rod larson president es de t - oceaneering · 2017-03-27 · rod larson president scotia howard...

TRANSCRIPT

Rod LarsonRod LarsonPresidentPresident

Scotia Howard Weil Energy ConferenceScotia Howard Weil Energy ConferenceM h 29 2017M h 29 2017

es de tes de t

March 29, 2017 March 29, 2017 New Orleans, LANew Orleans, LA

Forward-Looking Statements

Statements we make in this presentation that express a belief, expectation, or intention are forward looking. Forward-looking statements are generally accompanied by words such asare generally accompanied by words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “plan,” “forecast,” “budget,” “goal,” or other words that convey the uncertainly of future events or outcomes. These forward looking statements are basedThese forward-looking statements are based on our current information and expectations that involve a number of risks, uncertainties, and assumptions. Among the factors that could cause the actual results to differ materially from those indicated in the forward-looking statements are: industry conditions, prices of crude oil and natural gas, our ability to obtain and the timing of new projects, and changes in competitive factors. Should one or g pmore of these risks or uncertainties materialize, or should the assumptions underlying the forward-looking statements prove incorrect, actual outcomes could vary materially from those indicatedmaterially from those indicated.

For additional information regarding these and other factors, see our periodic filings with the Securities and Exchange Commission,

2

including our most recent Reports on Forms 10-K and 10-Q.

Why Oceaneering?

Global provider of diversified services and products in all phases Global provider of diversified services and products in all phases Global provider of diversified services and products in all phases of the offshore oilfield life cycle Global provider of diversified services and products in all phases

of the offshore oilfield life cycle

Strong market positions

S lid b l h t d h fl

Strong market positions

S lid b l h t d h fl Solid balance sheet and cash flow

Return of capital to our shareholders

Solid balance sheet and cash flow

Return of capital to our shareholdersReturn of capital to our shareholders

Leveraged to deepwater - longer term, deepwater is still critical to

Return of capital to our shareholders

Leveraged to deepwater - longer term, deepwater is still critical to reserve replenishmentreserve replenishment

