senior seminar: systems of differential equations

DESCRIPTION

The research and paper behind the focus of my senior project: Systems of Differential Equations.TRANSCRIPT

1

Systems of Differential Equations

Joshua Dagenais

12-04-09

Mentor: Dr. Arunas Dagys

2

Table of Contents

Introduction

Section 1: Solving Systems of Differential Equations with Distinct Real Eigenvalues

Section 2: Solving Systems of Differential Equations with Complex Eigenvalues

Section 3: Solving Systems of Differential Equations with Repeated Eigenvalues

Section 4: Solving Systems of Nonhomogenous Differential Equations

Section 5: Application of Systems of Differential Equations – Arms Races

Section 6: Application of Systems of Differential Equations – Predator-Prey Model

Conclusion

References

3

Introduction

Many laws and principles that help explain the behavior of the natural world are

statements or relations that involve rates at which things change. When explained in

mathematical terms, the relations become equations and that rates become derivatives.

Equations that contain these rates or derivatives are called differential equations. Therefore,

systems of ordinary differential equations arise naturally in laws and principles explaining

behavior of the natural world involving several dependent variables, each of which is a function

of single independent variable. This then becomes a mathematical problem that consists of a

system of two or more differential equations. These systems of differential equations that

describe these laws or principles are called mathematical models of the process (Boyce &

DiPrima, 2001).

A system of first order ordinary differential equations is an interesting mathematical

concept as it combines 2 different studies of mathematics for its use. By dissecting the phrase,

system of first order differential equations, into 2 parts, the 2 different areas of mathematics used

to solve these equations can be found. In the system part of the phrase, it involves linear algebra

to solve the system of equations and in this case the system of equations consists of first order

differential equations. The ladder part of the phrase, first order of differential equations,

indicates that solution strategies for solving them will also be involved when solving systems of

differential equations.

So with linear algebra for systems and differential equations in mind, what other

underlying concepts and skills involved with these mathematical concepts must be learned and

explained to solve systems of differential equations? Well, for the linear algebra aspect of

4

solving systems of differential equations, topics that are to mentioned briefly in this paper

include matrices, characteristic equations, roots of the characteristic equations (eigenvalues),

eigenvectors, and the diagonalization of a matrix. For the differential equation part of solving

systems, topics that are discussed include solving first order differential equations, solving

simple diagonal systems ( 'y Dy ), and solutions of the original systems ( x Cy where

( ) atx t ke ). When everything mentioned is put together, solutions of different types are found

for systems of differential equations and with the help of mathematical software such as Maple,

graphs are able to visually represent the answers of these systems (slope fields) to show that

there are actually more than one solution called a family of solutions. Also, depending on the

types of eigenvalues that are found for the system of differential equations, different methods for

solving the systems will be used for eigenvalues that are distinct and real, eigenvalues that are

complex, and eigenvalues that are repeated, all of which graphically represented in a different

manner.

Along with different methods for solving systems of differential equations, methods for

solving homogenous and nonhomogenous systems will be explained to help further the scope of

this subject. Why do we care about solving systems of differential equations? Well, there are

many physical problems that involve a number of separate elements linked together in some

manner such as generic application problems which include spring-mass systems, electrical

circuits, and interconnected tanks that need solutions of systems of differential equations to be

understood and solved. Other, more advanced applications of the theory behind systems of

differential equations include the Predator-Prey Model (Lotka-Volterra Model) and the

Richardson’s Arms Race Model which connects mathematics with concepts that would have

never been able to be explained without such elegant mathematical equations. The Predator-Prey

5

Model is a system of nonlinear differential equations (even though it is considered an almost

linear system) and the Arms Race Model that uses systems of differential equations that are

nonhomogenous. Both models are very interesting applications that will be discussed and

explained later on in this paper. Hopefully, this paper will give the reader insight on what

systems of linear differential equations are, how to solve them, how to apply them, and how to

understand and interpret the answers that are derived from problems.

6

Section 1: Solving Systems of Differential Equations with Distinct Real Eigenvalues

In this section, we will be solving systems of differential equations where the eigenvalues

found from the characteristic equation are all real and all distinct. In order to do this, we will

first take the system

1 11 1 1 1

1 1

( ) ... ( ) ( )

( ) ... ( ) ( )

n n

n n nn n n

x p t x p t x g t

x p t x p t x g t

and write it in matrix notation. To do this, we write 1,..., nx x in vector form:

1

n

x

x

x

we put the coefficients 11( ),..., ( )nnp t p t in an n x n matrix:

11 1

1

( ) ( )

( )

( ) ( )

n

n nn

p t p t

P t

p t p t

we again write 1,..., nx x in vector form:

1

n

x

x

x

and write 1( ),..., ( )ng t g t in vector form:

7

1( )

( )

( )n

g t

g t

g t

Therefore, the resulting equation using the above vector and matrix notation is represented by

( ) ( )x P t x g t

We will first consider homogenous systems where ( ) 0g t , thus

( )x P t x

To find the general solution of the above system when ( )P t is a 1 x 1 matrix, the system above

reduces to a single first order equation

dxpx

dt

where the solution is ptx ce . Therefore, to solve any other systems with second order or

higher, we will look for solutions of the form

rtx e

where is a column vector instead of a constant c (because we are dealing with solutions to

more than one differential equation thus giving us multiple constants equating to a vector) and r

is an exponent to be solved. Substituting rtx e into both sides of ( )x P t x gives

( )rt rtr e P t e

Upon canceling rte , we obtain ( )r P t or

8

( ( ) ) 0P t rI

where I is the n x n identity matrix. In order to solve ( ( ) ) 0P t rI , we will use theorem 1.

Theorem 1: Let A be an n x n matrix of constant real numbers and let X be an n-dimensional

column vector. The system of equations 0AX has nontrivial solutions, that is, 0X , if and

only if the determinant of A is zero.

In our case, ( ( ) )P t rI is the n x n matrix represented by A and is the n-dimensional column

vector represented by X. Therefore, in order to find the nontrivial solutions of ( ( ) ) 0P t rI ,

we must take the determinant of ( ( ) ) 0P t rI which is represented

11 1

1

( ) ( )

0

( ) ( )

n

n nn

p t r p t

p t p t r

Computing the determinant will yield a characteristic equation, which resembles the structure of

a polynomial of degree n, where the roots of the characteristic equation, eigenvalues denoted by

r, will be computed. After the eigenvalues have been computed, r will be substituted back into

( ( ) ) 0P t rI and solved for the nonzero vector, , which is called the eigenvector of the

matrix ( )P t corresponding to the eigenvalue 1r . The eigenvector will be an n x 1 column vector

that will have as many values as there are equations to solve for. After finding the eigenvalues

and the eigenvectors for those specific values, they will be substituted back into the equation

rtx e

which will be represented as the following specific solutions

9

11 1

(1) ( )

1

( ) ( )

( ) ,..., ( ) ,...

( ) ( )

k

k

n nk

x t x t

x t x t

x t x t

for the initial system. If the Wronskian of (1) ( ),..., nx x (represented as (1) ( )[ ,..., ]nW x x ) does not

equal zero, then the general solutions can be represented as a linear combination of the specific

solutions

(1) ( )

1 ( ) ( )k

kx c x t c x t

The following examples will help illustrate how to solve n x n systems of differential equations

with distinct real eigenvalues. The general solution of the given system of equations will be

solved for along with a graph that shows the direction field of the answer.

Example 1: Solve the following 2 x 2 system for x

1 1 2

2 1 2

3 2

2 2

x x x

x x x

To solve the problem, we rewrite the equations into its matrix form

3 2

2 2x x

which is of the form

( )x P t x

where

10

3 2( )

2 2P t

We then find the eigenvalues of P(t) by finding the characteristic equation and solving for r.

Therefore,

23 2

det( ( ) ) 2 ( 1)( 2) 02 2

rP t rI r r r r

r

and the eigenvalues of P(t) are 1 1r and

2 2r . Now we compute the eigenvectors for each of

their respective eigenvalues. We will compute the nontrivial solutions of

1

2

3 20

2 2

cr

cr

For 1 1r

1 1 1 2

2 1

2 2 1 2

4 2 03 ( 1) 2 4 20 0 2

2 02 2 ( 1) 2 1

c c c cc c

c c c c

(Note that both of the resulting equations with 1c and

2c are the same). One such solution of the

equation is found by choosing 1 1c thus making

2 2c to give the eigenvector1

1

2

.

Knowing that ( ) ( )( ) nr tn nx t e , it follows that (1)

1

1( )

2

tx t c e

is a solution of the initial system.

