seminar 07092013 gopalji

TRANSCRIPT

NORTHERN INDIA REGIONAL COUNCIL

OF THE INSTITUTE OF CHARTERED

ACCOUNTANTS OF INDIASATURDAY, SEPTEMBER 7, 2013

ACCOUNTING FOR REAL ESTATE

TRANSACTIONS

GOPAL JI AGRAWALB.COM LLB DISA IFRS (ICAI)

For any query, discussion or suggestion, please mail at [email protected] +91 9811264160

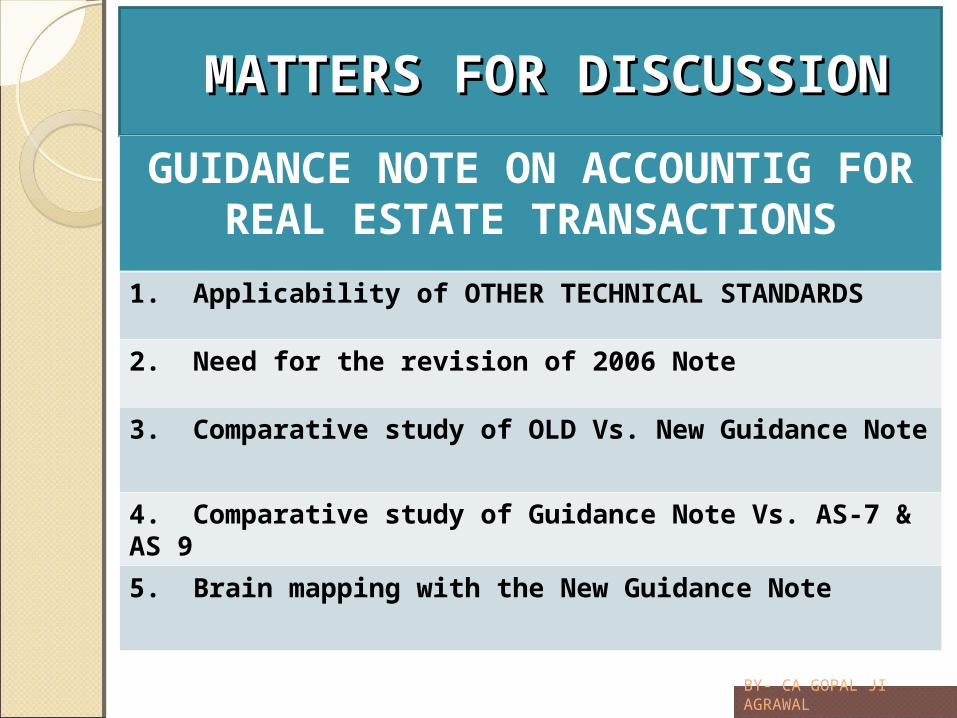

MATTERS FOR MATTERS FOR DISCUSSIONDISCUSSION

BY- CA GOPAL JI AGRAWAL

GUIDANCE NOTE ON ACCOUNTIG FOR REAL ESTATE TRANSACTIONS

1. Applicability of OTHER TECHNICAL STANDARDS

2. Need for the revision of 2006 Note

3. Comparative study of OLD Vs. New Guidance Note

4. Comparative study of Guidance Note Vs. AS-7 & AS 95. Brain mapping with the New Guidance Note

Guidance Note on Accounting Guidance Note on Accounting for for

Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

Whether any AS or GN was applicable for real estate transactions before the issuance of this Guidance Note?

Whether AS 7 or AS 9 or this GN governs the accounting of real estate transactions?

Whether any other AS/GN is also considered for such RET?

What is the impact of this GN on the industry?

