russian automotive market analyst briefing

TRANSCRIPT

Is the One Way Russian Market Attractive Enough as an Assembly Base?

R.Sagitha, Research AnalystEconomic Research and Analytics

Automotive & TransportationJuly 31, 2008

2

Focus Points - Russia Automotive Industry

2. Automotive Industry Definitions

4. Drivers Favoring Car Assembly in Russia

5. Restraints not Favoring Car Assembly Process in Russia

7. Growth Opportunities

3. Russian Automotive Industry Snapshot

6. Existing and Planned OEM’s

1. Russia - Country Profile

3

� Population in 2007 – 142 million

� Decline in population by an average 700,000 people

each year

� Presidential elections was on March 2, 2008

� Dmitry Medvedev – as third President of Russia

Russia – Country Profile

� Exchange rate USD to RUB – 25.57

� Appreciation of national currency – Ruble

� Policy aimed at curbing currency appreciation

� The real GDP growth in 2007 was 8.1 percent

� Growth of industrial output recorded at 6.2 percent in 2007

� Unemployment rate – 3.6 percent in 2007

� GDP per capita - $14,600

� Inflation rate – 11.9 percent

Political Overview Economic Overview

Demographic Indicators Exchange Rate

4

Automotive Industry Definitions

Automotive Parts and Accessories

Automotive Industry

Passenger Cars

Motor Vehicles

Commercial Vehicles

Heavy Trucks

Buses

5

GAZ

2%Chery

2%Honda

2%

Mazda

2%

Uaz

3%

Opel

3%Kia

4%

Renault

5%

Mitsubishi

5%

Nissan

6%

Hyundai

6%

Toyota

7%

Ford

7%

Chevrolet

13%

VAZ

32%

VW

1%

Skoda

1%

Suzuki

1%

Russia – Automotive Industry Snapshot

Market Share by Sales in Russia in 2007

2007 sales determined the leading group of 9 foreign brands (Chevrolet, Ford, Toyota, Hyundai, Nissan, Mitsubishi, Renault, Kia and Opel) which all together hold almost 50 percent of the total market

6

Russia – Automotive Industry Snapshot

VEHICLE MANUFACTURERS

LIGHT COMMERCIAL VEHCILES

PASSENGER CARS

� AvtoVAZ

� GAZ

� GM-AvtoVAZ

� IZH-Avto

� TagAZ

� Ford Motor Co.

� GAZ

� UAZ

� PAZ

� LiAZ

� KavZ

� GAZ

� UAZ

� IZH-Avto

� AMO ZIL

� TagAZ

BUSESHEAVY TRUCKS

� KamAZ – ZMA

� GAZ

� UralAZ

� AMO ZIL

AvtoVaz GM

FordToyota

Joint Venture

Foreign OEMsUAZ

AvtoTorDomestic Players

TagAZ IZH-Avto

Russian players assembling foreign brands

� KamAZ - ZMA

� UAZ

� AvtoTor

� SeAZ

� Avtoframos

7

Russia – Drivers Favoring Car Assembly Process

Increasing Affordability

Growing Demand for

Imported Cars

Russian Automotive

Industry Policy

Russia’s WTO Entry

Russian Trade

Agreements

Changing Consumer

Preferences

Drivers that Favor Car Assembly

Process in Russia

8

Russia – Drivers Favoring Car Assembly Process

Sales

Affordability

Increasing car sales and increasing proportion of foreign cars in total sales

Sales and Affordability

� Rising real estate prices in Russia increases the affordability car sales� Development of financial institutions in Russia� Spending on communication, housing and transport is expected double

