seminar on tax audit (recent amendment) friday, 8 th august 2014

DESCRIPTION

SEMINAR ON TAX AUDIT (RECENT AMENDMENT) Friday, 8 th August 2014 **************************************************** Speaker : CA Deepak Maheshwari **************************************************** Hosted by:. Jointly with :- Indore Branch of CIRC of ICAI. - PowerPoint PPT PresentationTRANSCRIPT

CA Deepak Maheshwari, Indore

SEMINAR

ON

TAX AUDIT (RECENT AMENDMENT)Friday, 8th August 2014

****************************************************

Speaker :

CA Deepak Maheshwari

****************************************************

Hosted by:

Jointly with :- Indore Branch of CIRC of ICAI

CA Deepak Maheshwari, Indore

Whether the assessee is liable to pay indirect tax like

excise duty, service tax, sales tax, customs duty, etc. if

yes, please furnish the registration number or any

other identification number allotted for the same.

Clause No. - 4

CA Deepak Maheshwari, Indore

Tax Auditor is expert of Income Tax act but cannot expect to be expert of all other acts

Obtain details from the assessee about his liability and registration number .

Purpose – Obtain data for the purpose of cross verification from other indirect tax department.

CA Deepak Maheshwari, Indore

Cross verify details from sales bill & other relevant

documents.

Suggestive Reporting :-

As informed by the assessee he is

liable to pay tax under following Acts, details of

which are given below along with their registration

number :-

CA Deepak Maheshwari, Indore

Indicate the relevant clause of section 44AB under

which the audit has been conducted

Clause No. - 8

CA Deepak Maheshwari, Indore

44AB

Clause (a) Business assessee Turnover exceeds 1 CR.

Clause(b) Professionals Gross Receipt exceeds 25 Lakh

Clause(c) Assessee covered u/s 44AE, 44BB, 44BBB

Clause(d) Assessee covered u/s 44AD

Now, audit ceiling limit compliance under ICAI

rules can be effectively checked.

CA Deepak Maheshwari, Indore

(b) List of books of account maintained and the address at which the books of accounts are kept.

(c) List of books of account and nature of relevant

documents examined.

Clause No – 11

CA Deepak Maheshwari, Indore

Place of business includes where the books of accounts are kept

Information is useful for department for the purpose of survey u/s 133-A

If more than one place than give detail of all places

obtain details from auditee regarding location

Section 2(12A)- Books of accounts includes ledgers, day books, cash books and any other books

CA Deepak Maheshwari, Indore

13 (C). Where there is a change in method of accounting employed vis-a-vis the method employed in immediately preceding previous year, details of such change and effect thereof on profit and loss to be indicated in specific format

Serial No. Particulars Increase in

Profit (Rs.)Decrease in Profit (Rs. )

Nil

Clause - 13(c) & 14(b)

14(b). In case of deviation from the method of valuation prescribed u/s 145A, and the effect thereof on the profit or loss to be indicated in specific format

CA Deepak Maheshwari, Indore

Tabular format has inserted for proper reporting

Self explanatory

CA Deepak Maheshwari, Indore

Where any land or building or both is transferred

during the previous year for a consideration less than

value adopted or assessed or assessable by any

authority of a State Government referred to in Section

43CA or 50C, Please furnish :-

Details of Property

Consideration received or accrued

Value adopted or assessed or assessable

Nil

Clause -17

CA Deepak Maheshwari, Indore

Huge reporting & examination required in case of assessee engaged in real estate sector

Any land or building or both are covered (rural agriculture land too)

Reporting required for property appearing in books only

CA Deepak Maheshwari, Indore

In case of transaction through power of attorney , ratio deal, ask for valuation certificate, if not available than take representation letter from assessee & appropriate disclosure of this fact to be made.

If consideration received in installments, reporting to be made in the year in which transfer of property took place

Cross verification from 26-AS

CA Deepak Maheshwari, Indore

Clause - 19

Amounts admissible under sections:

Section

Amount debited to

P&L account

Amounts admissible as per the provisions of the Income Tax Act, 1961 and also fulfils the

conditions, if any specified under the conditions, if any specified under the relevant

14provisions of Income Tax Act, 1961 or Income Tax Rules,1962 or any other guidelines, circular,

etc., issued in this behalf.

