securitization+us crisis

DESCRIPTION

A brief note about Securitization Process and US Sub Prime CrisisTRANSCRIPT

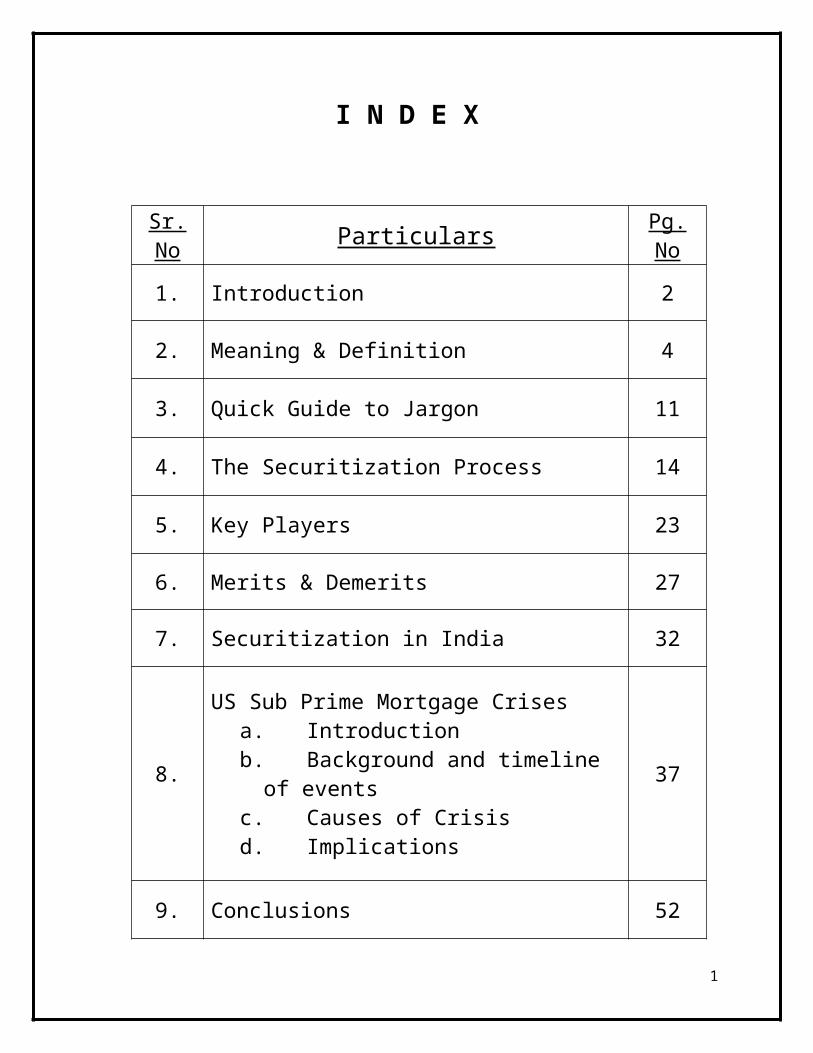

I N D E X

Sr. No Particulars Pg. No

1. Introduction 2

2. Meaning & Definition 4

3. Quick Guide to Jargon 11

4. The Securitization Process 14

5. Key Players 23

6. Merits & Demerits 27

7. Securitization in India 32

8.

US Sub Prime Mortgage Crisesa. Introductionb. Background and timeline of eventsc. Causes of Crisisd. Implications

37

9. Conclusions 52

10. Bibliography 54

1

INTRODUCTION

Technological advancements have changed the face of the world of finance. It is today more a world of transactions than a world of relations. Most relations have been transactionalized.

Transactions mean coming together of two entities with a common purpose, whereas relations mean keeping together of these two entities. For example, when a bank provides a loan of a sum of money to a user, the transaction leads to a relationship: that of a lender and a borrower. However, the relationship is terminated when the very loan is converted into a debenture. The relationship of being a debenture holder in the company is now capable of acquisition and termination by transactions.

"Securitization" in its widest sense implies every such process which converts a financial relation into a transaction.

Securitization is the financial practice of pooling various types of contractual debt such as residential mortgages, commercial mortgages, auto loans or credit card debt obligations and selling said consolidated debt as bonds, pass-through securities, or collateralized mortgage obligation (CMOs), to various investors. The principal and interest on the debt, underlying the security, is paid back to the various investors regularly. Securities backed by mortgage receivables are called mortgage-backed securities (MBS), while those backed by other types of receivables are asset-backed securities (ABS).

Critics have suggested that the complexity inherent in securitization can limit investors' ability to monitor risk, and that competitive securitization markets with multiple securitize may be particularly prone to sharp declines in underwriting standards. Private, competitive mortgage securitization is believed to have played an important role in the U.S. subprime mortgage crisis.

In addition, off-balance sheet treatment for securitizations coupled with guarantees from the issuer can hide the extent of leverage of the securitizing

2

firm, thereby facilitating risky capital structures and leading to an under-pricing of credit risk. Off-balance sheet securitizations are believed to have played a large role in the high leverage level of U.S. financial institutions before the financial crisis, and the need for bailouts.

The granularity of pools of securitized assets is a litigant to the credit risk of individual borrowers. Unlike general corporate debt, the credit quality of securitized debt is non-stationary due to changes in volatility that are time - and structure-dependent. If the transaction is properly structured and the pool performs as expected, the credit risk of all tranches of structured debt improves; if improperly structured, the affected tranches may experience dramatic credit deterioration and loss.

Securitization has evolved from its beginnings in the late eighteenth century to an estimated outstanding of $10.24 trillion in the United States and $2.25 trillion in Europe as of the 2nd quarter of 2008. In 2007, ABS issuance amounted to $3.455 trillion in the US and $652 billion in Europe. WBS (Whole Business Securitization) arrangements first appeared in the United Kingdom in the 1990s, and became common in various Commonwealth legal systems where senior creditors of an insolvent business effectively gain the right to control the company.

Securitization started as a way for financial institutions and corporations to find new sources of funding—either by moving assets off their balance sheets or by borrowing against them to refinance their origination at a fair market rate. It reduced their borrowing costs and, in the case of banks, lowered regulatory minimum capital requirements.

For example, suppose a leasing company needed to raise cash. Under standard procedures, the company would take out a loan or sell bonds. Its ability to do so, and the cost, would depend on its overall financial health and credit rating. If it could find buyers, it could sell some of the leases directly, effectively converting a future income stream to cash. The problem is that there is virtually no secondary market for individual leases. But by pooling those leases, the company can raise cash by selling the package to an issuer, which in turn converts the pool of leases into a tradable security.

3

MEANING & DEFINITION

I. Definition

Below are some of the ways to define Securitization: -

1. The process through which an issuer creates a financial instrument by combining other financial assets and then marketing different tiers of the repackaged instruments to investors. The process can encompass any type of financial asset and promotes liquidity in the marketplace.

2. Securitization is the process of taking an illiquid asset, or group of assets, and through financial engineering, transforming them into a security.

3. Securitization is a process by which a company clubs its different financial assets/debts to form a consolidated financial instrument which is issued to investors. In return, the investors in such securities get interest.

4. A securitization is a financial transaction in which assets are pooled and securities representing interests in the pool are issued.

II. Meaning and Explanation

History of evolution of finance, and corporate law, the latter being supportive for the former, is replete with instances where relations have been converted into transactions. In fact, this was the earliest, and by far unequalled, contribution of corporate law to the world of finance, viz., and the ordinary share, which implies piecemeal ownership of the company. Ownership of a company is a relation, packaged as a transaction by the creation of the ordinary share. This earliest instance of securitization was so instrumental in the growth of the corporate form of doing business, and hence, industrialization, that someone rated it as one of the two greatest inventions of the 19th century -the other one being the steam engine. That truly reflects the significance of the ordinary share, and if the

4

same idea is extended, to the very concept of securitization: it as important to the world of finance as motive power is to industry.

Other instances of securitization of relationships are commercial paper, which securitizes a trade debt.

However, in the sense in which the term is used in present day capital market activity, securitization has acquired a typical meaning of its own, which is at times, for the sake of distinction, called asset securitization. It is taken to mean a device of structured financing where an entity seeks to pool together its interest in identifiable cash flows over time, transfer the same to investors either with or without the support of further collaterals, and thereby achieve the purpose of financing. Though the end-result of securitization is financing, but it is not "financing" as such, since the entity securitizing its assets it not borrowing money, but selling a stream of cash flows that was otherwise to accrue to it.

Mortgage-backed securities are a perfect example of securitization. By combining mortgages into one large pool, the issuer can divide the large pool into smaller pieces based on each individual mortgage's inherent risk of default and then sell those smaller pieces to investors.

The process creates liquidity by enabling smaller investors to purchase shares in a larger asset pool. Using the mortgage-backed security example, individual retail investors are able to purchase portions of a mortgage as a type of bond. Without the securitization of mortgages, retail investors may not be able to afford to buy into a large pool of mortgages.

This process enhances liquidity in the market. This serves as a useful tool, especially for financial companies, as its helps them raise funds. If such a company has already issued a large number of loans to its customers and wants to further add to the number, then the practice of securitization can come to its rescue.

The simplest way to understand the concept of securitization is to take an example.

5

III. Example

1. An example would be a financing company that has issued a large number of auto loans and wants to raise cash so it can issue more loans. One solution would be to sell off its existing loans, but there isn't a liquid secondary market for individual auto loans. Instead, the firm pools a large number of its loans and sells interests in the pool to investors. For the financing company, this raises capital and gets the loans off its balance sheet, so it can issue new loans. For investors, it creates a liquid investment in a diversified pool of auto loans, which may be an attractive alternative to a corporate bond or other fixed income investment. The ultimate debtors—the car owners—need not be aware of the transaction. They continue making payments on their loans, but now those payments flow to the new investors as opposed to the financing company.

