securities fraud rule 10b-5 last updated 20 feb 12

TRANSCRIPT

Securities Fraud

Rule 10b-5

Last updated 20 Feb 12

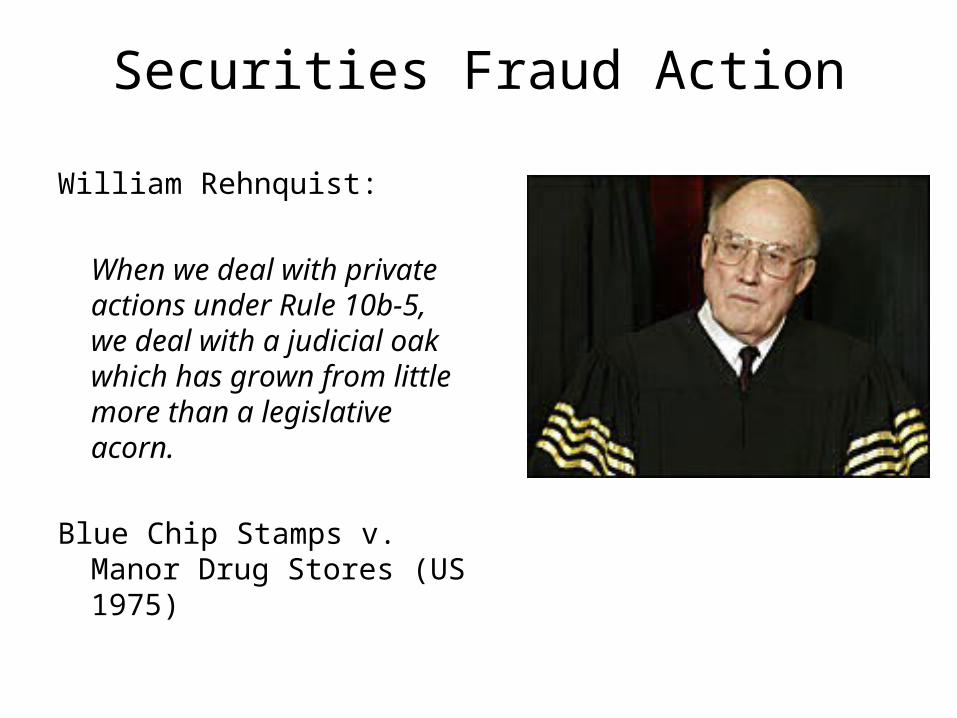

Securities Fraud Action

William Rehnquist:

When we deal with private actions under Rule 10b-5, we deal with a judicial oak which has grown from little more than a legislative acorn.

Blue Chip Stamps v. Manor Drug Stores (US 1975)

Securities Exchange Act of 1934

Section 10 -- Manipulative and Deceptive Devices

It shall be unlawful for any person, directly or indirectly, by the use of any means or instrumentality of interstate commerce or of the mails, or of any facility of any national securities exchange--

(b) To use or employ, in connection with the purchase or sale of any security registered on a national securities exchange or any security not so registered … any manipulative or deceptive device or contrivance in contravention of such rules and regulations as the Commission may prescribe as necessary or appropriate in the public interest or for the protection of investors.

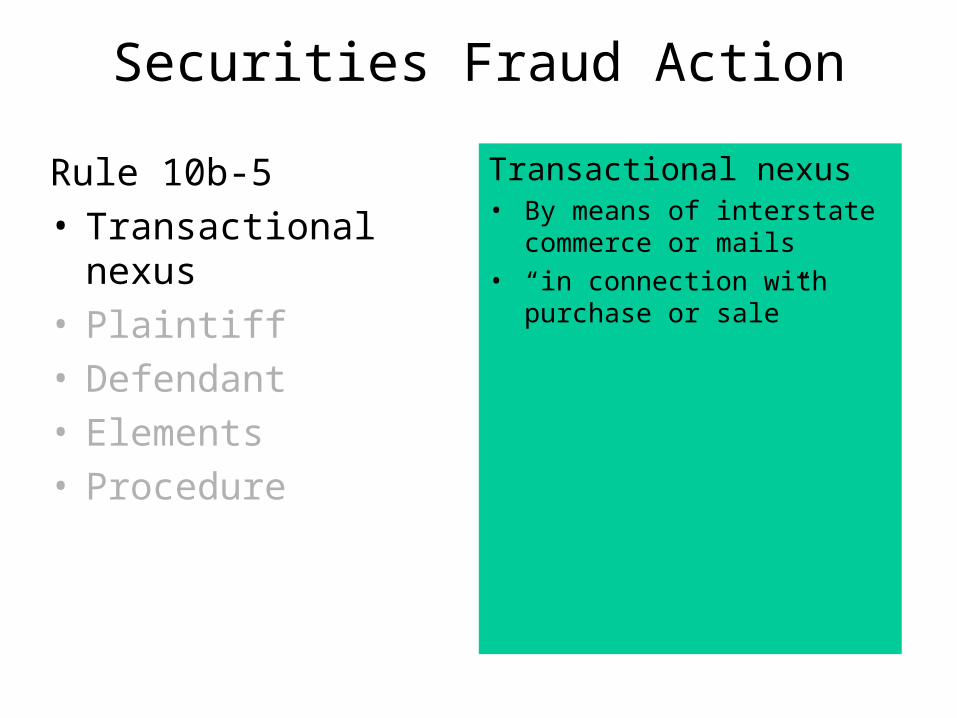

Securities Fraud Action

Rule 10b-5• Transactional nexus• Plaintiff• Defendant• Elements• Procedure

Transactional nexus• By means of interstate

commerce or mails• “in connection with

purchase or sale”

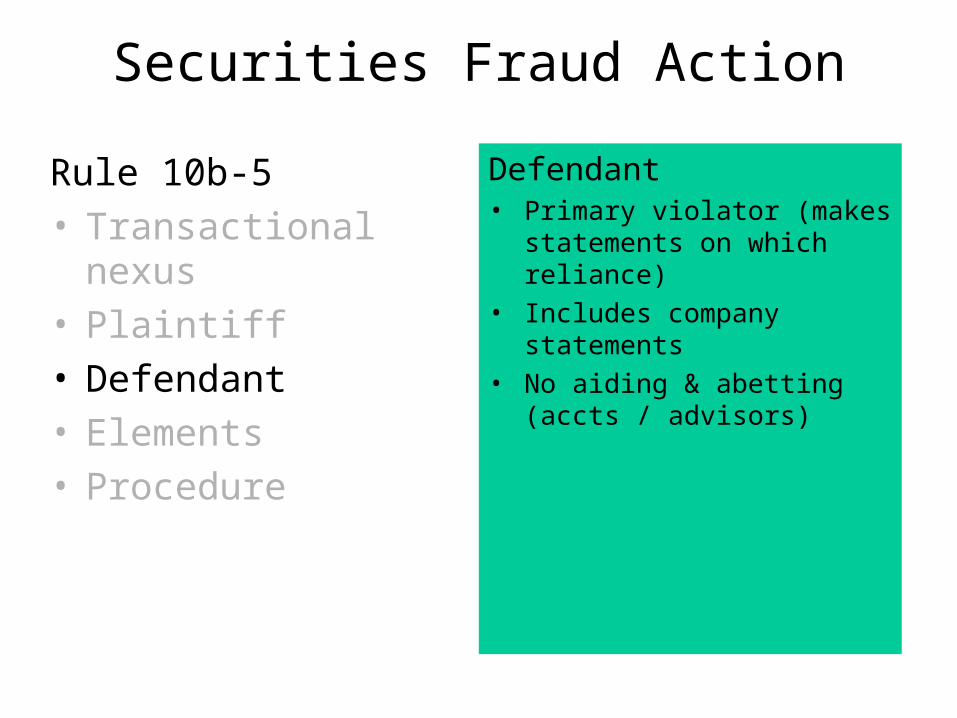

Securities Fraud Action

Rule 10b-5• Transactional nexus• Plaintiff• Defendant• Elements• Procedure

Plaintiff• Purchaser or seller• Except in SEC action

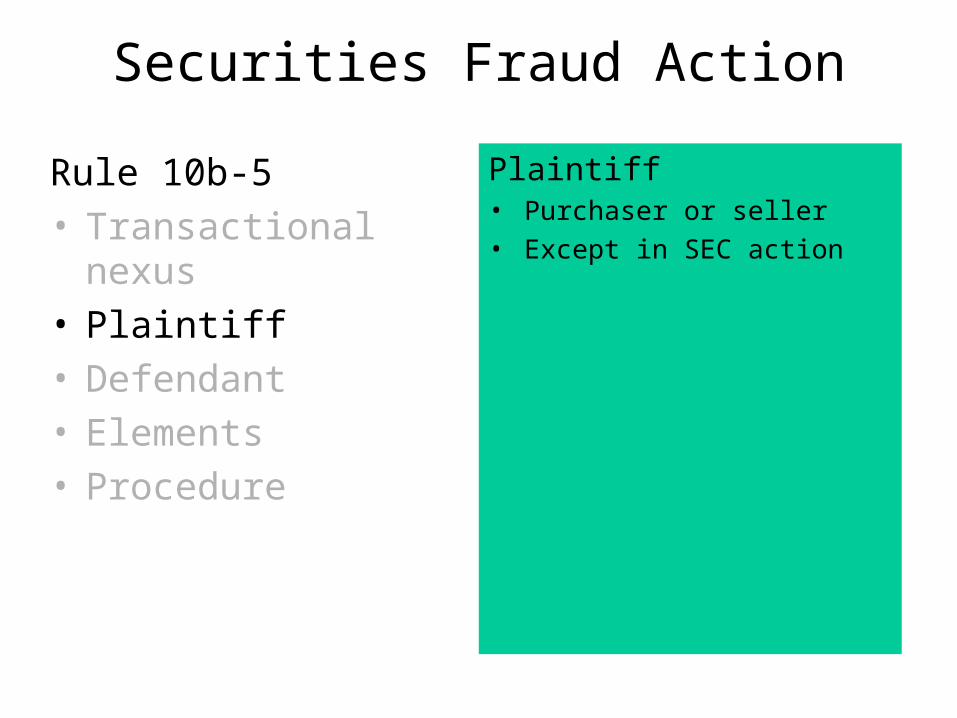

Securities Fraud Action

Rule 10b-5• Transactional nexus• Plaintiff• Defendant• Elements• Procedure

Defendant• Primary violator (makes

statements on which reliance)

