section 1 the origins of money. barter economy an economy with no money. an economy with no money....

TRANSCRIPT

Section 1Section 1

The Origins of MoneyThe Origins of Money

Barter EconomyBarter Economy

An economy with no money.An economy with no money. Based on trading one item for Based on trading one item for

another.another. What makes living in a barter What makes living in a barter

economy difficult is that many of the economy difficult is that many of the people you want to trade with don’t people you want to trade with don’t want to trade with you.want to trade with you.

Trade is time consuming.Trade is time consuming.

Transaction CostsTransaction Costs

High in a barter economy. The time High in a barter economy. The time and effort you have to spend before and effort you have to spend before you make an exchange. you make an exchange.

Time of discussing the transaction Time of discussing the transaction and making a deal. and making a deal.

Once people begin accepting a good Once people begin accepting a good because it reduces the transaction because it reduces the transaction costs of exchange, others will follow. costs of exchange, others will follow.

MoneyMoney

Any good that is Any good that is widely accepted in widely accepted in exchange and in the exchange and in the repayment of debts. repayment of debts.

Historically goods Historically goods that evolved into that evolved into money included money included gold, silver, copper, gold, silver, copper, rocks, cattle, and rocks, cattle, and shells. shells.

What Gives Money ValueWhat Gives Money Value

It is accepted. It is accepted. It has value to you because you know It has value to you because you know

that you can use it go get what you that you can use it go get what you want.want.

Means of exchangeMeans of exchange

Are you better off living in a Money Are you better off living in a Money Economy?Economy?

The transaction costs of exchange The transaction costs of exchange are lower in a money economy than are lower in a money economy than in a barter economy. in a barter economy.

In a money economy, then, people In a money economy, then, people produce more goods and services produce more goods and services and consume more leisure than they and consume more leisure than they would in a barter economy. would in a barter economy.

Three Functions of MoneyThree Functions of Money

1.1. Medium of exchange – anything that is Medium of exchange – anything that is generally acceptable in exchange for generally acceptable in exchange for goods and services. goods and services.

2.2. Unit of Account – common measurement Unit of Account – common measurement used to express value. Money functions used to express value. Money functions as a unit of account, which means that as a unit of account, which means that all goods can be expressed in terms of all goods can be expressed in terms of money. For example, we express the money. For example, we express the value of a house in terms of dollars. value of a house in terms of dollars.

3. Store of value – it maintains its 3. Store of value – it maintains its value over time. But does not mean value over time. But does not mean that it is always constant. that it is always constant.

Early Bankers: GoldsmithEarly Bankers: Goldsmith

The person most individuals turned to The person most individuals turned to was the goldsmith, someone who was was the goldsmith, someone who was already equipped with a safe storage already equipped with a safe storage facility. facility.

To acknowledge that they held deposited To acknowledge that they held deposited gold, goldsmiths issued warehouse gold, goldsmiths issued warehouse receipts to their customers.receipts to their customers.

The receipts simply represented or stood The receipts simply represented or stood in place of, the actual gold in storage. in place of, the actual gold in storage.

Some goldsmiths did lend out some Some goldsmiths did lend out some of the gold deposited with them and of the gold deposited with them and collected the interest on the loans. collected the interest on the loans.

Fractional reserve banking – create Fractional reserve banking – create money by holding on reserve only a money by holding on reserve only a fraction of the money deposited and fraction of the money deposited and lending the remainder. lending the remainder.

Section 2Section 2

The Money SupplyThe Money Supply

Components of the Money Supply Components of the Money Supply M1M1

1.1. Currency – includes both coins minted by Currency – includes both coins minted by the U.S. Treasury and paper money. The the U.S. Treasury and paper money. The paper money in circulation consists of paper money in circulation consists of Federal Reserve notes. Federal Reserve notes.

2.2. Checking Accounts – Accounts in which Checking Accounts – Accounts in which funds are deposited and can be funds are deposited and can be withdrawn simply by writing a check. withdrawn simply by writing a check. Sometimes checking accounts are Sometimes checking accounts are referred to as demand deposits because referred to as demand deposits because the funds can be converted to currency the funds can be converted to currency on demand and given to the person to on demand and given to the person to whom the check is made payable. whom the check is made payable.