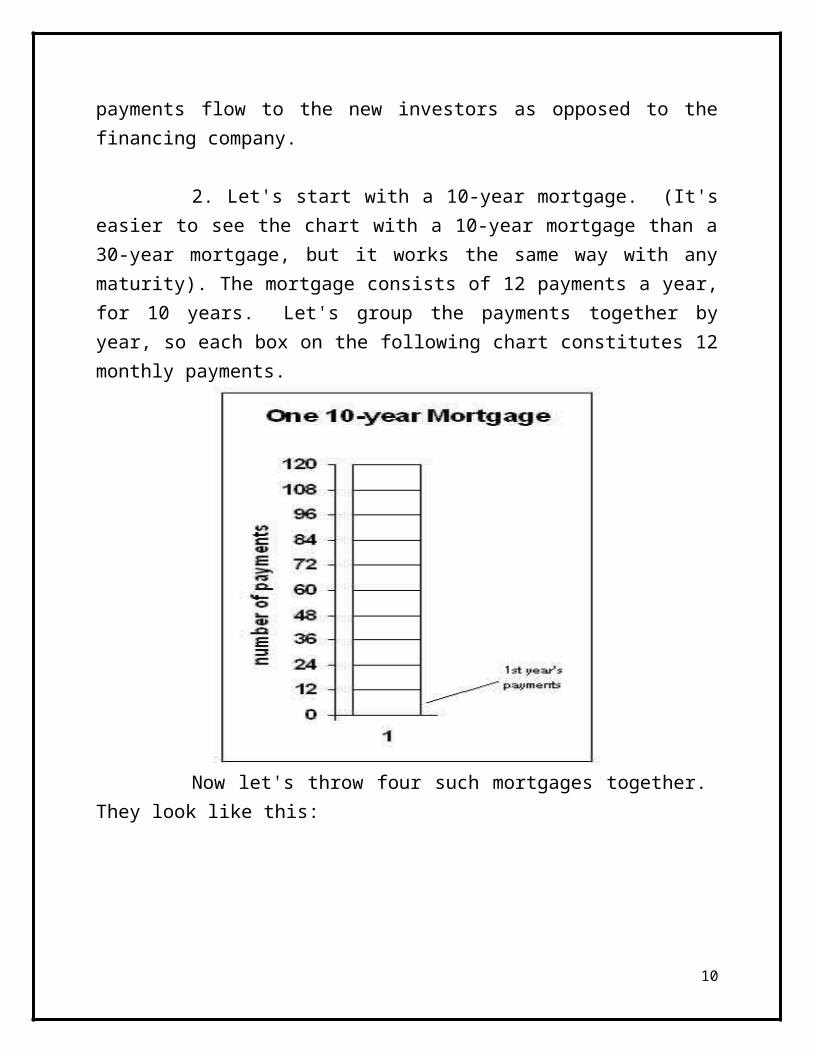

2. Let's start with a 10-year mortgage. (It's easier to see the chart with a 10-year mortgage than a 30-year mortgage, but it works the same way with any maturity). The mortgage consists of 12 payments a year, for 10 years. Let's group the payments together by year, so each box on the following chart constitutes 12 monthly payments.

6

Now let's throw four such mortgages together. They look like this:

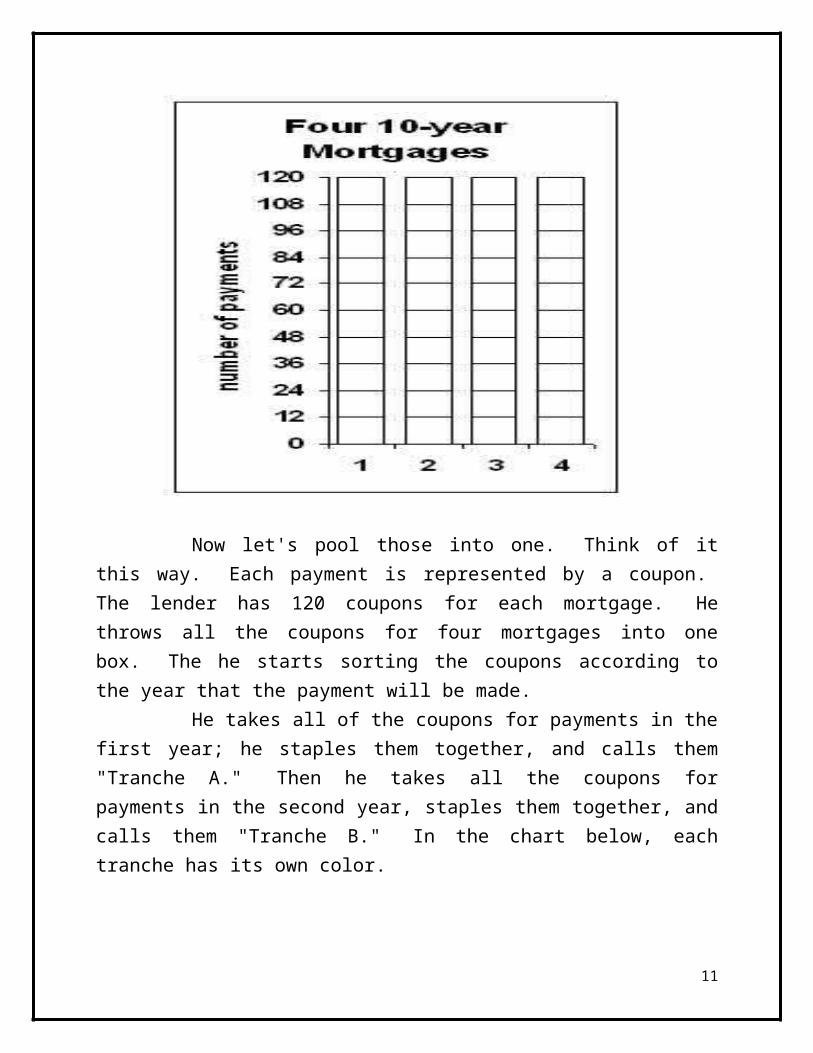

Now let's pool those into one. Think of it this way. Each payment is represented by a coupon. The lender has 120 coupons for each mortgage. He throws all the coupons for four mortgages into one box. The he starts sorting the coupons according to the year that the payment will be made.

He takes all of the coupons for payments in the first year; he staples them together, and calls them "Tranche A." Then he takes all the coupons for payments in the second year, staples them together, and calls them "Tranche B." In the chart below, each tranche has its own color.

7

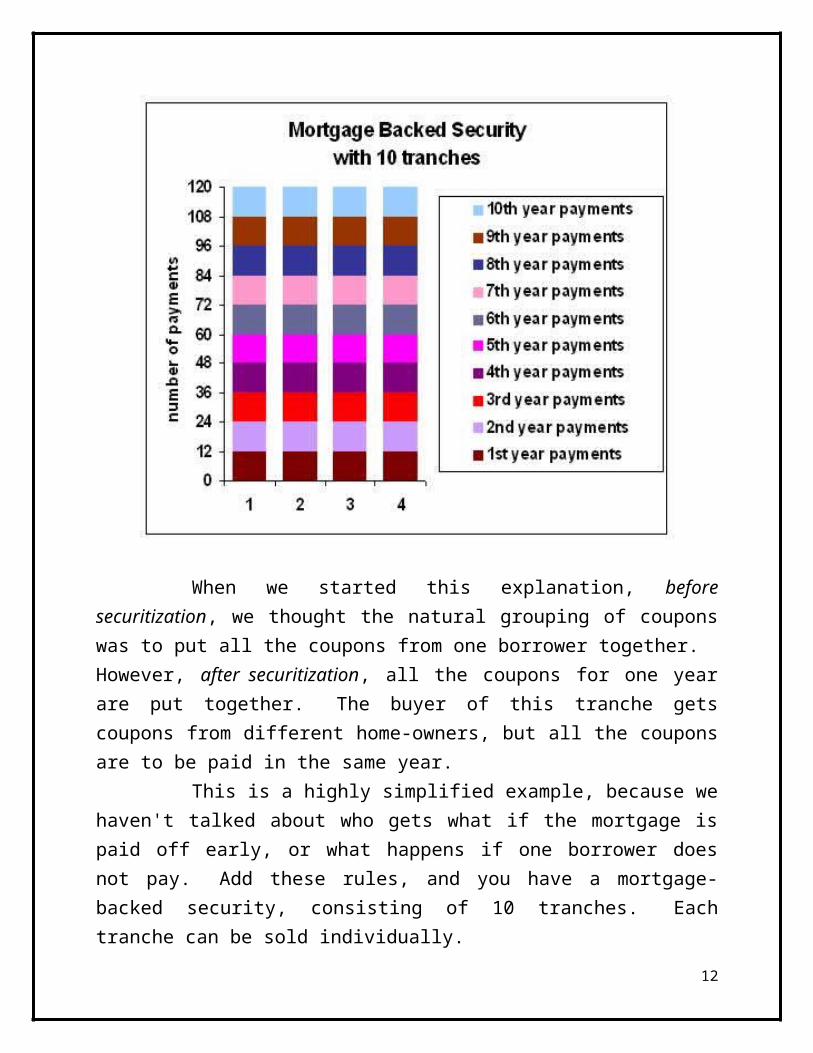

When we started this explanation, before securitization, we thought the natural grouping of coupons was to put all the coupons from one borrower together. However, after securitization, all the coupons for one year are put together. The buyer of this tranche gets coupons from different home-owners, but all the coupons are to be paid in the same year.

This is a highly simplified example, because we haven't talked about who gets what if the mortgage is paid off early, or what happens if one borrower does not pay. Add these rules, and you have a mortgage-backed security, consisting of 10 tranches. Each tranche can be sold individually.

8

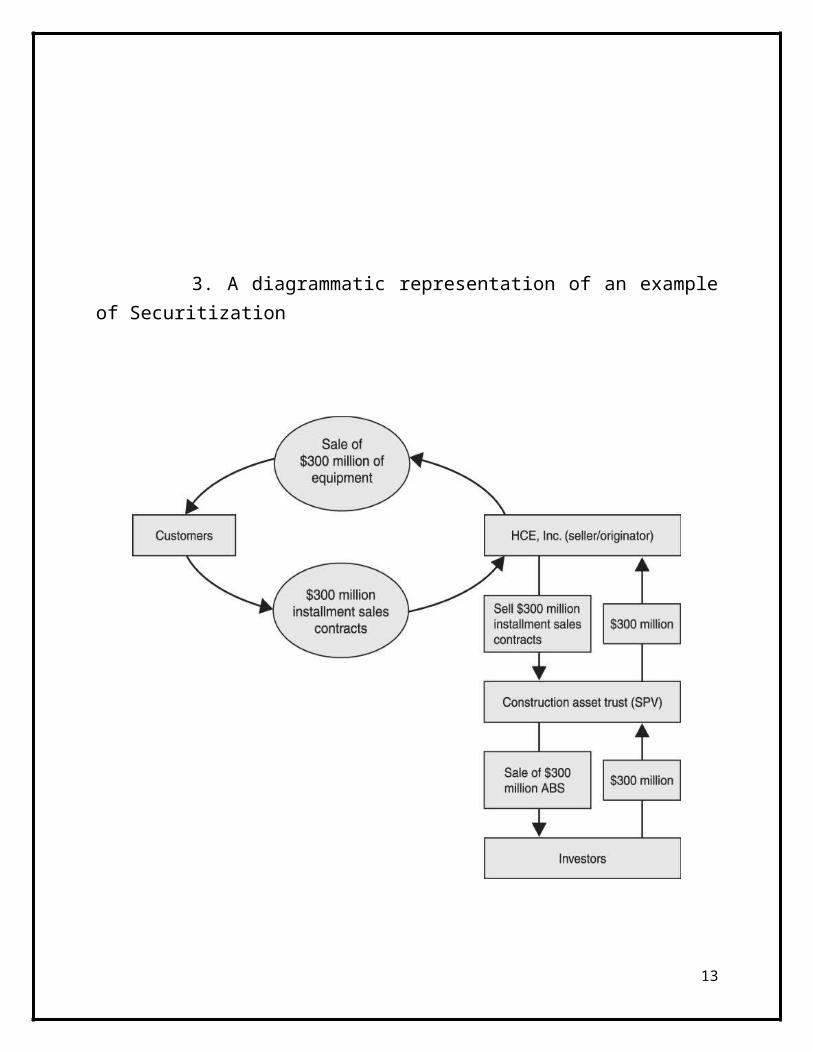

3. A diagrammatic representation of an example of Securitization

Thus, the present-day meaning of securitization is a blend of two forces that are critical in today's world of finance: structured finance and capital markets. Securitization leads to structured finance as the resulting security is not a generic risk in entity that securitizes its assets but in specific assets or cash flows of such entity. Two, the idea of securitization is to create a capital market product - that is, it results into creation of a "security" which is a marketable product.