3

5 Operating Segments

1 Remotely Operated Vehicles (“ROVs”)1 Remotely Operated Vehicles (“ROVs”)1. Remotely Operated Vehicles ( ROVs )

2 Subsea Products

1. Remotely Operated Vehicles ( ROVs )

2 Subsea Products2. Subsea Products

3 Subsea Projects

2. Subsea Products

3 Subsea Projects3. Subsea Projects

4. Asset Integrity

3. Subsea Projects

4. Asset Integrity4. Asset Integrity

5. Advanced Technologies

4. Asset Integrity

5. Advanced Technologies gg

4

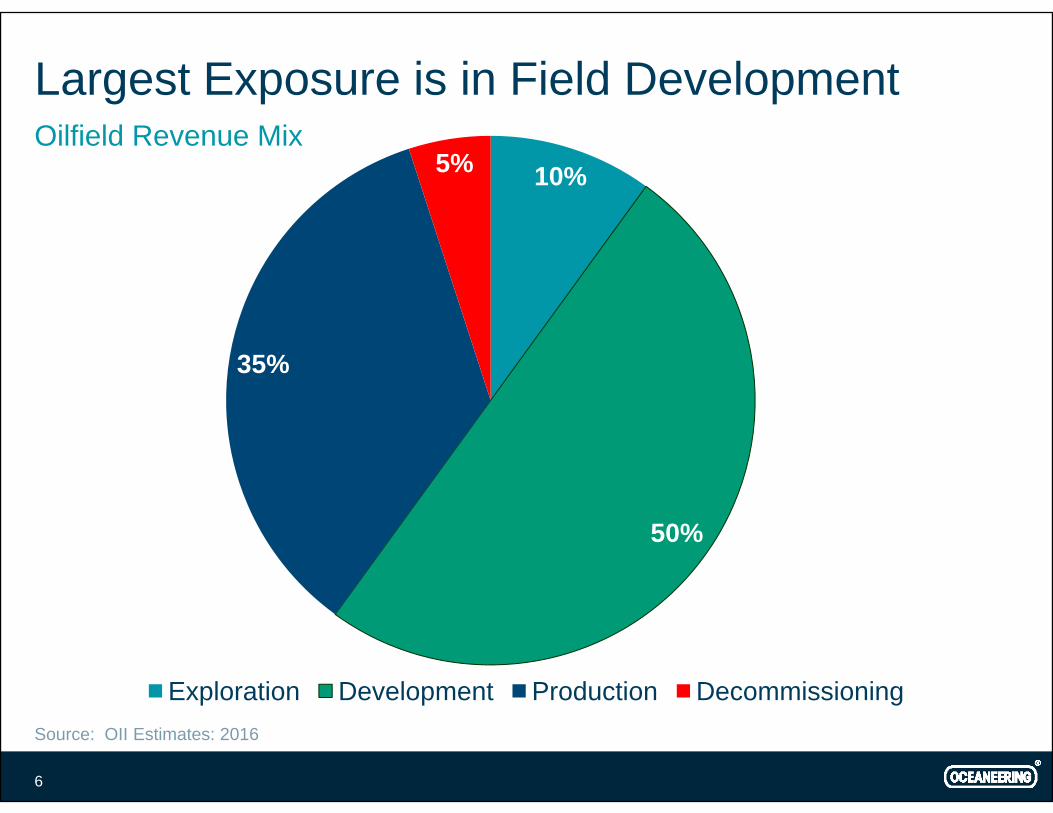

In All Phases of the Offshore Oilfield Life CycleEXPLORATION

10%

DEVELOPMENT

50%

PRODUCTION

35%

DECOMMISSIONING

5%

# of Operating # of Subsea Tree # of Subsea Trees # of Field

PHASE

% OII Revenue

#1 Market # of OperatingFloating Drilling Rigs

# of Subsea Tree Installations

# of Subsea TreesIn Service

# of Field Abandonments

#1 Market Driver

Business Segment Product

and S i

•• ROVROV•• Survey (SP)Survey (SP)•• Tooling (SSP)Tooling (SSP)

Service Revenue Streams

• ROV• Survey (SP)• Tooling (SSP)• IWOCS – Installation &

Workover Control Systems

• ROV• Tooling (SSP)• IWOCS (SSP)• Subsea Hardware (SSP)• Vessel-based Inspection,

• ROV • Tooling (SSP)• IWOCS (SSP)

(SSP)• Subsea Hardware (SSP)• Umbilicals (SSP)• Vessel-based Installation

Services (SP)• Inspection Services (AI)

Maintenance & Repair Services (SP)

• Inspection Services (AI)

ROV = Remotely Operated Vehicles SSP = Subsea Products SP = Subsea Projects AI = Asset Integrity

5

Largest Exposure is in Field Development

10%5%Oilfield Revenue Mix

35%

50%

Exploration Development Production Decommissioningp p gSource: OII Estimates: 2016

