sagar cements limited - sifyim.sify.com/sifycmsimg/jan2010/finance/14927293_sagar...sagar cements...

TRANSCRIPT

Sagar Cements Limited

BUY Target Price:Rs.231.00

CMP: Rs.201.25. Market Cap: Rs.3019.15mn.

Date: 12 Jan,2010.

Key Ratios:

Particulars FY08 A FY09 A FY10E FY11E

OPM(%) 26 20 24 24

NPM(%) 14 5 9 8

ROE(%) 30 9 20 19

ROCE(%) 17 9 20 19

P/BV(x) 2.05 0.98 1.26 1.03

P/E(x) 6.95 11.40 6.42 5.56

EV/EBDITA(x) 2.90 5.04 2.52 2.24

Debt

Equity(x)

1.95 1.25 1.11 0.99

Key Data:

Sector Cement

Face Value 10.00

52 wk. High/Low (Rs.) 271.75/111.00

Volume (2 wk. Avg.) 11650

BSE Code 502090

SYNOPSIS

• We initiated the coverage of Sagar Cements Ltd

and set a target price of Rs.231. for medium to long

term gains.

• Sagar Cements Limited is one of the most modern

mini cement plants in the state of Andhra Pradesh.

The most sophisticated state-of-the-art technology

it uses is one of the strengths of the company.

• The company has recently enhanced its clinker

capacity to 2.1 million TPA and its cement capacity

to 2.5 million TPA.

• It manufactures several of cement and all its

products are sold under brand name of Sagar.

• The revenue of the company for the quarter ended

on Sept 30th increased 264.4% YoY

• The topline of the company are expected to grow

at a CAGR of 43% over 2008A to 2011E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

Table of Content

Investment Highlights ................................................................................................................................... 3

Peer Group Comparison ................................................................................................................................ 5

Financials ....................................................................................................................................................... 7

Charts ............................................................................................................................................................ 9

Outlook and Conclusion .............................................................................................................................. 11

Industry Overview ....................................................................................................................................... 11

Investment Highlights

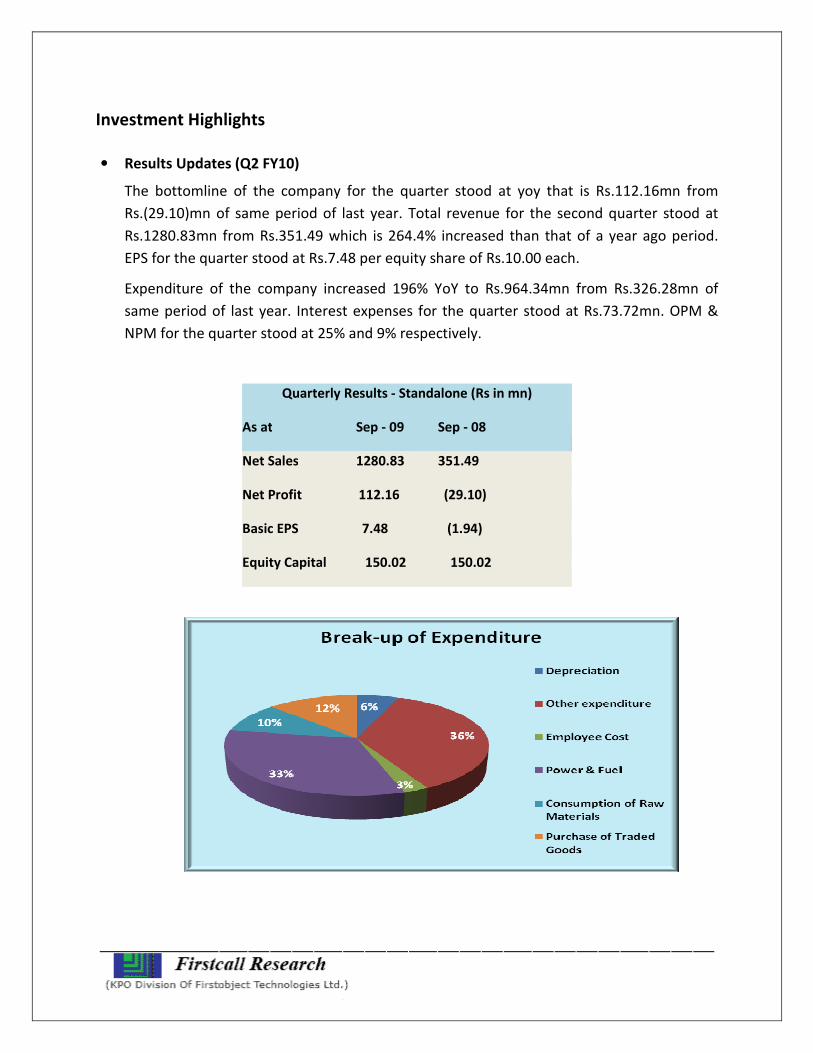

• Results Updates (Q2 FY10)

The bottomline of the company for the quarter stood at yoy that is Rs.112.16mn from

Rs.(29.10)mn of same period of last year. Total revenue for the second quarter stood at

Rs.1280.83mn from Rs.351.49 which is 264.4% increased than that of a year ago period.

