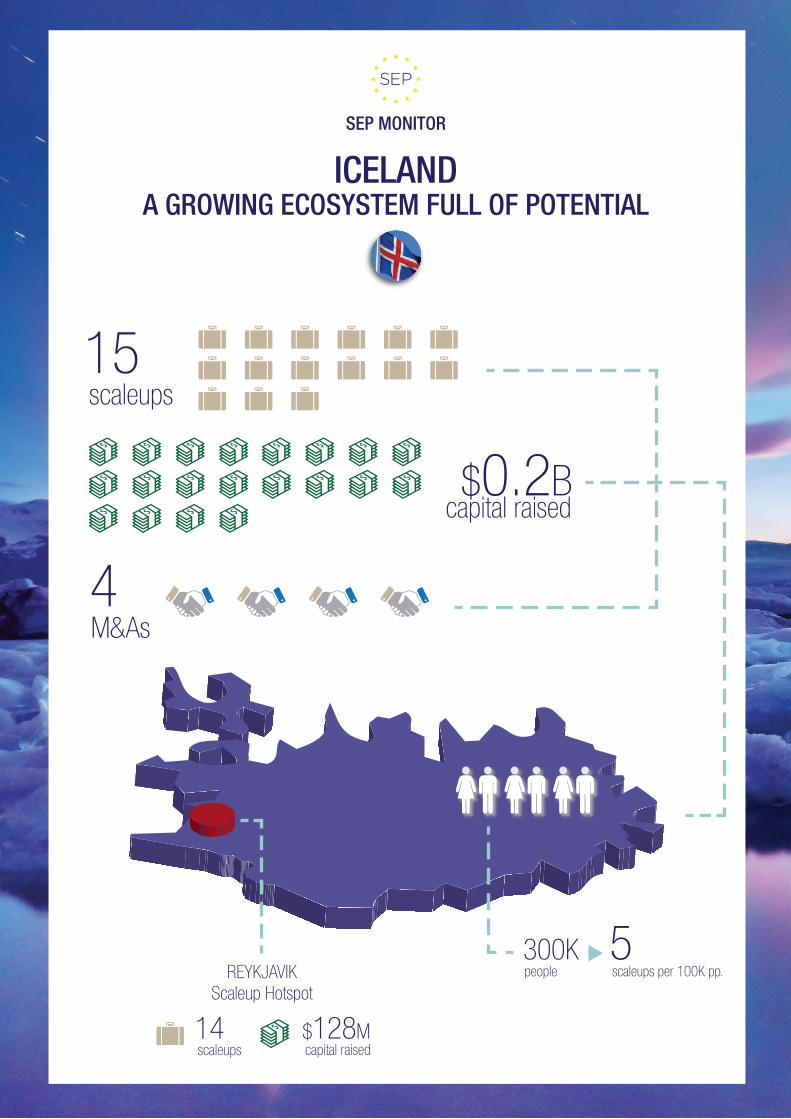

15scaleups

$0.2Bcapital raised

4M&As

REYKJAVIKScaleup Hotspot

14scaleups

$128Mcapital raised

300Kpeople

5scaleups per 100K pp.

INTRODUCTION

Our recent research confirms that the Nordic countries are without a doubt an innovation powerhouse in

Europe. In the Nordic region (Denmark, Finland, Iceland, Norway and Sweden), 430 scaleups have been able

to cumulatively secure over $6.5B in investments. That places the Nordics at a similar level of investment as

Germany.

Iceland is a relatively small and young scaleup ecosystem in Europe, but it seems quite effective in produc-

ing fast growing companies. SEP recorded 15 scaleups in Iceland, which raised around $200M combined. This

accounts for approximately 4% of all Nordic scaleups and 3% of capital raised. It might not seem like much, but

factoring in Iceland size (Iceland is around 1.5% of the population of the Nordics), these numbers are quite impres-

sive. Iceland has seen 5 scaleups for every 100,000 people, which is the highest ratio of the 11 European

countries we have analyzed so far.

Data about Icelandic startups and their funding from before 2015 are not easily available, since systematical

gathering of investment data for the Icelandic ecosystem wasn’t started before that time. That means there’s

some risk of missing data points in the report. One of Norðurskautið’s goals is to provide access to data about

the Icelandic startup scene, and with time, the data will become more detailed, reliable and accurate. Having

good data is important, especially when cross-border initiatives like the SEP reports are made and distributed, so

reports paint an accurate picture of the state of affairs.

That being said, Iceland shows potential and activity in the startup scene. We’ve seen several notable exits

in the last years, and increased interest from both Icelandic and international parties. Iceland has had more

capital available to startups in the last two years than ever before, and entrepreneurs are increasingly active

in raising money from outside the country as well. While Iceland may not be a globally recognized startup hub

yet, the ecosystem is definitely on its way there.

Guðbjörg Rist JónsdóttirHead of Research, Norðurskautið

Iceland: a relatively small and young scaleup ecosystem in Europe,but quite effective in producing fast growing companies.

