royalty trusts - latham & watkins

TRANSCRIPT

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limitedliability partnerships conducting the practice in the United Kingdom, France, Italy and Singapore and as affiliated partnerships conducting the practicein Hong Kong and Japan. Latham & Watkins practices in Saudi Arabia in association with the Law Office of Mohammed A. Al-Sheikh. In Qatar, Latham& Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2012

Royalty Trusts

Jeff MuñozSean WheelerTim Fenn

Wednesday, September 26, 2012

2

Royalty Trusts

• Section 1 – Characteristics of Royalty Trusts• Section 2 – Two Primary Types of Royalty Trusts: “Perpetual

Royalty Trusts” vs. “Term Royalty Trusts”• Section 3 – The Two Types In Action: VOC Energy Trust

(“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

• Section 4 – A Brief Comparison of Current Royalty Trusts

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limitedliability partnerships conducting the practice in the United Kingdom, France, Italy and Singapore and as affiliated partnerships conducting the practicein Hong Kong and Japan. Latham & Watkins practices in Saudi Arabia in association with the Law Office of Mohammed A. Al-Sheikh. In Qatar, Latham& Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2012

Section 1Characteristics of Royalty Trusts

4

Royalty TrustsSection 1 – Characteristics of Royalty Trusts

Definition and Purpose• A “Royalty Trust” is a state law trust, created by a “Sponsor” who

transfers an interest in minerals to the trust, which is administered by a “Trustee”

• The Sponsor creates the trust, divides the trust into interests (called units), and sells the units to the public in an IPO

• The units are generally listed on a national securities exchange

• A Royalty Trust is generally used to monetize producing assets• A Royalty Trust is similar to a Master Limited Partnership (“MLP”) in that

the entity has tax advantages over traditional corporate forms and distributes to unitholders substantially all of the entity’s cash flow

• But unlike an MLP, a Royalty Trust:• has no general partner• has no incentive distribution rights• is essentially a liquidation vehicle; the entity’s primary purposes are

to conserve and distribute the trust assets

5

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

Formation and Operation - Overview

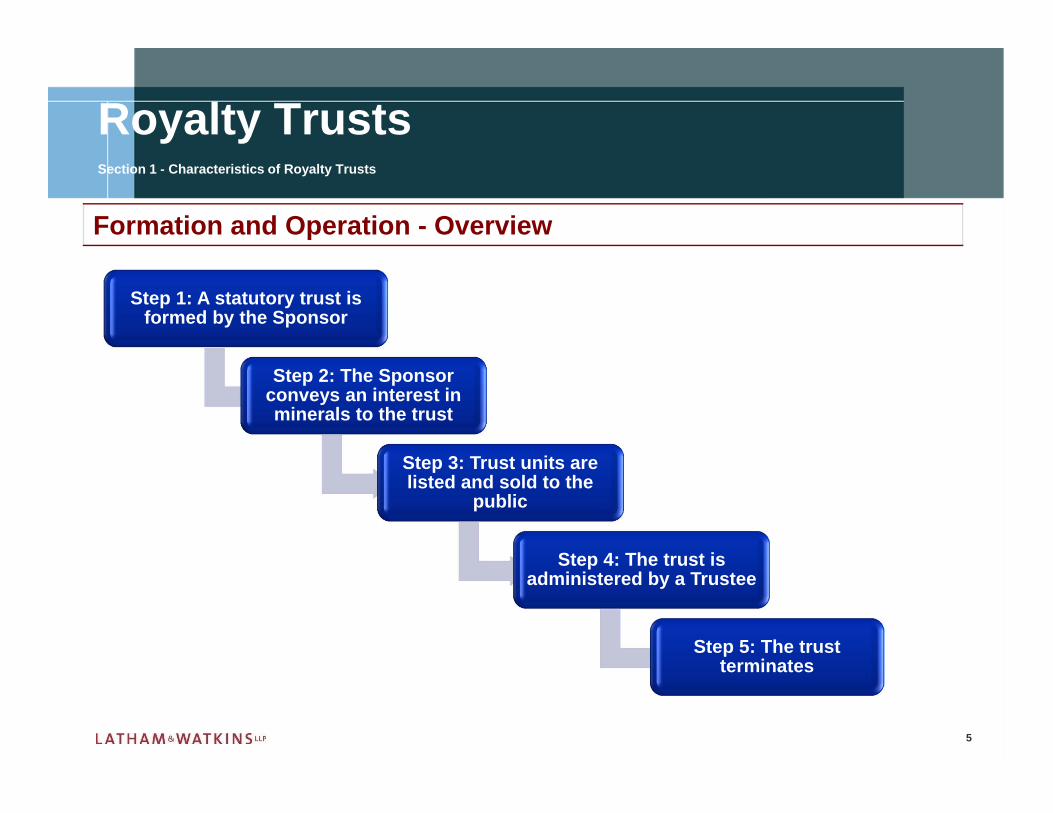

Step 1: A statutory trust is formed by the Sponsor

Step 2: The Sponsor conveys an interest in minerals to the trust

Step 3: Trust units are listed and sold to the

public

Step 4: The trust is administered by a Trustee

Step 5: The trust terminates

6

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

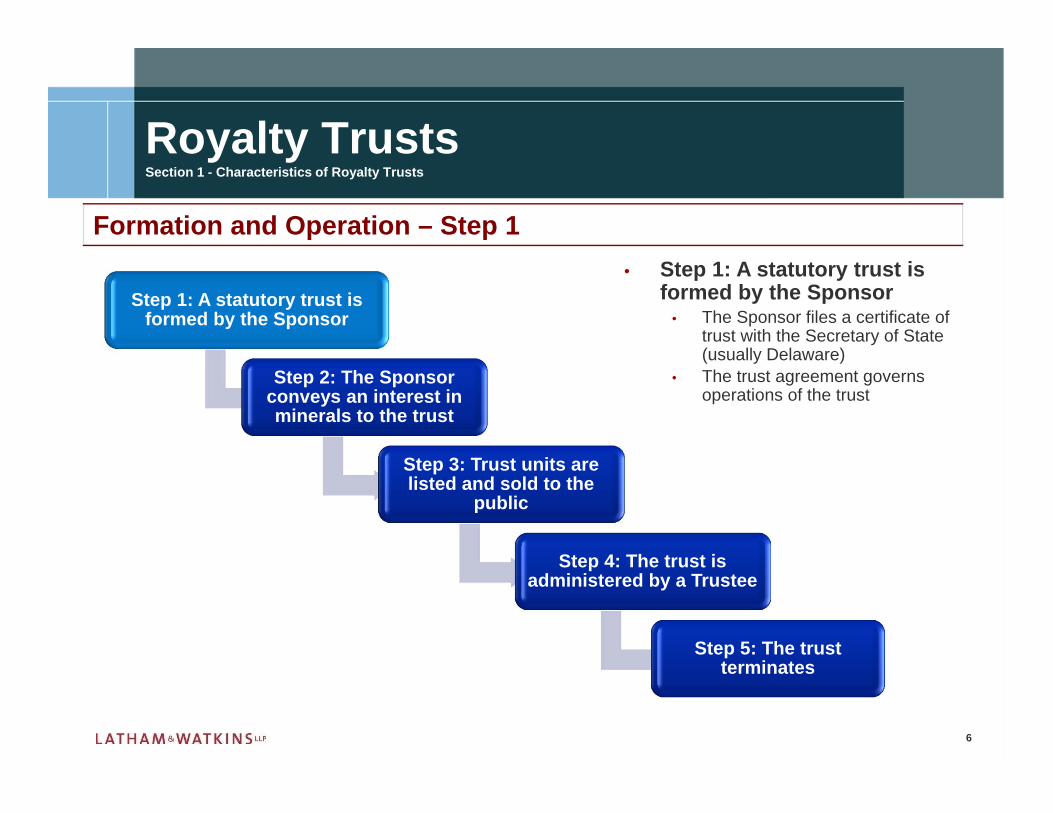

Formation and Operation – Step 1• Step 1: A statutory trust is

formed by the Sponsor• The Sponsor files a certificate of

trust with the Secretary of State (usually Delaware)

• The trust agreement governs operations of the trust

Step 1: A statutory trust is formed by the Sponsor

Step 2: The Sponsor conveys an interest in minerals to the trust

Step 3: Trust units are listed and sold to the

public

Step 4: The trust is administered by a Trustee

Step 5: The trust terminates

7

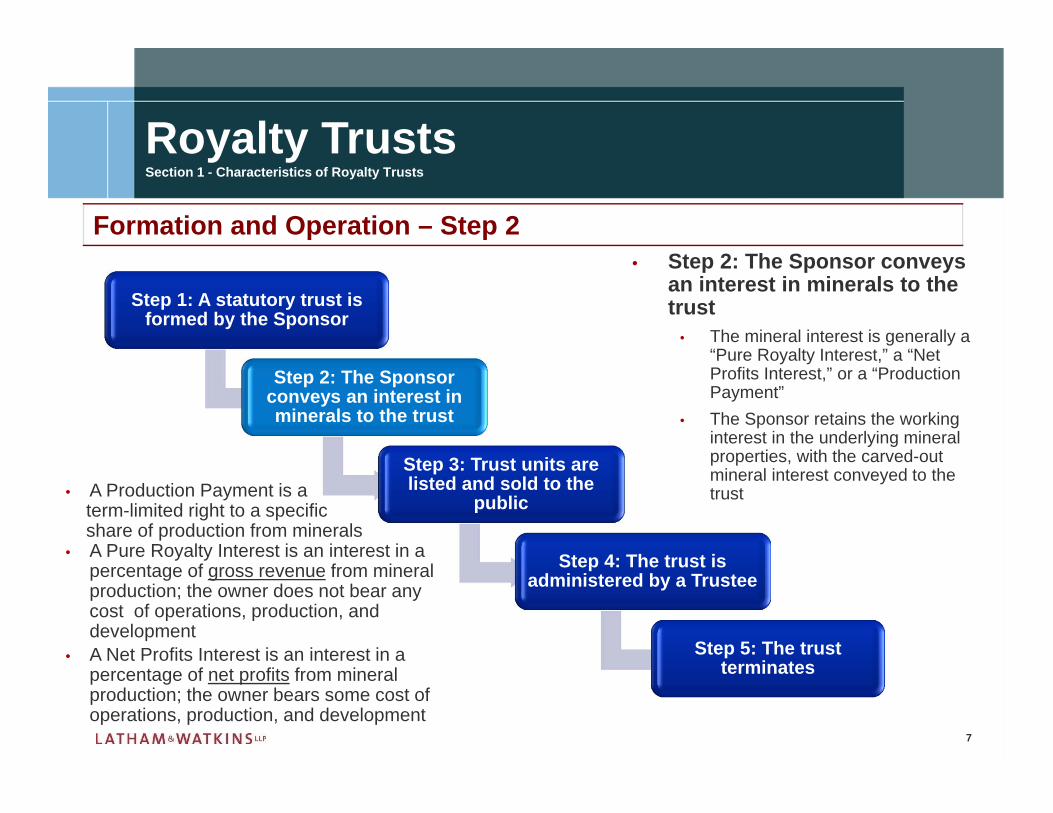

Formation and Operation – Step 2• Step 2: The Sponsor conveys

an interest in minerals to the trust

• The mineral interest is generally a “Pure Royalty Interest,” a “Net Profits Interest,” or a “Production Payment”