For 2 2r

1 1 1 2

1 2

2 1 2

2 03 2 2 1 20 0 2

2 4 02 2 2 2 4n

c c c cc c

c c c c

11

By choosing 1 2c to solve the equation,

2 1c . Proper notation of eigenvectors, if possible,

insists that fractions should be avoided when representing the numerical value of the eigenvalue.

Therefore, for2 2r , 2

2

1

and a second solution is

(2) 2

2

2( )

1

tx t c e

Now, we check to see if we can represent 1x and

2x as a general solution by taking the Wronskian

of both specific solutions. The Wronskian of (1)( )x t and (2) ( )x t is

2

(1) (2)

2

2[ , ] 3

2

t t

t

t t

e eW x x e

e e

which is never equal to zero. It follows that the solutions (1)( )x t and (2) ( )x t are linearly

independent. Therefore, the general solution of the system ( )x P t x is

2

1 2

1 2( )

2 1

t tx t c e c e

12

All the general solutions (represented by the family of red lines), a combination of (1)( )x t and

(2) ( )x t , for which 1 0c and

2 0c , are asymptotic to the line 2 12x x . The blue trajectories

represent specific solutions to the system with each trajectory having a different initial value

(1 2(0) (0)x a and x b where a and b are any real number ).

For the remaining examples in this section, the derivation of the final solution will be

shown without all steps shown The purpose of these examples is to show the variety of systems

of differential equations that have distinct real eigenvalues such as a 3 x 3 system and a 2 x 2

system with initial conditions given.

Example 2: Solve the following 3 x 3 system for x

1 1 2 3

2 1 2 3

3 1 2 3

1 1 1

2 2 1 1

8 5 38 5 3

x x x x

x x x x x x

x x x x

First, we find the eigenvalues for the coefficient matrix by the following equation

1 1 1

det( ( ) ) 2 1 1 0

8 5 3

r

P t rI r

r

and solving the resulting characteristic equation.

>

13

>

Using maple yields the eigenvalues

1 2r , 2 2r , and

3 1r

and eigenvectors

1 2 3

4 0 3

5 , 1 , 4

7 1 2

The eigenvalues above are the same as the given Maple output but manipulated in properly

format where all values of the eigenvector are integers and the first value is positive. After the

eigenvalues and eigenvectors are computed, we find the Wronskian

(1) (2) (3)[ , , ] 12 0tW x x x e therefore we can substitute all the eigenvalues and eigenvectors

found into ( ) ( ) nr tn nx e and express the solution as a linear combination

(1) (2) (3) 2 2

1 2 3

4 0 3

( ) ( ) ( ) ( ) 5 1 4

7 1 2

t t tx t x t x t x t c e c e c e

Example 3: Solve the 2 x 2 system with initial conditions given for x

1 1 2 1

2 1 2 2

5 (0) 2 5 1 2 where where (0)

3 (0) 1 3 1 1

x x x xx x x

x x x x

14

We will start off the example by using Maple to find the eigenvalues and eigenvectors of the

coefficient matrix:

>

>

>

Therefore, 1 4r ,

11

1

, 2 2r , and

21

3

. The Wronskian (1) (2) 6[ , ] 2 0tW x x e

therefore the specific solutions (1)x and (2)x can be expressed as the general solution

4 2

1 2

1 1( )

1 3

t tx t c e c e

After the general solution has been found, we substitute 2

(0)1

x

into ( )x t to get

4*0 2*0

1 2 1 2

1 1 2 1 1 2(0)

1 3 1 1 3 1x c e c e c c

After the equation has been simplified, we multiply 1c and

2c by their respected vectors to yield

the follow system of equations

1 2 2c c and 1 23 1c c

15

We then solve the system of equations for 1c and

2c to get 1

7

2c and 2

3

2c

. Substituting

back into the general solution to get the specific solution of the system as

4 21 17 3

( )1 32 2

t tx t e e

The direction field of general solution along with a trajectory of the specific solution is

represented as

The above direction field shows the different families of solutions for the general solution

denoted by the red arrows and the blue trajectory represents the specific solution to the system

for when the initial starting value was 2

(0)1

x

. Now, after establishing the basis for solving

systems of differential equations, we will now delve into different cases of solving systems

where the eigenvalues are not real and/or distinct.

16

Section 2: Solving Systems of Differential Equations with Complex Eigenvalues

In this section, we will use what was previously discussed in the section for solving

systems with real and distinct eigenvalues on how to generate eigenvalues for an n x n system of

linear homogenous equations with constant coefficients denoted as

( )x P t x

Now if P(t) is real then the coefficients that make up the characteristic equation for r are real and

any complex eigenvalues must occur in conjugate pairs (Boyce & DiPrima, 2001, p. 384).

Therefore, for a 2 x 2 system, 1r a bi and

2r a bi would be eigenvalues where a and b are

real. Also, it follows that the corresponding eigenvectors are complex conjugate pairs of each

other. Therefore, 2 1r r and 2 1 . To help visualize this, take the equation that was formed

in the previous section

( ( ) ) 0P t rI

and substitute 1r and 1 into the equation to get

1

1( ( ) ) 0P t r I

which forms a corresponding general solution to the system. Now, by taking the complex

conjugate of the entire equation, the resulting equation becomes

1

1( ( ) ) 0P t r I

where P(t) and I are not affected by the conjugation because they both have all real values. The

equation then forms another corresponding general solution where 2 1r r and 2 1 . Now,

17

with the eigenvalues and eigenvectors solved for, we can use Euler’s formula to express a

solution with real and imaginary parts just as real solutions to the system. Euler’s formula states

cos sini te t i t

But, for use with general complex solutions to a system of differential equations, we will use the

a modified version of the formula

( ) (cos( ) sin( )) cos( ) sin( )i t t t te e t i t e t i e t

to find the real-value solutions to the system. We can choose either (1)( )x t or (2) ( )x t to find the 2

real-valued solutions because they are conjugates of each other and both will yield the same real-

valued solutions. Using (2) ( )x t and 2 a bi where a and b are real, then we have

(2) ( )( ) ( ) ( ) (cos( ) sin( ))i t tx t a bi e a bi e t i t

Factoring the above equation results in

(2) ( ) ( cos( ) cos( ) sin( ) sin( ))tx t e a t bi t ai t b t

and separating (2) ( )x t into its real and imaginary parts, (2) ( )x t will yield

(2) ( ) ( cos( ) sin( )) ( sin( ) cos( ))t tx t e a t b t ie a t b t

If (2) ( )x t is written as the sum of 2 vectors ( (2) ( ) ( ) ( )x t u t iv t ), then the vectors yielded are

( ) ( cos( ) sin( ))tu t e a t b t and ( ) ( sin( ) cos( ))tv t e a t b t

18

We can disregard the i in front of ( )v t because it is considered to be a multiplier of the vector

and we are only interested in the real-numbered vector solution. If we chose to solve for (1)( )x t

instead of (2) ( )x t , we would have gotten the same solution except (1)( ) ( ) ( )x t u t iv t . i is also

considered a multiplier of the ( )v t vector therefore we can disregard it and the answers for ( )u t

and ( )v t would be the same as the ones that were solved for above. ( )u t and ( )v t are the

resulting real-valued vector solutions to the system.

It is worth mentioning that ( )u t and ( )v t are linearly independent and can be expressed as

a single general solution. Therefore, for 1 2,r i r i and that

3,..., nr r are all real and

distinct. Let the corresponding eigenvectors be 1 2 3, , ,..., na bi a bi (Boyce &

DiPrima, 2001, p. 385). Then the general solution to systems of differential equations with

complex eigenvalues is

33

1 2 3( ) ( ) ( ) ... nr t r tn

nx t c u t c v t c e c e

where ( ) ( cos( ) sin( ))tu t e a t b t , ( ) ( sin( ) cos( ))tv t e a t b t , and P(t) consists of all

real coefficients. It is only when P(t) consists of all real coefficients that complex eigenvectors

and eigenvalues will occur in conjugate pairs (Boyce & DiPrima, 2001, p. 385). The following

examples will help illustrate how to solve n x n systems of differential equations with complex

eigenvalues. Both the complex and real-valued solutions will be given for each of the examples

and some direction fields will be shown to demonstrate the nature of systems with complex

eigenvalues.

