section one: money chapter 10 money, banking & finance

TRANSCRIPT

Section One: Money

Chapter 10Money, Banking & Finance

Money

Three uses of money:Medium of exchange

Unit of account

Store of value

Medium of ExchangeAnything that is used to determine value

during the exchange of goods and services

In the past most societies used a barter systemA barter system is a direct exchange of

one set of goods or services for another.Money as a medium of exchange made

exchanging goods and services much easier.

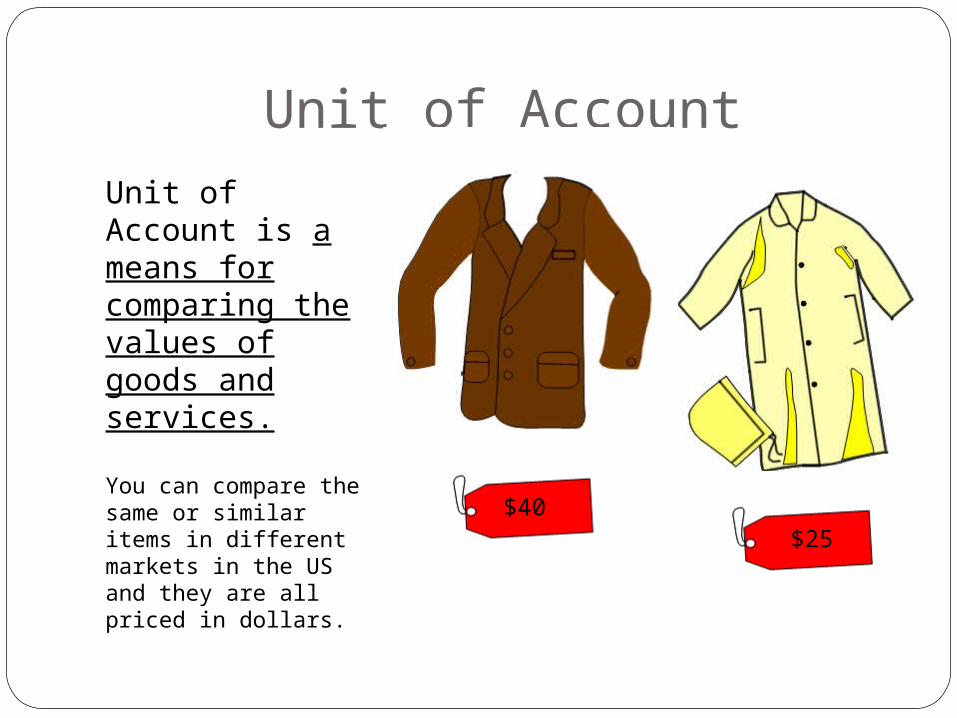

Unit of Account

Unit of Account is a means for comparing the values of goods and services.

You can compare the same or similar items in different markets in the US and they are all priced in dollars.

$40$25

Store of ValueSomething that keeps its value if it is stored rather than used.

This is true with money except in times of rapid inflation.

