rural valuation update, ludlow, 19 june 2015

TRANSCRIPT

Charles CowapMBA MRICS FAAV

Valuation Update

RICS West Midlands CPD FoundationLudlow

9 June 2015

Charles CowapMBA MRICS FAAV

Valuation is becoming ….

• Broader

• More Complex

• More Challenging

• Riskier

Charles CowapMBA MRICS FAAV

Basis of Farm Stocktaking Valuations

BEN 19

Business Income Manual 55410:Farming: stock

valuation

Help SheetHS 232

2014 and 2015

SPOT THE DIFFERENCES!!

Charles CowapMBA MRICS FAAV

Guidance ……

Charles CowapMBA MRICS FAAV

BIM 55410• FRS 100, 101, 102 – ‘New UK GAAP’

– Periods starting after 1.1.2015• Fair Value (less costs to sell) choice• Biological assets

– Living animals and plants• Agricultural Produce

– Harvested product of a biological asset

Charles CowapMBA MRICS FAAV

Biological Assets• Fair value less costs to sell• Fair value at point of

harvest = cost at that date• Market prices if possible• Market derived prices• Present value of expected

cash flows, discounted …..

Agricultural Produce• Fair value as well

• FRS 102, section 34: Fair Value model is a policy choice (against cost model)

• Reporting requirements

Charles CowapMBA MRICS FAAV

Reporting Requirements

• RICS Red Book ….• AND FRS 102 ….

Charles CowapMBA MRICS FAAV

Down in the woods today …

Charles CowapMBA MRICS FAAV

INHERITANCE TAX

Charles CowapMBA MRICS FAAV

Is Woodland:

1. A Business Asset?

2. Agricultural Property?

3. None of the above?

Charles CowapMBA MRICS FAAV

Woodland as a Business Asset

• Business Property Relief– Not investment business

(Balfour)

• How to demonstrate Business Nature?

Charles CowapMBA MRICS FAAV

Woodland as agricultural property

• Agricultural Property Relief– Nature of ‘agricultural

property’– ‘with’ and ‘ancillary’

• ‘Agricultural Value’

Charles CowapMBA MRICS FAAV

None of the Above

• Woodlands Relief– Prairie Value – the custom and

practice

– What the IHTA 1984 (s125) says

Charles CowapMBA MRICS FAAV

An example

10 acre woodland, broadleaf, vacant possession, location accessible, upmarket and popular

Various scenarios

Charles CowapMBA MRICS FAAV

Values

• Freehold market value £70,000• Agricultural value £40,000• Prairie value £15,000• Value of trees and underwood £20,000

Charles CowapMBA MRICS FAAV

BPR

• Claim at 100% of MV

• Nil IHT

Charles CowapMBA MRICS FAAV

APR• Claim at 100% of Agricultural Value

(£40,000)• BPR on balance (£30,000)• Nil IHT

• BPR not available? IHT on £30,000, ie £12,000

Charles CowapMBA MRICS FAAV

Woodlands Relief (1)

• Value to Prairie Value• IHT due on £15,000 @ 40% = £6,000

• Further IHT on subsequent sale of timber (if ever)

