sales tax 2013 presented by: denise benbrook 2-18-2013 2-22-2013

TRANSCRIPT

Sales Tax 2013

Presented by: Denise Benbrook

2-18-20132-22-2013

WHAT WILL BE COVERED

Fundraisers and Fees

Sale/ Not a Sale

Taxable Sales/Non-Taxable Sales

Tax Fee Days

Proper Reporting of Sales Tax

Fundraiser Application/Recap

Questions

Change in Procedures

Why – State requires us to report quarterly

January – March: Filed in April April – June: Filed in July July – September: Filed in October October – December: Filed in January

Need to report all Sales, not just sales we owe tax on.

Fundraiser or Fees Fees: Example: Funds collected for class projects… Art Class, Shop, Band, Dues for Student Clubs..

Most often fees are placed in 461 accounts. Fundraisers: Fundraiser App. is completed and approved by the Deputy Superintendent. $10,000.00 or more in gross sales require Board approval A fund-raising activity may be defined as any activity involving participation of a student body, a school recognized student group undertaken for the purchase of deriving funds for a school or a school faculty sponsored group.

Decision Tree

Sale Not a Sale

Not Taxabl

e

Taxabl

e

Tax-Free Day

Pay Tax

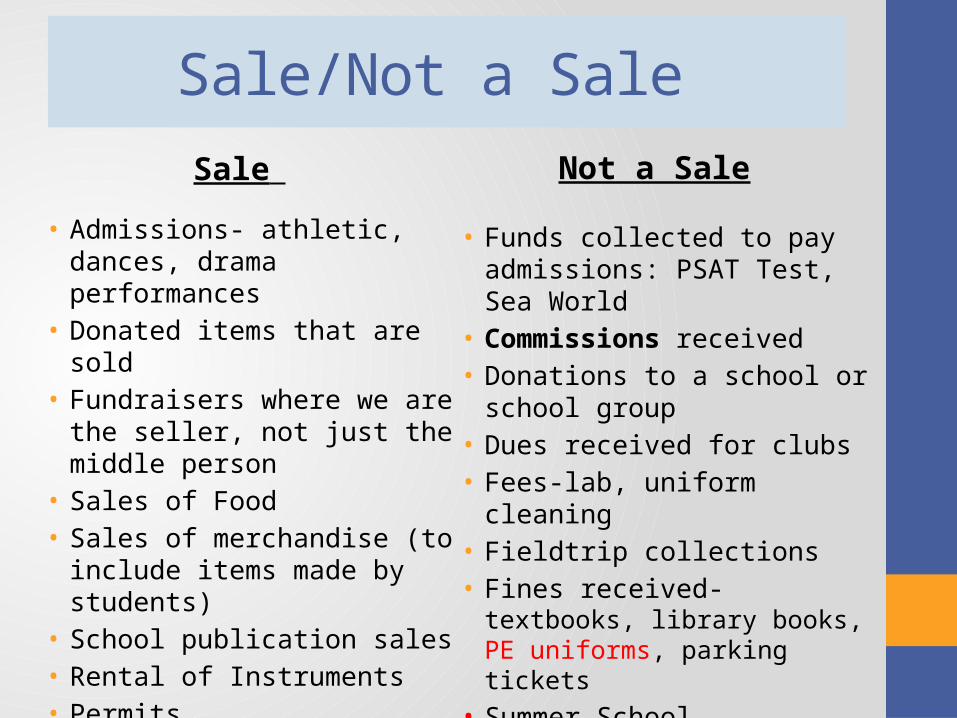

Sale/Not a Sale

Sale

• Admissions- athletic, dances, drama performances

• Donated items that are sold • Fundraisers where we are

the seller, not just the middle person

• Sales of Food • Sales of merchandise (to

include items made by students)

• School publication sales • Rental of Instruments • Permits• Banquet Fees • Uniforms-Cheer, PE, Dance, Club

Shirts

Not a Sale

• Funds collected to pay admissions: PSAT Test, Sea World

• Commissions received • Donations to a school or

school group• Dues received for clubs • Fees-lab, uniform cleaning• Fieldtrip collections • Fines received- textbooks,

library books, PE uniforms, parking tickets

• Summer School

Taxable Sales vs. Non-Taxable Sales

Taxable Sales• Schools must collect & remit taxes for all taxable

items that do not have a specific exemptions Examples: supplies, publications, school store, rentals, Fees for materials when the end product becomes a possession of the student. (Example: Reeds, Sewing Kits)

Non-Taxable Sales• Report as sales on Tax Return but pay no tax• Examples: Admissions, food items, parking permits, Ad Sales, etc.