32AC

TO

35AD

CA Deepak Maheshwari, Indore

Some more sections like 32AC, 35AD inserted

No major changes in reporting

CA Deepak Maheshwari, Indore

Details of contributions received from employees for various funds as referred to in section 36(1)(va) :

Clause - 20(b)

Serial number

Nature of fund

Sum received

from employees

Due date for

payment

The actual

amount paid

The actual date of payment to the

concerned authorities

CA Deepak Maheshwari, Indore

Tabular format is inserted for proper reporting

Self explanatory

CA Deepak Maheshwari, Indore

Detailed information to be furnished of amounts debited to profit & loss account, being in nature of capital, personal, advertisement expenditure etc in specified format

Clause – 21(a)

Nature

Sl. No.

Particulars

Amount (in Rs)

CA Deepak Maheshwari, Indore

Tabular format for reporting inserted

Advertisement expenses word used in the clause but

a) It is to be interpreted as advertisement expenses in any souvenir, brochure, tract or pamphletpublished by a political party as used in old TAR

b) Disallowable expenses relate to section 37

CA Deepak Maheshwari, Indore

i) Payment to Non resident without deduction of tax A. Details of payment on which tax is not deducted:

Date of Payment Amount of Payment Nature of payment Name and Address of the

Payee

(i) (ii) (iii) (iv)

Clause - 21{b}

B. Details of payment on which tax has been deducted but has not been paid during the previous year or in the subsequent year before the expiry of time prescribed under section 200(1)

Date of Payment

Amount of Payment Nature of payment Name and Address of the

PayeeAmount of Tax

deducted

(i) (ii) (iii) (iv) (v)

Amounts inadmissible under section 40(a):-

CA Deepak Maheshwari, Indore

Clause - 21{b}

ii) Payment to resident without deduction of tax (A) Details of payment on which tax is not deducted:

Date of Payment

Amount of Payment Nature of payment Name and Address of the

PayeeAmount of Tax

deducted

(i) (ii) (iii) (iv) (v)

(B) Details of payment on which tax has been deducted but has not been paid on or before the due date specified in sub- section (1) of section 139.

Date of Payment

Amount of Payment

Nature of payment

Name and Address of the Payee

Amount of Tax deducted

Amount out of (v) deposited, of any

(i) (ii)(iii)

(iv) (v) (vi)

CA Deepak Maheshwari, Indore

(iii) under sub-clause (ic) [Wherever applicable] FBT

(iv) under sub-clause (iia) Wealth Tax

(v) under sub-clause (iib) Royalty from State Government undertaking

(vi) under sub-clause (iii) Salary to NRI without TDS

Date of Payment Amount of Payment Name and Address of the Payee

(i) (ii) (iii)

Details as under:

(vii) under sub-clause (iv) Payment to employee’s benefit fund TDS not insured

(viii) under sub-clause (v) Tax paid on non monetary perquisites

CA Deepak Maheshwari, Indore

Clause - 21{d} Disallowance/deemed income under section 40A(3)

(A)On the basis of the examination of books of account and other relevant documents/evidence, whether the expenditure covered under section 40A(3) read With rule 6DD were made by a/c payee cheque or a/c payee bank draft If not, please furnish the details:(B) On the basis of the examination of books of account and other relevant documents/evidence, whether the payment referred to in section 40A(3A) read with rule 6DD were made by account payee cheque drawn on a bank or account payee bank draft If not, please furnish the details of amount deemed to be the profits and gains of business or profession under section 40A(3A):

Serial number Date of payment

Nature of payment

Amount Name and Permanent Account Number of

the payee, if available

CA Deepak Maheshwari, Indore

Tabular format inserted

Sub clause(B) inserted for reporting of transaction covered u/s 40A (3A)

Requirement of obtaining certificate from assessee

has removed (Safeguard removed)

Now reporting is to be given on the basis of examination of books and other relevant documents

CA Deepak Maheshwari, Indore

Clause -28 & 29

28. Whether during the previous year the assessee has received any property, being share of a company not being a company in which the public are substantially interested, without consideration or for inadequate consideration as referred to in section 56(2)(viia), if yes, please furnish the details of the same.

29. Whether during the previous year the assessee received any consideration for issue of shares which exceeds the fair market value of the shares as referred to in section 56(2)(viib), if yes, please furnish the details of the same.

CA Deepak Maheshwari, Indore

If any firm or Pvt. Ltd. Company receives shares of any Pvt. Ltd. company without consideration or inadequate consideration then reporting required u/s 56(2)(viia) (clause no.28)

If Pvt. Ltd. Company issue shares more than its NAV than difference to be reported under clause 29

CA Deepak Maheshwari, Indore

Determination of FMV is as per Rule 11U & 11UA

Information to be called from assessee regarding FMV valuation.