Charles CowapMBA MRICS FAAV

Woodlands Relief (2)Literal interpretation

• Market Value – Timber and underwood value

• £70,000 - £20,000 = £50,000• IHT on £50,000 @ 40% = £20,000

Charles CowapMBA MRICS FAAV

No claim for relief

• Market Value at 40% IHT

• £28,000

Charles CowapMBA MRICS FAAV

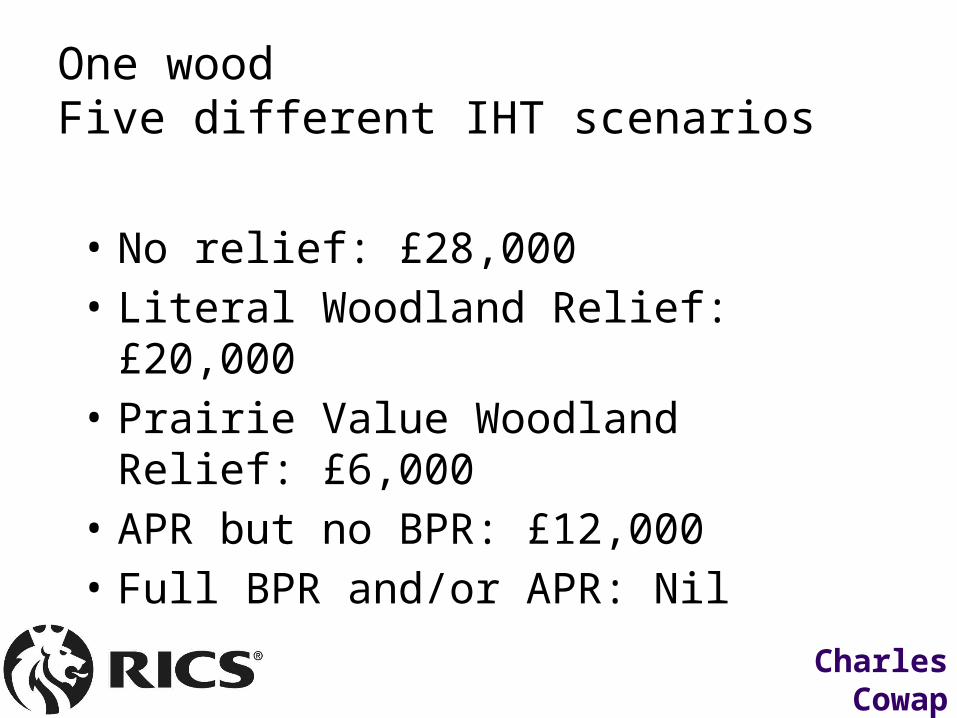

One woodFive different IHT scenarios

• No relief: £28,000• Literal Woodland Relief: £20,000• Prairie Value Woodland Relief: £6,000• APR but no BPR: £12,000• Full BPR and/or APR: Nil

Charles CowapMBA MRICS FAAV

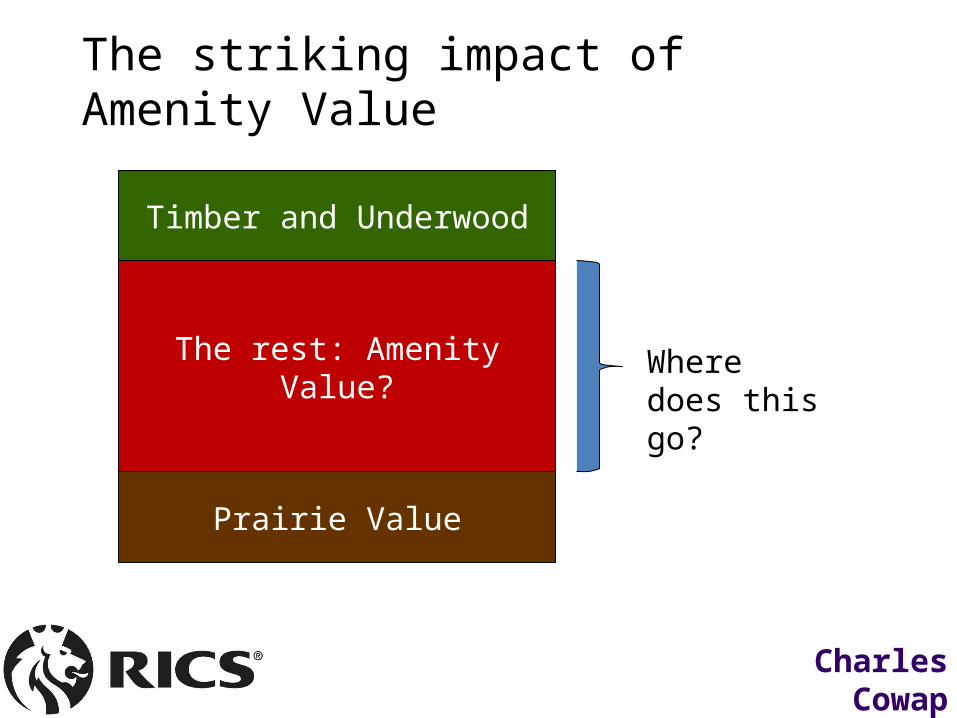

The striking impact of Amenity Value

Prairie Value

Timber and Underwood

The rest: Amenity Value? Where does this go?

Charles CowapMBA MRICS FAAV

The moral of this story

MAKE IT AND KEEP IT

COMMERCIALAND be able to

prove it!

Charles CowapMBA MRICS FAAV

OTHER VALUATION CHALLENGES

Charles CowapMBA MRICS FAAV

• Market Value

• Fair Value

• Worth

Charles CowapMBA MRICS FAAV

The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm’s length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion.

The price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date. (IFRS 13)

The estimated price for the transfer of an asset or liability between identified knowledgeable and willing parties that reflects the respective interests of those parties. (IVS 2013). The value of an asset to the owner or

a prospective owner for individual investment or operational objectives.

Fair Value

Investment Value

Worth

Market Value

Bequest Value

Existence Value

Charles CowapMBA MRICS FAAV

Renewable Investment Example10 ha site for 7 wind turbines on 28 year lease, 3 years expired

Turbines: 7 x 2.3 MW x 27% capacity. Output (Elec + ROC) = £83/MWh

Basic Rent: £7,000 + RPI for 14 years; £12,000 + RPI thereafter

Turnover Rent: 5% of gross income for 14 years; 9% thereafter

Lease is taken from a larger site , rough grazing, of 100 ha in total

Let to a large well established generator

Charles CowapMBA MRICS FAAV

Charles CowapMBA MRICS FAAV

Charles CowapMBA MRICS FAAV

Charles CowapMBA MRICS FAAV

Charles CowapMBA MRICS FAAV

DCF Methods• In practice widely undertaken

for larger developments

• Market Value??

