saudi economic outlook 2018 - aljaziracapital.com.sa · march 2018 2 all rights reserved please...

TRANSCRIPT

March 2018

1 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

Executive Summary

For the Kingdom of Saudi Arabia (KSA), 2017 proved to be an eventful year, as the plan for the way forward

was formulated. It is projected that 2018 would mark the start of the execution and implementation

process for the major reforms laid out in 2017. All these efforts would eventually push the nation closer to

‘Vision 2030’.

The 2018 budget focuses on non-oil expansion, reflected in the form of higher capital allocations for non-

oil sectors such as transport, construction, and utilities. The economy is also marching toward privatization,

as the government announced several reforms to lure private players, including a SAR 72bn stimulus with

a focus on housing, exports, and manufacturing.

The three pillars driving ‘Vision 2030’ are listed below. The government’s major reforms, announced until

2017, revolve around these very pillars.

• Fiscal outlook: The target to achieve the fiscal balance has been pushed to 2023 from 2020, while

subsidy rationalization will continue this year. The government had increased prices of some fuels as of

December 31, 2017. It may announce additional price hikes in the near future to remain on track with

its fiscal roadmap. By unveiling the largest budget in the Kingdom’s history, the government has clearly

indicated its aggressive expansion plans. GDP growth slowed in 2017, largely driven by a decline in the

oil sector’s contribution. However, non-oil sector seems to be the rescue gate as the GDP growth in the

near future will increasingly depend on it, especially with the introduction of several new taxes and

levies.

• Capital market: The Saudi equity market is likely to benefit from generous government spending in 2018,

in terms of capital and current expenditure (in the form of special allowances). Increased expectations

of KSA’s inclusion in MSCI and FTSE indices in 2018 are set to attract foreign institutional investors to

domestic equity markets. Moreover, the probable listing of Aramco in 2018 could be a landmark event.

• Reforms leading to social integration: The Kingdom took a major stride forward socially by allowing

Saudi women to drive and be a part of sports and other forms of entertainment initiatives, starting 2018.

Moreover, the Kingdom is expected to begin issuing tourist visas to foreign travelers and allow cinema

halls to open this year. These progressive reforms will bring Saudi women into the economic fold and

boost the tourism, automobile and entertainment sectors.

Overall, 2018 signals good news for the Saudi Arabian economy, starting with generous government

spending after last year’s constraints. The government is now working positively toward its fiscal target.

Simultaneously, the adverse impact of price increases on consumption will be partially subdued by

government allowances and aids in the form of beneficial policies, made possible by higher crude oil prices.

Capital markets are set to outperform if the announced capital/current expenditure is realized and probable

inclusions materialize. Moreover, social reforms are expected to groom the economic environment that

could help the Kingdom transform from an oil-dependent nation into a diversified market for investors.

Head of Research

Talha Nazar +966 11 [email protected]

March 2018

2 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

2017: The Year Gone By........................................................................................................................ 3

Fiscal Outlook ...................................................................................................................................... 4

2018 Budget Key Highlights........................................................................................................................................ 4

Expenditure Plans........................................................................................................................................................... 4

Sector-wise Allocation................................................................................................................................................... 4

Revenues............................................................................................................................................................................ 5

Fiscal Deficit...................................................................................................................................................................... 6

Fiscal Policy....................................................................................................................................................................... 6

Economic Outlook.................................................................................................................................7

GDP Growth...................................................................................................................................................................... 7

Economic Sentiment...................................................................................................................................................... 8

Monetary Policy............................................................................................................................................................... 8

Inflation...............................................................................................................................................................................9

Credit Growth....................................................................................................................................................................9

TASI Outlook........................................................................................................................................10

Sectoral Performance...................................................................................................................................................10

Conclusion...........................................................................................................................................11

Contents

March 2018

3 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

2017: The Year Gone By

KSA announced its ambitious agenda of ‘Vision 2030’ in 2016. The foundation of major refurbishments was

laid in 2017. The decline in oil prices forced the Kingdom to rethink its economic strategy. The government

progressed toward privatizing key state assets and stimulating investments, which reportedly are a part of

its long-term plan to diversify the economy away from dependency on oil revenues.

KSA’s 2018 budget, its largest ever, contributed to the plans of broadening the economy’s base. The

government indicated this by increasing public spending and slowing of austerity.

Turnaround story: After a dramatic 2017, KSA is looking forward to a flourishing 2018. Most of last year saw

subdued growth, as oil prices were submissive. The government continued to tighten its grip on spending,

with expenditure for the first nine months of 2017 increasing only 0.4% YoY. Conversely, the private sector

held back on investments, which further reflected in credit growth. The economy advanced at a moderate

pace of 1.7% in 2016 and continued its weak momentum in the first half of 2017. However, the second half of

2017 witnessed a major turnaround in oil prices, which started moving up riding on supply-side constraints

such as continued OPEC production cut, a nationwide strike in Nigeria, the pipeline blast in Libya, the North

Sea pipeline outage, and shrinking US stockpiles. Moreover, the KSA government accelerated spending in

Q4 2017 (36% YoY increase), thus leading to the bullish Saudi budget forecast.

