school of accounting and finance - amazon...

TRANSCRIPT

School of Accounting and FinanceAFM 461: Taxation II

Fall 2014Course Syllabus

COURSE INSTRUCTORS

Professor: Dan Rogozynski Office: HH HH2101Telephone: 647-403-3345 (cell) E-mail: [email protected] Hours: Class days, 11:30 - 1:00 pm and by appointment

COURSE WEBSITE http://learn.uwaterloo.ca/

COURSE DESCRIPTION

AFM 461 integrates and extends topics from AFM 201 and AFM 361 with an emphasis on basic planning. Topics focus on the use of private corporations and their owners, including corporate reorganizations. The approach is a form of the case method and is applications-based and interactive. Short lectures will precede each major topic to introduce key concepts

LECTURE SCHEDULE

Section Days of the week Time Room Instructor001 Monday & Wednesday 8:30AM-9:50AM AL105 Rogozynski002 Monday & Wednesday 10:00 AM – 11:20 AM AL105 Rogozynski003 Monday & Wednesday 1:00PM – 2:20 PM HH1102 Rogozynski004 Monday & Wednesday 2:30 PM – 3:50 PM HH1102 Rogozynski005 Monday & Wednesday 4:00 PM – 5:20 PM HH1102 Rogozynski

COURSE OBJECTIVES

This is the last of two and one-half introductory courses in federal income tax law from a professional accountant's perspective that are designed to achieve the following objectives:

• to explain the theoretical concepts behind the specific provisions of the law,• to apply the law in practical problems and case settings,• to interpret the law, taking into account the specific wording of the provisions, judicial

decisions and the Canada Revenue Agency's position, and• to introduce basic tax planning concepts through problem application.

COURSE GOALS

Programs delivered by the School of Accounting and Finance (SAF) are designed to provide students with the competencies, professionalism and practical experience that they need to excel in their chosen careers. With this in mind, SAF programs (and courses within the programs) are created to deliver the knowledge, skills and competencies needed. The course contributes to that goal by covering knowledge and skills from the following categories:

AFM 461: Taxation II 2 Fall 2012

1. Functional Competencies – technical knowledge in the area of taxation2. Thinking & Problem Solving Skills3. Communication Skills4. Ethical Conduct5. Learning How to Learn

Upon completing this course, you should be able to meet the learning goals established at the beginning of every chapter in the textbook covered in the course, that is, Chapters 12 to 18.

COURSE RESOURCES

Text Materials

The required texts are:

1) R.E. Beam, S.N. Laiken and J.J. Barnett, Introduction to Federal Income Taxation in Canada, 2012-2013, 35th Edition, CCH Canadian Limited, North York, Ontario, 2014. (Study Guide included)

2) Canadian Income Tax Act with Regulations, 2014 Autumn, 96th Softcover (Academic) Edition, CCH Canadian Limited, North York, Ontario, 2014. (A copy of the equivalent current edition of the Carswell Practitioner's Income Tax Act, edited by David Sherman is a permitted alternative.)

Reference List

The following is by no means an exhaustive list of material on Canadian income taxation. The student might wish to follow articles in The Globe and Mail and National Post, among others.

Electronic Products

The following link, using "Explorer", will lead directly to CCH online service described below the link instructions:

http://www.lib.uwaterloo.ca/Ejournals/passwords/gocch.html

Click on "Go to CCH". While the circle enclosing "Java" spins, click on it or the connection will freeze and fail.

Canadian Tax Library, CCH Canadian Ltd. (Also, in part, on DVD accompanying textbook)

This service is a Windows product containing all of the basic material needed for research on tax law including: the Income Tax Act and Regulations with commentary organized by section number and often presented with good numerical examples, draft or proposed amendments to the law and explanatory notes, budget documents from the latest federal budget, the full text of all court decisions since 1917, the Canada Revenue Agency (CRA) publications including

AFM 461: Taxation II 3 Fall 2012

Interpretation Bulletins, Information Circulars, Advance Tax Rulings and technical interpretation letters (Tax Window Files) with commentary (Window on Canadian Tax), and the GST legislation with commentary.

Tax Find, Canadian Tax Foundation

This service is a Windows product containing various articles written by Canadian tax practitioners from most importantly, the Canadian Tax Journal and the annual Canadian Tax Foundation Conference Report, and also from various provincial conferences. This service contains articles written after 1990. For earlier articles, the paper products of the Canadian Tax Foundation are available in the library. The information contained in these articles can be an excellent resource to deepen your knowledge on a research topic, to help ensure your research of a tax is thorough and to look for tax planning ideas for a client.

Paper Products

Beriault, Yoko and Carol Mohammed, CCH Guide to Researching Canadian Income Tax, CCH Canadian Ltd., North York, current edition.

Bleiwas, P. and J. Hutson, Taxation of Private Corporations and Their Shareholders, current edition, Canadian Tax Foundation, Toronto, current edition.