I

SEP MONITOR - June 2016 - Iceland

Alberto OnettiChairman, Mind the BridgeCoordinator, Startup Europe Partnership

EDITOR NOTE

The current analysis is focused on Iceland and the other Nordic countries including Denmark, Finland, Norway and Sweden. International comparison is limited to France, Germany, Italy, Portugal, Spain and the United Kingdom. Scaleups and exits from other countries are not yet covered.

The current analysis is limited to ICT companies. Other key areas in the startup ecosystem, such as biotech/life science, hard-tech and cleantech, are currently under investigation and are not included.

SEP includes in the scaleup category startups that raised over $1 million (see Methodol-ogy for further details). This criterion may fail to consider startups that are scaling-up in a sustainable way (such as bootstrapped companies that grow organically and generate revenue and employment), although it includes startups that raised enormous seed investment while still in the “search phase.” Although the data fails to represent the complete scaleup landscape, we chose this methodology because it is the only one that allows an up-to-date “who’s who” of scaling-up in the various startup ecosystems. Furthermore, it is often not possible to report revenue and employment data (the real key variables to assess growth of a startup) as most cases are private companies, and data on those is simply not accessible in a timely manner in many countries.

SEP sources include public data (e.g. press articles, blogs), and direct information collected by investors and companies. The accuracy of our dataset is limited to the available information and disclosed data.

This Monitor has been realized with the active contribution of Norðurskautið.I’d like to thank them together with all the local investors and accelerators that contributed to the data collection and qualification.

II

Iceland shows potential and activity in the startup scene.

Bárðarbunga Volcano, September 4 2014, photo by Peter Hartree

ICEL

AND

1

KEY TAKEAWAYSIn the Nordic region we recorded 1.6 scaleups per 100,000 people.

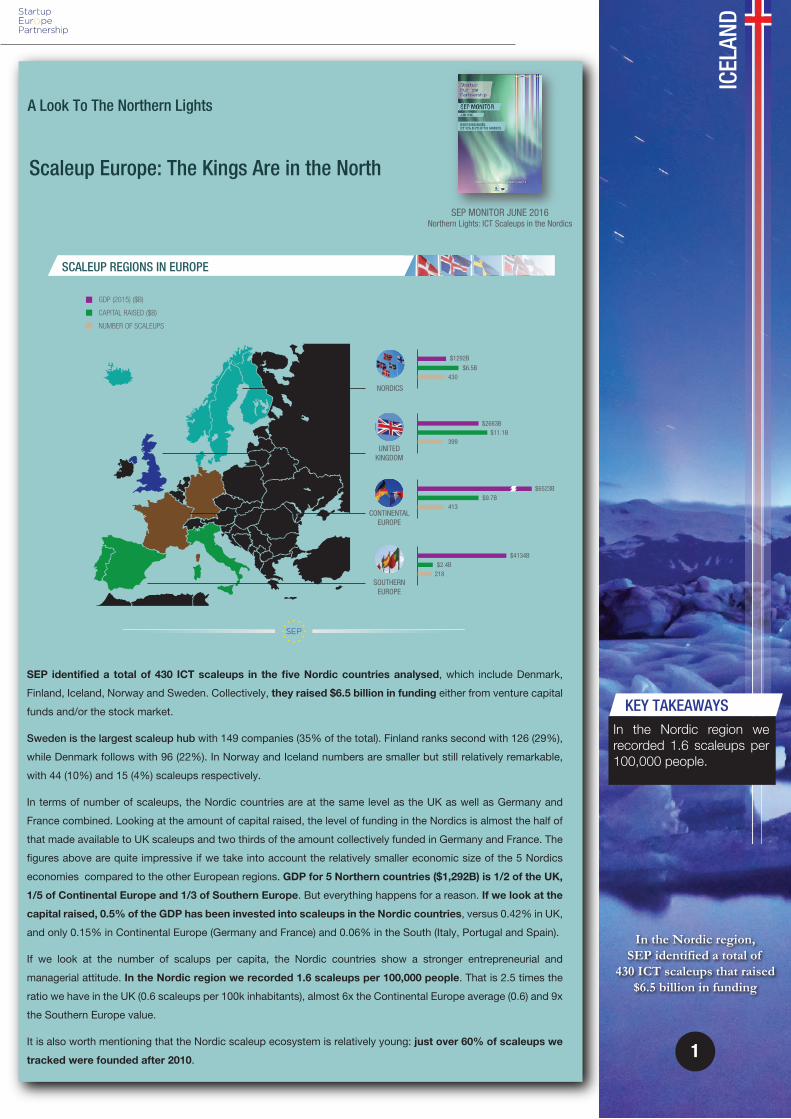

SEP identified a total of 430 ICT scaleups in the five Nordic countries analysed, which include Denmark,

Finland, Iceland, Norway and Sweden. Collectively, they raised $6.5 billion in funding either from venture capital

funds and/or the stock market.

Sweden is the largest scaleup hub with 149 companies (35% of the total). Finland ranks second with 126 (29%),

while Denmark follows with 96 (22%). In Norway and Iceland numbers are smaller but still relatively remarkable,

with 44 (10%) and 15 (4%) scaleups respectively.