9

This meaning of securitization can be expressed in various dramatic words:

i. Securitization is the process of commoditization. The basic idea is to take the outcome of this process into the market, the capital market. Thus, the result of every securitization process, whatever might be the area to which it is applied, is to create certain instruments which can be placed in the market.

ii. Securitization is the process of integration and differentiation. The entity that securitizes its assets first pools them together into a common hotchpots (assuming it is not one asset but several assets, as is normally the case). This process of integration. Then, the pool itself is broken into instruments of fixed denomination. This is the process of differentiation.

iii. Securitization is the process of de-construction of an entity. If one envisages an entity's assets as being composed of claims to various cash flows, the process of securitization would split apart these cash flows into different buckets, classify them, and sell these classified parts to different investors as per their needs. Thus, securitization breaks the entity into various sub-sets.

10

QUICK GUIDE TO JARGON

There is a great deal of terminology that is specific to Securitization. Though there is a complete terminology appended, this section will help the reader to quickly get familiarized with the essential securitization jargon.

The entity that securitizes its assets is called the originator: the name signifies the fact that the entity was responsible for originating the claims that are to be ultimately securitized. There is no distinctive name for the investors who invest their money in the instrument: therefore, they might simply be called investors.

The claims that the originator securitizes could either be an existing claim, or existing assets (in form of claims), or expected claims over time. In other words, the securitized assets could be either existing receivables, or receivables to arise in future. The latter, for the sake of distinction, is sometimes called future flows securitization, in which case the former is a case of asset-backed securitization.

In US markets, another distinction is mostly common: between mortgage-backed securities and asset-backed securities. This only is to indicate the distinct application: the former relates to the market for securities based on mortgage receivables, which in the USA forms a substantial part of total securitization markets, and securitization of other receivables.

Since it is important for the entire exercise to be a case of transfer of receivables by the originator, not a borrowing on the security of the receivables, there is a legal transfer of the receivables to a separate entity. In legal parlance, transfer of receivables is called assignment of receivables. It is also necessary to ensure that the transfer of receivables is respected by the legal system as a genuine transfer, and not as mere eyewash where the reality is only a mode of borrowing. In other words, the transfer of receivables has to be a true sale of the receivables, and not merely a financing against the security of the receivables.

11

Since securitization involves a transfer of receivables from the originator, it would be inconvenient, to the extent of being impossible, to transfer such receivables to the investors directly, since the receivables are as diverse as the investors themselves. Besides, the base of investors could keep changing as the resulting security is essentially a marketable security.

Therefore, it is necessary to bring in an intermediary that would hold the receivables on behalf of the end investors. This entity is created solely for the purpose of the transaction: therefore, it is called a special purpose vehicle (SPV) or a special purpose entity (SPE) or, if such entity is a company, special purpose company (SPC). The function of the SPV in a securitization transaction could stretch from being a pure conduit or intermediary vehicle, to a more active role in reinvesting or reshaping the cash flows arising from the assets transferred to it, which is something that would depend on the end objectives of the securitization exercise.

Therefore, the originator transfers the assets to the SPV, which holds the assets on behalf of the investors, and issues to the investors its own securities. Therefore, the SPV is also called the issuer.

There is no uniform name for the securities issued by the SPV as such securities take different forms. These securities could either represent a direct claim of the investors on all that the SPV collects from the receivables transferred to it: in this case, the securities are called pass through certificates or beneficial interest certificates as they imply certificates of proportional beneficial interest in the assets held by the SPV.

Alternatively, the SPV might be re-configuring the cash flows by reinvesting it, so as to pay to the investors on fixed dates, not matching with the dates on which the transferred receivables are collected by the SPV. In this case, the securities held by the investors are called pay through certificates. The securities issued by the SPV could also be named based on their risk or other features, such as senior notes or junior notes, floating rate notes, etc.

12

Another word commonly used in securitization exercises is bankruptcy remote transfer. What it means is that the transfer of the assets by the originator to the SPV is such that even if the originator were to go bankrupt, or get into other financial difficulties, the rights of the investors on the assets held by the SPV is not affected. In other words, the investors would continue to have a paramount interest in the assets irrespective of the difficulties, distress or bankruptcy of the originator.

13

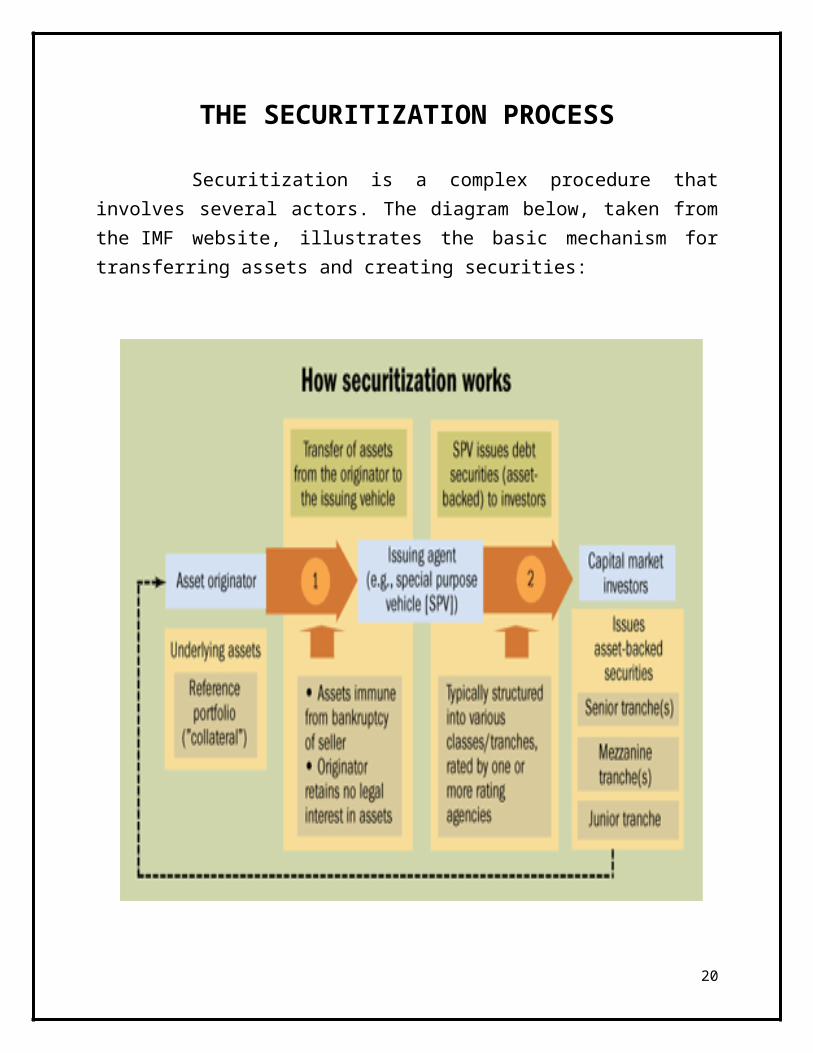

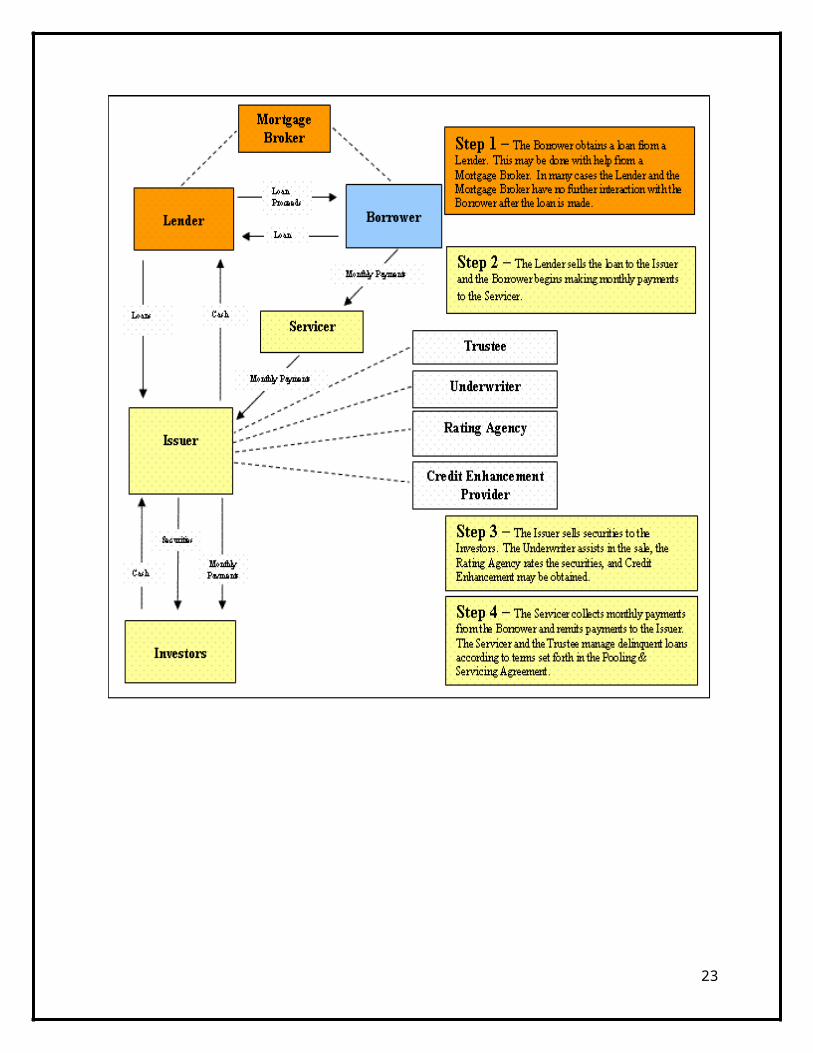

THE SECURITIZATION PROCESS

Securitization is a complex procedure that involves several actors. The diagram below, taken from the IMF website, illustrates the basic mechanism for transferring assets and creating securities:

The entity that originally holds the assets (the originator) initiates the process by selling the assets to a legal entity, an SPV (Special Purpose Vehicle), specially created to limit the risk of the final investor vis-à-vis the issuer of the

14

assets. An SPV is also referred to as a “conduit.” Then, depending on the situation, the SPV either issues the securities directly or resells the pool of assets to a “trust” that, in turn, issues the securities (the trust is actually used for several securitization transactions and therefore oversees several SPVs).

