saskatchewan teachers’ federation · pdf fileteacher crisis ... accounts receivable...

TRANSCRIPT

SASKATCHEWAN TEACHERS’

FEDERATION

FINANCIAL STATEMENTS June 30, 2016

Deloitte LLP 122 1st Ave. S. Suite 400, PCS Tower Saskatoon SK S7K 7E5 Canada Tel: 306-343-4400 Fax: 306-343-4480 www.deloitte.ca

INDEPENDENT AUDITOR’S REPORT TO THE COUNCIL OF SASKATCHEWAN TEACHERS’ FEDERATION: We have audited the accompanying financial statements of Saskatchewan Teachers’ Federation, which comprise the statement of financial position as at June 30, 2016, and the statements of operations and changes in net assets and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian accounting standards for not-for-profit organizations, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of Saskatchewan Teachers’ Federation as at June 30, 2016, and the results of its operations and its cash flows for the year then ended in accordance with Canadian accounting standards for not-for-profit organizations. Chartered Professional Accountants, Chartered Accountants Licensed Professional Accountants September 30, 2016 Saskatoon, Saskatchewan

SASKATCHEWAN TEACHERS’ FEDERATIONSTATEMENT OF OPERATIONS AND CHANGES IN NET ASSETS

year ended June 30, 2016

Restricted FundsProfessional Working Operations

Development Capital Endowment Contingency and Capital

Unit Fund Fund Fund Fund

2016 2015 2016 2016 2016 2016 2015 2016 2016 2016 2015

REVENUESMembership fees Regular fees $ 10,946,581 $ 10,803,429 $ - $ - $ - $ - $ - $ 770,455 $ - $ 770,455 $ 764,571 Substitute fees 654,542 653,416 - - - - - - - - - Associate fees 450 780 - - - - - - - - -

11,601,573 11,457,625 - - - - - 770,455 - 770,455 764,571 Projects - - 1,243,631 - - 1,243,631 1,101,331 - - - - Saskatchewan Teachers’ Federation Members’ - Health Plan administration fee (Note 11) 216,900 217,002 - - - - - - - - - Saskatchewan Teachers’ Federation - Portaplan administration fee (Note 11) 130,800 143,300 - - - - - - - - - Saskatchewan Teachers’ Federation Income - Continuance Plan administration fee (Note 11) 537,500 598,700 - - - - - - - - - Saskatchewan Teachers’ Retirement Plan - administration fee (Note 11) 763,500 818,700 - - - - - - - - - Saskatchewan Teachers’ Federation Employees’ -

Pension Plan adminstration fee (Note 11) 20,100 24,800 - - - - - - - - - Dr. Stirling McDowell Foundation for Research -

Into Teaching Inc. administration fee (Note 11) 17,900 20,700 - - - - - - - - - Direct cost service revenue (Note 11) 775,910 744,941 - - - - - - - - - Superannuated Teachers of Saskatchewan -

external fee for service 21,810 20,190 - - - - - - - - - Building operations cost recovery (Note 11) 503,063 435,313 - - - - - - - - - Saskatchewan Teachers’ Federation -

external leases 17,570 26,324 - - - - - - - - - Investment (expense) income (Note 5) (932) 2,538 340 12,492 786 13,618 22,036 1,454,336 471,770 1,926,106 2,027,314 Advertising, materials and service 23,636 28,436 - - - - - - - - - Fixed asset overhead recovery (Note 11) 152,493 85,662 - - - - - - - - - Sundry income 9,564 743 - - - - - - - - -

14,791,387 14,624,974 1,243,971 12,492 786 1,257,249 1,123,367 2,224,791 471,770 2,696,561 2,791,885

EXPENSESGovernance 1,471,515 1,641,657 - - - - - - - - - Professional stewardship and responsibility 1,008,980 763,543 775,732 - - 775,732 522,568 - - - - Advocacy 152,049 449,310 1,689 - 2,000 3,689 4,177 524,788 - 524,788 126,438 Economic services 4,735 43,292 - - - - - - - - - Human resources 8,757,524 8,535,279 361,854 - - 361,854 414,108 - - - - Professional services 969,526 987,080 - - - - - 227,822 - 227,822 355,934 Infrastructure 1,980,484 1,568,658 17,519 - - 17,519 23,207 144 - 144 1,597 Board of reference and disputes - - - - - - - 66,951 - 66,951 319 Conciliation, mediation, and arbitration - - - - - - - 615 - 615 190,555 Teacher crisis - - - - - - - 99,448 - 99,448 5,000 Loss on disposal of capital assets 804 15,402 - - - - - - - -

14,345,617 14,004,221 1,156,794 - 2,000 1,158,794 964,060 919,768 - 919,768 679,843 445,770 620,753 87,177 12,492 (1,214) 98,455 159,307 1,305,023 471,770 1,776,793 2,112,042

UNREALIZED LOSS IN MARKET VALUE OFINVESTMENT FUNDS - - - - - - - (855,146) (304,086) (1,159,232) (187,866)

NET REVENUES (EXPENSES) 445,770 620,753 87,177 12,492 (1,214) 98,455 159,307 449,877 167,684 617,561 1,924,176 NET ASSETS, BEGINNING OF YEAR 7,334,982 6,668,837 257,469 3,191,266 155,604 3,604,339 2,936,828 22,306,492 6,969,624 29,276,116 27,490,639 INTERFUND TRANSFERS 854,842 (361,301) 150,000 (303,541) - (153,541) 500,000 - (701,301) (701,301) (138,699) EMPLOYEE FUTURE BENEFITS RE-MEASUREMENTS

AND OTHER ITEMS (1,187,111) 406,693 (23,947) - - (23,947) 8,204 - - - - NET ASSETS, END OF YEAR $ 7,448,483 $ 7,334,982 $ 470,699 $ 2,900,217 $ 154,390 $ 3,525,306 $ 3,604,339 $ 22,756,369 $ 6,436,007 $ 29,192,376 $ 29,276,116

The accompanying notes are an integral part of these financial statements.

Unrestricted Funds

Total

1

Total TotalGeneral Fund

SASKATCHEWAN TEACHERS’ FEDERATIONSTATEMENT OF FINANCIAL POSITION

as at June 30, 2016Professional Working Operations

General Development Capital Endowment Contingency and CapitalFund Unit Fund Fund Fund Fund 2016 2015

CURRENT ASSETSCash $ 272,923 $ 48,245 $ - $ - $ 312,518 $ 1,523 $ 635,209 $ 1,184,598 Short-term investments (Note 4) 13,056 - - - - - 13,056 251,500 Accounts receivable (Notes 6 and 11) 1,948,921 25,872 - - 71,799 - 2,046,592 1,222,424 Prepaid expenses 439,945 7,710 - - - - 447,655 339,742

2,674,845 81,827 - - 384,317 1,523 3,142,512 2,998,264

INVESTMENT FUNDS (Note 5) 54,078 - 2,900,542 154,407 22,442,125 6,435,187 31,986,339 32,529,375 DEFINED BENEFIT ASSET (Note 7) 1,443,848 - - - - 1,443,848 3,302,284 CAPITAL ASSETS (Note 3)

Tangible assets 4,133,133 4,071 - - - - 4,137,204 4,038,177 Intangible assets 1,524,504 429,424 - - - - 1,953,928 805,921

7,155,563 433,495 2,900,542 154,407 22,442,125 6,435,187 39,521,319 40,675,757 $ 9,830,408 $ 515,322 $ 2,900,542 $ 154,407 $ 22,826,442 $ 6,436,710 $ 42,663,831 $ 43,674,021

CURRENT LIABILITIESAccounts payable and accrued charges (Notes 3, 8 and 11) $ 1,920,744 $ 48,689 $ 325 $ 17 $ 52,546 $ - $ 2,022,321 $ 3,074,042 Deferred revenue 438,639 36,706 - - - - 475,345 384,542 Interfund advances 22,542 (40,772) - - 17,527 703 - -

2,381,925 44,623 325 17 70,073 703 2,497,666 3,458,584

COMMITMENTS (Notes 12 and 14)

NET ASSETSUnrestricted 7,448,483 470,699 2,900,217 154,390 - - 10,973,789 10,939,321 Externally restricted (Note 9) - - - - 22,756,369 - 22,756,369 22,306,493 Internally restricted - - - - - 6,436,007 6,436,007 6,969,623

7,448,483 470,699 2,900,217 154,390 22,756,369 6,436,007 40,166,165 40,215,437 $ 9,830,408 $ 515,322 $ 2,900,542 $ 154,407 $ 22,826,442 $ 6,436,710 $ 42,663,831 $ 43,674,021

The accompanying notes are an integral part of these financial statements.