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

MANDATORY

1. Framework for the preparation and presentation of FSs

2. Disclosure of Accounting Policies[AS-1/IAS1]

3. Changes in Accounting Policies [AS-5/IAS 8]

4. Construction Contracts [AS -7/IAS11]

5. Revenue Recognition [AS-9/IAS18]

6. Borrowing Costs [AS -1AS 23 ]

7. Provisions, CL & CA [AS-29/IAS37]

8. Inventories (though NA) [AS-2/IAS 2]

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

Recommendatory

1. Guidance note on Accounting for Real Estate Transactions [IFRIC 15]

2. Guidance note on turnover in case of contractors

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

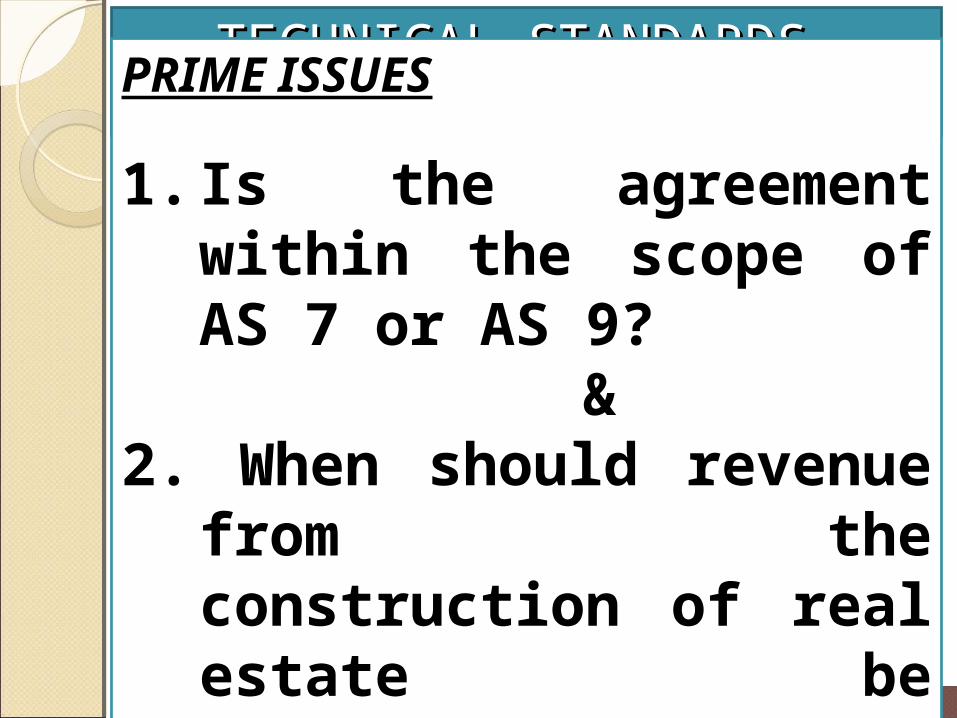

PRIME ISSUES

1. Is the agreement within the scope of AS 7 or AS 9?

&2. When should revenue

from the construction of real estate be recognized?

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

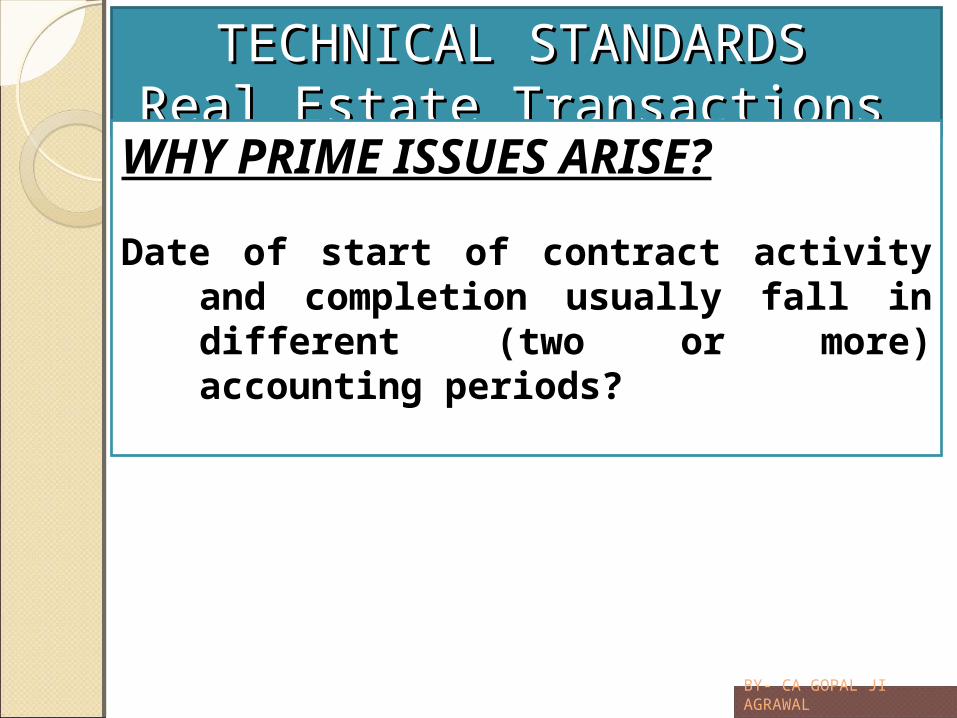

WHY PRIME ISSUES ARISE?

Date of start of contract activity and completion usually fall in different (two or more) accounting periods?

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

Contractor Vs. Contractee

Or Seller Vs. Buyer

AS 7 Vs. AS 9

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

GN states that economic substance of the transaction will determine whether it would fall in AS 7 or AS 9.

GN further states that since in real estate transactions, the major terms and conditions are similar to principles in AS 7, hence usually, AS 7 should be applied.