• Includes company statements

• No aiding & abetting (accts / advisors)

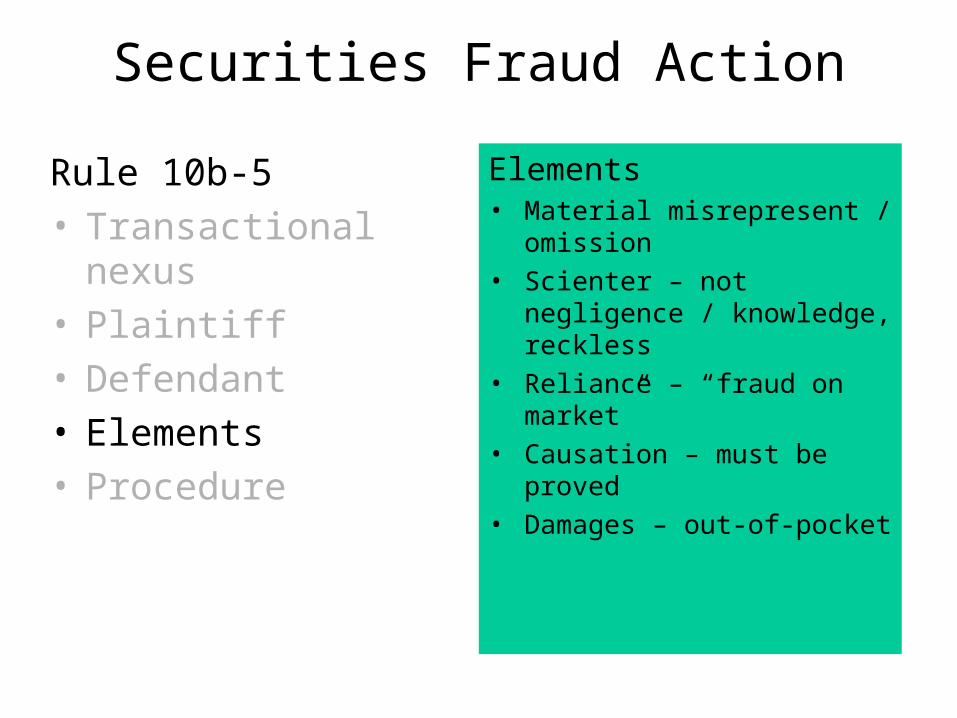

Securities Fraud Action

Rule 10b-5• Transactional nexus• Plaintiff• Defendant• Elements• Procedure

Elements• Material misrepresent /

omission• Scienter – not negligence /

knowledge, reckless• Reliance – “fraud on

market” • Causation – must be

proved• Damages – out-of-pocket

Securities Fraud Action

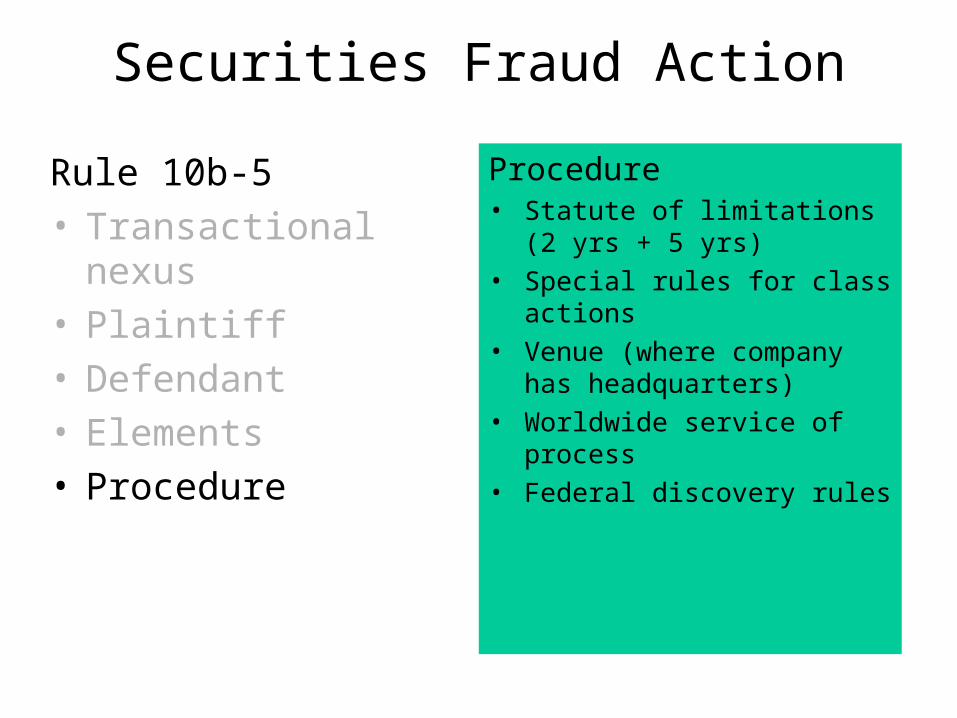

Rule 10b-5• Transactional nexus• Plaintiff• Defendant• Elements• Procedure

Procedure• Statute of limitations (2 yrs

+ 5 yrs)• Special rules for class

actions• Venue (where company

has headquarters)• Worldwide service of

process • Federal discovery rules

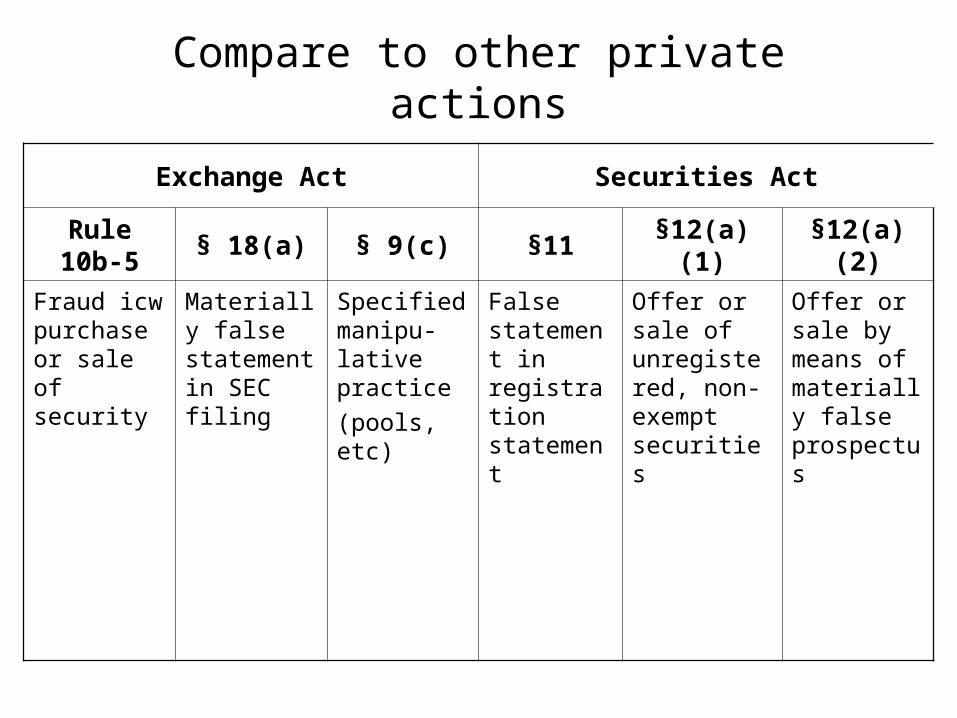

Compare to other private actions

Exchange Act Securities Act

Rule 10b-5

§ 18(a) § 9(c) §11 §12(a)(1)§12(a)

(2)

Fraud icw purchase or sale of security

Materially false statement in SEC filing

Specified manipu-lative practice(pools, etc)

