san diego county employees retirement association (sdcera)

TRANSCRIPT

0 Elibrary_templates/cover_sep

San Diego County Employees Retirement Association (SDCERA)

July 21, 2011

Strategy Review

1

Biographical Information

6733_cover

David J. Blair, CFAMr. Blair is a senior vice president and account manager in the Newport Beach office. He was a member of PIMCO's municipal portfolio management team from 2006-2010 and was previously a credit analyst for 10 years at Nuveen Investments, focusing on high yield California bonds, primarily in the land-secured sector, as well as utilities, multi-family housing and toll road bonds. Mr. Blair was also an auditor and certified public accountant at Arthur Andersen for three years. He has 17 years of investment experience and holds an MBA from the University of Chicago Graduate School of Business. He holds an undergraduate degree from the University of California, Santa Barbara.

Neel KashkariMr. Kashkari is a managing director and head of new investment initiatives in the Newport Beach office. Prior to joining PIMCO in 2009, Mr. Kashkari served in the U.S. Treasury Department from 2006-2009, first as senior advisor to Secretary Henry Paulson and then as Assistant Secretary of the Treasury. In the latter role, he established and led the Office of Financial Stability and oversaw the Troubled Assets Relief Program (TARP). Before joining the Treasury Department, Mr. Kashkari was a vice president at Goldman Sachs in San Francisco, advising technology companies on financings and mergers and acquisitions. Previously, he was an aerospace engineer at TRW Corporation. He holds both bachelor's and master's degrees in engineering from the University of Illinois at Urbana-Champaign and an MBA from the Wharton School at the University of Pennsylvania.

Julie A. Meggers, CFAMs. Meggers is an executive vice president and account manager in the Newport Beach office, focusing on institutional client servicing. Prior to joining PIMCO in 2003, she was a strategic management consultant with Bain & Company. Prior to that, she was a senior auditor at Arthur Andersen and also lectured at St. Augustine University in Tanzania on auditing and cost accounting. She has 12 years of investment experience and holds an MBA from Harvard Business School. She earned undergraduate degrees from Santa Clara University and is a certified public accountant.

2 6733_cover

Agenda

I. SDCERA Objectives

II. Portfolio Performance & Positioning

III. Economic Outlook & Challenges Facing Policy Makers

IV. PIMCO Update

3

SDCERA: Objectives and Requirements

Portfolio benchmarked to 3 month LIBOR and customized to meet SDCERA’s liquidity, volatility, and return objectives

Focus keenly on risk management and limiting downside risk with the primary objectives of capital preservation and liquidity

Consistently add value through a conservative investment approach focused on diversified sources of value added

Establish an ongoing partnership with PIMCO's cash management team to facilitate a portfolio structure that is dynamically adjusted to fit SDCERA’s needs

Provide superior client service, including highly accessible professionals, proactive idea generation and customized reporting, to exceed SDCERA’s expectations

6733_ST_objectives_SDCERA

The objectives above were provided by SDCERA and there is no assurance that the portfolio or strategy will achieve its investment objectives or that the stated results will be achieved.

4

Performance Review

6733_ST_perf_retu

As of June 30, 2011

Before Fees (%) 1.2 1.2 0.9 0.3

After Fees (%) 1.1 1.1 0.9 0.3

3 Month LIBORIndex (quarterly reset) (%) 0.3 0.2 0.2 0.1

9 Mos.

SinceInception09/16/10 6 Mos. 3 Mos.