In terms of number of scaleups, the Nordic countries are at the same level as the UK as well as Germany and

France combined. Looking at the amount of capital raised, the level of funding in the Nordics is almost the half of

that made available to UK scaleups and two thirds of the amount collectively funded in Germany and France. The

figures above are quite impressive if we take into account the relatively smaller economic size of the 5 Nordics

economies compared to the other European regions. GDP for 5 Northern countries ($1,292B) is 1/2 of the UK,

1/5 of Continental Europe and 1/3 of Southern Europe. But everything happens for a reason. If we look at the

capital raised, 0.5% of the GDP has been invested into scaleups in the Nordic countries, versus 0.42% in UK,

and only 0.15% in Continental Europe (Germany and France) and 0.06% in the South (Italy, Portugal and Spain).

If we look at the number of scalups per capita, the Nordic countries show a stronger entrepreneurial and

managerial attitude. In the Nordic region we recorded 1.6 scaleups per 100,000 people. That is 2.5 times the

ratio we have in the UK (0.6 scaleups per 100k inhabitants), almost 6x the Continental Europe average (0.6) and 9x

the Southern Europe value.

It is also worth mentioning that the Nordic scaleup ecosystem is relatively young: just over 60% of scaleups we

tracked were founded after 2010.

Scaleup Europe: The Kings Are in the North

A Look To The Northern Lights

SEP MONITOR JUNE 2016Northern Lights: ICT Scaleups in the Nordics

NORDICS

UNITEDKINGDOM

CONTINENTALEUROPE

SOUTHERNEUROPE

$6.5B430

$11.1B399

$9.7B413

$2.4B218

$6523B

$2663B

$1292B

$4134B

CAPITAL RAISED ($B)

NUMBER OF SCALEUPS

GDP (2015) ($B)

SCALEUP REGIONS IN EUROPE

In the Nordic region,SEP identified a total of

430 ICT scaleups that raised$6.5 billion in funding

96

126

15

44

149

15

$1.3B

$1B

$0.2B

$0.6B

$3.4B

$0.2B

$0.2BTHROUGH VC

$15MAVERAGECAPITAL RAISED

NUMBER OF SCALEUPS IN ICELAND

CAPITAL RAISED IN ICELAND

ICEL

AND SEP MONITOR - June 2016 - Iceland

2

A Small But Fast Growing Ecosystem

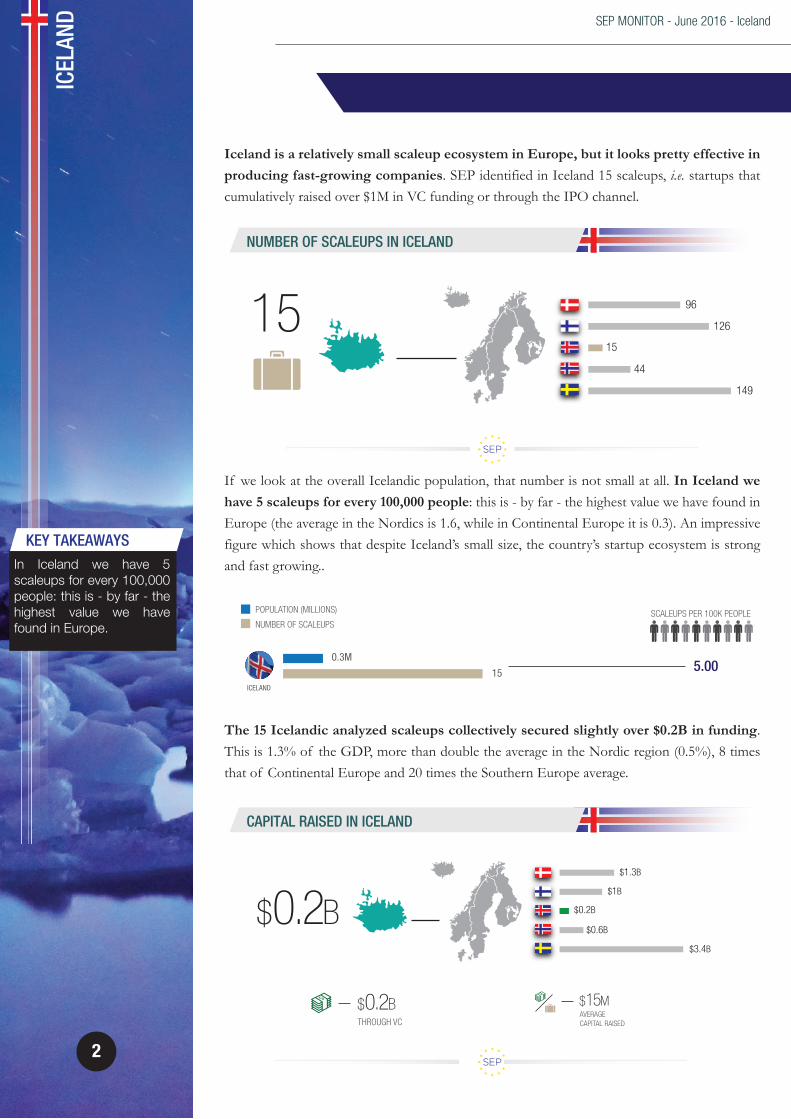

Iceland is a relatively small scaleup ecosystem in Europe, but it looks pretty effective in producing fast-growing companies. SEP identified in Iceland 15 scaleups, i.e. startups that cumulatively raised over $1M in VC funding or through the IPO channel.

