sect. 263a: allocating direct and indirect...

TRANSCRIPT

Presenting a live 110‐minute teleconference with interactive Q&A

Sect 263A: Allocating Direct and Indirect CostsSect. 263A: Allocating Direct and Indirect CostsMastering Established and Evolving Regs, Guidance and Rulings

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, DECEMBER 20, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Michael Lueck Director Washington National Tax Practice KPMG Washington D CMichael Lueck, Director, Washington National Tax Practice, KPMG, Washington, D.C.

Kari Peterson, Tax Manager, RSM McGladrey, Minneapolis

Donald A. Barnes, Principal, Law Offices of Donald A. Barnes, PLLC, Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442 and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

S t 6 A All ti Di t d Sect. 263A: Allocating Direct and Indirect Costs Seminar

Dec. 20, 2011

Kari Peterson, RSM [email protected]

Michael Lueck, [email protected]

Donald A. Barnes, Law Offices of Donald A.Barnes, [email protected]

Today’s Program

Fundamental Sect. 263A Concepts[Michael Lueck and Kari Peterson]

Slide 7 – Slide 30

Relevant Sect. 263A Guidance[Michael Lueck and Kari Peterson]

Slide 31 – Slide 47

Ongoing Compliance Challenges Under Sect. 263A[Donald A. Barnes]

Slide 48 – Slide 58

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OFCLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any p y g ytax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be j g pp y pdetermined through consultation with your tax adviser.

© 2011 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG and the KPMG logo are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity.

Mi h l L k KPMG

FUNDAMENTAL SECT 263A

Michael Lueck, KPMGKari Peterson, RSM McGladrey

FUNDAMENTAL SECT. 263A CONCEPTS

Sect. 263A – Inventory AnalysisGeneral Introduction

Why care now?y- IRS audit approach is changing.- Opportunity to manage risk or reduce capitalizable costs- Mixed service costs are a Tier I issue- Mixed service costs are a Tier I issue

What does it apply to?- Produced inventory- Purchased inventory- Self-constructed assets

9

Sect. 263A – Computational Steps

Step 1p- Identify inventory costs reflected on financial statements

(full absorption)

Step 2- Identify additional Sect. 263A inventoriable costs

Step 3- Allocate inventory costs between ending inventory and

cost of goods sold

10

Step 1 – Understand FullAbsorption Inventory Methodp y

Required prior to enactment of Sect. 263Aq p

Sect. 471 costs (key term)- Direct production costs- Direct production costs- Indirect production costs

• Category 1: Always capitalized• Category 2: Not capitalized• Category 3: Possibly capitalized but generally related

to production activities

11

Step 1 – Full Absorption Indirect Cost Allocation Methods

Burden rate- Objective → Allocate appropriate amount of indirect

production costs to ending inventory- Operation → Use pre-determined rates to approximateOperation → Use pre determined rates to approximate

costs- Adjustment → Variances, if material, adjust ending

inventoryinventory

Standard costR i ll ti f t iti ti h d- Requires allocation of net positive or negative overhead variance to ending inventory

- Standard/budgeted costs used to approximate costs

12

Step 2 – Identify And Allocate Additional Sect. 263A Costs

Regulations identify 23 types of indirect production costs.g y yp p- Allocable share of administrative, service or support

functions Determine what costs are already capitalized under taxpayer’sDetermine what costs are already capitalized under taxpayer s

full absorption method.- Regulations do not really address how this should be

accomplishedaccomplished.- Sect. 471 costs may include some of these costs.

ApproachesA t b t l i- Account-by-account analysis

- Department analysis

13

Step 2 – Additional Sect. 263A Indirect Production Costs

Indirect labor Officer’s compensation

Depletion Rentp

Pension and other related costs Employee benefits Indirect materials

Taxes (other than income) Insurance Utilities Indirect materials

Purchasing costs Handling costs

Utilities Repairs and maintenance Engineering and design

( S t 174 t ) Storage costs Cost recovery Quality control

(non-Sect. 174 costs) Spoilage Tools and equipmenty

Interest (only if Sect. 263A(f) applies)

Bidding costs (successful bids)