• The Sponsor retains the working interest in the underlying mineral properties, with the carved-out mineral interest conveyed to the trust

Step 1: A statutory trust is formed by the Sponsor

Step 2: The Sponsor conveys an interest in minerals to the trust

Step 3: Trust units are listed and sold to the

public

Step 4: The trust is administered by a Trustee

Step 5: The trust terminates

• A Production Payment is a term-limited right to a specificshare of production from minerals

• A Pure Royalty Interest is an interest in a percentage of gross revenue from mineral production; the owner does not bear any cost of operations, production, and development

• A Net Profits Interest is an interest in a percentage of net profits from mineral production; the owner bears some cost of operations, production, and development

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

8

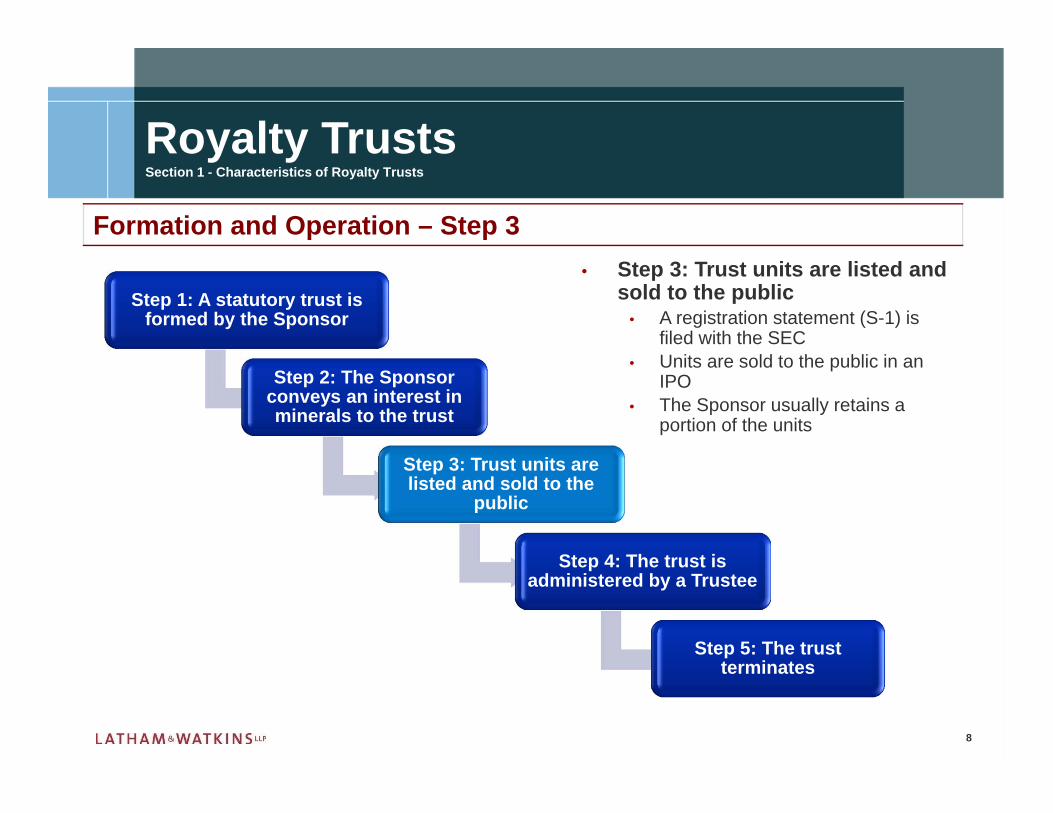

Formation and Operation – Step 3• Step 3: Trust units are listed and

sold to the public• A registration statement (S-1) is

filed with the SEC• Units are sold to the public in an

IPO • The Sponsor usually retains a

portion of the units

Step 1: A statutory trust is formed by the Sponsor

Step 2: The Sponsor conveys an interest in minerals to the trust

Step 3: Trust units are listed and sold to the

public

Step 4: The trust is administered by a Trustee

Step 5: The trust terminates

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

9

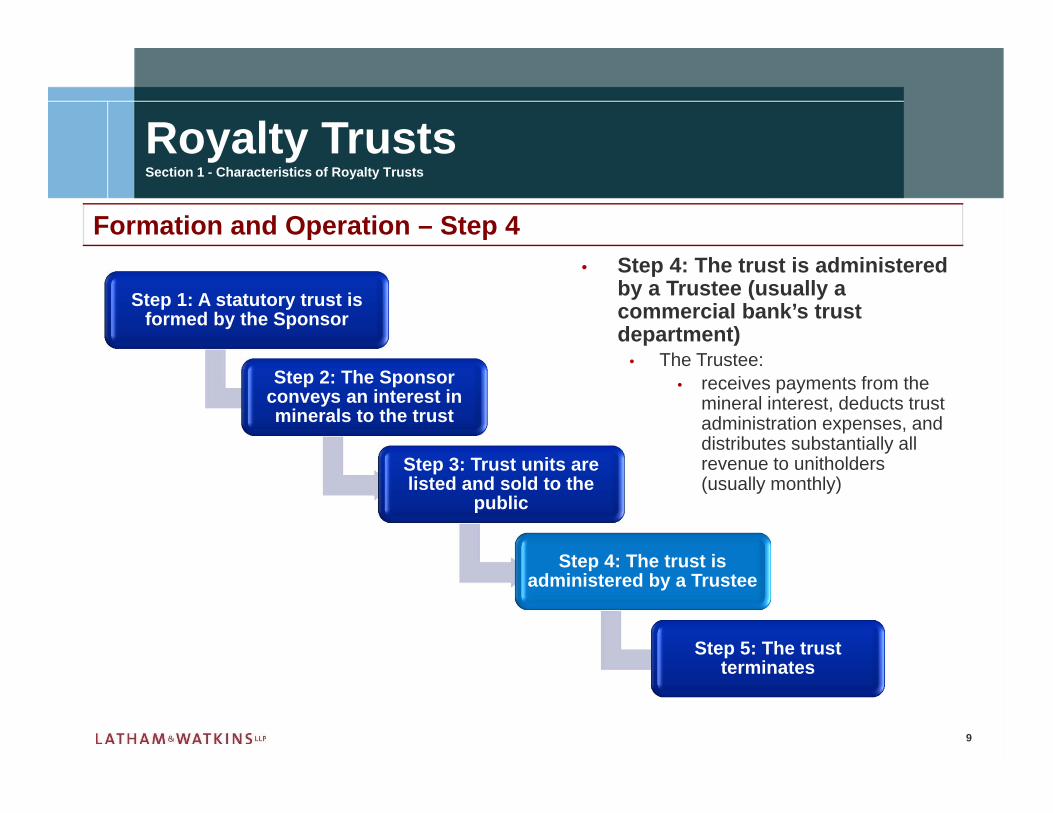

Formation and Operation – Step 4• Step 4: The trust is administered

by a Trustee (usually a commercial bank’s trust department)

• The Trustee:• receives payments from the

mineral interest, deducts trust administration expenses, and distributes substantially all revenue to unitholders (usually monthly)

Step 1: A statutory trust is formed by the Sponsor

Step 2: The Sponsor conveys an interest in minerals to the trust

Step 3: Trust units are listed and sold to the

public

Step 4: The trust is administered by a Trustee

Step 5: The trust terminates

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

10

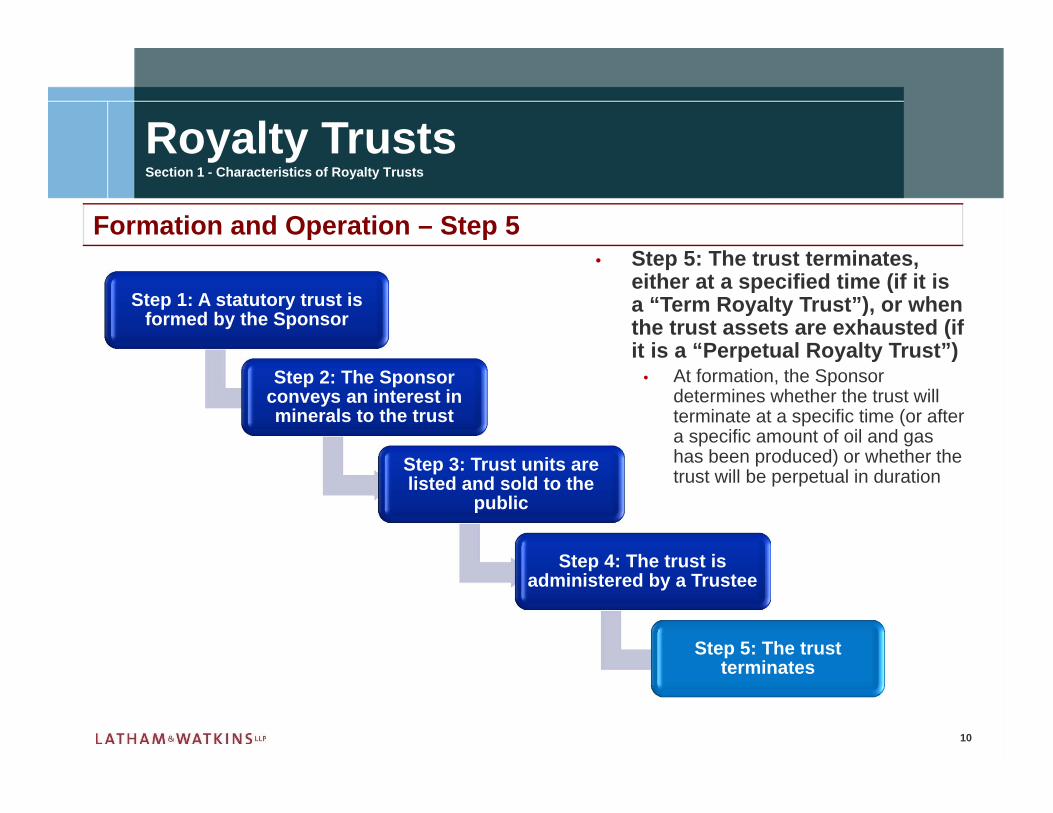

Formation and Operation – Step 5• Step 5: The trust terminates,

either at a specified time (if it is a “Term Royalty Trust”), or when the trust assets are exhausted (if it is a “Perpetual Royalty Trust”)