Both Sales are reported to the Comptroller’s Office.See Page 12 and 13 of the Activity Manual for a more detailed listing.

Taxable Sales /Non-Taxable Sales

Taxable Sales

• Vending- Non edible items when we

service the machine. (Example: pencils)

• School Store- all items except food

• Transcripts • Copies• Santa Pictures-we are the

seller • Catering • Spirit items

Non-Taxable Sales

• Ad Sales-Yearbook • Admissions • Food items sold during

fundraising • Car Washes • Parking Permits

All sales, both taxable and non-taxable must be reported to the Comptroller’s Office.

Tax Free Days Who qualifies?

Each school district, each school, and each bona fide

student club of each school.Clubs should be organized. Have By-Laws, monthly meetings, elected officers. Must be organized for some

business or activity other than instruction.For Example: The school-wide fundraiser qualifies for a tax-free day. The Basketball Club qualifies, but the basketball team does not. The Senior Club qualifies, but not one particular senior class that has seniors in it.

Groups meeting for classroom instruction or team sports are not categorized as a Bona Fide club and do not qualify for the tax-free day sales.

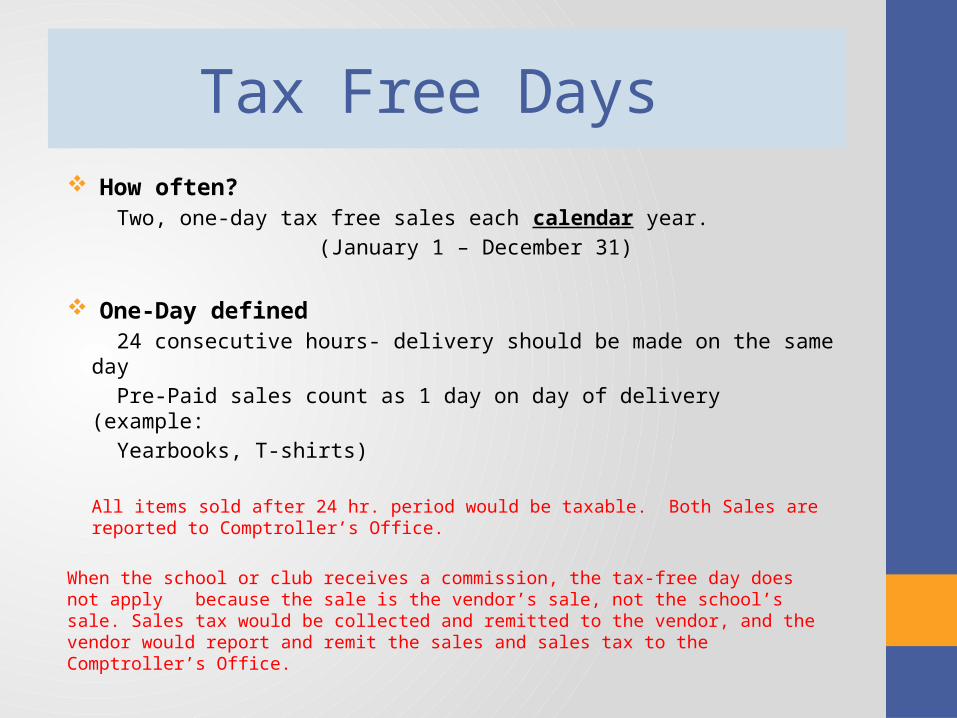

Tax Free Days How often?

Two, one-day tax free sales each calendar year. (January 1 – December 31)

One-Day defined 24 consecutive hours- delivery should be made on the same day Pre-Paid sales count as 1 day on day of delivery (example: Yearbooks, T-shirts)

All items sold after 24 hr. period would be taxable. Both Sales are reported to Comptroller’s Office.

When the school or club receives a commission, the tax-free day does not apply because the sale is the vendor’s sale, not the school’s sale. Sales tax would be collected and remitted to the vendor, and the vendor would report and remit the sales and sales tax to the Comptroller’s Office.

Calculating Sales Tax Add tax to selling

price

Example- Selling price is $1.00and the tax rate is 8.25%, the school would collect $1.08 from the buyer for each item sold.

Including tax in the price of

the item being sold

Example- An item is sold for $1.00, including tax. Tax will be subtracted for the amount collected on the sale. If this method is used, and the tax rate is 8.25%, divide the sale price or total collections by 1.0825($1.00/1.0825= $.92) $1.00 -$.92=$.08 is the amount owed for state and local tax.