The unemployment rate for KSA nationals rose above the 12% mark and was expected to remain high for

several years amid low oil prices and the absence of upbeat recovery in non-oil growth.

Key reforms: In 2017, the authorities obliged to last year’s OPEC deal by reducing oil production and

introduced major reform initiatives. Although the Kingdom continued to face economic challenges in 2017,

its reforms and measures that were set in the fiscal balance agenda within Vision 2030 have demonstrated

a positive effect, contributing to an increase in non-oil revenues. Most of its fiscal consolidation efforts in

2017 were aimed at improvements in the short-to-medium fiscal outlook that was attained at the expense

of growth.

Revenue initiatives for 2017 were crucial with reforms such as adjustment of visa and municipality fees,

implementation of the expat levies, and application of excise tax on some products such as tobacco and

its derivatives, soft drinks, and energy drinks. In addition, the government introduced 5% value-added

tax (VAT) on most goods and services. Although the amount of revenue generated through VAT would

be modest, such steps have laid the foundation to move forward. The government further reduced fuel

subsidies, increased electricity tariffs and domestic oil prices.

Several capital market reforms took place in 2017 such as the launch of the Nomu parallel market,

reclassification of sectors, and introduction of the T+2 settlement cycle. In June 2017, MSCI added Tadawul

to a watchlist for potential inclusion in the MSCI Emerging Markets Index, which was a major milestone

and reflects the Kingdom’s significant progress in capital market reforms. The authorities also had plans to

enable foreign investors to participate in share floats, and introduce new rules to ease out the issuance of

debt securities.

Overall, the Kingdom continued to make progress in creating a stronger and more diversified economy by

building dependency on oil and non-oil sectors.

March 2018

4 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

440

180

135

10844

Compensation of Employees

Non-Financial Assets (Capital)

Social Benefits

Financing Expenses

334

228

133

85

49

3930 29

Military & Security

Municipality Services

Education

Economic Resources

438

206

143

95

65

Use of Goods and Services

Other Expenses

Subsidies

Grants

311

192147

105

89

5453 26

Health & Social Development

Public Administration

Public Programs Unit

Infrastructure & Transport

2017

2017

2018E

2018E

Source: Ministry of Finance – Budget Statement 2018

Source: Ministry of Finance – Budget Statement 2018

Fiscal Outlook

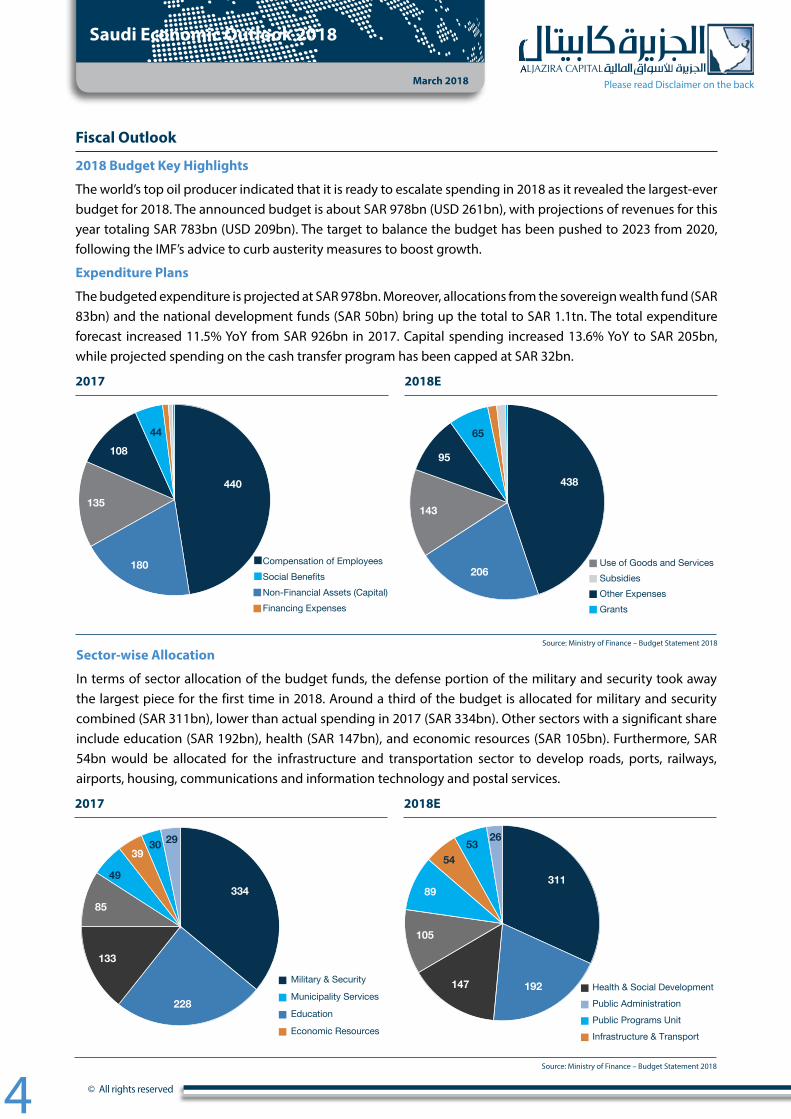

2018 Budget Key Highlights

The world’s top oil producer indicated that it is ready to escalate spending in 2018 as it revealed the largest-ever budget for 2018. The announced budget is about SAR 978bn (USD 261bn), with projections of revenues for this year totaling SAR 783bn (USD 209bn). The target to balance the budget has been pushed to 2023 from 2020, following the IMF’s advice to curb austerity measures to boost growth.

