security analysis and portfolio mgt 28-9-21

TRANSCRIPT

SECURITY ANALYSISAND PORTFOLIOMANAGEMENT

Anish Thomas Jithin JoyAssistant Professor & Head, Assistant Professor,P.G. Department of Commerce, P.G. Department of Commerce,

Deva Matha College, Deva Matha College,Kuravilangad, Kottayam. Kuravilangad, Kottayam.

ISO 9001:2015 CERTIFIED

© No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording and/or otherwise without the prior written permission ofthe authors and the publisher.

FIRST EDITION: 2021

Published by : Mrs. Meena Pandey for Himalaya Publishing House Pvt. Ltd.,“Ramdoot”, Dr. Bhalerao Marg, Girgaon, Mumbai - 400 004.Phone: 022-23860170, 23863863; Fax: 022-23877178E-mail: [email protected]; Website: www.himpub.com

Branch Offices :New Delhi : “Pooja Apartments”, 4-B, Murari Lal Street, Ansari Road, Darya Ganj,

New Delhi - 110 002. Phone: 011-23270392, 23278631; Fax: 011-23256286Nagpur : Kundanlal Chandak Industrial Estate, Ghat Road, Nagpur - 440 018.

Phone: 0712-2721215, 2721216

Bengaluru : Plot No. 91-33, 2nd Main Road, Seshadripuram, Behind Nataraja Theatre,Bengaluru - 560 020. Phone: 080-41138821; Mobile: 09379847017, 09379847005

Hyderabad : No. 3-4-184, Lingampally, Besides Raghavendra SwamyMatham, Kachiguda,Hyderabad - 500 027. Phone: 040-27560041, 27550139

Chennai : New No. 48/2, Old No. 28/2, Ground Floor, Sarangapani Street, T. Nagar,Chennai - 600 017. Mobile: 09380460419

Pune : “Laksha” Apartment, First Floor, No. 527, Mehunpura,Shaniwarpeth (Near Prabhat Theatre), Pune - 411 030.Phone: 020-24496323, 24496333; Mobile: 09370579333

Lucknow : House No. 731, Shekhupura Colony, Near B.D. Convent School, Aliganj,Lucknow - 226 022. Phone: 0522-4012353; Mobile: 09307501549

Ahmedabad : 114, “SHAIL”, 1st Floor, Opp. Madhu Sudan House, C.G. Road, Navrang Pura,Ahmedabad - 380 009. Phone: 079-26560126; Mobile: 09377088847

Ernakulam : 39/176 (New No. 60/251), 1st Floor, Karikkamuri Road, Ernakulam,Kochi - 682 011. Phone: 0484-2378012, 2378016; Mobile: 09387122121

Cuttack : Plot No. 5F-755/4, Sector 9, CDAMarket Nagar, Cuttack - 753 014, Odisha.Mobile: 09338746007

Kolkata : 108/4, Beliaghata Main Road, Near ID Hospital, Opp. SBI Bank,Kolkata - 700 010. Phone: 033-32449649; Mobile: 07439040301

DTP by : Sudhakar Shetty (On behalf of HPH Pvt. Ltd.)Printed at : M/s. Aditya Offset Process (I) Pvt. Ltd., Hyderabad. On behalf of HPH.

PREFACE

This book is a rigorous attempt to help the readers to understand the enthralling subject ofportfolio management in a systematic and lucid form. Portfolio management is the art and scienceof making decisions about investment. It is essential for every human being to invest wisely forthe rainy days and to make their future secure. One can only achieve it by understanding thetheories and practices in portfolio management.

This text book is intended for the THIRD Semester students of the M.Com. (Finance andTaxation Stream) Programme (2019 Admission onwards), under the Credit and Semester System(C.S.S.), offered by the Mahatma Gandhi University, Kottayam. The book consists of fivemodules, which are constituted to address the investment process more proficiently. The firstmodule is intended to make the readers able to understand the concepts of investments, differenttypes of investments and investors, views of investment, avenues for investment, process ofinvestment and sources of investment information. Amidst these important topics, the differencebetween investment, speculation and gambling are also covered in the first module.

From the first module, the foundation can be made, but the castle is yet to be built. Thesecond module and third module help the readers to decide which securities are required toconstruct the portfolio, our castle. To efficiently pick a security, the investor should have theability to assess its risk and intrinsic value. The second module helps the readers to learn how tocalculate the intrinsic value of a security by keeping in mind its risk potential. The module talksabout the various economical, industrial and company related factors to be assessed to determinethe intrinsic value of an asset. A brief detailing of various types of risks and detailed note of bond,bond types, return calculations and other bond related terminologies are also given in this module.

In the third module, the reader can understand various theories and tools for technicalanalysis, which enable the investors to take investment decisions after understanding marketefficiency. Traditional methods like charts, price trends and trend reversals along with moderntechniques like mathematical indicators and market indicators are discussed in this module. Theapplication of fundamental and technical analysis tools are limited to market efficiency. Therefore,different forms of market efficiency along with its measurement techniques are also included inthis module.

After going through previous modules, the reader can now evoke the construction ofportfolio, our castle. The fourth module helps the readers to apply modern portfolio theories andconstruct optimum portfolios. This module gives answers to: What role correlation plays inportfolio construction? How portfolios can be constructed? How the most efficient portfolio canbe selected?, etc.