2

APPROVED ON BEHALF OF THE STF EXECUTIVE

“Patrick Maze, STF Executive President”“Gwen Dueck, Executive Director”

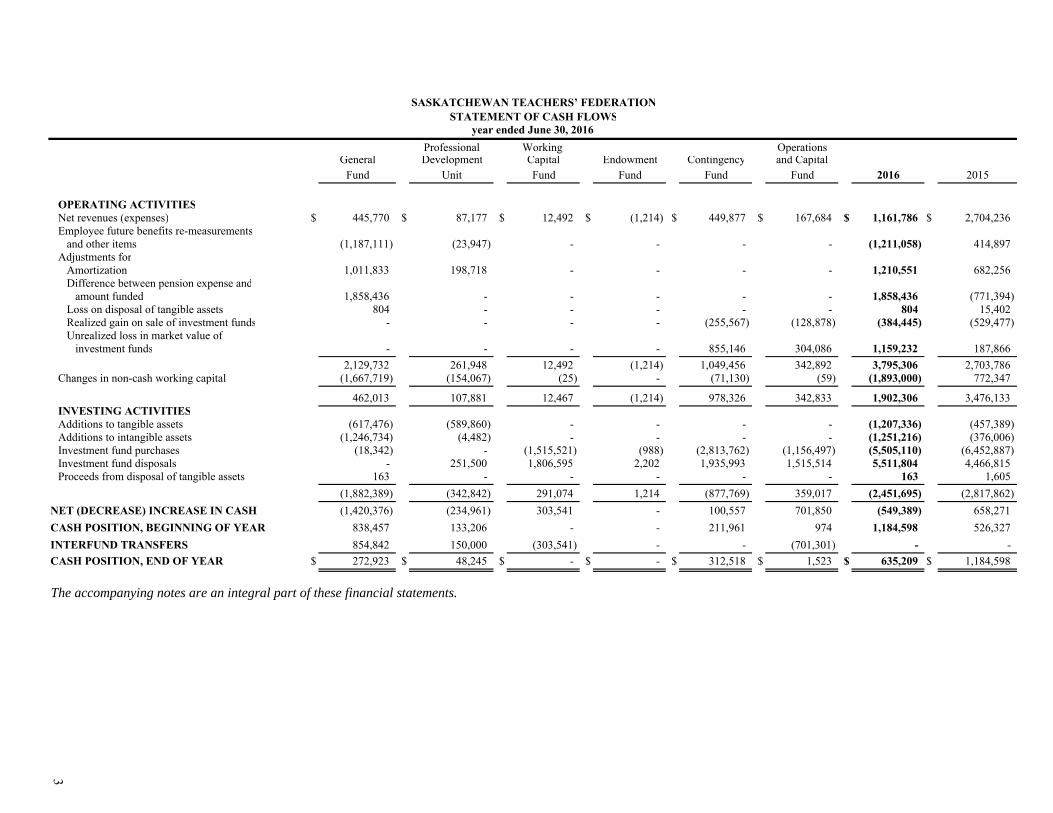

SASKATCHEWAN TEACHERS’ FEDERATIONSTATEMENT OF CASH FLOWS

year ended June 30, 2016

Professional Working OperationsGeneral Development Capital Endowment Contingency and Capital

Fund Unit Fund Fund Fund Fund 2016 2015

OPERATING ACTIVITIESNet revenues (expenses) $ 445,770 $ 87,177 $ 12,492 $ (1,214) $ 449,877 $ 167,684 $ 1,161,786 $ 2,704,236 Employee future benefits re-measurements

and other items (1,187,111) (23,947) - - - - (1,211,058) 414,897 Adjustments for

Amortization 1,011,833 198,718 - - - - 1,210,551 682,256 Difference between pension expense and amount funded 1,858,436 - - - - - 1,858,436 (771,394) Loss on disposal of tangible assets 804 - - - - - 804 15,402 Realized gain on sale of investment funds - - - - (255,567) (128,878) (384,445) (529,477) Unrealized loss in market value of investment funds - - - - 855,146 304,086 1,159,232 187,866

2,129,732 261,948 12,492 (1,214) 1,049,456 342,892 3,795,306 2,703,786 Changes in non-cash working capital (1,667,719) (154,067) (25) - (71,130) (59) (1,893,000) 772,347

462,013 107,881 12,467 (1,214) 978,326 342,833 1,902,306 3,476,133 INVESTING ACTIVITIESAdditions to tangible assets (617,476) (589,860) - - - - (1,207,336) (457,389) Additions to intangible assets (1,246,734) (4,482) - - - - (1,251,216) (376,006) Investment fund purchases (18,342) - (1,515,521) (988) (2,813,762) (1,156,497) (5,505,110) (6,452,887) Investment fund disposals - 251,500 1,806,595 2,202 1,935,993 1,515,514 5,511,804 4,466,815 Proceeds from disposal of tangible assets 163 - - - - - 163 1,605

(1,882,389) (342,842) 291,074 1,214 (877,769) 359,017 (2,451,695) (2,817,862)

NET (DECREASE) INCREASE IN CASH (1,420,376) (234,961) 303,541 - 100,557 701,850 (549,389) 658,271

CASH POSITION, BEGINNING OF YEAR 838,457 133,206 - - 211,961 974 1,184,598 526,327

INTERFUND TRANSFERS 854,842 150,000 (303,541) - - (701,301) - -

CASH POSITION, END OF YEAR $ 272,923 $ 48,245 $ - $ - $ 312,518 $ 1,523 $ 635,209 $ 1,184,598

The accompanying notes are an integral part of these financial statements.

3

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

4

1. DESCRIPTION OF OPERATIONS The Saskatchewan Teachers’ Federation (the “Federation”) is a corporation as set out in The Teachers’ Federation Act, 2006. The Federation is by this legislation a holistic professional organization that serves both the interests of teachers and the public. Its purposes as mandated in Section 5 of the Act are, among others, to represent and support teachers, to carry on activities to improve the quality of education and delivery of education support for and by teachers, and to promote the cause of education and raise the status of the teaching profession. The Federation also provides various benefit and pension plans for its members and former members, bargains collectively on behalf of teachers, and provides member supports and resources that promote teachers’ professional stewardship and responsibility. The Federation is funded by teachers through membership fees.

2. SIGNIFICANT ACCOUNTING POLICIES These financial statements have been prepared in accordance with Canadian accounting standards for not-for-profit organizations (“ASNPO”) in Part III of the CPA Handbook and reflect the following significant policies: Basis of Presentation These financial statements do not reflect operations of the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, the Saskatchewan Teachers’ Retirement Plan, the Saskatchewan Teachers’ Federation Employees’ Pension Plan, or Dr. Stirling McDowell Foundation for Research Into Teaching Inc. Separate financial statements have been prepared for these plans. See Note 13 for summary information.

Use of Estimates The preparation of the financial statements in conformity with ASNPO requires management to make estimates and assumptions that affect reported amounts of assets and liabilities, revenues and expenses and in the disclosure of commitments and contingencies. Examples of such estimations and assumptions include the useful lives and amortization of capital assets, the cost of employee future benefits, and provisions for contingencies. Actual results could differ from those estimates. Adjustments, if any, will be reflected in operations in the period of settlement.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

5

2. SIGNIFICANT ACCOUNTING POLICIES (continued) Use of Estimates (continued)

The Federation has a defined benefit pension plan whereby plan members are entitled to a specified level of benefit payment at a future date. The obligation of the Federation is determined with the assistance of an actuary and is a complex calculation involving a large number of estimates relating to matters such as employee demographics, mortality and illness rates, retirement dates, trends in interest rates and the performance of the current and future investment portfolio of the benefit plan. A small change in any one of these estimates could have a significant impact on the obligation. In assessing the recoverability of defined benefit assets, the Federation is required to make assumptions about the ability to recover the amount recognized through reductions in funding in future periods. A similar assessment is required in the recognition of any liability for future minimum funding requirements. Management has applied its judgment in this complex area. Fund Accounting The Federation follows the restricted method of accounting for contributions. The General Fund accounts for the Federation’s programs and administrative activities. This fund reports unrestricted resources. The Saskatchewan Professional Development Unit reports unrestricted resources that are used to enhance effective in-service education for members of the teaching profession of Saskatchewan and to provide support for the education communities’ pursuit of the same. The Working Capital Fund reports unrestricted resources that are to be used for expenses during times when the Federation is not receiving membership fees and to maximize investment earnings of the Federation. The Contingency Fund reports only externally restricted resources that are to be used to provide legal and financial support for members who are involved in disputes related to collective bargaining or contracts of employment, to provide financial support to respond to an education crisis, to provide financial means for an ongoing public relations program in support of public education and the teaching profession, and to provide financial support for emergent circumstances that result during the course of an already established budget year.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

6

2. SIGNIFICANT ACCOUNTING POLICIES (continued) Fund Accounting (continued) The Operations and Capital Fund reports only internally restricted resources that are to be used for capital purchases and improvements and collective agreement liabilities. As of July 26, 2007, the funding in the Endowment Fund no longer has any restrictions. The investment income from these funds continues to be paid out as annual scholarships awarded to teacher applicants from the province of Saskatchewan seeking studies in the field of resource centre management.

Employee Future Benefits

All of the Federation’s employees that are not members of a teachers’ pension plan are participants in the Saskatchewan Teachers’ Federation Employees’ Pension Plan, which is a contributory defined benefit pension plan. The Federation is the sponsor of Saskatchewan Teachers’ Federation Employees’ Pension Plan. The Federation follows Part II Handbook Section 3462, Employee Future Benefits, and Part III Handbook Section 3463, Employee Future Benefits by Not-for-Profit Organizations (“Section 3463”), for the measurement of the pension obligation and employee future benefit expense. Section 3463 requires the separate recording of pension obligation re-measurements in Net Assets. Accordingly, the Federation’s portion of these re-measurements have been recorded in Net Assets with an accompanying amount owing to (from) the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, the Saskatchewan Teachers’ Retirement Plan, and the Dr. Stirling McDowell Foundation for Research Into Teaching Inc. Revenue Recognition Unrestricted membership fees as set by the Federation’s Council are recognized as revenue in the General Fund in the fiscal year due.