Licensing and franchise costs

Capitalizable service costs

14

Bidding costs (successful bids) p

Step 2 – Costs Not Capitalized

Selling and distribution costs

Sect 174 costs

Income taxes Strike costs Warranty costsSect. 174 costs

Sect. 179 expenses Sect. 165 losses C t f idl

Warranty costs On-site storage costs at

retail store facility U f l bid Cost recovery of idle

assets Unsuccessful bids Deductible service costs

(see next slide)

15

Step 2 – Deductible Service Costs

Overall management or Insurance or risk gpolicy-setting

Strategic business planning General financial accounting

management policy Environmental

management policyGeneral financial accounting General financial planning

and management Personnel policy

g p y General economic

analysis and forecasting Internal audit Personnel policy

Quality control policy Safety engineering policy

Internal audit Shareholder, public and

industrial relations Tax services Tax services Marketing, selling or

advertising

16

Step 2 – Allocating Costs Among Departmentsg p

Specific identification methodp Allocation methods

- Burden rate- Standard cost method- Standard cost method- Significant variances capitalized to ending inventory

Any other reasonable method- Total costs capitalized not significantly different from other

methods- Applied consistently- Does not circumvent Sect. 263A requirements- Allocates costs to specific items in inventory (TAM

9717002)

17

)

Step 2 – Allocating Costs Of Mixed Service Departmentsp

Mixed service costs- Partially allocable to production or capitalizable resale

activities and partially allocable to deductible activitiesactivities, and partially allocable to deductible activities• Accounting• Payroll

HR• HR• IT• Legal

18

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

Concept of allocationsp- Manufacturer has two divisions and a personnel

department that serves both divisions.- Personnel department has $50 000 of costsPersonnel department has $50,000 of costs.- Division 1 has 40 employees; 30 are in non-production

activities.- Division 2 has 60 employees; 40 are in non production- Division 2 has 60 employees; 40 are in non-production

activities.- How much of the personnel department costs are actually

inventoriable?inventoriable?

19

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

Self-developed method- Categorize costs of mixed service department

• Entirely production• Entirely production• Entirely non-production• Partially related to production and non-production

20

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

Direct reallocation- Total costs of all mixed service departments are allocated

to production departments.- Ignores benefits of service departments servicing oneIgnores benefits of service departments servicing one

another- Use this method when you want to maximize taxable

incomeincome.

21

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

Step-allocationp- Sequence of allocations- Begin with service department benefiting the most other

departmentsdepartments- Allocate costs to:

• Manufacturing operationsOth i d t t• Other service departments

• Non-service departments (financial planning, tax department) benefiting only non-production activities

22

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

Elective 90-10 de minimis rule- Treas. Reg. 1.263A-1(g)(4)(ii)

• 90% or more of MSD costs deductible; 100% are period costsperiod costs

• 90% or more of MSD costs capitalizable; 100% are inventoriable

• Constitutes a method of accounting• Constitutes a method of accounting• Applies to all mixed service departments

23

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

Simplified service cost methodp- Applies to all inventory- At election, certain self-constructed assets may be

excludedexcluded- Applies to all activities of the trade or business- Formula

All ti ti t t l i d i t• Allocation ratio x total mixed service costs– Total MSCs means total department costs.– Risk/exposure if SSCM ratio applied to less than

total department costs

24

Step 2 – Allocating Costs Of Mixed Service Departments (Cont.)p ( )

- Allocation ratio• Production cost allocation ratio

– Total production costs/total costs, less mixed service costs and interest

• Labor cost allocation ratio– Manufacturer

o Total production labor costs/total labor costs, less mixed service labor

R ll– Resellero Total purchasing labor costs/total labor costs, less

mixed service laborTotal storage and handling labor costs/total laboro Total storage and handling labor costs/total labor costs, less mixed service labor

– 1/3 – 2/3 ruleo Election method of accounting

25

o Election, method of accounting

Step 3 – Allocating Additional Sect. 263A Costs To Inventoryy

Self-developedp- Specific identification- Burden rates- Standard cost- Standard cost- Do not confuse these with methods previously discussed.

Simplified- With or without historic absorption ratio

26

Step 3 – Allocating Additional Sect. 263A Costs To Inventory (Cont.)263A Costs To Inventory (Cont.)