The castle is constructed. Now, you need to defend it from various threats. The fifth moduleteaches the readers about various techniques to evaluate and revise the portfolio so as to maintainits supremacy.

Once an academician rightly said “It is not true we have only one life to love, if we can read,we can live as many lives and as many kinds of lives as we wish.” So, we tried our best to ensureour readers really do have a quality life with our book. Happy learning!!

August 31, 2021 AUTHORS

SYLLABUS

MAHATMAGANDHI UNIVERSITY, KOTTAYAM, KERALACSS M.Com. Programme – Syllabus & Curriculum

(2019 Admission onwards)Course Code CM010303Title of the Course Security Analysis and Portfolio ManagementSemester ThreeType Core – ElectiveCredits 4Hours 6 per week and Total 108

Objectives of the Course:To create awareness among the learners about different investment avenues and enrich them to handlemodern portfolio techniques to construct efficient portfolios, evaluation and revision of the inefficientportfolios.

CourseOutcomeNo.

Expected Course Outcome CognitiveLevel

ProgrammeSpecificOutcomeLinkage

1 Understanding the concepts of investments, different typesof investments, views of investment and process ofinvestment, and applying the theoretical knowledge ininvestment information for selecting the securities.

Understandand Apply

PSO4, 6

2 Understanding the types of risk in security market andapplying various tools for the valuation of bonds as well aseconomic indicators to predict the market.

Understandand Apply

PSO4, 6

3 Understanding the tools of technical analysis, analysing thepatterns and trends in the market by using various tools, andenable to take investment decisions after understandingmarket efficiency level also.

Understand,Evaluateand Apply

PSO4, 6

4 Applying modern portfolio theories and constructingoptimum portfolios.

Understandand Apply

PSO4, 6

5 Revising constructed portfolios as per risk and returnassociation by using different strategies.

Understandand Apply

PSO4, 6

Unit-wise Arrangement of the Course

Module Sl. No.of Units Contents of the Unit Remarks

Module 1: Investment (15 hours)

1 1.1 Different views on investment – Types of investment –Characteristics of investment – Objectives of investment.

Short question,Short essay,Long essay

1.2 Types of investors – Investment vs. speculation – Investment vs.gambling – Speculation vs. gambling.

Short question,Short essay

1.3 Assets – Financial assets – Real assets. Short question,Short essay,Long essay

1.4 Investment process – Investment information – Sources ofinvestment information.

Short question,Short essay,Long essay

Module 2: Security Analysis (20 hours)

2 2.1 Security Analysis – Meaning – Tools – Risk – Risk ininvestment – Components – Classification – Systematic risk –Unsystematic risk – Risk measurement – Methods.

Theory andproblems

2.2 Bond: Types, risk, return and valuation – Convexity – Durationof a bond.

Theory andproblems

2.3 Fundamental analysis – Economic analysis – Economicforecasting, economic indicators, diffusion and compositeindices, business confidence index.

Short question,Short essay,Long essay

2.4 Industry analysis: Economy and industry analysis, industrygroups, industry life cycle analysis and structural analysis.

Short question,Short essay,Long essay

2.5 Company analysis: Qualitative analysis, quantitative analysis,methods and tools.

Short question,Short essay,Long essay

Module 3: Technical Analysis and EMH (28 hours)

3 3.1 Meaning – Basic assumptions – Dow theory – Elliot waveprinciples – Neutral network.

Short question,Short essay,Long essay

3.2 Charts: Line charts, bar charts, point and figure charts,candlestick chart – Trends: support and resistance level.

Short question,Short essay,Long essay,Theory

3.3 Chart patterns – Types of trends – Head and shoulders –Inverted head and shoulders – Double top and bottom –Rounding bottom – Triangles, flags and gaps.

