second consultation on policy owners' protection …...second consultation paper december 2009...

TRANSCRIPT

CONSULTATION PAPERP010 - 2009December 2009

Second Consultation on Policy Owners'Protection Fund

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE i

PREFACE

Currently, the Insurance Act provides for separate Policy Owners’ Protection Fund (“PPF”) schemes for life and general insurance to compensate policy owners of life policies and compulsory insurance policies1 respectively, in the event of the default of their insurer. To ensure that the PPF schemes remain relevant taking into account market and regulatory developments, the Monetary Authority of Singapore (“MAS”) had commenced a review of the PPF schemes. The review is guided by two fundamental principles: the need to provide adequate protection to policy owners while keeping the cost of PPF affordable, and achieving an equitable allocation of cost amongst insurers participating in the scheme. 2 In December 2005, MAS issued the first consultation paper2 on the review of the PPF schemes, relating to the membership of the PPF schemes, scope and level of PPF coverage, continuity of insurance coverage, funding method, target fund size and levies. This second consultation paper revisits some of the issues covered in the first consultation paper (namely, membership, and scope and level of coverage) in light of some recent developments. This paper also sets out proposals relating to the implementation details of the PPF schemes such as the administration of the schemes, management of the PPF funds, collection of levies, payouts using PPF funds and the priority ranking of liabilities. 3 MAS invites interested parties to forward their views and comments on the proposals made in this paper. Electronic submission is encouraged. Please submit your written comments by 29 January 2010 to:

Prudential Policy Department Monetary Authority of Singapore 10 Shenton Way MAS Building Singapore 079117 Fax: 6220 3973 Email: [email protected]

4 Please note that all submissions received may be made public unless confidentiality is specifically requested for the whole or part of the submission.

1 “Compulsory insurance policies” is defined in the Insurance Act as any policy or security

which satisfies the requirements of the Motor Vehicles (Third Party Risks and Compensation) Act (Cap 189) or the Work Injury Compensation Act (Cap 354).

2 A copy of the first consultation paper as well as MAS’ response to feedback received can be found at http://www.mas.gov.sg/publications/consult_papers/2005/index.html.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

Preface i Table of Contents ii 1. Introduction 1 2. Review of Proposals in First Consultation Paper 2 3. PPF Agency: Governance And Mandate 8 4. Management of the PPF Funds 10 5. Levy Collection 11 6. PPF Payout 13 7. Priority Ranking of Liabilities 17 8. Annex A 18

MONETARY AUTHORITY OF SINGAPORE ii

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

1 INTRODUCTION 1.1 Currently, the Insurance Act provides for separate PPF schemes for life and general insurance which will protect or compensate policy owners of life policies and compulsory insurance policies respectively, in the event of the default of their insurer. Besides alleviating financial distress to individual policy owners, the PPF schemes enhance public confidence in the insurance industry by giving policy owners greater certainty as to how much of their policy monies will be protected and whether the losses they have incurred from insured events will be compensated should their insurer default. This will help limit possible disruption to the economy. 1.2 MAS has embarked on a review of the existing PPF schemes to ensure that they keep pace with industry and regulatory developments, and issued a consultation paper in December 2005 on the first phase of the PPF review. This covered issues relating to the membership, scope and level of coverage, continuity of coverage, funding and size of levies. 1.3 Some of these issues, namely, scope and level of coverage of the PPF life and general insurance schemes, and membership of the PPF general insurance scheme, are revisited in this consultation paper to take into account developments since 2005. The revised proposals are set out in Section 2 of this consultation paper. 1.4 MAS has also completed the second phase of its review of the PPF schemes. The second phase focuses on implementation issues such as the administration of the PPF schemes, management of the PPF funds, collection of levies, payouts using PPF funds and priority ranking of liabilities. Sections 3 to 7 set out the specific proposals pertaining to these issues. The full set of proposals from both the first and second phases of review is summarised in Annex A.

MONETARY AUTHORITY OF SINGAPORE 1

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 2

2 REVIEW OF PROPOSALS IN FIRST CONSULTATION PAPER PPF Life Insurance Scheme Level of Coverage 2.1 The first consultation paper in 2005 proposed that:

- The PPF life insurance scheme will provide compensation for 90% of the amount of protected liabilities of all life, and accident and health (“A&H”) policies3.

- With the exception of disability income, long-term care and medical expense insurance policies, all other policies will be subject to an aggregate cap of S$500,000 for sum assured and S$100,000 for surrender value.

- The caps will apply on the aggregate sum assured and aggregate surrender value of all life policies owned by the policy owner and issued by the same insurer.

- A simple ratio approach will be used to derive the protection ratio of the affected policy owner.

MAS proposes to amend these proposals as detailed below. Compensation Coverage 2.2 MAS proposes to remove the 90% limit and provide for 100% coverage of protected liabilities of all life and A&H policies instead, subject to the aggregate caps where applicable. The 90% limit is provided for under the existing PPF provisions in the Insurance Act and it was retained previously to serve as an incentive for policy owners to exercise prudence and market discipline in their selection of insurers. However, the introduction of the aggregate cap of S$500,000 for sum assured and S$100,000 for surrender value will create such an incentive as well. For policies which are not subject to the aggregate caps, namely disability income, long-term care and medical expense insurance policies, these policies are generally intended to indemnify losses as they occur. Thus any risk of moral hazard by moving to 100% coverage is low. As such, for greater certainty of coverage and better protection to policy owners, MAS proposes to provide for 100% coverage, subject to the aggregate caps where applicable.