The 15 Icelandic analyzed scaleups collectively secured slightly over $0.2B in funding. This is 1.3% of the GDP, more than double the average in the Nordic region (0.5%), 8 times that of Continental Europe and 20 times the Southern Europe average.

If we look at the overall Icelandic population, that number is not small at all. In Iceland we have 5 scaleups for every 100,000 people: this is - by far - the highest value we have found in Europe (the average in the Nordics is 1.6, while in Continental Europe it is 0.3). An impressive figure which shows that despite Iceland’s small size, the country’s startup ecosystem is strong and fast growing..

0.3M

15 5.00ICELAND

POPULATION (MILLIONS)

NUMBER OF SCALEUPSSCALEUPS PER 100K PEOPLE

KEY TAKEAWAYSIn Iceland we have 5 scaleups for every 100,000 people: this is - by far - the highest value we have found in Europe.

2010

2011

2012

2013

2014

2015

9

3

1

1

1

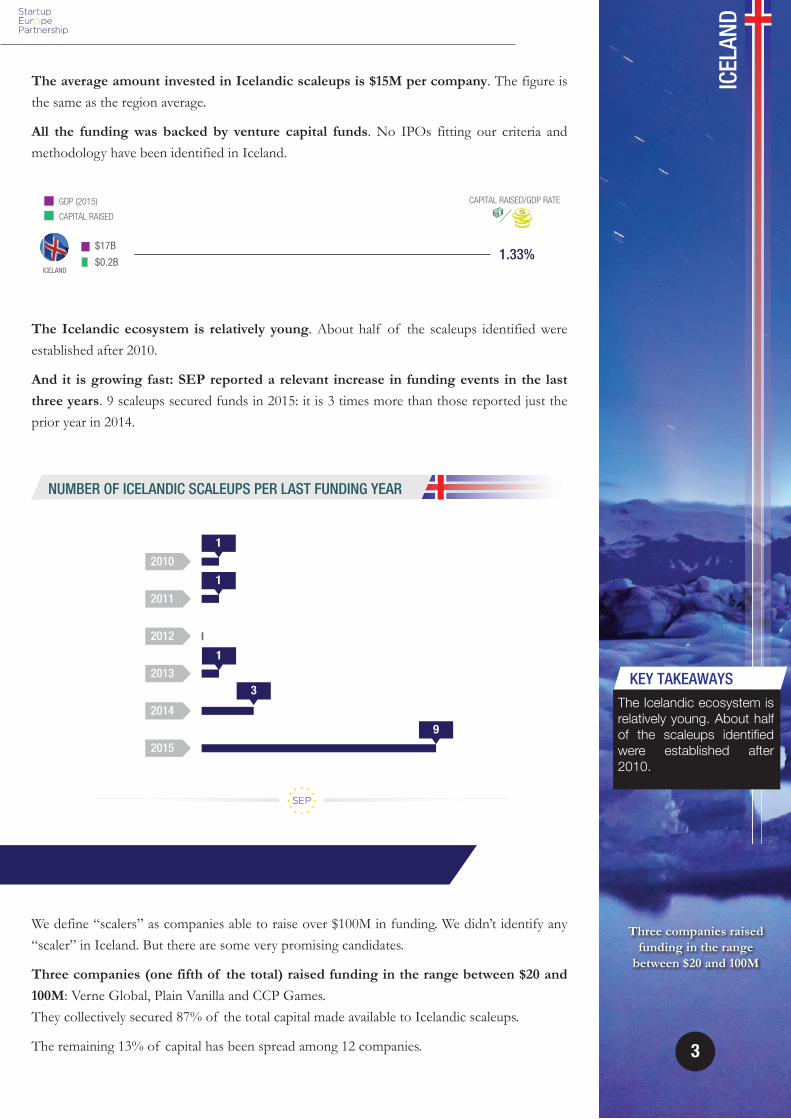

NUMBER OF ICELANDIC SCALEUPS PER LAST FUNDING YEAR

ICEL

AND

3

$17B

$0.2B1.33%

ICELAND

GDP (2015)

CAPITAL RAISED

CAPITAL RAISED/GDP RATE

The Icelandic ecosystem is relatively young. About half of the scaleups identified were established after 2010.

And it is growing fast: SEP reported a relevant increase in funding events in the last three years. 9 scaleups secured funds in 2015: it is 3 times more than those reported just the prior year in 2014.

No Icelandic Unicorns Spotted (Yet)

We define “scalers” as companies able to raise over $100M in funding. We didn’t identify any “scaler” in Iceland. But there are some very promising candidates.

Three companies (one fifth of the total) raised funding in the range between $20 and 100M: Verne Global, Plain Vanilla and CCP Games.They collectively secured 87% of the total capital made available to Icelandic scaleups.

The remaining 13% of capital has been spread among 12 companies.

The average amount invested in Icelandic scaleups is $15M per company. The figure is the same as the region average.