Restricted membership fees as set by Council are recognized as revenue of the appropriate restricted fund in the fiscal year due. Contributions for endowment are recognized as revenue in the Endowment Fund.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

7

2. SIGNIFICANT ACCOUNTING POLICIES (continued) Revenue Recognition (continued)

Administration fees recovered from the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, the Saskatchewan Teachers’ Retirement Plan, the Saskatchewan Teachers’ Federation Employees’ Pension Plan, and Dr. Stirling McDowell Foundation for Research Into Teaching Inc. represents a reimbursement for the cost of salaries and benefits, facilities and supplies. Direct cost service revenue recovered from the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, the Saskatchewan Teachers’ Retirement Plan, the Saskatchewan Teachers’ Federation Employees’ Pension Plan, and Dr. Stirling McDowell Foundation for Research Into Teaching Inc. represents a reimbursement for the cost of salaries and benefits. All other revenue is recognized in the appropriate fund, in the year earned. Capital Assets Tangible assets are recorded at cost. The building is amortized on a declining-balance basis over its estimated useful life. Furniture and equipment along with computer hardware, leasehold improvements and books and periodicals are amortized on a straight-line basis over their estimated useful lives. Intangible assets are recorded at cost. Computer software and the rights under licensing agreements are amortized on a straight-line basis over its estimated useful life. Impairment of Long-Lived Assets Long-lived assets are tested for impairment whenever events or changes in circumstances indicate that their carrying value may not be recoverable. An impairment loss is recognized when their carrying value exceeds the total undiscounted cash flows expected from their use and eventual disposition. The amount of the impairment loss is determined as the excess of the carrying value of the asset over its fair value. Deferred Revenue Deferred revenue represents funds received in the current year which apply to subsequent fiscal years.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

8

2. SIGNIFICANT ACCOUNTING POLICIES (continued) Contributed Services The work of the Federation is dependent on the voluntary service of many members. Since these services are not normally purchased by the Federation and because of the difficulty of determining their fair value, contributed services are not recognized in these financial statements. Financial Instruments Financial assets and financial liabilities are recognized when the Federation becomes a party to the contractual provisions of the instrument. Financial assets and liabilities are initially recognized at fair value and their subsequent measurement is measured at amortized cost, except for short-term investments and investment funds which are measured at fair value as at the reporting date. Changes in fair value, including realized and unrealized gains and losses, are recorded in the Statement of Operations and Changes in Net Assets. Fair values are based on quoted market prices, specifically the latest bid price, where available from active markets, otherwise fair values are estimated using a variety of valuation techniques and models. Financial assets purchased and sold, where the contract requires the asset to be delivered within an established time frame, are recognized on a trade-date basis. Transaction costs are expensed as incurred for all short-term investments and investment funds. Transaction costs related to other financial instruments are netted against the carrying value of the asset or liability and are then recognized over the expected life of the instrument using the effective interest method. Pension Plan The Federation sponsors and funds a contributory defined benefit pension plan for its employees that are not members of a teachers’ pension plan. The plan provides pensions based on length of service and final average earnings. The Federation accrues its obligations under the defined benefit pension plan as the employees render the services necessary to earn the pension benefits. The cost of the defined benefit pension plan is determined periodically by an independent actuary.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

9

2. SIGNIFICANT ACCOUNTING POLICIES (continued) Pension Plan (continued) The defined benefit obligation of the plan is based on an actuarial valuation prepared for funding purposes (but not one prepared using a solvency, wind-up, or similar valuation basis) using the most recently completed actuarial valuation. A funding valuation is prepared in accordance with pension legislation and regulations, generally to determine required cash contributions to the plan. The Federation recognizes the defined benefit obligation net of the fair value of plan assets. Current service costs and finance cost for the period are recognized in the Statement of Operations and Changes in Net Assets. Employee future benefits re-measurements and other items are recognized directly in net assets in the Statement of Financial Position and presented as a separately identified line item in the Statement of Operations and Changes in Net Assets.

3. CAPITAL ASSETS

Tangible Assets

Accumulated Accumulated Net BookRates Cost Amortization Cost Amortization Value

Building 4% $ 5,404,355 $ 2,240,097 $ - $ - $ 3,164,258 Furniture and 5,10, &

equipment 15 yrs. 1,292,944 861,330 - - 431,614 Computer

hardware 3 yrs. 951,609 805,390 16,124 12,053 150,290 Leasehold

improvements 10 yrs. 209,538 209,538 - - - Stewart

ResourcesCentre 10 yrs. 761,821 402,598 - - 359,223

8,620,267 4,518,953 16,124 12,053 4,105,385 Land 31,819 - - - 31,819 2016 Totals $ 8,652,086 $ 4,518,953 $ 16,124 $ 12,053 $ 4,137,204

2015 Totals $ 8,357,304 $ 4,321,681 $ 13,560 $ 11,006 $ 4,038,177

General FundProfessional

Development Unit

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

10

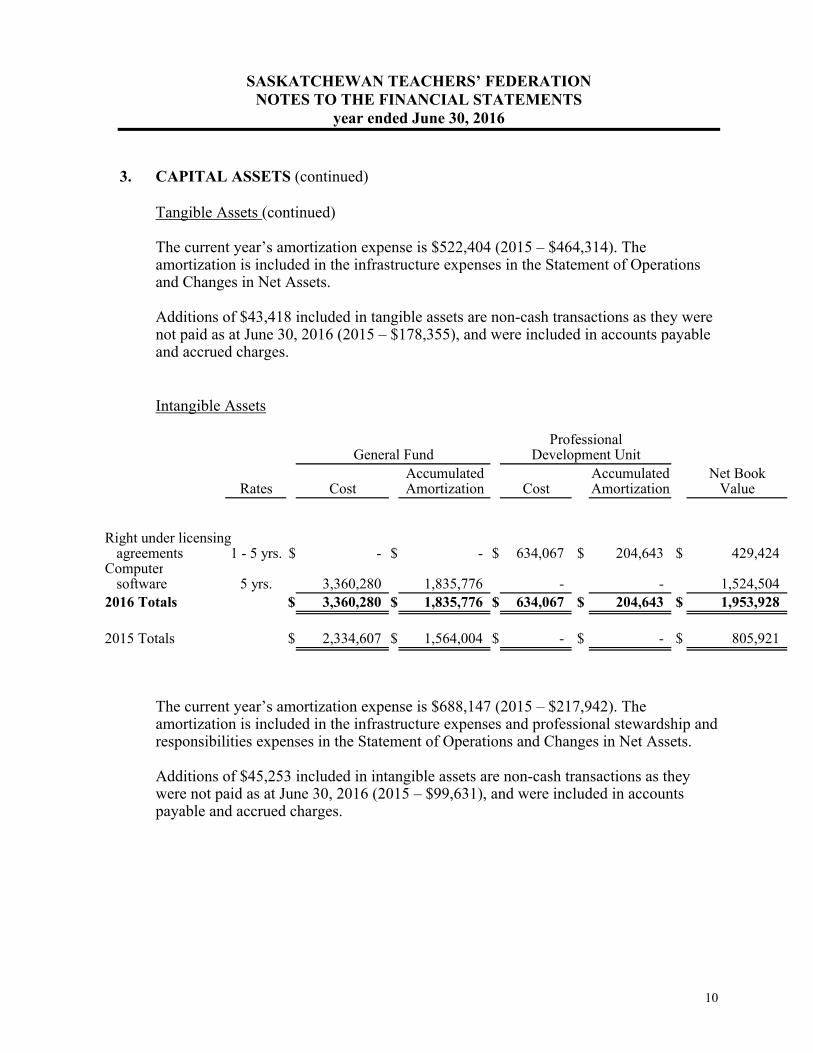

3. CAPITAL ASSETS (continued) Tangible Assets (continued) The current year’s amortization expense is $522,404 (2015 – $464,314). The

amortization is included in the infrastructure expenses in the Statement of Operations and Changes in Net Assets.

Additions of $43,418 included in tangible assets are non-cash transactions as they were

not paid as at June 30, 2016 (2015 – $178,355), and were included in accounts payable and accrued charges.

Intangible Assets

Accumulated Accumulated Net BookRates Cost Amortization Cost Amortization Value

Right under licensing agreements 1 - 5 yrs. $ - $ - $ 634,067 $ 204,643 $ 429,424 Computer

software 5 yrs. 3,360,280 1,835,776 - - 1,524,504 2016 Totals $ 3,360,280 $ 1,835,776 $ 634,067 $ 204,643 $ 1,953,928

2015 Totals $ 2,334,607 $ 1,564,004 $ - $ - $ 805,921

General FundProfessional

Development Unit

The current year’s amortization expense is $688,147 (2015 – $217,942). The

amortization is included in the infrastructure expenses and professional stewardship and responsibilities expenses in the Statement of Operations and Changes in Net Assets.