3 Section 46 of the Insurance Act currently protects 90% of an insurer’s liability on any life

policy in the event of default of the insurer.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 3

Application of Aggregation Caps 2.3 While it is envisaged that generally, the policy owner and the life assured are the same person, there may be cases where the policy owner is not the life assured. For example, the head of a household may purchase life insurance policies for all family members. This may result in the reduction in the PPF payout for a particular life assured at the claims stage, if there are other policies under the same policy owner which upon aggregation will exceed the caps for sum assured and surrender value. MAS therefore proposes to apply the caps on all life insurance policies issued on the same life assured (instead of owned by the same policy owner as previously proposed) and by the same insurer. Policies to be Included in Aggregation Caps 2.4 In the first consultation paper, MAS proposed to introduce an absolute cap4 of S$500,000 on the sum assured and S$100,000 on the surrender value of policies covered under the PPF life insurance scheme. This maintains the incentive for consumers to exercise some market discipline in their selection of insurers and keeps the PPF life insurance scheme affordable at the same time.

2.5 Only main policies were considered in the aggregation of policies in the first consultation paper. However, it is common for policy owners to attach riders to their main policies to supplement their insurance coverage. Riders typically do not accrue cash value but instead offer other benefits, such as increase of sum assured, acceleration of payment of benefits, disability income, etc. In particular, term riders (including level term, decreasing term, convertible term and additional critical illness term rider) effectively increase the sum assured. MAS therefore proposes to include all term riders when aggregating the sum assured to calculate the protection ratio to determine PPF payout. 2.6 Group policies are typically arranged by an individual’s employer, with the individual having little or no say over the choice of the insurer. As such, while group policies will be covered under the PPF life insurance scheme, MAS proposes to exclude group insurance policies when aggregating the sum assured and surrender value to calculate the protection ratio to determine PPF payout for the individual life insurance policies. MAS is reviewing the separate cap5 that group insurance policies should be subject to. Protection Ratio 2.7 Previously, it was proposed that a simple ratio approach be used to derive the protection ratio of affected policy owners. However, using the

4 With the exception of disability income, long-term care and medical expense insurance

policies. 5 This cap is different from the aggregate cap of $500,000 and $100,000 for sum assured

and surrender value respectively as proposed for the individual life insurance policies.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 4

simple ratio approach may lead to anomalous results 6 (as illustrated in Figure 1, which assumes the case of 3 life policies issued on a life assured by an insurer which defaults) than applying the protection ratio separately to the aggregate sum assured and surrender value. Thus, MAS proposes to apply the protection ratio separately to the aggregate sum assured and surrender value when deriving the PPF payout. The application of the protection ratio separately to the aggregate sum assured and surrender value is illustrated in Figure 2, using the example of the same policy owner.

Figure 1: Application of Simple Ratio to Derive Protection Ratio

Figure 2: Application of Protection Ratio Separately

6 Under the simple ratio approach, the total PPF payout for sum assured works out to be

less than $500,000, whilst the total PPF payout for surrender value works out to be more than $100,000.

Before applying average protection ratio

Guaranteed Sum Assured

Guaranteed Surrender Value

Policy 1 S$200,000 S$100,000 Policy 2 S$100,000 S$ 50,000 Policy 3 S$300,000 - Total S$600,000 S$150,000 Amount protected (subject to caps) S$500,000 S$100,000 Protection Ratio 83.3% 66.7% Average Protection Ratio 75.0% 75.0% After applying average protection ratio

Policy 1 S$150,000 S$ 75,000 Policy 2 S$ 75,000 S$ 37,500 Policy 3 S$225,000 - Total S$450,000 S$112,500

Before applying average protection ratio

Guaranteed Sum Assured

Guaranteed Surrender Value

Policy 1 S$200,000 S$100,000 Policy 2 S$100,000 S$ 50,000 Policy 3 S$300,000 - Total S$600,000 S$150,000 Amount protected (subject to caps) S$500,000 S$100,000 Protection Ratio 83.3% 66.7% After applying protection ratio separately

Policy 1 S$166,667 S$ 66,667 Policy 2 S$ 83,333 S$ 33,333 Policy 3 S$250,000 - Total S$500,000 S$100,000

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 5

Scope of Coverage Coupon Deposits 2.8 Most life insurers offer life insurance policies such as anticipated endowment plans, which provide a cash coupon at regular intervals. Besides claiming the cash coupons, policy owners may alternatively leave the coupons with the life insurer to earn higher interest to build up a higher payout at maturity or surrender. These are known as coupon deposits. As coupon deposits could make up a significant portion of policy benefits, MAS proposes that coupon deposits be covered under the PPF life insurance scheme. Advance Premium Payments 2.9 Though uncommon, there may be instances where life insurers receive advance premium payments from policy owners for life insurance policies. As such advance premium payments are akin to unearned premiums under the PPF general insurance scheme, MAS proposes that advance premium payments be covered under the PPF life insurance scheme. Unclaimed Monies 2.10 There may also be cases where admitted claim, maturity and surrender payments have not been sent out to the policy owners due to delays in arranging payments 7 , or have not been collected or banked in by policy owners. It will not be fair to policy owners if such benefits, which they have not collected, are not protected under the PPF life insurance scheme. As such, MAS proposes that such unclaimed monies be covered under the PPF life insurance scheme. 7 These will not include claims which are pending investigation by the insurer.