19

Example 1: Solve the following 2 x 2 system for x

1 1 2

2 1 2

3 2 3 2

4 4 1

x x xx x

x x x

We will begin the example by using Maple to find the eigenvalues and eigenvectors of the

coefficient matrix:

>

>

>

Therefore, 1 1 2r i ,

2 1 2r i , 1

1

1 i

, and

21

1 i

. To get the eigenvectors in

proper form from the Maple output, we multiplied both eigenvalues (resulting from the Maple

output) by its conjugate to get a real number for the first value and then multiplied it again by 2

so that all values in the eigenvector were integers. The Wronskian (1) (2) 2[ , ] 2 0tW x x e i

therefore the specific solutions (1)x and (2)x can be expressed as the general solution in complex

form

(1 2 ) (1 2 )

1 2

1 1( )

1 1

i t i tx t c e c ei i

20

But, we want to be able to find the real-valued solutions of the complex general solution so we

will use (1)x to find the real-valued vectors. Therefore,

(1) (1 2 )1

( )1

i tx t ei

Using Euler’s formula, (1)x becomes

1(cos(2 ) sin(2 ))

1

te t i ti

After Euler’s formula has been applied, we factor the above equation

cos(2 ) sin(2 )

cos(2 ) sin(2 ) cos(2 ) sin(2 )

tt i t

et i t i t t

and separate the real and imaginary elements into

cos(2 ) sin(2 )

sin(2 ) cos(2 ) sin(2 ) cos(2 )

t tt t

e iet t t t

The result is the two real-valued solutions of the form ( ) ( )u t iv t where

cos(2 ) sin(2 )( ) and ( )

sin(2 ) cos(2 ) sin(2 ) cos(2 )

t tt t

u t e v t et t t t

Therefore, the general solution to the system with real-valued solutions is

1 2 1 2

cos(2 ) sin(2 )( ) ( ) ( )

sin(2 ) cos(2 ) sin(2 ) cos(2 )

t tt t

x t c u t c v t c e c et t t t

21

The resulting direction field showing families of solutions to the general solution to the system is

The blue trajectories show specific solutions when initial conditions are given. Thus, the

direction field creates spiraled solutions where the origin is the center of the spirals called a

spiral point. The direction of the motion is away from the spiral point and the trajectories

become unbounded. Also, the spiral point, for this particular solution, is unstable. There are

also systems with complex eigenvalues where the general solution has a spiral point that is stable

because all trajectories approach it as t increases.

Example 2: Solve for the following 3 x 3 system for x

1 1

2 1 2 3

3 1 2 3

1 0 0

2 2 2 1 2

3 2 13 2

x x

x x x x x x

x x x x

22

Again, we will begin the example by using Maple to find the eigenvalues and eigenvectors of the

coefficient matrix:

>

>

>

Thus, the eigenvalues are1 1r ,

2 1 2r i , and 3 1 2r i . The simplified eigenvectors are

1

2

3

2

, 2

0

1

i

, and 3

0

1

i

. Notice that 1r and 1 already contain real-values therefore

no computations are needed to turn them into real-valued solutions like the other complex

eigenvalues and eigenvectors. The Wronskian (1) (2) (3) 3[ , , ] 4 0tW x x x e i therefore the

specific solutions (1)x , (2)x , (3)x and can be expressed as the general solution in complex form

(1 2 ) (1 2 )

1 2 3

2 0 0

( ) 3

2 1 1

t i t i tx t c e c i e c i e

To find the real-valued solutions of the general solution, we will use (2) ( )x t and Euler’s formula

in the following equations

23

(2) (1 2 )

0 0 0 0

( ) (cos(2 ) sin(2 )) cos(2 ) sin(2 )

1 1 sin(2 ) cos(2 )

i t t t tx t i e i e t i t e t ie t

t t

Therefore,

0 0

( ) cos(2 ) and ( ) sin(2 )

sin(2 ) cos(2 )

t tu t e t v t e t

t t

and the general solution to the system with real-valued solutions is

1

1 1 2 3 1 2 3

2 0 0

( ) ( ) ( ) 3 cos(2 ) sin(2 )

2 sin(2 ) cos(2 )

t t tx t c r c u t c v t c e c e t c e t

t t

Now that we know how to solve systems that yield real and/or imaginary eigenvalues and

eigenvectors, we will now focus our attention on the next case if a eigenvalue is repeated when

found from the characteristic equation.

24

Section 3: Solving Systems of Differential Equations with Repeated Eigenvalues

In this section, we will be solving systems of differential equations where the eigenvalues

found from the characteristic equation are repeated. We will still be finding solutions of the

following equation

( )x P t x

and will still find at least one of the eigenvalues/eigenvectors in the way we previously solved

systems with distinct eigenvalues. But, when solving for the other repeated eigenvalue, we will

see that the other solution will take the form

rt rtx te e

where and are constant vectors. After finding the first solution of the form (1) 1( ) rtx t e , it

may be intuitive to find a second solution to the system of the form

(2) 1( ) rtx t te

because of how repeated roots are solved when finding the solution to a second order differential

equation. Substituting that back into ( )x P t x yields

1 1 1 1 1 1 1( ) ( ) 0 1 ( ) 0rt rt rt rt rt rt rtr te e P t te r te e P t te e rt P t t

But, for the equation to be solved so it is satisfied for all t, the coefficients of rtte and rte must

each be zero (Boyce & DiPrima, 2001, p. 403). Therefore, we find out that in this case, 1 0

and thus 2 1 rtx te is not a solution for the second repeated eigenvalue. But, from

25

1 1 1( ) 0rt rt rtr te e P t te ,

we see that there is a form of rtx te in the substituted equation along with another term of the

form rte . Therefore, we need to assume that

2 1 rt rtx te e

Where and are constant vectors. Substituting the above expression into ( )x P t x gives

1 1 1 1 1 1( )( ) ( ) ( )( )rt rt rt rt rt rt rt rt rtr te e r e P t te e r te r e P t te e

Equating the coefficients of rtte and rte gives the following conditions

1 1 1 1 1( ) 0 ( ) 0 ( ( ) ) 0rt rtP t te r te P t r P t rI

1 1 1( ) 0 ( ) ( ( ) )rt rt rtP t e e r e P t r P t rI

for the determination of 1 and . The underlined portions are the important conditions derived

from the equation. To solve 1( ( ) ) 0P t rI , all we do is solve for one of the repeated

eigenvalue and eigenvector just like in previous sections. We will solve a matrix equation of the

form

1 1

11 1 1 1 11 1 1 1

1 1

1 1 1

( ) ( ) ( ) ( )

( ) ( ) ( ) ( )

n n n

n nn n n n nn n n

p t r p t p t r p t

p t p t r p t p t r

Solving for 1,..., n in the above equation will result in the solution of the vector denoted

26

1

n

After equating 1 and , we substitute them into (2) ( )x t to get the second specific solution

2 1( ) rt rtx t te e

The last term in the above equation can be disregarded because it is a multiple of the first

specific solution (1) 1( ) rtx t e but the first 2 terms make a new solution of the form

(2) 1( ) rt rtx t te e

Finding (1) (2)[ , ]( ) 0W x x t will prove that (1) (2) and x x are linearly independent thus allowing us

to represent the a general solution to the system in the form

11 1 1(1) (1) ( ) 1 1 1

1 2 1 2( ) ( ) ( ) [ ] ... kr tr t r t r tk k

k kx c x t c x t c x t x c e c te e c e

where (1) (2) and x x include the repeated eigenvalues of multiplicity 2.

For the sake of simplicity, we will focus our examples on solving systems that have

repeated eigenvalues of only multiplicity 2. Also included in one of the examples is a case

where a repeated eigenvalue give rise to linearly independent eigenvectors (which is easily

identifiable using Maple) of the matrix ( )P t thus avoiding the complications of solving systems

with repeated eigenvalues.

27

Example 1: Solve the following 2 x 2 system for x

1 1 2

2 1 2

4 4 1

4 8 4 8

x x xx x

x x x

We will begin the example by using Maple to find the eigenvalues and eigenvectors of the

coefficient matrix:

>

>

>

Notice in the resulting eigenvectors that 2

0

0

which is a zero multiple of 1 and does us no

help in finding the second specific solution of the above system. But, the results derived from

Maple gives us 1 2 6r r ,

11

2

, and (1) 6

1( )

2

tx t e

. We need to use the equation

(2) 1( ) rt rtx t te e

to solve for and thus have a second specific solution to the system. To find out the second

specific solution, we substitute (2) 6 6

1( )

2

t tx t te e

into 4 1

4 8x x

to get the following

expression

28

1 16 6 6 6 6

2 2

1 1 4 1 1 4 16 6

2 2 4 8 2 4 8

t t t t te te e te e

Multiplying out 64 1 1

4 8 2

tte

and factoring out a 6 from the result yields

1 16 6 6 6 6

2 2

1 1 1 4 16 6 6

2 2 2 4 8

t t t t te te e te e

Canceling out the 6

16

2

tte

on each side of the equation and rearranging the equation yields

1 16 6 6

2 2

4 1 16

4 8 2

t t te e e

Factoring out 1 6

2

te

on the left side of the equation and simplifying gives us

1 6 6

2

1 6 6

2

1

2

4 1 16

4 8 2

4 1 6 0 1

4 8 0 6 2

2 1 1

4 2 2

t t

t t

I e e

e e

The end product of the above expression,1

2

2 1 1

4 2 2

, is of the form 1( ( ) )P t rI .