False statement in registration statement

Offer or sale of unregistered, non-exempt securities

Offer or sale by means of materially false prospectus

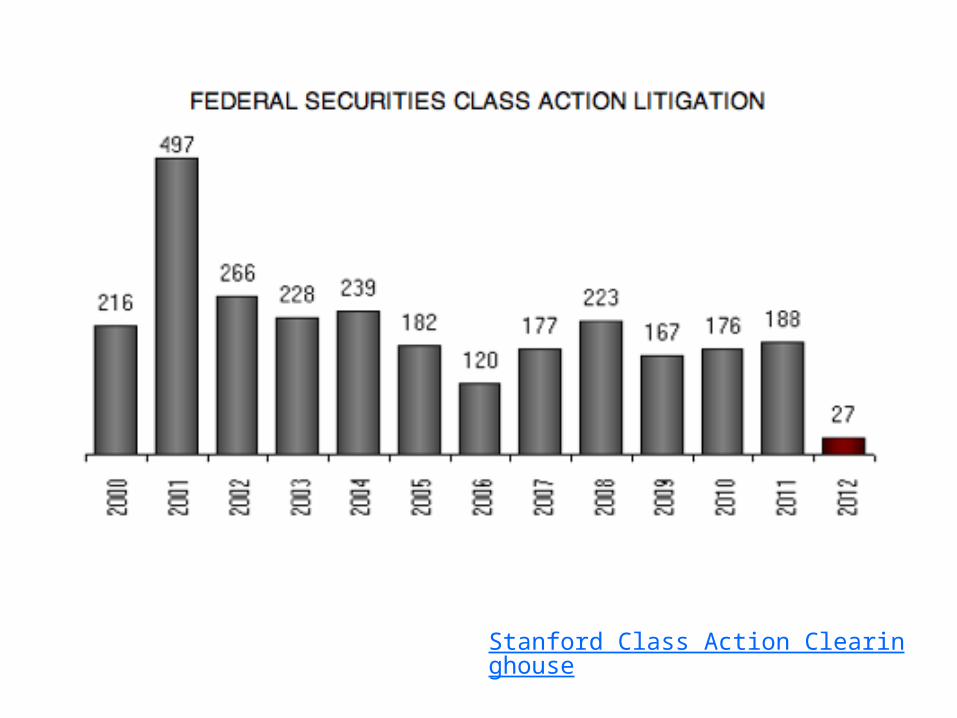

Securities FraudClass Action

“when talk is not cheap”

Stanford Class Action Clearinghouse

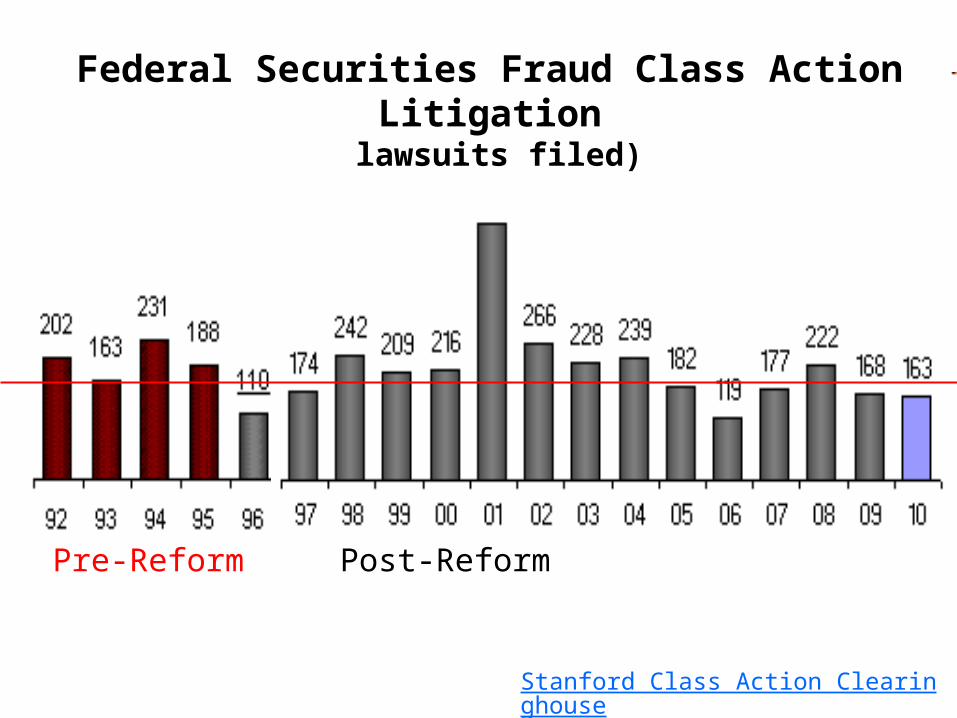

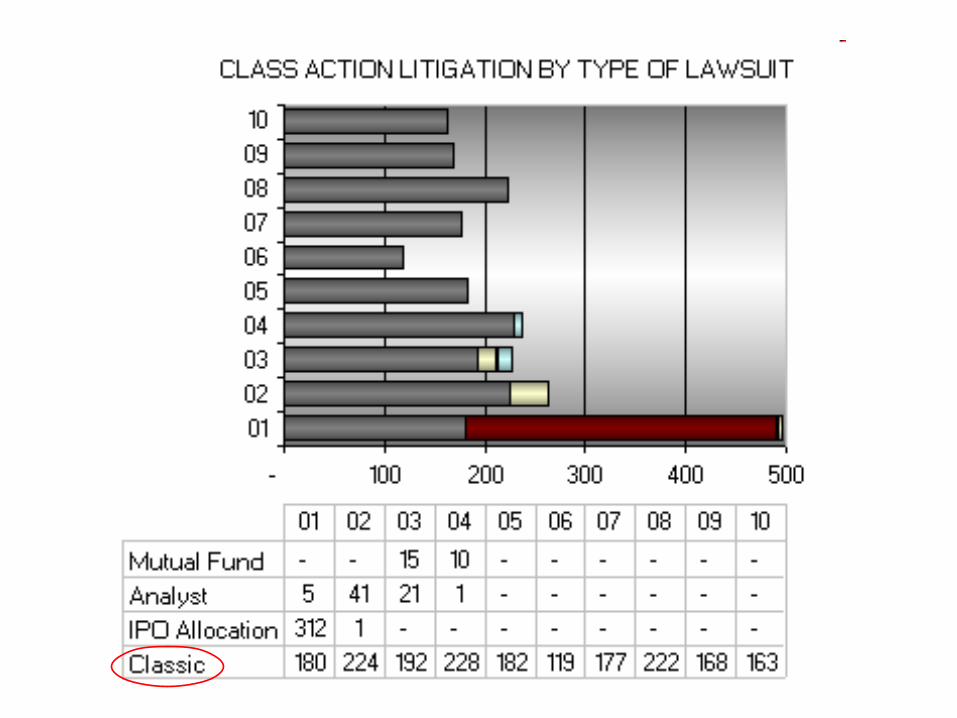

Federal Securities Fraud Class Action Litigation

(lawsuits filed)

Pre-Reform Post-Reform

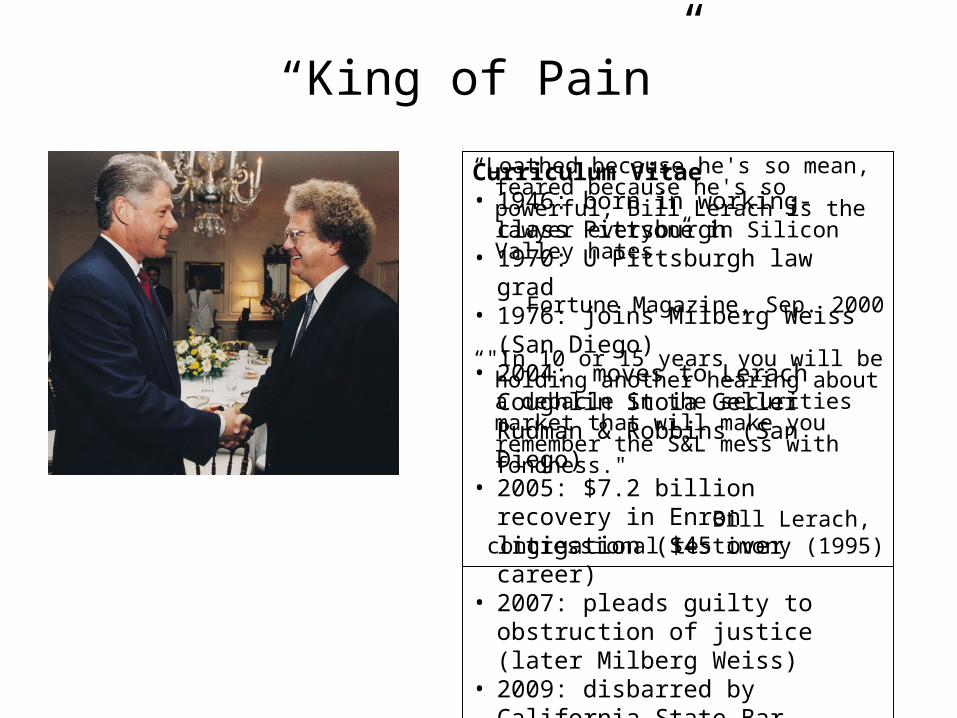

“King of Pain”

“Loathed because he's so mean, feared because he's so powerful, Bill Lerach is the lawyer everyone in Silicon Valley hates.”