Proposal 1: The PPF life insurance scheme will provide 100% coverage of protected liabilities of all life and A&H policies. Proposal 2: The caps on aggregate sum assured and surrender value will apply on all life insurance policies (with the exception of disability income, long-term care and medical expense policies) issued on the same life assured and by the same insurer. Proposal 3: All term riders will be included in the aggregation process to calculate the protection ratio to determine PPF payout. Proposal 4: Group insurance policies will be excluded in the aggregation process to calculate the protection ratio to determine PPF payout. Proposal 5: The protection ratio will be applied separately to the aggregate sum assured and surrender value when calculating PPF payout.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

2.11 However, MAS does not propose that the coverage of coupon deposits, advance premium payments and unclaimed monies be subject to the aggregate caps imposed under the PPF life insurance scheme as the imposition of the caps will introduce additional complications in levy computations without significant savings in PPF costs. Definition of Protected Liabilities 2.12 For the avoidance of doubt as to what constitute protected liabilities to be covered under the PPF life insurance scheme, Table 1 sets out the definition of protected liabilities.

Table 1: Definition of Protected Liabilities

For the purpose of ... Protected Liabilities mean… Levy Calculation

Policy liabilities for the guaranteed portions only of sum assured and surrender value, calculated as at 31 December of the preceding year in accordance with the Insurance (Valuation and Capital) Regulations.

Claims which have crystallised

In the case of death/Total and Permanent Disability (“TPD”)/critical illness/accidental/medical claims etc. - Guaranteed sum assured (including all past bonuses (if any) which have been declared and vested). In the case of surrenders- Guaranteed surrender value at the point of surrender.

Transfer

Policy liabilities for the guaranteed portions only of sum assured and surrender value calculated, depending on when the transfer takes place, in accordance with the Insurance (Valuation and Capital) Regulations.

Cut-off Guaranteed surrender value, if any.

Run-off

Policy liabilities for the guaranteed portions only of sum assured and surrender value, calculated at the valuation date in accordance with the Insurance (Valuation and Capital) Regulations.

Proposal 6: The PPF life insurance scheme will cover accumulated values of coupon deposits, advance premium payments and unclaimed monies, without any aggregate caps imposed.

MONETARY AUTHORITY OF SINGAPORE 6

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

PPF General Insurance Scheme Membership 2.13 In the first consultation paper, it was proposed that all registered direct general insurers, except professional reinsurers, captive insurers and specialist insurers, be members of the PPF general insurance scheme, which would provide coverage for the following classes of business:

(i) Motor third party liability injury insurance; (ii) Work Injury Compensation Act liability insurance; (iii) Personal motor insurance; (iv) Individual and group A&H insurance; (v) Personal property (structure and contents) insurance; (vi) Foreign domestic maid insurance; and (vii) Personal travel insurance.

2.14 There are currently some direct general insurers that do not write any class of business protected under the PPF general insurance scheme. Being a member of the scheme will thus add little value to these insurers as their policy owners will not benefit from the coverage provided under the scheme. 2.15 MAS therefore proposes that direct general insurers which do not write any of the business covered under the PPF general insurance scheme can seek MAS’ approval for exemption from membership.

Proposal 7: Subject to MAS’ approval, exemption from membership of the PPF general insurance scheme can be made for direct general insurers that do not write any of the protected business covered under the PPF general insurance scheme.

Level of Coverage 2.16 The first consultation paper proposed to cover 100% of liabilities of compulsory lines (i.e. motor third party liability injury insurance and Work Injury Compensation Act liability insurance), and 90% of liabilities of other protected general lines. To be consistent with the proposal to revise the level of coverage for all life and A&H policies from 90% to 100%, MAS proposes to provide 100% coverage for all protected general lines in order to offer better protection to policy owners. No caps will be imposed for all general insurance lines, as proposed in the first consultation paper. This is because general insurance policies typically indemnify losses as they occur and payouts will only be made based on actual claims incurred.

Proposal 8: The PPF general insurance scheme will provide 100% coverage of all protected liabilities of covered lines of business.