In this case

29

14 1 6 0 1

( ( ) )4 8 0 6 2

P t rI

Thus, to solve for , we solve

1 1 2

1 2

2 1 2

2 12 1 1 00 and 1

4 2 24 2 2 1

(Note that both of the resulting equations with 1 and

2 are the same). After solving for , we

substitute it into (2) 1( ) rt rtx t te e to find the second solution of the system to be

(2)1 0

( )2 1

rt rtx t te e

The Wronskian (1) (2) 12[ , ] 0tW x x e . Therefore the specific solutions (1)x and (2)x can be

expressed as the general solution

6 6

1 2

1 1 0( )

2 2 1

t tx t c e c t e

The resulting direction field showing families of solutions to the general solution to the system is

30

The blue trajectories show specific solutions when initial conditions are given. The origin is

called an improper node. If the eigenvalues are negative, then the trajectories are similar but

traversed in the inward direction. An improper node is asymptotically stable or unstable,

depending on whether the eigenvalues are negative or positive (Boyce & DiPrima, 2001, p. 404).

Example 2: Solve the following 3 x 3 system for x

1 1 2 3

2 2 3

3 3

2 1 2 1

0 1 1

0 0 22

x x x x

x x x x x

x x

We will begin the example by using Maple to find the eigenvalues and eigenvectors of the

coefficient matrix:

>

31

>

>

From the Maple results: 1 2 1r r ,

3 2r , 1

1

( ) 0

0

tx t e

, and 3 2

1

( ) 1

1

tx t e

. What we need to

find is the specific solution to (2) ( )x t . In this example, we will use the equation 1( ( ) )P t rI

to solve for , substitute it into (2) 1( ) rt rtx t te e , and use the shortcut to find out the third

specific solution to the system. Therefore

1

1

2

3

1

2

3

1 2 1 1

( ( ) ) 0 1 1 1 0

0 0 2 0

0 2 1 1

0 0 1 0

0 0 1 0

t t

t t

P t rI I e e

e e

and

2 3

3 1 2 3

3

02 1

1 10 0, , 0

2 20

0

32

Substituting what we found for into (2) 1( ) rt rtx t te e yields

(2)

01 2 0

1( ) 0 0 1

20 0 0

0

t t t tx t te e te e

The Wronskian (1) (2) (3) 4[ , , ] 0tW x x x e . Therefore, the specific solutions (1) (2) (3), ,x x and x can

be expressed as the general solution

2

1 2 3

1 1 2 0

( ) 1 0 0 1

1 0 0 0

t t tx t c e c e c t e

Example 3: Solve the following 3 x 3 system for x

1 2 3

2 1 2 3

3 1 2 3

3 0 1 3

2 3 3 2 3 3

2 1 12

x x x

x x x x x x

x x x x

For this example, using Maple can unlock a potential shortcut in solving for the general solution

to the above system. Again, we will begin the example by using Maple to find the eigenvalues

and eigenvectors of the coefficient matrix:

>

>

33

>

Unlike the other 2 examples, the Maple output displays 2 linearly independent eigenvectors of

the repeated eigenvalues2 3 2r r . Another shortcut for finding eigenvectors of repeating

eigenvalues is found if a math program, such as Maple, is utilized to solve systems of differential

equations. Therefore

1 2 2 2 3 2

1 1 3

( ) 1 , ( ) 2 , ( ) 0

1 0 2

t t tx t e x t e x t e

and the general solution to the system is

2 2

1 2 3

1 1 3

1 2 0

1 0 2

t tx c e c c e

A more advanced look at systems with repeated eigenvalues would include repeated

eigenvalues with multiplicities higher than 2. The equations to solve higher multiplicities of

repeated eigenvalues become more detailed and difficult to solve for but to find the eigenvalues

for such values, we would follow the same thought process in how we found the eigenvalue for

repeated eigenvalues of multiplicity 2. For the next section, we will return to our original form

34

of a differential equation 1 1( ) ... ( ) ( )n nx p t x p t x g t and solve nonhomogenous systems

where the value of ( ) 0g t .

35

Section 4: Solving Systems of Nonhomogenous Differential Equations

Unlike the previous sections where we solved different types of systems of homogeneous

differential equations with constant coefficients, this section will focus on solving systems of

nonhomogenous differential equations of the form

( ) ( )x P t x g t

The following theorem related to nonhomogenous systems should help us figure out

where to start solution process:

Theorem 2: If (1) ( )( ),..., ( )nx t x t are linearly independent solutions of the n-dimensional

homogenous system ( )x P t x on the interval a < t < b and if ( )px t is any solution of the

nonhomogenous system ( ) ( )x P t x g t on the interval a < t < b, then any solution of

the nonhomogenous system can be written (1) ( )

1 ( ) ( ) ( )n

k px c x t c x t x t for a unique

choice of the constants1,..., nc c (Rainville, Bedient, & Bedient, 1997, p. 199).

The theorem states that we will need to find a particular solution ( )px t and add it on to the

general solution of the homogenous system that is part of the nonhomogenous system. To do

that, we will be using a variation of parameters technique to find ( )px t and solve the equation

( ) ( )x P t x g t .

Solutions of the homogenous part of the nonhomogenous systems will take the form

11

1nr tr t n

nx c e c e

and using the variation of parameters technique suggests we seek a solution to the

nonhomogenous system to be

36

11

1( ) ( ) ( ) nr tr t n

p nx t c t e c t e

Direct substitution back into ( ) ( )x P t x g t yields

1 1 11 1 1

1 1 1 1( ( ) ( ) ) ( ( ) ( ) ) ( ( ) ( ) ( ) ( ) ) ( )n n nr t r t r tr t r t r tn n n

n n n nrc t e r c t e c t e c t e P t c t e P t c t e g t

( )P t multiplied by any eigenvalue found to be a part of the specific solution will result in that

particular eigenvalue multiplied by its eigenvector because it is already part of the solution to the

homogeneous system. Therefore

1 1 1

1

1 1 1

1 1 1 1 1

1

1

( ( ) ( ) ) ( ( ) ( ) ) ( ( ) ( ) ) ( )

( ( ) ( ) ) ( )

n n n

n

r t r t r tr t r t r tn n n

n n n n n

r tr t n

n

rc t e r c t e c t e c t e rc t e r c t e g t

c t e c t e g t

The resulting equation can be rewritten in matrix form as

11

1 1 1 1

1

( ) ( )

( ) ( )n

r tn

r tn

n n n n

c t e g t

c t e g t

To solve for 1( ),..., ( )nc t c t , we must use Cramer’s Rule to solve Ax b for x where

11

1 1 1 1

1

( ) ( )

, ,

( ) ( )n

r tn

r tn

n n n n

c t e g t

A x b

c t e g t

Cramer’s Rule states that the system has a unique solution that is given by

det( )1,...,

det( )

kk

Bx for k n

A

37

Therefore

1

1

1 1 1 1

1

1 1 1

1 1 1 1

1 1

( ) ( )

( ) ( )( ) ,..., ( ) n

n

n

n n n nr tr t

nn n

n n

n n n n

g t g t

g t g tc t e c t e

Thus,

1 1

1 1 1 1 1 1

1 1 1 1

( ) ( ) ... ( ) ( ) [ ( ) ... ( )]

( ) ( ) ... ( ) ( ) [ ( ) ... ( )]n n

r t r t

n n n n

r t r t

n n n n n n

c t e a g t a g t c t a g t a g t e

c t e b g t b g t c t b g t b g t e

for some arbitrary constants 1 1,..., and ,...,n na a b b . To solve for the general solution, integrate

both sides of the above equation to get 1( ),..., ( )nc t c t , substitute them into

11

1( ) ( ) ( ) nr tr t n

p nx t c t e c t e to find the particular solution, and substitute ( )px t into

(1) ( )

1 ( ) ( ) ( )n

k px c x t c x t x t to find the general solution for the system. The following

examples will help demonstrate how to solve systems of nonhomogenous differential equations

and lead into an application of nonhomogenous systems.