Fortune Magazine, Sep. 2000

“"In 10 or 15 years you will be holding another hearing about a debacle in the securities market that will make you remember the S&L mess with fondness."

Bill Lerach, congressional testimony (1995)

Curriculum Vitae• 1946: born in working-class

Pittsburgh• 1970: U Pittsburgh law grad• 1976: joins Milberg Weiss (San

Diego)• 2004: moves to Lerach

Coughlin Stoia Geller Rudman & Robbins (San Diego)

• 2005: $7.2 billion recovery in Enron litigation ($45 over career)

• 2007: pleads guilty to obstruction of justice (later Milberg Weiss)

• 2009: disbarred by California State Bar

• 2010: released from prison / “Circle of Greed” published

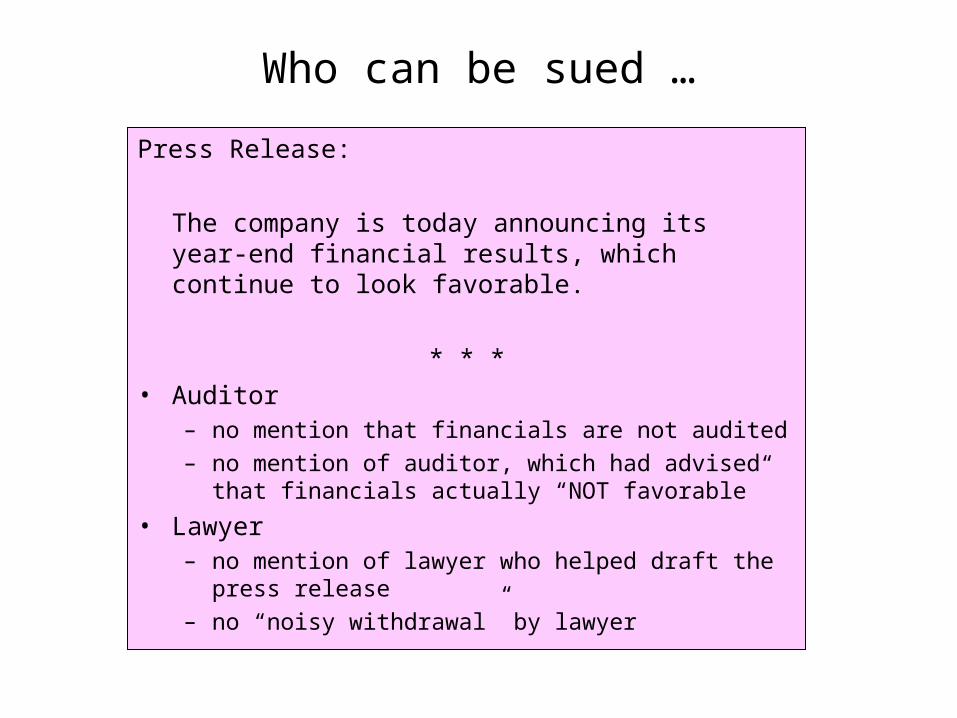

Who can be sued …

Press Release:

The company is today announcing its year-end financial results, which continue to look favorable.

* * *• Auditor

– no mention that financials are not audited– no mention of auditor, which had advised that

financials actually “NOT favorable”

• Lawyer– no mention of lawyer who helped draft the

press release– no “noisy withdrawal” by lawyer

Identify corporate “fiction” …

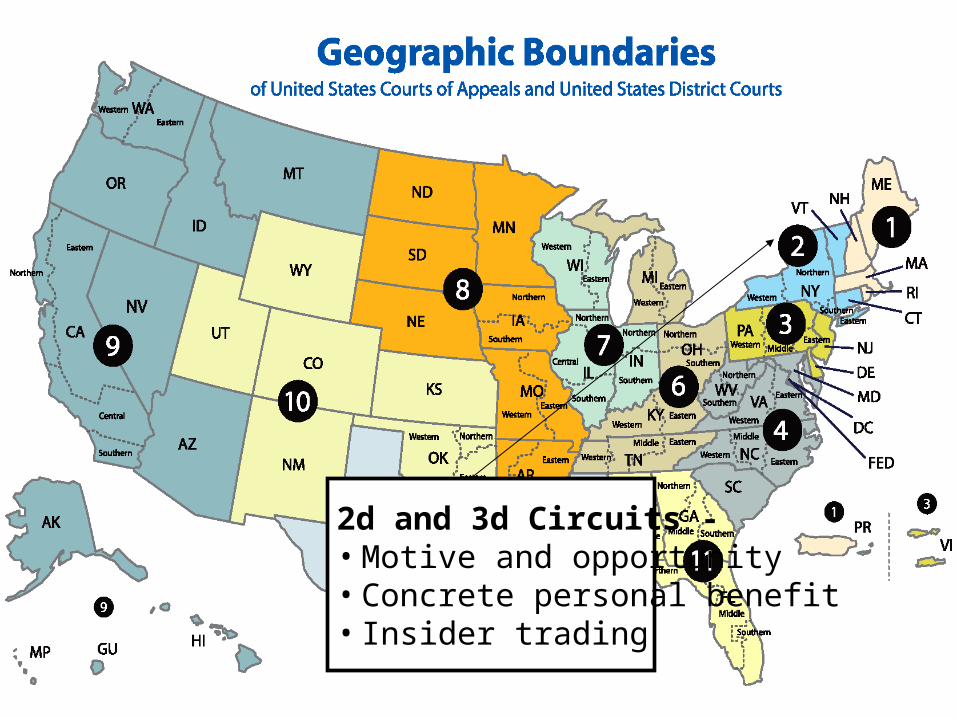

2d and 3d Circuits -• Motive and opportunity• Concrete personal benefit• Insider trading

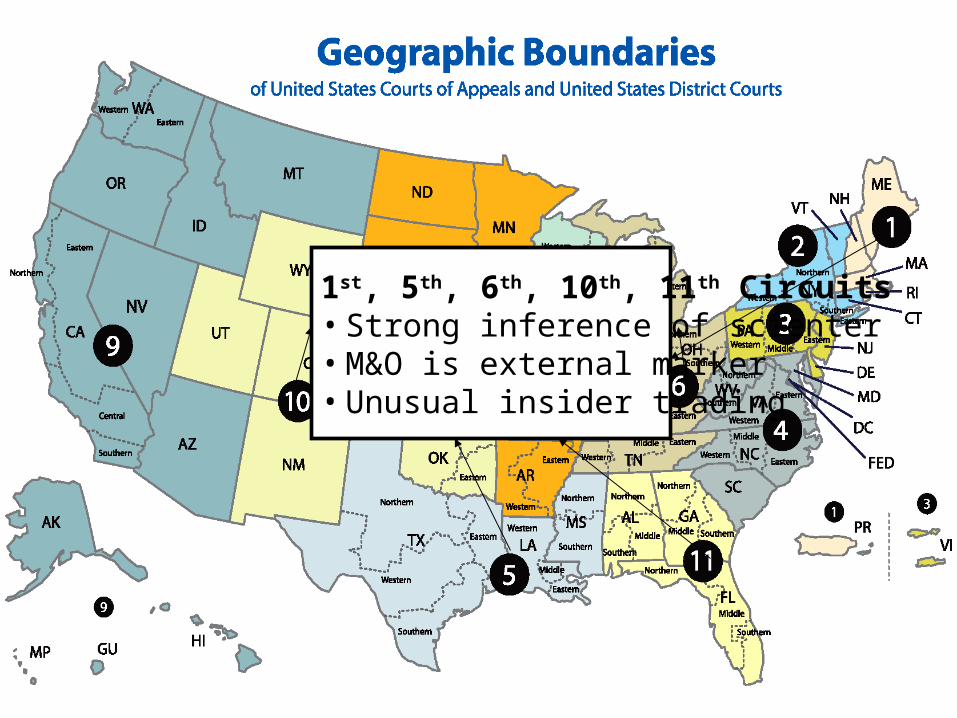

1st, 5th, 6th, 10th, 11th Circuits• Strong inference of scienter• M&O is external marker• Unusual insider trading