Added for the purpose of reporting transaction of companies known as briefcase company

CA Deepak Maheshwari, Indore

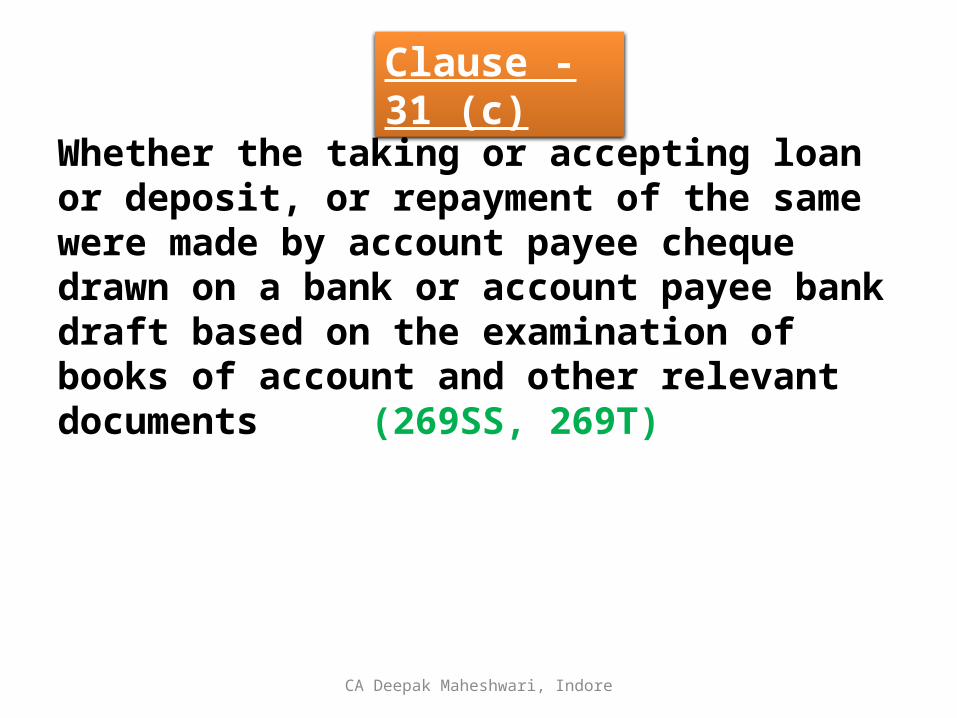

Clause -31 (c)

Whether the taking or accepting loan or deposit, or repayment of the same were made by account payee cheque drawn on a bank or account payee bank draft based on the examination of books of account and other relevant documents (269SS, 269T)

CA Deepak Maheshwari, Indore

Requirement of obtaining certificate from assessee has been removed

Now reporting to be made on the basis of examination of books & other relevant documents

CA Deepak Maheshwari, Indore

Clause-32(c) & 32 (d)

(c) Whether the assessee has incurred any speculation loss referred to in section 73 during the previous year, If yes, please furnish the details of the same.(d) whether the assessee has incurred any loss referred to in section 73A in respect of any specified business during the previous year, if yes, please furnish details of the same .

CA Deepak Maheshwari, Indore

32(c) Requires reporting of speculation loss.

Commodity loss from agriculture produce is speculation loss

32(d) Requires reporting & speculation loss of specified business as defined under section 35 (AD)