Additions of $45,253 included in intangible assets are non-cash transactions as they

were not paid as at June 30, 2016 (2015 – $99,631), and were included in accounts payable and accrued charges.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

11

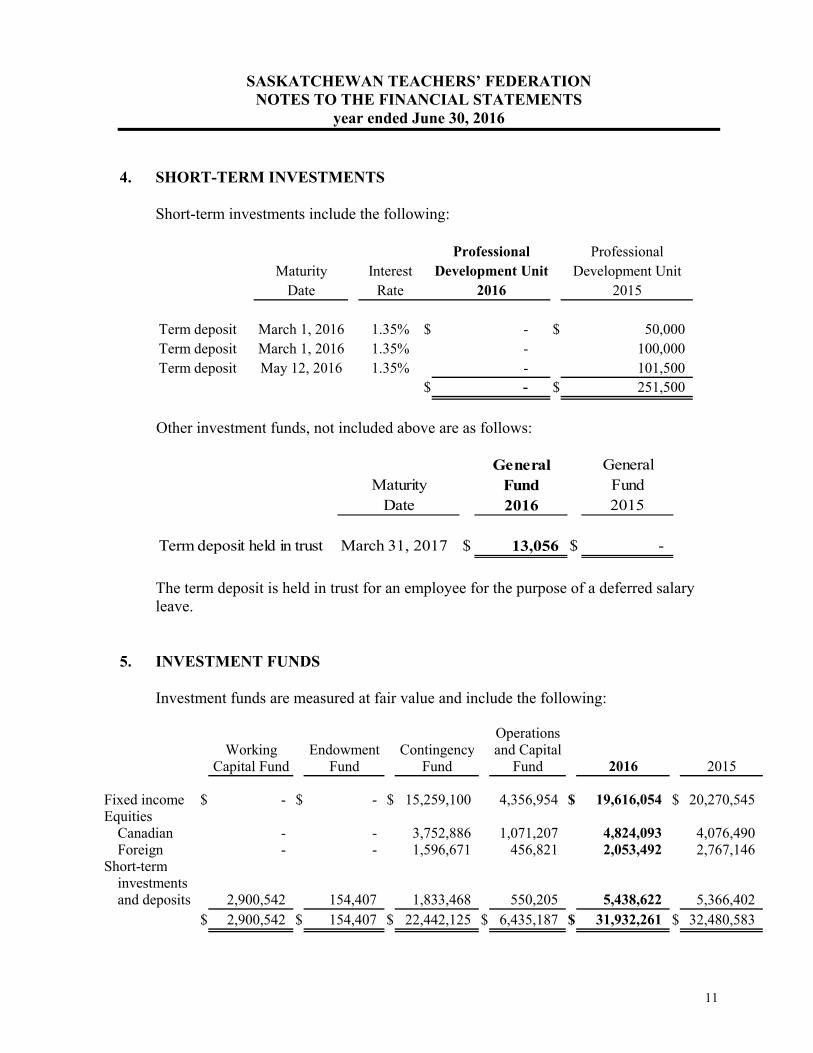

4. SHORT-TERM INVESTMENTS Short-term investments include the following:

Professional ProfessionalMaturity Interest Development Unit Development Unit

Date Rate 2016 2015

Term deposit March 1, 2016 1.35% $ - $ 50,000 Term deposit March 1, 2016 1.35% - 100,000 Term deposit May 12, 2016 1.35% - 101,500

$ - $ 251,500

Other investment funds, not included above are as follows:

General GeneralMaturity Fund Fund

Date 2016 2015

Term deposit held in trust March 31, 2017 $ 13,056 $ -

The term deposit is held in trust for an employee for the purpose of a deferred salary leave.

5. INVESTMENT FUNDS Investment funds are measured at fair value and include the following:

OperationsWorking Endowment Contingency and Capital

Capital Fund Fund Fund Fund 2016 2015

Fixed income $ - $ - $ 15,259,100 4,356,954 $ 19,616,054 $ 20,270,545Equities

Canadian - - 3,752,886 1,071,207 4,824,093 4,076,490 Foreign - - 1,596,671 456,821 2,053,492 2,767,146

Short-terminvestmentsand deposits 2,900,542 154,407 1,833,468 550,205 5,438,622 5,366,402

$ 2,900,542 $ 154,407 $ 22,442,125 $ 6,435,187 $ 31,932,261 $ 32,480,583

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

12

5. INVESTMENT FUNDS (continued) Other investment funds, not included above are as follows:

General GeneralMaturity Fund Fund

Date 2016 2015

Term deposit held in trust August 31, 2017 $ 54,078 $ 48,792

The term deposit is held in trust for an employees for the purpose of a deferred salary leave. Greystone Managed Investments Inc. is the investment manager appointed by the Federation to manage the pooled investment funds of the Federation. The Federation’s investment (expense) income is as follows:

Professional Operations

General Development Working Endowment Contingency and Capital

Fund Unit Capital Fund Fund Fund Fund 2016 2015

Interest $ (932) $ 340 $ 15,521 $ 988 $ 11,179 $ 3,261 $ 30,357 $ 49,544

Dividends - - - - 1,216,679 348,079 1,564,758 1,514,690

Realized gain

on sale of

investment funds - - - - 255,568 128,878 384,446 529,477

Investment

management fees - - (3,029) (202) (29,090) (8,448) (40,769) (41,823)

$ (932) $ 340 $ 12,492 $ 786 $ 1,454,336 $ 471,770 $ 1,938,792 $ 2,051,888

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

13

6. ACCOUNTS RECEIVABLE

ProfessionalGeneral Development Contingency

Fund Unit Fund 2016 2015

Membership fees $ 1,101,382 $ - $ 71,799 $ 1,173,181 $ 1,129,739 Saskatchewan Teachers'

Federation – Members’Health Plan 54,545 - - 54,545 -

Saskatchewan Teachers' Federtion – Portaplan 14,427 - - 14,427 -

Saskatchewan Teachers' Federtion – IncomeContinuance Plan 558,805 - - 558,805 -

Saskatchewan Teachers’Retirement Plan 201,008 - - 201,008 63,900

Saskatchewan Teachers’Federation Employees’Pension Plan 6,235 - - 6,235 2,128

Trade receivables andaccruals 12,519 25,872 - 38,391 26,657

$ 1,948,921 $ 25,872 $ 71,799 $ 2,046,592 $ 1,222,424

7. PENSION COSTS AND OBLIGATIONS

Plan for Federation Employees Who Are Not Members of a Teachers’ Pension Plan The Federation measures its accrued defined benefit obligations and the fair value of the Plan assets for accounting purposes as at June 30 of each year. Based on the most recent actuarial determination of pension plan benefits for funding purposes completed as at June 30, 2013 and extrapolated to June 30, 2016, the status of the defined benefit pension plan is as follows:

2016 2015

Fair value of plan assets $ 31,116,340 $ 31,153,379 Defined benefit obligation 29,672,492 27,851,095 Defined benefit asset $ 1,443,848 $ 3,302,284

The next required actuarial determination of pension plan benefits for funding purposes to be filed with the Saskatchewan Financial Services Commission Pension Division is due by December 31, 2016 with an effective date of June 30, 2016.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

14

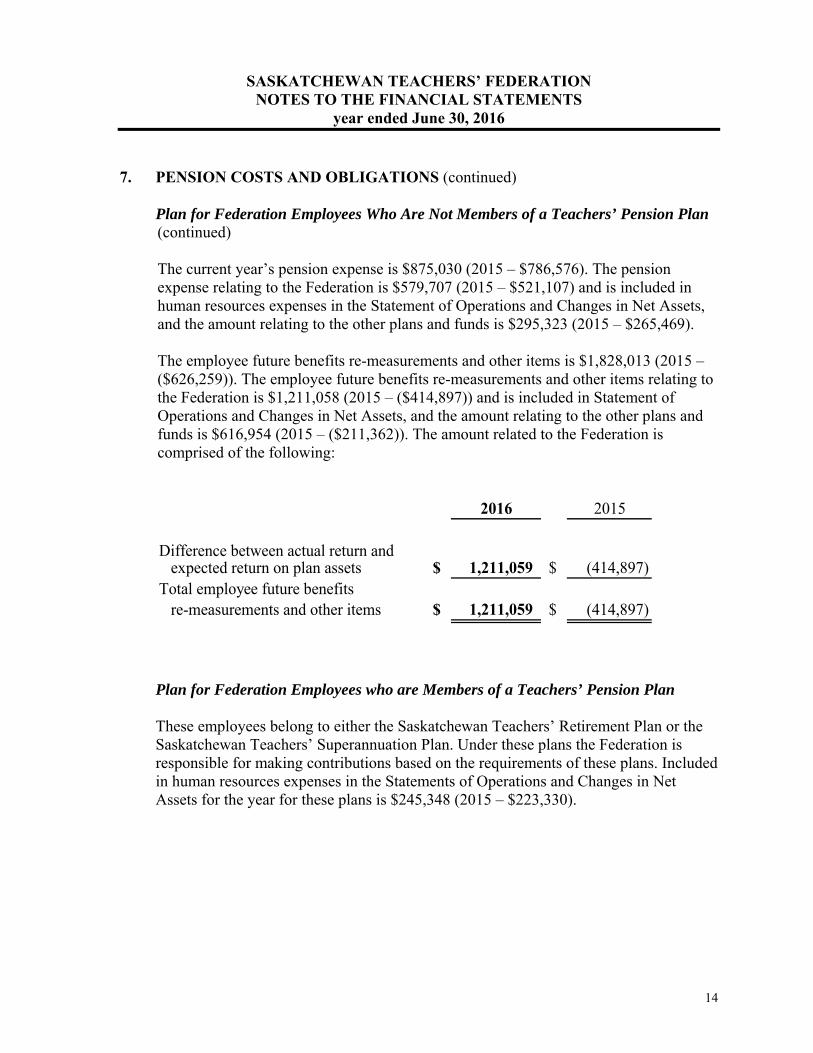

7. PENSION COSTS AND OBLIGATIONS (continued) Plan for Federation Employees Who Are Not Members of a Teachers’ Pension Plan (continued) The current year’s pension expense is $875,030 (2015 – $786,576). The pension expense relating to the Federation is $579,707 (2015 – $521,107) and is included in human resources expenses in the Statement of Operations and Changes in Net Assets, and the amount relating to the other plans and funds is $295,323 (2015 – $265,469). The employee future benefits re-measurements and other items is $1,828,013 (2015 – ($626,259)). The employee future benefits re-measurements and other items relating to the Federation is $1,211,058 (2015 – ($414,897)) and is included in Statement of Operations and Changes in Net Assets, and the amount relating to the other plans and funds is $616,954 (2015 – ($211,362)). The amount related to the Federation is comprised of the following:

2016 2015

Difference between actual return and expected return on plan assets $ 1,211,059 $ (414,897) Total employee future benefits re-measurements and other items $ 1,211,059 $ (414,897)

Plan for Federation Employees who are Members of a Teachers’ Pension Plan

These employees belong to either the Saskatchewan Teachers’ Retirement Plan or the Saskatchewan Teachers’ Superannuation Plan. Under these plans the Federation is responsible for making contributions based on the requirements of these plans. Included in human resources expenses in the Statements of Operations and Changes in Net Assets for the year for these plans is $245,348 (2015 – $223,330).