Simplified production or resale method (without HAR election)p p ( )- Step 1 – Compute absorption ratio

• Total additional Sect. 263A costs (except interest) / total Sect 471 coststotal Sect. 471 costs– Split absorption ratio, if a reseller

o Purchasing costs ratioSt d h dli t tio Storage and handling costs ratio

- Step 2 – Use absorption ratio to allocate costs to ending inventory• Absorption ratio x ending FIFO inventory (or LIFO

increment)

27

Step 3 – Allocating Additional Sect. 263A Costs To Inventory (Cont.)263A Costs To Inventory (Cont.)

Simplified production method, without historic absorptionhistoric absorption

28

Step 3 – Allocating Additional Sect. 263A Costs To Inventory (Cont.)263A Costs To Inventory (Cont.)

Simplified resale method, without historic absorption (Cont )absorption (Cont.)

Purchasing Storage and Combined Purchasing Absorption

Ratio+

Storage and Handling

Absorption RatioAbsorption

Ratio=

Ending FIFO Inventory Combined x or (LIFO increment)Absorption Ratio x

29

Step 3 – Allocating Additional Sect. 263A Costs To Inventory (Cont.)263A Costs To Inventory (Cont.)

Simplified production or resale method (with HAR election)p p ( )- Steps are the same as without historic absorption ratio.- Absorption ratio is set based upon prior three years’ use of

simplified production methodsimplified production method.- Advantage of HAR

• Simplicity, as Sect. 263A calculation need only be completed once over the qualifying period (five years)completed once over the qualifying period (five years)

- Disadvantage• Must be used over the qualifying period, even if

ti hoperations change

30

Mi h l L k KPMG

RELEVANT SECT 263A

Michael Lueck, KPMGKari Peterson, RSM McGladrey

RELEVANT SECT. 263A GUIDANCE

Sales-Based Royalties In general, royalty payments are required to be capitalized to

the extent properly allocable to property produced or acquired for resale Treas Reg 1 263A 1(e)(3)(ii)(U)for resale. Treas. Reg. 1.263A-1(e)(3)(ii)(U)

Sales-based royalties

- Plastic Engineering & Technical Services, Inc. v. Comm’r, T.C. Memo 2001-324

- Robinson-Knife Manufacturing Co. v. Comm’r, 600 F.3d 121 (2nd Cir. 2010)

Facts-and-circumstances v. simplified methods of allocating costs between ending inventory and cost of goods sold