6

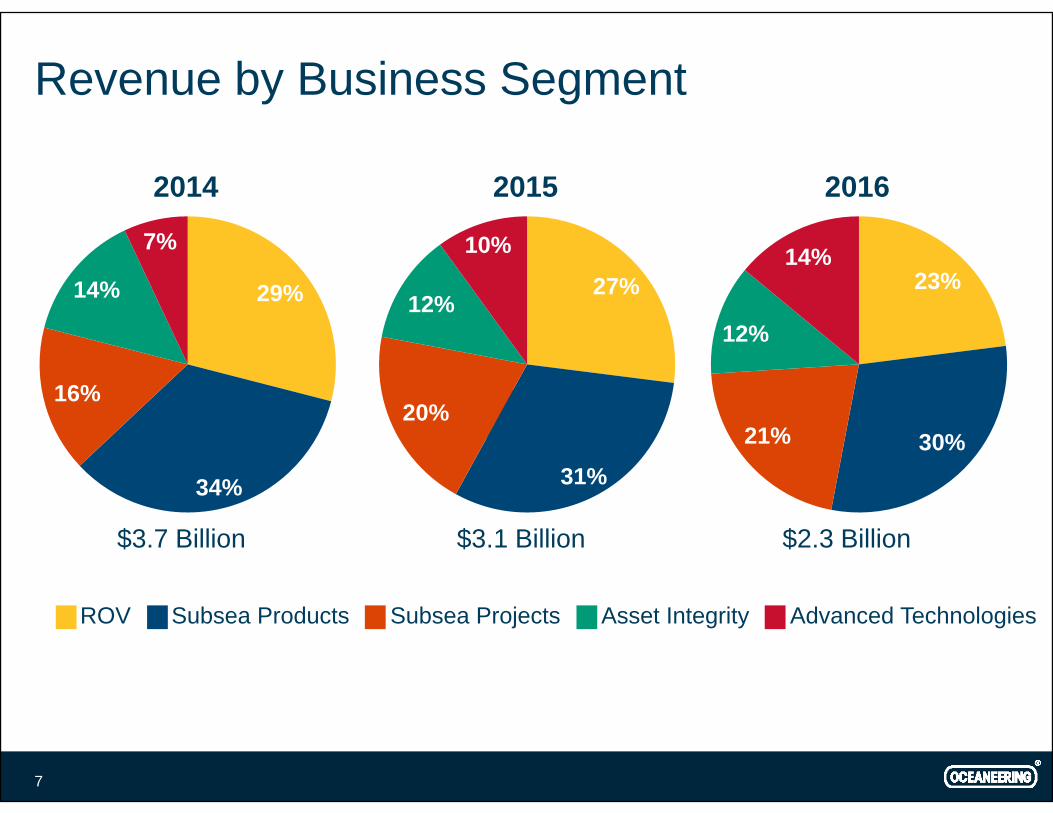

Revenue by Business Segment

2014 2015 2016

29%14%

7%

27%12%

10%23%

14%

16%20%

12%12%

34% 31%

20%30%21%

$3.7 Billion $3.1 Billion $2.3 Billion

ROV Subsea Products Subsea Projects Asset Integrity Advanced Technologies

7

Remotely Operated Vehicles 23%

Revenue Contribution 2016

Flagship of the Oceaneering Franchise

8

Oceaneering ROV Fleet Size – 280 ROVs

350

as of December 31, 2016

350

End

300

nt a

t Per

iod

250

ehic

le C

oun

Ve

2002008 2009 2010 2011 2012 2013 2014 2015 2016*

9

* Retired 39 ROVs in Q3 2016.