Ernst & Young's Guide to Tax Research and Writing, Robert (Bob) Neale and Murray Pearson, editors, The Canadian Institute of Chartered Accountants, Toronto, current edition.

Hogg, Peter W. , Joanne E. Magee and Jinyan Li, Principles of Canadian Income Tax Law, Carswell, Toronto, current edition.

Krishna, V. The Fundamentals of Canadian Income Tax, Carswell, Toronto, current edition. (Available on Nexus network in Tax Partner. Contains useful footnote references to court cases and a fairly extensive bibliography at the end of each chapter.)

Preparing Your Corporate Tax Returns, CCH Canadian Ltd., North York, current edition. (Covers tax return preparation with examples and references to forms.)

Preparing Your Income Tax Return, CCH Canadian Ltd., North York, current edition. (Covers tax return preparation with examples and references to forms.)

Sherman, David M., Tax Research: A Practical Guide, Carswell, Toronto, current edition. (Lists basic reference sources in tax law and explains how to use them.)

AFM 461: Taxation II 4 Fall 2012

COURSE EVALUATION AND POLICIES

The student's achievement of the objectives will be evaluated using a written assignment, a mid-term exam, a final exam and classroom contribution.

Examination Dates, Deadlines and Weights

1) Classroom participation, throughout the term over 24 classes 10%

2) Mid-term: Thursday October 30, 2014, 6:30PM-8:30PM (location TBA) 30%

3) 3 Part Assignment: Due Wednesday November 12, 2014, Wednesday November 26, 2014 and Monday December 1, 2014 at 8:30 am in the designated drop box and uploaded to Turnitin. Late assignments will not be accepted 20% No credit will be given for this course unless an assignment paper is submitted.

4) Final: Exam period (date, time and location TBA by Registrar's Office) 40%

Assignment

The written assignment, which must be completed by a group of five, unless the course enrolment is not evenly divisible by five, is attached to this course outline. If the course enrolment is not evenly divisible by five, one or more groups of four will be given specific permission to form, as necessary. No group may be less than four or more than five. Students have the primary responsibility to form a group of five.

Students will enrol in their groups using Learn by Monday September 29, 2014. Switching of group members after that time will not be permitted.

All work is to be performed exclusively by the members of the group and it will be assumed that all group members will contribute their fair share to the assignment. If outside research is performed, sources are to be cited and information discovered via outside research is to be clearly labelled as such. If outside research is performed, the products of your research are not to be shared with any student who is not a member of the group. Violations of academic integrity will be referred to the relevant Associate Dean(s).

Examinations

The exams will present fact situations in which the student will be required to identify potential tax problems and opportunities and to resolve these situations by reference to the Income Tax Act and the relevant common law. Further detailed information on the exams will be posted prior to the exams.

Calculators and one reasonably annotated copy of the Income Tax Act will be the only material allowed for examinations. While the Act may be written in (annotated), highlighted, underlined and tabbed, no additional pages may be inserted. Tabs must be an overall maximum of 1.25 cm by 4 cm (standard size), labelled with section numbers and/or titles only.

AFM 461: Taxation II 5 Fall 2012

Please note that any student who is found to be in violation of this policy during the writing of the mid-term or final examination will have his/her Income Tax Act confiscated immediately and for the duration of the examination. Additional academic penalties as applicable will be pursued for any such violation.

Written appeals of the grading of a mid-term examination must be made within one week after the date the examination has been first been made available for return to the students. A written appeal must be submitted for any reason that requires an adjustment to the mark. The appeal must indicate very clearly the specific additional marks that should be awarded and the reason. The instructors reserve the right to re-grade the entire examination.

A final examination of two and one-half hours duration will be scheduled by the Registrar's Office. This exam will be written during the end of term examination period.

“Faculty of Arts policy provides that students who wish to review their final examination papers informally may do so without instituting a formal appeal procedure. Such review will take place under supervised access only, and will be arranged in a way that is mutually convenient for the instructor and the student.” For the purposes of this course, the review will be conducted in the presence of an independent third party who will not be in a position to answer questions or enter into any discussion about your performance on the exam. Such a review is not intended to provide a learning experience, but to avoid the need to a formal appeal.

School of Accounting and Finance Deferred Exam Policy

Students are expected to write their examinations as regularly scheduled; however, there may be circumstances where accommodating a missed assessment is approved. Accommodation is not automatic upon the presentation of documentation. Instructors will use the documentation along with all information available to them, when determining whether accommodation is warranted. Please note, there will not be deferred mid-terms or final exams for this course.

In the event that a student is unable to sit a final exam during its regularly scheduled time, provided there is a satisfactory basis for the absence with appropriate supporting evidence, the student will normally write the final exam when final exams are scheduled for the next offering of the course, usually, one year later. At the end of the current term you will receive an INC course grade. Since the course is not offered in the immediately subsequent term, at the end of that subsequent term the course grade will automatically change to a FTC and you will be assigned a grade of 32%. This is a systems issue and it is your responsibility to contact the SAF Undergraduate Coordinator, Carol Treitz in HH 3156, at the end of that term and request that the FTC be replaced with an INC. You will need to do this for each subsequent term, until the course is offered and you are able to write the final exam. When you have written the final exam, a grade revision will be submitted, based on the results of the final exam written and your other course work. Failure to write the deferred exam the next time the course is offered will result in a course grade based on the elements of the course you completed.