Expenditure Plans

The budgeted expenditure is projected at SAR 978bn. Moreover, allocations from the sovereign wealth fund (SAR 83bn) and the national development funds (SAR 50bn) bring up the total to SAR 1.1tn. The total expenditure forecast increased 11.5% YoY from SAR 926bn in 2017. Capital spending increased 13.6% YoY to SAR 205bn, while projected spending on the cash transfer program has been capped at SAR 32bn.

Sector-wise Allocation

In terms of sector allocation of the budget funds, the defense portion of the military and security took away the largest piece for the first time in 2018. Around a third of the budget is allocated for military and security combined (SAR 311bn), lower than actual spending in 2017 (SAR 334bn). Other sectors with a significant share include education (SAR 192bn), health (SAR 147bn), and economic resources (SAR 105bn). Furthermore, SAR 54bn would be allocated for the infrastructure and transportation sector to develop roads, ports, railways, airports, housing, communications and information technology and postal services.

March 2018

5 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

Growth%12.6

291

Non-Oil Revenues

Oil Revenues

Oil Revenues

Non-Oil Revenues

SAR Bn SAR Bn SAR Bn SAR Bn

492256440

2017 2018

Expected Revenues

Source: Ministry of Finance – Budget Statement 2018

Revenues

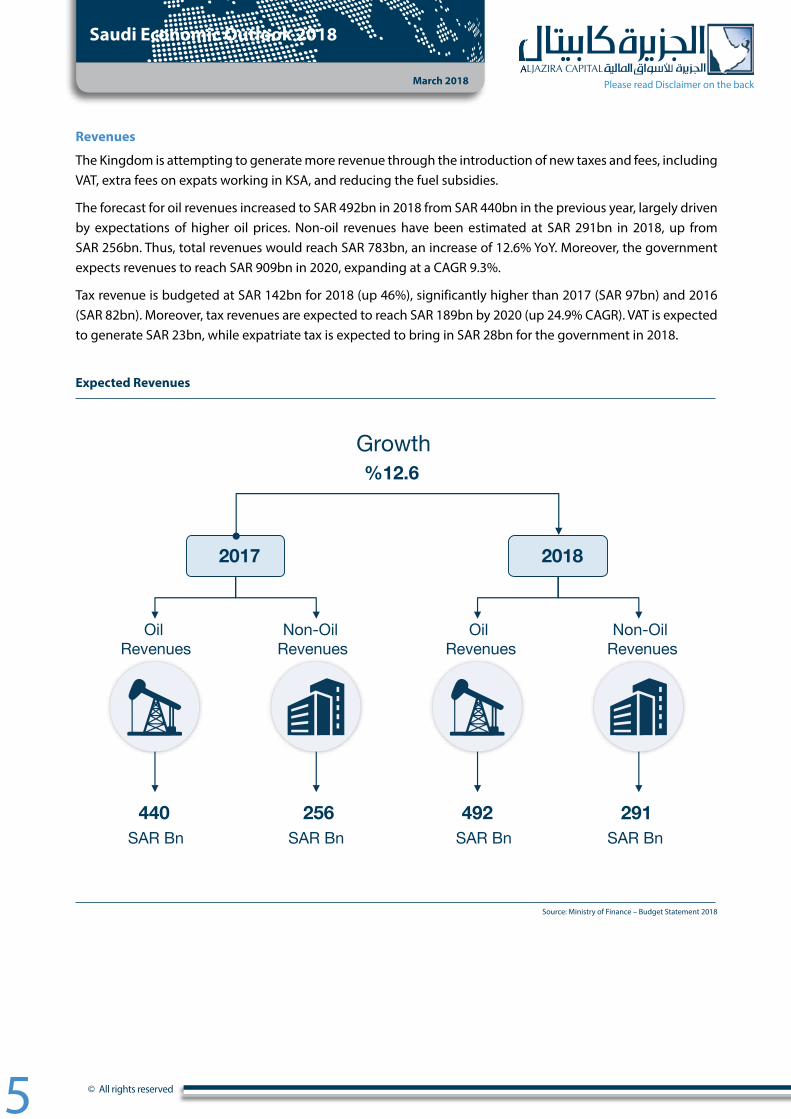

The Kingdom is attempting to generate more revenue through the introduction of new taxes and fees, including VAT, extra fees on expats working in KSA, and reducing the fuel subsidies.