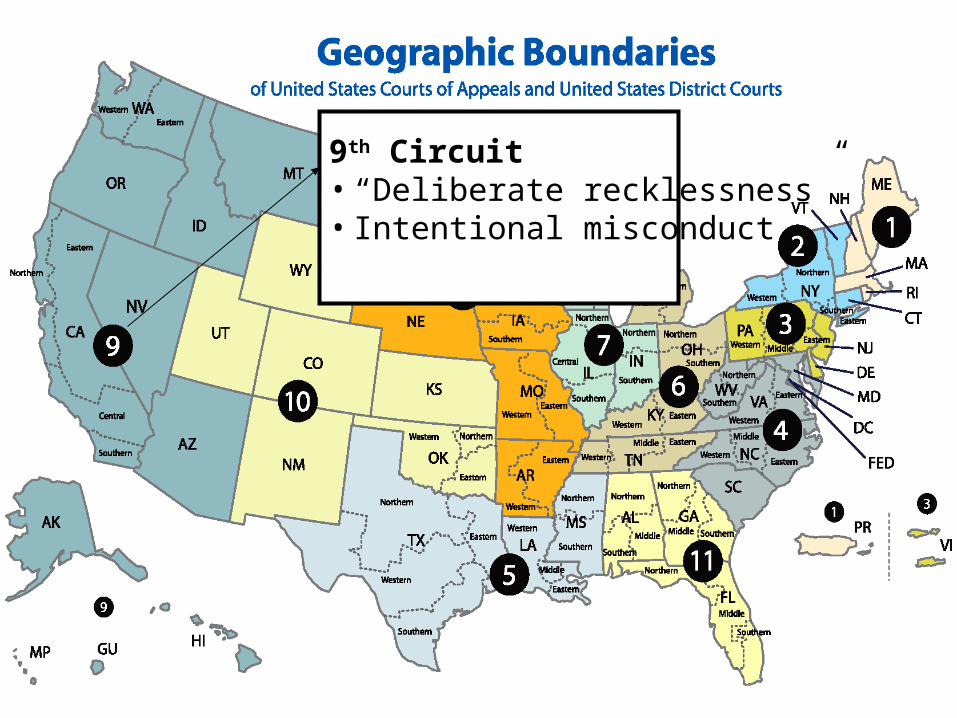

9th Circuit • “Deliberate recklessness”• Intentional misconduct

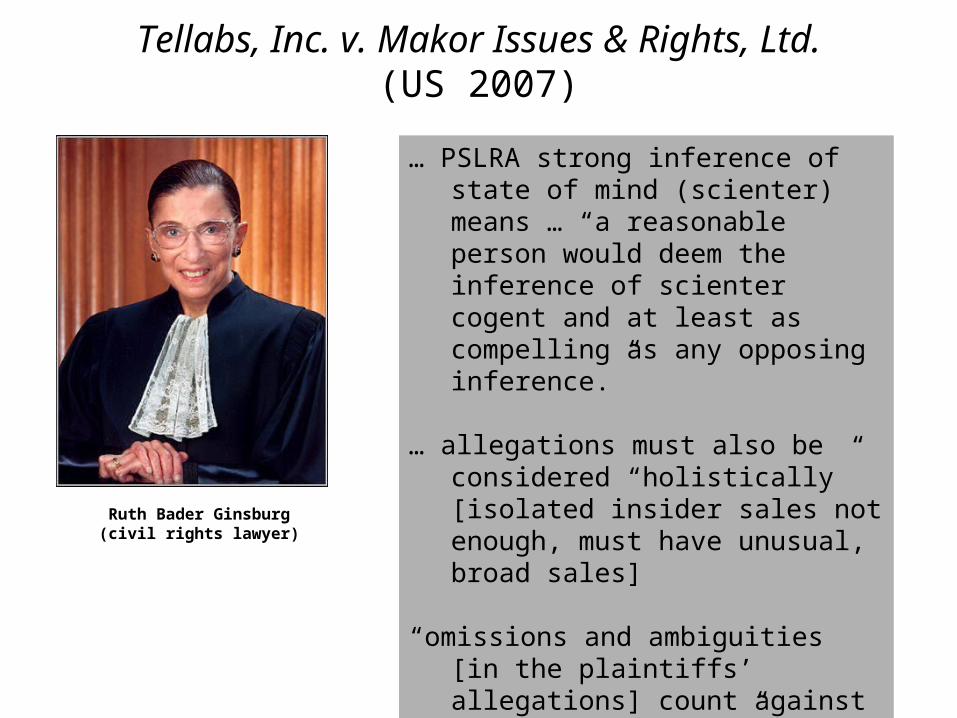

Tellabs, Inc. v. Makor Issues & Rights, Ltd.(US 2007)

Ruth Bader Ginsburg(civil rights lawyer)

… PSLRA strong inference of state of mind (scienter) means … “a reasonable person would deem the inference of scienter cogent and at least as compelling as any opposing inference.”

… allegations must also be considered “holistically” [isolated insider sales not enough, must have unusual, broad sales]

“omissions and ambiguities [in the plaintiffs’ allegations] count against inferring scienter” [discount confidential witnesses]

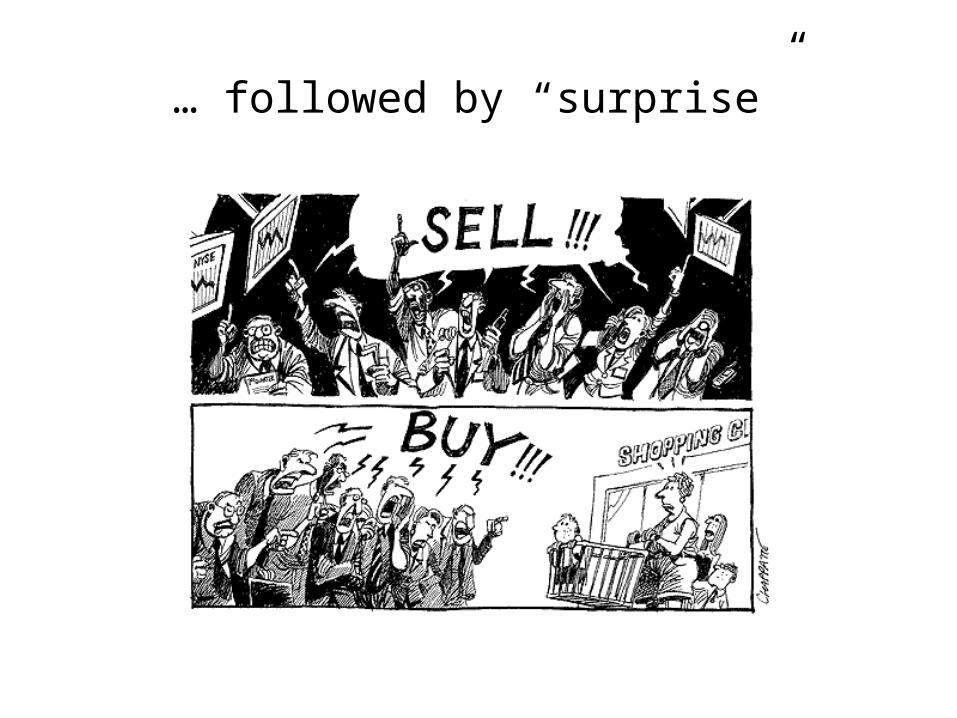

… followed by “surprise”

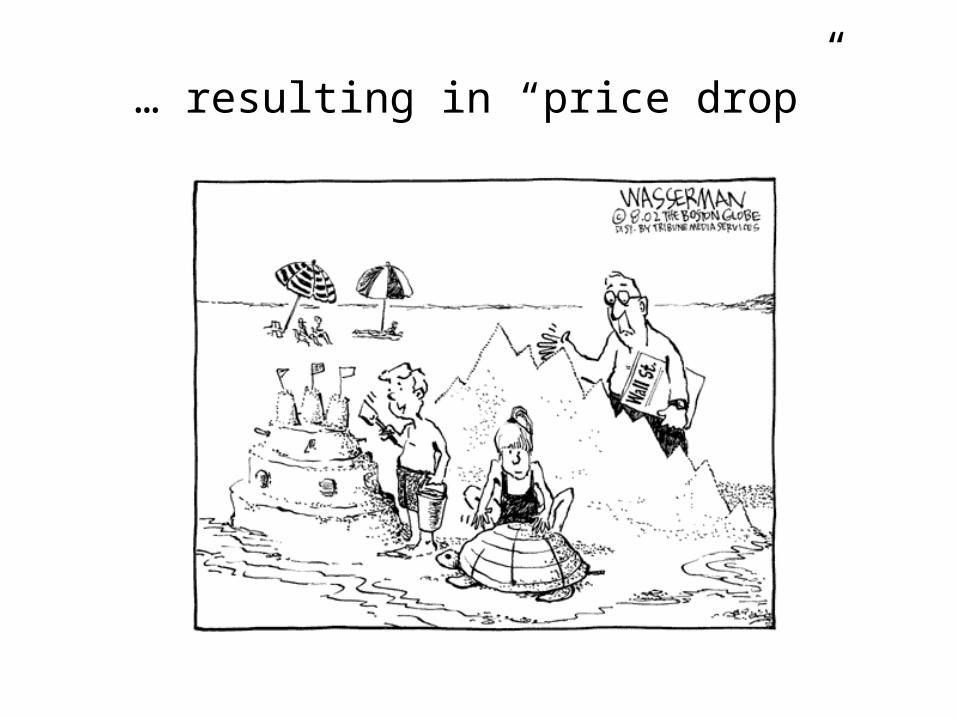

… resulting in “price drop”