SDCERA-Short TermMarket Value at Inception: 1,597,862,714$

Contributions / Withdrawals 613,747,745

Net Investment Earnings 28,755,173

Market Value as of Jun. 2011 2,240,365,632$

5

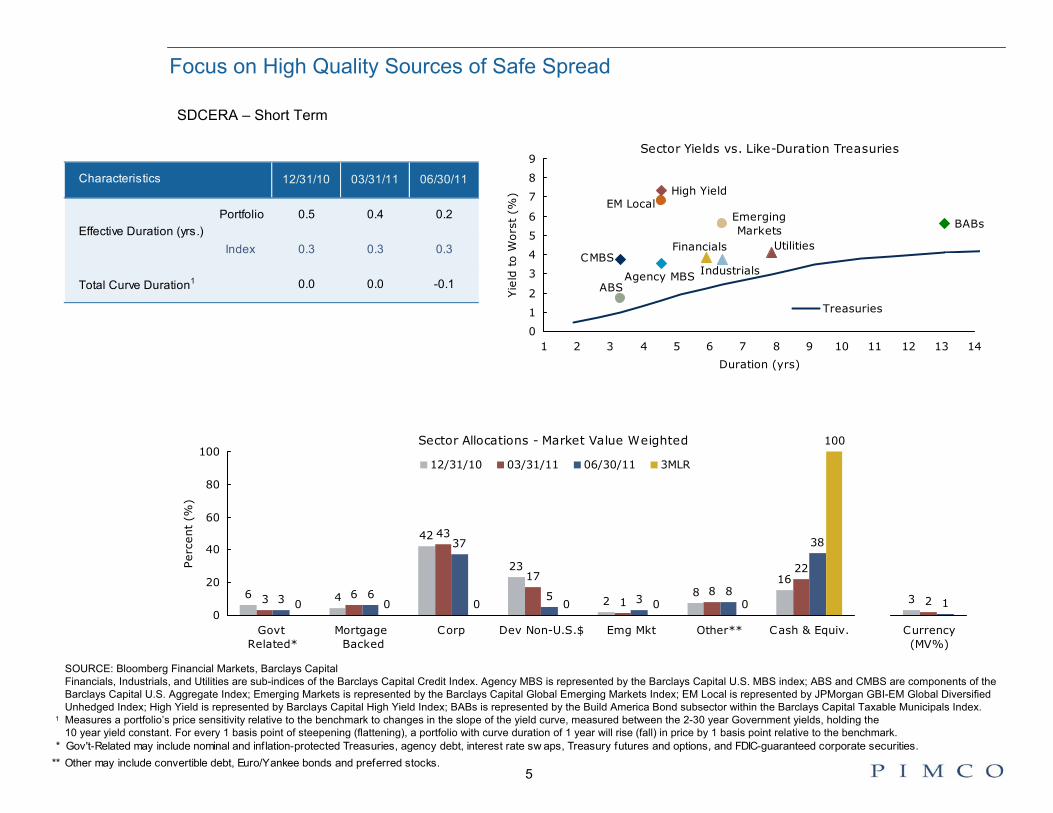

Focus on High Quality Sources of Safe Spread

6733_ST_attrib_02

SDCERA – Short Term

SOURCE: Bloomberg Financial Markets, Barclays CapitalFinancials, Industrials, and Utilities are sub-indices of the Barclays Capital Credit Index. Agency MBS is represented by the Barclays Capital U.S. MBS index; ABS and CMBS are components of the Barclays Capital U.S. Aggregate Index; Emerging Markets is represented by the Barclays Capital Global Emerging Markets Index; EM Local is represented by JPMorgan GBI-EM Global Diversified Unhedged Index; High Yield is represented by Barclays Capital High Yield Index; BABs is represented by the Build America Bond subsector within the Barclays Capital Taxable Municipals Index.

1 Measures a portfolio’s price sensitivity relative to the benchmark to changes in the slope of the yield curve, measured between the 2-30 year Government yields, holding the 10 year yield constant. For every 1 basis point of steepening (flattening), a portfolio with curve duration of 1 year will rise (fall) in price by 1 basis point relative to the benchmark.

12/31/10 03/31/11 06/30/11

Portfolio 0.5 0.4 0.2

Index 0.3 0.3 0.3

Total Curve Duration1 0.0 0.0 -0.1

Characteristics

Effective Duration (yrs.)

* Gov't-Related may include nominal and inflation-protected Treasuries, agency debt, interest rate sw aps, Treasury futures and options, and FDIC-guaranteed corporate securities.** Other may include convertible debt, Euro/Yankee bonds and preferred stocks.

Sector Allocations - Market Value Weighted

6 4

42

23

28

16

3 6

43

17

18

22

3 6

37

5 38

38

0 0 0 0 0 0

100

0

20

40

60

80

100

Govt Related*

Mortgage Backed

Corp Dev Non-U.S.$ Emg Mkt Other** Cash & Equiv.