All the funding was backed by venture capital funds. No IPOs fitting our criteria and methodology have been identified in Iceland.

KEY TAKEAWAYSThe Icelandic ecosystem is relatively young. About half of the scaleups identified were established after 2010.

Three companies raisedfunding in the range

between $20 and 100M

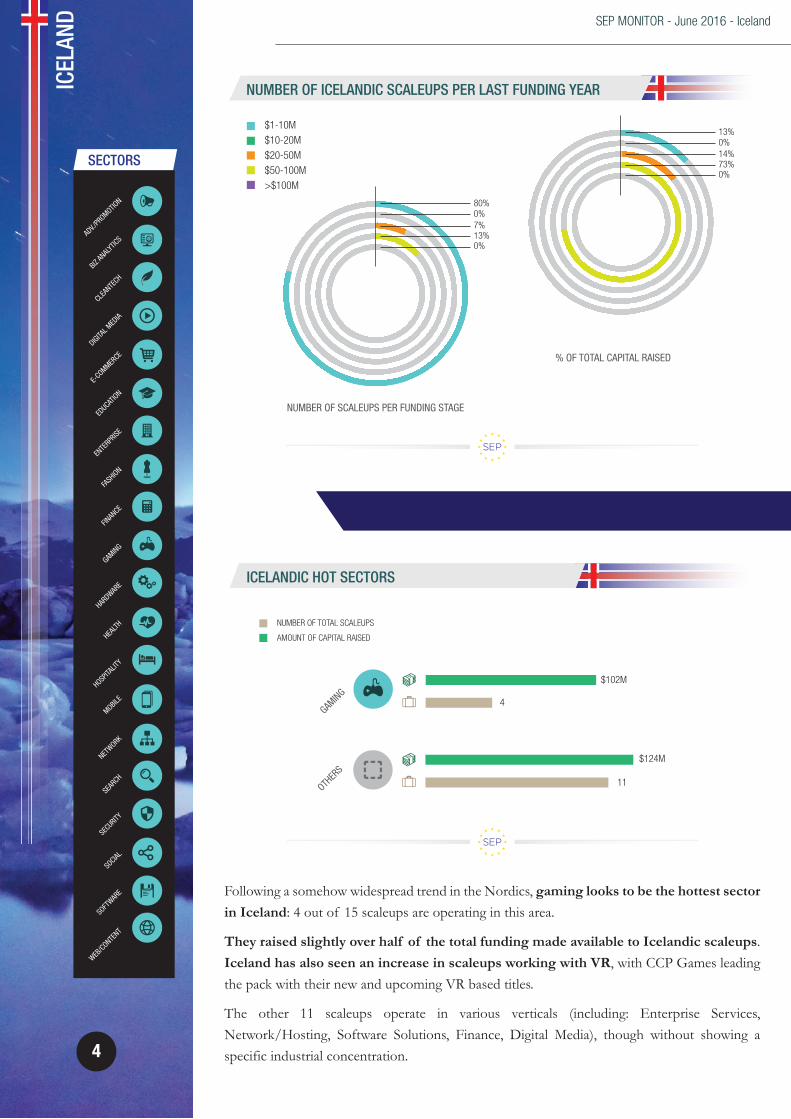

NUMBER OF ICELANDIC SCALEUPS PER LAST FUNDING YEAR

NUMBER OF SCALEUPS PER FUNDING STAGE

% OF TOTAL CAPITAL RAISED

$1-10M

$10-20M

$20-50M

$50-100M

>$100M

80%0%7%13%0%

13%0%14%73%0%

ICEL

AND SEP MONITOR - June 2016 - Iceland

4

Welcome to the VR (Virtual Reality) Valley

ICELANDIC HOT SECTORS

NUMBER OF TOTAL SCALEUPS

AMOUNT OF CAPITAL RAISED

4

$102M

GAMING

11

$124M

OTHER

S

Following a somehow widespread trend in the Nordics, gaming looks to be the hottest sector in Iceland: 4 out of 15 scaleups are operating in this area.

They raised slightly over half of the total funding made available to Icelandic scaleups. Iceland has also seen an increase in scaleups working with VR, with CCP Games leading the pack with their new and upcoming VR based titles.

The other 11 scaleups operate in various verticals (including: Enterprise Services, Network/Hosting, Software Solutions, Finance, Digital Media), though without showing a specific industrial concentration.