32

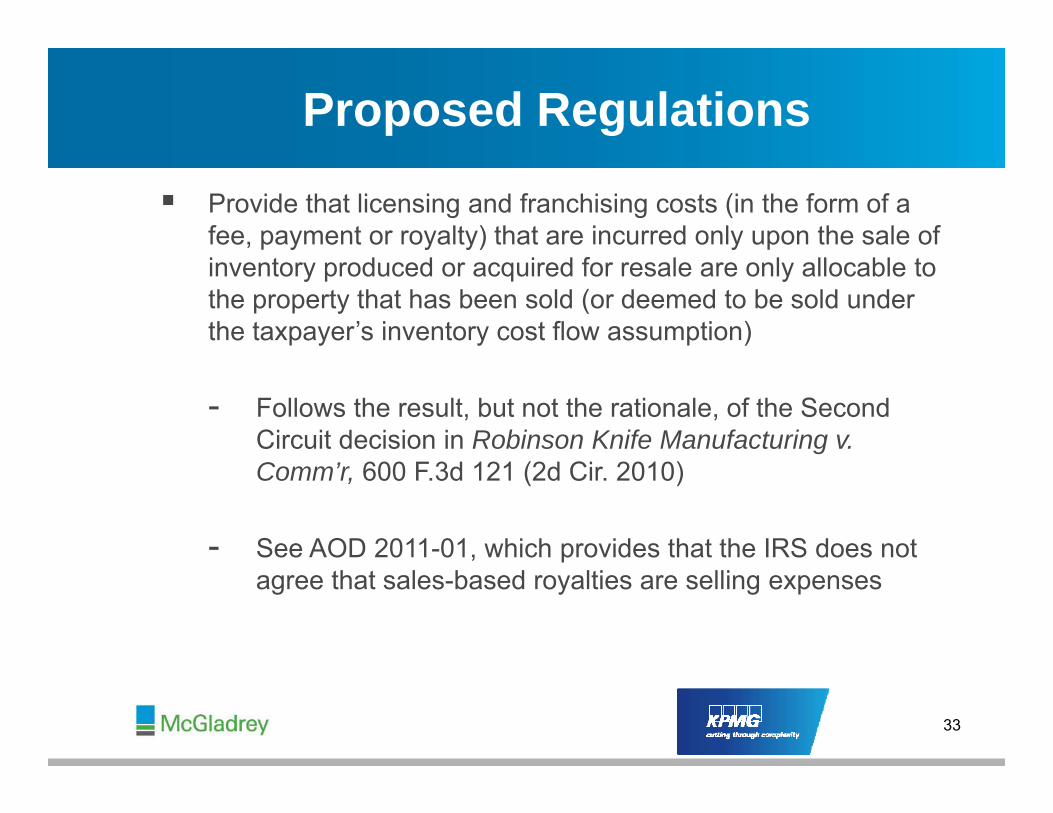

Proposed Regulations

Provide that licensing and franchising costs (in the form of a fee, payment or royalty) that are incurred only upon the sale of inventory produced or acquired for resale are only allocable to the property that has been sold (or deemed to be sold under the taxpayer’s inventory cost flow assumption)

- Follows the result, but not the rationale, of the Second Circuit decision in Robinson Knife Manufacturing v. Comm’r, 600 F.3d 121 (2d Cir. 2010)

- See AOD 2011-01, which provides that the IRS does not , pagree that sales-based royalties are selling expenses

33

Proposed Regulations (Cont.)

Also proposes to amend Reg. §§1.263A-2 and -3 to provide (simplified production and resale methods) as follows:

- Additional Sect. 263A costs, Sect. 471 costs incurred during year, and Sect. 471 costs remaining on hand at g y , gyear-end, do not include sales-based royalties.

Applies to tax years ending on or after the publication as finalApplies to tax years ending on or after the publication as final regulations.

LB&I 4 0211 (Mar 1 2011): Field directive advises- LB&I-4-0211 (Mar. 1, 2011): Field directive advises examiners not to expend resources challenging a taxpayer’s treatment that is consistent with the proposed regulations

34

regulations.

Impact On Simplified Formulas: Example

Simplified production method, without historic absorptionhistoric absorption

35

Proposed Regulations: Sales-Based Vendor Allowances

Prop. Reg. § 1.471-3(e)p g § ( )

- Vendor allowances include allowances, discounts or price rebates a taxpayer earns by selling specific merchandiserebates a taxpayer earns by selling specific merchandise.

- Amends current regulations to provide that a sales-based vendor allowance is an adjustment only to the cost ofvendor allowance is an adjustment only to the cost of merchandise sold during the year

- Would prohibit use of specific tracing method to allocate to ending inventory

36

Proposed Regulations: Sales-Based Vendor Allowances (Cont.)( )

Prop. Reg. § 1.471-3(e), Cont.

- Also proposes to amend Reg. §§1.263A-2 and -3 to provide (simplified production and resale methods) as follows:

• Additional Sect. 263A costs, Sect. 471 costs incurred during year and Sect 471 costs remaining on hand atduring year, and Sect. 471 costs remaining on hand at year-end do not include cost reductions described in §1.471-3(e).

Proposed to be effective for tax years ending on or after publication of final regulations

37

Tax Accounting Guidance Plan: Negative 263A Costsg

Negative Sect. 263A costs are costs not required or permitted to be capitalized for tax purposes, but are capitalized for financial reporting purposes.p g p p

- Schedule M adjustments (e.g., book-over-tax depreciation)

- Not capitalized for tax (e g Sect 174 costs)- Not capitalized for tax (e.g., Sect. 174 costs)

Need to convert book inventories to a tax basis

- Simplified approach

- Replication of costing system on a tax basis

IRS concern that removal of costs under a simplified approach will generally differ from costs removed using the taxpayer’s book allocation methodology; TAM 200607021

38

Tax Accounting Guidance Plan: Negative 263A Costs (Cont.)g ( )

Notice 2007-29 provides:

The Service will not challenge the inclusion of negative amounts in computing additional costs under Sect. 263A.

The IRS will not continue to pursue the issue in any tax year ending on or before the publication of anticipated guidance.

The IRS will not deny consent for the changes in method of accounting that involve negative 263A costs.

Government also requests comments.