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

15

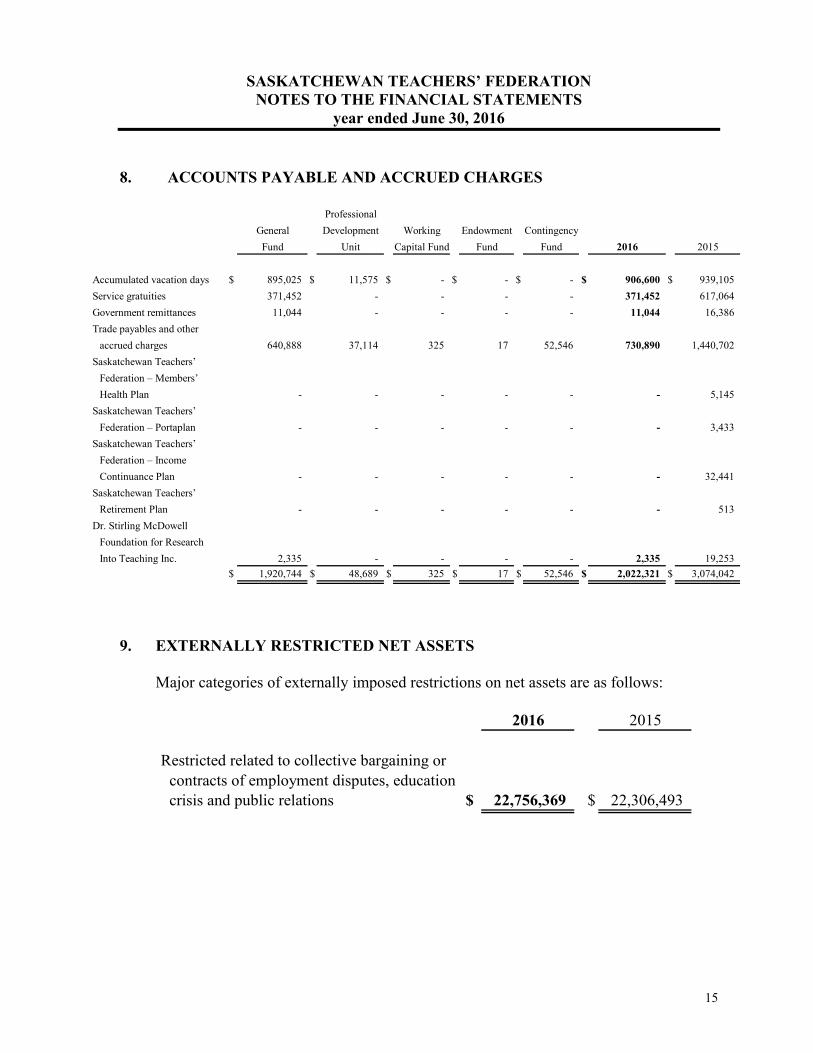

8. ACCOUNTS PAYABLE AND ACCRUED CHARGES

Professional

General Development Working Endowment Contingency

Fund Unit Capital Fund Fund Fund 2016 2015

Accumulated vacation days $ 895,025 $ 11,575 $ - $ - $ - $ 906,600 $ 939,105

Service gratuities 371,452 - - - - 371,452 617,064

Government remittances 11,044 - - - - 11,044 16,386

Trade payables and other

accrued charges 640,888 37,114 325 17 52,546 730,890 1,440,702

Saskatchewan Teachers’

Federation – Members’

Health Plan - - - - - - 5,145

Saskatchewan Teachers’

Federation – Portaplan - - - - - - 3,433

Saskatchewan Teachers’

Federation – Income

Continuance Plan - - - - - - 32,441

Saskatchewan Teachers’

Retirement Plan - - - - - - 513

Dr. Stirling McDowell

Foundation for Research

Into Teaching Inc. 2,335 - - - - 2,335 19,253

$ 1,920,744 $ 48,689 $ 325 $ 17 $ 52,546 $ 2,022,321 $ 3,074,042

9. EXTERNALLY RESTRICTED NET ASSETS

Major categories of externally imposed restrictions on net assets are as follows:

2016 2015

Restricted related to collective bargaining orcontracts of employment disputes, educationcrisis and public relations $ 22,756,369 $ 22,306,493

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

16

10. FINANCIAL INSTRUMENTS

The Federation is exposed to various risks through its financial instruments. The following analysis provides a measure of the Federation’s risk exposure and concentrations at June 30, 2016. Market Risk Market risk is the risk of loss that may arise from change in market factors such as interest rates, foreign currency rates, and equity prices. The Federation is exposed to this market risk in its investing activities.

The STF Executive approves the sections of the Investment Objectives and Policy Statement (“IOPS”) common to all Federation plans and funds based on a recommendation from the Investment and Services Committee and delegates governance responsibilities for management of the assets of the Federation to the Budget, Finance and Audit Committee through approval of the terms of reference. The STF Executive by recommendation of the Budget, Finance and Audit Committee approves the IOPS schedule specific to the Federation and is responsible for monitoring investment performance to ensure compliance with the investment policy and to ensure a risk management program is in place. The investment manager is responsible for managing market risk in accordance with the Federation’s IOPS. The external consultant reports quarterly, to the Investment and Services Committee, on the investment manager’s performance which includes compliance with the policy and regulatory requirements. All exceptions noted are to be reported to the Budget, Finance and Audit Committee. a) Interest rate risk

Interest rate risk refers to the adverse consequences of interest rate changes on the Federation’s cash flows and net assets.

The investment portfolio of the Federation is directly exposed to interest rate risk in respect of its fixed income and short-term investments and deposits. Fixed rate instruments subject the Federation to a fair value risk while the floating rate instruments subject it to a cash flow risk. To manage the interest rate risk, the STF Executive has adopted an approach whereby investments are strategically distributed, on a long-term basis, among several classes of assets to reduce exposure to investment volatility.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

17

10. FINANCIAL INSTRUMENTS (continued)

Market Risk (continued)

b) Foreign currency risk

Foreign currency exposure arises from the Federation’s holdings of non-Canadian investments, which as at June 30, 2016, consist of pooled investments which comprise 6.4% or $2,053,492 (2015 – 8.5% or $2,767,146) of the total portfolio.

Maximum exposure in any single foreign investment is 10% of the market value of

the Federation’s foreign equity portfolio. Investments in individual equities shall not exceed 10% of the outstanding shares of the issuing corporation and at least 20 different equity holdings shall exist in the portfolio, either directly or through

index replication instruments. No more than 15% of the foreign equity portfolio shall be invested in stocks that fall outside of the relevant benchmark index.

c) Equity price risk

Equity price risk is the risk that the fair value or future cash flows of an equity investment will fluctuate because of changes in market prices (other than those arising from interest rate risk or foreign currency risk), whether those changes are caused by factors specific to the individual equity instrument, or factors affecting similar equity instruments traded in the market.

The investment portfolio is directly exposed to equity price risk in respect of its

pooled equities which total $6,877,585 at June 30, 2016 (2015 – $6,843,636).

The IOPS limits the total direct investment in a single equity investment to 10% of the total market value of the Federation’s Canadian equity portfolio. At least 20 different Canadian equity holdings shall exist in the portfolio, either directly or through index replication instruments. No more than 15% of the Canadian equity portfolio shall be invested in stocks that fall outside of the S&P/TSX composite index.

The business of the Federation necessitates the management of credit risk. Credit risk is the potential financial loss resulting from the failure of a customer or counterparty to settle its financial and contractual obligations of the Federation, as and when they fall due. The Federation limits credit risk by dealing with investees that are considered to be of high quality.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

18

10. FINANCIAL INSTRUMENTS (continued)

Credit Risk Credit risk concentration exists where a significant portion of the portfolio is invested in securities which have similar characteristics or obey similar variations relating to economic or political conditions.