MONETARY AUTHORITY OF SINGAPORE 7

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 8

3 PPF AGENCY: GOVERNANCE AND MANDATE PPF Agency: Who to Administer? 3.1 The Singapore Deposit Insurance (“DI”) scheme is currently administered by the Singapore Deposit Insurance Corporation (“SDIC”). To enable cost efficiency to be achieved and to leverage on existing administrative resources and structure, MAS proposes that SDIC administer the PPF schemes as well. PPF Agency: Governance 3.2 To avoid potential conflicts of interest, individuals who are currently directors of, employed by or otherwise connected to member institutions of the PPF schemes cannot be directors of SDIC. The board of directors of SDIC will also be accountable to the Minister for its acts and decisions on the PPF schemes. These requirements are similar to those for the DI scheme. PPF Agency: Roles and Responsibilities 3.3 SDIC will establish two PPF funds, one for life insurance and the other for general insurance. For equity, transparency and accountability, the two PPF funds and the DI fund will be maintained separately, as each fund is built up from contributions from different types of financial institutions for the benefit of their respective customers. Inter-fund lending among the three funds will also not be allowed. 3.4 The principal functions of the SDIC with respect to the PPF schemes will be levy collection, management of the PPF funds, making payouts and consumer education. These functions are similar to those that the SDIC is currently performing for the DI scheme. 3.5 In addition to making payouts for PPF-covered claims8, SDIC will be allowed to use the PPF life insurance scheme to fund the transfer of life insurance policies in force as far as the transfer is reasonably practicable. This is so that the PPF life insurance scheme will continue to provide for continuity of insurance protection for policy owner. Where it is not practicable for the remaining life insurance policies to be transferred, the PPF life insurance scheme will be given the flexibility to run-off the portfolio of policies or to compensate policy owners up to the PPF coverage limit and terminate the policies accordingly. In the event that the run-off approach is adopted, SDIC will set up a company to hold the policies, and outsource the administration of the policies to a third party. 3.6 Similar to the DI scheme, MAS will make the decision on whether to trigger payouts using PPF funds as it is the agency responsible for supervising insurers and would thus be in possession of more information

8 These would be claims that have crystallised at the point when PPF is triggered.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

than SDIC to make that assessment. However, as custodian and manager of the PPF funds, SDIC would have an interest in how the PPF funds are disbursed. MAS therefore proposes for SDIC to verify that MAS has adhered to the established procedures in triggering payouts using PPF funds.

Proposal 9: The PPF schemes will be administered by SDIC. Proposal 10: Directors of SDIC cannot currently be directors of, employed by or otherwise connected to member institutions of the PPF schemes. The Board of Directors of SDIC will be accountable to the Minister for its acts and decisions on the PPF schemes. Proposal 11: SDIC will establish a PPF fund for life insurance and a PPF fund for general insurance. The two PPF funds and the DI fund will be maintained separately and no inter-lending is allowed among the three funds. Proposal 12: The principal functions of SDIC with respect to the PPF schemes will be levy collection, management of the PPF funds, making payouts and consumer education. In the event that policies are to be placed on run-off, SDIC will set up a company to hold the policies and outsource the administration of the policies to a third party. Proposal 13: MAS will make the decision on whether to trigger payouts using PPF funds. SDIC will verify that MAS has adhered to established procedures in triggering payouts.

MONETARY AUTHORITY OF SINGAPORE 9

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

4 MANAGEMENT OF THE PPF FUNDS

Investment of PPF Funds 4.1 PPF funds should be invested in safe and liquid assets to meet the objectives of capital preservation and maintenance of liquidity to expedite payouts to policy owners. MAS therefore proposes that the PPF funds be invested in any security issued by the Singapore Government, Singapore dollar deposits with MAS and such other investments as may be approved by the Minister. Liquidity Provision 4.2 In the event that payouts exceed the size of the PPF funds, SDIC may borrow to finance the difference, pending recovery of the payout amount from the disposal of assets of the failed member institution.

Proposal 14: PPF funds should be invested in any security issued by the Singapore Government, Singapore dollar deposits with MAS and such other investments as may be approved by the Minister. Proposal 15: SDIC will be empowered to borrow to finance the shortfall, in the event that payouts exceed the size of the PPF funds.

MONETARY AUTHORITY OF SINGAPORE 10

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 11

5 LEVY COLLECTION Frequency of Levy Assessment 5.1 For ease of administration, MAS proposes that member institutions be assessed once a year, on a calendar year basis, for PPF levies. Reference Date for Levy Contribution 5.2 For the PPF life insurance scheme, it was proposed in the first consultation paper that the levies to be charged to life insurers (including life insurers on run-off) should be based on the amount of guaranteed policy liabilities that are covered under the scheme (“protected liabilities”). MAS proposes that the reference date for assessment of protected liabilities should be 31 December of the preceding year. 5.3 For the PPF general insurance scheme, it was proposed in the first consultation paper that for active general insurers, the levies to be charged should be based on the gross written premium received or receivable for the classes of business protected under the scheme. MAS proposes that this should be the gross written premium received or receivable from 1 January to 31 December of the preceding year9. For general insurers on run-off, it was proposed to use the amount of protected liabilities as the assessment base as such insurers do not write any new business. As such, the reference date for assessment of protected liabilities should be the same as that for the life insurers, i.e. 31 December of the preceding year. 5.4 To allow insurers sufficient time to collate the necessary information to calculate the PPF levies, MAS proposes that member institutions submit information on the assessment base by 30 April of each year. Date and Method of Levy Collection 5.5 Taking into consideration the time needed to process the information on the assessment base submitted by member institutions, MAS proposes for member institutions to be invoiced by 1 June of each year, and for PPF levies to be paid by 1 July of each year. Levy contribution should be made in a single payment. MAS will deduct the PPF levies from the member institutions’ designated agent bank account with MAS and credit to SDIC’s PPF accounts maintained with MAS. Entry and Exit of Member Institutions 5.6 MAS proposes that new member institutions that join the PPF schemes during the course of a calendar year, be charged levies for the year on a pro-rata basis, according to the number of months remaining for that year. The 9 Unlike for life insurers, for active general insurers, the PPF levy is calculated as a

percentage of gross written premium received or receivable for the protected classes. Hence, a “point-in-time” estimate is not applicable.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

levy will be payable in advance, one month after the commencement of operations by the member institution. 5.7 For member institutions that deregister as insurers during the course of the year, no levies will be re-funded. Minimum Levy to be Imposed 5.8 To ensure that the costs of administering the PPF schemes are adequately covered, MAS proposes that member institutions be required to pay a minimum levy of S$2,500 per annum.