39

Proposal For Negatives

Proposal for new absorption ratio

40

Retail Industry Issue Resolution Program

Field directive (LMSB-04-0910-026)

- Advises exam to treat SBVAs and MPPs as purchase price- Advises exam to treat SBVAs and MPPs as purchase price adjustment, NOT income

Ad i t ti t l T R §1 471 8- Advises exam to continue to rely on Treas. Reg. §1.471-8 to calculate ending inventory under RIM

41

Proposed Regulations: Retail Inventory Methody

Treas. Reg. 1.471-8 cost complement:

To approximate lower of cost or market, 1.471-8(d) allows a taxpayer to exclude permanent mark-downs from the denominator.

42

Proposed Regulations: Retail Inventory Method, Exampley , p

One item purchased, and one item in EI

43

Proposed Regulations: Retail Inventory Method (Cont.)y ( )

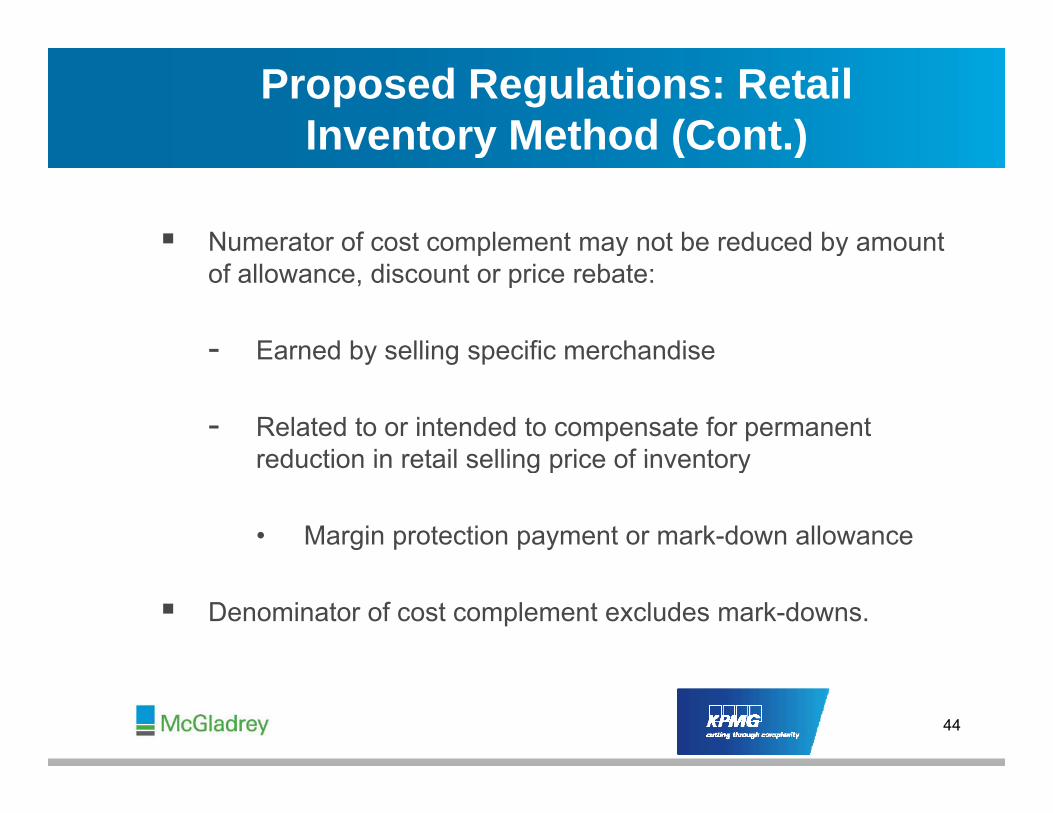

Numerator of cost complement may not be reduced by amount p y yof allowance, discount or price rebate:

- Earned by selling specific merchandiseEarned by selling specific merchandise

- Related to or intended to compensate for permanent reduction in retail selling price of inventoryreduction in retail selling price of inventory

• Margin protection payment or mark-down allowance

Denominator of cost complement excludes mark-downs.