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

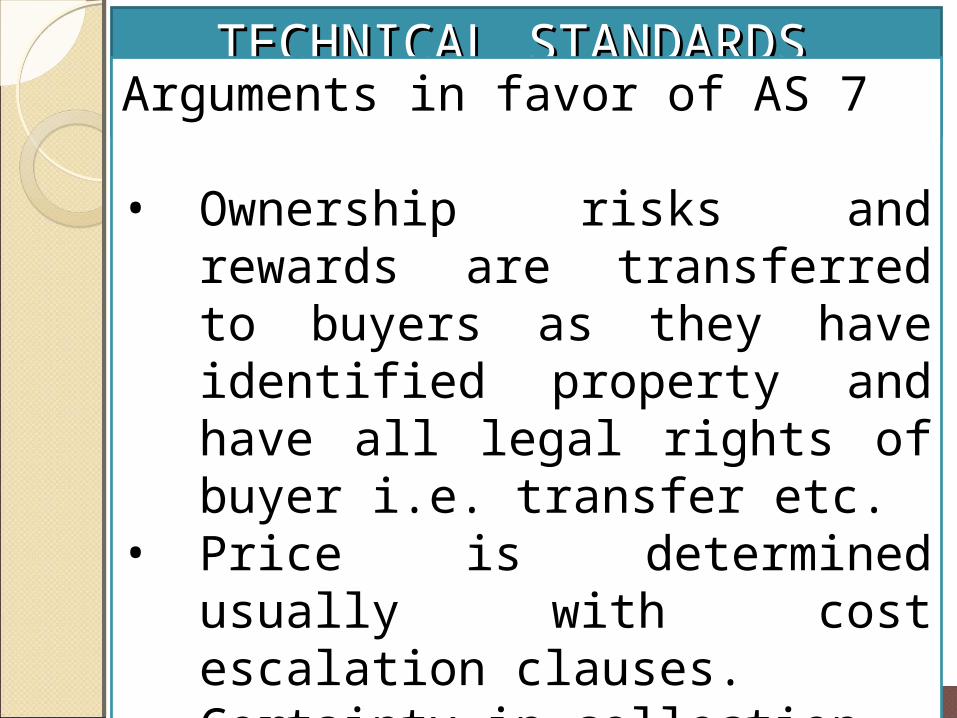

Arguments in favor of AS 7

• Ownership risks and rewards are transferred to buyers as they have identified property and have all legal rights of buyer i.e. transfer etc.

• Price is determined usually with cost escalation clauses.

• Certainty in collection

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

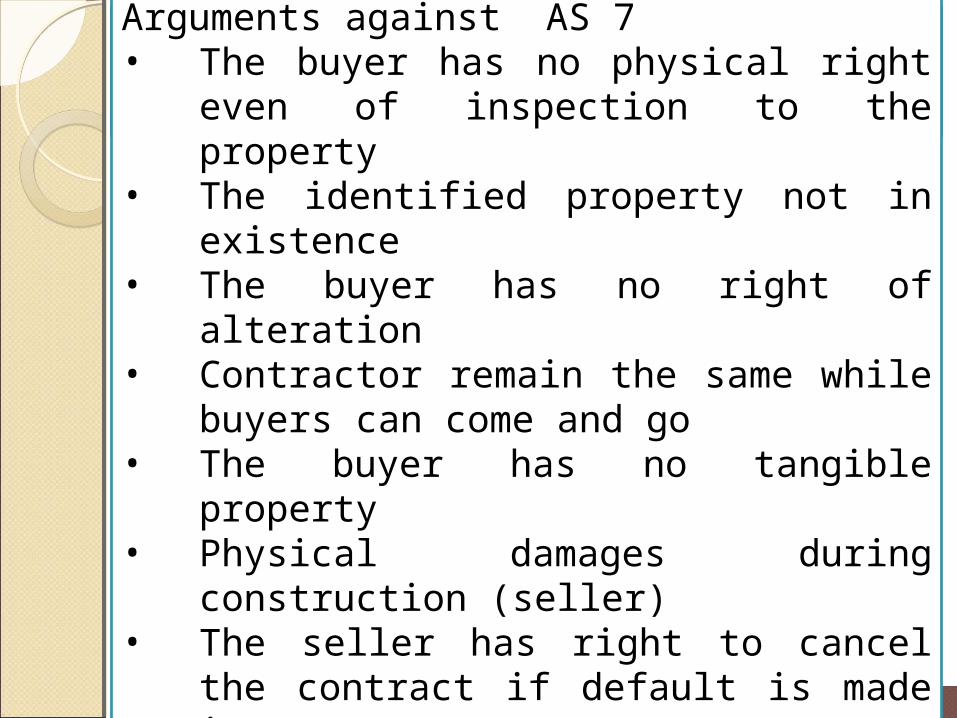

Arguments against AS 7 • The buyer has no physical right even

of inspection to the property• The identified property not in

existence• The buyer has no right of alteration • Contractor remain the same while

buyers can come and go • The buyer has no tangible property • Physical damages during construction

(seller)• The seller has right to cancel the

contract if default is made in payment• Take precaution in buy back and

guaranteed %

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

Per IFRIC 15 For a construction contract

When the buyer is able to specify the major structural elements of the design of the real estate before construction and/or specify major structural changes once construction is in progress.IAS11