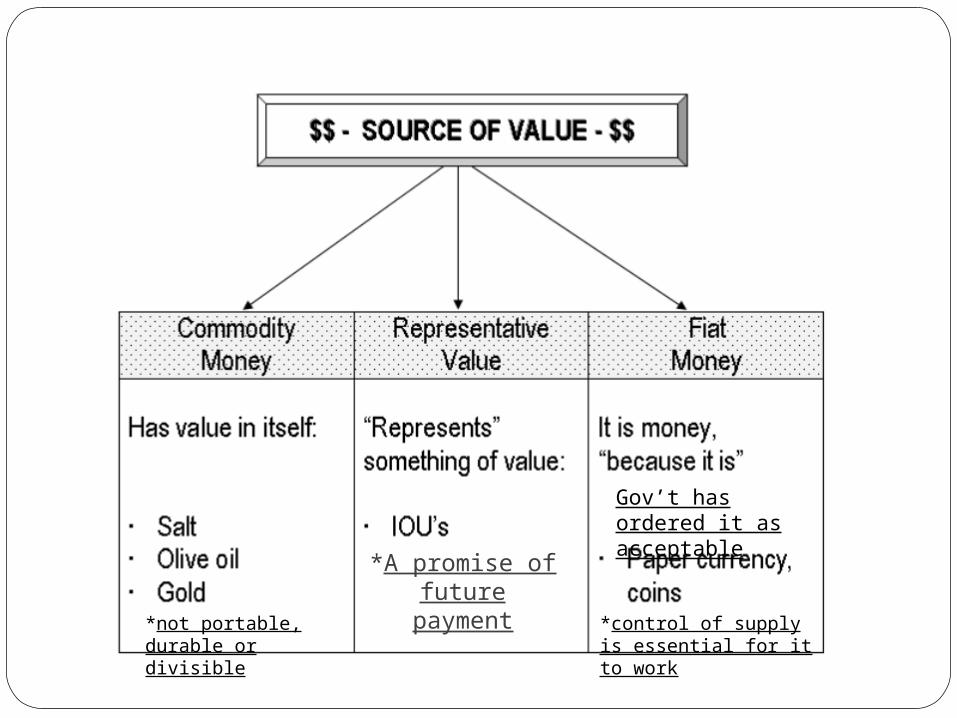

Six Characteristics of MoneyDurability: able to withstand wear and

tearPortability: easy to hold and transferDivisibility: easily divided into smaller

denominationsUniformity: all the same in terms of

what it will buyLimited supply: must be regulatedAcceptability: everyone in society must

accept it

*A promise of future payment

*not portable, durable or divisible

Gov’t has ordered it as acceptable

*control of supply is essential for it to work

Section Two

The History of American Banking

Bank: An institution for receiving, keeping and lending money.

Early on merchants would hold on to people’s money (keep it safe) for a fee. They would also extend loans to people.

Not a very good system; money was not always safe and merchants were not always honest.

Recap of American HistoryFederalists wanted a strong central

government to establish economic and social order.Alexander Hamilton believed a strong

centralized bank was needed for the US to develop healthy industries and trade.

Hamilton proposed a national bank to be chartered, or licensed by the National government.

He wanted one currency for the entire nation.The national bank would manage the federal

government’s funds and monitor other banks throughout the country.

Recap of American HistoryAnti- Federalists wanted most of

the power in the hands of the states.Thomas Jefferson wanted decentralized banks.

Individual states would establish and regulate the banks within their borders.

Recap of American HistoryFirst Bank of the US (1791 – 1811)

Had a license to operate for 20 yearsObjectives:

Hold government money (taxes)Help the government carry out its power to tax,

borrow money in public interest, regulate interstate and foreign commerce

Issue representative money in the form of bank notes (backed by gold and silver)

Regulate state- chartered banksOnce the Nation’s Bank Charter expired it

was shut down.States gave licenses to many banks without

considering whether they would be stable or even credit worthy.

Corruption and chaos ensued.

Recap of American HistorySecond Bank of the US

Another 20 years but charter not renewed.

Free Banking or “Wildcat” Era (1836 – 1863)Many problems arose:Bank runs: Widespread panic in which great

numbers of people try to redeem their paper money.Wildcat Banks: banks located on the edges of

settled areas often times failed.Fraud: Banks would collect gold and silver, issue

notes and then run.Different currencies: Each city/state had its own

currency. This made trade very hard and counterfeiting easy.

Recap of American HistoryThe Civil War made things worse…

The US Treasury issued “demand notes”, called “greenbacks”.

The South issued currency backed by cotton. By the end of the war, that currency became worthless.

Recap of American HistoryUnifying American Banks (1863

– 1864): Government reforms which gave the federal government three important powers:The power to charter banksThe power to require adequate gold and silver reserves

The power to issue a single national currency

Recap of American HistoryThe Gold Standard is a monetary

system in which paper money and coins are equal to the value of a certain amount of gold.

Two advantages:Set a definite value for the dollarThe government could issue currency only if it had gold in the treasury to back the notes

Recap of American HistoryAfter the Panic of 1907, the

government made plans to reinstate a central bank.

In 1913, the Federal Reserve System served as the nation’s first true central bank.

A central bank is a bank that can lend to other banks in times of need.

