rkp - recent dvpts and controversies v2 - transfer pricing · transfer pricing - recent...

TRANSCRIPT

Transfer Pricing - Recent Developments and Controversies

Rohan K. PhatarphekarPartner and National Head,Global Transfer Pricing Services

BCAS

4th November 2015

1© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Areas of Discussion

1

BPO vs. KPO

Contract R&D vs. Entrepreneurial R&D

2

Location Savings

3

5

6TP Dispute Resolution Mechanisms –Developments in APA and MAP

4

Marketing Intangible

Share Valuation

Way forward

7

Glossary

8

9

Recent Developments

2© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transfer Pricing – Key Controversies

3© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Indian TP environment

Statistics of TP Audit Adjustments till date

Source : Annual Report 2014-15 – Ministry of Finance

4© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transfer Pricing - Key Issues/Controversies

Key issues

Marketing Intangibles

Share Valuation

BPO vs. KPO

Contract R&D vs.

Entrepreneurial R&D

Location Savings

5© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Marketing Intangibles

6© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Marketing Intangibles (Advertisement, Marketing and Promotion – AMP expenses)

Issue involved / Approach of the Revenue

� Assessee spends significant amount on AMP expense benefitting the AE by creating marketing intangibleswithout corresponding compensation/ reimbursement to the assessee.

� Revenue authorities compare expense to sales ratio of assessee with other comparables – disallows AMPexpense in excess of “bright-line” as TP adjustment alleging contribution by taxpayer is towards strengtheningAE owned brands.

� Expectation of mark-up on recovery of AMP expense in excess of bright line. The average AMP expensesincurred by companies in the industry is considered as Bright Line for the purpose of Transfer Pricing analysis.

ExcessExcessAssumed to be incurred for strengthening brand name of foreign AE

Indian licensee:Must be reimbursed along with suitable profit mark-up

AMP spend by Indian licensee

Arm’s length licensee

expenditure

(-)(-)

Bright line

Bright line method adoptedby relying on US Tax

court case in DHL

7© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

LG Electronics : Special Bench decision to deal with legal issues not factual issues

� Indian company, engaged in manufacturing of Electronicgoods in India , is a subsidiary of a Foreign Company

� Indian Company incurs AMP expenses for marketing thegoods produced in India

� Indian company has incurred AMP expenses whichexceeds the Bright Line limit

�Excess AMP expenses incurred by the Indian Company

is perceived to enhance the brand value of ForeignCompany

� Indian tax authorities have contended that AMPexpenditure incurred by a taxpayer at a level that exceedsthe “bright line” is to be reimbursed by the foreign AE with

a mark-up

Brand Creation / Marketing

Intangible

Indian Company

Foreign Company

Excessive AMP

Expenses

Owner of Brand

In India

Outside

India

Judicial Precedent

• Incurring of AMP expenses by the assessee towards brand legally owned by the foreign AE constituted a'transaction' subject to TP provisions;

• Upholds use of Bright Line Test for determining cost / value of such transactions:

• Under IT Act, it is legal ownership of brand that is recognized - Special Bench Majority View

• Matter on the quantification set aside to re-look at comparables and appropriate cost base

8© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Judicial Precedent

Sony Ericsson - Delhi High Court

� Delhi High Court in the Sony Ericsson Mobile Communication India Pvt. Ltd and several other connected mattersITA No. 16/2014:

� Characterizing AMP expenses as an international transaction subject to transfer pricing

� Distribution and marketing are intertwined functions and can be analysed together as a bundled transaction

� Segregation of non-routine AMP expenditure using the bright line approach inappropriate

� For selection of comparables, intensity of AMP functions is critical

� Separate remuneration for the AMP activities may not be required if such compensation is already provided by wayof lower purchase price or reduced payment of royalty

� Concept of ‘economic ownership’ of brand recognized

9© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Share Valuation

10© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Share Valuation

General contentions of the Taxpayers

� Issue of equity share capital does not constitute ‘income’ hence not covered by section 92(1) of the

Income Tax Act and therefore there is no requirement to satisfy the arm’s length test laid down by the Act.