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

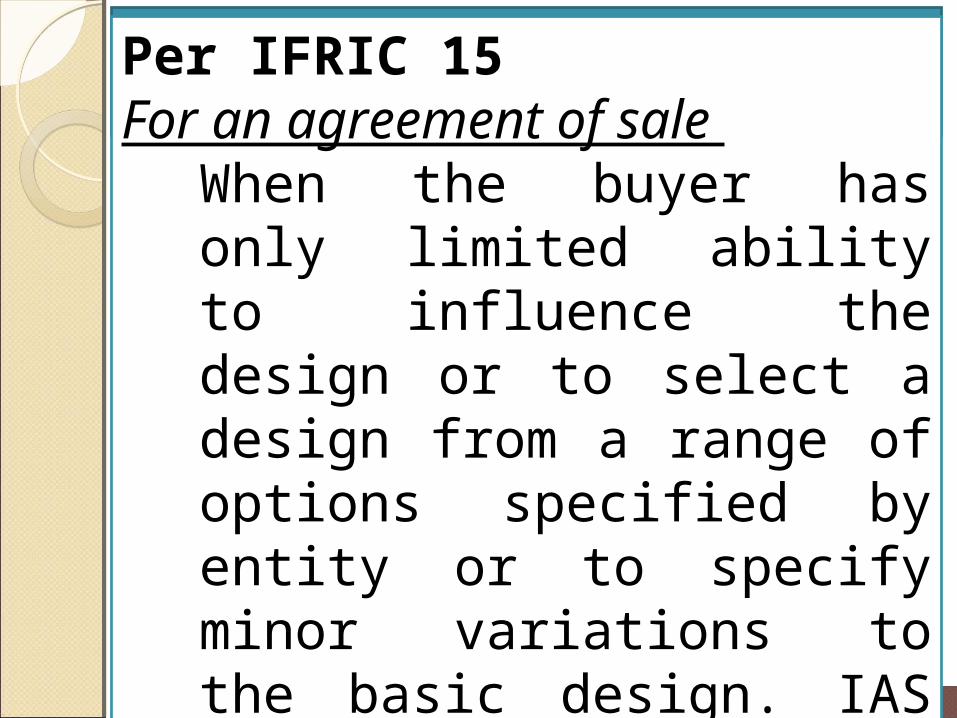

Per IFRIC 15 For an agreement of sale

When the buyer has only limited ability to influence the design or to select a design from a range of options specified by entity or to specify minor variations to the basic design. IAS 18

TECHNICAL STANDARDS TECHNICAL STANDARDS Real Estate Transactions Real Estate Transactions

BY- CA GOPAL JI AGRAWAL

AS 7 Construction contracts [2002]1. Applicable for construction contracts of

any assets 2. Real estate transactions not dealt with

separately 3. Only PCM is recognized. (CCM

permitted earlier)4. Applicable for contractors only (earlier

version covered construction in own a/c)

Before 2006, EAC had opined that AS-9 should be followed in real estate transaction.

NEED FOR REVISION OFNEED FOR REVISION OFGUIDANCE NOTE [2006]GUIDANCE NOTE [2006]

BY- CA GOPAL JI AGRAWAL

What was the need for revision of the earlier Guidance Note [2006]

What aspects have been brought in by the new GN?

When this GN would be applicable?

NEED FOR REVISION OFNEED FOR REVISION OFGUIDANCE NOTE [2006]GUIDANCE NOTE [2006]

BY- CA GOPAL JI AGRAWAL

No guidance in respect of:

• Whether land costs should be included in computing in stage of completion in PCM

• Whether borrowing costs should be included in computing stage of completion in PCM

• No threshold limit for stage of completion

• Not dealt with the TDRs

BROADER GUIDELINES IN BROADER GUIDELINES IN GUIDANCE NOTE [2012]GUIDANCE NOTE [2012]

BY- CA GOPAL JI AGRAWAL

1. Scope specified in detail – land, building, TDRs

2. Definitions of project and project costs

3. AS-9 permitted if economic substance is similar to sale of goods while old GN states if conditions of AS 9 satisfy, apply AS 7.

4. Additional conditions for threshold limits, minimum sale and collection specified. -Rules

5. Items to be considered for threshold costs

6. Additional detailed disclosures required.

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Real Estate Transactions Applicability

• Land, buildings and rights in relation thereto.

• Real estate developers, builders, contractors, sellers i.e. only contractors

Not Applicable for transactions covered in AS-7

• Any asset like plant & machinery, ships, roads, dams, bridge, tunnel, software etc.