In the event that a student is unable to sit a midterm exam during its regularly scheduled time, provided there is a satisfactory basis for the absence with appropriate supporting and verifiable evidence, the 30% weight will be added to the weight of the final exam. If the basis for the

AFM 461: Taxation II 6 Fall 2012

absence is not satisfactory, a mark of zero will be awarded for the midterm. University policy on evidence will be followed.

UW’s policy regarding documentation to support requests for accommodation due to illness can be found at http://www.registrar.uwaterloo.ca/students/accom_illness.html. To support requests for accommodation due to illness, students should seek medical treatment and then provide a completed University of Waterloo Verification of Illness Form. This form is normally the only acceptable medical documentation and is available on line at http://info.uwaterloo.ca/infoheal/_StudentMedicalClinic/VIF Online.pdf. For other requests for accommodations, such as death of a family member, appropriate documentation should be provided within a reasonable time period. Students who miss the final exam also must provide the Faculty of Arts Incomplete Grade Agreement Form which is available on line at http://arts.uwaterloo.ca/sites/ca.arts/files/download_doc/INC Grade Agreement Form - final June 2012.pdf

• School of Accounting and Finance students should provide supporting documentation to the SAF Undergraduate Coordinator, Carol Treitz at HH 3156 (if the Undergraduate Coordinator is not available, the documentation should be provided to the receptionist in the Program Office), within 2 working days of the missed assessment. School of Accounting and Finance students must also complete and submit the SAF Request for Exam Accommodation Form (mid-term or final exams) in addition to the supporting documentation noted above. This form can be obtained from the SAF Undergraduate Coordinator at HH 3156. All forms must include student name, ID number, course number of missed examination, and instructor’s name. The SAF Undergraduate Coordinator will complete the bottom section of the SAF Request for Exam Accommodation Form, and provide a copy to the instructor. The Coordinator will maintain a record of missed exams by student (name, ID#), so that unusual situations can be identified and addressed.

Preparation and Classroom Participation

In this course, the typical class will involve in-depth discussion of pre-assigned problems or cases; short lectures will be given on major topic areas. These lectures will be based on the powerpoint presentations linked to the course outline on the classes shown on the outline. Note that the powerpoint presentations contain the technical tax information for the following class(es). As a result, it is very important for you to come prepared to discuss the material assigned for each class, as indicated in the Class Schedule. To prepare material in advance, read the background material and the powerpoint presentations for the class, practice on exercises and wrestle with issues as you attempt to answer the assigned problems. Then, the class time will be used to learn through the discussion. Solutions to assigned problems will not be handed out or posted. Those who do not come prepared will only have a superficial knowledge of the material and will not have a basis for good participation. Your preparation deepens your knowledge, your ability to identify tax issues in a client situation from that knowledge and your understanding and ability to explain these tax issues -- your tax skills.

Classroom contribution evaluation will be based on class participation in presenting and discussing assigned problem material. The classroom performance component of the evaluation is an essential requirement of the course and will not be waived.

AFM 461: Taxation II 7 Fall 2012

Demonstrated effort, rather than correctness, will be the basis of evaluating this component of the course. Everything needed to prepare, including sample solutions, can be found in the textbook and accompanying study guide.

Students will be required to sit in the same seat, according to a seating plan, for each class, and to display a name card for participation identification purposes.

Switching sections during a class day will not be permitted, given the size of the classes. Participation will only be recorded in the section in which the student is registered. No excuse for switching is valid. Hence, appointments and meetings of various kinds and interviews should not be scheduled during a class that the student is expected to attend.

RECORDING OF LECTURES

The SAF recognizes that recording (e.g., audio, video) a class for the purpose of private study may be a useful learning tool. Any student wanting to record (in whole or part) a lecture is required to seek the consent of the instructor before doing so and the instructor may, at her/his discretion, withhold consent. Where recording is required as part of disability accommodation, as a matter of professional courtesy the instructor should be advised and completion of appropriate Office of Persons with Disabilities paperwork typically achieves this purpose. In the event that consent is provided by an instructor, unless otherwise stated in writing, the consent for recording is strictly limited to the purpose of private/personal study and for no other reason (i.e., loaning the recording or reproducing a copy for another student, contesting grading, posting in whole or part online, etc.). Any failure to abide by these requirements will be treated by a course instructor and the SAF as a misuse of intellectual property and a violation of the university's academic integrity requirements and dealt with accordingly.

USING LEARN

We will be using LEARN to administer the course, record group selection, post announcements between classes, record grades and post materials for class. You should check LEARN on a daily basis.