Short question,Short essay,Long essay

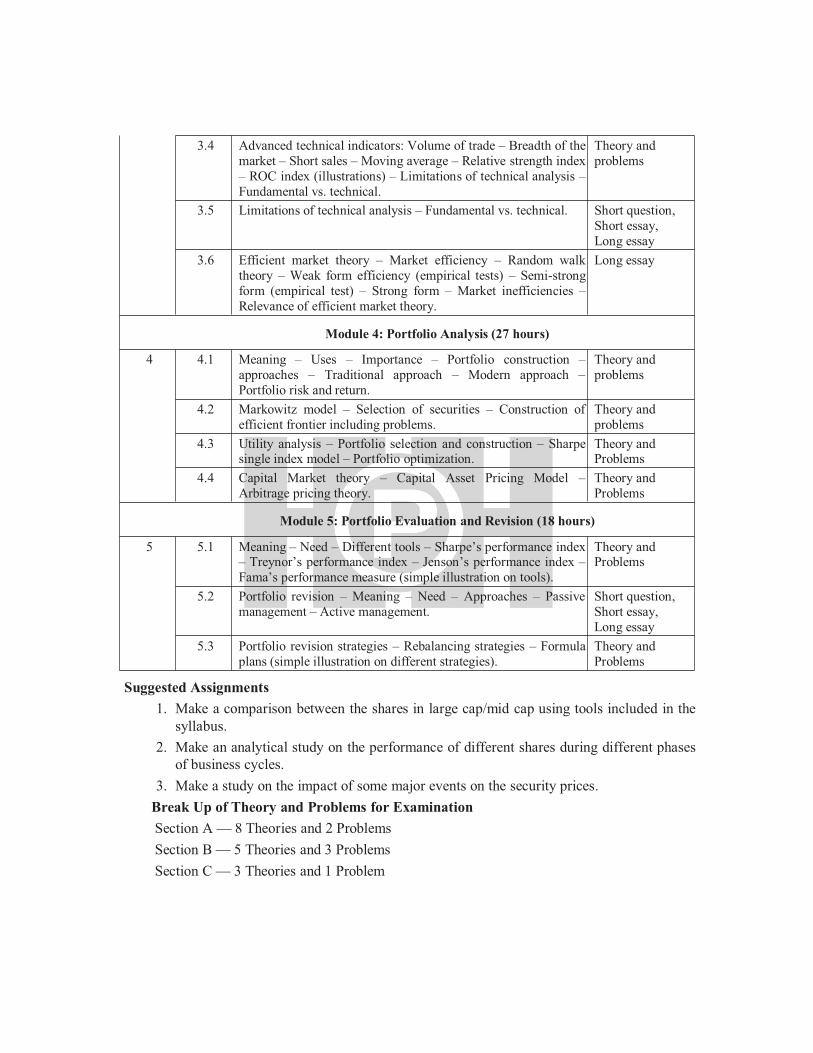

3.4 Advanced technical indicators: Volume of trade – Breadth of themarket – Short sales – Moving average – Relative strength index– ROC index (illustrations) – Limitations of technical analysis –Fundamental vs. technical.

Theory andproblems

3.5 Limitations of technical analysis – Fundamental vs. technical. Short question,Short essay,Long essay

3.6 Efficient market theory – Market efficiency – Random walktheory – Weak form efficiency (empirical tests) – Semi-strongform (empirical test) – Strong form – Market inefficiencies –Relevance of efficient market theory.

Long essay

Module 4: Portfolio Analysis (27 hours)

4 4.1 Meaning – Uses – Importance – Portfolio construction –approaches – Traditional approach – Modern approach –Portfolio risk and return.

Theory andproblems

4.2 Markowitz model – Selection of securities – Construction ofefficient frontier including problems.

Theory andproblems

4.3 Utility analysis – Portfolio selection and construction – Sharpesingle index model – Portfolio optimization.

Theory andProblems

4.4 Capital Market theory – Capital Asset Pricing Model –Arbitrage pricing theory.

Theory andProblems

Module 5: Portfolio Evaluation and Revision (18 hours)

5 5.1 Meaning – Need – Different tools – Sharpe’s performance index– Treynor’s performance index – Jenson’s performance index –Fama’s performance measure (simple illustration on tools).

Theory andProblems

5.2 Portfolio revision – Meaning – Need – Approaches – Passivemanagement – Active management.

Short question,Short essay,Long essay

5.3 Portfolio revision strategies – Rebalancing strategies – Formulaplans (simple illustration on different strategies).

Theory andProblems

Suggested Assignments1. Make a comparison between the shares in large cap/mid cap using tools included in thesyllabus.

2. Make an analytical study on the performance of different shares during different phasesof business cycles.

3. Make a study on the impact of some major events on the security prices.Break Up of Theory and Problems for ExaminationSection A — 8 Theories and 2 ProblemsSection B — 5 Theories and 3 ProblemsSection C — 3 Theories and 1 Problem

CONTENTS

MODULE 1: INVESTMENT 1 – 32

INTRODUCTION TO THE MODULE 11. INVESTMENT PROPERTIES DIFFERENT VIEWS OF INVESTMENT 3

TYPES OF INVESTMENT 4OBJECTIVES OF INVESTMENT 7CHARACTERISTICS OF INVESTMENT 9IMPORTANCE OF INVESTMENT 10

2. INVESTORS INTRODUCTION 11TYPES OF INVESTORS 11SPECULATION 12INVESTMENT VS. SPECULATION 13INVESTMENT VS. GAMBLING 14SPECULATION VS. GAMBLING 15

3. INVESTMENT AVENUES INVESTMENT ALTERNATIVES IN INDIA 164. INVESTMENT PROCESS INVESTMENT PROCESS 21

INVESTMENT INFORMATION 24DESIGNING INVESTMENT PORTFOLIO 27RATIONAL CONSIDERATIONS 28COMPONENTS OF INVESTMENT PORTFOLIO 30REVIEW QUESTIONS 31

MODULE 2: SECURITY ANALYSIS 33 – 95

INTRODUCTION TO THE MODULE 331. SECURITY ANALYSIS ANDRISK

INVESTMENT RISK – TYPES – COMPARISON 35RISK MEASUREMENTS 39RANGE ANALYSIS 39PROBABILITY DISTRIBUTION 40STANDARD DEVIATION 41COEFFICIENT OF VARIATION 42BETA 43ALPHA 44R SQUARE 45VALUE AT RISK (VAR) 45