This risk is managed by strategically diversifying investments, on a long-term basis, among several classes of assets. The assets of the Federation are directly exposed to credit risk in respect of its pooled fixed income, pooled short-term investments and deposits, term deposits, accounts receivable and cash. As at June 30, 2016, the Federation’s maximum exposure to credit risk was $27,795,085 (2015 – $28,368,357) being the total of the carrying values of these assets. The IOPS requires that all short-term investments have a minimum rate of R1 or equivalent rating as rated by a recognized bond rating agency at time of purchase. The IOPS requires that all bonds and debentures have a rating of BBB or equivalent as rated by a recognized bond rating agency at time of purchase. The IOPS limits the Federation to holding not more than 5% of the market value of fixed income securities in any one non-government entity and not more than 2.5% of the market value of fixed income securities in a single BBB issuer at the time of purchase. The IOPS limits the total direct investment in bonds rated BBB to 20% of the market value of the fixed income portfolio. Private placement bonds shall not exceed 5% of the fixed income portfolio market value. Investments in foreign issuers shall have a minimum rating of A and no single foreign issuer may represent more than 1% of the total fixed income portfolio. Foreign currency exposure is limited to 10% of the market value of the fixed income portfolio. None of the assets in the investment portfolio are past due or impaired as at June 30, 2016 (2015 – none).

Liquidity Risk

The business of the Federation necessitates the management of liquidity risk. Liquidity

risk is the risk of being unable to meet financial commitments, under all circumstances, without having to raise funds at unreasonable prices or sell assets on a forced basis.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

19

10. FINANCIAL INSTRUMENTS (continued)

Liquidity Risk (continued) As at June 30, 2016, the Federation has current financial liabilities of $2,022,321 (2015

– $3,074,042) relating to accounts payable and accrued charges. In addition, it has an ongoing obligation to pay benefits to members of the Saskatchewan Teachers’ Federation Employees’ Pension Plan in respect of pensions payable, which the actuarial present value totalled $29,672,492 for the year ended June 30, 2016 (2015 – $27,851,095).

At June 30, 2016, the Federation held cash and money market instruments, as well as

fixed income and equities which are readily available to settle such obligations. 11. RELATED PARTY TRANSACTIONS

During the year, the Federation entered into transactions with the following related parties: Saskatchewan Teachers’ Federation – Members’ Health Plan, a health benefits plan administered by the Federation. Saskatchewan Teachers’ Federation – Portaplan, a voluntary insurance plan administered by the Federation. Saskatchewan Teachers’ Federation – Income Continuance Plan, a compulsory insurance plan administered by the Federation. Saskatchewan Teachers’ Retirement Plan, a pension plan administered by the Federation. Saskatchewan Teachers’ Federation Employees’ Pension Plan, a contributory defined benefit pension plan for selected employees of the Federation. Dr. Stirling McDowell Foundation for Research Into Teaching Inc., a registered charity with the Federation as its sole member.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

20

11. RELATED PARTY TRANSACTIONS (continued) Revenues Administration fees represent a reimbursement of costs related to the internal support services provided to the Saskatchewan Teachers’ Federation – Members’ Health Plan, Saskatchewan Teachers’ Federation – Portaplan, Saskatchewan Teachers’ Federation – Income Continuance Plan, Saskatchewan Teachers’ Retirement Plan, Saskatchewan Teachers’ Federation Employees’ Pension Plan and Dr. Stirling McDowell Foundation for Research Into Teaching Inc. During the year, the Federation received the following administration fees:

2016 2015Saskatchewan Teachers’ Federation – Members’ Health Plan $ 216,900 $ 217,002 Saskatchewan Teachers’ Federation – Portaplan 130,800 143,300 Saskatchewan Teachers’ Federation – Income Continuance Plan 537,500 598,700 Saskatchewan Teachers’ Retirement Plan 763,500 818,700 Saskatchewan Teachers’ Federation – Employees’ Pension Plan 20,100 24,800 Dr. Stirling McDowell Foundation for Research Into Teaching Inc. 17,900 20,700

$ 1,686,700 $ 1,823,202

Direct cost service revenue represents a reimbursement of the cost of salaries and benefits for services rendered by the Federation. The Saskatchewan Teachers’ Federation – Professional Development Unit includes an amount of $144,300 in the professional stewardship and responsibilities expenses in the Statement of Operations and Changes in Net Assets. During the year, the Federation received the following direct cost service revenue:

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

21

11. RELATED PARTY TRANSACTIONS (continued) Revenues (continued)

2016 2015Saskatchewan Teachers’ Federation – Members’ Health Plan $ 73,100 $ 62,560 Saskatchewan Teachers’ Federation – Portaplan 63,800 57,860 Saskatchewan Teachers’ Federation – Income Continuance Plan 104,800 107,300 Saskatchewan Teachers’ Retirement Plan 267,810 320,191 Saskatchewan Teachers’ Federation – Employees’ Pension Plan 33,900 32,480 Dr. Stirling McDowell Foundation for Research Into Teaching Inc. 88,200 38,550 Saskatchewan Teachers’ Federation – Professional Development Unit 144,300 126,000

$ 775,910 $ 744,941

Fixed asset overhead recovery represent a recovery of costs related to certain capital assets that are used by the Saskatchewan Teachers’ Federation – Members’ Health Plan, Saskatchewan Teachers’ Federation – Portaplan, Saskatchewan Teachers’ Federation – Income Continuance Plan and Saskatchewan Teachers’ Retirement Plan. During the year the Federation received the following fixed asset overhead recovery costs:

2016 2015

Saskatchewan Teachers' Federation – Members’ Health Plan $ 38,814 $ 28,704 Saskatchewan Teachers’ Federation – Portaplan 7,715 2,478 Saskatchewan Teachers’ Federation – Income Continuance Plan 45,217 24,780 Saskatchewan Teachers’ Retirement Plan 60,747 29,700

$ 152,493 $ 85,662

The Federation charges the plans and the Dr. Stirling McDowell Foundation for Research Into Teaching Inc. costs to recover certain expenses relating to activities such as printing and photocopying, recorded as part of infrastructure expenses in the Statement of Operations and Changes in Net Assets. During the year, the Federation received the following other charges:

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

22

11. RELATED PARTY TRANSACTIONS (continued) Revenues (continued)

2016 2015Saskatchewan Teachers’ Federation – Members’ Health Plan $ 21,843 $ 32,870 Saskatchewan Teachers’ Federation – Portaplan 16,900 21,813 Saskatchewan Teachers’ Federation – Income Continuance Plan 8,929 8,969 Saskatchewan Teachers’ Retirement Plan 51,970 38,149 Dr. Stirling McDowell Foundation for Research Into Teaching Inc. 5,817 8,008

$ 105,459 $ 109,809

The Federation pays all the operating costs of the building. The Federation then recovers a percentage of these costs from the Saskatchewan Teachers’ Retirement Plan based on its percentage ownership of the building. In 2016, the amount recovered was $428,802 (2015 – $369,242) and is included in the building operations cost recovery revenues in the Statement of Operations and Changes in Net Assets. The Federation carries out property management services for the Saskatchewan Teachers’ Retirement Plan. These costs are recovered directly from the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, and the Saskatchewan Teachers’ Retirement Plan. During the year, the Federation recovered the following building operation recovery amounts:

2016 2015 Property

Management Fees

Operating Costs

Base Rent - Common

Parking Fees Total Total

Saskatchewan Teachers’ Federation – Members’ Health Plan $ 3,776 $ - $ 4,679 $ 960 $ 9,415 $ 9,263 Saskatchewan Teachers’ Federation – Portaplan 779 - 969 480 2,228 3,451 Saskatchewan Teachers’ Federation – Income Continuance Plan 9,457 - 11,725 2,400 23,582 22,455 Saskatchewan Teachers’ Retirement Plan 12,302 428,802 15,425 3,360 459,889 398,692 Saskatchewan Teachers’ Federation – Professional Development Unit - 4,914 2,795 240 7,949 1,452