An SPV is more of a legal framework than an element that plays an active part in the transaction. The most important role is played by the arranger, typically a bank, who sets up the transaction and evaluates the pool of assets,the way in which it will be fed, the characteristics of the securities to be issued, and the potential structuring of the fund.

The object of the structuring is to model the characteristics of the securities such that they correspond to the needs of the final investor. Instead of simply paying the final investor the revenue generated by the assets, the amortization rules for the security are defined in advance.

Some ABSs are able to be “topped up,” meaning that the pool of assets can be reefed during the life of the security. This makes it possible to refinance short-term debts (such as credit-card debt) with long-term bonds.

Finally, the arranger plays an important role in distributing the securities to the final investors (distribution). Quite often, the securities are not issued on an exchange, but are distributed over-the-counter to a small number of investors.

The trio of actors comprising the “originator, SPV, and arranger” constitutes the “Originate-to-Distribute” model, which has thrived over the course of the past few years.

An important distinction must be made between “traditional” securitization, where the assets are actually sold to the SPV (“true sale”), and what is known as “synthetic” securitization, where the originator retains ownership of the assets and transfers only the risk to the SPV, via a credit derivative. This transaction brings no liquidity to the assignor, but enables him to externalize the risk associated with holding the securitized assets.

15

A diagrammatic presentation on the Securitization Process: -

16

Thus, the process of Securitization can be summarized as below: -

I. Pooling and Transfer

The originator initially owns the assets engaged in the deal. This is typically a company looking to either raise capital or restructure debt or otherwise adjust its finances. Under traditional corporate finance concepts, such a company would have three options to raise new capital: a loan, bond issue, or issuance of stock. However, stock offerings dilute the ownership and control of the company, while loan or bond financing is often prohibitively expensive due to the credit rating of the company and the associated rise in interest rates.

The consistently revenue-generating part of the company may have a much higher credit rating than the company as a whole. For instance, a leasing company may have provided $10m nominal value of leases, and it will receive a cash flow over the next five years from these. It cannot demand early repayment on the leases and so cannot get its money back early if required. If it could sell the rights to the cash flows from the leases to someone else, it could transform that income stream into a lump sum today (in effect, receiving today the present value of a future cash flow). Where the originator is a bank or other organization that must meet capital adequacy requirements, the structure is usually more complex because a separate company is set up to buy the assets.

A suitably large portfolio of assets is "pooled" and transferred to a "special purpose vehicle" or "SPV" (the issuer), a tax-exempt company or trust formed for the specific purpose of funding the assets. Once the assets are transferred to the issuer, there is normally no recourse to the originator. The issuer is "bankruptcy remote", meaning that if the originator goes into bankruptcy, the assets of the issuer will not be distributed to the creditors of the originator. In order to achieve this, the governing documents of the issuer restrict its activities to only those necessary to complete the issuance of securities.

Accounting standards govern when such a transfer is a sale, a financing, a partial sale, or a part-sale and part-financing. In a sale, the originator is

17

allowed to remove the transferred assets from its balance sheet: in a financing, the assets are considered to remain the property of the originator. Under US accounting standards, the originator achieves a sale by being at arm's length from the issuer, in which case the issuer is classified as a "qualifying special purpose entity" or "QSPE".

Because of these structural issues, the originator typically needs the help of an investment bank (the arranger) in setting up the structure of the transaction.

II. Issuance

To be able to buy the assets from the originator, the issuer SPV issues tradable securities to fund the purchase. Investors purchase the securities, either through a private offering (targeting institutional investors) or on the open market. The performance of the securities is then directly linked to the performance of the assets. Credit rating agencies rate the securities which are issued to provide an external perspective on the liabilities being created and help the investor make a more informed decision.

In transactions with static assets, a depositor will assemble the underlying collateral, help structure the securities and work with the financial markets to sell the securities to investors. The depositor has taken on added significance under Regulation AB. The depositor typically owns 100% of the beneficial interest in the issuing entity and is usually the parent or a wholly owned subsidiary of the parent which initiates the transaction. In transactions with managed (traded) assets, asset managers assemble the underlying collateral, help structure the securities and work with the financial markets in order to sell the securities to investors.

Some deals may include a third-party guarantor which provides guarantees or partial guarantees for the assets, the principal and the interest payments, for a fee.

18

The securities can be issued with either a fixed interest rate or a floating rate under currency pegging system. Fixed rate ABS set the “coupon” (rate) at the time of issuance, in a fashion similar to corporate bonds and T-Bills. Floating rate securities may be backed by both amortizing and non-amortizing assets in the floating market. In contrast to fixed rate securities, the rates on “floaters” will periodically adjust up or down according to a designated index such as a U.S. Treasury rate, or, more typically, the London Interbank Offered Rate (LIBOR). The floating rate usually reflects the movement in the index plus an additional fixed margin to cover the added risk.

III. Credit Enhancement

Unlike conventional corporate bonds which are unsecured, securities generated in a securitization deal are "credit enhanced", meaning their credit quality is increased above that of the originator's unsecured debt or underlying asset pool. This increases the likelihood that the investors will receive cash flows to which they are entitled, and thus causes the securities to have a higher credit rating than the originator. Some securitizations use external credit enhancement provided by third parties, such as surety bonds and parental guarantees (although this may introduce a conflict of interest).

Individual securities are often split into tranches, or categorized into varying degrees of subordination. Each tranche has a different level of credit protection or risk exposure than another: there is generally a senior (“A”) class of securities and one or more junior subordinated (“B”, “C”, etc.) classes that function as protective layers for the “A” class. The senior classes have first claim on the cash that the SPV receives, and the more junior classes only start receiving repayment after the more senior classes have repaid. Because of the cascading effect between classes, this arrangement is often referred to as a cash flow waterfall. In the event that the underlying asset pool becomes insufficient to make payments on the securities (e.g. when loans default within a portfolio of loan claims), the loss is absorbed first by the subordinated tranches, and the upper-level tranches remain unaffected until the losses exceed the entire amount of the subordinated tranches. The senior securities are typically AAA rated, signifying a

19

lower risk, while the lower-credit quality subordinated classes receive a lower credit rating, signifying a higher risk.

The most junior class (often called the equity class) is the most exposed to payment risk. In some cases, this is a special type of instrument which is retained by the originator as a potential profit flow. In some cases the equity class receives no coupon (either fixed or floating), but only the residual cash flow (if any) after all the other classes have been paid.

There may also be a special class which absorbs early repayments in the underlying assets. This is often the case where the underlying assets are mortgages which, in essence, are repaid every time the property is sold. Since any early repayment is passed on to this class, it means the other investors have a more predictable cash flow.

If the underlying assets are mortgages or loans, there are usually two separate "waterfalls" because the principal and interest receipts can be easily allocated and matched. But if the assets are income-based transactions such as rental deals it is not possible to differentiate so easily between how much of the revenue is income and how much principal repayment. In this case all the income is used to pay the cash flows due on the bonds as those cash flows become due.

Credit enhancements affect credit risk by providing more or less protection to promised cash flows for a security. Additional protection can help a security achieve a higher rating, lower protection can help create new securities with differently desired risks, and these differential protections can help place a security on more attractive terms.

In addition to subordination, credit may be enhanced through:

A reserve or spread account, in which funds remaining after expenses such as principal and interest payments, charge-offs and other fees have been paid-off are accumulated, and can be used when SPE expenses are greater than its income.

20

Third-party insurance, or guarantees of principal and interest payments on the securities.

Over-collateralization, usually by using finance income to pay off principal on some securities before principal on the corresponding share of collateral is collected.

Cash funding or a cash collateral account, generally consisting of short-term, highly rated investments purchased either from the seller's own funds, or from funds borrowed from third parties that can be used to make up shortfalls in promised cash flows.

A third-party letter of credit or corporate guarantee. A back-up servicer for the loans. Discounted receivables for the pool.

IV. Servicing

A servicer collects payments and monitors the assets that are the crux of the structured financial deal. The servicer can often be the originator, because the servicer needs very similar expertise to the originator and would want to ensure that loan repayments are paid to the Special Purpose Vehicle.

The servicer can significantly affect the cash flows to the investors because it controls the collection policy, which influences the proceeds collected, the charge-offs and the recoveries on the loans. Any income remaining after payments and expenses is usually accumulated to some extent in a reserve or spread account, and any further excess is returned to the seller. Bond rating agencies publish ratings of asset-backed securities based on the performance of the collateral pool, the credit enhancements and the probability of default.

When the issuer is structured as a trust, the trustee is a vital part of the deal as the gate-keeper of the assets that are being held in the issuer. Even though the trustee is part of the SPV, which is typically wholly owned by the Originator, the trustee has a fiduciary duty to protect the assets and those who own the assets, typically the investors.

21

V. Repayment Structures

Unlike corporate bonds, most securitizations are amortized, meaning that the principal amount borrowed is paid back gradually over the specified term of the loan, rather than in one lump sum at the maturity of the loan. Fully amortizing securitizations are generally collateralized by fully amortizing assets such as home equity loans, auto loans, and student loans. Prepayment uncertainty is an important concern with fully amortizing ABS. The possible rate of prepayment varies widely with the type of underlying asset pool, so many prepayment models have been developed in an attempt to define common prepayment activity. The PSA prepayment model is a well-known example.