The forecast for oil revenues increased to SAR 492bn in 2018 from SAR 440bn in the previous year, largely driven by expectations of higher oil prices. Non-oil revenues have been estimated at SAR 291bn in 2018, up from SAR 256bn. Thus, total revenues would reach SAR 783bn, an increase of 12.6% YoY. Moreover, the government expects revenues to reach SAR 909bn in 2020, expanding at a CAGR 9.3%.

Tax revenue is budgeted at SAR 142bn for 2018 (up 46%), significantly higher than 2017 (SAR 97bn) and 2016 (SAR 82bn). Moreover, tax revenues are expected to reach SAR 189bn by 2020 (up 24.9% CAGR). VAT is expected to generate SAR 23bn, while expatriate tax is expected to bring in SAR 28bn for the government in 2018.

March 2018

6 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

311-

230-195-

163-141- 125-

58-

4

350-

300-

250-

200-

150-

100-

50-

0

50

2016 2017 2018E 2019E 2020E 2021E 2022E 2023E

%50

%30

%12

%8

Oil Revenue

Debt

Government Balances

Non-Oil Revenues

Fiscal Balance (SAR bn)

Funding of 2018 Budget

Source: Ministry of Finance – Budget Statement 2018

Source: Ministry of Finance – Budget Statement 2018

Fiscal Deficit

With its revised target, the Kingdom now aims a deficit of SAR 195bn in 2018; down from SAR 230bn registered in 2017 (exceeds from planned deficit in 2017 budget of SAR 198bn). The higher deficit in 2017 came in despite several reforms being introduced by the government to drive non-oil revenues, rationalize expenditures, reduce the budget deficit and control public debt growth.

In 2018, the budget deficit is expected to reach 7.3% of the GDP, which is 1.6% lower than the budgeted deficit for 2017 and considerably lower than the 2016 budget deficit of 12.8% of the GDP. The decline in estimate is the result of a 12.6% rise in total revenues; however, this could be offset by a 5.6% increase in spending, including the 13.6% rise in capital spending to fund Vision 2030’s projects and initiatives, including infrastructure development, to stimulate economic growth and generate more jobs.

Fiscal Policy

KSA’s medium-term fiscal policy has been developed strategically to achieve the plans specified in Vision 2030. In view of the economic developments and growth targets, the timeframe of the Fiscal Balance Program was delayed and the goal to achieve fiscal balance has been moved to 2023 from 2020. This was followed by IMF’s advice to Saudi authorities to adopt fiscal consolidation gradually to ensure that economic growth is not adversely affected.

Overall, the policy is aimed at developing capital expenditure and infrastructure; and the former has been projected at SAR 205bn (21% of total expenditure) in 2018 budget. The ratio is further projected to rise to 22% in 2020 from 19% in 2017. The government’s total expenditure is expected to average 4.3% over 2018–20, while growth of capital expenditure over the medium term is pegged at an average 8.3%.

Public debt has been projected at SAR 555bn (21% of GDP), higher than SAR 438bn (17% of GDP) in 2017. Debt issuance in 2018 has been capped at SAR 117bn compared to SAR 134bn in 2017, largely to fund some portion of the expenditure in 2018.

March 2018

7 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

Non-Oil Sector

%2.7 %3.7 %4.1 %1.7

%0.7-

%2.7

%4-

%2-

%0

%2

%4

%6

%8

2013 2014 2015 2016 2017 2018E

GDP Growth Oil Sector

Non-Oil

1,145 1,035 913

446 329 440 492

103 121

131

170 199

256 291

0

500

1,000

1,500

2012 2013 2014 2015 2016 2017 2018E

Oil

GDP Growth

Oil and Non-Oil Revenue Contribution

Source: Ministry of Finance – Budget Statement 2018

Source: Ministry of Finance – Budget Statement 2018

GDP GrowthContribution from Oil and Non-Oil Sectors

KSA’s GDP growth was slowed by 0.74% in 2017 compared to 1.7% growth in 2016. This negative growth can be largely ascribed to a decline in real oil GDP (negative growth of 3% during 2017). The non-oil sector, however, proved to be a breather, as it grown by 0.7% in 2017 (as compared to actual growth rate of 0.6% in the first half ).

In 2018, the government expects real GDP to grow 2.7%, supported by a strong non-oil GDP growth rate of 3.7%. The private sector will play a major role in non-oil GDP growth. Furthermore, the IMF revised KSA’s GDP growth outlook to 1.6% in 2018 compared to its previous estimate of 1.1%, although the pace of expansion remains below government estimates. Moreover, the ministry estimates that real GDP growth rate will surpass 2.8% in 2020, driven by the real non-oil GDP growth (expected to register a 3.2% increase in 2020).

It has been a challenging task for the government to shift the overall focus from an oil-centric economy to a diversified platform. However, with revolutionary reforms and tactical steps, the government managed to deliver, as non-oil sector outperformed in most of the parameters. The contribution of non-oil sectors towards KSA’s GDP has increasingly strengthened over the years. Non-oil revenue rose to a staggering share of 36.8% (SAR 256bn) in 2017 from SAR 102.6bn (8.2% of the total revenue) in 2012. Furthermore, the trend is expected to continue going forward, with 2018 non-oil revenue estimated at SAR 291bn (37.2% of the total revenue expected).