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Not Applicable for real estate transactions covered in

AS 10 Accounting for fixed assetsAS 12 Accounting for

government grantsAS 19 LeasesAS 26 Intangible assets

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

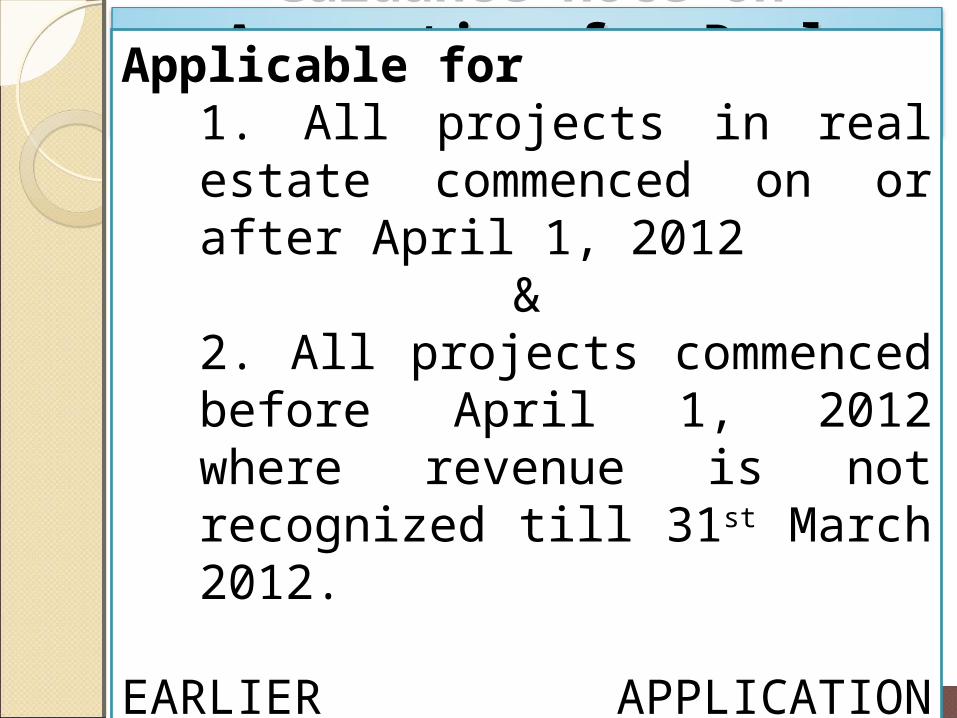

Applicable for1. All projects in real estate commenced on or after April 1, 2012

&2. All projects commenced before April 1, 2012 where revenue is not recognized till 31st March 2012.

EARLIER APPLICATION PERMITTED

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Project (Determination is significant)

Project is smallest group of units/plots/saleable space linked with common set of amenities available and functional to make it ready for intended effective use.

A SINGLE TOWER/TOWNSHIP CAN BE PROJECT

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Project Costs – Direct/attributable/allocable

1. Cost of land and development rights

2. Borrowing costs (AS-16)3. Construction and development

costs• Land conversion, sanction & approvals• Material & labour• Depreciation/hire charges, freight of