A controlled amortization structure is a method of providing investors with a more predictable repayment schedule, even though the underlying assets may be non amortizing. After a predetermined “revolving” period, during which only interest payments are made, these securitizations attempt to return principal to investors in a series of defined periodic payments, usually within a year. An early amortization event is the risk of the debt being retired early.

On the other hand, bullet or slug structures return the principal to investors in a single payment. The most common bullet structure is called the soft bullet, meaning that the final bullet payment is not guaranteed on the expected maturity date; however, the majority of these securitizations are paid on time. The second type of bullet structure is the hard bullet, which guarantees that the principal will be paid on the expected maturity date. Hard bullet structures are less common for two reasons: investors are comfortable with soft bullet structures, and they are reluctant to accept the lower yields of hard bullet securities in exchange for a guarantee.

Securitizations are often structured as a sequential pay bond, paid off in a sequential manner based on maturity. This means that the first tranche, which may have a one-year average life, will receive all principal payments until it is retired; then the second tranche begins to receive principal, and so forth. Pro rata bond structures pay each tranche a proportionate share of principal throughout the life of the security.

22

KEY PLAYERS

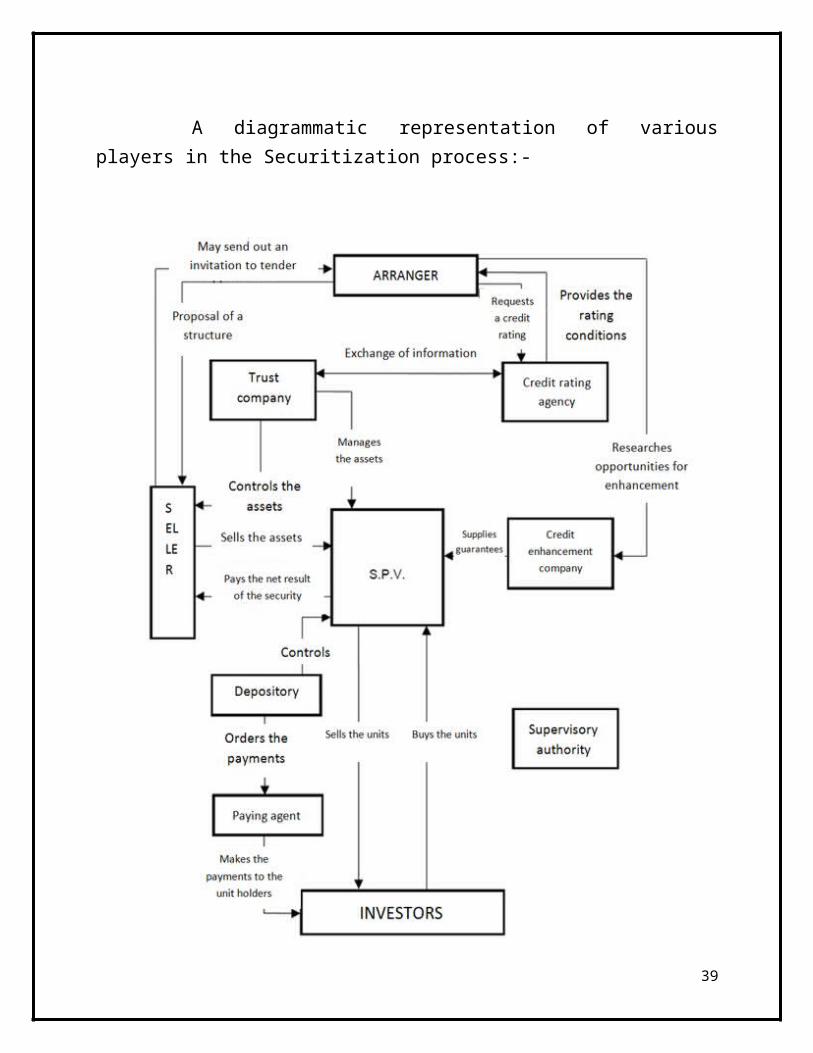

The KEY "players" in the securitization process, all of whom require legal representation to some degree, are as follows:

I. Originator

The entity that either generates receivables in the ordinary course of its business or purchases or assembles portfolios of receivables (in that sense, not a true "originator"). Its counsel works closely with counsel to the Underwriter/Placement Agent and the Rating Agencies in structuring the transaction and preparing documents and usually gives the most significant opinions. It also retains and coordinates local counsel in the event that it is not admitted in the jurisdiction where the Originator's principal office is located and in situations where significant Receivables are generated and the security interests that secure the Receivables are governed by local law rather than the law of the state where the Originator is located.

II. Issuer

The special purpose entity, usually an owner trust (but can be another form of trust or a corporation, partnership or fund), created pursuant to a Trust Agreement between the Originator (or in a two step structure, the Intermediate SPE) and the Trustee, that issues the Securities and avoids taxation at the entity level. This can create a problem in foreign Securitizations in civil law countries where the trust concept does not exist (see discussion below under "Foreign Securitizations").

III. Trustees

Usually a bank or other entity authorized to act in such capacity. The Trustee, appointed pursuant to a Trust Agreement, holds the Receivables, receives payments on the Receivables and makes payments to the Securityholders. In many structures there are two Trustees. For example, in an Owner Trust structure, which

23

is most common, the Notes, which are pure debt instruments, are issued pursuant to an Indenture between the Trust and an Indenture Trustee, and the Certificates, representing undivided interests in the Trust (although structured and treated as debt obligations), are issued by the Owner Trustee. The Issuer (the Trust) owns the Receivables and grants a security interest in the Receivables to the Indenture Trustee. Counsel to the Trustee provides the usual opinions on the Trust as an entity, the capacity of the Trustee, etc.

IV. Investors

The ultimate purchasers of the Securities. Usually banks, insurance companies, retirement funds and other "qualified investors." In some cases, the Securities are purchased directly from the Issuer, but more commonly the Securities are issued to the Originator or Intermediate SPE as payment for the Receivables and then sold to the Investors, or in the case of an underwriting, to the Underwriters.

V. Underwriters/Placement Agents

The brokers, investment banks or banks that sell or place the Securities in a public offering or private placement. The Underwriters/Placement Agents usually play the principal role in structuring the transaction, frequently seeking out Originators for Securitizations, and their counsel (or counsel for the lead Underwriter/Placement Agent) is usually, but not always, the primary document preparer, generating the offering documents (private placement memorandum or offering circular in a private placement; registration statement and prospectus in a public offering), purchase agreements, trust agreement, custodial agreement, etc. Such counsel also frequently opines on securities and tax matters.

VI. Custodian

An entity, usually a bank, that actually holds the Receivables as agent and bailee for the Trustee or Trustees.

24

VII. Rating Agencies

Moody's, S&P, Fitch IBCA and Duff & Phelps. In Securitizations, the Rating Agencies frequently are active players that enter the game early and assist in structuring the transaction. In many instances they require structural changes, dictate some of the required opinions and mandate changes in servicing procedures.

VIII. Servicer

The Servicer is the entity that actually deals with the Receivables on a day to day basis, collecting the Receivables and transferring funds to accounts controlled by the Trustees. In most transactions the Originator acts as Servicer.

IX. Backup Servicer

The entity (usually in the business of acting in such capacity, as well as a primary Servicer when the Originator does not fill that function) that takes over the event that something happens to the Servicer. Depending upon the quality of the Originator/Servicer, the need and significance of the Backup Servicer may be important. In some cases the Trustee retains the Backup Servicer to perform certain monitoring functions on a continuing basis.

25

A diagrammatic representation of various players in the Securitization process:-

26

27

MERITS AND DEMERITS

The advantages of Securitization are as follows:

I. The Seller

For the originator, the main reason for securitizing is to reduce (some might say “get rid of”) the amount of assigned debt from his balance sheet, which on the one hand leads to a corresponding reduction in his regulatory capital requirements under Basel II, and on the other hand enables him to bring in additional liquidity (which can be used to make new loans).

i. Reduces Funding Costs: Through securitization, a company rated BB but with AAA worthy cash flow would be able to borrow at possibly AAA rates. This is the number one reason to securitize a cash flow and can have tremendous impacts on borrowing costs. The difference between BB debt and AAA debt can be multiple hundreds of basis points. For example, Moody's downgraded Ford Motor Credit's rating in January 2002, but senior automobile backed securities, issued by Ford Motor Credit in January 2002 and April 2002, continue to be rated AAA because of the strength of the underlying collateral and other credit enhancements.

ii. Reduces asset-liability mismatch: "Depending on the structure chosen, securitization can offer perfect matched funding by eliminating funding exposure in terms of both duration and pricing basis." Essentially, in most banks and finance companies, the liability book or the funding is from borrowings. This often comes at a high cost. Securitization allows such banks and finance companies to create a self-funded asset book.

iii. Lower capital requirements: Some firms, due to legal, regulatory, or other reasons, have a limit or range that their leverage is allowed to be. By securitizing some of their assets, which qualifies as a sale for accounting purposes, these firms will be able to remove assets from

28

their balance sheets while maintaining the "earning power" of the assets.

iv. Locking in profits: For a given block of business, the total profits have not yet emerged and thus remain uncertain. Once the block has been securitized, the level of profits has now been locked in for that company, thus the risk of profit not emerging, or the benefit of super-profits, has now been passed on.

v. Transfer risks (credit, liquidity, prepayment, reinvestment, asset concentration): Securitization makes it possible to transfer risks from an entity that does not want to bear it, to one that does. Two good examples of this are catastrophe bonds and Entertainment Securitizations. Similarly, by securitizing a block of business (thereby locking in a degree of profits), the company has effectively freed up its balance to go out and write more profitable business.

vi. Off balance sheet: Derivatives of many types have in the past been referred to as "off-balance-sheet." This term implies that the use of derivatives has no balance sheet impact. While there are differences among the various accounting standards internationally, there is a general trend towards the requirement to record derivatives at fair value on the balance sheet. There is also a generally accepted principle that, where derivatives are being used as a hedge against underlying assets or liabilities, accounting adjustments are required to ensure that the gain/loss on the hedged instrument is recognized in the income statement on a similar basis as the underlying assets and liabilities. Certain credit derivatives products, particularly Credit Default Swaps, now have more or less universally accepted market standard documentation. In the case of Credit Default Swaps, this documentation has been formulated by the International Swaps and Derivatives Association (ISDA) who have for long time provided documentation on how to treat such derivatives on balance sheets.

vii. Earnings: Securitization makes it possible to record an earnings bounce without any real addition to the firm. When a securitization takes place, there often is a "true sale" that takes place between the Originator (the parent company) and the SPE. This sale has to be for the market value of the underlying assets for the "true sale" to stick

29

and thus this sale is reflected on the parent company's balance sheet, which will boost earnings for that quarter by the amount of the sale. While not illegal in any respect, this does distort the true earnings of the parent company.

viii. Admissibility: Future cash flows may not get full credit in a company's accounts (life insurance companies, for example, may not always get full credit for future surpluses in their regulatory balance sheet), and a securitization effectively turns an admissible future surplus flow into an admissible immediate cash asset.

ix. Liquidity: Future cash flows may simply be balance sheet items which currently are not available for spending, whereas once the book has been securitized, the cash would be available for immediate spending or investment. This also creates a reinvestment book which may well be at better rates.