• At formation, the Sponsor determines whether the trust will terminate at a specific time (or after a specific amount of oil and gas has been produced) or whether the trust will be perpetual in duration

Step 1: A statutory trust is formed by the Sponsor

Step 2: The Sponsor conveys an interest in minerals to the trust

Step 3: Trust units are listed and sold to the

public

Step 4: The trust is administered by a Trustee

Step 5: The trust terminates

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

11

Governance

• Voting• The trust agreement typically provides voting rights to trust unitholders to

remove and replace (but not elect) the Trustee and to approve or disapprove major trust transactions

• Fiduciary Duties• The Trustee’s fiduciary duties are typically limited so that the Trustee will

be liable to unitholders only for: • fraud, • gross negligence, or • acts or omissions constituting bad faith

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

12

Conveyance of Mineral Interest

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

• Overriding Royalty Interest• An interest in oil and gas produced at the surface, free of the expense of

production• An interest carved out of the lessee’s share of the working interest as

distinguished from the mineral owner’s reserved royalty interest• Typically lasts for the life of the underlying lease

• Net Profits Interest• A non-operating, non-expense bearing interest that represents a share of

gross production from oil and gas leases that is determined by the net profits received in connection with the ownership and operation of the leases

• NPI =Revenues from oil and gas leases

- Costs associated with generating the revenuesPositive balance X net profit percentage

• Typically lasts for the life of the underlying lease• Interest paid in dollars rather than in-kind

13

Conveyance of Mineral Interest

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

• Production Payment• Non-operating, non-expense bearing, limited term overriding royalty

interest in oil and gas leases• Can cover either a fixed quantity of hydrocarbons from the oil and gas

leases (a volumetric production payment) or a fixed quantity of proceeds from the sale of such hydrocarbons (a dollar denominated production payment)

• Terminates when the fixed quantity or fixed dollar amount is delivered or the oil and gas lease out of which it is created terminates

14

Conveyance of Mineral Interest

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

• Nature of Interest• State law governs• Real property v. personal property v. contract right

• Title Due Diligence• Creation of Interest

• Recordable instruments• Consent/preferential purchase issues• Maintenance of uniform interest issues• Warranties

• Operating Covenants

15

Conveyance of Mineral Interest

• Conveyance Issues• Sometimes, potential sponsors may need to address issues with co-

owner agreements, debt documents, and other agreements that prohibit its transfer of its mineral interests

• Bankruptcy Issues• The treatment of a mineral interest under state law (i.e., whether it is

treated as a property interest or a mere contractual right) determines whether the right survives bankruptcy of the Sponsor

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

16

Securities Laws

• Registration• The trust must register the offering of the units and provide a prospectus• Because the trust is the issuer, the Trustee has securities act liability• The Sponsor is treated as a co-registrant by the SEC and, as a result,

has securities act liability• Full S-1 Information for Trust

• Business• MD&A• Financials• Projections

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

17

Securities Laws

• Registration (continued)• Partial S-1 Information for Sponsor

• Business• MD&A• Financials• No Compensation Information• Can be Incorporated by Reference for Public Sponsor

• Content Requirements Evolving via SEC Review

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

18

Securities Laws

• Reporting• The Trustee (but not the Sponsor) must file specified periodic

reports with the SEC• Trust Files 10-Qs, 10-Ks, 8-Ks• Sponsor Assists in Preparation• Sponsor Information Not Included in 1934 Act Reports• Sponsor May Elect to Issue Earnings and Operational

Releases as well as Hold Periodic Analyst Calls

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

19

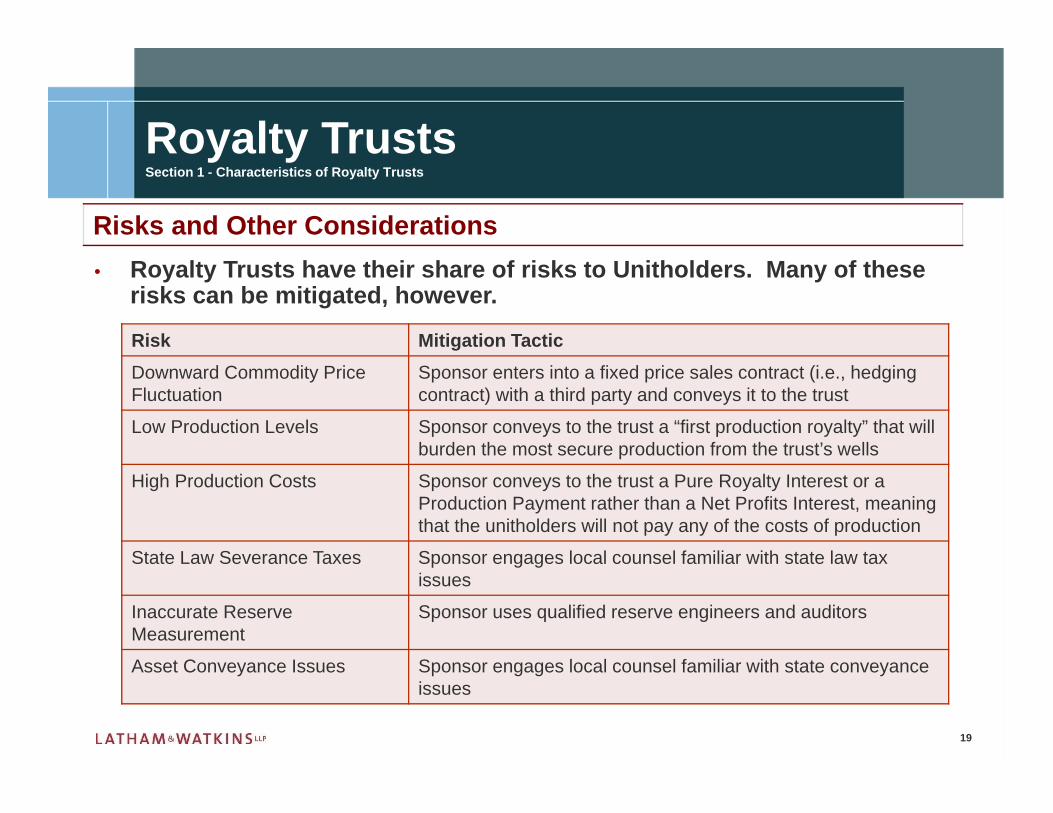

Risks and Other Considerations• Royalty Trusts have their share of risks to Unitholders. Many of these

risks can be mitigated, however.

Risk Mitigation TacticDownward Commodity Price Fluctuation

Sponsor enters into a fixed price sales contract (i.e., hedging contract) with a third party and conveys it to the trust

Low Production Levels Sponsor conveys to the trust a “first production royalty” that will burden the most secure production from the trust’s wells

High Production Costs Sponsor conveys to the trust a Pure Royalty Interest or a Production Payment rather than a Net Profits Interest, meaning that the unitholders will not pay any of the costs of production

State Law Severance Taxes Sponsor engages local counsel familiar with state law tax issues

Inaccurate Reserve Measurement

Sponsor uses qualified reserve engineers and auditors

Asset Conveyance Issues Sponsor engages local counsel familiar with state conveyance issues

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

20

Today’s Publicly Traded Royalty Trusts

TrustYear

FormedPerpetual or Term Mineral Interest Properties

Pacific Coast Oil Trust (ROYT) 2012 Perpetual Net Profits CA - oil

SandRidge Mississippian Trust II (SDR) 2012 Term Production Payment KS, OK – oil and gas

SandRidge Mississippian Trust I (SDT) 2011 Term Production Payment OK - oil and gas

SandRidge Permian Trust (PER) 2011 Term Production Payment TX - oil

VOC Energy Trust (VOC) 2011 Term Production Payment KS, TX - oil and gas

Enduro Royalty Trust (NDRO) 2011 Perpetual Net Profits TX, LA, NM - oil and gas

Chesapeake Granite Wash Trust (CHKR) 2011 Term Production Payment OK - oil and gas

ECA Marcellus Trust I (ECT) 2010 Term Production Payment Marcellus shale - gas

Whiting USA Trust I (WHX) 2008 Term Production Payment ND, OK, TX - oil and gas

MV Oil Trust (MVO) 2007 Term Production Payment KS, CO - oil

Hugoton Royalty Trust (HGT) 1999 Perpetual Net Profits OK, TX, KS - oil and gas

Dominion Res. Black Warrior Trust (DOM) 1994 Perpetual Royalty AL - natural gas

Cross Timbers Royalty Trust (CRT) 1991 Perpetual Net Profits TX, OK, NM - oil and gas

Sabine Royalty Trust (SBR) 1982 Perpetual Royalty FL, LA, MS, NM, OK, TX - oil and gas

