school finance - tasbo

TRANSCRIPT

SCHOOL BUDGET

SCHOOL FINANCE

School Finance – TASBO Conference 2013

I. School District Total Revenue Sources (2011-2012 per State Report Card)

State Average

Your District

State 46.5% ?? % Local 39.2% ?? %

Federal 14.3% ?? %

School Finance – TASBO Conference 2013 2

State Funding Where does it come from?

Sales Tax

Mixed Drink Tax

Cigarette Tax (beginning July 1, 2007)

School Finance – TASBO Conference 2013 3

State Funding How is it determined?

Basic Education Program (BEP)

Formula that determines the funding level required for each school system to provide a common, basic level of service for all students.

School Finance – TASBO Conference 2013 4

BEP Funding Formula History Adopted by the Legislature in 1992 as part of the Education Improvement Act (EIA)

Developed in response to Small Schools I lawsuit, where TN Supreme Court ruled State’s previous school funding formula was inequitable

“Funding formula, not a spending plan”

School Finance – TASBO Conference 2013 5

BEP Funding Formula

Highlights

1. Comprehensive

2. Attempts to equalize state and local funding (fiscal capacity; cost differential factor)

3. Provides flexibility

4. Attempts to keep up with increased costs

School Finance – TASBO Conference 2013 6

BEP Funding Formula Comprehensive Formula contains a number of components

(45 total) that the Legislature has deemed necessary for schools to succeed.

School Finance – TASBO Conference 2013 7

BEP Funding Formula

Equalization

Formula determines actual state share of

education funding by each county’s relative

ability to pay or its

“FISCAL CAPACITY”

School Finance – TASBO Conference 2013 8

FISCAL CAPACITY County’s “ability to pay” based on:

Tax base (sales, property) Per capita income

Resident tax burden

Students relative to total population

Expressed as an index measure, which is a proportion of the total fiscal capacity for all counties

School Finance – TASBO Conference 2013 9

BEP Funding Formula Flexibility

School boards have broad flexibility

in determining how to allocate

state funds.

School Finance – TASBO Conference 2013 10

BEP Funding Formula Cost evaluation

BEP component costs are recalculated

and updated for inflation

each year.

School Finance – TASBO Conference 2013 11

BEP Funding Formula Inadequacies

Not enough teaching positions funded to meet class-size mandates as required by state law

High cost of educating English Learner (EL) students not recognized adequately

Teacher salaries still not adequately addressed

School Finance – TASBO Conference 2013 12

BEP Funding Formula Inadequacies

Teacher insurance not adequately addressed

School nurse ratio inadequate

Professional development for teachers not included

Technology not adequately funded

School Finance – TASBO Conference 2013 13

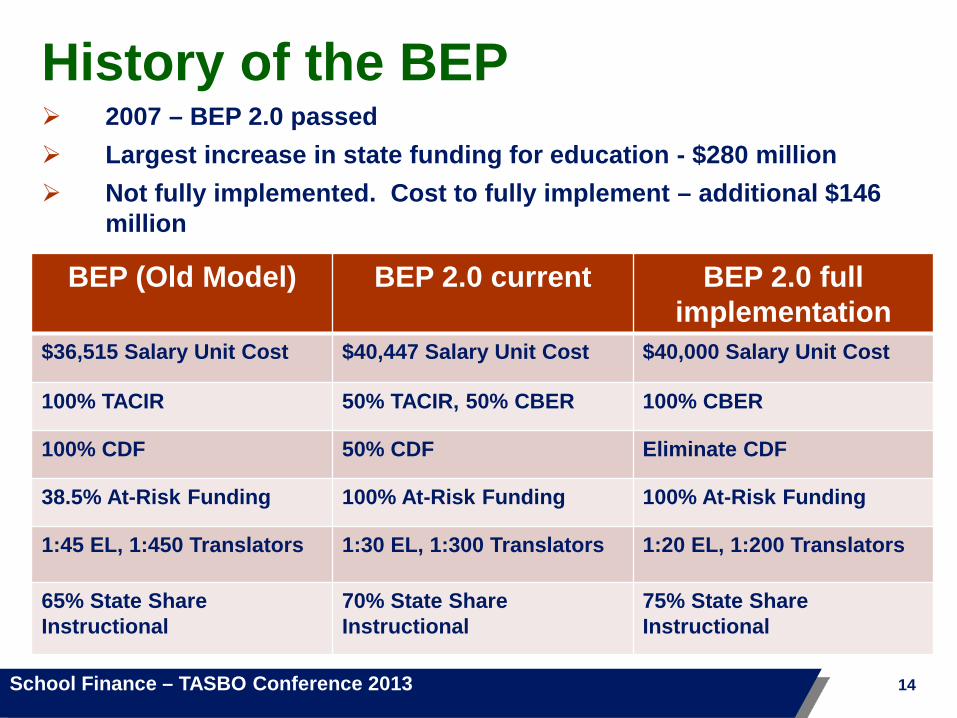

History of the BEP 2007 – BEP 2.0 passed Largest increase in state funding for education - $280 million Not fully implemented. Cost to fully implement – additional $146