Example 1: Solve the following 2 x 2 system for x

1 2

2 1 2

0 1 0

2 3 32 3 3tt

x xx x

ex x x e

We will begin the example by using Maple to find the eigenvalues and eigenvectors of the

homogenous part of the system

38

0 1

2 3x x

Therefore

>

>

>

The resulting eigenvalues and eigenvectors are 1 2

1 2

1 11, 2, , and

1 2r r

. The

Wronskian (1) (2) 12[ , ] 0tW x x e thus, the general solution to the homogenous part of the system

is

2

1 2

1 1

1 2

t t

hx c e c e

To find the particular solution of the nonhomogenous part of the system, we will use the

variation of parameters technique to find a solution of the above equation of the form

2

1 2

1 1( ) ( )

1 2

t t

px c t e c t e

39

We will first substitute px for x and x directly into

0 1 0

2 3 3 tx x

e

to get the following

expression

2 2 2

1 1 2 2 1 2

2

1 1 2 2

1 1 1 1 0 1 1 0 1 1 0( ) ( ) 2 ( ) ( ) ( ) ( )

1 1 2 2 2 3 1 2 3 2 3

1 1 1 1( ) ( ) 2 ( ) ( )

1 1 2 2

t t t t t t

t

t t t

c t e c t e c t e c t e c t e c t ee

c t e c t e c t e c t

2 2

1 2

2

1 2

1 1 0( ) 2 ( )

1 2 3

1 1 0( ) ( )

1 2 3

t t t

t

t t

t

e c t e c t ee

c t e c t ee

The final expression given above can be written in matrix notation as

1

2

2

1 1 0( )

1 2 3( )

t

tt

c t e

ec t e

To solve for 1 2( ) and ( )c t c t , we will apply Cramer’s Rule to find

2

1 2

0 1 1 0

3 2 1 33 3( ) and ( )

0 1 0 12 2

2 3 2 3

t tt tt te ee e

c t e c t e

Thus

2

1 2

3 3 3 3( ) = and ( )

2 2 2 2

t t tt te e e

c t e c t e

To solve for 1 2( ) and ( )c t c t , integrate both sides of both equations so that

40

1 2

3 3( ) and ( )

2 2

tt ec t c t

and substituting into the partial solution 2

1 2

1 1( ) ( )

1 2

t t

px c t e c t e

yields

21 1 1 13 3

3 31 2 1 22 2

tt t t t

p

t ex e e te e

Therefore, the general solution to the nonhomogenous system is

2

1 2

1 1 1 13 3

1 2 1 2

t t t t

h px x x c e c e te e

Example 2: Solve the following 2 x 2 system for x

1 1 2

2 1 2

2 12

1 22 3 3

t tx x x e ex x

x x x t t

We will begin the example by using Maple to find the eigenvalues and eigenvectors of the

homogenous part of the system

2 1

1 2x x

Therefore

>

>

41

>

The resulting eigenvalues and eigenvectors are 1 2

1 2

1 11, 3, , and

1 1r r

. The

Wronskian (1) (2) 12[ , ] 0tW x x e thus, the general solution to the homogenous part of the system

is

3

1 2

1 1

1 1

t t

hx c e c e

To find the particular solution of the nonhomogenous part of the system, we will use the

variation of parameters technique to find a solution of the above equation of the form

3

1 2

1 1( ) ( )

1 1

t t

px c t e c t e

Substituting px for x and x directly into

2 1

1 2 3

tex x

t

to get the following

3

1 2

1 1( ) ( )

1 1 3

t

t t ec t e c t e

t

The final expression above can be written in matrix notation as

1

3

2

1 1 ( )

1 1 ( ) 3

t t

t

c t e e

c t e t

To solve for 1 2( ) and ( )c t c t , we will apply Cramer’s Rule to find

42

3

1 2

3 3( ) and ( )

2 2 2 2

t tt te t e t

c t e c t e

Thus

2 3

1 2

1 3 3( ) and ( )

2 2 2 2

t t tte e tec t c t

To solve for 1 2( ) and ( )c t c t , integrate both sides of both equations so that

2

1 2

2 23

1 2

3 3 3 3( ) + and ( )

2 2 2 4 2 2

1 1 1 13 3 3 3( ) ( ) +

1 1 1 12 2 2 4 2 2

tt t t t

t t t tt t

h p

ete e t te ec t c t

t te e te ex x x c t e c t e

and substituting into the partial solution 3

1 2

1 1( ) ( )

1 1

t t

px c t e c t e

yields

2

3

2 2

1 13 3 3 3+

1 12 2 2 4 2 2

1 13 3 3 3+

1 12 2 2 4 2 2

tt t t tt t

p

t t t t

p

ete e t te ex e e

t te e te ex

Therefore, the general solution to the nonhomogenous system is

2 23

1 2

1 1 1 13 3 3 3( ) ( ) +

1 1 1 12 2 2 4 2 2

t t t tt t

h p

t te e te ex x x c t e c t e

43

Section 5: Application of Systems of Differential Equations – Arms Races

(Nonhomogenous Systems of Equations)

In the previous section, we discussed how to solve systems of differential equations that

were nonhomogenous using a variation of parameters technique. Now, we can apply that

knowledge of solving systems with nonhomogenous equations to solve a model that illustrates an

arms race between two competing nations. L.F. Richardson, an English meteorologist, first

proposed this model (also known as the Richardson Model) that tried to mathematically explain

an arms race between two rival nations. Richardson himself seemed to have believed that his

perceptions relating to the way nations compete militarily might have been useful in preventing

the outbreak of hostilities in World War II (Brown, 2007, p. 60). Both nations are self-defensive,

both fight back to protect their nation, both maintain army and stock weapons, and when one

nation expands their army the other nation finds it offensive. Therefore, both nations will spend

money (in billions of dollars) on armaments x and y that are functions of time t measured in

years. x(t) and y(t) will represent the yearly rate of armament expenditures of the two nations

using some standard unit. Richardson then made some of the following assumptions about his

model:

The expenditure for armaments of each country will increase at a rate that is proportional

to the other country’s expenditure (each nation's mutual fear's rate is directly proportional

to the expenditure of the other nation) (Rainville, Bedient, & Bedient, 1997, p. 228).

The expenditure for armaments of each country will decrease at a rate that is proportional

to its own expenditure (extensive armament expenditures create a drag on the nation's

economy) (Rainville, Bedient, & Bedient, 1997, p. 228).

44

The rate of change of arms expenditure for a country has a constant component that

measures that level of antagonism of that country toward the other (Rainville, Bedient, &

Bedient, 1997, p. 228).

The effects of the three previous assumptions are additive (Rainville, Bedient, & Bedient,

1997, p. 228).

The previous assumptions make up the differential equations of the arms race system denoted by

0

0

(0)

for

(0)

dx x xay mx rdt

dybx ny s y y

dt

where a, m, b, and n are all positive constants. The positive terms ay and bx represent the drive to

spend more money are arms due to the level of spending of the other nation, and the negative

terms mx and ny reflect a nation’s desire to inhibit future military spending because of the

economic burden of its own spending. But, r and s can be any value because they represent the

attitudes of each nation towards each other (negative values represent feelings of good will while

positive values represent feelings of distrust). The initial values (0) and (0)x y represent the

initial amount of money (in billions of dollars) each nation will spend towards armaments. The

system can be simplified into

( )

( )

x t mx ay r

y t bx ny s

and is expressed in matrix notation where

( ) ( )( )

( ) ( )

x t m a x t rX P t X B

y t b n y t s

45

To solve for the system, we will use the knowledge from the previous section to develop

general solutions to the homogenous system. For the nonhomogenous part of the system, the

solution will be a constant solution of the form f

g

because the vector B is made up of

constants thus making the process of solving by variation of parameters much easier. Lastly, the

initial values (trajectories) for the solution will represent the starting amount of money each

country will be spending on armaments.

General solutions to the arms race system will represent one of a few types of races: a

stable arms race, a runaway arms race, a disarmament, or disarmament/runaway/stable arms race

depending on the initial values. The following examples will help demonstrate each of the above

mentioned arms races along with slope fields to graphically represent the races.