Perc

ent

(%)

12/31/10 03/31/11 06/30/11 3MLR

3 2 1

Currency(MV%)

Sector Yields vs. Like-Duration Treasuries

Emerging Markets

High Yield

BABs

Treasuries

UtilitiesFinancials

IndustrialsCMBS

ABSAgency MBS

EM Local

0

1

2

3

4

5

6

7

8

9

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Duration (yrs)

Yie

ld t

o W

ors

t (%

)

6

Strong Performance While Preserving High Quality Focus

SDCERA – Short Term

+

+++

+

+

2Q ‘11

Attribution

+

+++

Yield Enhancement Strategies High average portfolio quality Held fixed income securities that offered a higher yield than Treasuries

– Mortgage-Backed Securities– Investment-Grade Credit– Emerging Markets

+Currency Exposure

Held currencies which were expected to benefit from our forecast of a secular decline in the U.S. Dollar

– EM Currencies

+

Global Interest Rate Strategies Diversified interest rate exposure in bond markets where we believed yields would fall

– Duration positioning slightly longer than benchmark for most of the quarter

– Employed strategies that would benefit from rolldown

Since Inception*

Strategy

6733_ST_attrib_01

* Inception date: 09/16/10.

7

Economic Outlook & Challenges Facing Policy Makers

Where did we come from?

– The Bubble Economy

Where are we now?

– A Bumpy Journey to a New Normal

What does the future hold?

– An opportunity to enhance U.S. competitiveness

8

Increasing debt in the U.S. economy fueled increasing equity returns and higher valuations

SOURCE: Haver AnalyticsAs of December 31, 2009

Over the Past 30 Years, We Became Used to Never-Ending P/E Expansion

0

10

20

30

40

50

60

70

52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09

S&

P500 P

/E

9

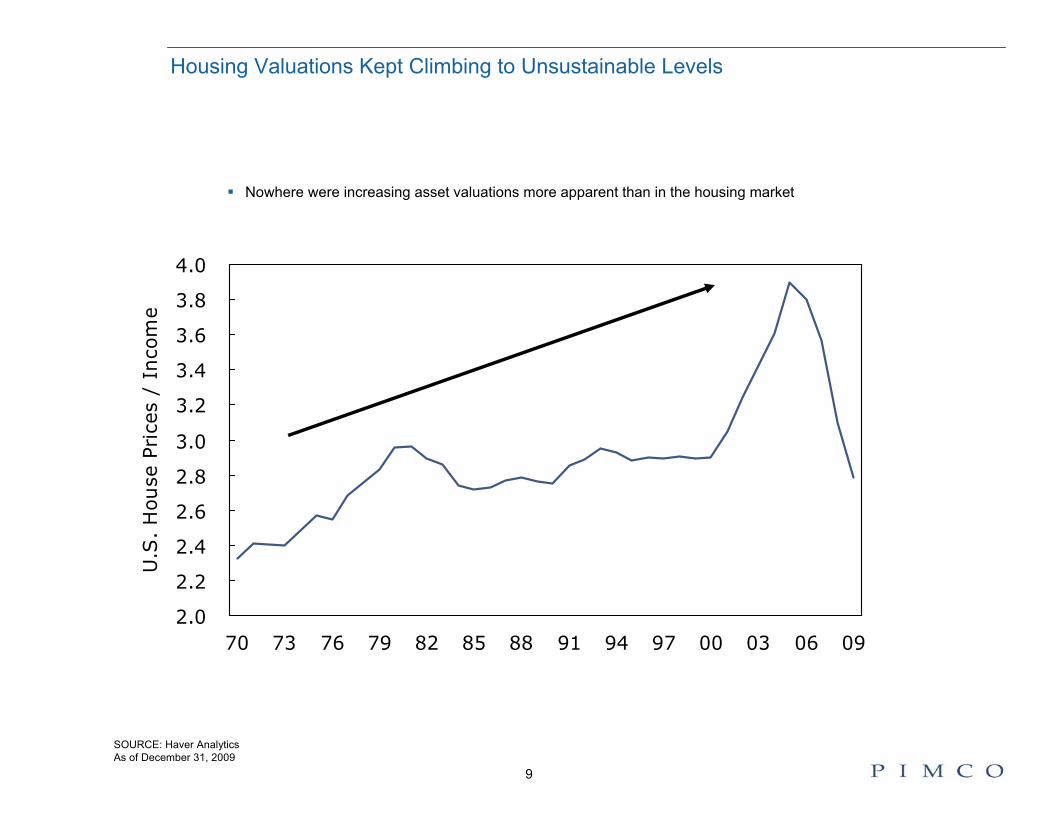

Nowhere were increasing asset valuations more apparent than in the housing market

Housing Valuations Kept Climbing to Unsustainable Levels

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

70 73 76 79 82 85 88 91 94 97 00 03 06 09

U.S

. H

ouse

Pri

ces

/ In

com

e

SOURCE: Haver AnalyticsAs of December 31, 2009

10

The Bubble Economy was Fueled by Ever-Increasing Debt

0%

50%

100%

150%

200%

250%

52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 00 03 06 09

Deb

t as

% o

f U

.S.