P&M • Design and technical assistance• Costs of rectification, guarantee,

warranty• Claims from third parties• Insurance

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

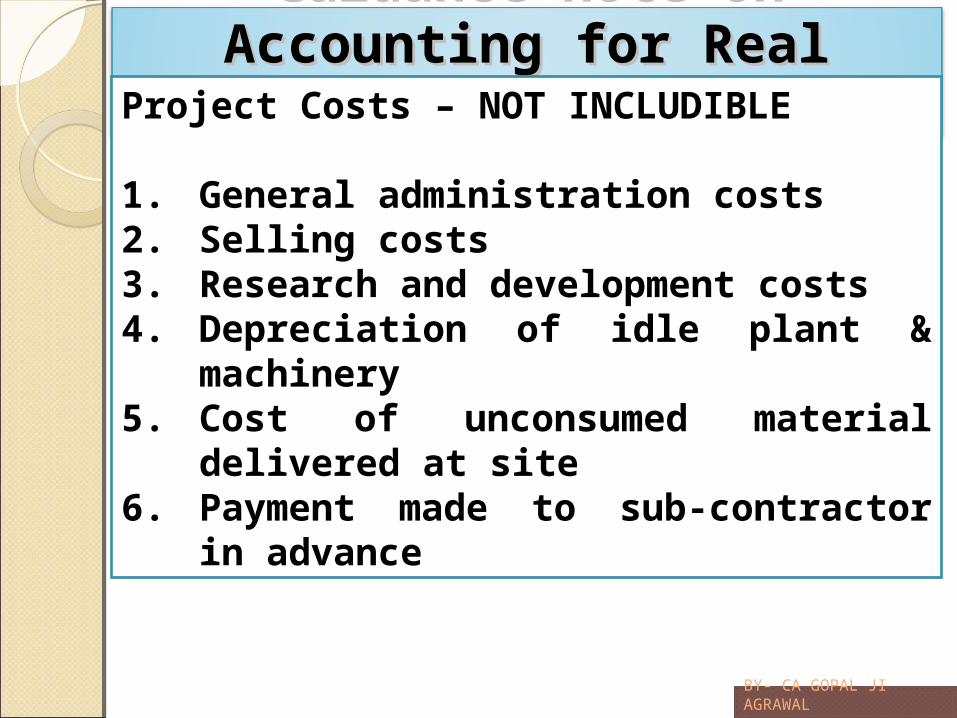

Project Costs – NOT INCLUDIBLE

1. General administration costs2. Selling costs3. Research and development costs4. Depreciation of idle plant &

machinery5. Cost of unconsumed material

delivered at site6. Payment made to sub-contractor

in advance

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

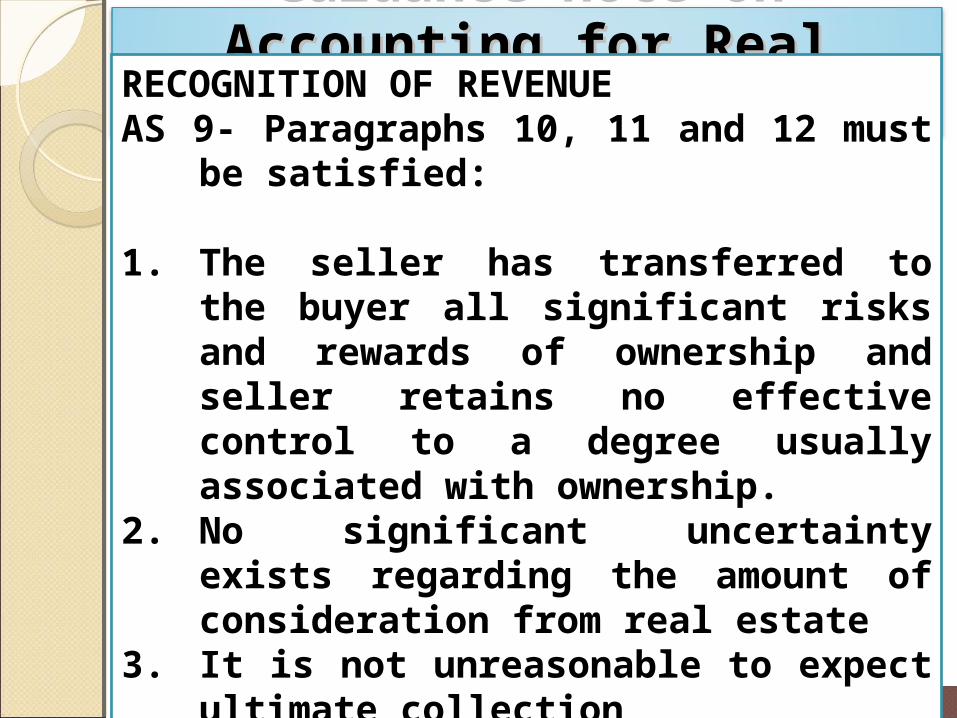

RECOGNITION OF REVENUEAS 9- Paragraphs 10, 11 and 12 must

be satisfied:

1. The seller has transferred to the buyer all significant risks and rewards of ownership and seller retains no effective control to a degree usually associated with ownership.

2. No significant uncertainty exists regarding the amount of consideration from real estate

3. It is not unreasonable to expect ultimate collection

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Application of PCM- economic substance is similar to AS-7 Construction contracts associated with following conditions:

• Project > 12 months, falling in 2 periods

• Most construction contract features exist like land development, structural engineering, design

• Despite several buyers but delivery is interdependent and interrelated having common amenities

• Construction and development activity form significant proportion of project activity

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Application of PCM- when the outcome of Project can be estimated reliably with ALL below:

1. Total project revenue can be estimated reliably

2. Probable that economic benefits will in flow

3. Estimated total project costs and stage of project completion at reporting date can be measured reliably.

4. Projects costs attributable to project can be clearly identified and measured reliably so that actual costs incurred can be compared with prior estimates.