San Juan Basin Royalty Trust (SJT) 1980 Perpetual Royalty NM - natural gas

Permian Basin Royalty Trust (PBT) 1980 Perpetual Royalty Permian Basin - oil and gas

Mesa Royalty Trust (MTR) 1979 Perpetual Royalty San Juan Basin - oil

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

21

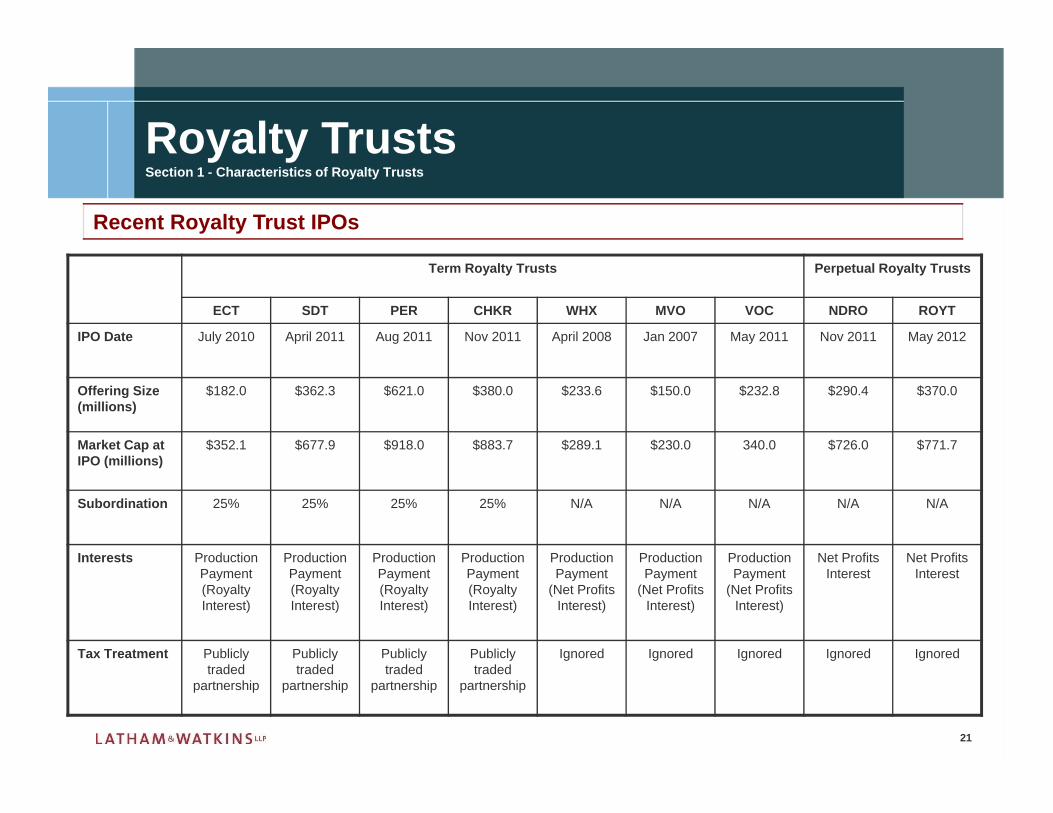

Recent Royalty Trust IPOs

Term Royalty Trusts Perpetual Royalty Trusts

ECT SDT PER CHKR WHX MVO VOC NDRO ROYT

IPO Date July 2010 April 2011 Aug 2011 Nov 2011 April 2008 Jan 2007 May 2011 Nov 2011 May 2012

Offering Size (millions)

$182.0 $362.3 $621.0 $380.0 $233.6 $150.0 $232.8 $290.4 $370.0

Market Cap at IPO (millions)

$352.1 $677.9 $918.0 $883.7 $289.1 $230.0 340.0 $726.0 $771.7

Subordination 25% 25% 25% 25% N/A N/A N/A N/A N/A

Interests Production Payment (Royalty Interest)

Production Payment (Royalty Interest)

Production Payment (Royalty Interest)

Production Payment (Royalty Interest)

Production Payment

(Net Profits Interest)

Production Payment

(Net Profits Interest)

Production Payment

(Net Profits Interest)

Net Profits Interest

Net Profits Interest

Tax Treatment Publicly traded

partnership

Publicly traded

partnership

Publicly traded

partnership

Publicly traded

partnership

Ignored Ignored Ignored Ignored Ignored

Royalty TrustsSection 1 - Characteristics of Royalty Trusts

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limitedliability partnerships conducting the practice in the United Kingdom, France, Italy and Singapore and as affiliated partnerships conducting the practicein Hong Kong and Japan. Latham & Watkins practices in Saudi Arabia in association with the Law Office of Mohammed A. Al-Sheikh. In Qatar, Latham& Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2012

Section 2Two Primary Types of Royalty Trusts: “Perpetual Royalty Trusts” vs. “Term Royalty Trusts”

23

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

Perpetual Royalty Trusts and Term Royalty Trusts

• There are two primary types of Royalty Trusts – “Perpetual Royalty Trusts” and “Term Royalty Trusts”

• They each have different characteristics, tax treatment, and risks to unitholders

• A Perpetual Royalty Trust:• Assets: Contains a Net Profits Interest or Royalty Interest (never contains a Production Payment)

• Term: Exists until the underlying mineral interest is effectively exhausted

• Ability to Add Assets: Generally contains all assets and hedging contracts the trust will have at the time of formation (though, technically, a Perpetual Royalty Trust could have the ability to add assets and hedges and, in such a case, would be treated as a publicly-traded partnership for tax purposes)

• Note: All current Perpetual Royalty Trusts generally prohibit the addition of assets

• Classes of Interests: Generally has only one class of interests (though, technically, a Perpetual Royalty Trust could have multiple classes of interests and, in such a case, would be treated as a publicly-traded partnership for tax purposes)

• Note: All current Perpetual Royalty Trusts have only one class of interests

• Tax Treatment: Generally is ignored for tax purposes (i.e., treated as a Grantor Trust for tax purposes)

24

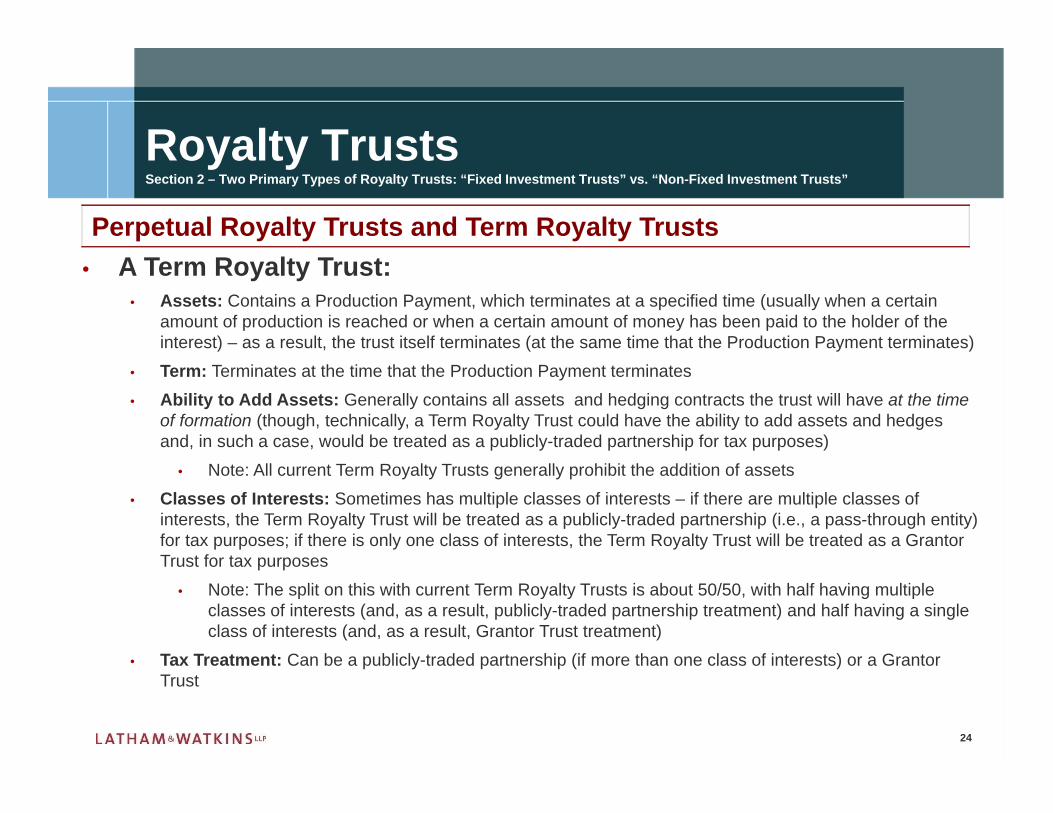

Perpetual Royalty Trusts and Term Royalty Trusts• A Term Royalty Trust:

• Assets: Contains a Production Payment, which terminates at a specified time (usually when a certain amount of production is reached or when a certain amount of money has been paid to the holder of the interest) – as a result, the trust itself terminates (at the same time that the Production Payment terminates)

• Term: Terminates at the time that the Production Payment terminates• Ability to Add Assets: Generally contains all assets and hedging contracts the trust will have at the time

of formation (though, technically, a Term Royalty Trust could have the ability to add assets and hedges and, in such a case, would be treated as a publicly-traded partnership for tax purposes)

• Note: All current Term Royalty Trusts generally prohibit the addition of assets • Classes of Interests: Sometimes has multiple classes of interests – if there are multiple classes of

interests, the Term Royalty Trust will be treated as a publicly-traded partnership (i.e., a pass-through entity) for tax purposes; if there is only one class of interests, the Term Royalty Trust will be treated as a Grantor Trust for tax purposes

• Note: The split on this with current Term Royalty Trusts is about 50/50, with half having multiple classes of interests (and, as a result, publicly-traded partnership treatment) and half having a single class of interests (and, as a result, Grantor Trust treatment)

• Tax Treatment: Can be a publicly-traded partnership (if more than one class of interests) or a Grantor Trust

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

MCLE Code

Record this code now:

*******All Participants will need to record this code on the MCLE

Activity Form to receive MCLE credit for viewing this program. Download the MCLE form (if you haven’t already done so) from the “MCLE Activity” button located at the

bottom of your screen.