2. BOND MEANING 47FEATURES 48TYPES OF BONDS 50BOND RISKS 55

RETURN AND VALUATION 56SENSITIVITY OF BOND 64DURATION OF BOND – PRINCIPLES –CALCULATIONS

64

VOLATILITY OF BOND 67CONVEXITY OF A BOND 68

3. FUNDAMENTAL ANALYSIS FUNDAMENTAL ANALYSIS 71FRAMEWORK FOR FUNDAMENTALANALYSIS

72

ECONOMY-INDUSTRY-COMPANY ANALYSIS(E-I-C FRAMEWORK OF ANALYSIS)

72

4. INDUSTRY ANALYSIS INDUSTRY ANALYSIS 79INDUSTRY FACTORS 80

5. COMPANY ANALYSIS COMPANY ANALYSIS 85MICRO COMPANY FACTORS 85TOOLS OF FINANCIAL ANALYSIS 88FORECASTING OF EARNINGS 91REVIEW QUESTIONS 93

MODULE 3: TECHNICAL ANALYSIS AND EMH 97 – 150

INTRODUCTION 971. TECHNICAL ANALYSIS MEANING – ASSUMPTIONS 99

DOW THEORY 100ELLIOT WAVE THEORY – PRINCIPLES –TYPES OF MOTIVEWAVES AND TYPES OFCORRECTIVE WAVES

106

NEUTRAL NETWORK 1132. CHARTS TECHNICAL TOOLS – PRICE CHARTS, TREND

AND TREND REVERSALS114

SUPPORT AND RESISTANCE LEVELS 1193. CHART PATTERNS INTRODUCTION – SUPPORT AND

RESISTANCE PATTERNS, REVERSALPATTERNS (TYPES), CONTINUATIONPATTERNS (TYPES) AND GAPS

121

4. ADVANCED TECHNICALINDICATORS

MODERNMETHODS – MATHEMATICALINDICATORS AND MARKET INDICATORS

132

5. FUNDAMENTAL VS.TECHNICAL ANALYSIS

FUNDAMENTAL ANALYSIS VS. TECHNICALANALYSIS

141

LIMITATIONS OF TECHNICAL ANALYSIS 1426. EFFICIENT MARKETHYPOTHESIS (EMH)

RANDOMWALK THEORY 143EFFICIENTMARKET HYPOTHESIS (EMH) –EMPIRICAL TESTS

143

EMH VS. FUNDAMENTAL ANALYSIS 148EMH VS. TECHNICAL ANALYSIS 148REVIEW QUESTIONS 149

MODULE 4: PORTFOLIO ANALYSIS 151 – 206

INTRODUCTION AND OPTIMAL PORTFOLIO 1511. PORTFOLIOCONSTRUCTION –APPROACHES

MEANING 153APPROACHES – TRADITIONAL ANDMODERNAPPROACHES OF PORTFOLIOCONSTRUCTION

153

2. MARKOWITZ MODEL MARKOWITZMODEL 157RISK AND RETURN AS PER MARKOWITZMODEL

159

REDUCTION OF PORTFOLIO RISK THROUGHDIVERSIFICATION

166

CALCULATION OF COVARIANCE 169EFFICIENT FRONTIER 172SHARPE INDEXMODEL – MEASURINGRETURN AND RISK UNDER SINGLE INDEXMODEL

174

3. UTILITY ANALYSIS PORTFOLIO UTILITY THEORY 180OPTIMAL PORTFOLIO OF MARKOWITZ 180SHARPE’S OPTIMAL PORTFOLIO 181

4. CAPITAL ASSET PRICINGMODEL (CAPM)

CAPITAL ASSET PRICING MODEL (CAPM) 185SECURITY MARKET LINE (SML) 189CAPITALMARKET LINE (CML) 190CML – EFFICIENT FRONTIER 192CML VS. SML 195ARBITRAGE PRICING THEORY (APT) 196SOLVED EXAMPLESREVIEW QUESTIONS

200203

MODULE 5: PORTFOLIO EVALUATION AND REVISION 207 – 227

1. PORTFOLIO EVALUATION PORTFOLIO EVALUATION 209PORTFOLIO EVALUATIONMETHODS 210SHARPE’S RATIO (S) 211TREYNOR’S RATIO (T) 212JENSEN’S ALPHA (A) 213FAMA’S PERFORMANCE MODEL 214M SQUARE METHOD 215