PROFESSIONALISM AND RELATED UNIVERSITY POLICIES

Internet Access During Classes

Students are asked to refrain from connecting to or accessing the Internet during class time (including email), unless discussed in advance with the course professor. This includes connecting to the Internet via a portable computer or any hand-held device. Thank you for your co-operation.

Academic Integrity

In order to maintain a culture of academic integrity, members of the University of Waterloo community are expected to promote honesty, trust, fairness, respect, and responsibility.

AFM 461: Taxation II 8 Fall 2012

Academic Integrity Office (UW): www.uwaterloo.ca/academicintegrity/ Academic Integrity (Arts): http://arts.uwaterloo.ca/current-undergraduates/academic-responsibility

Grievance

A student who believes that a decision affecting some aspect of his/her university life has been unfair or unreasonable may have grounds for initiating a grievance. Read Policy70, Student Petitions and Grievances, Section 4, www.adm.uwaterloo.ca/infosec/Policies/policy70.htm.

Discipline

A student is expected to know what constitutes academic, to avoid committing an academic offence, and to take responsibility for his/her actions. A student who is unsure whether an action constitutes an offence, or who needs help in learning how to avoid offences (e.g., plagiarism, cheating) or about “rules” for group work/collaboration should seek guidance from the course instructor, academic advisor, or the Undergraduate Associate Dean. When misconduct has been found to have occurred, disciplinary penalties will be imposed under Policy 71 – Student Discipline. For information on categories of offences and types of penalties, students should refer to Policy 71 - Student Discipline, www.adm.uwaterloo.ca/infosec/Policies/policy71.htm.

Appeals

A student may appeal the finding and/or penalty in a decision made under Policy 70 - Student Petitions and Grievances, (other than regarding a petition) or Policy 71 - Student Discipline if a ground for an appeal can be established. Read Policy 72 - Student Appeals, www.adm.uwaterloo.ca/infosec/Policies/policy72.htm

Academic Offenses and Implications

Students majoring in accounting programs at UW should be aware that, due to the highly structured nature of the study plans and the fact that many AFM courses are offered on a limited basis, a penalty imposed as a result of an academic offence could result in a significant delay of the student’s degree completion and convocation dates - particularly if the penalty involves a suspension.

Avoiding Academic Offences

The Faculty of Arts has prepared a website dealing with ways to avoid academic offences. http://arts.uwaterloo.ca/arts/ugrad/academic_responsibility.html

Violation of Standards by Another Student

Allowing another student to obtain course marks by deceit contributes to a general lowering of the ethical standards of the University and contributes to deception of potential employers and other academic institutions. Thus, you have an obligation to take some action when you know another student is violating the course's academic integrity standards. This is a difficult personal

AFM 461: Taxation II 9 Fall 2012

trial to face, but it is an important part of your ethical obligation as a student. If you know that another student is violating the standards, it is your responsibility to inform the student's instructor. This requirement closely parallels those found in the standards of conduct of all of the professional accounting bodies in Canada (see, for example, the Institute of Chartered Accountants of Ontario, Rules of Professional Conduct, section 211).

Note for Students with Disabilities

The Office for Persons with Disabilities (OPD), located in Needles Hall, Room 1132, collaborates with all academic departments to arrange appropriate accommodations for students with disabilities without compromising the academic integrity of the curriculum. If you require academic accommodations to lessen the impact of your disability, please register with the OPD at the beginning of each academic term.

Turnitin

Plagiarism detection software (Turnitin) will be used to screen assignments in this course. This is being done to verify that use of all materials and sources in the assignment is documented. In this course outline, details are provided about the arrangements for the use of Turnitin in this course as follows:

• you will submit your assignment to Turnitin through LEARN for screening, unless you indicate that you do not wish to have that done;

• if you choose not to have your assignment screened by Turnitin, an alternative arrangement will be made in advance of any submission. The alternative could include your providing an annotated bibliography for all references used and/or providing an original copy of all rough drafts of the assignment, along with the version submitted.

AFM 461: Taxation II 10 Fall 2012

CLASS SCHEDULE

Class Date Topic Readings Exercises1 Problems

1 Sept. 8 •Introduction and Review of Major Concepts from AFM361

2 Sept. 10 •Review of corporate taxable income and tax calculations

Preface to text and study guide

Ch. 4: as needed

Ch. 11: as needed

Ch. 11: 7-9, 11

Ch 11: 8 11

3 Sept. 15 •Integration.

•Association.

Ch. 12: ¶ 12,000 – ¶ 12,210

Ch. 12: 2-5 Ch. 12: 9,10

4 Sept 17 •Income from an active business of a CCPC.

Ch. 12: ¶ 12,220 – ¶ 12,230

Ch. 12: 1, 6-11

Ch. 12: 13

5 Sept 22 •SR&ED.

•Refundable taxes & dividend refund.