25

26

Perpetual Royalty Trusts and Term Royalty Trusts

• At formation, the Sponsor must decide which type of Royalty Trust it wishes to form.

• The real difference between the two types lies in the tax treatment to Sponsor of the conveyance of the mineral interest

• If the Sponsor wishes to carve out a Production Payment from its underlying minerael interests, the Sponsor should form a Term Royalty Trust

• If, however, the Sponsor wishes to convey a Royalty Interest or a Net Profits Interest, the Sponsor generally would form a Perpetual Royalty Trust

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

27

Methods of Taxation – Fixed Investment Trusts vs. Non-Fixed Investment Trusts

• The Characteristics of the Royalty Trust determine the tax treatment.• A Fixed Investment Trust is ignored for tax purposes; unitholders are

treated as owning an undivided interest in the underlying trust properties • A Non-Fixed Investment Trust is treated as a publicly-traded partnership

for tax purposes

• The Treasury Regulations dictate that certain characteristics require certain tax treatment.• A Fixed Investment Trust is ignored for tax purposes because the entity

meets the qualification rules for such treatment found in Treas. Reg. §301.7701-4

• A Non-Fixed Investment Trust is treated as a publicly-traded partnership for tax purposes because the entity does not meet the Fixed Investment Trust qualification rules

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

28

Fixed Investment Trusts and the Trust Qualification Rules of Treas. Reg. § 301.7701-4

• In order for a Royalty Trust to be ignored for tax purposes, the entity must meet the qualification rules found in Treas. Reg. §301.7701-4

• (1) There can be no power under the Trust agreement to “vary the investment of the certificate holders”

• Corpus must be a “fixed investment,” and the Trustee can have no power to add additional properties

• (2) There can only be one class of ownership interests

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

29

Fixed Investment Trust Taxation

• A Fixed Investment Trust meets the qualification rules and, as a result, will be ignored for tax purposes. This means:

• Taxation of Sponsor: Conveyance by the Sponsor to the trust of the royalty interests in the underlying properties is a non-taxable event. The IPO sale by the Sponsor of the interests in the trust, however, will be a taxable transaction

• Gain to Sponsor = (consideration received) – (basis in the royalty interest conveyed to the trust)

• Taxation of Unitholders: Payments to the unitholders will be taxable as ordinary income

• Taxation of Tax Exempt Entities: Distributions are generally not considered Unrelated Business Taxable Income (“UBTI”), meaning that trust payments are not taxable to tax exempt entities

• Tax Shield for Unitholders: Unitholders are entitled to deductions for the greater of cost or percentage depletion

• Tax Information Provided to Unitholders: Provided on Form 1099

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

30

Non-Fixed Investment Trust Taxation• A Non-Fixed Investment Trust fails to meet the qualification rules, and,

as a result, is subject to tax as a publicly-traded partnership. This means:

• General Treatment: The Royalty Trust will be treated as a pass-through entity for tax purposes if the entity meets the Qualifying Income Test found in section 7704 (e.g., income from the exploration, development or marketing of oil and gas)

• Taxation of Sponsor: Conveyance by the Sponsor to the trust of the royalty interests in the underlying properties is a non-taxable event. The IPO sale by the Sponsor of the interests in the trust, however, is generally a taxable transaction

• Gain to Sponsor = (consideration received) – (basis in the royalty interest conveyed to the trust)

• Taxation of Unitholders: Payments to the unitholders will be taxable as ordinary income

• Taxation of Tax Exempt Entities: Royalty income is generally not considered UBTI, meaning that trust payments generally not taxable to tax exempt entities, except to the extent debt financed

• Tax Shield for Unitholders: Unitholders are entitled to deductions for the greater of cost or percentage depletion

• Tax Information Provided to Unitholders: Provided on Form K-1 (which requires a more sophisticated reporting system) – same as for MLPs

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

31

Tax Treatment Comparison - Fixed Investment Trusts vs. Non-Fixed Investment Trusts

Fixed Investment Trust Non-Fixed Investment Trust

General Tax Treatment Ignored for tax purposes Treated as a publicly-traded partnership (i.e., a pass-through entity) if the entity meets Qualifying Income Test

Taxation of Sponsor Conveyance of underlying properties is non-taxable; sale of interests in the trust is taxable

Same as Fixed Investment Trust if the entity meets Qualifying Income Test

Taxation of Unitholders Payments to unitholders are taxable to unitholders as ordinary income

Same as Fixed Investment Trust if the entity meets Qualifying Income Test

Taxation of Tax Exempt Entities

Royalty income not taxable to tax exempt entities, unless debt financed

Same as Fixed Investment Trust if the entity meets Qualifying Income Test

Tax Shield for Unitholders

Deductions are available for the greater of cost or percentage depletion

Same as Fixed Investment Trust if the entity meets Qualifying Income Test

Tax Information Provided to Unitholders

Provided on a 1099 Provided on a K-1 (which requires a more sophisticated reporting system) – same as for MLPs

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

32

Tax Treatment Comparison - Fixed Investment Trusts vs. Non-Fixed Investment Trusts

• The primary difference between taxation as a Fixed Investment Trust and taxation as a publicly-traded partnership is the reporting requirements –partnership taxation requires more detailed recordkeeping and a more sophisticated reporting system.

• This difference is relatively nominal, and several recently formed Royalty Trusts are treated as publicly-traded partnerships for tax purposes.

• For example, SandRidge Mississippian Trust I and ECA Marcellus Trust I are both treated as partnerships for federal income tax purposes.

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

33

A Brief Word on Production Payments

• Some Royalty Trusts include in their asset base interests known as “Production Payments”

• A trust with Production Payments in its trust corpus is taxed differently from Fixed Investment Trusts and Non-Fixed Investment Trusts

• A Production Payment is like a Net Profits Interest or Pure Royalty Interest except that it has a limited life – one that is shorter than the expected life of the mineral property that is burdened by it

• The limitation is generally expressed in volume, time or dollars

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

34

Tax Consequences of Production Payment Assets

• Because it is a term interest, a Production Payment is treated like a debt instrument for federal income tax purposes. As a result, if a trust includes Production Payments in its asset base:

• The Sponsor will recognize no gain from the conveyance of the Production Payment to the trust or from sale of the trust units – instead, the Sponsor will be treated as having issued a debt instrument, and will retain for tax purposes the ownership of the underlying mineral properties

• Proceeds from the sale of production from the property are treated as payments of principal and interest on a debt instrument resulting in a return of basis (principal) and ordinary interest income (interest) to the unitholders and an interest deduction to the Sponsor

• A portion of each payment made by the Sponsor is treated as principal (the price paid for the unit at the outset) and the remainder is treated as interest

• Production Payments provide the advantage to the Sponsor of accelerating deductions – the Sponsor can deduct the interest payments to the unitholders

Royalty TrustsSection 2 – Two Primary Types of Royalty Trusts: “Fixed Investment Trusts” vs. “Non-Fixed Investment Trusts”

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limitedliability partnerships conducting the practice in the United Kingdom, France, Italy and Singapore and as affiliated partnerships conducting the practicein Hong Kong and Japan. Latham & Watkins practices in Saudi Arabia in association with the Law Office of Mohammed A. Al-Sheikh. In Qatar, Latham& Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2012

Section 3 The Two Types In Action: VOC Energy Trust (“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

36

Royalty TrustsSection 3 – The Two Types In Action: VOC Energy Trust (“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

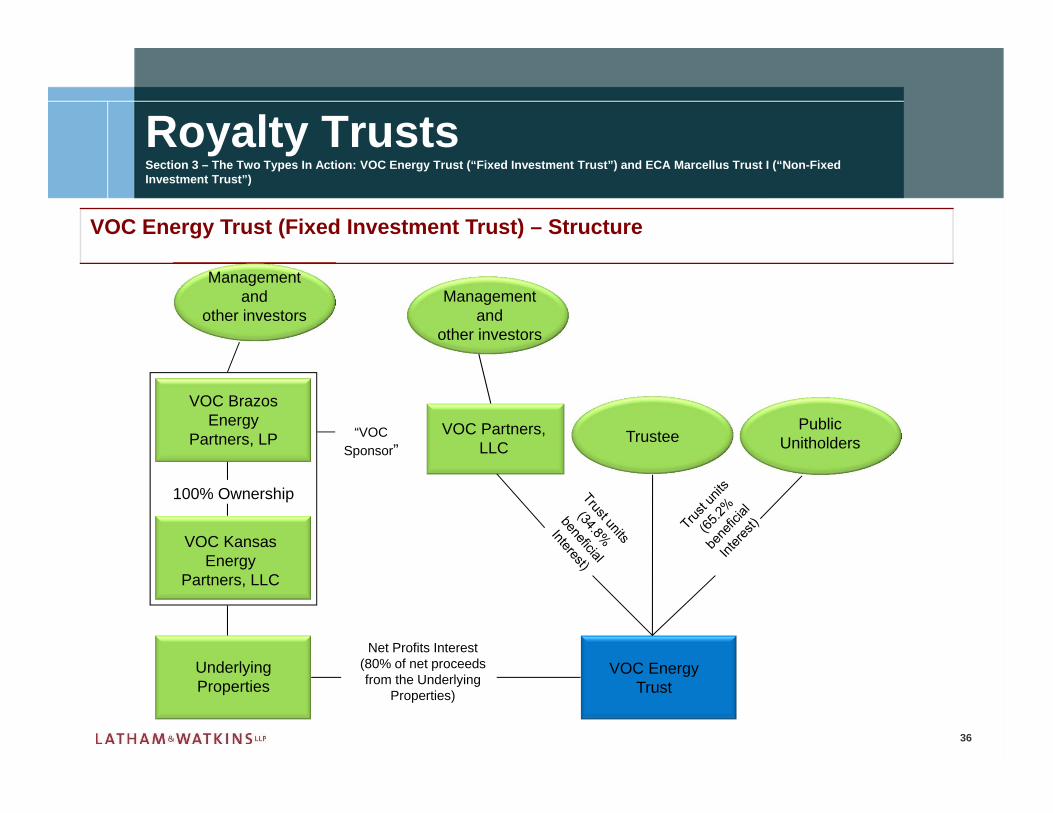

VOC Energy Trust (Fixed Investment Trust) – Structure

Management and

other investors

VOC Brazos Energy

Partners, LP

VOC Kansas Energy

Partners, LLC

Underlying Properties

VOC Partners, LLC

TrusteePublic

Unitholders

VOC Energy Trust

“VOCSponsor”