EPS for the quarter stood at Rs.7.48 per equity share of Rs.10.00 each.

Expenditure of the company increased 196% YoY to Rs.964.34mn from Rs.326.28mn of

same period of last year. Interest expenses for the quarter stood at Rs.73.72mn. OPM &

NPM for the quarter stood at 25% and 9% respectively.

Quarterly Results - Standalone (Rs in mn)

As at Sep - 09 Sep - 08

Net Sales 1280.83 351.49

Net Profit 112.16 (29.10)

Basic EPS 7.48 (1.94)

Equity Capital 150.02 150.02

In the quarter, realization levels witnessed a drop. However, in the last month of the

quarter Realizations were starting to look better but the recent floods in AP and

neighboring state have Played spoil, as a result of which it is taking longer for the

environment to stabilize.

Andhra Pradesh Plant

During the quarter, the Mattampally plant operated at high utilization levels producing

429,570 tons of clinker and 288,060 tons of cement. The volume of cement production in

Q2 FY2010 increase by about 25 percent when compare to the preceding last quarter and

over six folds when compared to the corresponding quarter last year.

As a continuous drive towards improving its share in new/outside AP markets, the

company was able to sell 17% of its total dispatches in the quarter to various markets

outside the home state,of which about 46% were to the state of Maharastra that translates

to 8% of total dispatches.

Markets

Quantity (in

tons)

Andhra Pradesh 276404

Maharashtra 26395

Karnataka 14892

Orissa 5617

Tamilnadu 5280

Others 5118

Karnataka Plant

The plan to set up a 5.5million ton capacity manufacturing facility in Gulbarga, Karnataka

through a JV with the Vicat Group is progressing as planned. The required licenses to

implement the project have been obtained and the placement of orders for core

equipment will be completed by end of the third quarter of fiscal. The JV has acquired 2000

acres of land including land for the plant as well as mining leases in Karnataka. Of the

estimated project cost of Rs 25 billion, the JV company has invested around Rs 700 millions

towards land acquisition and other necessary/obligatory sanctions.

The facility will have a 5.5 million ton cement grinding unit and a 4 million ton clinkerization

unit. It would also have a 60mw power plant for captive use. At a 4 million ton per anum

cement capacity the company also has sufficient limestone reserves at its disposal.

Company Profile

Sagar Cements Limited was incorporated in the year 1981 with the object, inter-alia, of

manufacturing of cement. The actual commercial journey started on January 26, 1985 with the

production capacity of 66,000 tonnes of OPC per annum at Mattampally, Nalgonda –

Hyderabad.

Sagar Cements Limited, is one of the most modern mini cement plants in the state of Andhra

Pradesh. The most sophisticated state-of-the-art technology it uses is one of the strengths of

the company. The plant is based on Dry Process Rotary Kiln Technology that is used in ‘Standard

Quality' cement companies.

As its contribution to the fast developing modern India, Sagar Group, Sagar Cements has been

playing the major role since 20 years by providing the cement that speaks for itself.

First Mini Plant: The first mini plant of the company is located at Mattampally, Nalgonda

district, located within 35 km from the National Highway No 9 connecting Vijayawada-

Hyderabad.

Subsidiary Company

o Sagar Power Limited

Products

Product range of the company includes:

• Cements of OPC: 53 grade,

• OPC: 43 grade,

• SRC,

• IRS T-40 Super grade,

• Portland Pozzolona Cement and

• Portland Slag Cement.

Peer Group Comparison

Name of the

company

CMP

(As on 12

Jan, 2010)

Market

Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E

(x)

P/BV

(x) Dividend(%)

Sagar Cements

Limited 201.25 3019.15 25.09 8.02

1.57 25

Madras Cements 128.65 30614.8 18.67 6.89 2.43 200

Deccan Cements

Limited 238.00 1666.9 53.64 4.44

0.97 30

Binani Cement

Limited 75.80 15374.8 11.64 6.50

3.23 21

Key Concerns

• Any change in the existing policies of Government of India and/or State Governments or

new policies, providing or withdrawing support to the industries in which the company

operates or otherwise affecting these industries, would adversely affect the supply and

demand balance and competition in markets in which the company operate there by

impacting the margins of the company.