$ 26,314 $ 433,716 $ 35,593 $ 7,440 $ 503,063 $ 435,313

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

23

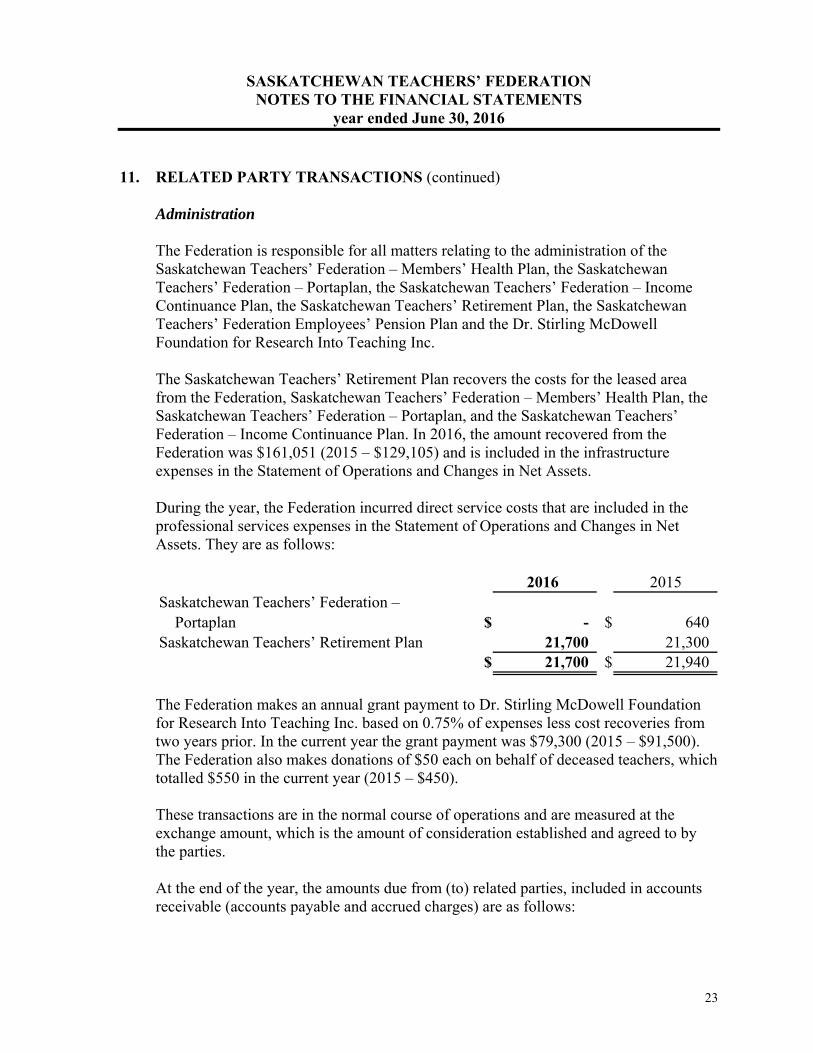

11. RELATED PARTY TRANSACTIONS (continued) Administration The Federation is responsible for all matters relating to the administration of the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, the Saskatchewan Teachers’ Retirement Plan, the Saskatchewan Teachers’ Federation Employees’ Pension Plan and the Dr. Stirling McDowell Foundation for Research Into Teaching Inc. The Saskatchewan Teachers’ Retirement Plan recovers the costs for the leased area from the Federation, Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, and the Saskatchewan Teachers’ Federation – Income Continuance Plan. In 2016, the amount recovered from the Federation was $161,051 (2015 – $129,105) and is included in the infrastructure expenses in the Statement of Operations and Changes in Net Assets. During the year, the Federation incurred direct service costs that are included in the professional services expenses in the Statement of Operations and Changes in Net Assets. They are as follows:

2016 2015Saskatchewan Teachers’ Federation – Portaplan $ - $ 640 Saskatchewan Teachers’ Retirement Plan 21,700 21,300

$ 21,700 $ 21,940

The Federation makes an annual grant payment to Dr. Stirling McDowell Foundation for Research Into Teaching Inc. based on 0.75% of expenses less cost recoveries from two years prior. In the current year the grant payment was $79,300 (2015 – $91,500). The Federation also makes donations of $50 each on behalf of deceased teachers, which totalled $550 in the current year (2015 – $450). These transactions are in the normal course of operations and are measured at the exchange amount, which is the amount of consideration established and agreed to by the parties. At the end of the year, the amounts due from (to) related parties, included in accounts receivable (accounts payable and accrued charges) are as follows:

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

24

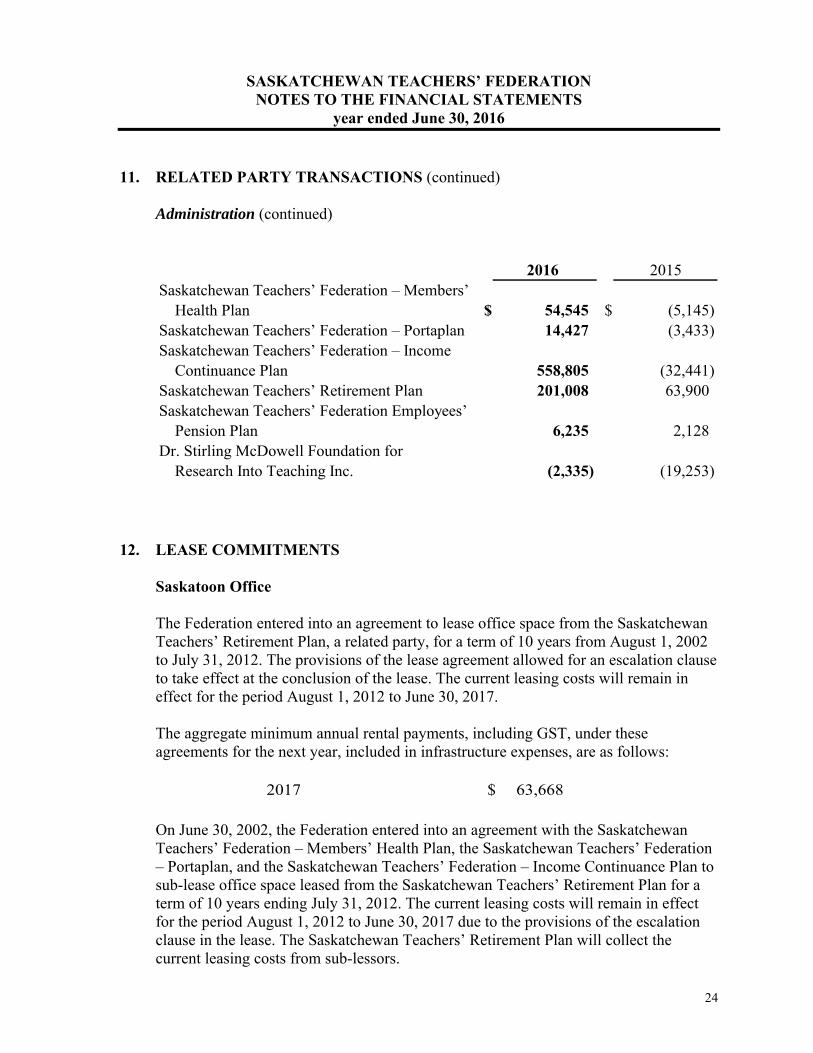

11. RELATED PARTY TRANSACTIONS (continued) Administration (continued)

2016 2015Saskatchewan Teachers’ Federation – Members’ Health Plan $ 54,545 $ (5,145) Saskatchewan Teachers’ Federation – Portaplan 14,427 (3,433) Saskatchewan Teachers’ Federation – Income Continuance Plan 558,805 (32,441) Saskatchewan Teachers’ Retirement Plan 201,008 63,900 Saskatchewan Teachers’ Federation Employees’ Pension Plan 6,235 2,128 Dr. Stirling McDowell Foundation for Research Into Teaching Inc. (2,335) (19,253)

12. LEASE COMMITMENTS

Saskatoon Office The Federation entered into an agreement to lease office space from the Saskatchewan Teachers’ Retirement Plan, a related party, for a term of 10 years from August 1, 2002 to July 31, 2012. The provisions of the lease agreement allowed for an escalation clause to take effect at the conclusion of the lease. The current leasing costs will remain in effect for the period August 1, 2012 to June 30, 2017. The aggregate minimum annual rental payments, including GST, under these agreements for the next year, included in infrastructure expenses, are as follows:

2017 $ 63,668

On June 30, 2002, the Federation entered into an agreement with the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, and the Saskatchewan Teachers’ Federation – Income Continuance Plan to sub-lease office space leased from the Saskatchewan Teachers’ Retirement Plan for a term of 10 years ending July 31, 2012. The current leasing costs will remain in effect for the period August 1, 2012 to June 30, 2017 due to the provisions of the escalation clause in the lease. The Saskatchewan Teachers’ Retirement Plan will collect the current leasing costs from sub-lessors.

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

25

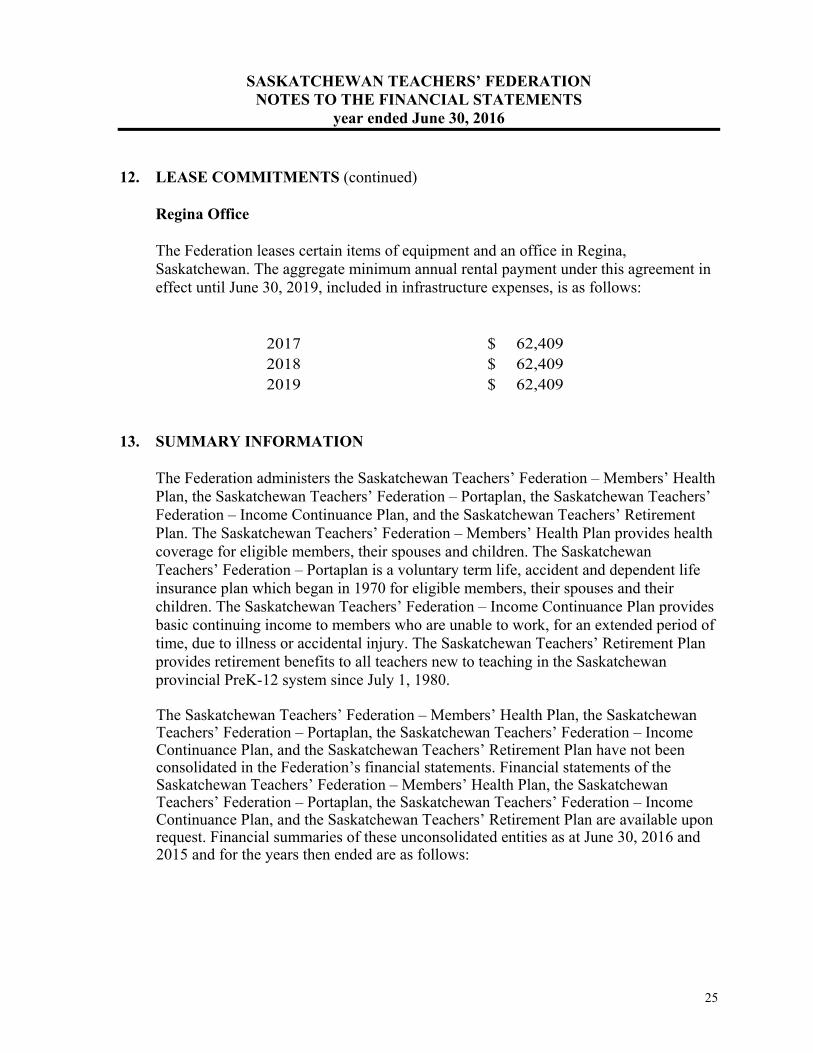

12. LEASE COMMITMENTS (continued) Regina Office

The Federation leases certain items of equipment and an office in Regina, Saskatchewan. The aggregate minimum annual rental payment under this agreement in effect until June 30, 2019, included in infrastructure expenses, is as follows:

2017 $ 62,409 2018 $ 62,409 2019 $ 62,409

13. SUMMARY INFORMATION

The Federation administers the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, and the Saskatchewan Teachers’ Retirement Plan. The Saskatchewan Teachers’ Federation – Members’ Health Plan provides health coverage for eligible members, their spouses and children. The Saskatchewan Teachers’ Federation – Portaplan is a voluntary term life, accident and dependent life insurance plan which began in 1970 for eligible members, their spouses and their children. The Saskatchewan Teachers’ Federation – Income Continuance Plan provides basic continuing income to members who are unable to work, for an extended period of time, due to illness or accidental injury. The Saskatchewan Teachers’ Retirement Plan provides retirement benefits to all teachers new to teaching in the Saskatchewan provincial PreK-12 system since July 1, 1980. The Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, and the Saskatchewan Teachers’ Retirement Plan have not been consolidated in the Federation’s financial statements. Financial statements of the Saskatchewan Teachers’ Federation – Members’ Health Plan, the Saskatchewan Teachers’ Federation – Portaplan, the Saskatchewan Teachers’ Federation – Income Continuance Plan, and the Saskatchewan Teachers’ Retirement Plan are available upon request. Financial summaries of these unconsolidated entities as at June 30, 2016 and 2015 and for the years then ended are as follows:

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

26

13. SUMMARY INFORMATION (continued)

2016 2015Saskatchewan Teachers’ Federation –Members’ Health Plan

Financial positionTotal assets $ 70,489,053 $ 68,489,032

Total liabilities $ 308,936 $ 2,006,779 Total unappropriated/appropriated funds 70,180,117 66,482,253

$ 70,489,053 $ 68,489,032

Results of operationsTotal revenues $ 23,607,283 $ 24,035,838 Total expenses 17,958,475 16,620,796 Unrealized loss in market value of

investment funds (1,897,932) (162,920)

Net revenues $ 3,750,876 $ 7,252,122

Cash flowsCash from operating activities $ 3,136,420 $ 7,767,094 Cash used in investing activities (2,974,382) (8,102,833) Increase (decrease) in cash $ 162,038 $ (335,739)

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

27

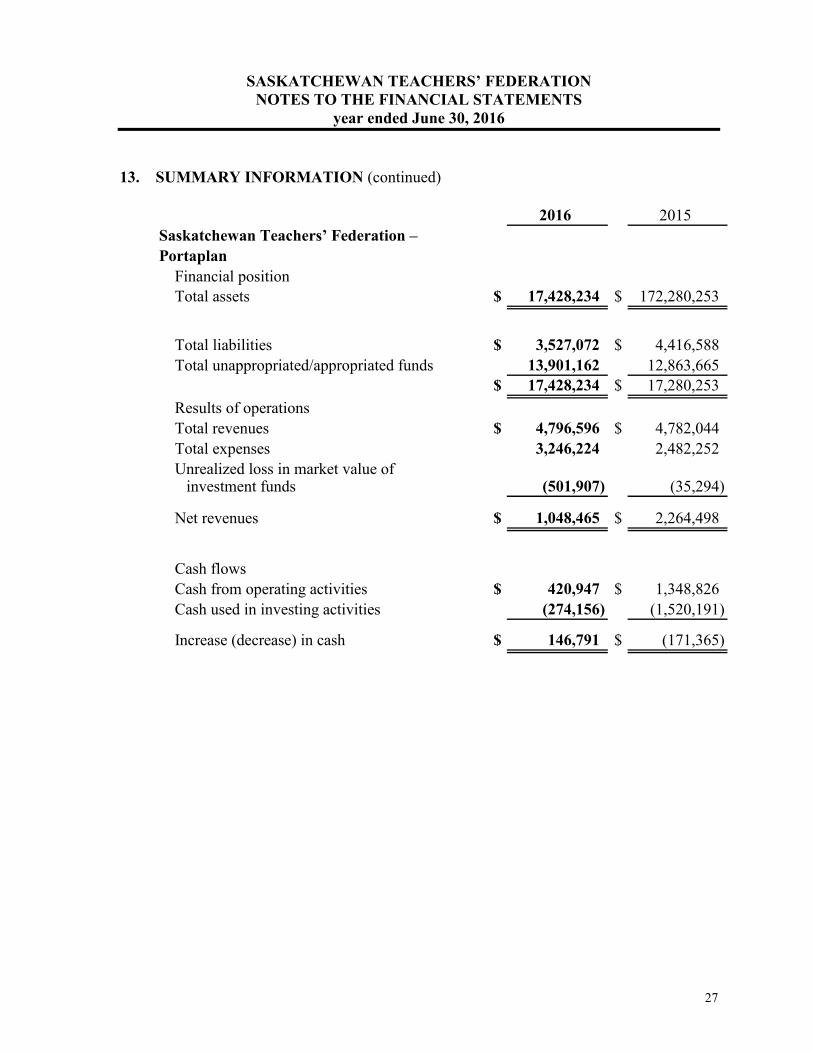

13. SUMMARY INFORMATION (continued)

2016 2015Saskatchewan Teachers’ Federation –Portaplan

Financial positionTotal assets $ 17,428,234 $ 172,280,253

Total liabilities $ 3,527,072 $ 4,416,588 Total unappropriated/appropriated funds 13,901,162 12,863,665

$ 17,428,234 $ 17,280,253

Results of operationsTotal revenues $ 4,796,596 $ 4,782,044 Total expenses 3,246,224 2,482,252 Unrealized loss in market value of

investment funds (501,907) (35,294)

Net revenues $ 1,048,465 $ 2,264,498

Cash flowsCash from operating activities $ 420,947 $ 1,348,826 Cash used in investing activities (274,156) (1,520,191)

Increase (decrease) in cash $ 146,791 $ (171,365)

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

28

13. SUMMARY INFORMATION (continued)

2016 2015Saskatchewan Teachers’ Federation –Income Continuance Plan

Financial positionTotal assets $ 192,883,922 $ 185,334,908

Total liabilities $ 97,582,193 $ 87,958,900 Total equity 95,301,729 97,376,008

$ 192,883,922 $ 185,334,908

Results of operationsTotal revenues $ 19,054,282 $ 30,743,944 Total expenses 20,694,591 16,306,194 Total income (1,640,309) 14,437,750 Total employee future benefits re-measurements and other items (433,970) 148,673 Total income and comprehensive income $ (2,074,279) $ 14,586,423

Cash flowsCash from operating activities $ 4,279,515 $ 5,515,901 Cash used in investing activities (4,428,836) (5,039,725)

Decrease (increase) in cash $ (149,321) $ 476,176

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

29

13. SUMMARY INFORMATION (continued)

2016 2015(Restated)

Saskatchewan Teachers’ Retirement PlanFinancial positionTotal assets $ 4,556,241,000 $ 4,445,067,000 Total liabilities 11,834,000 11,754,000 Net assets available for benefits $ 4,544,407,000 $ 4,433,313,000

Changes in pension obligationBeginning balance $ 4,027,883,000 $ 3,737,113,000 Increases (Restated) 381,246,000 366,822,000 Decreases (98,535,000) (76,052,000) Ending balance $ 4,310,594,000 $ 4,027,883,000

Results of operationsIncreases in assets $ 213,725,000 $ 504,396,000 Decreases in assets 102,631,000 79,866,000 Net increase in net assets $ 111,094,000 $ 424,530,000

During the current year, Saskatchewan Teachers’ Retirement Plan management identified an error in an actuarial calculation of the benefits accrued and net interest on accrued pension benefits for the year ended June 30, 2015. The error had no impact on the financial statements for any periods beginning prior to July 1, 2014. As a result of the correction the comparative figures as at and for the year ended June 30, 2015 presented above have been restated on a retroactive basis to correct the change in pension obligation. The result of the correction decreased the increases in changes in pension obligation by $61,222,000 from $428,044,000 previously reported to $366,822,000 shown above.

14. COMMITMENTS

The Federation has capital commitments into 2017 for building improvements ($43,418) and computer software ($45,253).

SASKATCHEWAN TEACHERS’ FEDERATION NOTES TO THE FINANCIAL STATEMENTS

year ended June 30, 2016

30

15. COMPARATIVE FIGURES

Certain comparative figures have been reclassified to conform to the current year’s presentation. On the Statement of Financial Position the intangible assets have increased by $35,317 and the prepaid expenses have decreased by $35,317. On the Statement of Cash Flows, the net revenues (expenses) have decreased by $8,890, the additions to intangible assets have increased by $44,207 and changes in non-cash working capital have decreased by $35,317.