100% Ownership

Net Profits Interest(80% of net proceeds from the Underlying

Properties)

Management and

other investors

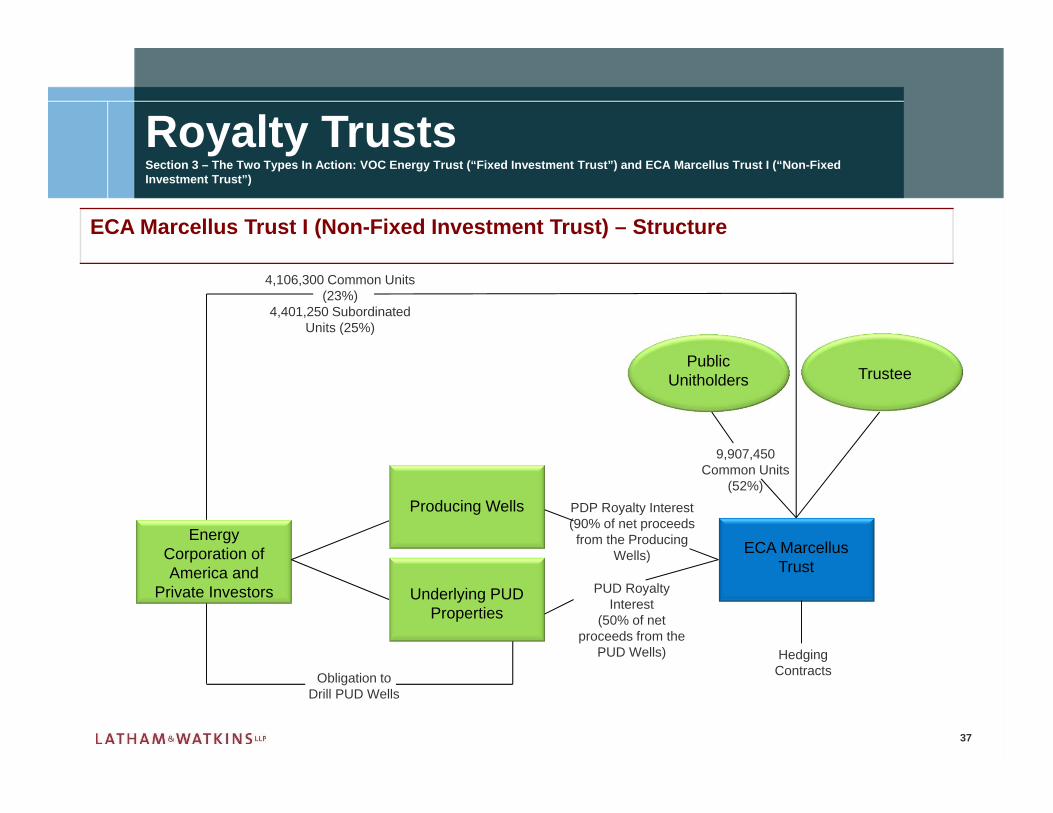

ECA Marcellus Trust I (Non-Fixed Investment Trust) – Structure

Producing Wells

TrusteePublic

Unitholders

ECA Marcellus Trust

Underlying PUDProperties

Energy Corporation of America and

Private Investors

9,907,450 Common Units

(52%)PDP Royalty Interest(90% of net proceeds from the Producing

Wells)

PUD Royalty Interest

(50% of net proceeds from the

PUD Wells)

4,106,300 Common Units (23%)

4,401,250 Subordinated Units (25%)

Obligation to Drill PUD Wells

Hedging Contracts

Royalty TrustsSection 3 – The Two Types In Action: VOC Energy Trust (“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

37

Comparison - VOC Energy Trust (Fixed Investment Trust) and ECA Marcellus Trust I (Non-Fixed Investment Trust) - Structure

VOC Energy Trust

ECA Marcellus Trust I

Underlying Properties Contain PUDLocations

Yes Yes

Percentage Public Ownership

85.2% 52%

Royalty Interest Conveyed

Net Profits Interest

Royalty Interest

Percentage of Royalty Interest Retained by Sponsor

20% 10% of PDP Wells 50% of PUD Wells

• Generally, if a Royalty Trust’s assets include substantial royalty interests in PUDlocations Wells, the royalty interests will be Pure Royalty Interests rather than Net Profits Interests. This is because it is unclear at the time of trust formation whether the PUD Wells will be profitable, and investors are sometimes hesitant to accept Net Profits Interests in properties that may cost more to develop than they are worth.

Royalty TrustsSection 3 – The Two Types In Action: VOC Energy Trust (“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

38

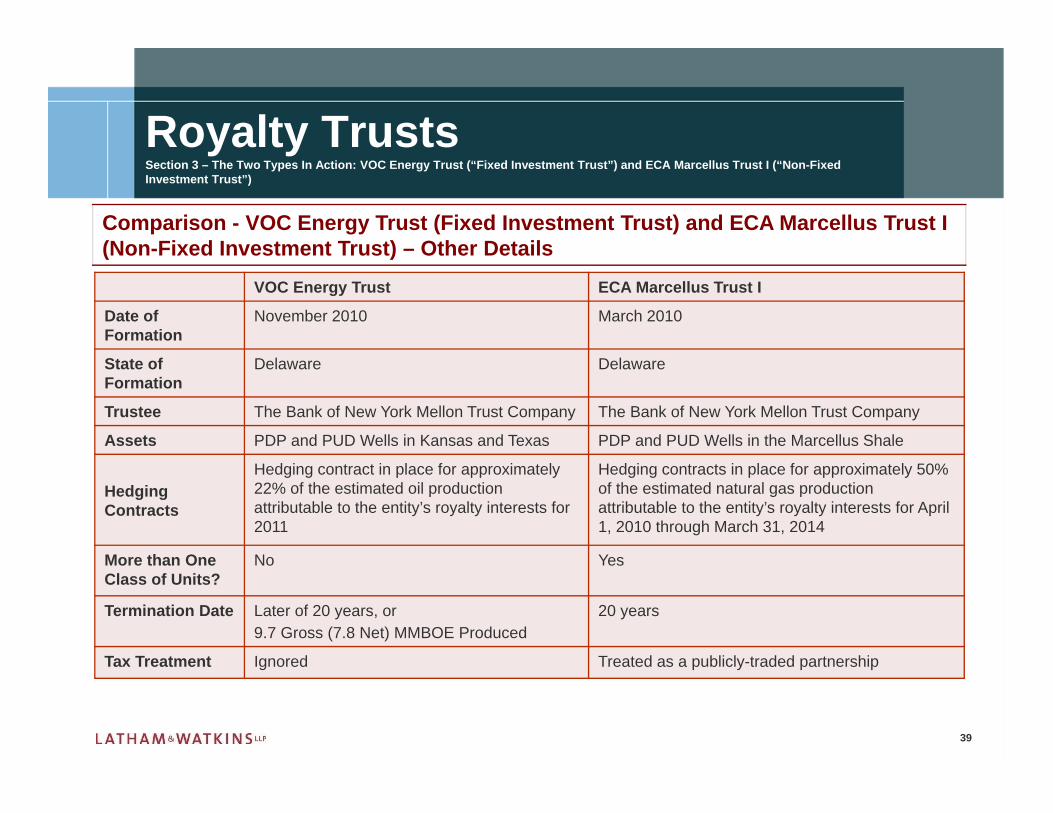

VOC Energy Trust ECA Marcellus Trust I

Date of Formation

November 2010 March 2010

State of Formation

Delaware Delaware

Trustee The Bank of New York Mellon Trust Company The Bank of New York Mellon Trust Company

Assets PDP and PUD Wells in Kansas and Texas PDP and PUD Wells in the Marcellus Shale

Hedging Contracts

Hedging contract in place for approximately 22% of the estimated oil production attributable to the entity’s royalty interests for 2011

Hedging contracts in place for approximately 50% of the estimated natural gas production attributable to the entity’s royalty interests for April 1, 2010 through March 31, 2014

More than One Class of Units?

No Yes

Termination Date Later of 20 years, or9.7 Gross (7.8 Net) MMBOE Produced

20 years

Tax Treatment Ignored Treated as a publicly-traded partnership

Comparison - VOC Energy Trust (Fixed Investment Trust) and ECA Marcellus Trust I (Non-Fixed Investment Trust) – Other Details

Royalty TrustsSection 3 – The Two Types In Action: VOC Energy Trust (“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

39

Comparison - VOC Energy Trust (Fixed Investment Trust) and ECA Marcellus Trust I (Non-Fixed Investment Trust) – Other Details

• VOC Energy Trust and ECA Marcellus Trust I are remarkably similar. Both:

• have asset pools that include royalty interests in PUD locations, • have the same Trustee, • have hedging contracts in place for at least a portion of production, and • have interests that terminate at a specified time.