• The Company's exposure to currency risk arises out of the import of materials like coal

for its cement plants and machinery and equipment for its projects.

Financials

12 Months Ended Profit & Loss Account (Standalone)

Particulars FY 08 A FY 09 A FY 10 E FY11 E

(Rs.Mn) 12m 12m 12m 12m

Net Sales 2,231.43 3,065.45 5395.19 6474.23

Other Income 9.96 8.0 22.40 26.88

Total Income 2,241.39 3,073.45 5417.59 6501.11

Expenditure -1,665.48 -2,474.89 -4100.3 -4952.79

Operating Profit 575.91 598.56 1317.25 1548.32

Interest -34.01 -158.99 -302.08 -362.50

Gross Profit 541.90 439.57 1015.17 1185.83

Depreciation -41.35 -187.23 -280.8 -337.0

Profit before Tax 500.55 252.34 734.32 848.81

Tax -190.99 -87.77 -264.4 -305.6

Net Profit 309.56 164.57 469.96 543.24

Equity Capital 133.37 150.02 150.02 150.02

Reserves 914.33 1,772.20 2,242.16 2,785.41

EPS 23.21 10.97 31.33 36.21

Quarterly Ended Profit & Loss Account (Standalone)

Particulars Mar 09 A June 09 A Sep 09 A Dec 09 E

(Rs.Mn) 3m 3m 3m 3m

Net Sales 1,261.48 1,384.06 1,280.83 1408.91

Other Income 3.11 1.25 8.63 6.04

Total Income 1,264.59 1,385.31 1,289.46 1414.95

Expenditure -991.73 -1,028.37 -964.34 -1063.73

Operating Profit 272.86 356.94 325.12 351.22

Interest -59.76 -73.9 -73.72 -81.09

Gross Profit 213.10 283.04 251.40 270.13

Depreciation -65.47 -67.97 -70.33 -73.85

Profit before Tax 147.63 215.07 181.07 196.29

Tax -78.95 -73.13 -68.91 -68.70

Net Profit 68.68 141.94 112.16 127.59

Equity Capital 150.02 150.02 150.02 150.02

EPS 4.58 9.46 7.48 8.50

*A=Actual, E=Estimated

Charts

Comparative Graph

SAGAR CEMENTS LT BSE SENSEX

Outlook and Conclusion

• At the current market price of Rs.201.25, the stock trades at a P/E of 6.42x and 5.56x for

FY10E and FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 2.52x and 2.24x for FY10E and FY11E

respectively.

• Price to Book Value of the stock is expected to be at 1.26 and 1.03 respectively for FY10E and

FY11E.

• EPS of the company for the earnings of FY10E and FY11E are expected to be at Rs.31.33 and

Rs. 36.21 respectively.

• The Net sales of the company are expected to grow at a CAGR of 43% over 2008 to 2011E.

• The plan to set up a 5.5million ton capacity manufacturing facility in Gulbarga, Karnataka

through a JV with the Vicat Group is progressing as planned. The facility will have a 5.5

million ton cement grinding unit and a 4 million ton clinkerization unit.

• We expect that the company will keep its growth story in the coming quarters also. We

recommend ‘BUY’ in this particular scrip with a target price of Rs.231.00. for Medium to

Long Term Gains.

Industry Overview

India is the world's second largest producer of cement after China, with cement companies

adding nearly 11 million tonnes (MT) capacity during April-September 2009, taking the total

installed capacity to around 231 MT by September 2009.

With the boost given by the government to various infrastructure projects, road networks and

housing facilities, growth in the cement consumption is anticipated in the coming years.

According to Jyotiraditya Scindia, Minister of State, Ministry of Commerce and Industry, cement

production could rise to 236.16 MT in FY11 and touch 262.61 MT in FY12.

With almost total capacity utilisation levels in the industry, cement despatches have maintained

a 10 per cent growth rate. Total despatches grew to 170 MT during 2007–08 as against 155 MT

in 2006–07.

Moreover, cement despatches were 12.22 MT in October 2009, showing a growth of 9 per cent

as compared to 11.21 MT in October 2008. During October 2009, cement production was 12.37

MT, registering a growth of 6.54 per cent as compared to 11.61 MT in October 2008. Between

April to October 2009, cement production totaled 89.59 MT while cement despatches totaled

88.72 MT.

A few of the leading manufacturers are UltraTech/Grasim combine, Dalmia Cements, India

Cements, Holcim etc.