Oceaneering ROV Pricing and Fleet Utilization

100%$11 000Revenue / Day on Hire Fleet Utilization

53% Fleet Utilization as of December 31, 2016

80%

90%

100%

$9,000

$10,000

$11,000

Hire

60%

70%

$6,000

$7,000

$8,000

iliza

tion

ue /

Day

on

30%

40%

50%

$3 000

$4,000

$5,000

Flee

t Ut

Rev

enu

10%

20%

$1,000

$2,000

$3,000

0%$02008 2009 2010 2011 2012 2013 2014 2015 2016

10

Floating Rig Demand History

100%300Floaters Contracted % with OII ROVs

Oceaneering 53% Market Share as of December 31, 2016

75%

100%

250

300

d En

d

75%200

I RO

Vs

gs a

t Per

iod

50%

100

150

% w

ith O

I

Floa

ting

Rig

25%50

Con

tract

ed F

0%02014 Q1

2014 Q2

2014 Q3

2014 Q4

2015 Q1

2015 Q2

2015 Q3

2015 Q4

2016 Q1

2016 Q2

2016 Q3

2016 Q4

C

Source: IHS-Petrodata, December 31, 2016

11

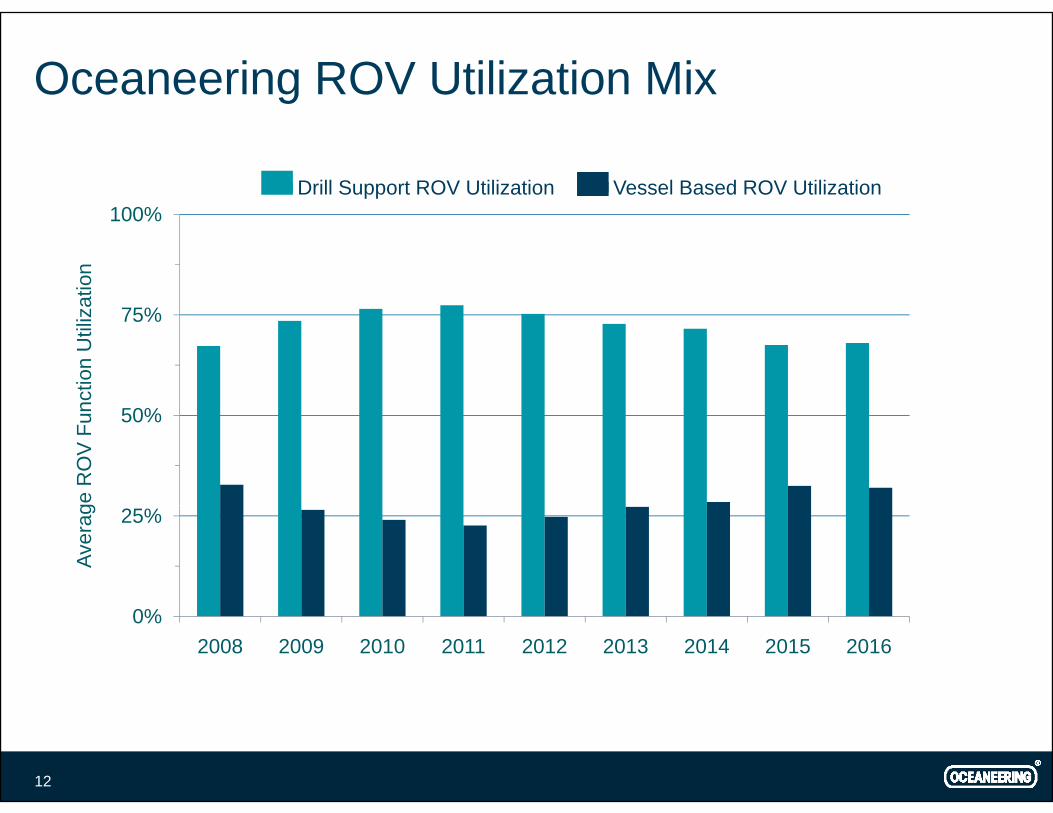

Oceaneering ROV Utilization Mix

100%Drill Support ROV Utilization Vessel Based ROV Utilization

75%

100%

atio

n

75%

nctio

n U

tiliz

50%

ge R

OV

Fun

25%

Aver

ag

0%2008 2009 2010 2011 2012 2013 2014 2015 2016

12

More Focus on Vessel-Based Services

10 ROVs to Heerema Marine Contractors 10 ROVs to Heerema Marine Contractors Providing ROVs and subsea tooling aboard Heerema’s deepwater

construction vessels and semi-submersible crane vessels on aconstruction vessels and semi submersible crane vessels on a global basis through 2020.

8 ROVs to Maersk Supply Services 8 ROVs to Maersk Supply Services Providing ROVs, survey and associated services, including subsea

tooling, engineering, communication and data solutions, to supporttooling, engineering, communication and data solutions, to support Mærsk’s global operations.

13

ROV New Technologies

14

Subsea Products 30%

Manufactured Products

Production Control UmbilicalsS

Revenue Contribution 2016

S i lt S b H d

Supply electric and hydraulic power to subsea trees and inject chemicals into reservoirs and well streams.

Specialty Subsea HardwareField development hardware used to connect production trees to umbilicals and flow lines.Also includes connectors and valves.

Service and Rental

Also includes connectors and valves.

T li & S b W k S tTooling & Subsea Work SystemsSupport drilling, construction, field maintenance, and plugging and abandonment activities.

Support drilling, construction, field maintenance, and plugging and abandonment activities

Installation and Workover Control Systems (IWOCS)

15

abandonment activities.

Subsea Hardware Capex Forecast

$6 000$1 000Subsea Capex, Infield Jan 2017 SS Products Backlog

Backlog at December 31, 2016, $ in millions

$4,800

$6,000

$800

$1,000

xg

$3,600$600

war

e C

apex

ucts

Bac

klog

$2,400$400

bsea

Har

dw

II S

S P

rodu

$1,200$200

SuO

$0$02012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Source: Infield Systems, Jan 2017; EPIC covers Capex for subsea trees, templates, manifolds, subsea boosters/compression/separation, umbilicals

16

Subsea Installations Forecast

$1 500500Trees Onstream SSProducts Revenue

$1,200

$1,500

400

500

Mill

ions

am

$900300

enue

, $ in

M

es O

nstre

a

$600200

oduc

ts R

evTre

$300100

OII

SS

Pro

$002012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Source: Infield Systems, January 2017

17

Subsea Projects 21%

Revenue Contribution 2016

Change out photo and replace with

AUVAUV

Consist of Project Management, Survey, Subsea

18

Installation and IMR Services

Subsea Projects Overview

Spot or Contract Location

CharterEnd

Assets Available for this Market

Deepwater Multi-Purpose Supply VesselsContract Location End

3 Owned

*Ocean Intervention Spot GOM N/A*Ocean Intervention

*Ocean Intervention II

*Ocean Evolution (available mid 2017)