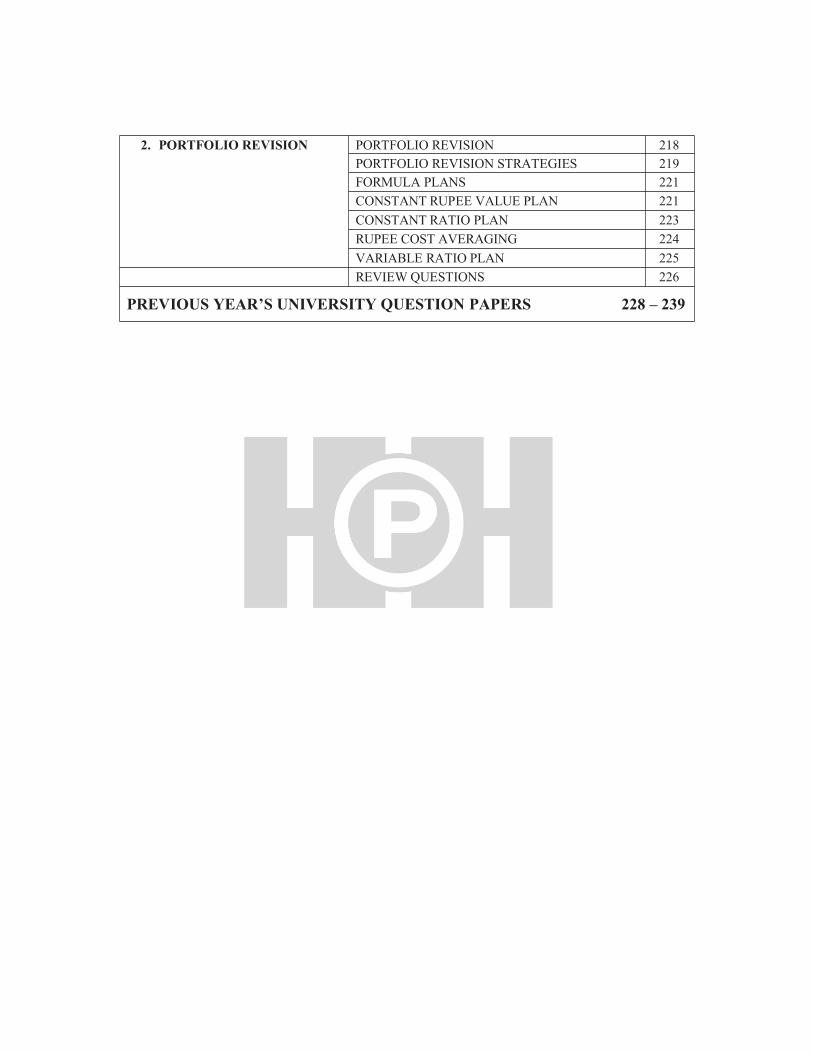

2. PORTFOLIO REVISION PORTFOLIO REVISION 218PORTFOLIO REVISION STRATEGIES 219FORMULA PLANS 221CONSTANT RUPEE VALUE PLAN 221CONSTANT RATIO PLAN 223RUPEE COST AVERAGING 224VARIABLE RATIO PLAN 225REVIEW QUESTIONS 226

PREVIOUS YEAR’S UNIVERSITY QUESTION PAPERS 228 – 239

Module 1: Investment 1

Different Views on Investment – Types of Investment – Characteristics of Investment –Objectives of Investment – Types of Investors – Investment Vs. Speculation – Investment Vs.Gambling – Speculation Vs. Gambling – Assets – Financial Assets – Real Assets – InvestmentProcess – Investment Information – Sources of Investment Information.

INTRODUCTIONThe basic philosophy of every generation is “think about the present and live in the present,

let the past go and thinking about the future is a waste”. Well it is right to some extent if it isexplained correctly. “Think about the present”: means work hard enough in your present as youhave only today in hand and you never know what your future is going to be. The motto of everyhard worker is working today will improve your future. Investment is one of the methods tosecure and improve one’s future.

INVESTMENTAll savings are not investments. It is the rational employment of one’s money in ventures

with an expectation of capital appreciation and fair return. Financial investment means thecommitment of financial resources in assets that are expected to appreciate and also yield somereturn over a period of time. From economists’ point of view investment is the net addition madeto the nation’s capital stock that consist of goods and services that are used in production process.To them, investment implies the production of new capital goods, plants, equipments, etc. JohnKeyens refers investment as real investment and not financial investment. But to us investmentmeans financial investment, which is the investment of money in monetary assets like stocks,bonds, derivatives, mutual funds, gold, certificate of deposits etc.

Disposable income, Consumption, Savings and InvestmentDisposable income = Gross income – Tax liabilities and Consumption + SavingsConsumption = Disposable income – SavingsSavings = Disposable income – ConsumptionInvestment = Disposable income – Consumption – Savings

MODULE

1INVESTMENT

2 Security Analysis and Portfolio Management

Module 1: Investment 3

UNIT 1

INVESTMENT PROPERTIESINTRODUCTION

Investment is a term spoken by laymen to financial experts but they are using the term torepresent different ideas. When you are in middle of a discussion with a financial expert, aneconomist, an entrepreneur and a layman about investment you need to understand they may betalking about different views of the term investment. So, before taking a part of that discussionlet’s understand different views of investment.

1.1 DIFFERENT VIEWS OF INVESTMENTThere are mainly, four different views of investments namely; economic view, financial

view, business view and household/ individual view.

1. Economic view

In economic sense, an investment is the investment in capital goods that are used in thefuture to create wealth. In other words, investment refers to the increase in the capital stock of anation which is used to produce other goods. The value is based on purchase price of the capitalgoods, not on stock value. Investment can be referred as a process of capital formation, or aprocess that increases the stock of capital during the year. So the value of investment in economicpoint of view is:

Investment = Change in capital stock during the year.As we know, to measure GDP of a nation, we are considering the economic view of

investment.GDP = C + I + G + NX

Where C is consumption, I is Investment, G is government spending, and NX is net exports.Thus investment is everything that remains of total expenditure after consumption,

government spending, and net exports are subtracted (i.e., I = GDP C G NX). “Netinvestment” deducts depreciation from gross investment. Net fixed investment is the value of thenet increase in the capital stock per year.