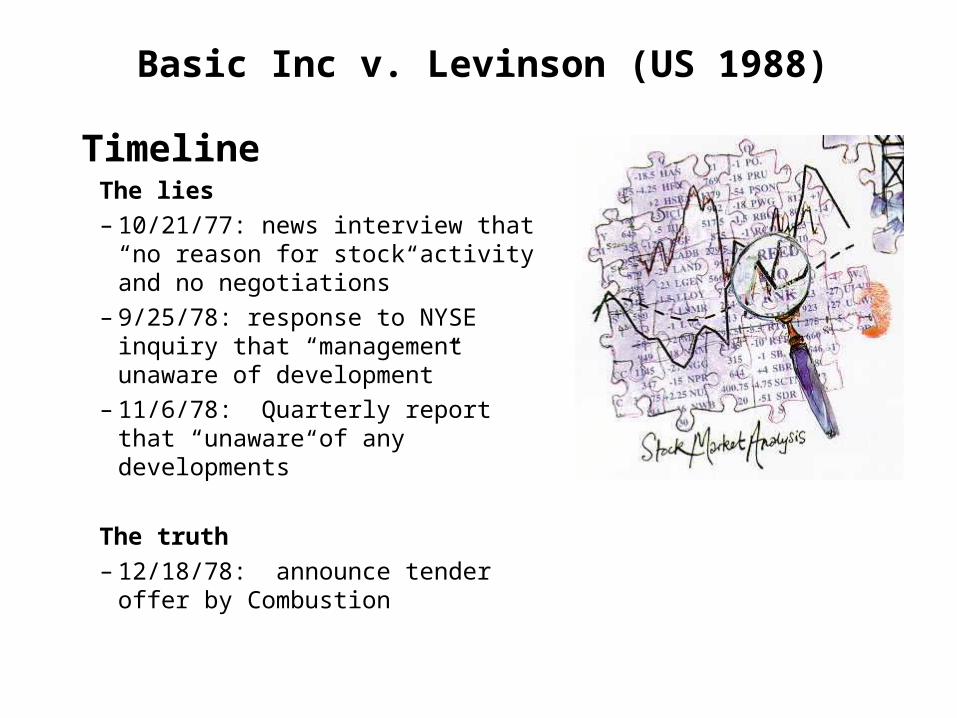

TimelineThe lies– 10/21/77: news interview that “no

reason for stock activity and no negotiations”

– 9/25/78: response to NYSE inquiry that “management unaware of development”

– 11/6/78: Quarterly report that “unaware of any developments”

The truth– 12/18/78: announce tender offer

by Combustion

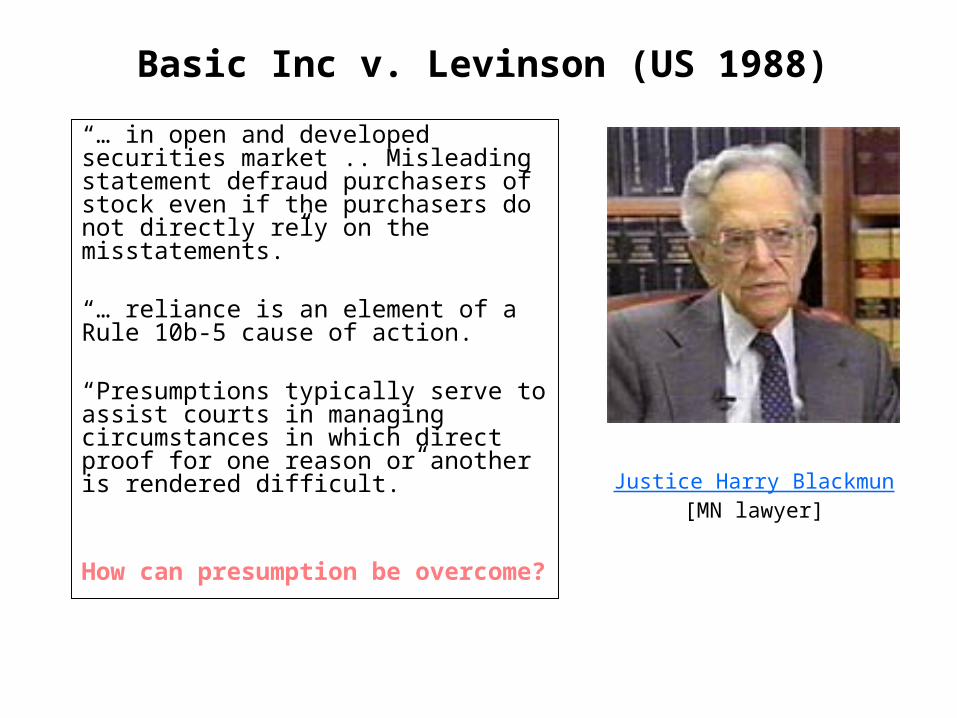

Basic Inc v. Levinson (US 1988)

Efficient Capital Market Hypothesis

“… in open and developed securities market .. Misleading statement defraud purchasers of stock even if the purchasers do not directly rely on the misstatements.”

“… reliance is an element of a Rule 10b-5 cause of action.

“Presumptions typically serve to assist courts in managing circumstances in which direct proof for one reason or another is rendered difficult.”

How can presumption be overcome?

Basic Inc v. Levinson (US 1988)

Justice Harry Blackmun[MN lawyer]

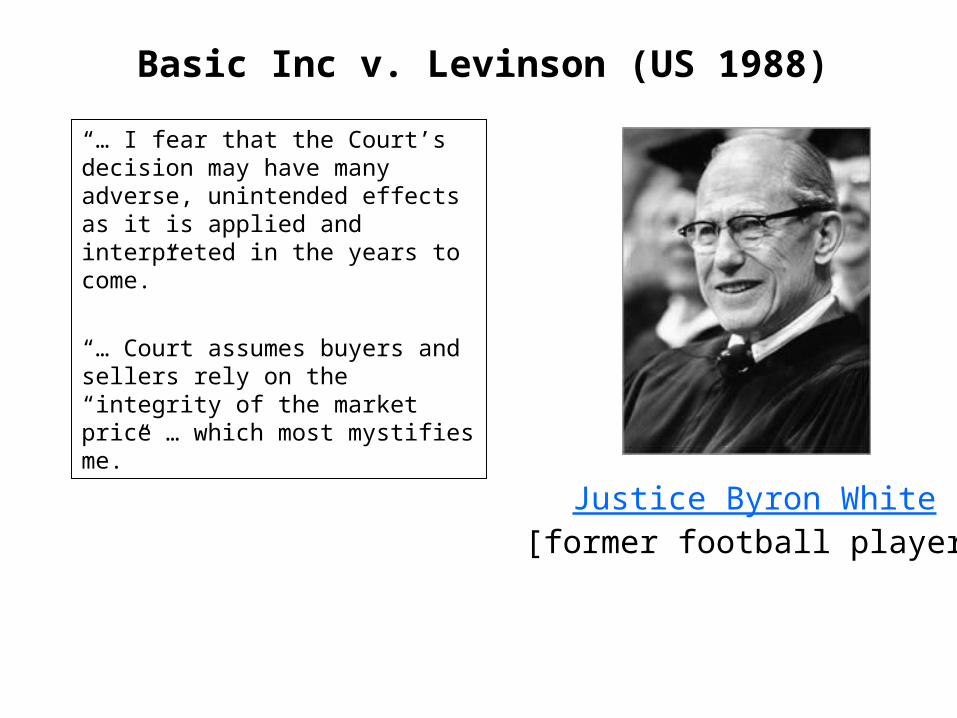

“… I fear that the Court’s decision may have many adverse, unintended effects as it is applied and interpreted in the years to come.”

“… Court assumes buyers and sellers rely on the “integrity of the market price … which most mystifies me.”

Basic Inc v. Levinson (US 1988)

Justice Byron White[former football player]

Big vs small companies

Big companies• Public disclosure• Many analysts• SEC investigation • Large damages

Small companies• Less publicized• Fewer analysts• No SEC interest• Smaller total damages