• The primary differences are:• Tax Treatment

• ECA Marcellus Trust I is treated as a partnership for tax purposes because the trust has more than one class of interest

• VOC Energy Trust’s counsel gave the opinion that the trust will be ignored for tax purposes• Royalty Interests – VOC Energy Trust conveyed a Net Profits Interest, while ECA Marcellus Trust I conveyed

a Royalty Interest; ECA Marcellus Trust I presumably used a Royalty Interest because a very substantial portion of the trust’s assets were related to PUD locations where the operating costs were not known at the time of the grant of the royalty interest

Royalty TrustsSection 3 – The Two Types In Action: VOC Energy Trust (“Fixed Investment Trust”) and ECA Marcellus Trust I (“Non-Fixed Investment Trust”)

40

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of the State of Delaware (USA) with affiliated limitedliability partnerships conducting the practice in the United Kingdom, France, Italy and Singapore and as affiliated partnerships conducting the practicein Hong Kong and Japan. Latham & Watkins practices in Saudi Arabia in association with the Law Office of Mohammed A. Al-Sheikh. In Qatar, Latham& Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2012

Section 4 A Brief Comparison of Current Royalty Trusts

42

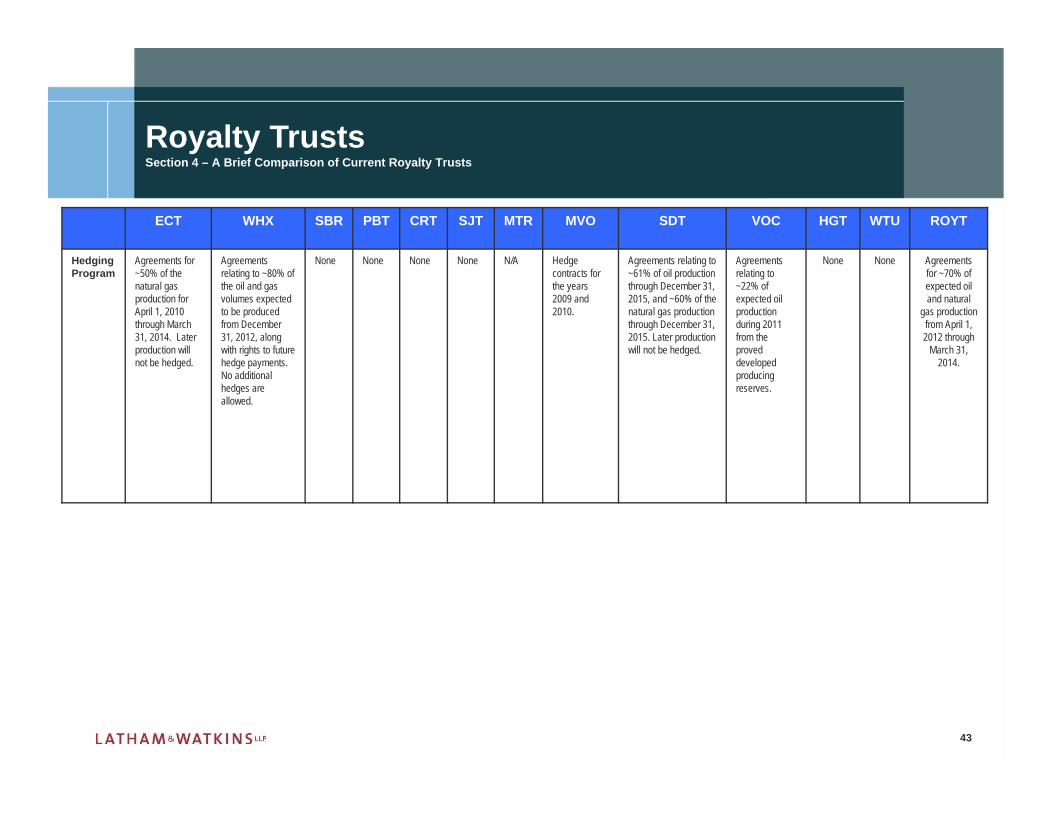

Royalty TrustsSection 4 – A Brief Comparison of Current Royalty Trusts

ECT WHX SBR PBT CRT SJT MTR MVO SDT VOC HGT WTU ROYT

Formation Date

2010 2007 1982 1980 1991 1980 1979 2006 2010 2010 1999 1992 2012

Asset Class Royalty Interest

Net Profits Interest

Royalty Interest

Net Over-riding

Royalty Interest

Net Profits Interest

Net Over-riding

Royalty Interest

Royalty Interest

Net Profits Interest

Royalty Interest

Net Profits Interest

Net Profits Interest

Net Profits Interest

Net Profits Interest

TaxTreatment

P-Ship Grantor Trust

Grantor Trust

Grantor Trust

Grantor Trust

Grantor Trust

Grantor Trust

Grantor Trust

P-Ship Grantor Trust

Grantor Trust

Grantor Trust

Grantor Trust

More than One Class of Units

Yes No No No No No No No Yes No No No No

Ability To Add Assets

No No No No No No No No No No No No No

Production Payment Treatment

Yes(in part)

Yes No No No No No Yes Yes(in part)

Yes No No No

ECT WHX SBR PBT CRT SJT MTR MVO SDT VOC HGT WTU ROYT

Hedging Program

Agreements for ~50% of the natural gas production for April 1, 2010 through March 31, 2014. Later production will not be hedged.

Agreements relating to ~80% of the oil and gas volumes expected to be produced from December 31, 2012, along with rights to future hedge payments. No additional hedges are allowed.

None None None None N/A Hedge contracts for the years 2009 and 2010.

Agreements relating to ~61% of oil production through December 31, 2015, and ~60% of the natural gas production through December 31, 2015. Later production will not be hedged.

Agreements relating to ~22% of expected oil production during 2011 from the proved developed producing reserves.

None None Agreements for ~70% of expected oil and natural

gas production from April 1, 2012 through

March 31, 2014.

Royalty TrustsSection 4 – A Brief Comparison of Current Royalty Trusts

43

44

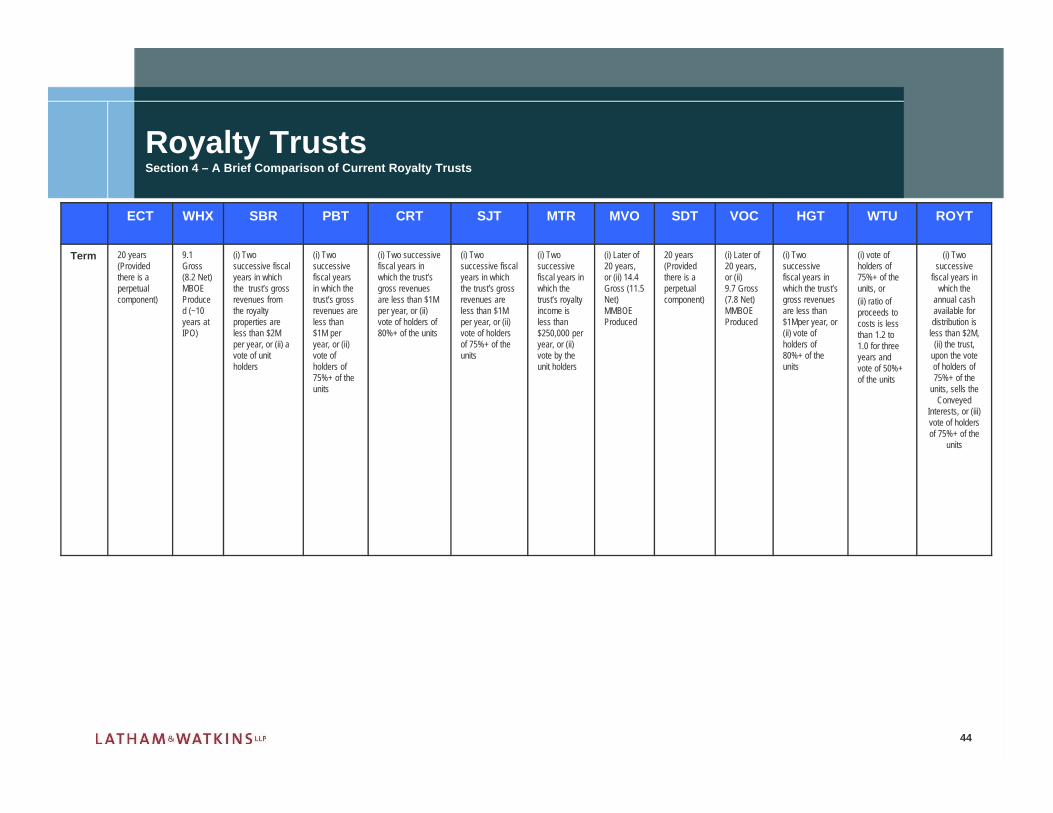

ECT WHX SBR PBT CRT SJT MTR MVO SDT VOC HGT WTU ROYT

Term 20 years (Provided there is a perpetual component)

9.1 Gross (8.2 Net) MBOEProduced (~10 years at IPO)

(i) Two successive fiscal years in which the trust’s gross revenues from the royalty properties are less than $2Mper year, or (ii) a vote of unit holders

(i) Two successive fiscal years in which the trust’s gross revenues are less than $1M per year, or (ii) vote of holders of 75%+ of the units

(i) Two successive fiscal years in which the trust’s gross revenues are less than $1Mper year, or (ii) vote of holders of 80%+ of the units

(i) Two successive fiscal years in which the trust’s gross revenues are less than $1Mper year, or (ii) vote of holders of 75%+ of the units

(i) Two successive fiscal years in which the trust’s royalty income is less than $250,000 per year, or (ii) vote by the unit holders

(i) Later of 20 years, or (ii) 14.4 Gross (11.5 Net) MMBOEProduced

20 years(Provided there is a perpetual component)

(i) Later of 20 years, or (ii) 9.7 Gross (7.8 Net) MMBOEProduced

(i) Two successive fiscal years in which the trust’s gross revenues are less than $1Mper year, or (ii) vote of holders of 80%+ of the units

(i) vote of holders of 75%+ of the units, or(ii) ratio of proceeds to costs is less than 1.2 to 1.0 for three years and vote of 50%+ of the units

(i) Two successive

fiscal years in which the

annual cash available for distribution is

less than $2M, (ii) the trust,

upon the vote of holders of 75%+ of the

units, sells the Conveyed

Interests, or (iii) vote of holders of 75%+ of the

units

Royalty TrustsSection 4 – A Brief Comparison of Current Royalty Trusts

ECT WHX SBR PBT CRT SJT MTR MVO SDT VOC HGT WTU ROYT

Reserve Data

Reserves ByCategory

32% PD / 68% PUD

100% PDP 96% PD / 4% PUD

99% PD / 1% PUD

100% PDP

95% PD / 5% PUD

99% PD / 1% PUD

86% PDP/ 14% PUD

36% PDP /64% PUD

85% PDP /15% PUD

88% PDP /12% PUD

N/A 56% PDP /6% PDNP /38% PUD

Reserve Mix 100% Gas 55% Oil / 45% Gas

49% Oil / 51% Gas

64% Oil / 36% Gas

31% Oil / 69% Gas

1% Oil / 99% Gas

30% Oil / 70% Gas

99% Oil / 1% Gas

48% Oil /52% Gas

92% Oil / 8% Gas

4% Oil / 96% Gas

N/A 98% Oil / 2% Gas

Partnership Features

Subordination 25% of Common Units

None None None None None None None 25% of Common Units

None None None None

SubordinationThreshold

80% of Target Distrib.