Ch. 12: ¶ 12,240 – ¶ 12,405

None Ch. 12: 14, 16

6 Sept. 24 •Tax calculation for CCPC.

•Income from investments of a CCPC.

Ch. 12: ¶ 12,500 None Ch. 12: 19, 20

7 Sept. 29 •Shareholder-manager remuneration; loans.

Ch. 13: ¶ 13,000 – ¶ 13,100

Ch. 13: 1-8 Ch. 13: 9

8 Oct 1 • Salary vs. dividends.

• Qualified small business corporation shares.

Ch. 13: ¶ 13,200 – ¶ 13,355

Ch. 13: 9 Ch. 13: 13, 1

9 Oct. 6 Computation of CGE.

Corporate attribution.

Ch. 13: ¶ 13,360 – ¶ 13,600

Ch. 13: 10-12

Ch. 13: 3,4,5

1 Solutions to Exercises can be found in the Study Guide that accompanies the text. Exercises will not be covered in class and are listed as self-study aids to clarify a student’s understanding of material covered in Problems.

AFM 461: Taxation II 11 Fall 2012

Income-splitting tax

GAAR.

10 Oct. 8 •Corporate surplus balances.

•Use of corporate surplus balances.

Ch. 15: ¶ 15,000 - ¶ 15,180

Ch. 15: 1-5 Ch. 15: 2, 3, 4

11 Oct. 15 (no class Oct. 13)

•Winding-up of a Canadian corporation.

•Sale of an incorporated business.

•GST and the winding-up of a corporation

Ch. 15: ¶ 15,200 – ¶ 15,240

Ch. 15: 6-8 Ch. 15: 6

12 Oct. 20 Asset vs. share sale.

Ch. 15: ¶ 15,300 – ¶ 15,400

None Ch. 15: 9

13 Oct. 22 •Transfer of property to a corporation (Section 85).

•

Ch. 16: ¶ 16,000 – ¶ 16,110

Ch. 16: 1-7 Ch. 16: 1, 3

14 Oct 27 Transfer of property to a corporation (Section 85).

Ch. 16: ¶ 16,120 – ¶ 16,190

None Ch. 16: 4

15 Oct 29 •Review Session

MIDTERM EXAMINA

TION: Thursday

October 30, 2014

– 6:30 – 8:30 PM

•16 Nov 3 • Transfer of

shares.

Section 84.1. dividend strips.

Section

Ch. 16: ¶ 16,200 – ¶ 16,255

Ch. 16: 8-10 Ch. 16: 7, 9 (Plan A)

AFM 461: Taxation II 12 Fall 2012

55 capital gains strips.

17 Nov 5 • Transfer of shares.

Section 84.1 dividend strips.

Section 55 capital gains strips.

Ch. 16: ¶ 16,200 – ¶16,255 as needed

None Ch. 16: 8, 9 (Plan B)

18 Nov 10 • Rollovers involving corporations and shareholders-Section 85.1.-Section 86.

Ch. 17: ¶ 17,000 – ¶ 17,060

Ch. 17: 1-3

Ch. 17: 1, 2 (Pkg. (a))

ASSIGNMENT #1 DUE: Wednesday November 12, 2014

• Due in designated drop box and uploaded to Turnitin before 8:30 AM

19 Nov 12 • Statutory amalgamations.

• Winding up a subsidiary.

Ch. 17: ¶ 17,070 – ¶ 17,140

Ch. 17: 4

Ch. 17: 2 (Pkg. (b)), 4, 5

20 Nov 17 • Rollovers involving shares or securities.

• Use of rollovers in estate freezing.

Ch. 17: ¶ 17,200 – ¶ 17,340

Ch. 17: 5

Ch. 17: 6

ASSIGNMENT #2 DUE: Wednesday November 26, 2014

• Due in designated drop box and uploaded to Turnitin before 8:30 AM

21 Nov 19 • Partnerships. Ch. 18: ¶ 18,000 – ¶ 18,100

Ch. 18: 1,2

Ch. 18: 1, 4

22 Nov. 24

•Trusts. Ch. 18: ¶ 18,200 – ¶ 18,310

Ch. 18: 3

Ch. 18: 5, 6, 7

ASSIGNMENT #3 DUE:

AFM 461: Taxation II 13 Fall 2012

Monday December 1, 2014•Due in designated drop box

and uploaded to Turnitin before 8:30 AM

23 Nov. 26

•Obligations of the taxpayer under the ITA.

•Powers and obligations of CRA.

• Rights of the taxpayer.

Ch. 14: ¶ 14,000 – ¶ 14,220

Ch. 14: 1-5, 8-12

Ch. 14: 5, 6, 8

24 Dec. 1 •Obligations of payers.

•Deceased taxpayers.

•Obligations of the registrant under the Excise Tax Act.

Ch. 14: ¶ 14,300 – ¶ 14,700

Ch. 14: 6,7, 13

Ch. 14: 13

AFM 461: Taxation II 14 Fall 2012

AFM 461: Taxation II 15 Fall 2012

ASSIGNMENT REQUIREMENTS AND CASE

Concept: This assignment must be based on the practical tax case presented below.