Usually a comparison of Marginal efficiency of investment with the going rate of interestmay be used to indicate the profitability of making a particular investment. Marginal efficiency ofinvestment is the expected rates of return on investment as additional units of investment aremade under specified conditions and over a stated period of time.

2. Financial view

In finance, an investment is the purchase of monetary assets with an intention of getting areturn in future. Return may be in the form of a capital gain realized from the sale of the monetaryasset, or income such as dividends, interest etc. generated from the monetary asset, or acombination of capital gain and income. An investment in any of the following monetary assets:

4 Security Analysis and Portfolio Management

Mutual Funds, Fixed Deposits, Bonds, Stock, Equities, Real Estate (Residential/CommercialProperty), Gold /Silver, Precious stones etc. can be considered as financial investment.

3. Business view

In business view, investment is the commitment of funds in capital expenditure for thepurpose of increasing revenue and thereby profit. It may include fixed investment, inventoryinvestment and intangible investment (these are explained later, under ‘Different types ofinvestment’). So here the investment is made by the entrepreneur on his business like buying newmachinery, setting up new plant, recruitment of labor, buying another company etc. in order toenhance his business.

4. Household view/Individual view

Under this view, the amount spends for household items are considered as an investment.They are making the investment with an expectation of getting a utility or return in future. Utilityis the want satisfying power of a commodity. When an expense incurred to acquire a utility, it canbe considered as an investment. For example, buying a television for getting entertainment andknowledge back.

Taking an action in the hopes of raising future revenue can also be considered an individualview of investment. For example, when choosing to pursue additional education, the goal is oftento increase knowledge and improve skills in the hopes of ultimately producing more income.

1.2 TYPES OF INVESTMENTUnder each investment view there are wide verities of investment types.

1. Intangible investment and Tangible investment

Intangible investment refers to an enterprise’s long-term operating costs incurred inresearch and development, long-term marketing, education and training, and other activitiesaimed at the development of the enterprise.

Tangible investment refers to the purchase of physical assets with the expectation ofgaining return in future. It may include both financial and non financial assets.

2. Business Fixed Investment

Business fixed investment means investment in the machines, tools and equipment thatbusinessmen buy for the uses in the further production of goods and services. The stock of thesemachines or plant equipment etc. represents fixed capital. The term ‘fixed’ in it implies thatexpenditure made on the machines, equipment etc. continues to be used for production for arelatively long time. Business fixed invest is similar to tangible investment but tangibleinvestment may also contain current assets as well.

3. Residential Investment

Residential investment refers to the expenditure which people incurred for constructing orbuying new houses or dwelling apartments for the purpose of living or renting out to others.

Module 1: Investment 5

4. Inventory Investment

Firms hold inventories of raw materials, semi-finished goods and finished goods to be soldshortly. The change in the inventories or stocks of these goods with the firms is called inventoryinvestment. Usually inventory investment is a very small part of total business investment; but itis of considerable importance to the economy of a country because fluctuations of suchinvestment cause business cycles.

5. Direct and indirect investment

Under direct investment the savings of the investor is directly channelized to the needyborrower. In other words, direct investment is the investment made by the investor directly to acompany or someone with a deficit of fund. Buying shares of a company by an investor is anexample for direct investment.

Indirect investment is investment where the savings of an investor is channelized to theneedy borrower through another investor. In other words, indirect investment is the investmentmade indirectly to a company or someone with a deficit of fund through an intermediary.Indirect investment can also be defined as the process of buying an investment without actuallybuying the investment itself directly. For example, buying units of mutual fund, where the mutualfund company is pooling various units and making direct investment in companies.

6. Autonomous investment and Induced investment

Autonomous investments are those investments which don’t change with the change inincome level. Therefore such investments are independent to the income of the investor.Autonomous investments are those that are made because they are deemed as basic necessities toindividual, organizational, or national well-being, health and safety. Investment made bygovernment in educational sector or agricultural sector can be considered as an example forautonomous investment.

Induced investment is that investment which is affected by the change in level of income.An increase in disposable income induces such investment. Such investments depend more onincome than on the rate of return.

7. Ex-ante and Ex-post investment

The investment which is planned or desired to be made by the firms or entrepreneurs in theeconomy during a period (say, a year) is called ex-ante (or planned) investment. Such investmentsare planned in the beginning of that specific period. It should be kept in mind that sometimesunplanned investment is made to meet changes in the current demand function.

Ex-post investment refers to the actual investment made by all the entrepreneurs in theeconomy during a given period. In short, the realised investment of a period, say, a year, is calledex-post investment (or actual investment). It is noteworthy to mention that Keynes included in theinvestment of unsold goods which he called unplanned investment. Thus, ex-post investmentequals planned + unplanned investment.

Actual investment = Planned investment + Unplanned investmentHence, actual investment may differ from planned investment because of unplanned

addition or reduction in inventories (stock of goods).

6 Security Analysis and Portfolio Management

8. Real investment and Financial investment

Real investments are the investments made in real assets. A real asset is a tangibleinvestment that has an intrinsic value due to its substance and physical properties. Commodities,real estate, equipment, and natural resources are all types of real assets. Real assets provideportfolio diversification, as they often move in opposite directions to financial assets like stocksor bonds. Real assets tend to be more stable but less liquid than financial assets.