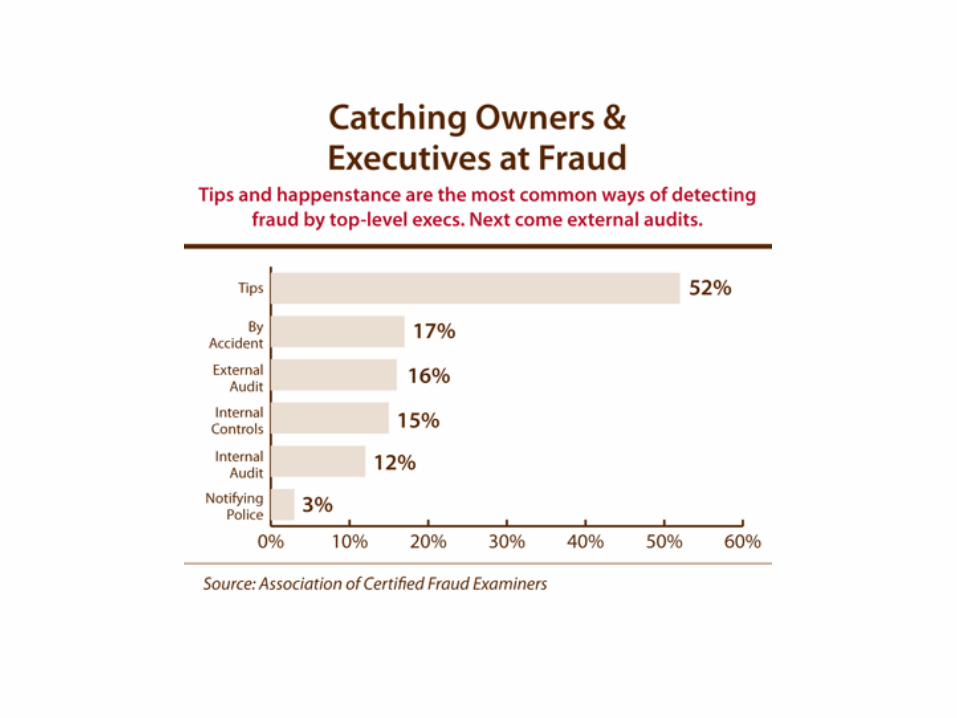

Identify “scienter” – such as …

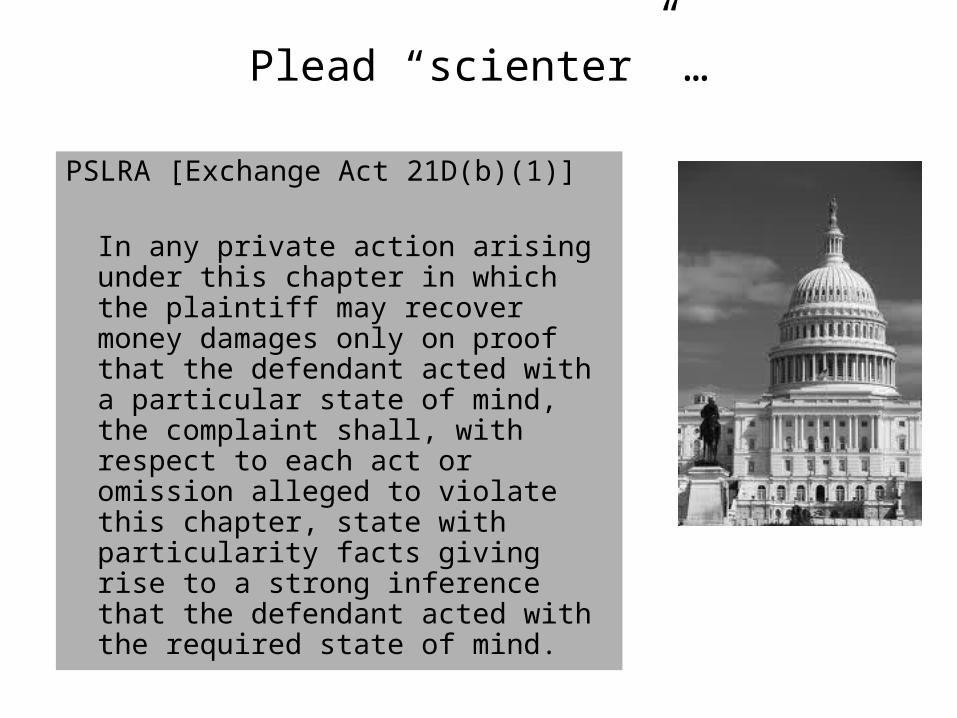

Plead “scienter” …

PSLRA [Exchange Act 21D(b)(1)]

In any private action arising under this chapter in which the plaintiff may recover money damages only on proof that the defendant acted with a particular state of mind, the complaint shall, with respect to each act or omission alleged to violate this chapter, state with particularity facts giving rise to a strong inference that the defendant acted with the required state of mind.

File a complaint

(e.g. Bay Networks, Inc)

Complaint must tell “fraud” story …

… to withstand “motion to dismiss”

If so, start settlement negotiations …

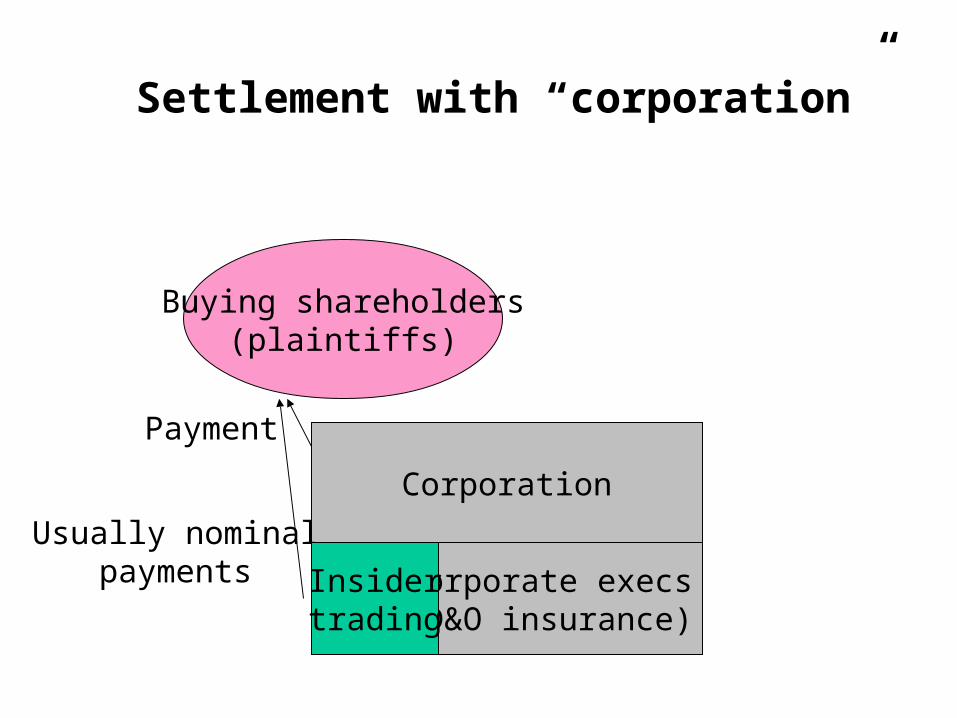

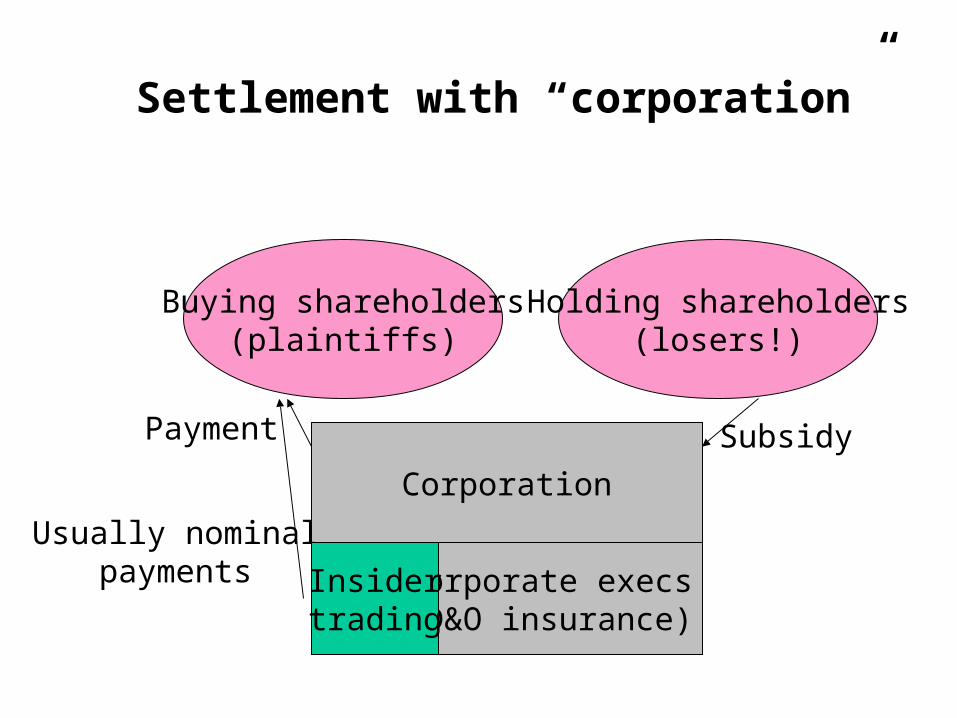

Settlement with “corporation”

Buying shareholders(plaintiffs)

Corporation

Payment

Corporate execs(D&O insurance)

Usually nominalpayments Insider

trading

Settlement with “corporation”

Buying shareholders(plaintiffs)

Holding shareholders(losers!)