Groups: The assignment must be completed in self-selected groups of five (5). Groups can be formed with students in any section of the course. You are responsible for forming a group. The first page of the report should identify the group number, all students’ names and student nubmers included in the group with their section numbers.

Groups must be formed on or before September 29 using the LEARN system.

Structure: You are to prepare three (3) reports as set out below. Please use point form in any written memorandum.

Report 1: Due Date: *** November 12, 2014 in the designated drop box and uploaded to Turnitin before 8:30 a.m. ***

A planning memorandum to your small business advisory partner (5 pages, single-spaced (maximum) written memorandum plus maximum 4 pages of tables and/or appendices providing calculations). This memorandum will contain your detailed steps that should be taken to meet your client’s objectives including the reasons for the steps proposed. The analysis should be at a reasonably detailed level at this stage so the legal and tax work can be done by the January 1, 2015 implementation date.

This memorandum should clearly identify each of the following:• Key facts (summarized, as necessary, recognizing that details are outlined in

the case statement) and assumptions• issue(s) clients’ objectives addressed•• advice/conclusions• technical analysis to support advice/conclusion demonstrating a logical

approach at a conceptual level with direct reference to your research sources• any information required to implement the proposed steps

Appropriate research sources are suggested in the Reference List on this course outline. The textbook is a good resource to assist you in identifying issues and focusing your research but is not considered a research source. Research sources must be acknowledged and documented in footnotes where used.

Report 2: Due Date: *** November 26, 2014 in the designated drop box and uploaded to Turnitin before 8:30 a.m. ***

Based on the suggested solution to Report 1 that will be provided on November 12, 2014 and additional information provided with the suggested solution, the client will implement the steps proposed in that solution on January 1, 2015 and the ensuing

AFM 461: Taxation II 16 Fall 2012

days. You are to prepare detailed calculations for any elections required to effect the plans and calculate taxes payable (federal and provincial) for any taxpayers that will need to file tax returns for the 2015 tax year as a result of the completion of the steps proposed in the suggested solution. This will allow the small business advisory partner to review the detailed tax implications of implementing the plan proposed in Report 1 with the client.

You are to assume that all tax rates, tax brackets, and tax credits and deduction limits for 2015 are the same as 2014 and that no additional sources of income or additional expenses will arise in 2015 that did not exist in 2014. In addition, assume that the business has the same accounting net income, depreciation and meals and entertainment expenses in 2015 that were used in the proforma results presented for 2014 and no new capital assets are purchased in 2015 by the consulting business.

Report 3: Due Date:*** December 1, 2014 in the designated drop box and uploaded to Turnitin before 8:30 a.m. ***

Based on the suggested solution to Report 1 that will be provided on November 12, 2014 and additional information provided with the suggested solution, you will prepare a memo to your small business advisory partner (2 pages, single-spaced (maximum) written memorandum plus maximum 9 pages of tables and/or appendices providing calculations) concerning the potential sale of her business assets on January 1, 2020. That is, 5 years have elapsed since the proposed plan was implemented and the client has received an offer to buy the business assets from a Canadian public company with operations in the same province as Engineerco and whose weighted average cost of capital is 10%. There have been no changes in ownership of the shares of the companies since the plan was effected in 2015 and no dividends have been paid to the shareholders during this period. You will be provided with the sale information on November 12, 2014.

Your memo should indicate the net proceeds that will be available to your clients personally after the proposed sale in 2020.

The memo should also include any issues surrounding the potential sale of the business assets and any alternatives for the client to consider taking to the potential buyer of the business.

You are to assume the following in preparing this report (do not restate these assumptions in your report):a)all tax rates, capital gains inclusions rates, tax brackets, and tax credits for 2020 are the same as 2014;b)Shannon and Noah will be in the highest tax bracket in 2020 before considering the effects of this sale;c)you are to assume that neither Noah nor Shannon have ever had any transactions (except for the reorganization activities undertaken in 2015);d)there will have been no share transactions or dividends paid after the completion of the reorganization plan implemented in 2015 as per Report 1.

AFM 461: Taxation II 17 Fall 2012

e)in the companies, the only capital transactions aside from normal purchases of depreciable properties from 2015 to 2020 was the sale of a capital property which yielded a capital gain of $80,000 in Engineerco in 2017;f)none of the companies in the group has ever had a GRIP balanceg)the balance sheets of the companies have been stable since the implementation of the plan in 2015 except that any cash retained after paying all expenses including normal debt repayments and shareholder salaries was used to pay down Realco’s bank debt

Grading: The submissions will be graded based on the following:• the quality of the research• the quality of the analysis and conclusions/recommendations• the quality of the reports (format, grammar, sentence structure, proper footnoting,

correct citing of the Income Tax Act, tax cases, etc.).