ADV./

PROMOTIO

N

WEB/CONTE

NT

BIZ AN

ALYT

ICS

CLEAN

TECH

DIGITAL M

EDIA

E-COMMER

CE

EDUCAT

ION

ENTE

RPRISE

FASH

ION

FINAN

CE

GAMING

HARDWAR

E

HEALT

H

HOSPITA

LITY

MOBILE

NETWORK

SEAR

CH

SECURITY

SOCIAL

SOFT

WARE

SECTORS

ICEL

AND

5

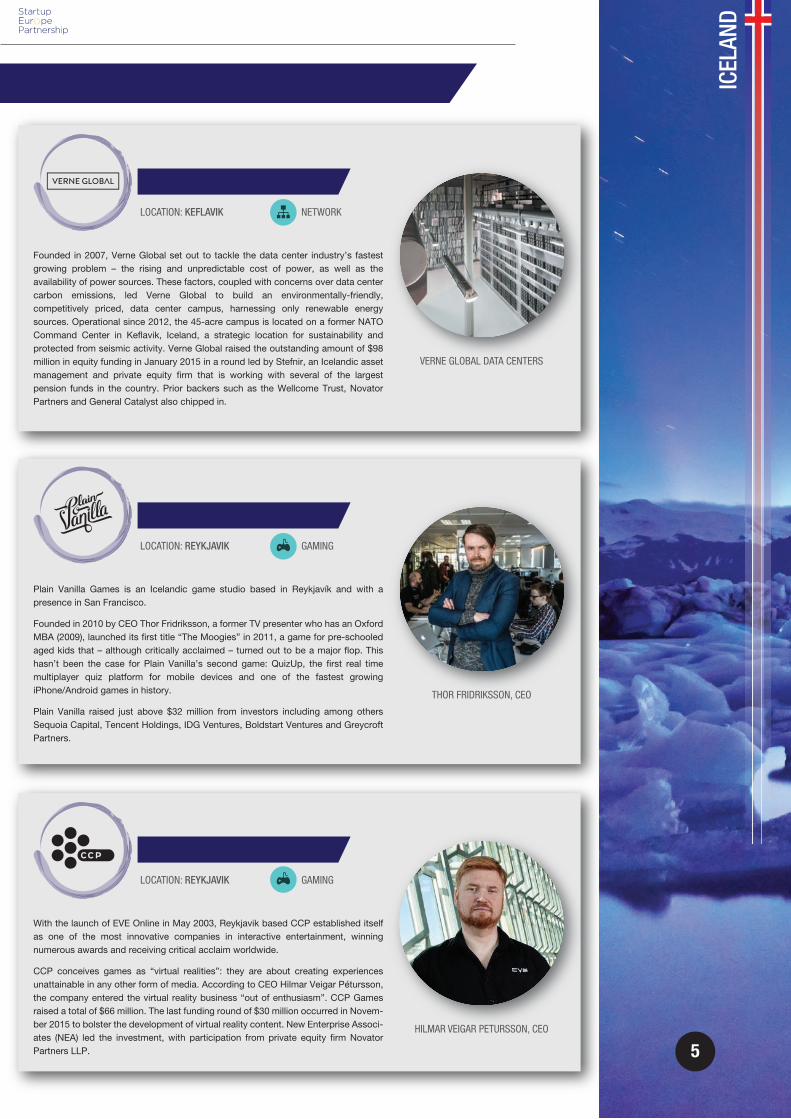

Plain Vanilla

GAMING

Plain Vanilla Games is an Icelandic game studio based in Reykjavík and with a presence in San Francisco.

Founded in 2010 by CEO Thor Fridriksson, a former TV presenter who has an Oxford MBA (2009), launched its first title “The Moogies” in 2011, a game for pre-schooled aged kids that – although critically acclaimed – turned out to be a major flop. This hasn’t been the case for Plain Vanilla’s second game: QuizUp, the first real time multiplayer quiz platform for mobile devices and one of the fastest growing iPhone/Android games in history.

Plain Vanilla raised just above $32 million from investors including among others Sequoia Capital, Tencent Holdings, IDG Ventures, Boldstart Ventures and Greycroft Partners.

THOR FRIDRIKSSON, CEO

LOCATION: REYKJAVIK

Verne Global

NETWORK

Founded in 2007, Verne Global set out to tackle the data center industry’s fastest growing problem – the rising and unpredictable cost of power, as well as the availability of power sources. These factors, coupled with concerns over data center carbon emissions, led Verne Global to build an environmentally-friendly, competitively priced, data center campus, harnessing only renewable energy sources. Operational since 2012, the 45-acre campus is located on a former NATO Command Center in Keflavik, Iceland, a strategic location for sustainability and protected from seismic activity. Verne Global raised the outstanding amount of $98 million in equity funding in January 2015 in a round led by Stefnir, an Icelandic asset management and private equity firm that is working with several of the largest pension funds in the country. Prior backers such as the Wellcome Trust, Novator Partners and General Catalyst also chipped in.

VERNE GLOBAL DATA CENTERS

LOCATION: KEFLAVIK

CCP Games

GAMING

With the launch of EVE Online in May 2003, Reykjavik based CCP established itself as one of the most innovative companies in interactive entertainment, winning numerous awards and receiving critical acclaim worldwide.

CCP conceives games as “virtual realities”: they are about creating experiences unattainable in any other form of media. According to CEO Hilmar Veigar Pétursson, the company entered the virtual reality business “out of enthusiasm”. CCP Games raised a total of $66 million. The last funding round of $30 million occurred in Novem-ber 2015 to bolster the development of virtual reality content. New Enterprise Associ-ates (NEA) led the investment, with participation from private equity firm Novator Partners LLP.

