sending money home_europe_2015

TRANSCRIPT

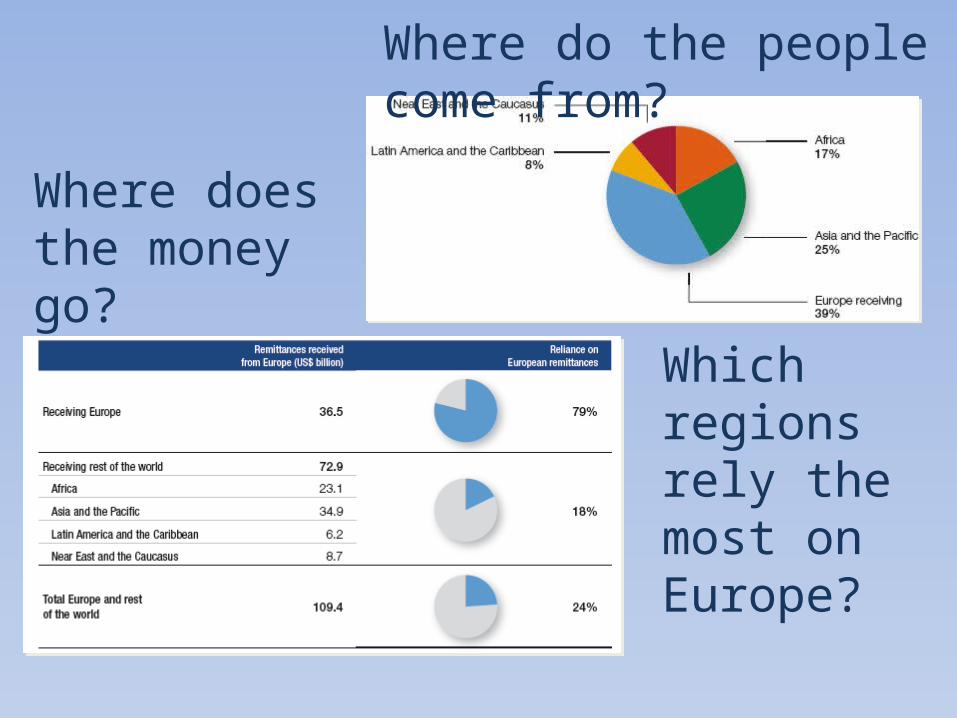

Remittances from Europe surpass US$109 billion

Where does the money go?

Where do the people come from?

Which regions rely the most on Europe?

Remittance outflows from main sending European countries, 2014 The sending side…Remittance outflows from main sending European countries, 2014

(Countries with annual GDP per capita > US$20,000)

The top 10 European countries

account for 82% of the outflows’’

Outflows

form Europe

represent 0.7% GDP of sending countrie

s

European

diasporas have US$100 million

accumulated in savings

…Russia send the most of the remittances to Central Asia and Eastern Europe…

..Remittances from the UK mainly go to Asia and Africa..

…France flows mainly go to countries in Africa…

…A significant amount of remittances form Germany go to Turkey and eastern Europe…

Receiving Europe…One-third (US$36.5 billion) of flows remain in Europe ‘’The most

remittance-reliant

countries have a

significant rural

population’’

35%Rural

Population

Sending remittances from Europe costs 7.3% - slightly below world

average

Average Europe

Western Europe

Russia

8.3%7.3% 7.9% World average

Costs to send $US200 from…

Dominating positions of the major

MTOs, high exchange rate commissions or high bank transfer fees

Competition among a large

number of MTOs and wide

dispersal of payout

locations

Costs increase when

Costs decrease when

2.4%

“A reduction to 5 per cent would save migrants and their families more than US$2.5 billion in transfer costs per year.”

Mobile OperatorsOnline services Banks

Banks play a major role as distribution channel for MTOs for sending and receiving flows in Europe.

MTOs

MTOs represent 70 per cent of all RSPs in the marketplace in receiving Europe.

These MTOs operate with their own license or in partnership with banks and postal networks

“Cash-to-cash continues to be the most used method for migrants in Europe, as in the rest of the world, to send money

home.”

Receiving EuropeActors in the marketplace

There are over 200 remittance service providers (RSPs) in Europe.

Postal networks

Mobile and online platforms offer less expensive products but still struggle to convince clients

Postal networks represent 30% of payout locations in receiving Europe.

They account for 85% of payout locations in rural areas.

Their market share is still limited.

Maximizing the impact of remittances

“Access”

Strengthen the remittance rural

market

“Use”

Promote Financial Inclusion

“Investment back home”

Promote investment of remittancesand migrant

savings

1

2

3

Financial Inclusion – Identified opportunities

- Leveraging the impact of remittances requires differentiated, contextualized and concerted policies and strategies between remittance sending and receiving countries.

- Regional harmonization is necessary to increase competition, expand financial options and lower risks.

- Competition could be enhanced by reducing regulatory limitations, promoting diversity in the marketplace, providing incentives for banking institutions to offer low-cost transfers, and nurturing the positive impact of new technologies.

Market Policy implications

“…its their Money”

• Shift transactions from “cash to cash” to “account to account”

• Encourage use and adoption of new technologies• Support financial education for both senders and receivers• Promote savings • Utilize remittances to establish credit history• Empower migrant workers and their families with more

options to invest• Leverage development in local communities

Opportunities