AFM 461: Taxation II 18 Fall 2012

Format Requirements:

Assignments that do not adhere to the following requirements will not be graded.

(a) Times New Roman 12 pt. font

(b) Technical memo double-spaced; client letter single-spaced

(c) Numerical charts/tables may be single-spaced and may utilize Times New Roman 10 pt font. The smaller font size applies only to the numeric aspect in the table and does not apply to related footnotes.

(c) 1" margins (left, right, top and bottom)

(d) References must be footnoted on the particular page of use. Footnotes must conform to the 12 pt font requirement and be used for reference purposes only. Footnotes should not be used as a substitute for regular text.

(e) One, corner-stapled, paper copy (i.e., no covers), per group per assignment

(f) Upload one Microsoft Word file per group to Turnitin in the designated drop box on LEARN and record your paper ID number

NOTE: Assignments which are not submitted by the due date and time will not be graded as the assignments will be taken up on the due date of each assignment in the classes those days.

All members of a group are assumed to make an equal contribution to the final product that is submitted. It is the responsibility of the group to ensure that this assumption is valid.

AFM 461: Taxation II 19 Fall 2012

The Case

It is September 19, 2014 and your small business advisory partner, Kane Daniel, just came into your office asking you to start on an engagement for an old acquaintance. Your firm has been engaged to provide a high level assessment of this client’s current financial and tax situation and proposed steps to address the client’s objectives and priorities.

He provided you with the following background from his recent meeting with Shannon Ivy, a lady with whom he went to high school and hadn’t seen for 20 years before running into her at his high school reunion during the summer.

Shannon is 45 years old and married to Noah Ivy, and they have no children.

Shannon has a successful engineering consulting firm that she runs as a proprietorship. All of the firm’s customers are based in Ontario. The firm will have $10 million of revenue in 2014 and it has 24 employees. The proprietorship rents the land and building that houses its offices and pays $150,000 of annual rent. Shannon has been offered the chance to buy the property for $1.2 million. She would very much like to buy this property as it is a perfect fit for her business and she believes it will continue to increase in value in the future, but is wary about taking on debt to do so. The firm’s bank has indicated it would definitely lend the money to fund the entire purchase price and any transaction costs. The bank has indicated that the rate would be at Canadian Prime +1% (currently Prime is 3%), with minimum repayments of $10,000 per month and security including the property, the firm’s future cash flow and Shannon’s personal guarantee since this is a proprietorship. Additional payments on the loan could be made at any time at the borrower’s option.

Shannon owns a corporate bond with a face value of $500,000 that pays 10% per year every July. The bond is due in July 2017 and cannot be cashed or sold before then. Shannon earns $100,000 per year as a director of the Engineering Society of Ontario. Kane has provided you with a proforma estimate of Shannon’s tax return for 2014 (see Exhibit One) based on his discussions with Shannon.

Shannon just paid off her home mortgage for the home that she lives in with Noah (value of the home is currently $2 million) and was wondering what she would do with her cashflow from the business now that she has paid off her house. The house is in her name as she has paid all of the expenses for it since she bought it 20 years ago. She has paid off this debt as quickly as possible since she hates debt.

Noah has never had a job. He has always done all the administration for the consulting firm, but has never been paid by the business. Shannon always liked reducing her tax bill by claiming Noah as a dependent on her tax return based on the her bookkeeper’s

AFM 461: Taxation II 20 Fall 2012

explanation of her tax return. Shannon and Noah have a neighbour that has a job similar to what Noah does and makes $75,000 per year. Shannon very much is a control freak and likes to make sure she has the last word on all things to do with the business.

Shannon has RRSP’s currently valued at $750,000, and she always makes her maximum RRSP contribution every February in advance of the RRSP deadline for the prior tax year. Noah does not have an RRSP. Neither Shannon nor Noah have a pension plan or any other retirement and/or savings assets. Retirement is something Shannon and Noah have begun to discuss a lot recently after the death of both their parents. Shannon would like to exit the business in 10 years so she can enjoy the “finer things at a leisurely pace” with Noah. Shannon would very much like to make saving for retirement a high priority in their lives starting next year.

In addition to hating debt, Shannon hates paying more taxes than is absolutely necessary. Another high school friend, who runs a small bookkeeping service, has been doing Shannon’s accounting and tax return every year since Shannon left university and started her small consulting business at the time. Every year when she has to write very large cheques to the Canada Revenue Agency, Shannon wonders if she needs to be paying all the tax she is, and if there are better ways she can be saving for a tax effective retirement and buying the office land and building. She has never done any financial or tax planning as that was not an area her accountant knew well, and Shannon did not want to take the time to start a relationship with another accounting firm.

Now that the house has been paid off, Shannon estimates that she and Noah will need $200,000 after tax to live in their current lifestyle.