None None None None None None None 80% of Target Distrib.

None None None None

IncentiveThreshold

120% of Target Distrib.

None None None None None None None 120% of Target Distrib.

None None None None

Trustee Matters

Trustee New York Mellon

Bank of New York

B of A B of A B of A CompassBank

New York Mellon

New York Mellon

New York Mellon

New York Mellon

B of A B of A New York Mellon

Royalty TrustsSection 4 – A Brief Comparison of Current Royalty Trusts

45

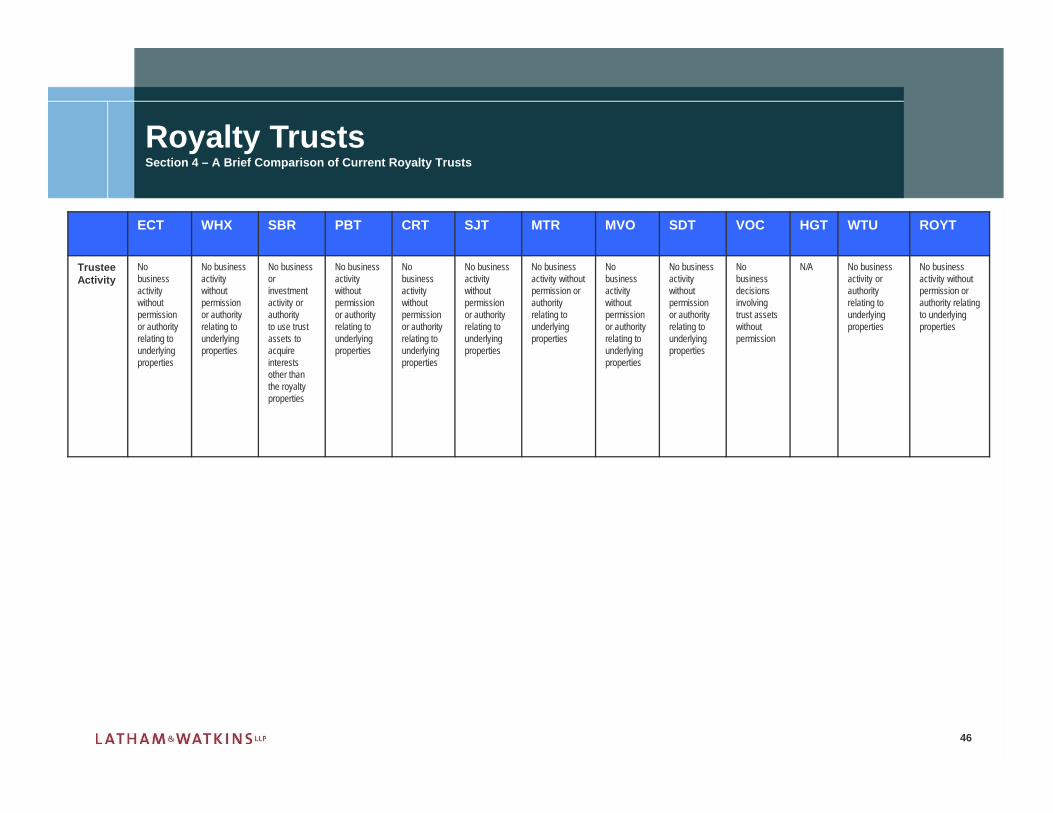

ECT WHX SBR PBT CRT SJT MTR MVO SDT VOC HGT WTU ROYT

TrusteeActivity

No business activity without permission or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

No business or investment activity or authority to use trust assets to acquire interests other than the royalty properties

No business activity without permission or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

No business decisions involving trust assets without permission

N/A No business activity or authority relating to underlying properties

No business activity without permission or authority relating to underlying properties

Royalty TrustsSection 4 – A Brief Comparison of Current Royalty Trusts

46

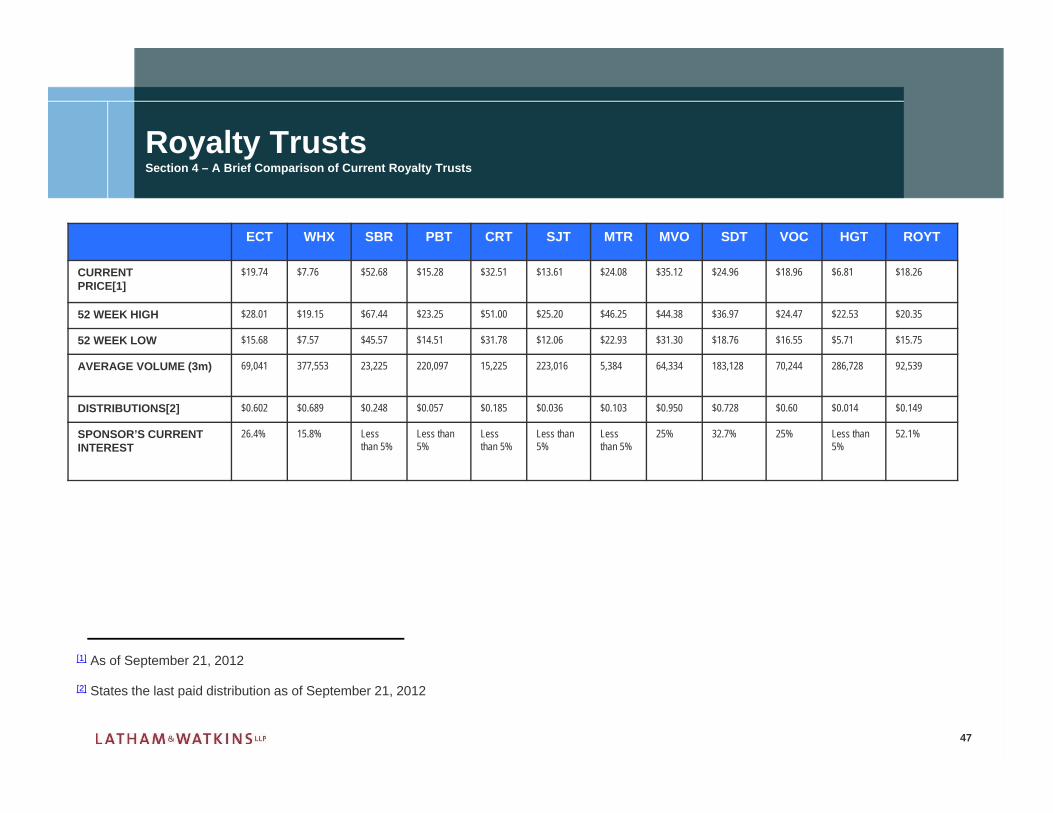

47

[1] As of September 21, 2012

[2] States the last paid distribution as of September 21, 2012

ECT WHX SBR PBT CRT SJT MTR MVO SDT VOC HGT ROYT

CURRENT PRICE[1]

$19.74 $7.76 $52.68 $15.28 $32.51 $13.61 $24.08 $35.12 $24.96 $18.96 $6.81 $18.26

52 WEEK HIGH $28.01 $19.15 $67.44 $23.25 $51.00 $25.20 $46.25 $44.38 $36.97 $24.47 $22.53 $20.35

52 WEEK LOW $15.68 $7.57 $45.57 $14.51 $31.78 $12.06 $22.93 $31.30 $18.76 $16.55 $5.71 $15.75

AVERAGE VOLUME (3m) 69,041 377,553 23,225 220,097 15,225 223,016 5,384 64,334 183,128 70,244 286,728 92,539

DISTRIBUTIONS[2] $0.602 $0.689 $0.248 $0.057 $0.185 $0.036 $0.103 $0.950 $0.728 $0.60 $0.014 $0.149

SPONSOR’S CURRENT INTEREST

26.4% 15.8% Less than 5%

Less than 5%

Less than 5%

Less than 5%

Less than 5%

25% 32.7% 25% Less than 5%

52.1%

Royalty TrustsSection 4 – A Brief Comparison of Current Royalty Trusts

48

Royalty TrustsTO COMPLY WITH INTERNAL REVENUE SERVICE CIRCULAR 230, YOU ARE HEREBY NOTIFIED THAT: (A) THIS PRESENTATION IS NOT INTENDED OR WRITTEN BY US TO BE USED, AND CANNOT BE USED BY ANY TAXPAYER, FOR THE PURPOSE OF AVOIDING PENALTIES THAT MAY BE IMPOSED ON THE TAXPAYER UNDER THE INTERNAL REVENUE CODE; (B) THIS PRESENTATION IS WRITTEN TO SUPPORT THE PROMOTION OR MARKETING OF THE TRANSACTIONS OR MATTERS ADDRESSED HEREIN; AND (C) A TAXPAYER SHOULD SEEK ADVICE BASED ON THE TAXPAYER’S PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAX ADVISOR.

Questions?

49

Contact Information

50

C. Timothy FennPartner (Houston)Email: [email protected]: +1.713.546.7432

Jeffrey S. MuñozPartner (Houston)Email: [email protected]: +1.713.546.7423

Sean T. WheelerPartner (Houston)Email: [email protected]: +1.713.546.7418

Disclaimer

Although this presentation may provide information concerning potential legal issues, it is not a substitute for legal advice from qualified counsel.

The presentation is not created or designed to address the unique facts or circumstances that may arise in any specific instance, and you should not and are not authorized to rely on this content as a source of legal advice and this seminar material does not create any attorney-client relationship between you and Latham & Watkins.

© Copyright 2012 Latham & Watkins. All Rights Reserved.

51