SpotSpot N/A

GOMGOM

N/AN/AN/A

1 Chartered on Spot Market

*Ocean Alliance Spot GOM Mar ‘18

2 Chartered with Term2 Chartered with TermOcean Intervention IIIIsland Pride

ContractContract

AngolaIndia

Jul ‘17Nov ‘17

Di i S t V l Diving Support Vessels Survey/AUV Services Global Data Solutions Global Data Solutions

19

* Jones Act Vessel

Strong Balance Sheet and Liquidity

Liquidity at 2016 year end

Capital Sources and Allocations

Liquidity at 2016 year end o $450 million of cash, over $300 million in the U.S. o $500 million undrawn revolving credit facility, $450 million expiring

October 2021October 2021o First debt maturities $30 million in October 2018

Organic capital expendituresOrganic capital expenditureso Expect to range from $90 million to $120 million in 2017

Acquisitions qo Continue to consider investments that augment our service or product

offerings, with more focus on our customers’ OPEX

Di id d Dividendso Quarterly $0.15 per share, sustainable

Consider share repurchases Consider share repurchases

20

Leveraged to Deepwater

Projects take years to develop Projects take years to developProjects take years to develop

Largely oil reservoirs

Projects take years to develop

Largely oil reservoirso With high production flow rates

Well capitalized customer base

o With high production flow rates

Well capitalized customer baseWell capitalized customer baseo ~50% revenue from E&P majors in prior 3 years

Well capitalized customer baseo ~50% revenue from E&P majors in prior 3 years

Investment based on long-term commodity price expectations Investment based on long-term commodity price expectations

21

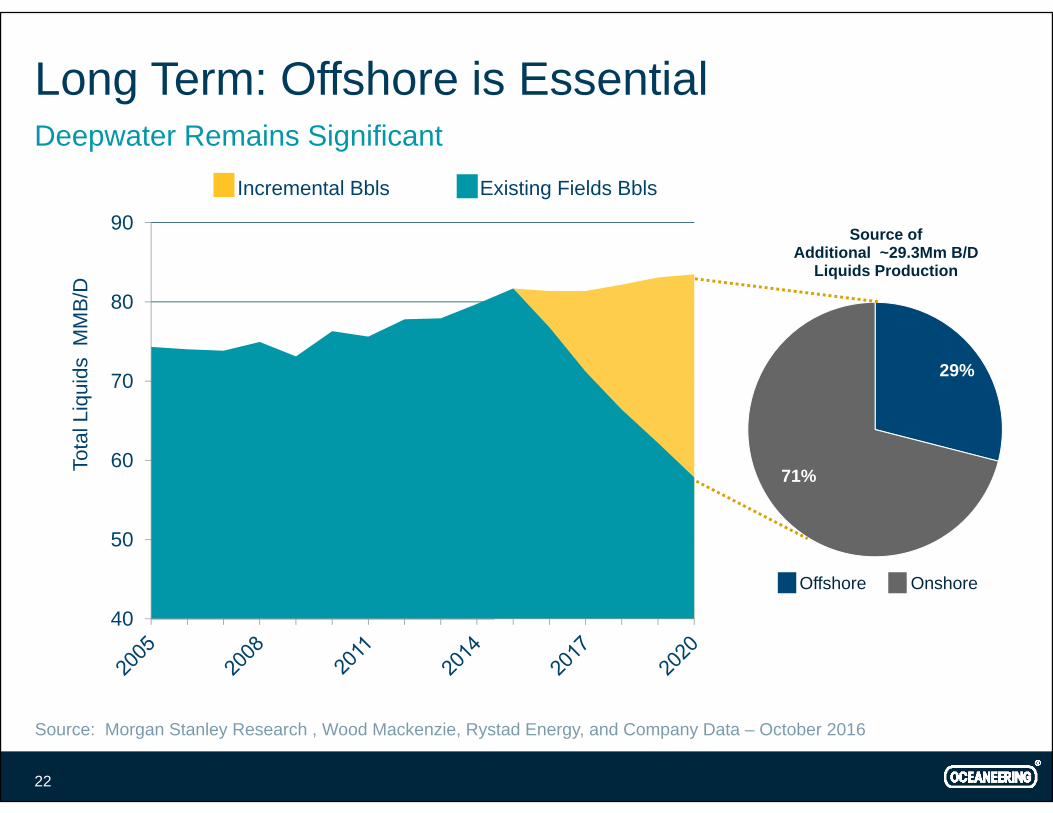

Long Term: Offshore is Essential

Incremental Bbls Existing Fields Bbls

Deepwater Remains Significant

Source of Additional ~29.3Mm B/D

Liquids Production

80

90

B/D

29%70

80

quid

s M

MB

71%60To

tal L

i

Offshore Onshore

50

40

Source: Morgan Stanley Research , Wood Mackenzie, Rystad Energy, and Company Data – October 2016

