savills plcir.savills.com/~/media/files/s/savills-ir-v2/annual reports/company... · business...

TRANSCRIPT

Savills plc

Results for the six months ended 30th June 2017

10 August 2017

Disclaimer: Forward-looking statements

2

These slides contain certain forward-looking statements including the Group’s financial condition,

results of operations and business, and management’s strategy, plans and objectives for the Group.

These statements are not guarantees of future performance and are subject to risks, uncertainties and

other factors, some of which are beyond the Group’s control, are difficult to predict and could cause

actual results to differ materially from those expressed or implied or forecast in the forward-looking

statements. These factors include, but are not limited to, the fact that the Group operates in a highly

competitive environment. All forward-looking statements in these slides are based on information known

to the Group on the date hereof. The Group undertakes no obligation publically to update or revise any

forward-looking statements, whether as a result of new information, future events or otherwise.

Results

1 Introduction, Highlights & Business Development 2 Financial Review 3 Management Focus 4 Summary and Outlook

3

Highlights

4

Performance overview Drivers

Group Revenue£714.4m

+14.7% (cc 7.1%)

Group UPBT £48.1m

+12.4% (cc 5.1%)

Transaction advisory revenues up 15%,

reflecting strong performance throughout

Asia, Continental Europe and UK

Commercial market.

Property Management revenue up 13%,

Consultancy revenue up 15%.

Continued expansion in Europe and

North America, through bolt-on

acquisitions and recruitment.

Savills IM revenue growth of 22% and

underlying profits up 69%.

Group UEPS 25.7p

+17.9%

Net Cash £1.4m

(2016 H1: £34.7m)

Dividend 4.65p

+5.7%

cc = constant currency

Ten Year H1 Revenues

5

-

100

200

300

400

500

600

700

800

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

£m

Transactional "Less-Transactional"