44

Proposed Regulations: Retail Inventory Method (Cont.)y ( )

Adjustment to inventory value related to permanent mark-ups j y p pand mark-downs made by adjustment to retail selling price of ending inventory- Comments requested on alternatives to computing LCM q p g

under RIM

Neither cost complement nor ending retail selling pricesNeither cost complement nor ending retail selling prices adjusted for temporary mark-downs and mark-ups

Will apply to tax years beginning after date published as final Will apply to tax years beginning after date published as final

45

Treatment Of Automobile Dealer Storage And Handling Costsg g

Broad definition of motor vehicle dealershipretail sales facility safe harbor

Treat entire facility as retail sales facility

Vehicle lot routinely visited by retail customers

Not required to capitalize storage and handling costs

46

Treatment Of Automobile Dealer Storage And Handling Costs (Cont.)Storage And Handling Costs (Cont.)

Reseller without production activities safe harbor Motor vehicle dealership may treat itself as a reseller without

production activities. Handling costs relating to activities performed on dealership

owned or customer owned vehicles not capitalized Must capitalize the cost of vehicle parts Use of “negative” additional Sect. 263A costs prohibited Automatic change

47

ONGOING COMPLIANCE Donald A. Barnes, Law Offices of Donald A. Barnes, PLLC

CHALLENGES UNDER SECT. 263A263A

Application Of Robinson Knife To Resellers

R l ti l t b th d d ll• Regulations apply to both producers and resellers

• Description of guidance changed • Description of guidance changed

• Robinson Knife and Plastic Engineering Robinson Knife and Plastic Engineering

• TAM 200630019

• Comments submitted to Treasury: All relate to producers

49

R llResellers

• Sales-based royalties: Inventory purchased for resale

• Royalties payable to supplier or third party

• Similar to additional earn-out payment

50

E lExample

• Taxpayer incurs $100 to purchase product for resale.

• Upon sale, taxpayer becomes obligated to pay additional $5.

• Direct acquisition cost of product is $105.

• $5 is an IRC §471 cost, not an additional IRC §263A cost.

51

IRC § 6 A C F R llIRC §263A Costs For Resellers

T R §1 263A 3( )(1) I di t t t ft i d • Treas. Reg. §1.263A-3(c)(1): Indirect costs most often incurred by resellers

― Purchasing, handling, storage costsg, g, g

• Treas. Reg. §1.263A-3(c)(2) through (5)

― Costs attributable to purchasing, handling and storage

• G&A costs that directly benefit or incurred by reason of purchasing, handling and storage activities

52

Li T S ll P dLicense To Sell Product

• Confused timing of accrual with “purpose” of cost

• FAA 20114703F• FAA 20114703F

• Abbreviated applications to Food and Drug Administration

• Seeking approval for generic drugsSeeking approval for generic drugs

• Provides taxpayer with right to market and sell generic drugs

• Costs are capitalized and amortized.

53

FAA F (C )FAA 20114703F (Cont.)

• Annual cost recovery is indirect production cost under IRC §263A.§

• Treas. Reg. §1.263A-1(e)(3)(ii)(U): Initial fees to obtain a license or franchise

T ’ d “ ld t b d d if th ld t b • Taxpayer’s drugs “would not be produced if they could not be marketed and sold.”

54

I H ld F S l O RInventory Held For Sale Or Rent

IRS i i t “Wh IRC § 263A • IRS examining agent: “Where are your IRC § 263A computations?

• Distributor of equipment held for sale or rent

• Equipment classified as inventory for book purposes

• But, depreciable for tax purposes

55

F l d P iForeclosed Properties

B k d C it l M k t T I tit t ti (11/3/11)• Bank and Capital Markets Tax Institute meeting (11/3/11)

• Holding costs of foreclosed properties• Holding costs of foreclosed properties

• Income-producing vs. non-income-producing Income producing vs. non income producing

• Holding costs of non-income-producing foreclosed properties

• Capitalized even prior to IRC §263A

56

LIFO TLIFO Taxpayer

• Existing IRC §263A method had several problems.

• Using simplified resale method

• Did not include all mixed service costs

57

LIFO T (C )LIFO Taxpayer (Cont.)

• Automatic method change to simplified production method

• Three-year average method to determine IRC §481 adjustment• Three-year average method to determine IRC §481 adjustment

• Revaluation factor (average current year cost of ending inventory)

• Former absorption ratio applied to LIFO value of entire inventory

R lt d i it li ti f dditi l IRC §263A t• Resulted in overcapitalization of additional IRC §263A costs

• Net negative IRC §481 adjustment

58