Proposal 16: Member institutions will be assessed once a year for PPF levies. Proposal 17: For life insurers (including those on run-off) and general insurers on run-off, the assessment base will be the amount of protected liabilities under the PPF life insurance scheme as at 31 December of the preceding year. Proposal 18: For active general insurers, the assessment base will be the gross written premium received or receivable for protected classes of business under the PPF general insurance scheme from 1 January to 31 December of the preceding year. Proposal 19: Member institutions should submit information on the assessment base by 30 April of each year. Proposal 20: Levy contribution for each assessment year will be made in full in a single payment. Member institutions will be invoiced on 1 June of each year, with the levy payable on 1 July of the same year. Proposal 21: PPF levies will be deducted from member institutions’ designated agent bank accounts with MAS and credited into SDIC’s PPF accounts maintained with MAS. Proposal 22: Where an insurer becomes a member institution during the course of a calendar year, levies for that year will be levied on a pro-rata basis, according to the number of months remaining for that year. Proposal 23: No levies will be refunded to a member institution which deregisters during the course of the year. Proposal 24: The minimum levy to be paid by member institutions is S$2,500 per annum.

MONETARY AUTHORITY OF SINGAPORE 12

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 13

6 PPF PAYOUT Conditions for Use of PPF Funds 6.1 It was proposed in the first consultation paper that PPF funds from the life insurance scheme may be used to make payouts for PPF-covered claims10 and to fund the transfer of life insurance policies in force from a life insurer to another insurer as far as the transfer is reasonably practicable. Where it is not practicable for remaining policies to be transferred, PPF funds may be used to run-off the portfolio of policies or to compensate policy owners up to the PPF coverage limit and terminate the policies accordingly. 6.2 Before payouts can be made using PPF funds for those purposes set out above, MAS proposes that the following conditions must be met:

- An insurer is in liquidation; or - An insurer is unable or unlikely to be able to meet obligations, is

or likely to become insolvent or about to suspend payments to policy owners/creditors.

6.3 The conditions will apply to both the PPF life and general insurance schemes. They will also be necessary but not sufficient conditions for the use of PPF funds. Depending on the circumstances of the insurer and the method of insurance resolution appropriate to the particular situation of the insurer and public policy objectives, payouts using PPF funds may not be necessary. For example, an insurer may be experiencing financial difficulties while still solvent and able to meet its obligations. 6.4 As the supervisor of insurers in Singapore, MAS will be responsible for deciding whether the use of PPF funds is appropriate, when either of the above conditions have occurred. MAS will take into account the various resolution options available in determining whether the use of PPF funds is necessary. MAS will notify SDIC if it decides that a payout from PPF funds is to be made. SDIC will then proceed to make the payout after verifying that MAS has adhered to established procedures in coming to that decision. Payout Process 6.5 When a payout using PPF funds is triggered, SDIC will make this known through:

- A Gazette on the notice of payment of compensation, stating that a payment of compensation is to be made to or on behalf of the insured policy owner of the failed insurer out of the respective PPF scheme;

10 For life and A&H insurance policies, these would be claims that have crystallised at the

point that PPF is triggered. For general insurance policies, these would include crystallised claims and claims incurred up to 30 days after the winding up order.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 14

- A media release, which will include radio broadcasts and the daily press in the four official languages; and

- Notices posted at the failed insurer’s premises.

6.6 For crystallised claims and compensation for policies terminated, SDIC will make compensation payment to or on behalf of policy owners by either issuing cheques or crediting the policy owners’ bank account as stated in the member institution’s database. Subrogation to Policy Owner’s Rights 6.7 Having made payouts to policy owners or to ensure continuity of insurance coverage for policy owners, SDIC will be subrogated to the rights of policy owners to claim against the assets of the failed insurer for the amount of payout made. For example, if SDIC pays S$50,000 to a policy owner, SDIC will be able to stand as a creditor to claim from the liquidator of the insurer, an equivalent amount paid to the policy owner. This does not affect the right of the policy owner to file a separate claim for the difference between his policy benefits and the PPF payout. However, he will not be able to claim any amount that has already been paid to him by SDIC or for benefits that continue to be insured by the new insurer. 6.8 To expedite the PPF payout process, MAS proposes that SDIC be automatically subrogated to the rights of policy owners for the amount of PPF payouts made, without the need to obtain prior express consent of the policy owners. This will be provided for in legislation. Netting of Policy Benefits Against Policy Loans 6.9 Policy owners may obtain policy loans from insurers. Policy loans are loans granted by insurers to policy owners which are taken against the cash value of the latter’s policies11. They include automatic advances to policy owners to meet unpaid premiums in order to keep the policies in force. 6.10 In the event that PPF is activated, for crystallised claims or where policies have been terminated, MAS proposes to net off all policy loans in full, as illustrated in Figure 3. For policies which have been transferred to another insurer (including to the run-off company), MAS proposes allowing the policy loans to continue under the new insurer. As the insurance policy continues to be in force, it is not necessary to net off the policy loan that was taken against the cash value of the policy.