Financial investments are the investments made in financial assets. A financial asset is aliquid asset that gets its value from a contractual right or ownership claim. Cash, stocks, bonds,mutual funds, and bank deposits are all are examples of financial assets. Unlike land, property,commodities, or other tangible physical assets, financial assets do not necessarily have inherentphysical worth or even a physical form. Rather, their value reflects factors of supply and demandin the marketplace in which they trade, as well as the degree of risk they carry.

9. Short term and Long term investment

Short-term investments are those instruments that are traded for a short period of time;typically up to one year. These are high liquidity instruments, generally involving lesser marketrisks. Investment in T-Bills is an example for short term investment.

Long term investments are investments that offer higher returns and traded for more than 1year. These involve more market risks, and generally provide higher returns. Investment indebentures is an example for long term investment.

10. Domestic and Foreign investment

Domestic investment is the investment in the companies and products of someone’s owncountry rather than in those of foreign countries. In other words, an investor is makinginvestments within his/her own nation. Domestic investment can in simple parlance be describedas an act of local or resident entrepreneur or producer placing capital within a country into aproject or business enterprise or assets with the intent of making a profit.

Foreign investment refers to the investment in foreign companies and assets of anothercountry by an investor. It may include;

Foreign direct investments— long-term physical investments made by a company in aforeign country, such as opening plants or purchasing buildings.Foreign indirect investment involves corporations, financial institutions, and privateinvestors that purchase shares in foreign companies that trade on a foreign stockexchange.Commercial loans are another type of foreign investment and involve bank loansissued by domestic banks to businesses in foreign countries or the governments of thosecountries.

11. Liquid and Illiquid investments

Investments in liquid assets like marketable securities, commonly traded equity shares, goldetc. are called as liquid investments and investments in illiquid assets like real estate, art works,private equity etc. are called as illiquid investments.

Module 1: Investment 7

12. High risk and Low risk investment

A high-risk investment is one for which there is either a large percentage chance of loss ofcapital or under-performance. Equity shares, commercial papers etc. are examples for high-riskinvestments. A low-risk investment is one for which there is either a lower percentage chance ofloss of capital or under-performance. Bank Deposits, Provident funds etc. are examples for low-risk investments.

13. Gross and Net Investment (Economic view)

Under economic view, investment is the addition to the capital stock of an economy. Forexample, construction of building, purchase of machinery, addition to inventories of goods, etc.The total addition made to the capital stock of economy in a given period is termed as GrossInvestment. The actual addition made to the capital stock of economy in a given period is termedas Net Investment. Therefore, net investment is the total capital expenditure minusdepreciation of assets.

Net Investment = Gross Investment – Depreciation

14. Public investment and Private investment

Public investment are the investments by the state in particular assets, whether throughcentral or local governments or through publicly owned industries or corporations. It tends to bedivided between physical or tangible investment in infrastructure (for example, transport,telecommunications and buildings); human or intangible investment in education, skills, andknowledge; and current investment in the consumption of goods and services (for example,welfare benefits and pensions).

Private investment, from a macroeconomic standpoint, is the purchase of a capital asset thatis expected to produce income, appreciate in value, or both. Such investments are made byprivate parties. Examples of capital assets include land, buildings, machinery, equipment etc.

1.3.OBJECTIVES OF INVESTMENTPeople make investment with a variety of purposes. The objectives of investment must be

stated clearly before starting an investment process. Various investment avenues and types ofinvestment assets are selected on the basis of an investor’s objectives. Following are the basic andsecondary objectives of investment:

1. Stable income2. Capital appreciation Basic/Primary objectives3. Safety and security of fund4. Risk mitigation5. Liquidity6. Tax consideration7. Time value of money8. Diversity of portfolio Secondary objectives9. Expertise management10. Hedging

8 Security Analysis and Portfolio Management

1. Stable income/return

One of the important objectives of investment is gaining a stable income. Investments aremade out of current savings with an expectation of getting regular income in future. Investors aresacrificing their current savings for future returns. The dividend or interest received from theinvestment is considered as return. The expectation regarding rate of return varies from investorto investor.

2. Capital Appreciation

Another objective of investment is capital appreciation. The term capital appreciation refersto the increase in the value of financial assets. It happens due to the increase in financialperformance of the company, increase in demand of financial asset or weakening the supply ofthat financial asset. The investor can derive a capital gain from capital appreciation. Capital gainis the profit achieved by selling a financial asset that has appreciated in value.

3. Safety and security of fund

Safety is another objective of investors though there is no such thing as completely safe andsecure investment. Yet we can get close to ultimate safety for our investment funds through thepurchase of government owned securities in a stable economy or through the purchase of bluechip companies’ securities.

4. Risk mitigation

The risk of an investment refers to the variability in its actual return from the expectedreturn. Numerous risks are associated with our money whether it is in our pocket or in the market.Some risks are more apparent than others. In order to minimize the risk investor should considerdiversification of assets while investing. By investing in different ventures with different risk theinvestor can reduce the chances of loss. Also a trader can reduce his financial risk by participatingin debenture market.