Technological change

Continuous technological upgrading and assimilation of latest technology has been going on in

the cement industry. Presently, 93 per cent of the total capacity in the industry is based on

modern and environment-friendly dry process technology and only 7 per cent of the capacity is

based on old wet and semi-dry process technology. There is tremendous scope for waste heat

recovery in cement plants and thereby reduction in emission level.

New Investments

• Dalmia Cement, South India’s second largest cement maker, will invest over US$ 652.6

million to add 10 MT capacity over the next 2-3 years.

• India Cements Ltd will invest US$ 104 billion to set up two thermal power plants in the

southern states of Tamil Nadu and Andhra Pradesh.

• Anil Ambani Group company Reliance Infrastructure will invest US$ 2.1 billion to set up

cement plants with a total capacity of 20 MT per annum over the next five years.

• Reliance Cementation, an Anil Dhirubhai Ambani Group (ADAG) company, plans to set

up a 5 MT integrated cement plant in Yavatmal district of Maharashtra at a cost of US$

463.2 million.

• Jaiprakash Associates Ltd has inked a MoU with state-owned Assam Mineral

Development Corporation Limited (AMDC) for setting up a 2 MT per annum capacity

cement plant at an estimated cost of US$ 221.36 million.

• Iron ore mining firm Rungta Mines (RML), the flagship company of SR Rungta group,

plans to set up a one million tonne cement plant in Orissa with an investment of around

US$ 123 million.

Mergers and Acquistions (M&As)

• Holcim strengthened its position in India by increasing its holding in Ambuja Cement

from 22 per cent to 56 per cent through various open market transactions with an open

offer for a total investment of US$ 1.8 billion. Moreover, it also increased its stake in

ACC Cement with US$ 486 million, being the single largest acquirer in the cement sector.

• UltraTech Cement, a unit of conglomerate Aditya Birla Group, is absorbing sister unit

Samruddhi Cement, to form India's biggest cement firm.

• Leading foreign funds like Fidelity, ABN Amro, HSBC, Nomura Asset Management Fund

and Emerging Market Fund have together bought around 7.5 per cent in India's third-

largest cement firm, India Cements (ICL), for US$ 124.91 million.

• Cimpor, the Portugese cement maker, paid US$ 68.10 million for Grasim Industries'

53.63 per cent stake in Shree Digvijay Cement.

• CRH Plc, the world's second biggest maker and distributor of building materials,

acquired a 50 per cent stake in My Home Industries Ltd for almost US$ 372.64 million.

• Vicat SA, a French cement maker acquired a 6.67 per cent stake in Hyderabad-based

Sagar Cement for US$ 14.35 million.

Government Initiatives

Government initiatives in the infrastructure sector, coupled with the housing sector boom and

urban development, continue being the main drivers of growth for the Indian cement industry.

• Increased infrastructure spending has been a key focus area over the last five years

indicating good times ahead for cement manufacturers.

• The government has increased budgetary allocation for roads under National Highways

Development Project (NHDP).

• Appointing a coal regulator is looked upon as a positive move as it will facilitate timely

and proper allocation of coal (a key raw material) blocks to the core sectors, cement

being one of them.

Keeping in mind the global meltdown which is impacting the cement companies in India, the

government re-imposed the counter-veiling duty (CVD) and special CVD on imported cement in

January. This is likely to provide a level playing field to domestic companies.

Road Ahead

According to a report by the ICRA Industry Monitor, the installed capacity is expected to

increase to 241 MTPA by FY 2010-end. India's cement industry is likely to record an annual

growth of 10 per cent in the coming years with higher domestic demand resulting in increased

capacity utilisation.

Moreover, according to the Centre for Monitoring Indian Economy (CMIE), cement production

is expected to grow by 8.1 per cent and demand for the same is likely to rise by a healthy 7-7.5

per cent in FY 2009-10.

____________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but we do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking & Financial Services

B. Prathap IT

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods; Real & Infra

D.Asha Kiran Kumar Auto

E. Swethalatha Oil & Gas

A.Rajesh FMCG

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,TakeoverOffers, Offer for Sale and Buy

Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,Placement of Equity / Debt with

multilateral organizations, Short Term Funds Management Debt & Equity, Working Capital Limits, Equity &

DebtSyndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and cross-border), divestitures, spin-offs,

valuation of business, corporate restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising of capital through FCCBs, GDRs,

ADRs and listing of the same on International Stock Exchanges namely AIMs, Luxembourg, Singapore Stock

Exchanges and other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com