Additional information and assumptions for 2014 and later years

Provincial corporate tax rate on Active Business Income eligible for small business deduction-5%

Provincial corporate tax rate on Income not eligible for small business deduction-14%

Use the federal and provincial personal tax rates in Exhibit Two belowUse the 2014 dividend gross up and tax credits for all analyses in this case

Exhibit One

2014 Proforma Personal Tax Return for Shannon Ivy

AFM 461: Taxation II 21 Fall 2012

3(a) Employment Income 100,000

Business income (note 1) 433,200

Interest income 50,000

583,200

Less:rrsp deduction (24,270)

3 c income =division b income = taxable income 558,930

Federal and provincial tax before credits 240,183

Non-refundable credits:

Basic personal 11,138

Spousal credit 11,138

CPP credit 2,456

EI credit 914

Canada Employment credit 1,127

Total base 26,743

Non-refundable credits @ 25% (6,686)

Total taxes payable for the year 233,497

Note 1:

Reconciliation of 2014 Business Income for Tax Purposes

Net income for accounting 410,,000

Add: depreciation for accounting 60,000

Non-deductible meals and entertainment 20,000

Less: CCA (below) (56,800)

Net income for tax 433,200

AFM 461: Taxation II 22 Fall 2012

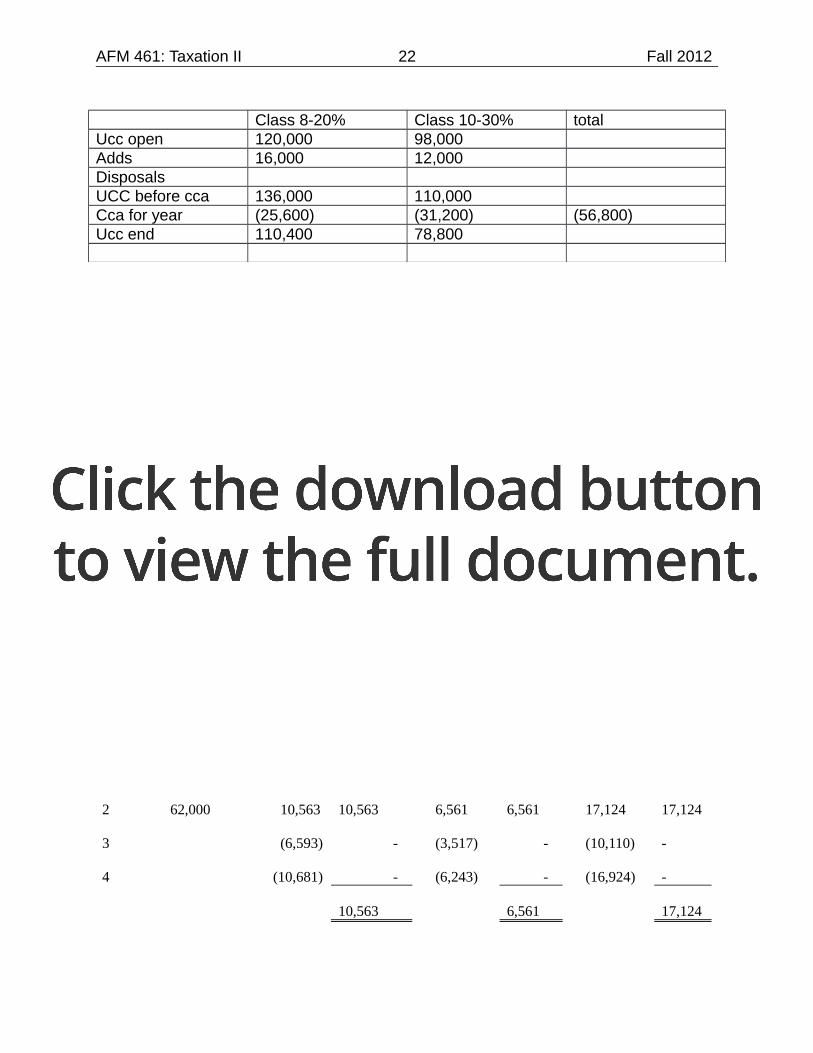

Class 8-20% Class 10-30% totalUcc open 120,000 98,000Adds 16,000 12,000DisposalsUCC before cca 136,000 110,000Cca for year (25,600) (31,200) (56,800)Ucc end 110,400 78,800

Exhibit Two

2014 Tax Calculations

Federal Tax Provincial Total

Tax on Tax rate Tax onTax rate Tax on

Tax rate

Taxable Incomelower limit on excess

lower limit

on excess

lower limit

on excess

- 43,953 - 15% - 10% - 25%

43,954

87,907 6,593 22%

4,395 12%

10,988 34%

87,908

136,270 16,263 26%

9,669 15%

25,932 41%

136,271 28,837 29%

16,923 17%

45,760 46%

Bracket 1 - - - 2

62,000 10,563

10,563

6,561

6,561

17,124

17,124

3 (6,593) -

(3,517) -

(10,110)

-

4 (10,681) -

(6,243) -

(16,924)

-

10,563

6,561

17,124

AFM 461: Taxation II 23 Fall 2012