million

BEP (Old Model) BEP 2.0 current BEP 2.0 full implementation

$36,515 Salary Unit Cost $40,447 Salary Unit Cost $40,000 Salary Unit Cost

100% TACIR 50% TACIR, 50% CBER 100% CBER

100% CDF 50% CDF Eliminate CDF

38.5% At-Risk Funding 100% At-Risk Funding 100% At-Risk Funding

1:45 EL, 1:450 Translators 1:30 EL, 1:300 Translators 1:20 EL, 1:200 Translators

65% State Share Instructional

70% State Share Instructional

75% State Share Instructional

School Finance – TASBO Conference 2013 14

BEP Unit Costs

ADMs

CDF Fiscal

Capacity

Salaries, Retirement, Insurance

BEP – many inputs

School Finance – TASBO Conference 2013 15

Instructional Classroom Non-Classroom Regular Education Vocational Education Special Education Elementary Guidance Secondary Guidance Elementary Art Elementary Music Elementary Physical Education Elementary Librarians (K-8) Secondary Librarians (9-12) ELL Instructors ELL Translators Principals Assistant Principals Elementary Assistant Principals Secondary System-wide Instructional Supervisors Special Education Supervisors Vocational Education Supervisors Special Education Assessment Personnel Social Workers Psychologists Staff Benefits and Insurance

K-12 At-risk Class Size Reduction Duty-free Lunch Textbooks Classroom Materials and Supplies Instructional Equipment Classroom Related Travel Vocational Center Transportation Technology Nurses Instructional Assistants Special Education Assistants Library Assistants Staff Benefits and Insurance Substitute Teachers Alternative schools Exit Exams

Superintendent System Secretarial Support Technology Coordinators School Secretaries Maintenance and Operations Custodians Non-instructional Equipment Pupil Transportation Staff Benefits and Insurance Capital Outlay

BEP Components (45) by Category

School Finance – TASBO Conference 2013 16

For further information… Tennessee Basic Education Program: An

Analysis http://www.comptroller1.state.tn.us/orea/ See the Legislative Brief

State Board of Education http://www.tn.gov/sbe/bep.html BEP Blue Book – up to date data on BEP components

http://www.tn.gov/sbe/BEP%20Booklet%20FY12.pdf

Recommendations of BEP Review Committee http://www.tn.gov.sbe/BEP%20November%201%202011%20Report%20-%20Final%20Draft.pdf

School Finance – TASBO Conference 2013 17

Local Funding

Where does it come from?

Property Taxes

•Assessed property values (Assessor of Property)

•Tax rate allocated for Schools

•Collection rate

•Value of penny on property tax rate

School Finance – TASBO Conference 2013 18

Local Funding

Where does it come from?

Local Option Sales Tax

Half of revenue must be appropriated to education

Other Sources (wheel tax, etc.)

School Finance – TASBO Conference 2013 19

Local Funding

Maintenance of Effort (TCA 49-2-203; TCA 49-3-314)

No local government can reduce its budgeted amount of local revenue for schools unless there is a decrease in student enrollment.

School Finance – TASBO Conference 2013 20

Local Funding

Fund Balance (TCA 49-3-352(c))

Any accumulated fund balance in excess of 3% of budgeted operating expenditures may be budgeted and expended for any purpose, but must be recommended by the Board of Education.

School Finance – TASBO Conference 2013 21

II. Budget Process

1. Planning

2. Approach

3. Calendar

School Finance – TASBO Conference 2013 22

Planning

Strategic Plan • District goals &

objectives (TCSPP)

• Individual schools’ SIP

Revenue Plan

Expenditure Plan

BUDGET TRIANGLE

School Finance – TASBO Conference 2013 23

Required Additional Expenditures

Labor (salaries & benefits) = over 80% of operating budget

•Health insurance

•Pension

•Salary steps

•Required state teacher raise

School Finance – TASBO Conference 2013 24

Required Additional Expenditures

Opening New Schools •Staff

•Utilities

•Materials & Equipment

School Finance – TASBO Conference 2013 25

Required Additional Expenditures Inflation

•Fuel

•Utilities

•Materials & Supplies

•Multi-Year Contracts

School Finance – TASBO Conference 2013 26

Calendar Develop/review goals, objectives

and needs assessment (Jan, Feb)

Develop draft budget, allow public input (March, April) – post on district website

Make any necessary revisions (May)

Vote on revised budget, present to governing body (June, July)

Send final certified copy of budget to State by August 1

School Finance – TASBO Conference 2013 27

Statistical Data District data (size of operation)

• # Employees (certificated / classified)

• # Years experience (25 yrs / 30 yrs)

• # Buildings (square footage / acreage / number of portables)

• # Buses (regular ed / special ed)

• # Students (ADM / ADA)

School Finance – TASBO Conference 2013 28

Statistical Data

State Report Card

• District

• Individual schools

State Data

• Expenditure per pupil calculation

• Other data (Annual Statistical Report)

School Finance – TASBO Conference 2013 29

SCHOOL FINANCE

THANK YOU! School Finance – TASBO Conference 2013 30