44%

56%

Total Revenue

£399.0m

Total Revenue

£714.4m

63%

37%

Less-Transactional

Revenue £402.3m

Total Revenue

£278.1m

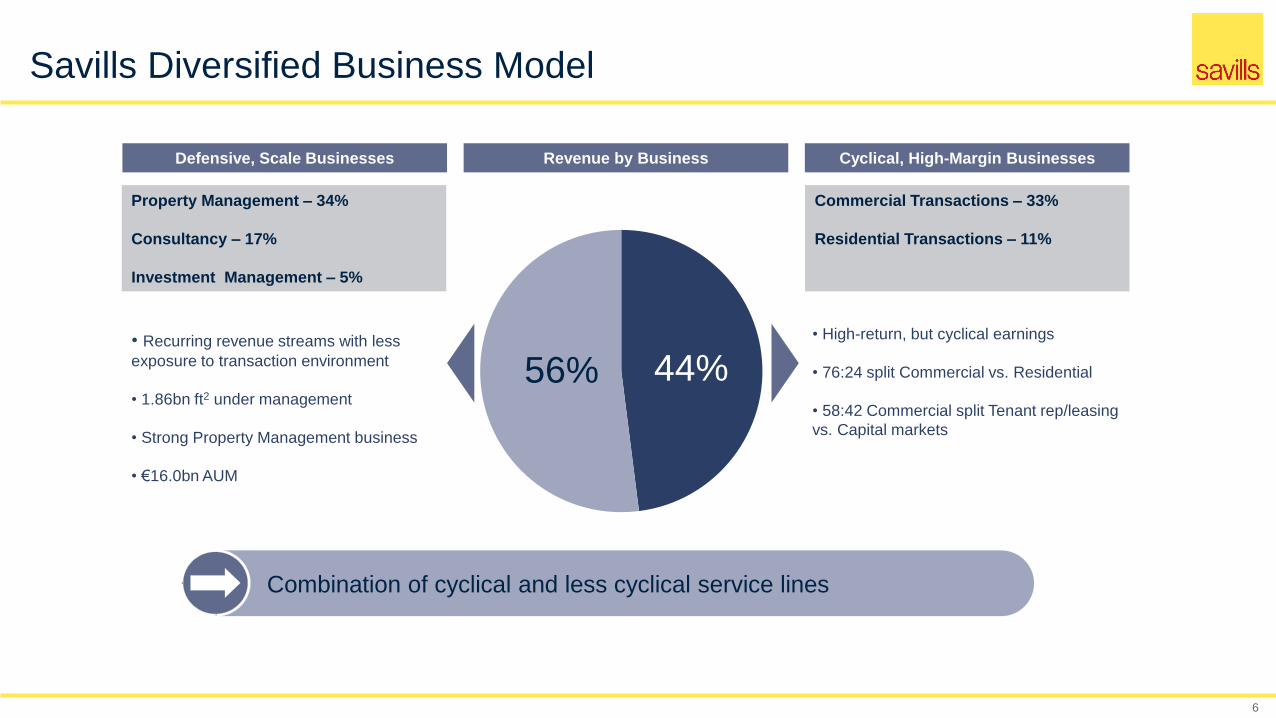

Savills Diversified Business Model

6

Defensive, Scale Businesses Revenue by Business Cyclical, High-Margin Businesses

Property Management – 34%

Consultancy – 17%

Investment Management – 5%

Commercial Transactions – 33%

Residential Transactions – 11%

• Recurring revenue streams with less

exposure to transaction environment

• 1.86bn ft2 under management

• Strong Property Management business

• €16.0bn AUM

• High-return, but cyclical earnings

• 76:24 split Commercial vs. Residential

• 58:42 Commercial split Tenant rep/leasing

vs. Capital markets

44%56%

Combination of cyclical and less cyclical service lines

Broad Geographic Spread

7

Over 31,000 employees in 700 offices in more than 60 countries

580Employees

5,442Employees

137Offices

1,118Employees

38Offices

26,501Employees

63Offices

Revenue

£103.6m

(14% of Total)

743Employees

30Offices

*Staff numbers –

weighted average

for 2017 H1

Revenue

£275.3m

(39% of Total)

Revenue

£72.0m

(10% of Total)

Revenue

£263.5m

(37% of Total)

Over 33,000* employees and over 600 offices in more than 60 countries

Recent acquisitions in Europe

8

Larry Smith (Italy)

Annual Revenue circa €7m

80 staff

Aguirre Newman (Spain / Portugal)

Annual Revenue circa €69m

(net €40m)

400 staff

Shows current offices of Aguirre Newman and Larry Smith. Savills has existing offices in Madrid, Barcelona and Milan.

Financial Review

9

Summary Underlying Result

10

6 months ended 30 June (£m) 2017 2016 % chg

Revenue 714.4 622.7 +14.7%

Underlying PBT 48.1 42.8 +12.4%

Underlying PBT margin 6.7% 6.9% (0.2)% pts

Underlying basic earnings per share 25.7p 21.8p +17.9%

Dividend per share 4.65p 4.40p +5.7%

Net cash 1.4 34.7 n/a

Net assets 382.8 346.7 10.4%

Revenue and underlying PBT by business

11

271.1

219.0

105.1

27.5

312.1

246.6

121.0

33.6

0

50

100

150

200

250

300

350

2016

2017

+13%

+15%

+22%

Revenue

23.3

10.28.2

3.9

24.6

10.2 10.2

6.6

0

5

10

15

20

25

30

0%+24%

+69%

Transaction

Advisory

Property

Management Consultancy

Investment

Management

UPBT

+15%

+6%

Margin 8.6% 7.9% 4.7% 4.1% 7.8% 8.4% 14.2% 19.6%

£m

The figures in these charts

exclude revenues of £1.1m

and other net costs of £3.5m

(2016-H1 £2.8m) not

allocated to the operating

activities of the group’s

business segments

Combined revenue and UPBT growth of 13% and 11% respectively

Revenue and underlying PBT by region

12

255.8

209.4

94.4

63.1

274.2263.5

103.6

72.0

0

50

100

150

200

250

300

2016

2017

Revenue

UK Asia Pacific North America

UPBT

+7%

Continental Europe

24.8

13.1

7.8

(0.1)