II. The Investor

Securitization present an opportunity to invest in asset classes that are not accessible in the markets and that offer a risk/return profile that is, in principle, attractive.

i. Opportunity to invest in a specific pool of high quality assets: Due to the stringent requirements for corporations (for example) to attain high ratings, there is a dearth of highly rated entities that exist. Securitizations, however, allow for the creation of large quantities of AAA, AA or A rated bonds, and risk adverse institutional investors, or investors that are required to invest in only highly rated assets have access to a larger pool of investment options.

ii. Portfolio diversification: Depending on the securitization, hedge funds as well as other institutional investors tend to like investing in bonds created through securitizations because they may be uncorrelated to their other bonds and securities.

iii. Isolation of credit risk from the parent entity: Since the assets that are securitized are isolated (at least in theory) from the assets of the originating entity, under securitization it may be possible for the

30

securitization to receive a higher credit rating than the "parent," because the underlying risks are different. For example, a small bank may be considered more risky than the mortgage loans it makes to its customers; were the mortgage loans to remain with the bank, the borrowers may effectively be paying higher interest (or, just as likely, the bank would be paying higher interest to its creditors, and hence less profitable).

The disadvantages and drawbacks of Securitization are as follows:-

I. The Seller

i. May reduce portfolio quality: If the AAA risks, for example, are being securitized out, this would leave a materially worse quality of residual risk.

ii. Costs: Securitizations are expensive due to management and system costs, legal fees, underwriting fees, rating fees and ongoing administration. An allowance for unforeseen costs is usually essential in securitizations, especially if it is an atypical securitization.

iii. Size limitations: Securitizations often require large scale structuring, and thus may not be cost-efficient for small and medium transactions.

iv. Risks: Since securitization is a structured transaction, it may include par structures as well as credit enhancements that are subject to risks of impairment, such as prepayment, as well as credit loss, especially for structures where there are some retained strips.

II. The Investor

i. Credit/default: Default risk is generally accepted as a borrower’s inability to meet interest payment obligations on time. For ABS, default may occur when maintenance obligations on the underlying collateral are not sufficiently met as detailed in its prospectus. A key indicator of a particular security’s default risk is its credit rating. Different tranches within the ABS are rated differently, with senior

31

classes of most issues receiving the highest rating, and subordinated classes receiving correspondingly lower credit ratings. Almost all mortgages, including reverse mortgages, and student loans, are now insured by the government, meaning that taxpayers are on the hook for any of these loans that go bad even if the asset is massively over-inflated. In other words, there are no limits or curbs on over-spending, or the liabilities to taxpayers.

ii. Prepayment/reinvestment/early amortization: The majority of revolving ABS is subject to some degree of early amortization risk. The risk stems from specific early amortization events or payout events that cause the security to be paid off prematurely. Typically, payout events include insufficient payments from the underlying borrowers, insufficient excess spread, a rise in the default rate on the underlying loans above a specified level, a decrease in credit enhancements below a specific level, and bankruptcy on the part of the sponsor or servicer.

iii. Currency interest rate fluctuations: Like all fixed income securities, the prices of fixed rate ABS move in response to changes in interest rates. Fluctuations in interest rates affect floating rate ABS prices less than fixed rate securities, as the index against which the ABS rate adjusts will reflect interest rate changes in the economy. Furthermore, interest rate changes may affect the prepayment rates on underlying loans that back some types of ABS, which can affect yields. Home equity loans tend to be the most sensitive to changes in interest rates, while auto loans, student loans, and credit cards are generally less sensitive to interest rates.

iv. Moral hazard: Investors usually rely on the deal manager to price the securitizations’ underlying assets. If the manager earns fees based on performance, there may be a temptation to mark up the prices of the portfolio assets. Conflicts of interest can also arise with senior note holders when the manager has a claim on the deal's excess spread.

v. Servicer risk: The transfer or collection of payments may be delayed or reduced if the servicer becomes insolvent. This risk is mitigated by having a backup servicer involved in the transaction.

32

SECURITIZATION IN INDIA

Securitization in India began in the early nineties. It has been of a recent origin. Initially it started as a device for bilateral acquisitions of portfolios of finance companies. These were forms of quasi-securitizations, with portfolios moving from the balance sheet of one originator to that of another. Originally these transactions included provisions that provided recourse to the originator as well as new loan sales through the direct assignment route, which was structured using the true sale concept. Through most of the 90s, securitization of auto loans was the mainstay of the Indian markets. But since 2000, Residential Mortgage Backed Securities (RMBS) have fuelled the growth of the market.

Securitization in India began with the sale of consumer loan pools. Originators directly sold loans to buyers. Originators acted as servicers and collected installments due on the loans. Creation of transferable securities backed by pool receivables (known as PTCs) became common in late 1990s.

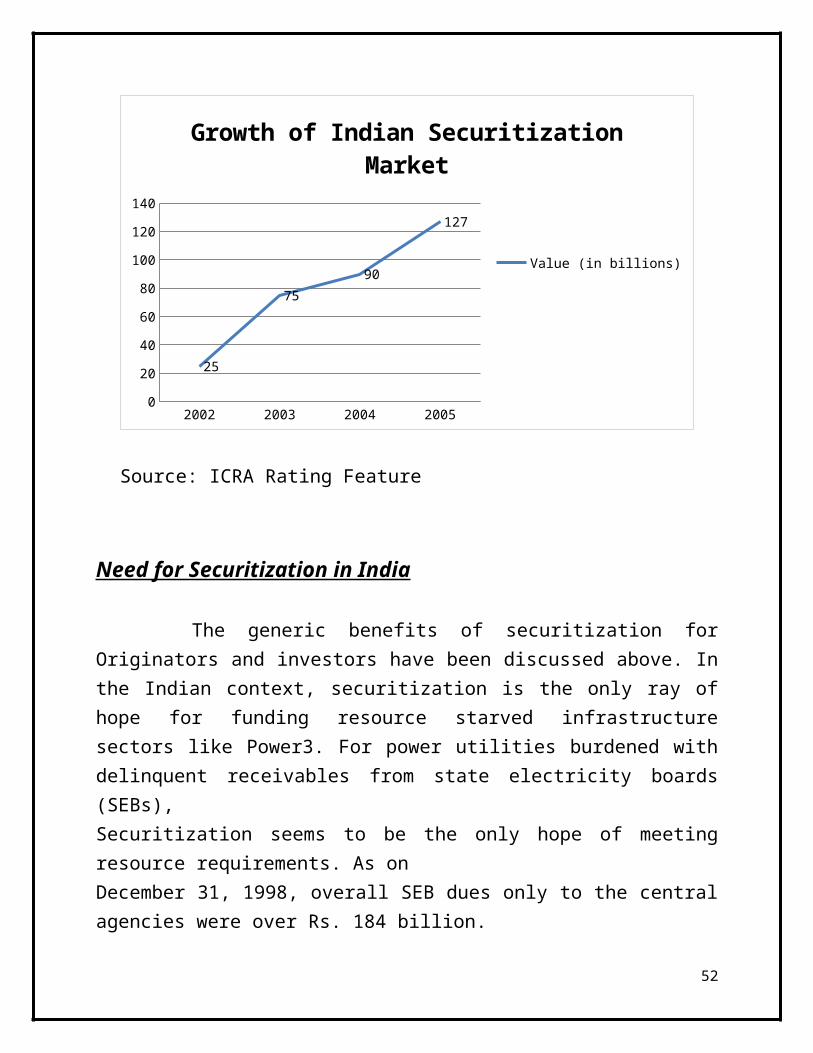

In 1990s, there were only six or seven issuances per year. Average issue size was about Rs.450 million. The volume of issuances grew exponentially beginning in 2000 due to rapid growth of consumer finance. Investor’s acceptance of securitized instruments also improved. There were approximately 75 issuances each year. Average issue size was about Rs.1900 million. There was pressure on the resources of large originators due to continued growth in consumer credit. From 2004 to 2005, 40% of vehicle finance was funded through ABS backed by auto loans.

Citibank completed India's first revolving securitization issuance for its small and medium enterprises working capital loans in 2004. The fixed rate issuance of Rs 50 crore comprised two series of pass through certificates with bullet maturity of two years. Strong performance and higher yields also attracted investors.

33

The first deal in India was in 1992 when Citibank securitized auto loans and placed a paper with GIC mutual fund worth about Rs. 16 crores. In 1994-95, SBI Caps structured an innovative deal where a pool of future cash flows of high value customers of RSIDC was securitized. ICICI had securitized assets to the tune of Rs. 2,750 crore in its books as at end March 1999. Another novel move was by Maharashtra government to securitize sales tax. The Maharashtra Vikrikar Rokhe Pradhikaran (MVRP) is the SPV to undertake this first of its kind transaction in the country.

2002 2003 2004 20050

20

40

60

80

100

120

140

25

75

90

127

Growth of Indian Securitization Market

Value (in billions)

Source: ICRA Rating Feature

Need for Securitization in India

The generic benefits of securitization for Originators and investors have been discussed above. In the Indian context, securitization is the only ray of

34

hope for funding resource starved infrastructure sectors like Power3. For power utilities burdened with delinquent receivables from state electricity boards (SEBs),Securitization seems to be the only hope of meeting resource requirements. As onDecember 31, 1998, overall SEB dues only to the central agencies were over Rs. 184 billion.

Securitization can help Indian borrowers with international assets in piercing the sovereign rating and placing an investment grade structure. An example, albeit failed, is that of Air India’s aborted attempt to securitize its North American ticket receivables. Such structured transactions can help premier corporates to obtain a superior pricing than a borrowing based on their non-investment grade corporate rating.

After the merger of India’s largest financial institution ICICI with ICICI Bank, ICICI, faced with SLR and other requirements, is actively seeking to launch a CLO to reduce its overall asset exposure. It appears to be only a matter of time before other Public Financial Institutions merge with other banks. Such mergers would result in the need for more CDOs in the foreseeable future.