22

2017 Full Year and First Quarter Outlook

Challenging market continues Challenging market continues

Aligned our operations with anticipated level of activity

P j ti f th d li i fit bilit f th f ll 2017 Projecting a further decline in profitability for the full year 2017

o Expecting marginally profitable at the operating income level

Forecasting 1Q 2017 considerably lower than adjusted 4Q 2016

o Sequentially lower operating income mainly from Asset Integrity, and higher Unallocated Expenses

o Expect a discrete additional income tax provision in accordance with a new accounting standard associated with our share based incentive plan

23

Conclusion

Longer term deepwater is still critical to reserve replenishment Longer term, deepwater is still critical to reserve replenishment

Global provider in all phases of offshore oilfield life cycle, with p p ya deepwater focus

Further differentiate with integrated solutions Further differentiate with integrated solutions

Strong liquidity and cash flowStrong liquidity and cash flow

Maintain or grow our market positions

Emerge from the current cycle ready for the upturn

24

EBITDA Reconciliation to Net Income

Earnings before interest, taxes, depreciation and amortization (EBITDA) is a non-GAAP financial measurement. Oceaneering’s management uses EBITDA because we believe that this measurement is a widely accepted financial indicator used by investors and

l t t l d i th b i f ti f d th t thi t b d b

(USD in millions)

analysts to analyze and compare companies on the basis of operating performance, and that this measurement may be used by some investors and others to make informed investment decisions. You should not consider EBITDA in isolation from or as a substitute for net income or cash flow measures prepared in accordance with generally accepted accounting principles or as a measure of profitability or liquidity. EBITDA calculations by one company may not be comparable to EBITDA calculations made by another company. The following table provides a reconciliation between net income (a GAAP financial measure) and EBITDA (a non-GAAP financial measure) for Oceaneering’s historical and projected results on a consolidated basis for the periods indicated:

Period Ended 2011 2012 2013 2014 2015 2016

for Oceaneering s historical and projected results on a consolidated basis for the periods indicated:

Net Income $ 235.7 $ 289.0 $ 371.5 $ 428.3 $ 231.0 $ 24.6

Depreciation & Amortization 151.2 176.5 202.2 229.8 241.2 250.2

Subtotal 386.9 465.5 573.7 658.1 472.2 274.8

Interest Expense/Income, Net 0.2 2.3 1.7 4.4 23.4 20.3

Income Tax Expense 102.2 132.9 170.8 195.2 105.3 18.8

EBITDA $ 489.3 $ 600.7 $ 746.2 $ 857.7 $ 600.9 $ 313.9

26

Free Cash Flow (Through the Cycle)

“Free Cash Flow” (FCF) is a non-GAAP financial measurement. FCF represents cash flow provided by operating activities less organic capital expenditures (i e purchases of property and equipment other than those in business

(USD in millions)

activities less organic capital expenditures (i.e., purchases of property and equipment other than those in business acquisitions. Management believes that this is an important measure because it represents funds available to reduce debt and pursue opportunities that enhance shareholder value, such as making acquisitions and returning cash to shareholders through dividends or share repurchases.