Economic Outlook

March 2018

8 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

48

50

52

54

56

58

60

62

Jan

15

Mar

15

May

15

Jul 1

5

Sep

15

Nov

15

Jan

16

Mar

16

May

16

Jul 1

6

Sep

16

Nov

16

Jan

17

Mar

17

May

17

Jul 1

7

Sep

17

Nov

17

Jan

18

Feb

18

60.1

58.7

53.2

57.5

53.053.2

0

500

1,000

1,500

2,000

Q20

13 4

Q20

14 1

Q20

14 2

Q20

14 3

Q20

14 4

Q20

15 1

Q20

15 2

Q20

15 3

Q20

15 4

Q20

16 1

Q20

16 2

Q20

16 3

Q20

16 4

Q20

17 1

Q20

17 2

Q20

17 3

Q20

17 4

M1 M2 M3

PMI Index

Money Supply (SAR bn)

Source: Bloomberg

Source: SAMA

Monetary Policy

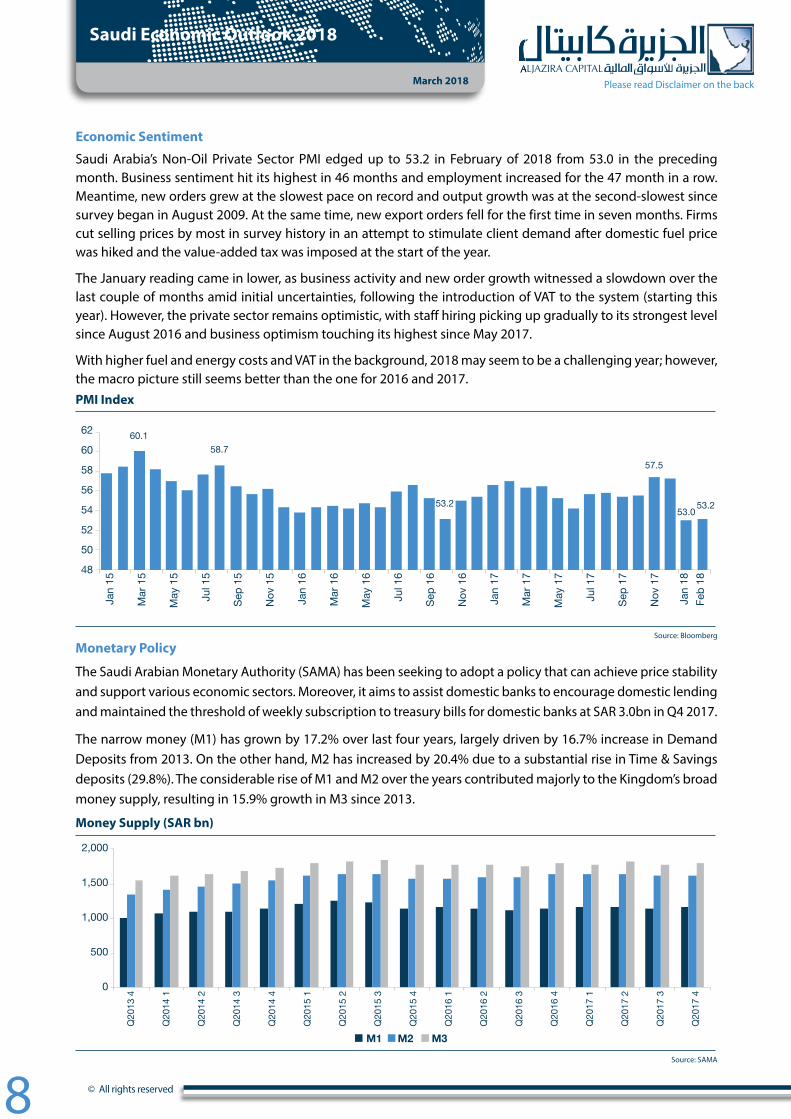

The Saudi Arabian Monetary Authority (SAMA) has been seeking to adopt a policy that can achieve price stability and support various economic sectors. Moreover, it aims to assist domestic banks to encourage domestic lending and maintained the threshold of weekly subscription to treasury bills for domestic banks at SAR 3.0bn in Q4 2017.

The narrow money (M1) has grown by 17.2% over last four years, largely driven by 16.7% increase in Demand Deposits from 2013. On the other hand, M2 has increased by 20.4% due to a substantial rise in Time & Savings deposits (29.8%). The considerable rise of M1 and M2 over the years contributed majorly to the Kingdom’s broad money supply, resulting in 15.9% growth in M3 since 2013.

Economic Sentiment

Saudi Arabia’s Non-Oil Private Sector PMI edged up to 53.2 in February of 2018 from 53.0 in the preceding month. Business sentiment hit its highest in 46 months and employment increased for the 47 month in a row. Meantime, new orders grew at the slowest pace on record and output growth was at the second-slowest since survey began in August 2009. At the same time, new export orders fell for the first time in seven months. Firms cut selling prices by most in survey history in an attempt to stimulate client demand after domestic fuel price was hiked and the value-added tax was imposed at the start of the year.