HILMAR VEIGAR PETURSSON, CEO

LOCATION: REYKJAVIK

Icelandic Scaleup Poster Children

ICT M&AS IN ICELAND

4M&As

51

48

4

23

79

ICEL

AND SEP MONITOR - June 2016 - Iceland

6

SCALEUP HOTSPOTS IN ICELAND

14

$128

M

1

$98M

REYKJAVIK KEFLAVIK

NUMBER OF SCALEUPS

AMOUNT OF CAPITAL RAISED

As expected, Reykjavik is the most relevant scaleup hotspot in Iceland. 14 out of 15 scale-ups all Icelandic scaleups are based in the capital city. The only scaleup located outside the capital Verne Global that is based in Keflavik.

Reykjavik Is the Icelandic Scaleup Hotspot

We tracked 4 ICT acquisitions in Iceland. This is a relatively small number, if compared with the total amount of exits in the Nordics (Icelandic M&As account only for 2% of total).

Main M&As for Icelandic Startups

KEY TAKEAWAYSReykjavik is the most relevant scaleup hotspot in Iceland.

We tracked 4 ICTacquisitions in Iceland

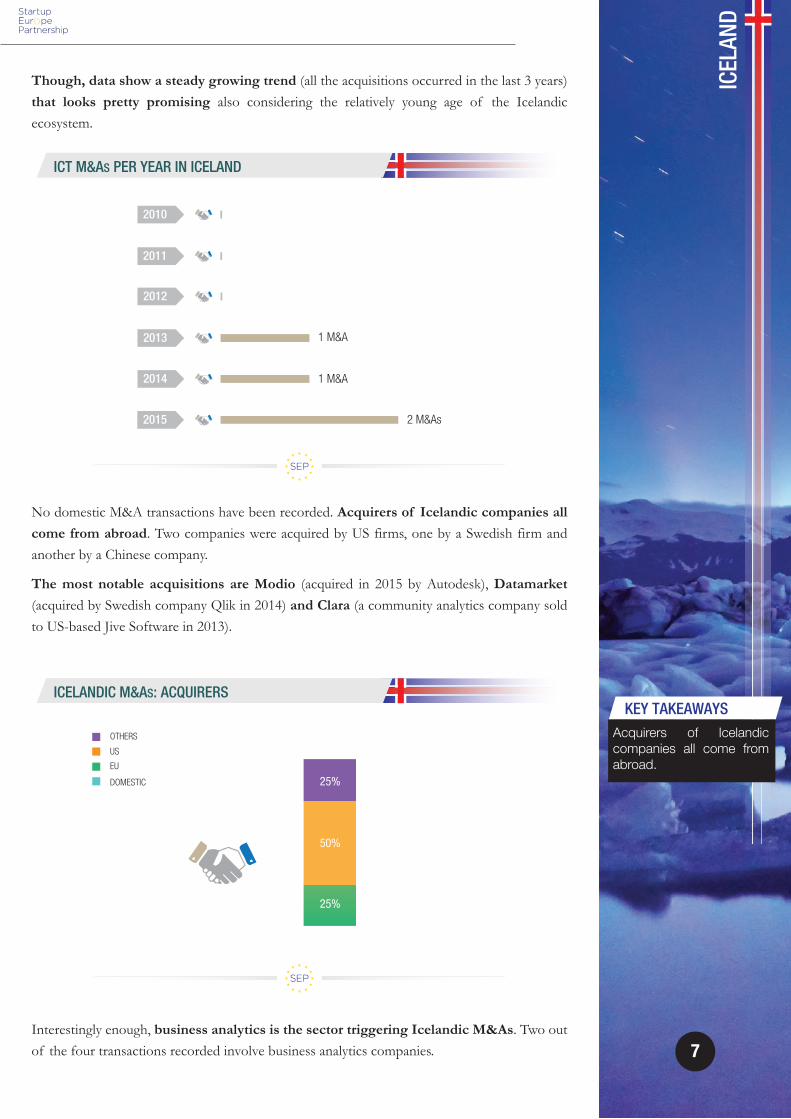

ICT M&AS PER YEAR IN ICELAND

2010

2011

2012

2013 1 M&A

2014 1 M&A

2015 2 M&As

Though, data show a steady growing trend (all the acquisitions occurred in the last 3 years) that looks pretty promising also considering the relatively young age of the Icelandic ecosystem.

ICEL

AND

7

No domestic M&A transactions have been recorded. Acquirers of Icelandic companies all come from abroad. Two companies were acquired by US firms, one by a Swedish firm and another by a Chinese company.

The most notable acquisitions are Modio (acquired in 2015 by Autodesk), Datamarket (acquired by Swedish company Qlik in 2014) and Clara (a community analytics company sold to US-based Jive Software in 2013).

25%

OTHERS

US

EU

DOMESTIC

50%

ICELANDIC M&AS: ACQUIRERS

Interestingly enough, business analytics is the sector triggering Icelandic M&As. Two out of the four transactions recorded involve business analytics companies.

25%

KEY TAKEAWAYSAcquirers of Icelandic companies all come from abroad.