0

500000

1000000

1500000

2000000

2500000

3000000

2004 2005 2006 2007

Year

Nu

mb

er

of

Un

its

Total Sales

Foreign car Sales

9

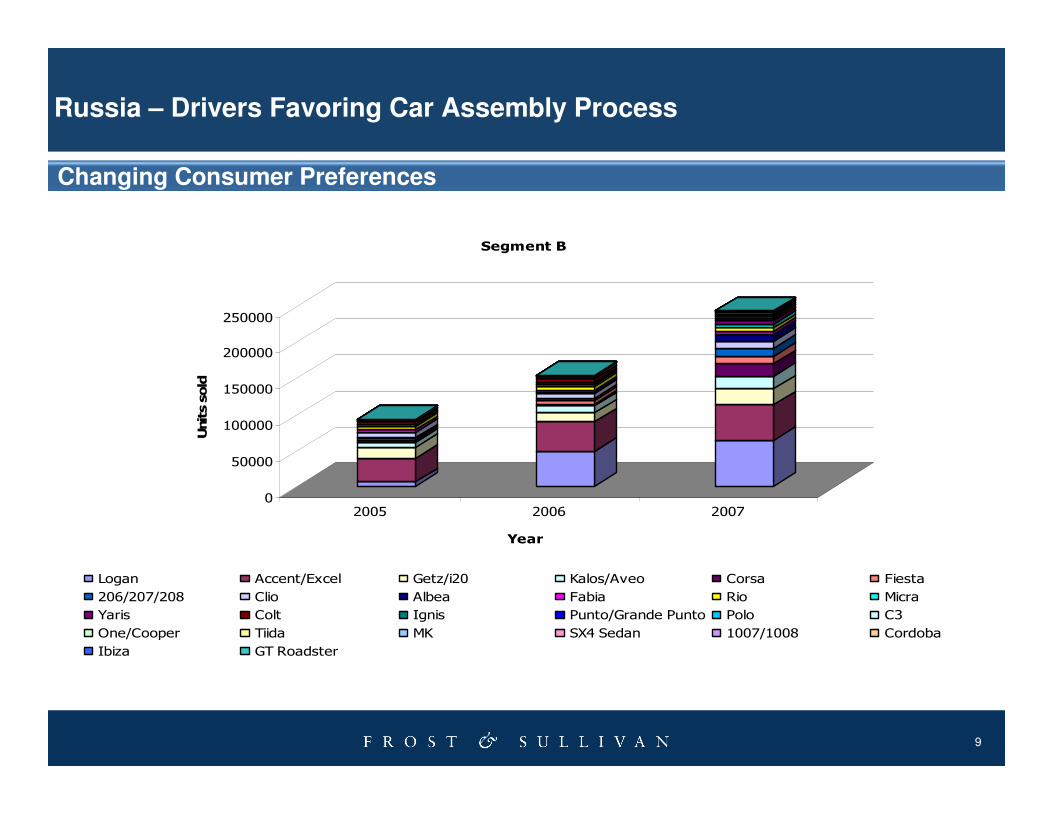

Changing Consumer Preferences

0

50000

100000

150000

200000

250000

Units sold

2005 2006 2007

Year

Segment B

Logan Accent/Excel Getz/i20 Kalos/Aveo Corsa Fiesta

206/207/208 Clio Albea Fabia Rio Micra

Yaris Colt Ignis Punto/Grande Punto Polo C3

One/Cooper Tiida MK SX4 Sedan 1007/1008 Cordoba

Ibiza GT Roadster

Russia – Drivers Favoring Car Assembly Process

10

Changing Consumer Preferences

Russia – Drivers Favoring Car Assembly Process

0

50000

100000

150000

200000

250000

300000

Units sold

2005 2006 2007

Year

SUV Segment

Niva Qashqai RAV4

Outlander Landcruiser/Colorado Tucson

X-Trail Escudo/Vitara Tiggo

Pajero Sportage CR-V

RX Santa Fe Forester

Sorento Touareg XC90

Captiva Pathfinder Discovery

Kyron Q7 Rexton

i FX-Series Freelander Actyon

X5 SX4 Murano

0

5000

10000

15000

20000

25000

30000

Units sold

2005 2006 2007

Year

SUV Segment

X3 Hover Range Rover

M-Class Cayenne Range Rover Sport

Jimny CX-7 GL-Class

Patrol TrailBlazer LX

Explorer Landmark B9 Tribeca

Compass Defender Grand Cherokee

Fortuner Cadillac Escalado Cadillac SRX

H2 H3 Nitro

G-Wagen Cherokee Commander

XL-7 Tribute Wrangler

Patriot 4007 Tahoe

C-Crosser

11

Trade Agreements

China

Russia

EgyptIndia Improving Chinese

buses and motor cyclesTo explore new

areas of trade

Industrial zone to manufacture Russian cars

Automotive trade being given emphasis in trade negotiations

Korea

Bilateral and Multilateral cooperation

Expansion of Trade and

Economic ties

Serbia

Duty free car tr

ade

Pakistan

Russia – Drivers Favoring Car Assembly Process

12

Russia’s WTO Entry and its Implications

Effects on Russia Effects on Russian Automotive Players

� Increase in unemployment rate is likely upon accession

� Accession forces Russia to restructure its economy

� Trade disputes between Russia and its trading partners will be resolved by WTO

� Stiff competitions from US., European and Japanese manufacturers

� Reduction in import duty is likely to increase the sales of foreign cars

� Fear of local assembly to become uncompetitive

Effects on Foreign Automotive Players

� Reducing the import duties upon accession will benefit the foreign players

� Russia will retain rights to grant subsidies and incentives to incoming foreign investments and customs benefits for semi knocked down kits