11 The amount of loan granted will not be permitted to exceed the cash value of the policy of

which the loan is taken against. If the loan amount and interest reaches the cash value of the policy, the policy will be terminated.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 15

Figure 3: Netting of Policy Benefits Against Loans for Crystallised Claims or Terminated Policies

A policy owner has the following policies issued by a life insurer, on which he is the life assured. He has taken a policy loan of S$60,000 against Policy 1. The life insurer has defaulted and PPF has been activated:

Guaranteed Sum Assured

Guaranteed Surrender Value

Policy Loan

Policy 1 S$200,000 S$100,000 S$60,000 Policy 2 S$100,000 S$ 50,000 - Policy 3 S$300,000 - - Total S$600,000 S$150,000 S$60,000

Scenario (a): Crystallised claims (in the case of death/TPD/critical illness etc) Total guaranteed sum assured of S$600,000 will be capped at S$500,000 (PPF cap for sum assured). Protection Ratio = 83.3%*

Sum Assured After Cap

Policy Loan PPF Payout After Netting

Policy 1 S$166,667 S$60,000 S$106,667 Policy 2 S$ 83,333 - S$ 83,333 Policy 3 S$250,000 - S$250,000 Total S$500,000 S$60,000 S$440,000

Total PPF payout for all 3 policies = $440,000 Scenario (b): Crystallised claims (in the case of surrender) and where all policies have been terminated Total guaranteed surrender value of S$150,000 will be capped at S$100,000 (PPF cap for surrender value). Protection Ratio = 66.7%*

Surrender Value After Cap

Policy Loan

PPF Payout After Netting

Policy 1 S$ 66,667 S$60,000 S$ 6,667 Policy 2 S$ 33,333 - S$33,333 Policy 3 - - - Total S$100,000 S$60,000 S$40,000

Total PPF payout for all 3 policies = $40,000 *Please see Figure 2 on how to calculate Protection Ratio.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

Proposal 25: The following pre-conditions must be met before payouts using PPF funds can be made:

- An insurer is in liquidation; or - An insurer is unable or unlikely to be able to meet obligations, is or

likely to become insolvent or about to suspend payments to policy owners/creditors.

These are necessary but not sufficient conditions for payouts using PPF funds. Proposal 26: For crystallised claims and compensation for policies terminated, PPF payouts will be made through the issuance of cheques or by crediting the policy owners’ bank account as stated in the member institution’s database. Proposal 27: SDIC will be automatically subrogated to the rights of policy owners for the amount of PPF payout. Proposal 28: In the event that PPF has been activated, policy loans are to be netted off in full where claims have crystallised or where policies have been terminated, to determine the amount of PPF payouts. For policies which have been transferred (including to a run-off company), there will be no netting of the policy loans as these will be taken on by the new insurer or run-off company and allowed to continue.