Calculating Sales Tax Taxes Paid to Vendor

Item is purchased for $1.00 plus tax of $.08, total $1.08 from a vendor. The item is sold by the school for $2.00. Tax is owed on the difference between purchase price of $1.00 and $2.00.

In this example, we would report the $2.00 as a Sale, with $.07 being owed for taxes.

$2.00 sale with taxes included. $2.00/1.0825 = $1.85, this would be the sale amount. The $.15 remaining would be the taxes owed. $.08 was paid to the vendor, so $.07 is still owed to the Comptroller’s Office.

Tax Rate by Campus 8.25%

• ADAPT• Alvin Elementary• Alvin High School • Alvin Jr High • Alvin Primary • ASSETS• EC Mason • Glenn York • Longfellow• Manvel High School • Mark Twain • Mary Marek • Nolan Ryan • Passmore• Stevenson • Walt Disney • Wilder

6.75%

These campuses do not pay City Taxes of 1.5%.

• Don Jeter• Fairview Jr High • Harby Jr High • Hood Case • Manvel Jr High• Savannah Lakes

City Tax Rate= 1.5%County Tax Rate=.50%State Tax Rate=6.25%

Sales Tax Form Alvin ISD

Report of Sales and Sales Tax

January 1 - March 31,2013

Tax Rate 1.0825

Instructions:

For each deposit from a Sale, record it on a line.

Include that amount in one of the next three columns: Non-Taxable, One Day Tax Free, Taxable Sale Including Tax