� The valuation report ought to be accepted by the Revenue unless it is proved to be vitiated by fraud, bias

or a patent mistake.

� The shortfall in the value of equity shares cannot be considered as a deemed loan, as no actual loan has

been given by the taxpayer and hence there is no question of Transaction as defined under section 92F

of the Act.

� The action proposed by the revenue in considering the shortfall as a deemed loan would tantamount to

consider every transfer pricing adjustment as a notional loan/receivable.

� It is not open to the department to prescribe or dictate to the assessee as to how it should have

conducted the business or earned income on its funds.

General contentions of the Revenue

� All type of transactions being in nature of Capital Financing under clause (v) of explanation to section 92F

of the Act have been included in the definition of international transactions from retrospective effect from

1st April 2002.

� Issue of equity shares is in nature of Capital Financing and hence is an international transaction which is

required to be at arm’s length under the Indian Transfer Pricing regulations.

11© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

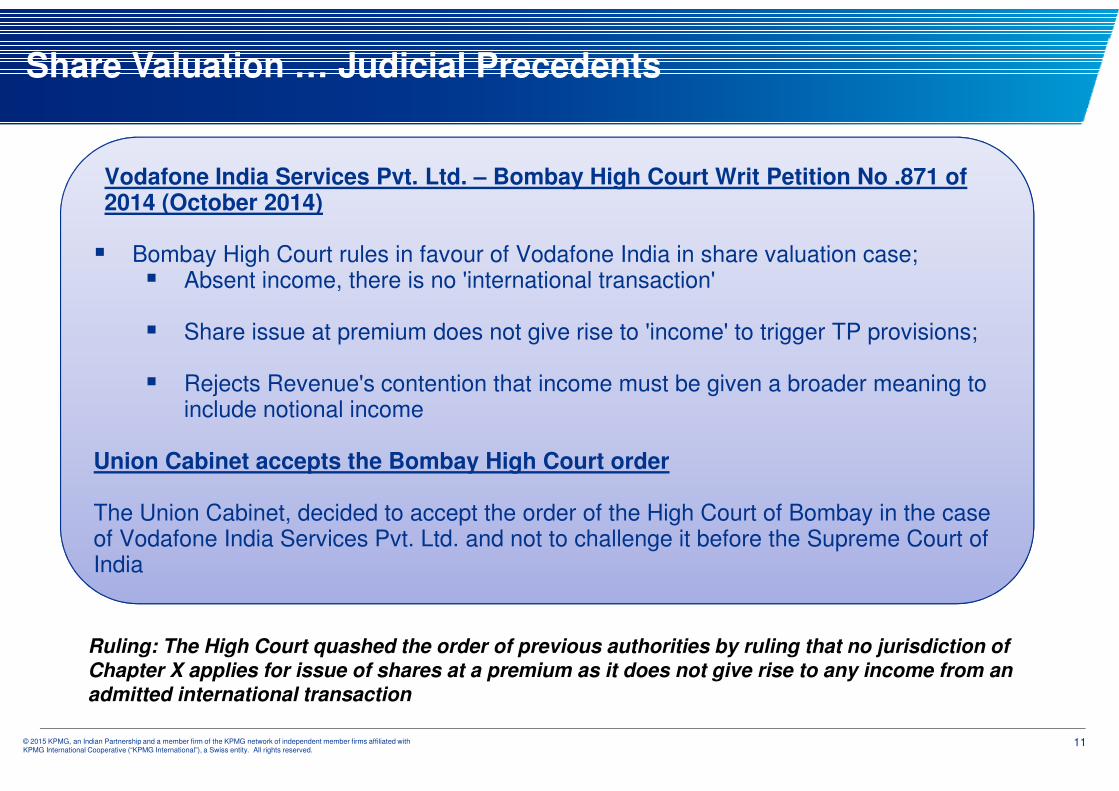

Share Valuation … Judicial Precedents

Vodafone India Services Pvt. Ltd. – Bombay High Court Writ Petition No .871 of 2014 (October 2014)

� Bombay High Court rules in favour of Vodafone India in share valuation case; � Absent income, there is no 'international transaction'