GD

P

Federal Households Corps State/Local

26%Households 96%

62% Federal 55%

31%

Corporate 77%9%

State/Local 17%

Total Debt has increased from 128% to 245% of GDP

SOURCE: Haver AnalyticsAs of December 31, 2009

11

Then, the Bubble Economy Popped

The necessary housing correction sparked a global financial crisis

The financial system was at risk of total collapse, which could have led to another Great Depression

Governments took extraordinary actions to take the deepest risks off the table –the risks of a catastrophic overcorrection and economic meltdown

– Massive central bank liquidity

– Bank capital

– Government guarantees

– Fiscal stimulus

The heart attack was stabilized – but the patient is still recovering

– The financial crisis triggered a terrible recession with devastating unemployment

12

3-5 Year Outlook: A Bumpy Journey to a New Normal (Driving without a Spare)

Private sector deleveraging – strained government balance sheets

Slower growth

Sustained high unemployment

Reregulation

Restrained globalization

More uncertainty: flatter distribution of possible outcomes. The impossible / improbable becomes possible

Refer to Appendix for additional outlook information.

13

What Does the New Normal Mean for Investors?

Developing economies lead global growth; developed markets grow more slowly

– Look globally for the best risk-adjusted return opportunities, rather than domestically

Increased inflationary uncertainty

– Potential short-run deflation; longer-term inflation possible

Investment returns across asset classes likely to be tempered and more volatile

Substantial differentiation between regions, countries and companies

– Invest up the quality curve

Be prepared for a wide range of economic and investment outcomes

Heightened volatility can provide buying opportunities, but with it comes risk –requires better tail hedging

Refer to Appendix for additional investment strategy, outlook, and risk information.

14SOURCE: International Monetary Fund (IMF), World Economic Outlook April 2010Refer to Appendix for forecast information.

global_advantage_review_42

Average Projected Real GDP Growth During 2010-2011 (Percent)

Emerging Market Dynamism Outpacing Industrial Countries

Below 0

Between 0 and 3

Between 3 and 6

Above 6

15 global_advantage_review_39

SOURCE: International Monetary Fund (IMF), World Economic Outlook April 2010

Traditional Patterns of Indebtedness Are Being Reversed

0

25

50

75

100

125

150

Perc

ent

(%)

G20 Industrialized Countries G20 Emerging Markets

Gross Government Debt-to-GDP Ratios

20072010F2015F

Gross Government Debt-to-GDP Ratios

16

Consumers Have Begun Paying Down Debt

SOURCE: Federal Reserve Bank of New York Consumer Credit PanelAs of September 30, 2010

Consumer debt grew 172% in under 10 years. It has since fallen 7% and will take time to reach a sustainable equilibrium

$0

$2

$4

$6

$8

$10

$12

$14

99:Q

199

:Q3

00:Q

100

:Q3

01:Q

101

:Q3

02:Q

102

:Q3

03:Q

103

:Q3

04:Q

104

:Q3

05:Q

105

:Q3

06:Q

106

:Q3

07:Q

107

:Q3

08:Q

108

:Q3

09:Q

109

:Q3

10:Q

110

:Q3

Tota

l C

onsu

mer

Debt

Outs

tandin

g (

$ T

rillio

n).

Other

Student Loan

Credit Card

Auto Loan

HE Revolving

Mortgage

$4.6

$12.5

$11.6

17

What Should Policymakers Do?

Attempts to re-inflate the bubble economy will fail – the dollars eventually must be turned off:

– Ongoing stimulus to maintain consumer spending

– Tax credits to boost housing

– Temporary jobs such as the census

The bubble economy must adjust to a new fundamental equilibrium, which may include:

– Lower consumer price increases

– Lower nominal GDP growth

– Lower asset returns

Monetary policy has limitations

18

If Prices Fall, is the U.S. Headed for a Deflationary Spiral?