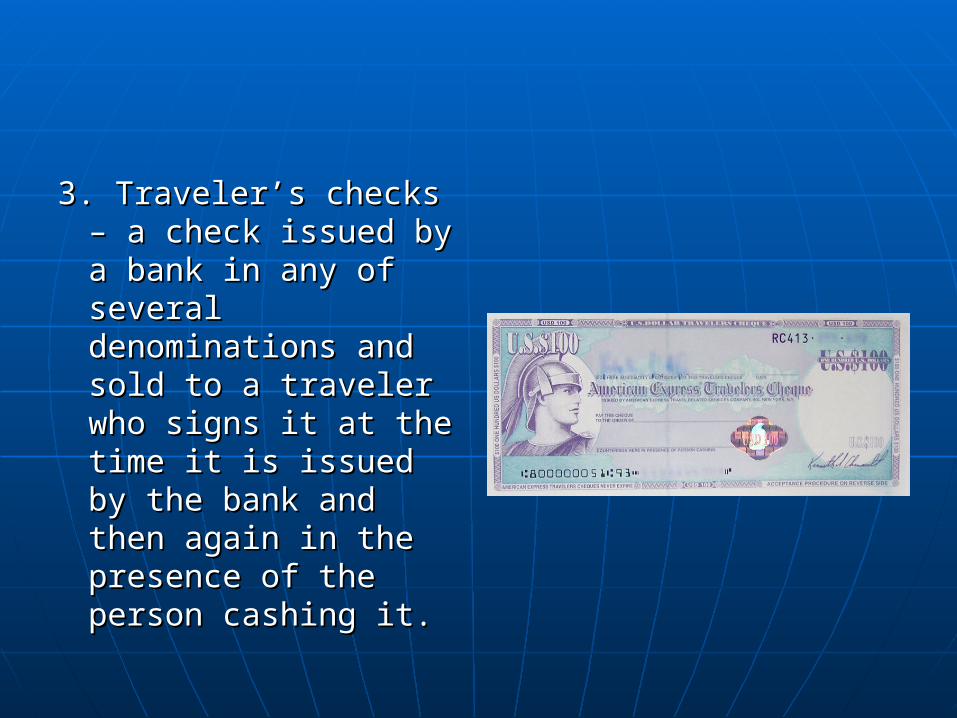

3. Traveler’s checks – a 3. Traveler’s checks – a check issued by a check issued by a bank in any of several bank in any of several denominations and denominations and sold to a traveler who sold to a traveler who signs it at the time it signs it at the time it is issued by the bank is issued by the bank and then again in the and then again in the presence of the presence of the person cashing it. person cashing it.

M2M2

Broader measure including Broader measure including everything in M1 plus savings everything in M1 plus savings deposits, small-denomination time deposits, small-denomination time deposits, money market deposit deposits, money market deposit accounts, and retail money market accounts, and retail money market mutual fund accounts. mutual fund accounts.

Savings Account – interest-earning Savings Account – interest-earning account at a commercial bank.account at a commercial bank.

Time deposits – an interest-earning Time deposits – an interest-earning deposit with a specified maturity deposit with a specified maturity date. (CD)date. (CD)

Money market deposit account – an Money market deposit account – an interest-earning account at bank. interest-earning account at bank. (kind of short term investment)(kind of short term investment)

Money market mutual fund – same Money market mutual fund – same as deposit account but with a mutual as deposit account but with a mutual fund.fund.

A mutual fund is an investment in a A mutual fund is an investment in a fund that represents like companies fund that represents like companies (cereals, technology) Usually for a (cereals, technology) Usually for a longer term. longer term.

Are Credit Cards money?Are Credit Cards money?

No.No. It is a debt that you incur. It is a debt that you incur. You a not giving money over at exact You a not giving money over at exact

time of purchase. time of purchase. It is an instrument that makes it It is an instrument that makes it

easier for the holder to obtain a loan. easier for the holder to obtain a loan. It is a piece of plastic that allows you It is a piece of plastic that allows you

to take out a loan from the bank that to take out a loan from the bank that issued the card. issued the card.

Borrowing, Lending, and Interest Borrowing, Lending, and Interest RatesRates

Interest rates are determined in the Interest rates are determined in the loanable funds market. loanable funds market.

The loanable funds market includes a The loanable funds market includes a demand for loans and a supply of demand for loans and a supply of loans. The demanders of loans are loans. The demanders of loans are called borrowers, the suppliers of called borrowers, the suppliers of loans are called lenders. loans are called lenders.

Based on the economy – determined Based on the economy – determined by the Fed.by the Fed.

Section 3Section 3

The Federal Reserve SystemThe Federal Reserve System

Federal Reserve SystemFederal Reserve System

Created in 1913 by the Federal Reserve Created in 1913 by the Federal Reserve Act.Act.

Started operation in 1914.Started operation in 1914. A central bank, which means it is the chief A central bank, which means it is the chief

monetary authority in the country. monetary authority in the country. Determining the money supply and Determining the money supply and

supervising banks, among other things. supervising banks, among other things. Consist of the Board of Governors and the Consist of the Board of Governors and the

12 Federal Reserve district banks. 12 Federal Reserve district banks.

Board of GovernorsBoard of Governors

Controls and coordinates the Fed’s Controls and coordinates the Fed’s activities. activities.

Made up of 7 members, each Made up of 7 members, each appointed to a 14-year term by the appointed to a 14-year term by the president with senate approval. president with senate approval.

The president also designates one The president also designates one member as chairperson of the board member as chairperson of the board for a 4-year term. for a 4-year term.

District BanksDistrict Banks

12 Districts12 Districts

What does the Fed do?What does the Fed do?