Example 1: A Runaway Arms Race

The following system will result in a runaway arms race:

( ) 2 4 8 2 4 8

( ) 4 2 2 4 2 2

x t x yX X

y t x y

To find the solution to this arms race, we will first find the general solution to the

homogenous part of the system using Maple:

>

>

>

46

Therefore, 1 2r , 1

1

1

, 2 6r , and 2

1

1

. The Wronskian (1) (2) 4[ , ] 2 0tW x x e

thus, the general solution to the homogenous part of the arms race is

2 6

1 2

1 1

1 1

t t

hx c e c e

As mentioned in the beginning of this section, the nonhomogenous system

( )X P t X B has a constant solution of the form e

f

because B is a vector of constants thus

the solution should also be a vector made up of constants. Therefore, in the equation

( )X P t X B , ( )e

X tf

can be substituted into and X X where

2 4 8( ) and

4 2 2P t B

to get the following expression

2 4 8 2 4 8 2 4 8 20

4 2 2 4 2 2 4 2 2 3n

f f f g fx

g g f g g

Therefore the general solution of the nonhomogenous system is

2 6

1 2

1 1 2

1 1 3

t t

h nx x x c e c e

47

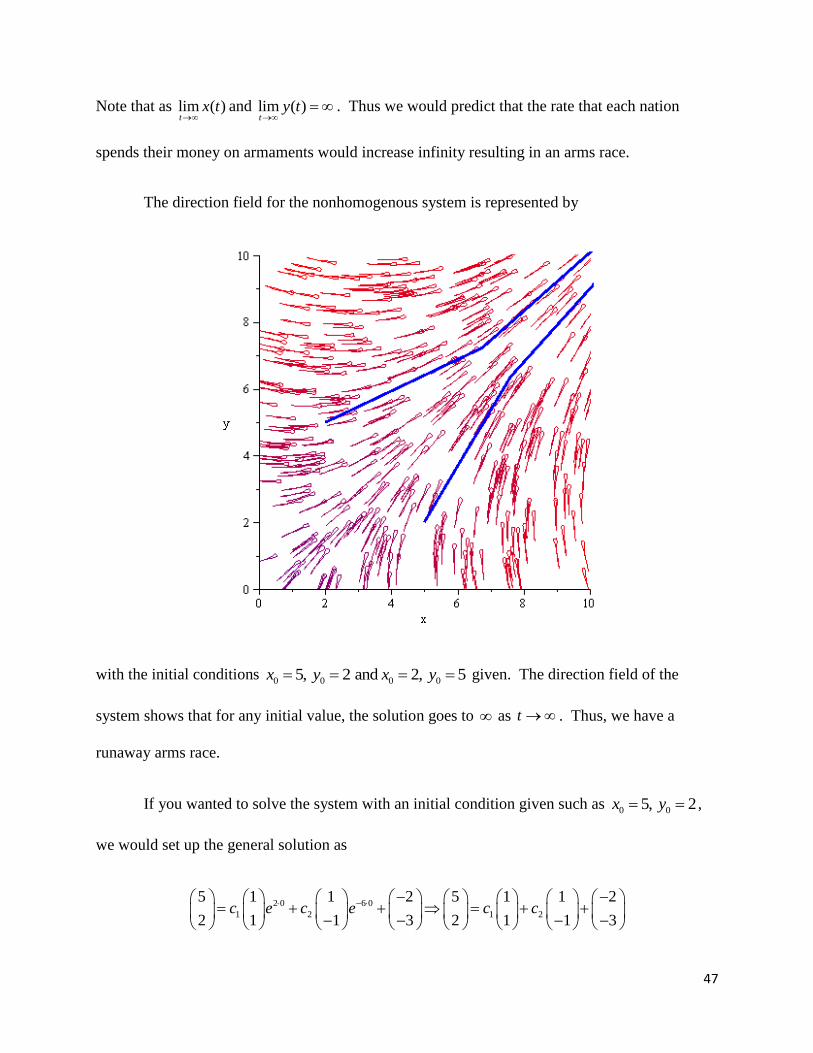

Note that as lim ( )t

x t

and lim ( )t

y t

. Thus we would predict that the rate that each nation

spends their money on armaments would increase infinity resulting in an arms race.

The direction field for the nonhomogenous system is represented by

with the initial conditions 0 0 0 05, 2 and 2, 5x y x y given. The direction field of the

system shows that for any initial value, the solution goes to as t . Thus, we have a

runaway arms race.

If you wanted to solve the system with an initial condition given such as 0 05, 2x y ,

we would set up the general solution as

2 0 6 0

1 2 1 2

5 1 1 2 5 1 1 2

2 1 1 3 2 1 1 3c e c e c c

48

and solve for 1c and

2c . Therefore

1 2 1 2

1 2 1 2

1 2 1 2

2 5 75 1 1 26 and 1

3 2 62 1 1 3

c c c cc c c c

c c c c

Thus, the final solution with the initial conditions given is

2 61 1 2

61 1 3

t tx e e

or

2 6

2 6

( ) 6 2

( ) 6 3

t t

t t

x t e e

y t e e

The role of the initial value is how much each nation will initially spend on armaments in

billions of dollars. Using initial values when solving an arms race system will lead to a specific

solution describing the race instead of families of general solutions describing all cases of the

system.

Example 2: A Stable Arms Race

The following system will result in a stable arms race:

( ) 5 2 1 5 2 1

( ) 4 3 2 4 3 2

x t x yX X

y t x y

To find the solution to this arms race, we will first find the general solution to the

homogenous part of the system using Maple:

49

>

>

>

Therefore, 1 7r , 1

1

1

,

2 1r , and 21

2

. The Wronskian (1) (2) 8[ , ] 3 0tW x x e

thus, the general solution to the homogenous part of the arms race is

7

1 2

1 1

1 2

t tx c e c e

The general solution to the nonhomogenous part of the arms race will be found by

substituting ( )f

X tg

into 5 2 1

4 3 2X X

. Therefore

5 2 1 5 2 1 00 1 and 2

4 3 2 4 3 2 0

f f gf g

g f g

and the solution of that system is 1

2nx

. Thus the general solution of the nonhomogenous

system is

7

1 2

1 1 1

1 2 2

t t

h nx x x c e c e

50

Note that as lim ( ) 1t

x t

and lim ( ) 2t

y t

because in both equations, the terms with both

7 and t te e go to 0 as t . All that is left from the differential equations are the constant

terms ( ) 1 and ( ) 2x t y t and what initial values of the system converge to.

The direction field with a few trajectories denoting the initial values for the

nonhomogenous system is represented by

The direction field of the system shows that for any initial value, the solution approaches the

point (1,2) as t . Thus, we have a stable arms race.

51

Example 3: Disarmament

The following system

( ) 4 1 4 1 1

( ) 2 1 1 2

x t x yX X

y t x y

will result in disarmament between the competing nations for all initial values.

For the sake of simplicity, only the graph of this system and the solution solved by Maple

will be shown because the eigenvectors and eigenvalues generated from P(t) become

complicated radicals that would be difficult to manipulate by hand to find an answer. Therefore,

the general solution to the system given by Maple output is

>

>

>

>

52

>

As you can see from the above solution, the general solution to the system is becomes very

complicated but, lim ( ) 1 and lim ( ) 3t t

x t y t

thus showing that eventually, the nations will

get to a point in time where they are decreasing the rate at which they are spending money on

armaments until they are spending no money on the arms race. The graph of the system is much

more beneficial in demonstrating an arms race that ends in disarmament.

The direction field with a few trajectories denoting the initial values for the

nonhomogenous system is represented by

53

For the initial values represented by the blue trajectories in the above directional field, the

trajectories will approach the point ( 1, 3) as t thus resulting in disarmament with any

initial value chosen for the system.

Example 4: Disarmament/Runaway Arms Race/Stable Arms Race

The following system

( ) 2 4 2 2 4 2

( ) 4 2 2 4 2 2

x t x yX X

y t x y

will result in disarmament if 0 0 2x y , a runaway arms race if

0 0 2x y , or a stable arms

race if 0 0 2x y .

To find the solution to this arms race, we will first find the general solution to the

homogenous part of the system using Maple:

>

>

>

Therefore, 1 2r ,

11

1

, 2 6r , and

21

1

. The Wronskian (1) (2) 4[ , ] 2 0tW x x e

thus, the general solution to the homogenous part of the arms race is

54

2 6

1 2

1 1

1 1

t t

hx c e c e

The general solution to the nonhomogenous part of the arms race will be found by

substituting ( )f

X tg

into 2 4 2

4 2 2X X

. Therefore

2 4 20 1 and 1

4 2 2

ff g

g

and the solution of the system is 1

1nx

. Thus the general solution of the nonhomogenous

system is

2 6

1 2

1 1 1

1 1 1

t t

h nx x x c e c e

The direction field with a few trajectories denoting the initial values for the nonhomogenous

system is represented by

55

For the initial values 0 0 0 0 0 01.7, 0, 0, 1.7, and 2x y x y x y in the above directional

field, the trajectories will approach as t thus resulting in disarmament. For the initial

values0 0 0 0 0 02, 0, 0, 2, and 2x y x y x y , the trajectories will approach the point (1,1)

as t thus resulting in a stable arms race. For the initial values

0 0 0 0 0 03, 0, 0, 3, and 2x y x y x y , the trajectories will go to as t thus resulting

in a runaway arms race.

Conjectures of Richardson’s Arms Race Model

After solving and graphing results of the Arms Race Model to show the different situations in

describing the model, in the following conjectures can be made to better summarize what is

theoretically happening in the model with certain values for the coefficients:

If mn - ab < 0, r > 0, and s >0, there will be a runaway arms race.