MONETARY AUTHORITY OF SINGAPORE 16

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

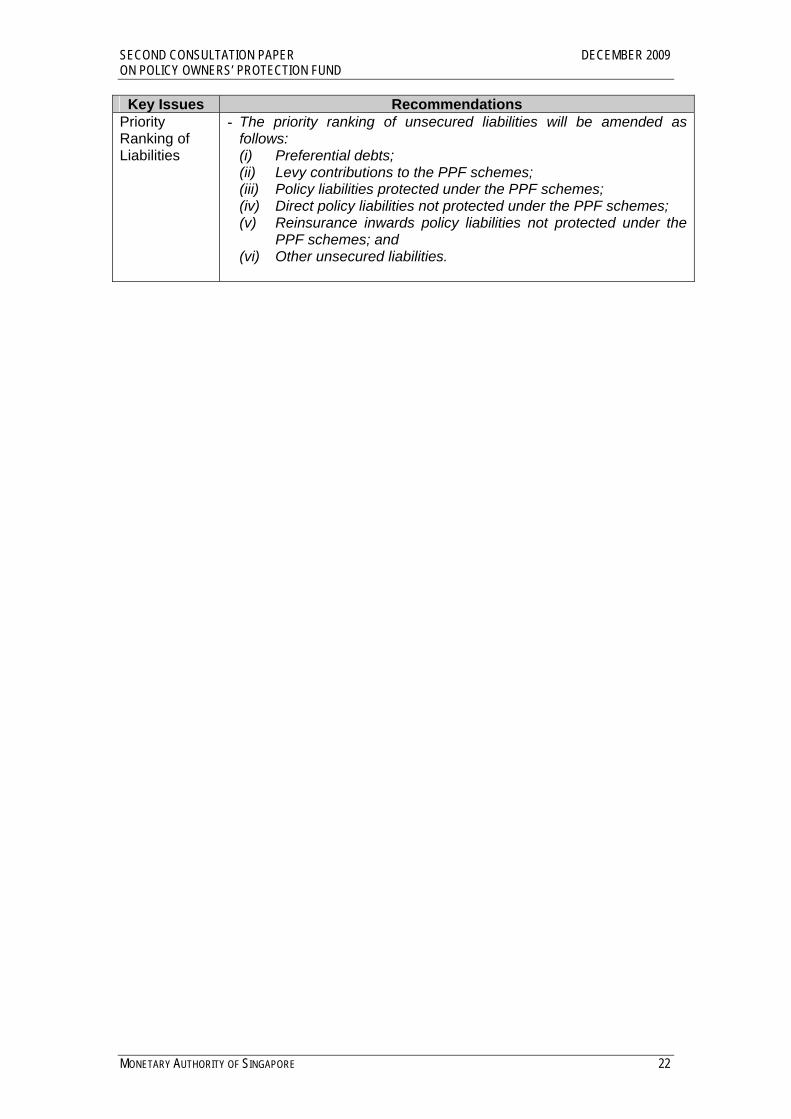

7 PRIORITY RANKING OF LIABILITIES 7.1 Currently, under section 45 of the Insurance Act, where an insurer becomes insolvent or is unable to meet its obligations, the assets of the insurer are available to meet its liabilities to all policy owners of Singapore policies and offshore policies, and these liabilities will have priority over all unsecured liabilities of the insurer other than preferential debts. 7.2 To provide effective protection to policy owners at a lower cost and to maximise protection for PPF protected liabilities, MAS proposes that levy payments made to the PPF schemes as well as policy liabilities covered under the PPF schemes be prioritised over policy liabilities that are not covered by the PPF schemes. This is consistent with the approach for DI, where insured deposit liabilities are given priority over uninsured deposit liabilities. 7.3 Of the policy liabilities that are not covered by the PPF schemes, as policy owners of reinsurance policies are generally more sophisticated than policy owners of direct policies, MAS proposes that direct insurance liabilities be granted priority over reinsurance policy liabilities. 7.4 MAS therefore proposes that the priority ranking of unsecured liabilities be amended as follows:

(i) Preferential debts; (ii) Levy contributions to the PPF schemes; (iii) Policy liabilities protected under the PPF schemes; (iv) Direct policy liabilities not protected under the PPF schemes; (v) Reinsurance inwards policy liabilities not protected under the

PPF schemes; and (vi) Other unsecured liabilities.

Proposal 29: The priority ranking of unsecured liabilities will be amended as follows:

(i) Preferential debts; (ii) Levy contributions to the PPF schemes; (iii) Policy liabilities protected under the PPF schemes; (iv) Direct policy liabilities not protected under the PPF schemes; (v) Reinsurance inwards policy liabilities not protected under the PPF

schemes; and (vi) Other unsecured liabilities.

MONETARY AUTHORITY OF SINGAPORE 17

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 18

Annex A

SUMMARY OF KEY RECOMMENDATIONS FOR PPF SCHEMES12

Key Issues Recommendations

PPF Life Insurance Scheme PPF General Insurance Scheme Membership - Compulsory membership for

all registered direct life insurers, except professional reinsurers and captive insurers.

- Subject to MAS’ approval, exemption from membership can be made if the life insurer provides sufficient evidence to demonstrate that the equivalent scheme in its home jurisdiction would accord policy owners in Singapore protection at least equivalent to that provided by the PPF life insurance scheme in Singapore.

- Compulsory membership for all registered direct general insurers, except professional reinsurers, captive insurers and specialist insurers13.

- Subject to MAS’ approval, exemption from membership can be made if the general insurer provides sufficient evidence to demonstrate that the equivalent scheme in its home jurisdiction would accord policy owners in Singapore protection at least equivalent to that provided by the PPF general insurance scheme in Singapore.

- Subject to MAS’ approval, exemption from membership can also be made for direct general insurers that do not write any of the protected business.

Scope of coverage

Covers: - Life policies and both short-

term and long-term A&H policies written in the life insurance fund.

- Guaranteed benefits only. - Accumulated values of coupon

deposits, advance premium payments and unclaimed monies.

- Singapore and offshore policies.

- Individual and group policies. - For registered life insurers

incorporated overseas, only the life insurance business

Covers: - Liabilities arising from the

Motor Vehicles (Third Party Risks and Compensation) Act and Work Injury Compensation Act insurance.

- Liabilities arising from Singapore policies of personal motor insurance, individual and group A&H insurance, personal property (structure and contents) insurance, foreign domestic maid insurance and personal travel insurance.

- For registered general insurers incorporated overseas, only the

12 Recommendations in italics are proposed in this second consultation paper while

recommendations in non-italics were proposed in the first consultation paper. 13 Specialist insurers refer to the protection and indemnity clubs, financial guarantee

insurers and credit insurers as prescribed by MAS.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 19

Key Issues Recommendations written by the Singapore branch.

Will not cover: - Life insurance business written

by overseas branches of registered life insurers incorporated locally.

- Inward reinsurance business written by direct life insurers.

general insurance business written by the Singapore branch.

Will not cover: - General insurance business

written by overseas branches of registered general insurers incorporated locally.

- Inward reinsurance business written by direct general insurers.

Level of coverage

- 100% coverage for protected liabilities of all life and A&H policies.

- With exception of disability income, long-term care, medical expense and group insurance policies, all other protected policies (including term riders) will be subject to an absolute cap of S$500,000 for sum assured and S$100,000 for surrender value. Accumulated values of coupon deposits, advance premium payments and unclaimed monies will also not be subject to the caps.

- The cap will apply on the aggregate sum assured and surrender value of all life policies issued on the same life assured and by the same insurer.

- The protection ratio will be applied separately to the aggregate sum assured and surrender value when calculating PPF payouts.

- 100% coverage for protected liabilities of all covered business lines.