CA Deepak Maheshwari, Indore

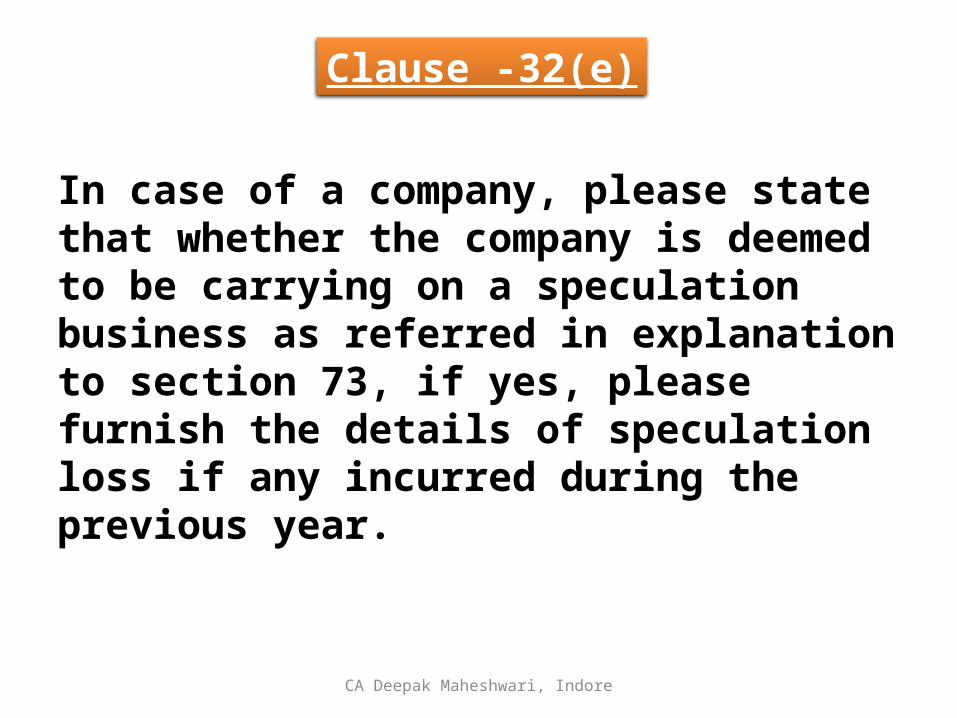

In case of a company, please state that whether the company is deemed to be carrying on a speculation business as referred in explanation to section 73, if yes, please furnish the details of speculation loss if any incurred during the previous year.

Clause -32(e)

CA Deepak Maheshwari, Indore

Reporting for speculation loss of companies which makes trading of shares of other companies

i. Exclusion for the companies whose GTI mainly consist of interest on securities, Income from House property, Capital gain & other sources.

ii. Whose principal business is banking or giving loans & advances.

iii. Finance Act 2014 has amended this section and exclusion is also made applicable for the companies whose principal business is share trading

CA Deepak Maheshwari, Indore

Clause -33

Section under which deduction is

claimed

Amounts admissible as per the provision of the Income Tax Act, 1961 and fulfils the conditions, if

any, specified under the relevant provisions of Income Tax Act, 1961 or Income Tax Rules,1962 or any other guidelines, circular, etc, issued in

this behalf.

Section-wise details of deduction, if any, admissible under Chapter VIA or Chapter III (Sec. 10A, Sec. 10AA)

CA Deepak Maheshwari, Indore

Now deduction details to be furnished for section 10A Free Trade Zone(FTZ) &

10AA Special Economic Zone (SEZ)

apart from chapter VI-A deductions

CA Deepak Maheshwari, Indore

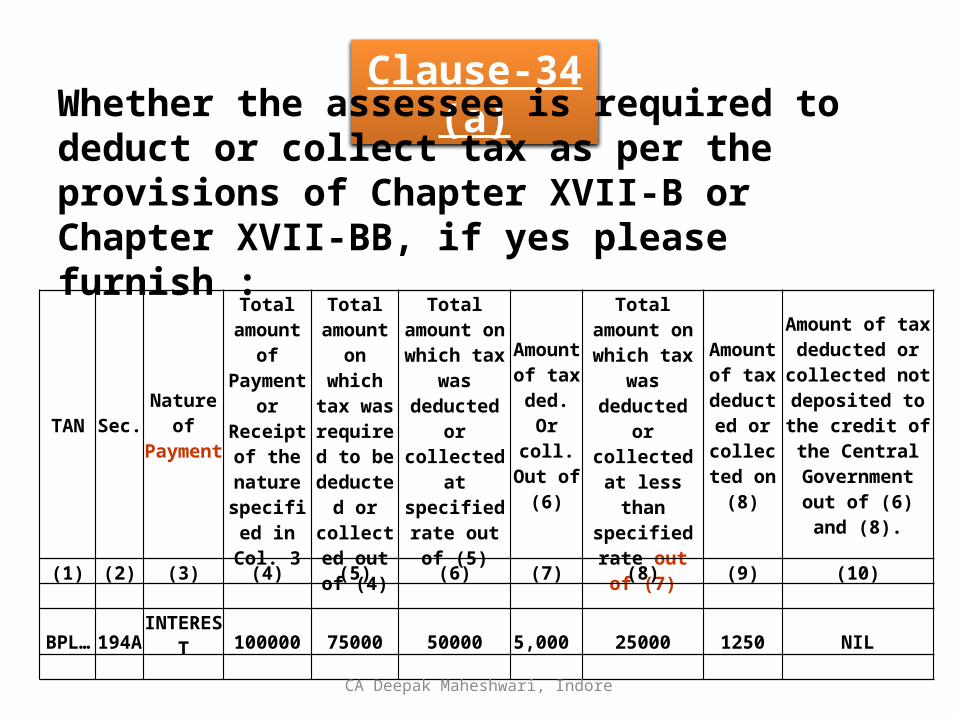

Clause-34 (a)