Shortcomings faced by Indian S ecuritized Markets :

i. Stamp Duty : One of the biggest hurdles facing the development of the securitization market is the stamp duty structure. Stamp duty is payable on any instrument which seeks to transfer rights or receivables, whether by way of assignment or novation (new clause added to the contract) or by any other mode. Therefore, the process of transfer of the receivables from the originator to the SPV involves an outlay on account of stamp duty, which can make securitization commercially unviable in several states. If the securitized instrument is issued as evidencing indebtedness, it would be in the form of a debenture or bond subject to stamp duty. On the other hand, if the instrument is structured as a Pass Through Certificate (PTC) that merely evidences title to the receivables, then such an instrument would not attract stamp duty, as it is not an instrument provided for specifically in the charging provisions.

35

Among the regulatory costs, the stamp duty on transfers of the securitized instrument is again a major hurdle. Some states do not distinguish between conveyances of real estate and that of receivables, and levy the same rate of stamp duty on the two. Stamp duty being a concurrent subject i.e. it is under the concurrent list in Schedule 7 of the Indian Constitution, specifically calls for a consensual legal position between the Centre and the States.

ii. Foreclosure Laws : Lack of effective foreclosure laws also prohibits the growth of securitization in India. The Existing foreclosure laws are not lender friendly and increase the risks of Mortgage Backed Securities by making it difficult to transfer property in cases of default. Transfer of property laws lacks on this aspect.

iii. Taxation Issues : Tax treatment of Mortgage Backed Securities, SPV Trusts and NPL Trusts is unclear. Currently, the investors (PTC and SR holders) pay tax on the income distributed by the SPV Trusts and on that basis the trustees make income pay outs to the PTC holders without any payment or withholding of tax. The view is based on legal opinions regarding assessment of investors instead of trustee in their representative capacity. It needs to be emphasized that the Income Tax Law has always envisaged taxation of an Unincorporated SPV such as a Trust at only one level, either at the Trust SPV level, or the Investor/Beneficiary Level to avoid double taxation. Hence, any explicit tax pass thro regime if provided in the Income Tax Act does not represent conferment of any real tax concession or tax sacrifice, but merely represents a position that the Investors in the trust would be liable to tax instead of the Trust being held liable to tax on the income earned. Amendments need to be made to provide an explicit tax pass thought treatment to securitization SPVs and Non Performing Assets Securitization SPVs on par with the tax pass through treatment applied under the tax law to Venture Capital Funds registered with SEBI. To make it certain that investors as holders of Mutual Fund (MF) schemes are liable to pay tax on the income from MF and ensure that there is no tax dispute about the MBS SPV Trust or NPA

36

Securitization Trust being treated as an AOP(Association of Persons), SEBI should consider the possibility of modifying the Mutual Fund Regulations to permit wholesale investors (investors who invests not less than Rs. 5 million in scheme) to invest and hold units of a closed-ended passively managed mutual fund scheme. The sole objective of this scheme is to invest its funds into PTCs and SRs of the designated Mortgage Backed Security.

iv. SPV/NPA Securitization Trust : Recognizing the wholesale investor and Qualified Institutional Buyers (QIB) in securitization trusts, there should be no withholding of tax requirements on interest paid by the borrowers (whose credit exposures are securitized) to the securitization trust. Similarly, there should be no requirement of withholding tax on distributions made by the securitization Trust to its PTC and SR holders. However, the securitization trust may be required to file an annual return with the Income-tax Department, Ministry of Finance, in which all relevant particulars of the income distributions and identity of the PTC and SR holders may be included. This will safeguard against any possibility of revenue leakage.

v. Legal Issues : Currently, the Securities Contract Regulation Act definition of ‘securities’ does not specifically cover PTCs. While there is indeed a legal view that the current definition of securities in the SCRA includes any instrument derived from, or any interest in securities, the nature of the instrument and the background of the issuer of the instrument, not being homogenous in respect of the rights and obligations attached, across instruments issued by various SPVs, has resulted in a degree of discomfort among exchanges listing these instruments. To remove any ambiguity in this regard, the Central Government should consider notifying PTCs and other securities issued by securitization SPV Trust as ‘securities’ under the SCRA.

37

US SUBPRIME MORTGAGE CRISIS

The U.S. subprime mortgage crisis was a set of events and conditions that led to the late-2000s financial crisis, characterized by a rise in subprime mortgage delinquencies and foreclosures, and the resulting decline of securities backed by said mortgages.

The percentage of new lower-quality subprime mortgages rose from the historical 8% or lower range to approximately 20% from 2004 to 2006, with much higher ratios in some parts of the U.S. A high percentage of these subprime mortgages, over 90% in 2006 for example, were adjustable-rate mortgages. These two changes were part of a broader trend of lowered lending standards and higher-risk mortgage products. Further, U.S. households had become increasingly indebted, with the ratio of debt to disposable personal income rising from 77% in 1990 to 127% at the end of 2007, much of this increase mortgage-related.

After U.S. house sales prices peaked in mid-2006 and began their steep decline forthwith, refinancing became more difficult. As adjustable-rate mortgages began to reset at higher interest rates (causing higher monthly payments), mortgage delinquencies soared. Securities backed with mortgages, including subprime mortgages, widely held by financial firms, lost most of their value. Global investors also drastically reduced purchases of mortgage-backed debt and other securities as part of a decline in the capacity and willingness of the private financial system to support lending. Concerns about the soundness of U.S. credit and financial markets led to tightening credit around the world and slowing economic growth in the U.S. and Europe.

Background and timeline of events:

The immediate cause or trigger of the crisis was the bursting of the United States housing bubble which peaked in approximately 2005–2006. High default rates on "subprime" and adjustable rate mortgages (ARM), began to increase quickly thereafter. Lenders began originating large numbers of high risk

38

mortgages from around 2004 to 2007, and loans from those vintage years exhibited higher default rates than loans made either before or after.

An increase in loan incentives such as easy initial terms and a long-term trend of rising housing prices had encouraged borrowers to assume difficult mortgages in the belief they would be able to quickly refinance at more favorable terms. Additionally, the increased market power of originators of subprime mortgages and the declining role of Government Sponsored Enterprises as gatekeepers increased the number of subprime mortgages provided to consumers who would have otherwise qualified for conforming loans.

The worst performing loans were securitized by private investment banks, which generally lacked the GSE's market power and influence over mortgage originators. Once interest rates began to rise and housing prices started to

39

drop moderately in 2006–2007 in many parts of the U.S., refinancing became more difficult. Defaults and foreclosure activity increased dramatically as easy initial terms expired, home prices failed to go up as anticipated, and ARM interest rates reset higher. Falling prices also resulted in 23% of U.S. homes worth less than the mortgage loan by September 2010, providing a financial incentive for borrowers to enter foreclosure. The ongoing foreclosure epidemic, of which subprime loans are one part, that began in late 2006 in the U.S. continues to be a key factor in the global economic crisis, because it drains wealth from consumers and erodes the financial strength of banking institutions.

In the years leading up to the crisis, significant amounts of foreign money flowed into the U.S. from fast-growing economies in Asia and oil-producing countries. This inflow of funds combined with low U.S. interest rates from 2002–2004 contributed to easy credit conditions, which fueled both housing and credit bubbles. Loans of various types (e.g., mortgage, credit card, and auto) were easy to obtain and consumers assumed an unprecedented debt load.

40

As part of the housing and credit booms, the amount of financial agreements called mortgage-backed securities (MBS), which derive their value from mortgage payments and housing prices, greatly increased. Such financial innovation enabled institutions and investors around the world to invest in the U.S. housing market. As housing prices declined, major global financial institutions that had borrowed and invested heavily in MBS reported significant losses. Defaults and losses on other loan types also increased significantly as the crisis expanded from the housing market to other parts of the economy. Total losses are estimated in the trillions of U.S. dollars globally.

While the housing and credit bubbles were growing, a series of factors caused the financial system to become increasingly fragile. Policymakers did not recognize the increasingly important role played by financial institutions such as investment banks and hedge funds, also known as the shadow banking system.

Shadow banks were able to mask their leverage levels from investors and regulators through the use of complex, off-balance sheet derivatives and securitizations. These instruments also made it virtually impossible to reorganize financial institutions in bankruptcy, and contributed to the need for government bailouts. Some experts believe these institutions had become as important as commercial (depository) banks in providing credit to the U.S. economy, but they were not subject to the same regulations. These institutions as well as certain regulated banks had also assumed significant debt burdens while providing the loans described above and did not have a financial cushion sufficient to absorb large loan defaults or MBS losses.

These losses impacted the ability of financial institutions to lend, slowing economic activity. Concerns regarding the stability of key financial institutions drove central banks to take action to provide funds to encourage lending and to restore faith in the commercial paper markets, which are integral to funding business operations. Governments also bailed out key financial institutions, assuming significant additional financial commitments.

41

The risks to the broader economy created by the housing market downturn and subsequent financial market crisis were primary factors in several decisions by central banks around the world to cut interest rates and governments to implement economic stimulus packages. Effects on global stock markets due to the crisis have been dramatic. Between 1 January and 11 October 2008, owners of stocks in U.S. corporations had suffered about $8 trillion in losses, as their holdings declined in value from $20 trillion to $12 trillion. Losses in other countries have averaged about 40%. Losses in the stock markets and housing value declines place further downward pressure on consumer spending, a key economic engine. Leaders of the larger developed and emerging nations met in November 2008 and March 2009 to formulate strategies for addressing the crisis. A variety of solutions have been proposed by government officials, central bankers, economists, and business executives. In the U.S., the Dodd–Frank Wall Street Reform and Consumer Protection Act was signed into law in July 2010 to address some of the causes of the crisis.

42

Causes of the Crisis:

The crisis can be attributed to a number of factors pervasive in both housing and credit markets, factors which emerged over a number of years. Causes proposed include the inability of homeowners to make their mortgage payments (due primarily to adjustable-rate mortgages resetting, borrowers overextending, predatory lending, and speculation), overbuilding during the boom period, risky mortgage products, increased power of mortgage originators, high personal and corporate debt levels, financial products that distributed and perhaps concealed the risk of mortgage default, bad monetary and housing policies, international trade imbalances, and inappropriate government regulation.