Corporation

Payment Subsidy

Corporate execs(D&O insurance)

Usually nominalpayments Insider

trading

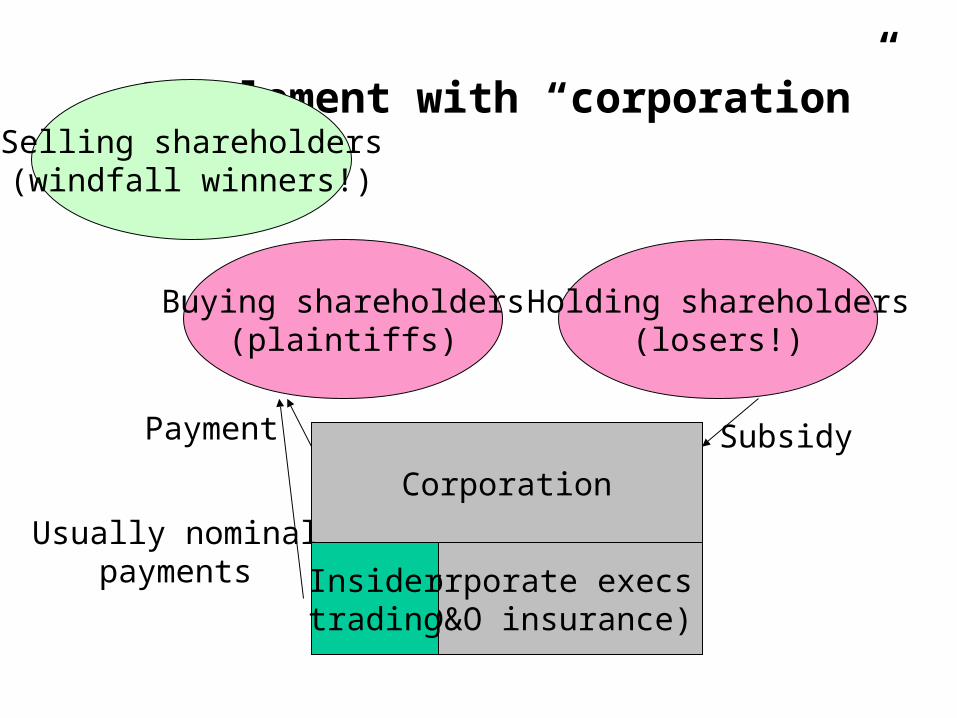

Settlement with “corporation”

Buying shareholders(plaintiffs)

Selling shareholders(windfall winners!)

Holding shareholders(losers!)

Corporation

Payment Subsidy

Corporate execs(D&O insurance)

Usually nominalpayments Insider

trading

"Index Funds and Securities Fraud Litigation"

(Booth)SFCA doesn’t make sense• Most investors are diversified • SFCA settlement : holders effectively pay buyers• Because of circularity: stock price declines on SFCA filingConsider index fund • almost always loses more than it gains when SFCA • index funds should oppose SFCA Capturing deterrent effect• w/o SFCA might be more securities fraud• Solution: corporation itself claim – against the individual wrongdoers • subject of a derivative action for the benefit of the corporation – and thus all

of the stockholders • constitute a significant deterrent to fraudProcedure• rules of civil procedure: derivative claim must be resolved before SFCA• No SFCA unless certified no other equally good way to litigate • Caveat: attorney fees are likely to be higher in class actions than in

derivative actions

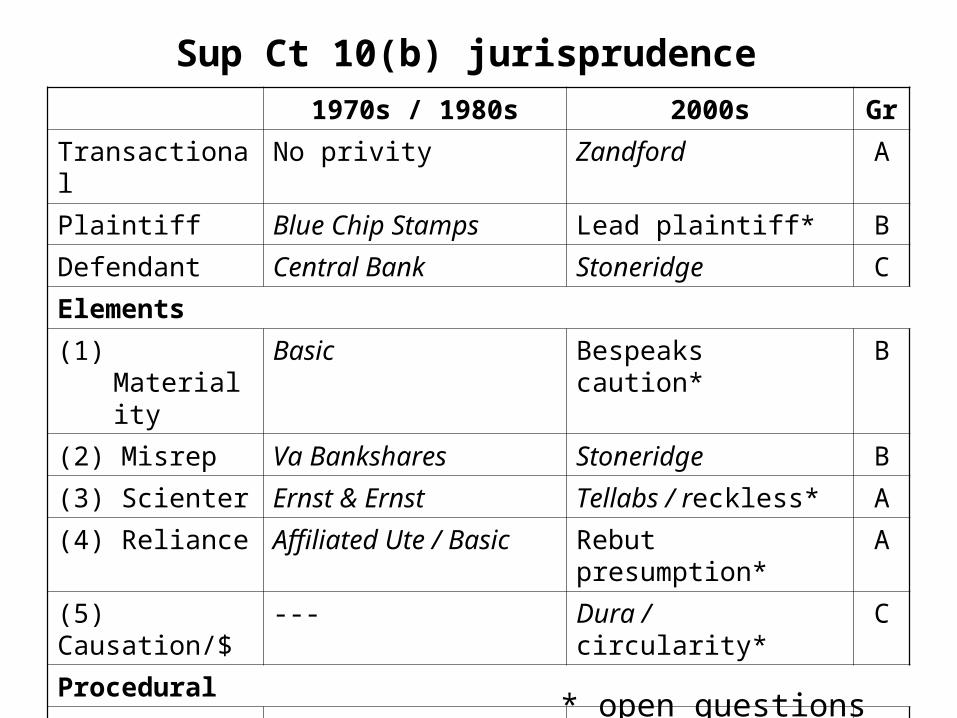

Sup Ct 10(b) jurisprudence 1970s / 1980s 2000s Gr

Transactional No privity Zandford A

Plaintiff Blue Chip Stamps Lead plaintiff* B

Defendant Central Bank Stoneridge C

Elements

(1) Materiality Basic Bespeaks caution* B

(2) Misrep Va Bankshares Stoneridge B

(3) Scienter Ernst & Ernst Tellabs / reckless* A

(4) Reliance Affiliated Ute / Basic Rebut presumption* A

(5) Causation/$ --- Dura / circularity* C

Procedural

(1) S/L Gilbertson / Huddleston SOX / Reynolds A

(2) Federal/state Santa Fe Dabit C

(3) Arbitration Shearson/Am Express FINRA / D-F* B

* open questions

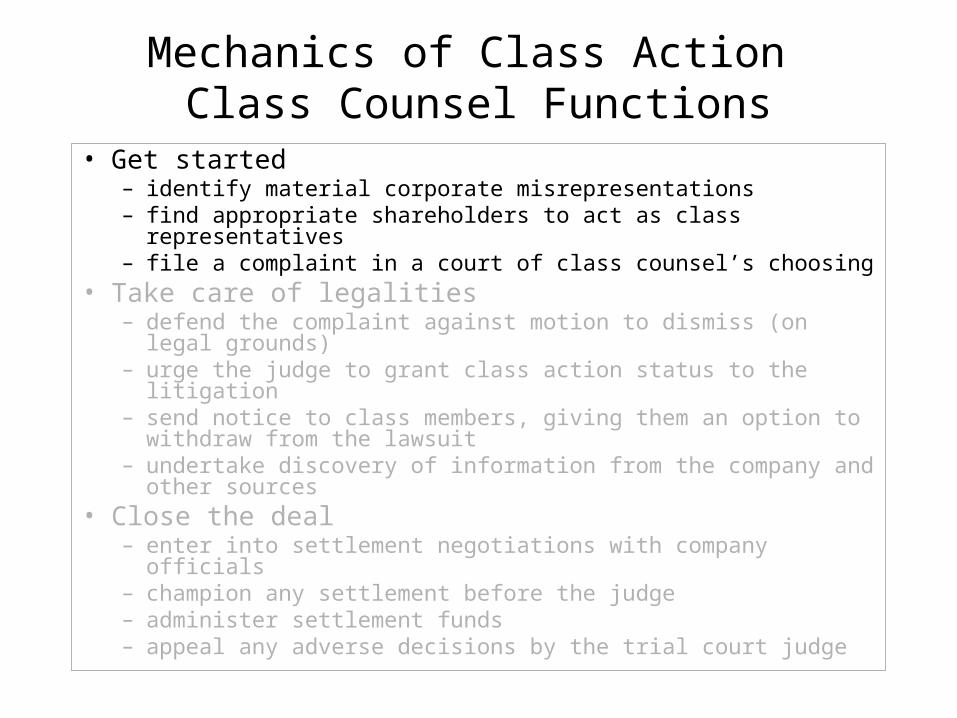

Mechanics of Class Action Class Counsel Functions

• Get started– identify material corporate misrepresentations– find appropriate shareholders to act as class

representatives– file a complaint in a court of class counsel’s choosing

• Take care of legalities– defend the complaint against motion to dismiss (on legal

grounds)– urge the judge to grant class action status to the litigation – send notice to class members, giving them an option to

withdraw from the lawsuit– undertake discovery of information from the company and

other sources• Close the deal

– enter into settlement negotiations with company officials – champion any settlement before the judge– administer settlement funds – appeal any adverse decisions by the trial court judge

Mechanics of Class Action Class Counsel Functions

• Get started– identify material corporate misrepresentations– find appropriate shareholders to act as class

representatives– file a complaint in a court of class counsel’s choosing

• Take care of legalities– defend the complaint against motion to dismiss (on legal

grounds)– urge the judge to grant class action status to the litigation – send notice to class members, giving them an option to

withdraw from the lawsuit– undertake discovery of information from the company and

other sources• Close the deal

– enter into settlement negotiations with company officials – champion any settlement before the judge– administer settlement funds – appeal any adverse decisions by the trial court judge

Mechanics of Class Action Class Counsel Functions

• Get started– identify material corporate misrepresentations– find appropriate shareholders to act as class

representatives– file a complaint in a court of class counsel’s choosing

• Take care of legalities– defend the complaint against motion to dismiss (on legal

grounds)– urge the judge to grant class action status to the litigation – send notice to class members, giving them an option to

withdraw from the lawsuit– undertake discovery of information from the company and

other sources• Close the deal

– enter into settlement negotiations with company officials – champion any settlement before the judge– administer settlement funds – appeal any adverse decisions by the trial court judge