Whether the assessee is required to deduct or collect tax as per the provisions of Chapter XVII-B or Chapter XVII-BB, if yes please furnish :

TAN Sec. Nature of Payment

Total amount of Payment

or Receipt of the nature

specified in Col. 3

Total amount on which tax

was required

to be deducted

or collected out of (4)

Total amount on which tax

was deducted or collected at specified

rate out of (5)

Amount of tax

ded. Or coll. Out

of (6)

Total amount on which tax

was deducted or collected at

less than specified rate

out of (7)

Amount of tax

deducted or

collected on (8)

Amount of tax deducted or collected not

deposited to the credit of the

Central Government out of

(6) and (8).

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10)

BPL… 194A INTEREST 100000 75000 50000 5,000 25000 1250 NIL

CA Deepak Maheshwari, Indore

Clause-34 (b)

whether the assessee has furnished the statement of tax deducted or tax collected within the prescribed time. If not, please furnish the details :

TAN Type of Form

Due Date for

furnishing

Date of Furnishing, if

furnished.

Whether the statement of Tax deducted or collected

contains information about all transactions which are

required to be reported.

(1) (2) (3) (4) (5)

CA Deepak Maheshwari, Indore

Clause-34 (c)

whether the assessee is liable to pay interest under section 201(1A) or section 206C(7).If yes, please furnish:

TAN Amount of Interest Payable

Amount paid out of Col. (2)

Date of Payment

(1) (2) (3) (4)

CA Deepak Maheshwari, Indore

Applicable for all assessee

Huge, voluminous & detailed information required

To avoid reporting under (b) , suggest clients to timely file TDS returns & pay TDS within due time.

Problem in conducting Tax Audit of Bank Branch

CA Deepak Maheshwari, Indore

Clause -36

In the case of a domestic company, details of tax on distributed profits under section 115-O in the following form :-

(a) Total amount of distributed profits;

(b) Amount of reduction as referred to in section 115-O(1A)(i);

(c) Amount of reduction as referred to in section 115-O(1A)(ii);

(d) Total tax paid thereon;

(e) Dates of payment with amounts

CA Deepak Maheshwari, Indore

Two points inserted in old TAR for reduction from

distributed profit 115-O(1A)(i) & 115-O(1A)(ii) which

is related to dividend received from subsidiary

company & dividend paid to any person for and on

behalf of the new pension system trust referred in

section 10(44).

CA Deepak Maheshwari, Indore

Clause-37

Whether any cost audit was carried out, if yes, give the details, if any, of disqualification or disagreement on any matter/item/value/quantity as may be reported/identified by the cost auditor.

Whether any audit was conducted under the Central Excise Act, 1944, if yes, give the details, if any, of disqualification or disagreement on any matter/item/ value/quantity as may be reported/identified by the auditor.

Clause- 38

CA Deepak Maheshwari, Indore

Whether any audit was conducted under section 72A of the Finance Act,1994 in relation to valuation of taxable services, Finance Act,1994 in relation to valuation of taxable services, if yes, give the details, if any, of disqualification or disagreement on any matter/item/value/quantity as may be reported/identified by the auditor.

Clause-39

CA Deepak Maheshwari, Indore

Now report to be made of disqualification or disagreement as reported in cost audit report/Excise report/Service Tax report.

Earlier only requirement of attaching that audit report was prescribed.

Service Tax Audit report clause, newly inserted.

CA Deepak Maheshwari, Indore

Clause - 40

Details regarding turnover, gross profit, etc., for the previous year and preceding previous year :

Serial number Particulars Previous year

Preceding previous year

1. Total turnover of the assessee

2. Gross profit/turnover

3. Net profit/turnover

4. Stock-in-trade/turnover

5. Material consumed/finished goods produced

CA Deepak Maheshwari, Indore

Ratio analysis to be given for previous year & preceding previous year

Total turnover comparison has been added

Annexure – A has been deleted.

CA Deepak Maheshwari, Indore

Clause - 41

Please furnish the details of demand raised or refund issued during the previous year under any tax laws other than Income Tax Act, 1961 and Wealth tax Act, 1957 along with details of relevant proceedings.

CA Deepak Maheshwari, Indore

Furnish details of demand raised/refund issued under any other act along with relevant proceeding

CA Deepak Maheshwari, Indore

Thanks

&

Best Wishes

For

HECTIC AUDIT SEASON AHEAD

CA Deepak Maheshwari, Indore

Prepared & Presented by:-

CA Deepak MaheshwariMob. 9827233731