During a period of strong global growth, growing capital flows, and prolonged stability earlier this decade, market participants sought higher yields without an adequate appreciation of the risks and failed to exercise proper due diligence. At the same time, weak underwriting standards, unsound risk management practices, increasingly complex and opaque financial products, and consequent excessive leverage combined to create vulnerabilities in the system. Policy-makers, regulators and supervisors, in some advanced countries, did not adequately appreciate and address the risks building up in financial markets, keep pace with financial innovation, or take into account the systemic ramifications of domestic regulatory actions.

During May 2010, Warren Buffett and Paul Volcker separately described questionable assumptions or judgments underlying the U.S. financial and economic system that contributed to the crisis. These assumptions included: 1) Housing prices would not fall dramatically; 2) Free and open financial markets supported by sophisticated financial engineering would most effectively support market efficiency and stability, directing funds to the most profitable and productive uses; 3) Concepts embedded in mathematics and physics could be directly adapted to markets, in the form of various financial models used to evaluate credit risk; 4) Economic imbalances, such as large trade deficits and low savings rates indicative of over-consumption, were sustainable; and 5) Stronger regulation of the shadow banking system and derivatives markets was not needed.

43

The U.S. Financial Crisis Inquiry Commission reported its findings in January 2011. It concluded that "the crisis was avoidable and was caused by: Widespread failures in financial regulation, including the Federal Reserve’s failure to stem the tide of toxic mortgages; Dramatic breakdowns in corporate governance including too many financial firms acting recklessly and taking on too much risk; An explosive mix of excessive borrowing and risk by households and Wall Street that put the financial system on a collision course with crisis; Key policy makers ill prepared for the crisis, lacking a full understanding of the financial system they oversaw; and systemic breaches in accountability and ethics at all levels.”

Three important catalysts of the subprime crisis were the influx of money from the private sector, the banks entering into the mortgage bond market and the predatory lending practices of the mortgage lenders, specifically the adjustable-rate mortgage, 2–28 loan, that mortgage lenders sold directly or indirectly via mortgage brokers. On Wall Street and in the financial industry, moral hazard lay at the core of many of the causes. In its "Declaration of the Summit on Financial Markets and the World Economy," dated 15 November 2008, leaders of the Group of 20 cited the following causes:

1. Boom and bust in the housing market: Low interest rates and large inflows of foreign funds created easy credit conditions for a number of years prior to the crisis, fueling a housing market boom and encouraging debt-financed consumption. The USA home ownership rate increased from 64% in 1994 (about where it had been since 1980) to an all-time high of 69.2% in 2004. Subprime lending was a major contributor to this increase in home ownership rates and in the overall demand for housing, which drove prices higher. Between 1997 and 2006, the price of the typical American house increased by 124%. During the two decades ending in 2001, the national median home price ranged from 2.9 to 3.1 times median household income. This ratio rose to 4.0 in 2004, and 4.6 in 2006. This housing bubble resulted in quite a few homeowners refinancing their homes at lower interest rates, or financing consumer spending by taking out second mortgages secured by the price appreciation. USA household debt as a percentage of annual

44

disposable personal income was 127% at the end of 2007, versus 77% in 1990.

2. Homeowner speculation: Speculative borrowing in residential real estate has been cited as a contributing factor to the subprime mortgage crisis. During 2006, 22% of homes purchased (1.65 million units) were for investment purposes, with an additional 14% (1.07 million units) purchased as vacation homes. During 2005, these figures were 28% and 12%, respectively. In other words, a record level of nearly 40% of homes purchased was not intended as primary residences. David Lereah, NAR's chief economist at the time, stated that the 2006 decline in investment buying was expected: "Speculators left the market in 2006, which caused investment sales to fall much faster than the primary market." Housing prices nearly doubled between 2000 and 2006, a vastly different trend from the historical appreciation at roughly the rate of inflation. While homes had not traditionally been treated as investments subject to speculation, this behavior changed during the housing boom. Media widely reported condominiums being purchased while under construction, then being "flipped" (sold) for a profit without the seller ever having lived in them. Some mortgage companies identified risks inherent in this activity as early as 2005, after identifying investors assuming highly leveraged positions in multiple properties.

3. High-risk mortgage loans and lending/borrowing practices: In the years before the crisis, the behavior of lenders changed dramatically. Lenders offered more and more loans to higher-risk borrowers, including undocumented immigrants. Lending standards particularly deteriorated in 2004 to 2007, as the GSEs market share declined and private securitizers accounted for more than half of mortgage securitizations Subprime mortgages amounted to $35 billion (5% of total originations) in 1994, 9% in 1996, $160 billion (13%) in 1999, and $600 billion (20%) in 2006. A study by the Federal Reserve found that the average difference

45

between subprime and prime mortgage interest rates (the "subprime markup") declined significantly between 2001 and 2007. The combination of declining risk premiums and credit standards is common to boom and bust credit cycles. Another example is the interest-only adjustable-rate mortgage (ARM), which allows the homeowner to pay just the interest (not principal) during an initial period. Still another is a "payment option" loan, in which the homeowner can pay a variable amount, but any interest not paid is added to the principal. Nearly one in 10 mortgage borrowers in 2005 and 2006 took out these “option ARM” loans, which meant they could choose to make payments so low that their mortgage balances rose every month. An estimated one-third of ARMs originated between 2004 and 2006 had "teaser" rates below 4%, which then increased significantly after some initial period, as much as doubling the monthly payment.

4. Mortgage fraud: In 2004, the Federal Bureau of Investigation warned of an "epidemic" in mortgage fraud, an important credit risk of nonprime mortgage lending, which, they said, could lead to "a problem that could have as much impact as the S&L crisis". The Financial Crisis Inquiry Commission reported in January 2011 that: "...mortgage fraud...flourished in an environment of collapsing lending standards and lax regulation. The number of suspicious activity reports – reports of possible financial crimes filed by depository banks and their affiliates – related to mortgage fraud grew 20-fold between 1996 and 2005 and then more than doubled again between 2005 and 2009. One study places the losses resulting from fraud on mortgage loans made between 2005 and 2007 at $112 billion. Lenders made loans that they knew borrowers could not afford and that could cause massive losses to investors in mortgage securities." New York State prosecutors are examining whether eight banks hoodwinked credit ratings agencies, to inflate the grades of subprime-linked investments. The Securities and Exchange Commission, the Justice Department, the United States attorney’s office and more are examining how banks

46

created, rated, sold and traded mortgage securities that turned out to be some of the worst investments ever devised. As of 2010, virtually all of the investigations, criminal as well as civil, are in their early stages.

5. Securitization practices: Securitization and Mortgage-backed security. The traditional mortgage model involved a bank originating a loan to the borrower/homeowner and retaining the credit (default) risk. Securitization is a process whereby loans or other income generating assets are bundled to create bonds which can be sold to investors. The modern version of U.S. mortgage securitization started in the 1980s, as Government Sponsored Enterprises (GSEs) began to pool relatively safe conventional conforming mortgages, sell bonds to investors, and guarantee those bonds against default on the underlying mortgages. A riskier version of securitization also developed in which private banks pooled non-conforming mortgages and generally did not guarantee the bonds against default of the underlying mortgages. In other words, GSE securitization transferred only interest rate risk to investors, whereas private label (investment bank or commercial bank) securitization transferred both interest rate risk and default risk. With the advent of securitization, the traditional model has given way to the "originate to distribute" model, in which banks essentially sell the mortgages and distribute credit risk to investors through mortgage-backed securities and collateralized debt obligations (CDO). The sale of default risk to investors created a moral hazard in which an increased focus on processing mortgage transactions was incentivized but ensuring their credit quality was not. A more direct connection between securitization and the subprime crisis relates to a fundamental fault in the way that underwriters, rating agencies and investors modeled the correlation of risks among loans in securitization pools. Correlation modeling – determining how the default risk of one loan in a pool is statistically related to the default risk for other loans – was based on a "Gaussian copula" technique developed by statistician David

47

X. Li. This technique, widely adopted as a means of evaluating the risk associated with securitization transactions, used what turned out to be an overly simplistic approach to correlation. Unfortunately, the flaws in this technique did not become apparent to market participants until after many hundreds of billions of dollars of ABSs and CDOs backed by subprime loans had been rated and sold. By the time investors stopped buying subprime-backed securities – which halted the ability of mortgage originators to extend subprime loans – the effects of the crisis were already beginning to emerge.

6. Inaccurate credit ratings: Credit rating agencies are now under scrutiny for having given investment-grade ratings to MBSs based on risky subprime mortgage loans. These high ratings enabled these MBSs to be sold to investors, thereby financing the housing boom. These ratings were believed justified because of risk reducing practices, such as credit default insurance and equity investors willing to bear the first losses. However, there are also indications that some involved in rating subprime-related securities knew at the time that the rating process was faulty. Between Q3 2007 and Q2 2008, rating agencies lowered the credit ratings on $1.9 trillion in mortgage-backed securities. Financial institutions felt they had to lower the value of their MBS and acquire additional capital so as to maintain capital ratios. If this involved the sale of new shares of stock, the value of the existing shares was reduced. Thus ratings downgrades lowered the stock prices of many financial firms. The Financial Crisis Inquiry Commission reported in January 2011 that: "The three credit rating agencies were key enablers of the financial meltdown. The mortgage-related securities at the heart of the crisis could not have been marketed and sold without their seal of approval. Investors relied on them, often blindly. In some cases, they were obligated to use them, or regulatory capital standards were hinged on them. This crisis could not have happened without the rating agencies. Their ratings helped the market soar and their downgrades through 2007 and

48

2008 wreaked havoc across markets and firms." The Report further stated that ratings were incorrect because of "flawed computer models, the pressure from financial firms that paid for the ratings, the relentless drive for market share, the lack of resources to do the job despite record profits, and the absence of meaningful public oversight."

7. Government policies: Government over-regulation, failed regulation and deregulation have all been claimed as causes of the crisis. In testimony before Congress both the Securities and Exchange Commission (SEC) and Alan Greenspan claimed failure in allowing the self-regulation of investment banks. In 1982, Congress passed the Alternative Mortgage Transactions Parity Act (AMTPA), which allowed non-federally chartered housing creditors to write adjustable-rate mortgages. Among the new mortgage loan types created and gaining in popularity in the early 1980s were adjustable-rate, option adjustable-rate, balloon-payment and interest-only mortgages. These new loan types are credited with replacing the long standing practice of banks making conventional fixed-rate, amortizing mortgages. Among the criticisms of banking industry deregulation that contributed to the savings and loan crisis was that Congress failed to enact regulations that would have prevented exploitations by these loan types. Subsequent widespread abuses of predatory lending occurred with the use of adjustable-rate mortgages. Approximately 90% of subprime mortgages issued in 2006 were adjustable-rate mortgages.