Not necessarily

Deflation is scary for a number of reasons:

– Traditional policy tools are of limited usefulness

– Relatively little experience for policymakers to rely upon

But there is a reason deflation is rare – demographics are a powerful force:

– A growing population is a natural countervailing force to runaway deflation

– Runaway inflation is far more common than a deflationary spiral

The demographics of Japan and the U.S. have similarities, but also important differences

19

U.S. Working-Age Population is Forecast to Continue to Grow

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Fore

cast

ed A

nnual

Gro

wth

Rat

e of

Wor

king-

Age

Popula

tion

(15-6

4)

Japan USA China Western Europe

Japan’s working-age population has been shrinking for more than a decade. The U.S. working-age population is expected to continue growing.

SOURCE: United Nations World Population Database

20

U.S. Demographic Trends Lead to Funding Challenges Even More Than to Deflation

SOURCE: United Nations World Population Database

50%

55%

60%

65%

70%

75%

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

Perc

enta

ge

of P

opula

tion

Bet

wee

n

15 a

nd 6

4 Y

ears

Old

Japan USA China Western Europe

Japan: (13%)

Western Europe:(11%)

USA:(5%)

China:(10%)

% Reductionin forecast period

A declining percentage of the population that is working-age will strain fiscal balance sheets via entitlement programs that rely on current funding.

21

Policymakers Should Focus on Enhancing U.S. Economic Competitiveness

1. Policymakers should allow the necessary adjustment to take place, while helping families navigate through the transition:

– Unemployment benefits

– Worker retraining

2. Improve the productive capacity of the U.S. economy by investing in:

– Education

– Basic research

– Infrastructure

– And encouraging high-skilled immigration

3. Give the private sector confidence to invest and create jobs:

– Fundamental pro-growth tax reform

– Minimize regulatory uncertainty

– Control long-term deficits

It is difficult to design government policies that will quickly create sustainable jobs – the private sector needs to create them

22

Unchecked, Entitlement Spending Will Crowd Out Investment and Harm Competitiveness

SOURCE: Congressional Budget Office – Long-term Budget Outlook (June 2010)

-50

0

50

100

150

200

250

300

350

400

1800 1850 1900 1950 2000 2050

Feder

al D

ebt

Hel

d b

y th

e Pu

blic

as

% o

f G

DP

World War I

"ExtendedBaseline"

current lawno AMT

patch, or other routineadjustment

GreatDepression

"Alternative Fiscal

Scenario" continuation

ofcurrent

underlying fiscal policy

World War II

The CBO forecasts either crippling tax increases or unsustainable deficits if entitlement programs are not restructured

23

Entitlement Spending is Forecast to Grow Unsustainably

SOURCE: Congressional Budget Office – Long-term Budget Outlook (June 2010)

0

2

4

6

8

10

12

14

16

18

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

Proj

ecte

d S

pen

din

g o

n E

nti

tlem

ents

(%

of

GD

P)

Alternative Fiscal Scenario Social Security Outlays

FederalHealth Care

Spending10.9%

3.4%

Social SecuritySpending

6.2%

4.1%

Due to demographic trends and risings costs, social security and health care are expected to grow unsustainably

24

Our Political System is Capable of Making Hard Choices (Though not Often)

Although rare, the U.S. political system is capable of making unpopular decisions

– 2008 TARP was passed by Democrat and Republican leaders

– Deeply unpopular but necessary to prevent economic devastation

Fiscal crisis is more challenging than the financial crisis:

– Must make cuts before the crisis is upon us

– Bailing out the financial system violated beliefs in fairness

Three steps are necessary to tackle entitlements

– Economy needs to grow so people feel secure

– Emotional bruising from financial crisis needs to heal

– Leaders need to risk their own political fortunes to make the case for entitlement reform

Refer to Appendix for additional outlook information.

25

What are the Policy Options to Deal With Entitlements?

Means testing

Increasing the retirement age

Changing the indexation of benefits to slow their growth

Raising revenue (potentially as part of comprehensive pro-growth tax reform)

The good news is, unlike most crises, we actually see this crisis coming and the policy solutions are easy to list

The challenge is finding the will to make hard choices before we have an acute fiscal crisis

26

An Acute Fiscal Crisis Could Severely Affect U.S. Economic Competitiveness

U.S. could lose its reserve currency status and could face substantial inflation

Treasury borrowing costs could increase meaningfully

Crowding out could leave less money for other national priorities, such as infrastructure, basic research, defense, education

CBO estimates a 4% increase in Treasury rates is almost $500bn additional debt service costs by 2015

– 10X Homeland Security spending

– 5X Education spending

Once confidence in Treasuries is lost, it could take years, or longer, to return

Rapid fiscal adjustment forced by an acute crisis will be far more painful for American families than making difficult choices in advance

Refer to Appendix for additional outlook information.