• Appraisal of worth to investor

• Would the market make same assumptions?

Charles CowapMBA MRICS FAAV

DCF: Discounting Future Cash Flows

Total NPV + Worthwhile

Total NPV –Not

worthwhile

Charles CowapMBA MRICS FAAV

DCF Appraisal• Remaining 25 years• Both rents adjusted for

3.5% inflation pa• Opening Valuation from

Investment valuation• PV of £1 at 15% gives

NPV of -£172,000• IRR is 14% including

Inflation, ie 10.5% net of inflation

Charles CowapMBA MRICS FAAV

Question• In view of the DCF Valuation we have just looked at, does the

previous investment valuation of £1.6 million for the freehold interest look:

1)Too high

2)About right

3)Too low

Charles CowapMBA MRICS FAAV

BACK TO BASICS

• Purpose of Valuation• Scope of investigations to be undertaken• Assumptions and Special Assumptions• Preliminary Information• Capacity and assumed duration• After uses, continuation, redevelopment• Reporting Requirements

Charles CowapMBA MRICS FAAV

Reporting

• Rationale for chosen method(s)• Detailed consideration of instructions,

assumptions, sources and reliability, extent of independent verification

• Sensitivity• Commentary on Risk?

Charles CowapMBA MRICS FAAV

Risk• Operator/Covenant

Risk• Market Risk• Technology Risk

Shropshire Star and Daily Mail

Charles CowapMBA MRICS FAAV

Some Common Issues• Operator Risk

• Complex lease or agreement terms

• Performance data

• Development Proposals for new Sites

• Hope Value

Charles CowapMBA MRICS FAAV

‘Hope’ Value

??Time

Val

ue

Charles CowapMBA MRICS FAAV

Some Common Issues• Reporting

Requirements

• Detailed instructions

• Market evidence

Charles CowapMBA MRICS FAAV

Bed Time Reading: the Red Book

January 2014

December 2014 amendments

Charles CowapMBA MRICS FAAV

Valuation: a broad scheme

Agree Terms of Engagement

Must include: Defined Basis

of Value ....

Apply Valuation Methods

Formal Reporting

Requirements

Follow up advice -

publication issues

Market ValueFair ValueWorthExisting Use ValueOther Basis??

CompetencePurposeAssumptionsSpecial AssumptionsInspection etc

Sales comparisonInvestment approachesDRCOther?

Extensive RevaluationReinspectionAppropriate publication

Charles CowapMBA MRICS FAAV

ExampleLet farm, AHA 1986

Discussion Point

How do these values relate to Market Value, Fair Value and Worth?

• Market Value, Fair Value and Special Assumptions

Farmland

Value VP £3 m

Value STT £1.8 m

Special Purchaser Bid: 3.5 million?

Charles CowapMBA MRICS FAAV

Not generally a Red Book matter, but …..

VALUATION METHODS

► Other allied guidance (Guidance Notes, Information Papers, other professional briefings)

Charles CowapMBA MRICS FAAV

Other Guidance ….

Charles CowapMBA MRICS FAAV

December 2014 Amendments

Charles CowapMBA MRICS FAAV

New UK VS and GN’s

The 2014 Amendments

Charles CowapMBA MRICS FAAV

New UK VS and GN’s

The 2014 Amendments

Charles CowapMBA MRICS FAAV

New UK VS and GN’s

The 2014 Amendments

Charles CowapMBA MRICS FAAV

Lessons from Practice• VRS Monitoring and other issues

• Conflicts of Interest– File Records

• Comparable summary and analysis

• Others?

Charles CowapMBA MRICS FAAV

CASES

Charles CowapMBA MRICS FAAV

Ham v Ham [2013] EWCA Civ 1301

• Farming partnership– Young John leaves family partnership– Mum and dad elect to buy out share

• Calculation of ‘net value’?– John had introduced no capital– Land shown at book value– Book value or market value?

• Market value– Need for clarity in partnership agreements

Charles CowapMBA MRICS FAAV

Freemont (Denbigh) Ltd v Knight Frank LLP [2014] EWHC 3347 (Ch)

• A former asylum• A valuation for secured lending• Was Knight Frank liable when P relied on it to judge an offer

on the property?• NO

– Exclusively for secured lending purposes

Charles CowapMBA MRICS FAAV

Valuation is becoming ….

• Broader

• More Complex

• More Challenging

• Riskier

Charles CowapMBA MRICS FAAV

Contact DetailsTranslating new knowledge for rural professional practice

[email protected] 07947 706505Twitter: @charlescowapBlog: http://charlescowap.wordpress.com/Slideshare: http://www.slideshare.net/cdcowap

Charles CowapMBA MRICS FAAV

Charles CowapMBA MRICS FAAV