- No caps will be imposed.

Continuity of insurance

- To fund the transfer of in-force policies out of a life insurer to another insurer as long as the transfer is reasonably practicable.

- For remaining policies that cannot be transferred or settled by termination of policies, the PPF will be given the flexibility to run-off the portfolio of policies where practicable.

- To compensate policy owners on claims incurred, up to 30 days after the winding up order, in respect of policies covered by PPF.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 20

Key Issues Recommendations Method of funding

- To establish a pre-funded PPF through collection of levies from participating insurers.

- Where the cost of failures exceeds target fund size, post-funded levies can be imposed.

- To establish a pre-funded PPF through collection of levies from participating insurers.

- Where the cost of failures exceeds target fund size, post-funded levies can be imposed.

Target fund size

- Target fund size of 0.2% of protected liabilities to be built up over a 10-year period.

- Target fund size of 1.5% of protected liabilities to be built up over a 10-year period.

Levies14

- To impose risk-based levies on insurers, ranging from 0.017% to 0.15% of protected liabilities.

- Levies can be charged to the insurance funds, subject to a limit of the simple average of the annual risk-based levies for the “Medium Low” and “Medium High” supervisory rating categories.

- Levies may be reduced or stopped when target fund size is reached.

- To impose risk-based levies on insurers, ranging from 0.13% to 1.15% of gross premium income of protected classes of business.

- Levies can be charged to the insurance funds, subject to a limit of the simple average of the annual risk-based levies for the “Medium Low” and “Medium High” supervisory rating categories.

- Levies may be reduced or stopped when target fund size is reached.

PPF Agency: Governance and Administration

- The PPF schemes will be administered by SDIC. - Directors of SDIC cannot currently be directors of, employed by or

otherwise connected to member institutions of the PPF schemes. The Board of Directors of SDIC will be accountable to the Minister for its acts and decisions on the PPF schemes.

- SDIC will establish a PPF fund for life insurance and a PPF fund for general insurance. The two PPF funds and the DI fund will be maintained separately and no inter-lending is allowed among the three funds.

- The principal functions of SDIC with respect to the PPF schemes will be levy collection, management of the PPF funds, making payouts and consumer education. In the event that policies are to be placed on run-off, SDIC will set up a company to hold the policies and outsource the administration of the policies to a third party.

- MAS will make the decision on whether to trigger payouts using PPF funds. SDIC will verify that MAS has adhered to established procedures in triggering payouts.

14 The precise levies to be imposed will be reworked closer to the date of the PPF

implementation.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 21

Key Issues Recommendations Management of PPF Funds

- PPF funds should be invested in any security issued by the Singapore Government, Singapore dollar deposits with MAS and such other investments as may be approved by the Minister.

- SDIC will be empowered to borrow to finance the shortfall, in the event that payouts exceed the size of the PPF funds.

Levy Collection

- Member institutions will be assessed once a year for PPF levies. - For life insurers (including those on run-off) and general insurers on

run-off, the assessment base will be the amount of protected liabilities under the PPF life insurance scheme as at 31 December of the preceding year.

- For active general insurers, the assessment base will be the gross written premium received or receivable for protected classes of business under the PPF general insurance scheme from 1 January to 31 December of the preceding year.

- Member institutions should submit information on the assessment base by 30 April of each year.

- Levy contribution for each assessment year will be made in full in a single payment. Member institutions will be invoiced on 1 June of each year, with the levy payable on 1 July of the same year.

- PPF levies will be deducted from member institutions’ designated agent bank accounts with MAS and credited into SDIC’s PPF accounts maintained with MAS.

- Where an insurer becomes a member institution during the course of a calendar year, levies for that year will be levied on a pro-rata basis, according to the number of months remaining for that year.

- No levies will be refunded to a member institution which deregisters during the course of the year.

- The minimum levy to be paid by member institutions is S$2,500 per annum.

PPF Payout - The following pre-conditions must be met before payouts using PPF

funds can be made: - An insurer is in liquidation; or - An insurer is unable or unlikely to be able to meet obligations, is

or likely to become insolvent or about to suspend payments to policy owners/creditors.

These are necessary but not sufficient conditions for payouts using PPF funds.

- For crystallised claims and compensation for policies terminated, PPF payouts will be made through the issuance of cheques or by crediting the policy owners’ bank account as stated in the member institution’s database.

- SDIC will be automatically subrogated to the rights of policy owners for the amount of PPF payout.

- Where PPF has been activated, policy loans are to be netted off in full where claims have crystallised or policies terminated, to determine the amount of PPF payouts. As for policies which have been transferred (including to a run-off company), there will be no netting of the policy loans as these will be taken on by the new insurer or run-off company and allowed to continue.

SECOND CONSULTATION PAPER DECEMBER 2009 ON POLICY OWNERS’ PROTECTION FUND

MONETARY AUTHORITY OF SINGAPORE 22

Key Issues Recommendations Priority Ranking of Liabilities

- The priority ranking of unsecured liabilities will be amended as follows: (i) Preferential debts; (ii) Levy contributions to the PPF schemes; (iii) Policy liabilities protected under the PPF schemes; (iv) Direct policy liabilities not protected under the PPF schemes; (v) Reinsurance inwards policy liabilities not protected under the

PPF schemes; and (vi) Other unsecured liabilities.