27

Conclusion – A Challenge and an Opportunity to Invest in Our Future

Decades of debt accumulation went on about as long as it could

It created the conditions that triggered the terrible financial crisis of 2008

Government policies were effective in preventing another Great Depression, but there are limits to what governments can quickly do to sustainably boost economic growth and create jobs

In the Bumpy Journey to a New Normal, we will see continued deleveraging and modest economic growth and asset appreciation. There are no quick, easy solutions

Rather, policymakers should focus on taking structural actions to enhance U.S. economic competitiveness

– Investing in people, research and infrastructure

– Controlling runaway deficits

– Implementing pro-growth tax reform

We have an opportunity. Do we have the political will to take advantage of it?

Refer to Appendix for additional outlook information.

28 1cs_pimco_update_04

PIMCO Snapshot

Global Presence

People

HistoryFounded in 1971

Specialty fixed income manager

Assets under management:

employees: investment professionalstechnical and support

Highly experienced Experience at PIMCO– All investment professionals

– Senior professionals

1,748

13 7

19 7

Average Years

As of March 31, 2011

Newport BeachIP’s: 261

New YorkIP’s: 62

TorontoIP’s: 6

LondonIP’s: 71 Munich

IP’s: 50

SingaporeIP’s: 7

Hong KongIP’s: 6 Tokyo

IP’s: 20

SydneyIP’s: 8

ZurichIP’s: 4

AmsterdamIP’s: 1

$ 1,282.2 B

1,252496

29

PIMCO Continues to Enhance Services and Resources to Meet Client Needs

1cs_pimco_update_01

As of March 31, 2011

Newport Beach Seminars– 2-day Fundamentals

– 5-day Investment Seminars

– Both sessions available in June and September

Regional Offerings

Topical Conference Calls

PIMCO Institute Educational Programs Robust Recruitment of Top Talent

Global EquityAnne Gudefin

20 years experienceCharles Lahr

16 years experience

Emerging Markets Equity

Masha Gordon 13 years experience

Client Analytics– Simple and accessible reporting

– Breakdown of allocation and assumptions

– Summary of factors and volatility

Product Solutions– Existing and customized

– Evaluation of impact on allocation

Solutions by Client-type, and Allocation Goals

– Liability Driven Investing

– Retirement, including Target Date

– Inflation and Rising Rates

– Portfolio and Tail Risk Hedging

Risk Factor Analysis– Customized analysis of target asset

allocation

– Decompose and identify sources of portfolio risk

– Focused portfolio analysis

PIMCO Solutions

30 6733_pimco_orga_assets_01

Assets Under Management by Strategy

PIMCO’s expertise spans asset classes to provide effective solutions that meet investor needs

Potential differences in asset totals are due to rounding. * Stable Value assets have not been netted from U.S. Total Return, US Moderate Duration and U.S. Low Duration assets. Total Stable Value assets equal $28.8 B

As of March 31, 2011

Alternative Absolute Return Strategies Long/short or unconstrained bond strategies, benchmarked to LIBOR indices $34.63Investments: Commodities Commodity-linked exposures enhanced with active bond portfolios 30.88

Real Estate Real Estate-linked exposure backed by inflation index bonds 0.22CBO / CLO Collateralized bonds / loan obligations 5.93

Asset Allocation: Asset Allocation Strategies Global Multi Asset, All Asset, All Asset All Authority 41.17

Equities: StocksPLUS® Combines derivatives-based equity exposure with active bond management 17.28Pathfinder Global and Europe - only deep value equity strategy 1.33

Fixed Intermediate* Total Return, Moderate Duration 510.5Income: Cash Management* Money Market, Short-Term, Low Duration 107.79

Long Duration Focus on long-term bonds; asset liability management 85.85Real Return TIPS and other inflation-hedging strategies 68.54Credit Investment Grade Corporates, High Yield 125.92Mortgages Emphasis on management of mortgage pass-throughs 42.88Global Non-U.S. and global multiple currency formats 104.53Emerging Markets Emerging market debt, EM local currency, active EM currency 48.63Diversified Income Global credit combining corporate and emerging markets debt 21.30Municipals Tax-efficient total return management 12.55Other 22.27

Total Assets Under Management: $ 1,282.29 B