Period Ended 2011 2012 2013 2014 2015 2016

Net Income $ 235.7 $ 289.0 $ 371.5 $ 428.3 $ 231.0 $ 24.6

Depreciation & Amortization 151.2 176.5 202.2 229.8 241.2 250.2

Other Changes in Cash ProvidedOther Changes in Cash Provided by Operating Activities (98.3) (27.7) (42.3) 63.7 88.2 65.7

Cash Provided by Operating Activities 288.6 437.8 531.4 721.8 560.4 340.5Purchases ofPurchases of Property & Equipment (235.0) (300.6) ( 382.5) (386.9) (200.0) (112.4)

Free Cash Flow $ 53.5 $ 137.2 $ 148.9 $ 334.9 $ 360.4 $ 228.1

27

Oceaneering ROV Leading Market Position

Ownership Drill Support Market Share

Remotely Operated Vehicles

Ownership pp

28028%

OII

8053%

Subsea 7FugroDOF SubseaC-InnovationsHelixSaipemTMTTechnippIKM GroupOtherWorldwide Fleet

1010 Vehicles*151 Floating Rigs Contracted**

Source: *OII Estimates - December 2016; **IHS Petrodata and OII Estimates – December 31, 2016

28

Oceaneering ROV Fleet – 280 ROVs

100

Geographic Profile – December 31, 2016

88

7280

90

100

53

72

50

60

70

OV

s

2229

30

40

50

RO

2216

10

20

0GOM Africa North

SeaBrazil Asia/Pac Other

Other includes Canada, Mexico, and the Middle East.

29

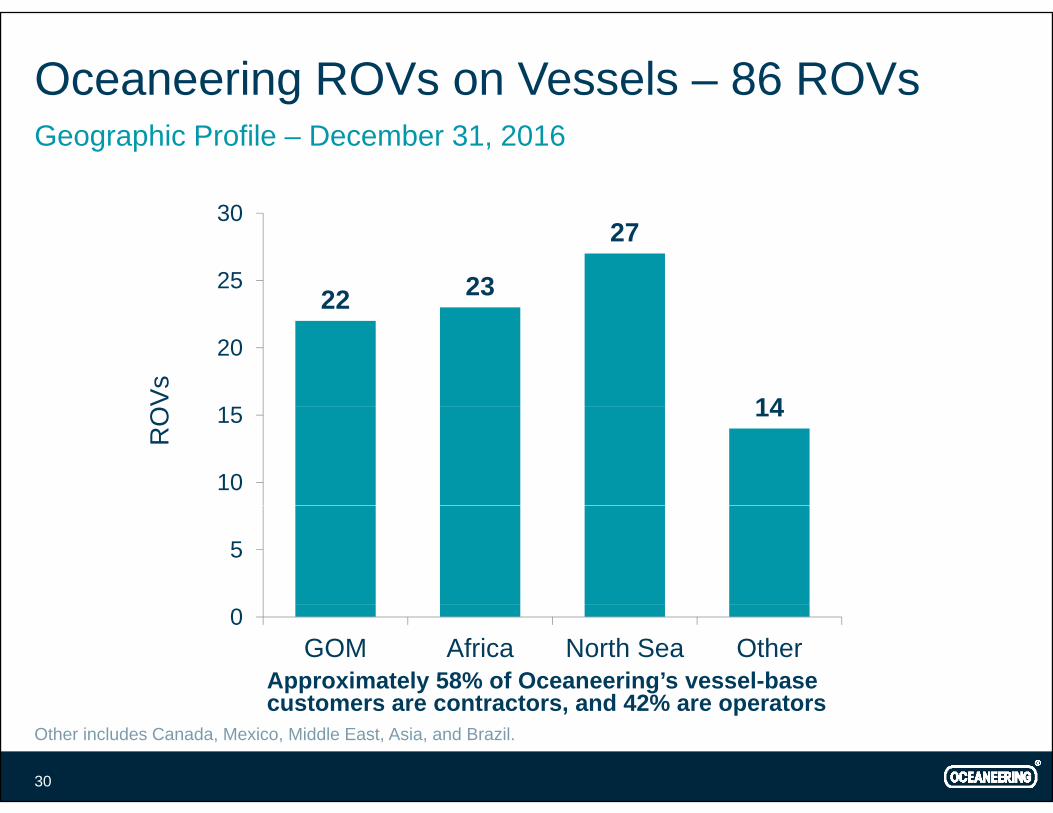

Oceaneering ROVs on Vessels – 86 ROVs

30

Geographic Profile – December 31, 2016

22 23

27

25

30

22

1415

20

Vs

14

10

15

RO

5

0GOM Africa North Sea Other

Approximately 58% of Oceaneering’s vessel-base customers are contractors and 42% are operators

Other includes Canada, Mexico, Middle East, Asia, and Brazil.

30

customers are contractors, and 42% are operators

Investor Relations ContactInvestor Relations Contact

Suzanne SperaSuzanne SperaDirector, Investor [email protected]

31