1.1. Controls the money supply.Controls the money supply.

2.2. Supply the economy with paper Supply the economy with paper money – the pieces of paper money money – the pieces of paper money we use are Federal Reserve notes. we use are Federal Reserve notes. Federal Reserve notes are printed Federal Reserve notes are printed at the Bureau of Engraving and at the Bureau of Engraving and Printing. Printing.

3. Hold bank reserves – Each 3. Hold bank reserves – Each commercial bank that is a member of commercial bank that is a member of the Federal Reserve System is the Federal Reserve System is required to keep a reserve account required to keep a reserve account (based on total of accounts on hand).(based on total of accounts on hand).

4. Provide check-clearing services. The 4. Provide check-clearing services. The numbers on the bottom of the check. numbers on the bottom of the check.

5. Supervise member banks – without 5. Supervise member banks – without warning the Fed can examine the warning the Fed can examine the books of member commercial banks books of member commercial banks to see what kind of loans they made, to see what kind of loans they made, whether they followed bank whether they followed bank regulations. Audit. regulations. Audit.

6. Serve as the lender of last resort – 6. Serve as the lender of last resort – for banks suffering cash for banks suffering cash management problems. Bail outmanagement problems. Bail out

Section 4Section 4

The Money Creation ProcessThe Money Creation Process

Total ReservesTotal Reserves

Total Reserves = Deposits in the Total Reserves = Deposits in the reserve account at the Fed + Vault reserve account at the Fed + Vault cashcash

Deposits in the reserve account = $10 Deposits in the reserve account = $10 milmil

Vault cash = $15 milVault cash = $15 mil

Total reserves = $25 mil Total reserves = $25 mil

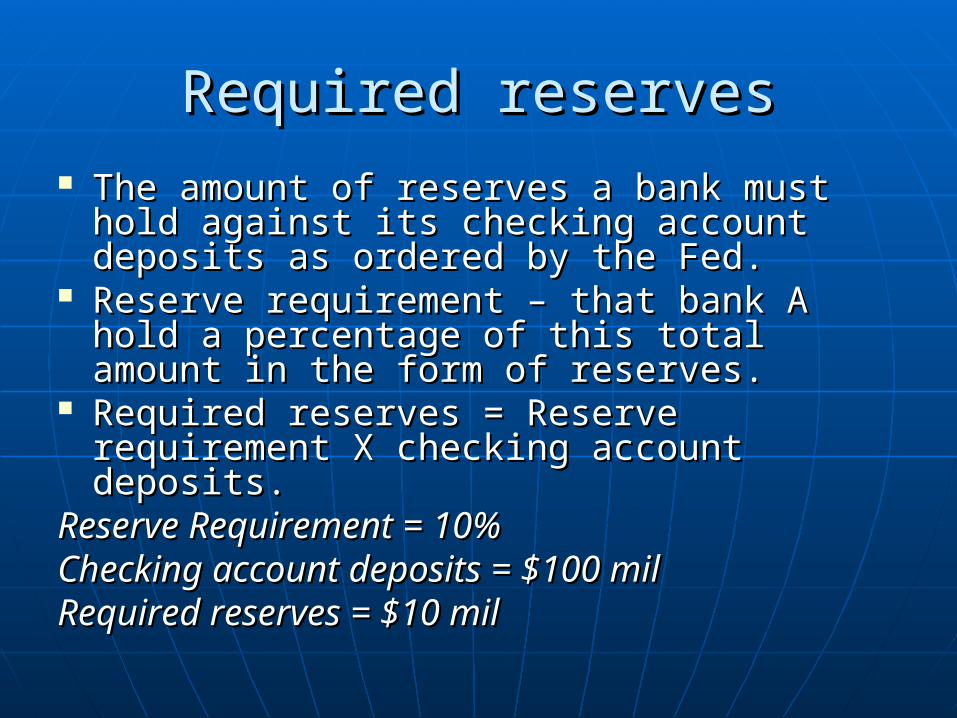

Required reservesRequired reserves The amount of reserves a bank must hold The amount of reserves a bank must hold

against its checking account deposits as against its checking account deposits as ordered by the Fed. ordered by the Fed.

Reserve requirement – that bank A hold a Reserve requirement – that bank A hold a percentage of this total amount in the percentage of this total amount in the form of reserves. form of reserves.

Required reserves = Reserve requirement Required reserves = Reserve requirement X checking account deposits.X checking account deposits.

Reserve Requirement = 10%Reserve Requirement = 10%Checking account deposits = $100 milChecking account deposits = $100 milRequired reserves = $10 milRequired reserves = $10 mil

Excess reservesExcess reserves

The difference between total The difference between total reserves and required reserves.reserves and required reserves.

Excess reserves = Total reserves – Excess reserves = Total reserves – required reservesrequired reserves

Total reserves = $25 milTotal reserves = $25 mil

Required reserves = $10 milRequired reserves = $10 mil

Excess reserves = $15 mil Excess reserves = $15 mil

The bank can create new loans with The bank can create new loans with excess reserves. excess reserves.