Recap of American HistoryThe central bank reorganized the federal

banking system as follows:It created twelve regional Federal Reserve

BanksMember banks: Banks that belong to the

Federal Reserve Banks.Federal Reserve Board: A supervisory

board appointed by the President of the US.Short- term loans: Regional Federal

Reserve Banks allowed members to borrow money to meet short term needs.

It established Federal Reserve Notes – the currency we use today.

Recap of American HistoryThe Great Depression: The severe

economic decline that began in 1929 and lasted for more than a decade.

Franklin D. Roosevelt created the FDIC.Federal Deposit Insurance

Corporation insures customer deposits if a bank fails.

Banks were highly regulated until the 1970’s and 1980’s. This deregulation paved the way for the next bank crisis.

The Savings and Loans CrisisThe causes of the Savings & Loans

Crisis:DeregulationHigh interest rates: Savings & Loans had to pay out high interest rates for depositors but were only charging low rates for loans given out earlier.

Bad loansFraud

Section Three

Banking Today

The Money SupplyThe money supply is all of the

money available in the US economy. This includes bills and coins,

traveler’s checks, checking account deposits, among others.

We track the money supply using TWO categories:M1M2

The Money Supply, cont.M1 represents money that people have

access to easily and immediately OR assets that have liquidity.Liquidity is the ability to be used as or

converted to cash.Examples:

Currency (almost 50%)Demand deposits (checking accounts)

(almost 50%)Traveler’s checks (almost 1%)

The Money Supply, cont.M2 includes all M1 and assets which cannot

be used as cash directly but can be easily converted.These assets are also called near money.Examples:

Savings account deposits (almost 40%)Small denomination time deposits (20%)Money market mutual funds (a fund that pools

money from small savers to purchase short term government and corporate securities) (20%)

M1 (22%)

Functions of Financial Institutions

Banks and other financial institutions offer many services:Store moneySave moneyLoansMortgagesCredit cards

Functions of Financial Institutions

Store money: safe, secure vaults

Saving money:Savings accounts low interest ratesChecking accounts

Money market accountsCertificates of deposits – higher interest

ratesset term (CDs)

Functions of Financial Institutions

Loans: loaning out people’s deposits to make a profitOld days – goldsmith / market

Stored money and then lent it out, keeping only a little in reserve.

Fractional reserve banking: a banking system that only keeps a fraction of deposits on hand.

If a borrower fails to pay back his loan, he is said to be in default.

Functions of Financial Institutions

Mortgages: Specific type of loan used to buy real estate.These loans are a major cause of the

situation we are in now.

Credit Cards: A card entitling its holder to buy goods and services based on the holder’s promise to pay for them.You use your card at a storeThe bank pays the storeOnce a month you pay back the bank for

your short- term loan

Functions of Financial Institutions

Credit Cards, cont.Banks charge interest: price paid for the use of borrowed money or principal.

Banks profit by charging more interest on their loans than the interest they pay on their deposits.

Types of Financial InstitutionsCommercial Banks:

most common; provide the most services; play the largest role in the economy.

Savings and Loans Associations (S & Ls):1800s for buying homesnow they are like commercial banks

Types of Financial InstitutionsSavings Banks: (Mutual Savings Banks in

1800s)Bank was owned by the depositors and they

shared profitsLater, they went public (stock offered)Now, shareholders earn the profit

Credit Unions: a cooperative lending association for a certain group.

Types of Financial Institutions

Finance Company:Make installment loans to consumers

Usually charge high interest rates because of the high level of default.

Electronic BankingAutomated Tellers Machines (ATMs):

Uses:Withdraw cashDeposit moneyTransfer from linked cashInformation

Debit Cards:Linked to a checking or saving accountMoney comes directly out of that account

when you purchase items

Electronic BankingHome-banking/Internet banking:

Further reducing bank costs and making it even more convenient for customers

Automatic Clearing Houses (ACHs):Allows customers to pay bills without writing

checksACH transfers funds automatically from

customers’ accounts to their creditors’ accounts.Usually used for monthly bills

Smart Cards:Similar to debit cards only they are prepaid Some can be “recharged”Some are linked with accounts for record keepingYou will probably be issued one at college