selected far cost principles: ir&d, b&p, selling and ... public relations costs; broadly...

TRANSCRIPT

Selected FAR Cost Principles:

IR&D, B&P, Selling and Related

Costs

Phillip R. SeckmanGale R. Monahan

• The “Selling” Cost Family

• Selling Costs

• Advertising/Public Relations Costs

• Market Planning

• Lobbying Costs

• B&P Costs

• IR&D Costs

• MP&E Costs

2

Introduction

The "Selling" Cost Family

3

• Complex area of cost and fact-driven• Selling Costs (31.205-38)

• Public Relations and Advertising Costs (31.205-1)

• Economic Planning Costs (31.205-12)

• Entertainment Costs (31.205-14)

• IR&D/B&P Costs (31.205-18)

• Manufacturing & Production Engineering (31.205-25)

• Lobbying and Political Activity Costs (31.205-22)

• Organization Costs (31.205-27)

• Recruitment Costs (31.205-34)

• Trade, business, technical and professional activity costs (31.205-43)

• Training and education costs (31.205-44)

• Travel Costs (31.205-46)

• Alcohol Costs (31.205-51)

4

Selling and Related Costs

• “Selling” is a generic term encompassing all efforts to market

the contractor’s products or services (FAR 31.205-38)

• Limits allowability to five categories of selling type costs:

• Advertising (FAR 31.205-1): the use of media to promote the sale

of products or services; narrow/limited rules for allowability

• Corporate Image Enhancement (FAR 31.205-1): generally

includes public relations costs; broadly targeted sales efforts

• B&P costs (FAR 31.205-18): costs incurred in preparing,

submitting, and supporting bids and proposals

• Market Planning (FAR 31.205-12): market research and analysis

and general management planning concerned with business

development; long-range economic planning costs under

5

Selling Costs

• Five allowable categories (cont.)

• Direct selling: acts or actions to induce particular customers

to purchase particular products or services by person-to-

person contact.

• Familiarization of potential customers with products or

services, conditions of sale, service capabilities, etc.

• Negotiation, liaison between customer and contractor,

technical and consulting efforts, individual demonstrations

• Any other efforts “having as their purpose the application or

adaptation of the contractor’s products or services for a

particular customer’s use”

• Seller compensation, fees, commissions limited to bona

fide employees/established commercial agency

6

Selling Costs (cont.)

• “Person-to-person” contact

• Generally occurs prior to issuance of RFP (communication

is unlikely after RFP is issued)

• Distinction is important: selling can include technical effort

similar to IR&D where direct selling is primary purpose

• Prototype construction that involves no development

(e.g., Technical Readiness Level remains unchanged)

• Design effort to permit use of a product for a particular

application that involves no development

(e.g., application engineering)

• Development to pursue single potential contract opportunity

(e.g., to demonstrate a capability)

7

Identifying Direct Selling Costs

• Pre-RFP presentation to existing customer about products

and capabilities

• Pre-RFP presentation to potential customer about

products and capabilities

• Development of a prototype aircraft (Gen. Dynamics Corp.

v. United States, 202 Ct. Cl. 347 (1973))

• Customer is considering updates to its software and asks

whether contractor offers a better product; contractor

responds

8

Distinguishing Selling Costs

• Public Relations/Advertising (FAR 31.205-1)

• Unallowable includes

• Costs whose primary purpose is to promote sale of products

or services by stimulating interest in a product or product line

• Costs of enhancing company image to sell products

• Costs of meetings, symposia, etc. when principal purpose is

other than dissemination of technical information or stimulation

of production

• Allowable includes

• Community service

• Communicating with public

• General liaison to keep public informed on matters of public

concern

9

PR/Advertising Costs

• Trade, Business, Technical and Professional Activity Costs

(FAR 31.205-43)

• Allowable when “principal purpose” of a meeting,

conference, etc. is “dissemination of trade, business,

technical or professional information”

• Costs of organizing, sponsoring meetings, including rentals,

incidentals, subsistence, transportation, etc.

• Business meals

• Includes travel costs

• Costs of non-employees (i.e., consultants) when attendance

is “essential"

10

Trade, Business, Technical and Professional Activity

Costs

• Unallowable lobbying costs include (FAR 31.205-22)

• Costs to influence executive branch personnel to give

consideration to or act regarding a regulatory or contract

matter on any basis “other than the merits”

• Key distinction is whether efforts are “on the merits”

• Direct selling to the government may be allowable if based

purely on the merits of the product/service (FAR 31.205-

38(b)(5), 31.205-22(a)(6), 3.401)

• Allowable efforts may include:

• Meeting with executive branch employee to discuss attributes

of specific products

• Meeting with DOD program manager encouraging support for

proposed program based on program benefits

11

Lobbying Costs

• 31 U.S.C. 1352 (2000), FAR Subpt. 3.8• Prohibits use of “appropriated” funds to influence any type of

federal award

• Requires disclosure of payments made to outside lobbyists to influence an award

• Influencing an award includes an extension, renewal or modification, or the earmarking of funds for a particular program within a bill

• Unless an exception applies, the costs of such activities are unallowable; an unallowable charge code should be used to capture this effort

• While disclosure applies only to federal awards >$150K, costs of Byrd activities for all awards (regardless of value) are still unallowable (FAR 3.808, 31.205-22, 52.203-11)

• Flow to sub-awardees (FAR 52.203-12)

• Standard Form LLL requires identification of LDA registrants engaged in covered activities for that award (but not internal employees)

• Awardee must certify that appropriated funds not used for lobbying

12

Lobbying/Byrd Amendment

• Look to the “principal function”

• Gen. Dynamics, ASBCA No. 12814, 68-2 BCA ¶ 7,297

• FAR 31.204(d): When more than one subsection is

relevant the cost shall be apportioned; if apportionment

cannot be performed, then allowability based on section

that most specifically deals with or best captures the

essential nature of the cost at issue

• Selling v. Lobbying?

• Selling v. IR&D?

• Selling v. Professional Costs?

Multi-Purpose Costs: Which Cost Principle Applies?

13

• Sampling

• Ramifications of unallowable costs: Business Systems

deficiencies, penalties, CAS 405

• Robust systems/policies

• Training

• Document

• Plan ahead vs. retroactive characterization

• DCAA favorite: targeting business purpose for things like

travel and business meals

14

Best Practices/Ramifications

B&P Costs

15

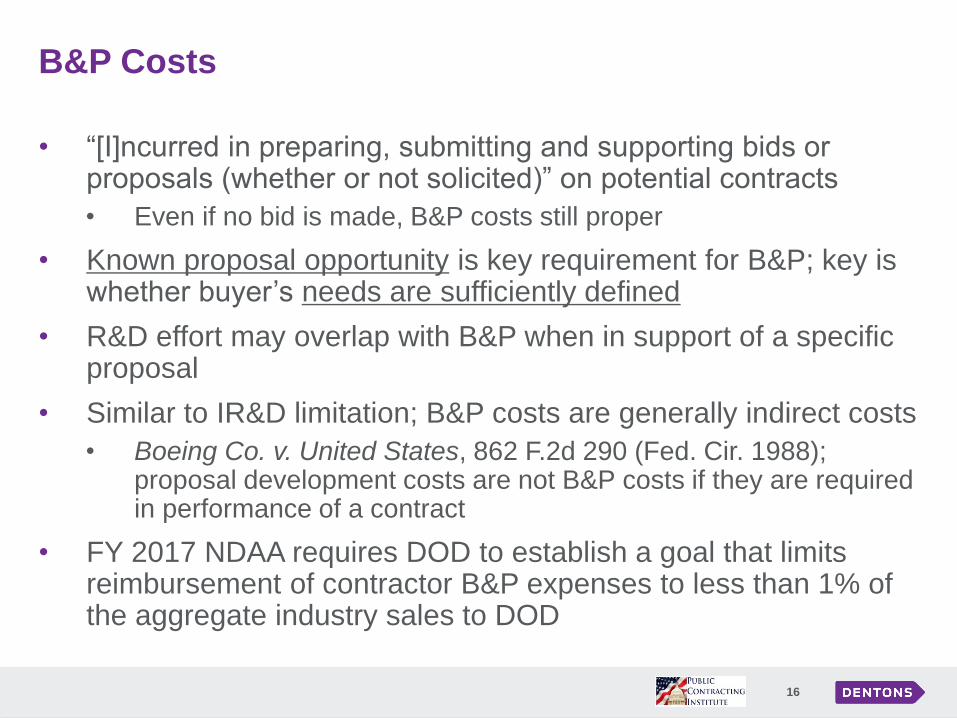

• “[I]ncurred in preparing, submitting and supporting bids or proposals (whether or not solicited)” on potential contracts

• Even if no bid is made, B&P costs still proper

• Known proposal opportunity is key requirement for B&P; key is whether buyer’s needs are sufficiently defined

• R&D effort may overlap with B&P when in support of a specific proposal

• Similar to IR&D limitation; B&P costs are generally indirect costs

• Boeing Co. v. United States, 862 F.2d 290 (Fed. Cir. 1988); proposal development costs are not B&P costs if they are required in performance of a contract

• FY 2017 NDAA requires DOD to establish a goal that limits reimbursement of contractor B&P expenses to less than 1% of the aggregate industry sales to DOD