If mn - ab> 0, r > 0, and s > 0, there will be a stable arms race.

If mn - ab > 0, r < 0, and s < 0, there will be disarmament.

If mn - ab < 0, r < 0, and s < 0, there will be disarmament if 0 02

r sx y

, a runaway

arms race if 0 02

r sx y

, and a stable arms race if 0 0

2

r sx y

.

Real World Examples of Richardson’s Model

At the level of strategic weapons during the Cold War, Russia and America were

in a two-way arms race. The structure of this is that both sides increased until the

Russians achieved equality, at which point the two sides began signing initial SALT

agreements as predicted by the model (Hunter, 1980, p. 252).

56

Both nations realized that once they were at equality, that the risk of spending more money on

armaments would have worse impact on their economies thus, as the model predicted, the arms

race started to stabilize (even though both nations still have negative feelings toward each other).

Another example reveals sharp limitation on the model. In 1939, Russia and Germany

signed a nonaggression pact which left Germany and Russia in a two-sided alliance

against England, France, and other weaker countries. Yet the arms race in both Russia

and Germany accelerated at the maximum economic rate. Why? Because both sides knew

that Hitler intended to invade Russia at the earliest feasible time (Hunter, 1980, p. 252).

Both nations secretly had negative feelings towards one another and were willing to spend more

money on armaments without much regard on the negative impact that the spending would have

on their economy. Thus, as Richardson’s Model could have predicted, the Germans and the

Russians were at a runaway arms race with each other (at the time).

Richardson’s Arms Race Model Extended

What was described in this section was the most generic model of the arms race. The

model has been expanded to include more than two nations and other variables that would affect

an arms race. What was interesting is that the arms race model could and was used to model

World War II which included numbers for 10 countries that were included. At the most basic

level of the arms race model, a lot of problems and difficulties arrive that are solved in more

detailed versions of the model but, Richardson’s Model laid a good foundation to understand a

social science topic mathematically.

57

Section 6: Application of Systems of Differential Equations – Predator-Prey Model

(Nonlinear System of Equations)

In the study of the dynamics of a single population, ecologists typically take into

consideration such factors as the "natural" growth rate and the "carrying capacity" of the

environment. Mathematical ecology requires the study of populations that interact, thereby

affecting each other's growth rates. In this section we study a very special case of such an

interaction, in which there are exactly two species, one of which, the predators, eats the other, the

prey. Such pairs exist throughout nature: Lions and gazelles, birds and insects, pandas and

eucalyptus trees, and Venus fly traps and flies (Moore & Smith, 2003).

Vito Volterra (1860-1940) was a famous Italian mathematician who retired from a

distinguished career in pure mathematics in the early 1920s. His son-in-law, Humberto

D'Ancona, was a biologist who studied the populations of various species of fish in the Adriatic

Sea. In 1926, D'Ancona completed a statistical study of the numbers of each species sold on the

fish markets of three ports from 1914-1923: Fiume, Trieste, and Venice (Moore & Smith, 2003).

D'Ancona observed that the highest percentages of predators occurred during and just

after World War I, when fishing was drastically curtailed. He concluded that the

predator-prey balance was at its natural state during the war and that intense fishing

before and after the war disturbed this natural balance. Having no biological or

ecological explanation for this phenomenon, D'Ancona asked Volterra if he could come

up with a mathematical model that might explain what was going on. In a matter of

months, Volterra developed a series of models for interactions of two or more species

58

(Moore & Smith, 2003). The first and simplest of these models is the subject of this

section.

Alfred J. Lotka (1880-1949) was an American mathematical biologist who formulated

many of the same models as Volterra, independently and at about the same time. His primary

example of a predator-prey system comprised a plant population and an herbivorous animal

dependent on that plant for food (Moore & Smith, 2003). Thus, the Predator-Prey Model is also

known as Lotka-Volterra Model named after the two mathematicians that helped developed the

equations.

To keep the model simple for easier understanding, we will make the following

assumptions that would be unrealistic in most predator-prey interactions:

The predator species is totally dependent on a single prey species as its only food supply.

The prey species has an unlimited food supply.

There is no threat to the prey other than the specific predator.

In constructing the model between the two species, we will make the following

assumptions to set up the model which relate to the above assumptions:

( )x t will represent the number of prey at a time given by t and ( )y t will represent the

number of predators at a time also given by t.

In the absence of the predator, the prey grows at a rate proportional to the current

population; thus , 0, when 0dx

ax a ydt

(Boyce & DiPrima, 2001, p. 503).

59

In the absence of the prey, the predator dies out; thus , c 0, when 0dy

cy xdt

(Boyce

& DiPrima, 2001, p. 503).

The number of encounters between predator and prey is proportional to the product of

their populations. Each such encounter tends to promote the growth of the predator and

to inhibit the growth of the prey. Thus the growth rate of the predator is increased by a

term of the form pxy , while the growth rate of the prey is decreased by a term bxy ,

where p and b are positive constants (Boyce & DiPrima, 2001, p. 503).

As a result of these assumptions, the following equations were formulated to represent the

change of predators and prey over time

( ) and ( )dx dy

ax bxy x a by cy pxy y c pxdt dt

where a, c, b, and p are all positive. The growth rate of the prey and the death rate of the

predator is represented by a and c respectively while b and p are measures of the effect of the

interaction between the two species (Boyce & DiPrima, 2001, p. 504). Even though the

differential equations of the Predator-Prey Model are nonlinear, we can use the linear part of the

equation to find a general solution to help explain the behavior of the system. Also, finding the

critical points, the directional field, and trajectories of the directional field will be key in further

explaining the behavior of the system. The critical points of the system are the solutions of

( ) 0 and ( ) 0x a by y c px

that is the points (0,0) and ( / , / )c p a b . We first examine the solutions of the corresponding

linear system near each critical point. The origin is a saddle point and hence unstable. Entrance

60

to the saddle point is along the y-axis and departs via the x-axis. All other trajectories depart

from the neighborhood of the critical point.

From the critical point at the origin, the corresponding linear system is

0(1)

0

x a xd

y c ydt

The eigenvalues and eigenvectors are

1 1

1 2

1 0, , , and

0 1r a r c

Therefore, the general solution is

1 2

1 0

0 1

at ctx

c e c ey

and the resulting direction field is

61

Next, consider the critical point ( / , / )c p a b . To examine the behavior and generate a general

solution around that critical point, we will add values u and v to them to get

and c a

x u y vp b

. Then we will substitute them into ( ) 0 and ( ) 0x a by y c px to

translate and c a

u x v yp b

. Therefore

0 and 0

0 and 0

0 and 0

c a a cu a b v v c p u

p b b p

c au a a bv v c c pu

p b

bc apv bu u pv

p b

Therefore, the corresponding linear system is

0(2)

0

u bc p ud

v ap b vdt

The eigenvalues of that system are r i ac so the critical point (stable) is along the y-axis;

all other trajectories depart from the neighborhood of the critical point (Boyce & DiPrima, 2001,

p. 507).

62

Returning to the nonlinear system, it can be reduced to a single equation represented as

( )

( )

dy dy dt y c px

dx dx dt x a by

The above equation can be separated and integrated to get the following solution

ln ln (3)a y by c x px C

where C is a constant of integration.

63

Even though we cannot solve the solution for x or y, the solution does show that the graph

of the equation for a fixed value of c is a closed curve surrounding the nonzero critical

point. Thus the critical point is also a center of the initial nonlinear system and the

predator/prey populations exhibit a cyclic variation (Boyce & DiPrima, 2001, p. 506).

The following examples will help demonstrate the Predator-Prey Model and the aspects

mentioned above that it contains.

Example 1: Determine the Behavior of x and y as t→∞

(1.5 0.5 ) and ( 0.5 )dx dy

x y y xdt dt

First, we will find the critical points of the system by using ( ) 0 and ( ) 0x a by y c px to

find the points

(0,0) and (1 2,3)

Next, we will examine the behavior at the critical point (0,0) by using equation (1)

0 1.5 0

0 0 0.5

x a x x xd d

y c y y ydt dt

Therefore, the eigenvalues and eigenvectors of the above equation are

1 1

1 2

1 01.5, , 0.5, and

0 1r r

and its general solution is

64

1.5 0.5

1 2

1 0

0 1

t tx

c e c ey

After examining the first critical point, we will examine the second critical point (1 2,3) by using

equation (2)

0 0.5 0.5 10

1.5 1 0.5 00

0 0.25

3 0

u bc p u u ud d

v ap b v v vdt dt

u ud

v vdt

The resulting eigenvalues are 1 2

3 3 and

2 2

i ir r . The resulting eigenvalues have

radicals and complex values that are difficult to express in simpler terms.