Deposit Date

Club/Organization Name

Acct. Number Description

Total Deposit

Non-Taxable Sale/Tax Paid on PO

One Day Tax Free

Taxable Sales Including Tax

Taxable Sales Excluding Tax

Total Tax Due

1/8/13 Library 6399-23 Pencils 55.00 55.00 50.81 4.19

1/16/13 Library 6399-15 Copies 34.00 34.00 31.41 2.59

1/23/13 Campus 2191-11 T-shirts 255.00 255.00

1/29/13 Campus 6399-77 Permits 375.00 375.00

2/6/13 Campus 6399-12 Soccer Uniforms 425.00 392.61 Taxes paid on PO

2/8/13 Campus 6399-18 Transcripts 16.00 16.00 14.78 1.22

2/11/13 Choir 2191-12 Carnations 125.00 125.00 115.47 9.53

2/19/13 Campus 6399-16 Yearbooks 625.00 625.00

2/20/13 Cheer 2191-17 Concessions 267.00 267.00

2/22/13 Band 6269-55 Instrument Rental 120.00 120.00 110.85 9.15

2/16/13 Lego Team 6399-24 T-shirts 325.00 325.00 300.23 24.77

Subtotals 2,622.00 1,034.61 880.00 675.00 623.56 51.44 675.00

Taxes Paid on PO

425.00 32.39Tax Paid on PO Total Sales $2,538.17 $2,538.17 Total Sales

392.61

Amnt. Reported as Sales Taxable Sales $623.56 $51.44 Taxes Owed

Taxes Owed $51.44 $32.39 Taxes Paid on PO

$2,622.00 Equals Total Deposits

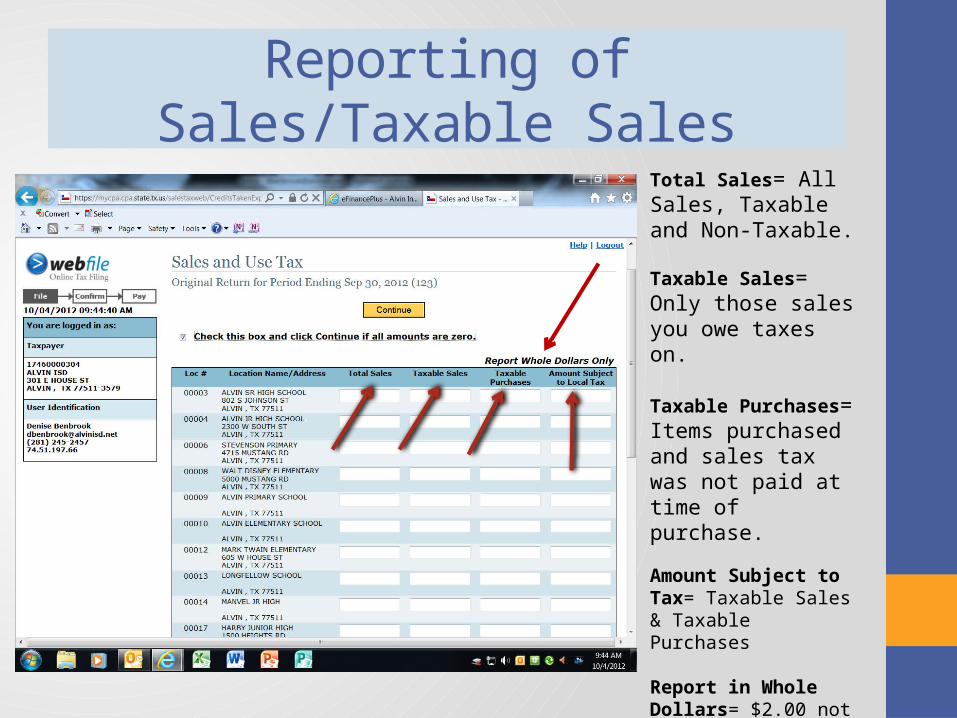

Reporting of Sales/Taxable Sales

Total Sales= All Sales, Taxable and Non-Taxable.

Taxable Sales= Only those sales you owe taxes on.

Taxable Purchases=Items purchased and sales tax was not paid at time of purchase.

Amount Subject to Tax= Taxable Sales & Taxable Purchases

Report in Whole Dollars= $2.00 not $1.98Round to the nearest $$

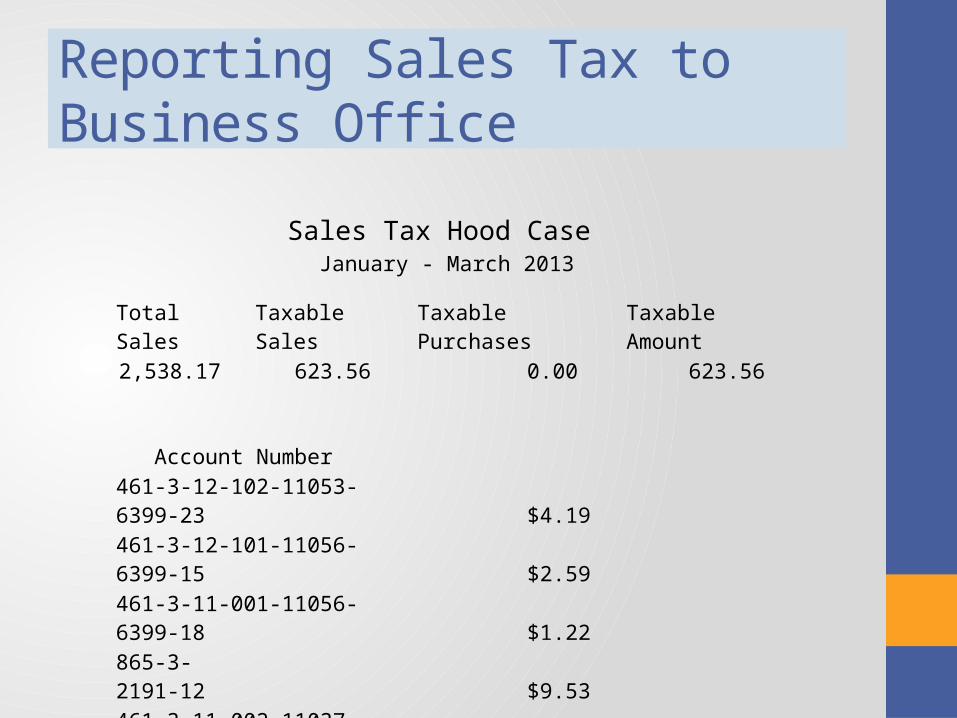

Reporting Sales Tax to Business Office

Sales Tax Hood Case January - March 2013

Total Sales Taxable Sales Taxable Purchases Taxable Amount2,538.17 623.56 0.00 623.56

Account Number 461-3-12-102-11053-6399-23 $4.19461-3-12-101-11056-6399-15 $2.59461-3-11-001-11056-6399-18 $1.22865-3-2191-12 $9.53461-3-11-002-11037-6269-55 $9.15461-3-11-041-11041-6399-24 $24.77

$51.45

Fundraiser Apps./Recap • Fundraiser Apps. Exempt? Fundraisers you receive Commissions on are not Tax Exempt.

• RecapCompleted within30 days of the completion of the fundraiser.

Texas Resale Certificate Schools may issue a Resale Certificate in lieu of paying tax to suppliers when purchasing taxable items to resale during its designated tax free sale days.

Questions?

Survey