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

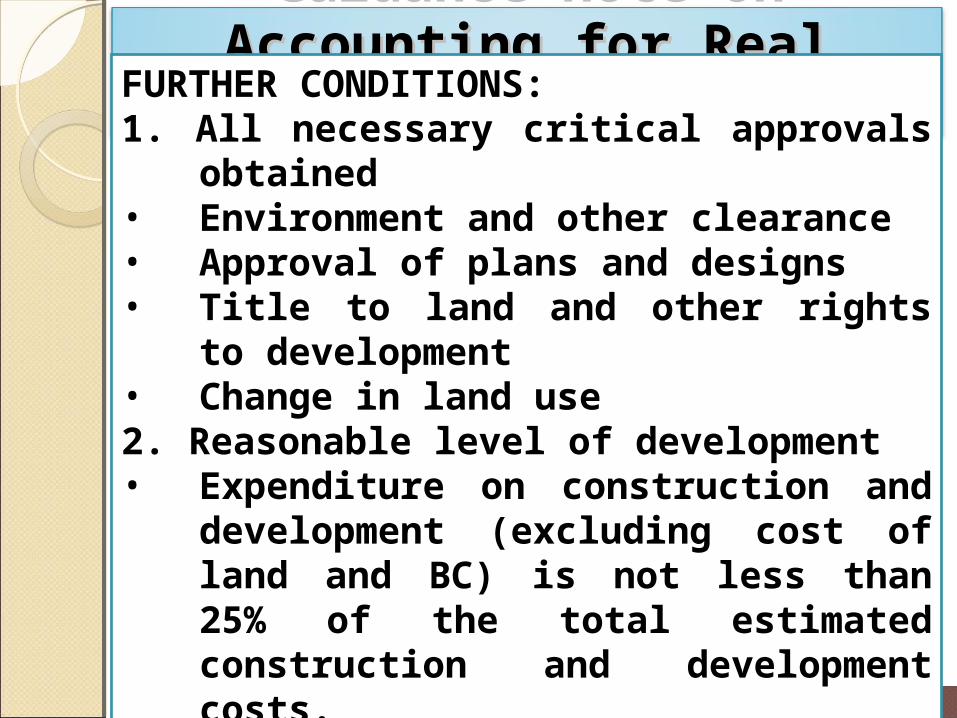

FURTHER CONDITIONS:1. All necessary critical approvals

obtained• Environment and other clearance• Approval of plans and designs• Title to land and other rights to

development• Change in land use2. Reasonable level of development• Expenditure on construction and

development (excluding cost of land and BC) is not less than 25% of the total estimated construction and development costs.

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

FURTHER CONDITIONS:3. At least 25% of the

saleable project area is secured by contracts or agreements with the buyers.

4. At least 10% of the total revenue as per agreements of sale are realized at the reporting date in respect of each of the contract

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Determination of stage of completion:

Project costs incurred but other methods are not prohibited like survey of work done, technical estimation

BUTRevenue can not exceed as computed

by project costs incurred method

It reflects the economic activity/performance during the period

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

ESTIMATED LOSS OF THE PROJECT

When it is probable that total project costs will exceed total project revenue, the expected loss is charged as an expense irrespective of

• Commencement of project work• Stage of completion of the project

activity

Change in estimate of project costs is change in estimate only.

Other significant items ACs , furniture should be componentized and a/for separately.

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Disclosures:1. Project revenue recognized2. Method used to determine project

revenue3. Method used to determine state of

completion

Disclosures for project in progress:1. Total costs incurred and profit/loss

recognized2. Amount of advance received3. Amount of WIP and value of

inventories4. Excess of revenue over actual bills

raised (unbilled)

Guidance note on Guidance note on Accounting for Real Estate Accounting for Real Estate

Transactions [2012]Transactions [2012]

BY- CA GOPAL JI AGRAWAL

Whether the Revised Guidance Note necessitates the change in Accounting Policy?

What additional disclosures are required?

Whether the Industries in the real estate segments are following AS 7 or AS 9?

Whether the GN would increase or decrease accounting income?

REVENUE RECOGNITIONREVENUE RECOGNITIONHDIL [2012 & 2013]HDIL [2012 & 2013]

BY- CA GOPAL JI AGRAWAL

The Company follows completed project method of accounting (“Project Completion Method of Accounting”). Allocable expenses incurred during the year are debited to work-in-progress account.

REVENUE RECOGNITIONREVENUE RECOGNITIONL & T Ltd. [2012]L & T Ltd. [2012]

BY- CA GOPAL JI AGRAWAL

A. Cost plus contract: Cost + proportionate margin

B. Fixed price contracts: 1. To the extent of cost incurred till outcome of the contract cannot be ascertained reliably.2. Others- PCM based on costs incurred.

Remarks: No percentage specified.Silent about the land/BC costs.

REVENUE RECOGNITIONREVENUE RECOGNITIONL & T Ltd. [2013]L & T Ltd. [2013]