The January reading came in lower, as business activity and new order growth witnessed a slowdown over the last couple of months amid initial uncertainties, following the introduction of VAT to the system (starting this year). However, the private sector remains optimistic, with staff hiring picking up gradually to its strongest level since August 2016 and business optimism touching its highest since May 2017.

With higher fuel and energy costs and VAT in the background, 2018 may seem to be a challenging year; however, the macro picture still seems better than the one for 2016 and 2017.

March 2018

9 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

%4.3%4.0

%2.0

%0.7-

%3.0

%1-

%0

%1

%2

%3

%4

%5

Jan

12

Ap

r 12

Jul 1

2

Oct

12

Jan

13

Ap

r 13

Jul 1

3

Oct

13

Jan

14

Ap

r 14

Jul 1

4

Oct

14

Jan

15

Ap

r 15

Jul 1

5

Oct

15

Jan

16

Ap

r 16

Jul 1

6

Oct

16

Jan

17

Ap

r 17

Jul 1

7

Oct

17

Jan

18

%44.3

%1.0-%10.0-

%0.0

%10.0

%20.0

%30.0

%40.0

%50.0

Jan

01

Aug

01

Mar

02

Oct

02

May

03

Dec

03

Jul 0

4

Feb

05

Sep

05

Ap

r 06

Nov

06

Jun

07

Jan

08

Aug

08

Mar

09

Oct

09

May

10

Dec

10

Jul 1

1

Feb

12

Sep

12

Ap

r 13

Nov

13

Jun

14

Jan

15

Aug

15

Mar

16

Oct

16

May

17

Dec

17

Inflation

Bank Lending Growth

Source: SAMA

Source: SAMA

Inflation

The Kingdom’s inflation declined throughout 2017, as consumer inflation remained in the negative territory for 10 successive months until October 2017. According to latest data, Saudi Arabia inflation rate stood at 3.0% at the end of January, an increase from 0.4% in December. This is as a result of the implementation of VAT and reforms in utility and fuel prices during the month. However, the introduction of VAT and reforms related to electricity and fuel prices are expected to boost inflation, which is set to rise to 5.7% in full year 2018 from a negative 0.15% last year. As part of additional measures, KSA announced several new allowances and tax breaks for state employees, military personnel, and some citizens, in an attempt to curb rising inflation.

Credit Growth

The value of loans in KSA dropped 1.0% YoY in December 2017. Loan growth in the Kingdom averaged 13.8% from 2001 until 2017, reaching an all-time high of 44.3% in October 2004 and a record low of -1.8% in October 2017.

Bank loans to the private sector edged lower (down 0.9% YoY in December), while it witnessed an all-time peak of 47.2% in October 2004 and lowest of -1.7% in June 2017 (during 2001–17). Sluggish growth since the start of 2017 shows that private sector held back fresh investments ascribed to an economic slump amid subdued oil prices and government austerity measures.

Although the Saudi banks’ ratio of non-performing loans to gross loans is expected to marginally increase from the current level of 1.8% after the implementation of IFRS9; Saudi Arabia’s banking outlook is expected to stabilize during 2018, as the economy will return to growth in 2018. Furthermore, lending growth is expected to gradually recover supported by recovery in corporate activity along with strong demand from residential loans. However, higher interest rates can hinder credit growth, as the Federal reserve has shown strong intention of sticking with the current Monetary policy. Any further hike in rates will potentially have a positive impact on banking sector earning ( 60.1% Non-interest bearing deposits), however given the negative credit growth experienced in 2017, credit growth can only pickup from here, especially due to the easing of ADR ratio calculation and strong economic recovery, due to recovery in oil price, Higher fiscal inflows ( VAT, expat fee, lower subsidy,) and higher contribution from non-oil revenue.

March 2018

10 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

5.461

11.149

0

150

300

450

600

0

5,000

10,000

15,000

'13 '14 '15 '16 '17 '18

Volume

Volu

me

(in m

illio

ns)

Index

Inde

x

925

1,196 1,325 1,271

1,400

1,753 1,813

1,579 1,682 1,690

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17

TASI Index vs Volume Market Capitalization (SAR bn)

Source: Tadawul

TASI Outlook

The Tadawul All Share Index (TASI) managed to hold its ground in the last couple of years after falling to levels as low as 5,416 points in October 2016. The index saw the largest fall after reaching high levels of 11,149 in September 2014. The plunge in oil prices and the subsequent setback in liquidity in the market largely resulted in weak investor confidence. The TASI witnessed subdued closing at the end of last year (at 7,226 points, edging 0.2% higher from 2016) due to recovering oil prices since end-2017, further leading to increased activity.

Total market capitalization at the end of March-2018 increased to SAR 1,860bn (almost 4.0% CAGR over the last five years), whereas Index performance increased by 8.5%YTD. Overall, with the upbeat budget announcement, positive economic sentiment, and recovering oil prices, one may expect trading interest to be revived in 2018.