16

B&P Costs

IR&D Costs

17

• IR&D is research and development that is not sponsored by a grant and “is not required in the performance of a contract”

• CAS 420; FAR 31.205-18: FAR and CAS definitions are the same (ATK Thiokol Inc. v. United States, 68 Fed. Cl. 612 (2005), aff’d 598 F.3d 1329 (Fed. Cir. 2010))

• If R&D cost is not specifically required by a contract, then it is not required in the performance of the contract and may qualify as IR&D

• IR&D costs are allowable when they meet the requirements of

• FAR 31.205-18

• DFARS 231.205-18

• CAS 420 (when applicable)

18

IR&D

• Two recent rules affect IR&D Costs

• DFARS Case 2016-D017 (still pending)

• Ensure that IR&D expenses as a means to reduce evaluated

bid prices in competitive source selections are evaluated in a

uniform way during competitive source selections

• Changes to DFARS Pt. 231

• Ensure that both contractors and DOD have sufficient

awareness of each other's efforts and to provide industry with

feedback on the relevance of proposed IR&D efforts

19

IR&D Cost Updates

• DFARS Case 2016-D017; Advanced Notice of Proposed

Rulemaking, IR&D Expenses, 81 Fed. Reg. 6,488 (Feb. 8,

2016)

• Requires offerors to describe in detail the nature and value

of prospective IR&D projects

• Notes that the “intended purpose of IR&D” is not to gain a

price advantage in a specific competitive bid

• On Feb. 2, 2017, the comment period closed for the

proposed rule

• Dentons submitted comments

IR&D Cost Developments Proposed Change

20

• Rule presents potential issues for contractors

• DOD position that IR&D costs are contract costs

• Proposed price adjustments penalize contractors for

conducting IR&D

• Requires contractors to provide cost or pricing data with

competitive procurements

• Ignores that contractors are permitted to use IR&D,

undertaken at their own risk, to gain a relative price and

technical advantage (Raytheon Co. v. United States, 809

F.3d 590, 593 (Fed. Cir. 2015))

• The fact that contractors are not required to complete IR&D

projects does not present a significant risk to DOD because

contractors are required to perform contracts or risk default

21

Price Adjustments for Future IR&D Costs

• Changes to DFARS Pt. 231

• Proposed IR&D efforts must be communicated to

appropriate DOD personnel prior to initiation (“technical

interchange”) for the costs to be allowable

• Requires annual reports on progress

• Rule applies to major contractors (i.e., those allocating more

than $11M in IR&D and B&P costs to covered-contracts in

the prior FY)

• Effective Nov. 4, 2016

22

IR&D Cost Developments: Final DFARS Rule

• New DFARS final rule makes IR&D cost allowability contingent upon compliance with certain reporting and oversight requirements

• Beginning in a contractor's FY 2017, IR&D costs are only allowable on DOD contracts, if prior to incurring IR&D costs, contractors:

• Provide summary information regarding ongoing and completed IR&D projects to ACO and DCAA; and

• Communicate proposed IR&D efforts to appropriate DOD personnel by means of a “technical interchange”

• This requirement was delayed by DOD for FY2017; must conduct technical interchange in FY 2017, not before IR&D cost are incurred

• Beginning in FY 2018, technical interchange must occur prior to start of IR&D project or the costs may be unallowable

23

IR&D Cost Allowability

MP&E Costs

24

• R&D to improve the quality and efficiency of production

processes, reduce manufacturing costs or utilize modern

production methods

• Focuses on development of the means to manufacture a

product

• Includes materials, equipment and tool development,

provided the company does not intend to sell the equipment

• Very similar to IR&D, but distinction may be important

• IR&D allocated over G&A base

• MP&E often allocated over overhead base

• M&PE costs frequently occur late in IR&D process, or just

after completion of IR&D effort

25

MP&E

Phil Seckman

303.364.4338

Gale Monahan

303.634.4311

Questions?

26

Thank you

Dentons US LLP

1400 Wewatta Street

Suite 700

Denver, CO 80202-5548

United States

Dentons is the world's largest law firm, delivering quality and value to clients around the globe. Dentons is

a leader on the Acritas Global Elite Brand Index, a BTI Client Service 30 Award winner and recognized by

prominent business and legal publications for its innovations in client service, including founding Nextlaw

Labs and the Nextlaw Global Referral Network. Dentons' polycentric approach and world-class talent

challenge the status quo to advance client interests in the communities in which we live and work.

www.dentons.com.

© 2017 Dentons. Dentons is a global legal practice providing client services worldwide through its member firms and affiliates. This publication is not designed to provide legal advice and you should not take, or refrain from taking, action based on its content. Please see dentons.com for Legal Notices.