Effects on New Automotive Entrants

� An open market environment for the new comers

� WTO entry would negate Decrees 166 and 566 and the new entrants will not enjoy the privileges of these decrees

Russia – Drivers Favoring Car Assembly Process

13

Automotive Industry Policy – Decree 166

• Tax benefits provided by local authorities are restricted• 10 percent of initial capital investments (in fixed assets) could be acknowledged as

expenses

Relevant

Tax

Reforms

Profit Tax

Reforms

• Possibility of crediting input VAT on invoice acceptance • Capital construction: Input VAT is offset in the period when the costs are attained

VAT

Reforms

• Additions to Tax Code are made to regulate procedures for costs accruals and payment of assets tax

• Inventory is not included into the assets tax base

Asset Tax

Reforms

Relevant

Customs

Duties

Reforms

• Measurements:

• 25,000 units• body assembly, welding and painting

• 18 months for existing plant• 30 months for constructed plant• 24 months: 10% less of components imported• 42 months: 10% less of components imported• 54 months: 10% less of components imported• 0-5% for exclusive components used in

manufacturing (standard rate – 15%)

Features: • Minimum annual production

capacity ………………………..• Operations to be performed…..

• Time for production set-up …...

• Restrictions on import ………...

• Applicable duty tax ……………

Decree #166

Concept of Industrial Assembly

Russia – Drivers Favoring Car Assembly Process

14

Russia – Restraints not favoring Car Assembly Process in Russia

General Economic and

Legal System ambiguity

Low Average Income

Level in Russia

Raising Cost of

Production

Poor State of

Russian Automotive

Component Industry

Restraints that

do not favor

Car Assembly

in Russia

15

Russia – Existing and Planned OEM’s

Uliyanovsk● ● Izhevsk

GM - AvtoVAZ

AvtoVAZ

IZH-Avto*

GAZ

GM Avtoframos

FORD

Hyundai

AvtoKOM

Opel

Renault

PSA-Mitsubishi

Samara ●

● Nizhniy Novgorod

● Kaluga

� Moscow

● Taganrog

Toyota

Nissan

BYD

VW

● St. Petersburg

Kaliningrad ●

Chery

● Cherkesk

Novouralsk ●

Geely

AvtoVAZ-Magna

Tata

RUSSIA

● ElabugaNab. Chelny ●

Fiat

Great Wall

KIA

LADA

Ssang Yong

BAIC

UAZ

BMW

KIA

Existing OEM’s (2008)

Planned places for OEM’s (2008)

FAW

Hyundai

LADA

Chrysler

KIA

Valmet Automotive

ZAZ

Source: Frost & Sullivan

16

Growth Opportunities in the Russian Automotive Industry

Transformation in Railroad System

Environmental – Friendly Technology

Mid to Low Priced Cars

After Market

Adoption of Environment – friendly Technology stimulates Fuel efficient vehicle segments

Only 2 to 3 percent of the population can afford luxury cars, most car sales are of mid-to-low range prices

Increasing demand for servicing and repairs leads to service centers

Transforming Russian Railroad provides new opportunities for Automotive players

17

Related and Upcoming Research - Country Industry Forecasts

Automotive IndustryAutomotive Industry

Political and Policy Analysis

Economic and Social Analysis

Other Studies

Published Studies

Japan

Mexico

Canada

Upcoming Studies

Turkey

China

Ukraine

Russia

Economic Research and Analytics Consulting Capabilities

Economic Research and Analytics Consulting Capabilities

Statistical Data Analysis

Multi-Country Analysis

Trade and Investment Analysis

Outsourcing

Econometric Modeling

Country Risk Analysis

PESTLE Analysis

Market /Industry Surveys

18

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

19

For Additional Information

• To leave a comment, ask the analyst a question, or receive the

free audio segment that accompanies this presentation, please contact Stephanie Ochoa, Analyst Briefing Coordinator, at (210)

247-2421 or via email, [email protected].