5. Liquidity

Most of the financial assets are reasonably liquid, which means they can be immediatelysold and easily converted into cash. Listed shares, debentures, bonds, mutual funds units etc. arefairly liquid in the market. An investor can gain return as well as maintain liquidity throughinvestment. In order to avoid unwanted spending and to save money for meeting various longterm requirements some investors choose less liquid instruments.

6. Tax consideration

Some investments provide tax benefits. To any genuine investor tax benefits maybe asecondary objective. By tax benefits we mean reducing the amount of tax payable or gettingexemption from paying tax itself. The benefits are allowed by using the provisions in the IncomeTax Act, in the form of exemption under section Sec. 80C of the Act, in India.

7. Time value of money

Inflation eats away at our savings. With each passing year, prices keep rising. Investmentshelp to protect our capital against price rise. A good way to beat inflation is to park your money

Module 1: Investment 9

in investments that offer returns that are higher than the rate of inflation. Historically, equityinvestments have given returns that are higher than the inflation rate thereby providing investorsreal returns (Real returns = Investment returns minus Inflation rate).

8. Diversity of portfolio

Portfolio means a collection of financial instruments. An investor usually makes investmentin a variety of financial instruments like stocks, bonds, mutual funds etc. By adding financialinstruments with different risk and return into the portfolio investor can optimize return andrisk associated with. An optimal portfolio can maintain an optimal risk-return trade off for aninvestor’s investment. An investor can reduce his financial risk by investing in a diversifiedportfolio.

9. Expertise management

Investment avenues like Mutual Fund (MF) offer high quality management facilities. Aperson who is investing in MF is totally free from management affairs of the portfolio. MFundertakes the obligation of managing the fund on behalf of the investors. A layman can rely onsuch facilities to safe guard his investments and to ensure proper return.

10. Hedging

Hedging is strategy of buying an asset designed to reduce or offset losses by taking anopposite position in a related asset. It helps to restrict losses that may arise due to unknownfluctuations in the price of the investment. Hedging strategies typically involve derivatives, andoptions are the most commonly used derivative. It gives you the right to buy or sell a stock at aspecified price within a specific period of time. Usually traders are using investment with anobjective of hedging in order to offset or minimize future losses from businesses due to marketfluctuations. These are the investors (Hedgers) with a present or anticipated exposure to theunderlying asset which is subject to price risks.

1.4 CHARACTERISTICS OF INVESTMENTFollowing are the important characteristics of investments:1. Return: Investments are made with the primary objective of deriving a return. The return

may be received in the form of capital appreciation plus yield. The difference between the salesprice and the purchase price is capital appreciation. The dividend or interest received from theinvestment is the yield.

2. Risk: Risk may relate to loss of capital, delay in repayment of capital, non-payment ofinterest, or variability of returns. While some investments like government securities and bankdeposits are riskless, others are more risky. The risk of an investment depends on the followingfactors:

1. The longer the maturity period, the larger is the risk.2. The lower credit worthiness of the borrower, the higher is the risk.3. Investments in ownership securities like equity shares carry higher risk compared toinvestments in debt instruments like debentures and bonds.

10 Security Analysis and Portfolio Management

Risk and return of an investment are related. Normally, the higher the risk, the higher is thereturn.

3. Safety: Safety is another feature which an investor desires for his investments. The safetyof an investment implies the certainty of return of capital without loss of money or time. Everyinvestor expects to get back his capital on maturity without loss and without delay. The safetylevel of the investment depends on many factors such as; issuer credit worthiness, nature ofinstrument, market cycle etc.

4. Liquidity: An investment which is easily saleable or marketable without loss of moneyand without loss of time is said to possess liquidity. Some investments like company deposits,bank deposits, Post Office Deposits, NSC, NSS etc are not marketable. Some investmentinstruments like preference shares and debentures are marketable, but there are no buyers in manycases and hence their liquidity is negligible. Equity shares of companies listed on stock exchangesare easily marketable through the stock exchanges.

5. Multi faced: Investment may mean different in different contexts. The meaning ofinvestment in economics may not be same in finance.

6. Objectives: Investment carries single or multiple objectives or intentions of investors.Some may be expecting regular return but some may be expecting capital appreciation and somemay be expecting both.

1.5 IMPORTANCE OF INVESTMENTKeynes’s psychological law of consumption shows that income is not equal to expenditure

and it makes a gap between income and consumption. It can be filled in only by additionalinvestment. If additional investment does not take place, income and expenditure will inevitablyfall. Following are the importance of investment:

1. Investing money in various financial avenues ensures that our money grows (capitalappreciation) instead of just lying idle.

2. Investments with yield high returns and high liquidity can take care of emergencyexpenses such as medical expenditure etc.

3. Investments are a good way to earn stable income from the accumulated wealth of aninvestor. For example, earning rent from a real estate investment or earning dividendsfrom stock market investments.

4. Tax minimization can be achieved by investing our money in various tax benefitingavenues.

5. Fighting inflation can be one of the key reasons for investment. It ensures that themoney grows and saves our purchasing power.

6. Investments lead to a certain amount of corpus that plays a vital role in providingfinancial security to the dependents.

7. Distant financial goals, both long-term as well as short-term can be planned and fulfilledby making intelligent and relevant investments. It creates a provision for the uncertainfuture.