BY- CA GOPAL JI AGRAWAL

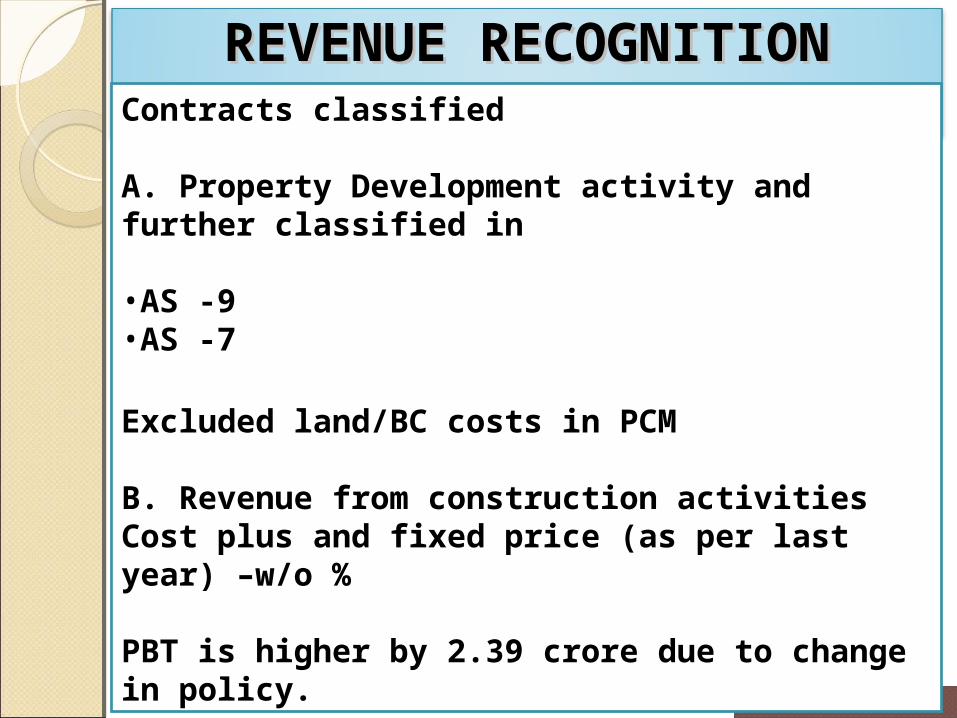

Contracts classified

A. Property Development activity and further classified in

•AS -9 •AS -7

Excluded land/BC costs in PCM

B. Revenue from construction activitiesCost plus and fixed price (as per last year) –w/o %

PBT is higher by 2.39 crore due to change in policy.

REVENUE RECOGNITIONREVENUE RECOGNITIONOMAXE [2012]OMAXE [2012]

BY- CA GOPAL JI AGRAWAL

Activities dividend into

A.Real Estate: PCM with 30% including cost of land

B. Contract : PCM but no disclosure as to % as certified by client not with regard to costs incurred.

REVENUE RECOGNITIONREVENUE RECOGNITIONOMAXE [2013]OMAXE [2013]

BY- CA GOPAL JI AGRAWAL

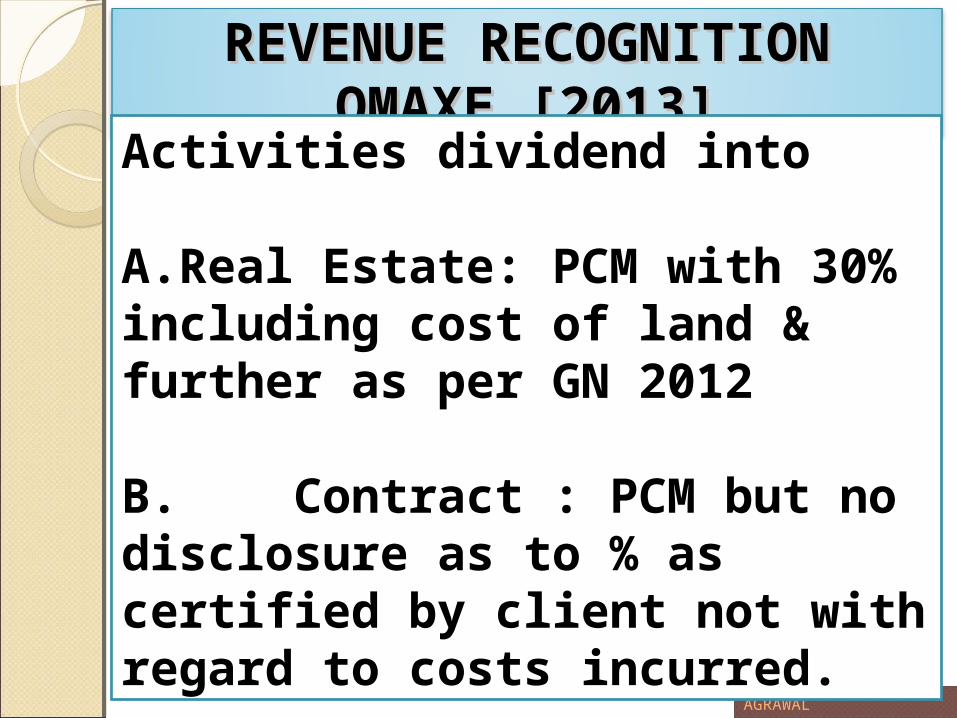

Activities dividend into

A.Real Estate: PCM with 30% including cost of land & further as per GN 2012

B. Contract : PCM but no disclosure as to % as certified by client not with regard to costs incurred.

REVENUE RECOGNITIONREVENUE RECOGNITIONPDL [2012]PDL [2012]

BY- CA GOPAL JI AGRAWAL

Activities dividend into

A.Real Estate: PCM with 30% including cost of land

B. Contract : PCM but no disclosure as to %

An humble appealI will acknowledge your critical comments and suggestions for

making our Coming Deliberations

more effective and copious

Gopal Ji AgrawalB.COM LLB DISA IFRS (ICAI)

For any query, discussion or suggestion, please mail at