25.3

21.8

3.01.5

-5

0

5

10

15

20

25

30+2%

+26%

+10%

+14%

+66%

n/a

(62)%

£m

Margin 9.7% 9.2% 6.3% 8.3% 8.3% 2.9% (0.2)% 2.1%

The figures in these charts

exclude revenues of £1.1m

and other net costs of £3.5m

(2016-H1 £2.8m) not

allocated to the operating

activities of the group’s

business segments

Cashflow performance

13

188

1

48

1

4

79

70

1417

33

1450

50

100

150

200

250

Net cash at31-Dec-2016

UPBT Non-cashitems

Workingcapital

Acquisitionspend -

current &deferred

Capex Cash flowsfrom

investments

Purchase ofEBT shares

Dividendspaid

Tax Foreignexchange

Other Net cash at30-Jun-2017

£m

Cash used in operations of £35m

At 30 June 2017 - Net cash of £1.4m

At 30 June 2016 - Net cash of £34.7m

Commercial Transaction Advisory

14

2017 Revenue £237.0m (+20%) 2017 UPBT £16.3m (+26%)

North America subdued capital markets and reduction in leasing activity in Chicago, New York and

Washington DC. Capital Markets and other team hires increased cost base short term.

Europe revenue growth across the region, in particular France and Germany. New start-ups in Czech Republic

and Luxembourg impacting cost base.

UK significant growth in Investment and Development revenue.

Asia Pacific strong growth in revenues in Hong Kong, Japan and Australia. Increasing controls over export of

Chinese capital

67.6

39.4

26.4

103.6

-

20

40

60

80

100

120

Asia Pacific UK Europe North America

Growth +39% +23% +18% +10%

9.7

4.5

(0.9)

3.0

(2)

-

2

4

6

8

10

12

Asia Pacific UK Europe North America

Growth +169% +67% n/a (62)%

Residential Transaction Advisory

15

2017 Revenue £75.1m (+2%) 2017 UPBT £8.3m (-20%)

UK second-hand sales broadly flat despite declining market volumes. Some currency underpin for international

buyers

UK new development sales reduced reflecting fewer exchanges and lower average unit values; but good

pipeline of reservations.

Asia Pacific strong growth in Hong Kong primary and secondary markets; further cooling measures in Hong

Kong

20.1

55.0

0

10

20

30

40

50

60

Asia Pacific UK

Growth +23% -4%

2.9

5.4

-

1

2

3

4

5

6

Asia Pacific UK

Growth -3% -27%

Property Management

16

2017 Revenue £246.6m (+13%) 2017 UPBT £10.2m (2016 H1: £10.2m)

Asia Pacific revenue growth in Hong Kong, China and Korea.

UK strong revenue growth in Residential lettings and Commercial property management.

Europe revenue growth in the Netherlands and Ireland.

150.4

76.2

20.0

-

20

40

60

80

100

120

140

160

Asia Pacific UK Europe

Growth +18% +3% +16%

6.2

5.0

(1.0)(2)

(1)

-

1

2

3

4

5

6

7

Asia Pacific UK Europe

Growth (2)% +2% n/a

Consultancy

17

2017 Revenue £121.0m (+15%) 2017 UPBT £10.2m (+24%)

UK strong performances in building & project consultancy and hotels & leisure.

Asia Pacific valuation growth in Australia, China and Hong Kong.

Europe lower revenues in Germany and the Netherlands offsetting growth elsewhere in Europe.

91.6

22.1

7.3

0

10

20

30

40

50

60

70

80

90

100

UK Asia Pacific Europe

Growth +13% +35% -4%

8.0

2.6

-0.4

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

UK Asia Pacific Europe

Growth +11% +1,200% n/a

Investment Management

18

2017 Revenue £33.6m (+22%) 2017 UPBT £6.6m (+69%)

Positive impact of Transaction fees on Fund disposals; but pure management fees still represented 67%

of revenue

Capital raising slightly ahead of H1 2016 at €0.8bn and €3.0bn transacted (H1 2016: €1.0bn)

Assets under management reduced through disposals to €16.0bn (2016-H1: €17.1bn), slightly higher

than forecast at this stage of the programme.

12.0

18.3

3.3

-

2

4

6

8

10

12

14

16

18

20

UK Europe Asia Pacific

Growth

2.4

3.8

0.4

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

UK Europe Asia Pacific

Growth+16%+3% +192%-8%n/a n/a

Management Progress

19

Integrate new acquisitions: Aguirre Newman and Larry Smith

Develop the New York Capital Markets team

20

Continue to invest and grow Property Management and Consultancy

Expand Savills Investment Management’s platform

Management Focus

Review new markets – India

A strong H1 despite some uncertain markets, but with positive currency effect

Results again demonstrate the breadth and depth of the business, both by geography and business sector

21

The Board’s expectations for the full year remain unchanged

Summary and Outlook

Connecting people and

property since 1855