The original system has a solution from equation (3)

ln ln 1.5ln 0.5 0.5lna y by c x px C y y x x C

65

The resulting directional field with trajectories for different initial populations of the

predator and prey is

The directional field and trajectories show the populations of predator and prey over time. The

ellipses around the critical point (1 2,3) show that over a certain period of time, the way in how

the predator and prey interact with each other go through a cycle of change and end up back at

the initial population of both the predator and the prey. Because the predator/prey start from a

relatively small population, the prey increase first because there is little predation. Then the

predators, with abundant food, increase in population also. This causes heavier predation and the

prey tend to decrease. Finally, with a diminished food supply, the predator population also

decreases, and the system returns to the original state. The following graph will demonstrate the

variations of the prey (blue) and predator (green) populations with time for the system

66

The above graph shows that relationship between predator and prey repeats sinusoidally with a

period of about 10t and that the predator population lags behind the prey population. The

next few examples will examine the manipulation of the coefficients a, c, b, and p and in the

differential equations and what it means in terms of the solutions. To best describe this, three

dimensional graphs will be utilized to show the change of predator and prey over time.

Example 2: Determine the Behavior of x and y as t→∞

For this example, we will use the initial values 1, 0.02, 0.4, and 0.01a b c p to

model the following Predator-Prey Model

0.03 and 0.4 0.01dx dy

x xy y xydt dt

67

To get a better understanding of how the solution of the system operates, we will analyze the

following graphs instead of the numerical solutions in the previous example. Therefore, the

graphs are

and

68

The first graph has multiple initial values of the predator/prey that include

(0) 15 and (0) 15x y while the other graphs exclusively model the same initial value. The

first graph shows general solutions of the Predator-Prey Model with a few initial populations

given by the blue trajectories on the graph. The trajectories are in the form of ellipses

surrounding the critical point (40,50)pc .

What is hard to see in the first graph that is modeled much more effectively in the third

graph is the path of the trajectory as t . Because the solutions of the system are periodic (as

demonstrated by the second graph with periodicity of about 12t ), the trajectories overlap each

other in the first graph t . In the third graph, which shows both the change of rate of

predator and prey over time, the trajectory doesn’t overlap itself because the graph is three

dimensional thus making the trajectory’s path easier to see that it is periodic as t . The

graphs systems are perfectly periodic because the model only takes into account the most basic

factors between the predator and prey interaction. In reality, the graphs wouldn’t be as perfect as

the ones above but, there are a few cases where actual predator and prey populations have been

sampled that reflect this idea of periodicity within the interaction.

69

The above graph shows is a classical set of data on a pair of interacting populations that

come close: the Canadian lynx and snowshoe hare pelt-trading records of the Hudson Bay

Company over almost a century (Moore & Smith, 2003).

To a first approximation, there was apparently nothing keeping the hare population in

check other than predation by lynx and it depended entirely on hares for food. To be sure,

trapping for pelts removed large numbers of both species from the populations but these numbers

were quite small in comparison to the total populations. So, trapping was not a significant factor

in determining the size of either population. On the other hand, it is reasonable to assume that the

success of trapping each species was roughly proportional to the numbers of that species in the

wild at any given time. Thus, the Hudson Bay data give us a reasonable picture of predator-prey

interaction over an extended period of time. The dominant feature of this graph is the oscillating

behavior of both populations shown in the second graph of example 2.

Focusing back on the example, an interesting observation about the graph would be to see

what the trajectory with the initial value of the critical point, (40,50)pc , would look like.

Using the graphing technology of Maple, we see that

70

and the trajectory shows no change between predator and prey as t . In this case, where the

initial value is the critical point, we see a ‘perfect balance’ of the predatory/prey interaction

illustrated by the model. Of course, in reality, this type of interaction would never exist but, in

this ideal situation with the Predator-Prey Model, it can exist.

71

Next, the following graphs will show what happens when the coefficients , , , and a b c p

are varied from the initial coefficients 1, 0.03, 0.4, and 0.01a b c p with the initial

values for all graphs to be (0) 15 and (0) 15x y . The first coefficient that will be manipulated

will be a with the following values

By increasing a by 50%, the overall ellipse of the trajectory becomes larger and the period

shortens from 10 to 5t t . By decreasing a by 50%, the overall ellipse of the trajectory

becomes smaller and the period lengthens from 10 to 15t t . The above graphs make sense

because a measures the growth rate of the prey and if there is more prey in the area, it allows for

more predators in the same area. The same could be said if there were less prey to feed on, then

there would be fewer predators that would be able to survive in the same area.

72

The next coefficient that will be manipulated will be b with the following values

By increasing b by 50%, the overall ellipse of the trajectory becomes smaller and the period

shortens from 10 to 9t t . By decreasing b by 50%, the overall ellipse of the trajectory

becomes larger and the period lengthens from 10 to 11t t . The above graphs make sense

because b measures the negative interaction of the prey and predator with regards to the rate of

change of the prey. If b becomes larger, the interaction reduces more amounts of prey but if b

becomes smaller, the interaction allows more prey to survive.

Another coefficient that will be manipulated will be c with the following values

73

By increasing c by 50%, the overall ellipse of the trajectory becomes larger and the period

shortens from 10 to 8t t . By decreasing c by 50%, the overall ellipse of the trajectory

becomes smaller and the period lengthens from 10 to 16t t . The above graphs make sense

because c measures the death rate of the predators. If the predators are dying out quicker, it

allows for more prey and also allows more predators at certain times of t when t . If the

predators are surviving for longer periods of time, there will be less prey in the area which will

lead to less predators overall but the cycle between predator/prey interaction will be slower than

if c increased.

The last coefficient that will be manipulated will be p with the following values

By increasing p by 50%, the overall ellipse of the trajectory becomes smaller and the period

lengthens from 10 to 11t t . By decreasing p by 50%, the overall ellipse of the trajectory

becomes larger and the period shortens from 10 to 9t t . The above graphs make sense

because p measures the positive interaction of the prey and predator with regards to the rate of

change of the predator. If p becomes larger, the interaction increases the rate of growth of the

predators and allows less of both the predator and the prey to survive. But, if p becomes smaller,

74

the interaction decreases the rate of growth of the predators thus allowing more predator and

prey to survive in the area.

The coefficients in the Predator-Prey Model do contribute to the overall make up of the

solutions with initial populations given. Depending on how the coefficient is manipulated, the

overall size of the ellipse of the can become larger or smaller and the periodicity of the predator-

prey interaction can become longer or shorter. We can use the equations to draw several

conclusions about the cyclic variation of the predator and prey on such trajectories:

The predator and the prey populations vary sinusoidally with period 2 ac . This period

of oscillation is independent of the initial conditions (Boyce & DiPrima, 2001, p. 508)

The predator and prey populations are out of phase by one-quarter of a cycle. The prey

leads and the predator lags (Boyce & DiPrima, 2001, p. 508).

The average populations of predator and prey over one complete cycle are and /c p a b ,

respectively. These are the same as the equilibrium proportions (Boyce & DiPrima,

2001, p. 508).

The last example will show what happens when an external variable, hunters, are figured into the

model.

Example 3: The Effect of Hunting Predators

To add the extra variable of hunting predators into the Predator-Prey Model, we will

subtract a constant coefficient and the end of the equation of the rate of growth for the predators.

Thus

75

and dx dy

ax bxy cy pxy hdt dt

where h is the effect of hunting and killing a constant amount of predators every cycle. Going

back to coefficients used in example two, we will use the equations

0.03 and 0.4 0.01 5dx dy

x xy y xydt dt

where 5h (death of 5 predators per unit of time) to generate a three dimensional graph

depicting what happens when hunters are introduced into the equation. With the initial

conditions (0) 40 and (0) 40x y , the above graph shows that when the variable of hunting

predators is introduced, the predators become extinct at 23t thus allowing the prey to grow

infinitely at an exponential rate. Also, as t increases, the spiral of the trajectory becomes more

76

unwound until the amount of predators in the area becomes extinct which allows overpopulation

of the prey. If there was a hunting variable proposed onto to the equation of the change of rate of

prey, both species lose as both would become extinct as t . Therefore, the addition of the

variable to either the predator, prey, or both will lead to the extinction of species over time.

77

Conclusion

Throughout the research process for my topic of systems of differential equations, the use

of the mathematical software Maple helped solve the systems and generate directional fields for

the solutions. Without the help of Maple, the process of drawing the directional field for a

solution would have been very tedious to generate if not impossible because of the precision and

different options Maple has to generate those directional fields. Maple was also helpful in

generating three dimensional graphs to help further understanding of the Predator-Prey Model.