MSCI and FTSE Russell have considered upgrading Saudi Arabia to the Emerging Market index. The decision is yet to be taken, but Saudi stocks have performed brightly on the expectation of such upgrades. FTSE Russell’s decision on Saudi’s inclusion is due at the end of March, 2018. If the decision comes out to be positive, the probability of MSCI EM inclusion will be at an all-time high. The possible weight to be assigned in MSCI and FTSE indexes is estimated to be around 2%-2.5% , which could bring around USD 9.0-12.0 bn of foreign inflows into the market.

Sectoral Performance

In terms of the number of transactions during 2017, insurance emerged as the most active sector, representing 19.7% of total trades during the year. It stood third in terms of the total value of shares traded. The materials sector (the largest sector in the TASI) stood second on both metrics with 4.20 million trades (value traded at SAR 192.7bn). In terms of value traded, banks dominated the market with SAR 194.9bn in value (23.3% share) and 2.12 million in volume.

In terms of sectoral performance in 2017, the media industry outperformed posting a 51% increase, followed by retailing (15%) and food and staples (11%). Conversely, the pharma sector was a laggard during the year (down 26%), with consumer services (down 24%) and transportation (down 21%) declining.

%51

%15 %11 %8%1

%0 %4- %6- %6- %7- %11- %11- %13- %14- %15- %17- %19- %21- %24- %26-%40-

%20-

%0

%20

%40

%60

Med

ia

Ret

ailin

g

Food

& S

tapl

es

Bank

s

Mat

eria

ls

Food

& B

ever

ages

Insu

ranc

e

Util

ities

Rea

l Est

ate

REI

Ts

Con

s. D

urab

les

Hea

lthC

are

Cap

ital G

oods

Ener

gy

Tele

com

Com

. & P

rof.

Svc

Div

ersi

fied

Fin

Tran

spor

tatio

n

Con

sum

er S

ervi

ces

Phar

ma,

Bio

tech

Performance of Industry Group Indices – 2017 (YoY)

Source: Tadawul

March 2018

11 © All rights reserved

Please read Disclaimer on the back

Saudi Economic Outlook 2018

March 2018

Conclusion

The most recent data suggests that the non-oil economy was hit hard by the introduction of VAT as PMI

recorded its lowest levels of 53.0 during Jan-2018, since the inception of the survey back in 2009. However,

impact on non-oil revenues is believed to be temporary as the glitch occurred due to strong order flows

prior to policy implementation. Having said that, the prospects still seems bright as businesses continued

to increase their staffing levels at the strongest rate since August 2016 and business sentiment achieved its

46 month high.

Overall, the economic outlook appears optimistic, as oil reached a three-year high in January 2018,

indicating a solid start to the year. Rising oil revenues and the implementation of VAT is firmly believed to

fill the fiscal gap by offsetting a fiscal deficit created by a more expansionary budget this year. With some

upbeat forecasts such as 2.7% GDP growth, increase in revenue share of the non-oil sector (37.2%), the

fiscal deficit’s gradual contraction, and inflation entering a positive territory after a long downturn, the

current overall picture seems interesting and dynamic. Moreover, potential inclusion of the TASI in the MSCI

and FTSE indexes and a possible IPO of Aramco in 2018 would open the domestic market. These landmark

events are being closely followed by fund managers and foreign investors, which would drive the equity

market backdrop in KSA.

Moreover, the new social reforms such as permitting women driving, opening of cinema theatres, and

launching of tourist visas seems revolutionary as these could get other economic sectors to gain their share

in the overall economy. However, it will be interesting to see how these reforms will play out in the Saudi

landscape.

The progressive reforms adopted by the Kingdom have been acknowledged globally, with IMF raising

its economic growth forecast to 1.6%, an upward revision from its previous estimate of 1.1%. Moreover,

growing confidence in Vision 2030 is clearly visible among international rating agencies, as the Kingdom’s

credit rating continued to improve despite falling oil prices in the recent past. In November 2017, Fitch

Ratings issued its Long-Term Foreign-Currency Issuer Default Rating (IDR) at ‘A+’ with a stable outlook. On

similar lines, S&P Global Ratings affirmed the Kingdom’s rating at ‘A-/A-2’ with a stable outlook.

With the host of new reforms and developments implemented so far and a few already in the pipeline, KSA

is a captivating prospect. With the nation already attracting the attention of economists and investors all

over the world, it would be interesting to see how the story unfolds in the near future.

Asset Management | Brokerage | Corporate Finance | Custody | Advisory

Head Office: King Fahad Road, P.O. Box: 20438, Riyadh 11455, Saudi Arabia، Tel: 011 2256000 - Fax: 011 2256068

Aljazira Capital is a Saudi Investment Company licensed by the Capital Market Authority (CMA), license No. 07076-37

RESE

ARC

H D

IVIS

ION

RESE

ARC

H

DIV

ISIO

NRA

TIN

GTE

RMIN

OLO

GY

BRO

KERA

GE A

ND IN

VEST

MEN

T CE

NTER

S DI

VISI

ON

Disclaimer

AlJazira Capital, the investment arm of Bank AlJazira, is a Shariaa Compliant Saudi Closed Joint Stock company and operating under the regulatory supervision of the Capital Market Authority. AlJazira Capital is licensed to conduct securities business in all securities business as authorized by CMA, including dealing, managing, arranging, advisory, and custody. AlJazira Capital is the continuation of a long success story in the Saudi Tadawul market, having occupied the market leadership position for several years. With an objective to maintain its market leadership position, AlJazira Capital is expanding its brokerage capabilities to offer further value-added services, brokerage across MENA and International markets, as well as offering a full suite of securities business.