ICELANDIC M&AS: HOT SECTORS

OTHERS

US

EU

DOMESTIC

2 M&As50%

50%

BUSINES

S ANAL

YTICS

ICEL

AND SEP MONITOR - June 2016 - Iceland

8

Top Icelandic M&As

Modio

Modio is an Icelandic startup delivering software solutions for 3D printing founded by Hilmar Gunnarsson,

who was a key person in the IT company OZ. At only 18 months old, it was acquired by US 3D design,

engineering and entertainment software giant Autodesk. The acquisition took place in March 2015 for an

undisclosed amount, leaving the company free to operate in Reykjavik where –in 2015- they ran the

company with a six-people staff. The main outcome of the operation is the rebranding of Modio’s software

under the new monicker “Tinkerplay”, a 3D design software joining Autodesk’s Tinkercad in a growing line

aimed at younger or inexperienced users of 3D software.

HILMAR GUNNARSSON, FOUNDER

ACQUIRED BY: Autodesk (US)LOCATION: ReykjavikM&A VALUE: undisclosedYEAR OF M&A: 2015

Datamarket is an Icelandic company specialized in analysis and virtual representation of data. It was

founded in Reykjavik in 2008 and has been sold to NASDAQ-registered software company Qlik, which

effectively acquired all shares in Datamarket for $13.5M (ISK 1.6B). This acquisition represents Qlik’s

increasing focus on data: an interesting turn for a rapidly growing organization with ore than $470M in

revenues in 2013 alone. Datamarket previously raised $1.2M from Icelandic fund Frumtak in August 2011. HJALMAR GISLASON, CEO

Datamarket

ACQUIRED BY: Qlik (SWE)LOCATION: ReykjavikM&A VALUE: $13.5MYEAR OF M&A: 2014

Clara is an Icelandic startup company founded by two college dropouts in 2008 devoted to the production

and distribution of community analytics tools for businesses that want to monitor and engage their

members on online platforms. CLARA uses advanced semantic analysis and data presentation methods

to automatically and instantly analyze attitudes, emotions, and user behavior online. The company, based

in Reykjavik, was acquired in Q2 2013 by San Francisco-based firm Jive Software for $9M. Its feature set

has since then effectively fit well in Jive’s business software portfolio.GUNNAR HOLMSTEINN, CEO

Clara

ACQUIRED BY: Jive Software (US)LOCATION: ReykjavikM&A VALUE: $9MYEAR OF M&A: 2013

KEY TAKEAWAYSBusiness analytics is the sector triggering Icelandic M&As.

Iceland: quite effective in producing fast growing companies.

Strokkur, Geysir Geothermal Field, Suðurland, Iceland, photo by Diego Delso

Iceland has seen an increase in scaleups working with VR,with CCP Games leading the pack.

“Iceland, glacier lagoon of Jokulsarlon with northern lights in the sky during september”, photo by Moyan Brenn

The SEP Monitor is based on the Startup Europe Partnership (SEP) mapping and scouting database that focuses on scaleups.SEP categorizes ICT companies as follows:

Startup:<$1M funding raised (since foundation) and at least one funding event since 2010.

Scaleup:>$1M funding raised (since foundation) and at least one funding event since 2010.

Scaler:>$100M funding raised (since foundation) and at least one funding event since 2010.

SEP categorization is based on capital raised (including both capital raised through VC and the stock market), not on valuation. An alternative methodology is the one used by The Wall Street Journal and Dow Jones Venture Source that are tracking venture-backed private companies valued at $1 billion or more (aka The Billion Dollar Startup Club or Unicorn Club). SEP considers:

Exit:Liquidity event that occurred since 2010.

M&A: For companies that exited via M&A, the valuation is the amount that the company got acquired for.

IPO:For companies that went public, the exit valuation is that on the day of the IPO.

Dual Companies:Startups founded in one country that relocated their headquarters – and with that part of their value chain – abroad, while maintaining a strong operational presence in their country of origin.

SEP Sources of information include the SEP database, portfolios of VC companies, corporate venture units, business angels, accelerators and active seed and early stage funds, crowdfunding platforms, tech competitions and events, and other relevant channels. Research is ongoing and results reported in the SEP Monitor are preliminary and cannot be considered as final. SEP welcomes research from everyone in the European startup ecosystem by providing data and indicating cases of scaleup companies and exits to be monitored.SEP Monitor is published by Mind the Bridge in collaboration with CrESIT.

SEP Methodology

III

With the support of:

Startup Europe Partnership - SEPSEP Monitor - No. 12 - June 2016First published in Belgium by Mind the BridgeCopyright © by Mind the Bridge

About Mind the BridgeFounded in 2007, Mind the Bridge is a Silicon Valley/European organization dedicated to developing, promoting, and supporting sustainable entrepreneurial ecosystems around the world and bridging them to the world’s most innovative center - Silicon Valley. Mind the Bridge offers a suite of programs and services (Startup School, Investors Program, Scaleup Mastery Program, Corporate Executive Program, Technology Scouting) with partnerships and operations in Europe, Asia, MENA, and LATAM.Mind the Bridge has also been chosen by the European Commission to drive “Startup Europe Partnership (SEP)”, the pan-European open innovation platform to connect startups to large corporates. It is also the host of Startup Europe Comes to Silicon Valley (SEC2SV), an intense week of activities in Silicon Valley for top EU scaleups, corporates and policy makers.

www.mindthebridge.comwww.startupeuropepartnership.eu@mindthebridge@sep_eu