1. Overweight: This rating implies that the stock is currently trading at a discount to its 12 months price target. Stocks rated “Overweight” will typically provide an upside potential of over 10% from the current price levels over next twelve months.

2. Underweight: This rating implies that the stock is currently trading at a premium to its 12 months price target. Stocks rated “Underweight” would typically decline by over 10% from the current price levels over next twelve months.

3. Neutral: The rating implies that the stock is trading in the proximate range of its 12 months price target. Stocks rated “Neutral” is expected to stagnate within +/- 10% range from the current price levels over next twelve months.

4. Suspension of rating or rating on hold (SR/RH): This basically implies suspension of a rating pending further analysis of a material change in the fundamentals of the company.

The purpose of producing this report is to present a general view on the company/economic sector/economic subject under research, and not to recommend a buy/sell/hold for any security or any other assets. Based on that, this report does not take into consideration the specific financial position of every investor and/or his/her risk appetite in relation to investing in the security or any other assets, and hence, may not be suitable for all clients depending on their financial position and their ability and willingness to undertake risks. It is advised that every potential investor seek professional advice from several sources concerning investment decision and should study the impact of such decisions on his/her financial/legal/tax position and other concerns before getting into such investments or liquidate them partially or fully. The market of stocks, bonds, macroeconomic or microeconomic variables are of a volatile nature and could witness sudden changes without any prior warning, therefore, the investor in securities or other assets might face some unexpected risks and fluctuations. All the information, views and expectations and fair values or target prices contained in this report have been compiled or arrived at by Aljazira Capital from sources believed to be reliable, but Aljazira Capital has not independently verified the contents obtained from these sources and such information may be condensed or incomplete. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this report. Aljazira Capital shall not be liable for any loss as that may arise from the use of this report or its contents or otherwise arising in connection therewith. The past performance of any investment is not an indicator of future performance. Any financial projections, fair value estimates or price targets and statements regarding future prospects contained in this document may not be realized. The value of the security or any other assets or the return from them might increase or decrease. Any change in currency rates may have a positive or negative impact on the value/return on the stock or securities mentioned in the report. The investor might get an amount less than the amount invested in some cases. Some stocks or securities maybe, by nature, of low volume/trades or may become like that unexpectedly in special circumstances and this might increase the risk on the investor. Some fees might be levied on some investments in securities. This report has been written by professional employees in Aljazira Capital, and they undertake that neither them, nor their wives or children hold positions directly in any listed shares or securities contained in this report during the time of publication of this report, however, The authors and/or their wives/children of this document may own securities in funds open to the public that invest in the securities mentioned in this document as part of a diversified portfolio over which they have no discretion. This report has been produced independently and separately by the Research Division at Aljazira Capital and no party (in-house or outside) who might have interest whether direct or indirect have seen the contents of this report before its publishing, except for those whom corporate positions allow them to do so, and/or third-party persons/institutions who signed a non-disclosure agreement with Aljazira Capital. Funds managed by Aljazira Capital and its subsidiaries for third parties may own the securities that are the subject of this document. Aljazira Capital or its subsidiaries may own securities in one or more of the aforementioned companies, and/or indirectly through funds managed by third parties. The Investment Banking division of Aljazira Capital maybe in the process of soliciting or executing fee earning mandates for companies that is either the subject of this document or is mentioned in this document. One or more of Aljazira Capital board members or executive managers could be also a board member or member of the executive management at the company or companies mentioned in this report, or their associated companies. No part of this report may be reproduced whether inside or outside the Kingdom of Saudi Arabia without the written permission of Aljazira Capital. Persons who receive this report should make themselves aware, of and adhere to, any such restrictions. By accepting this report, the recipient agrees to be bound by the foregoing limitations.

Head of Research

Talha Nazar +966 11 [email protected]

AnalystSultan Al Kadi, CAIA+966 11 [email protected]

Analyst

Jassim Al-Jubran +966 11 [email protected]

Analyst

Waleed Al-jubayr+966 11 [email protected]

Analyst

Muhanad Al-Odan+966 11 [email protected]

General Manager – Brokerage Services &

sales

Alaa Al-Yousef+966 11 [email protected]

AGM-Head of international and institutional

brokerage

Luay Jawad Al-Motawa +966 11 [email protected]

AGM- Head of Western and Southern Region Investment

Centers

Mansour Hamad Al-shuaibi +966 12 [email protected]

AGM-Head of Sales And Investment Centers

Central Region

Sultan Ibrahim AL-Mutawa +966 11 [email protected]

AGM-Head of Qassim & Eastern Province

Abdullah Al-Rahit +966 16 3617547 [email protected]