� Share issue at premium does not give rise to 'income' to trigger TP provisions;

� Rejects Revenue's contention that income must be given a broader meaning to include notional income

Union Cabinet accepts the Bombay High Court order

The Union Cabinet, decided to accept the order of the High Court of Bombay in the case of Vodafone India Services Pvt. Ltd. and not to challenge it before the Supreme Court of India

Ruling: The High Court quashed the order of previous authorities by ruling that no jurisdiction of Chapter X applies for issue of shares at a premium as it does not give rise to any income from an admitted international transaction

12© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

BPO vs. KPO

13© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

BPO vs. KPO

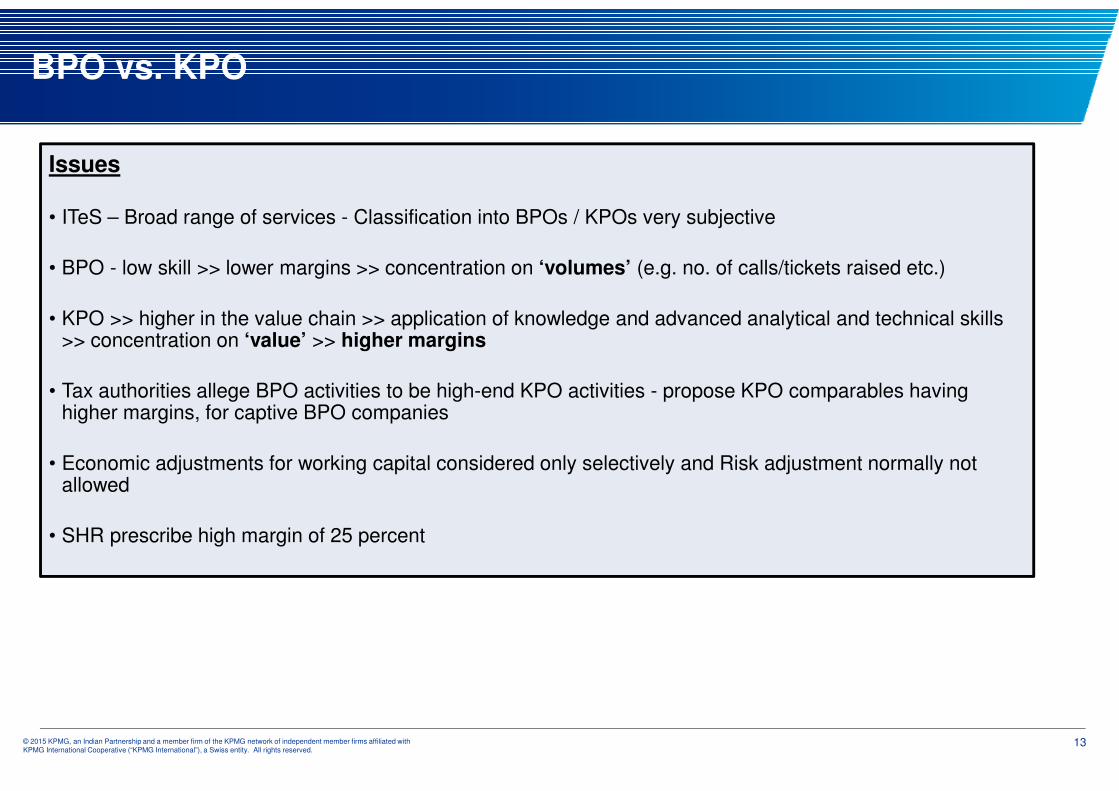

Issues

• ITeS – Broad range of services - Classification into BPOs / KPOs very subjective

• BPO - low skill >> lower margins >> concentration on ‘volumes’ (e.g. no. of calls/tickets raised etc.)

• KPO >> higher in the value chain >> application of knowledge and advanced analytical and technical skills >> concentration on ‘value’ >> higher margins

• Tax authorities allege BPO activities to be high-end KPO activities - propose KPO comparables having higher margins, for captive BPO companies

• Economic adjustments for working capital considered only selectively and Risk adjustment normally not allowed

• SHR prescribe high margin of 25 percent

14© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

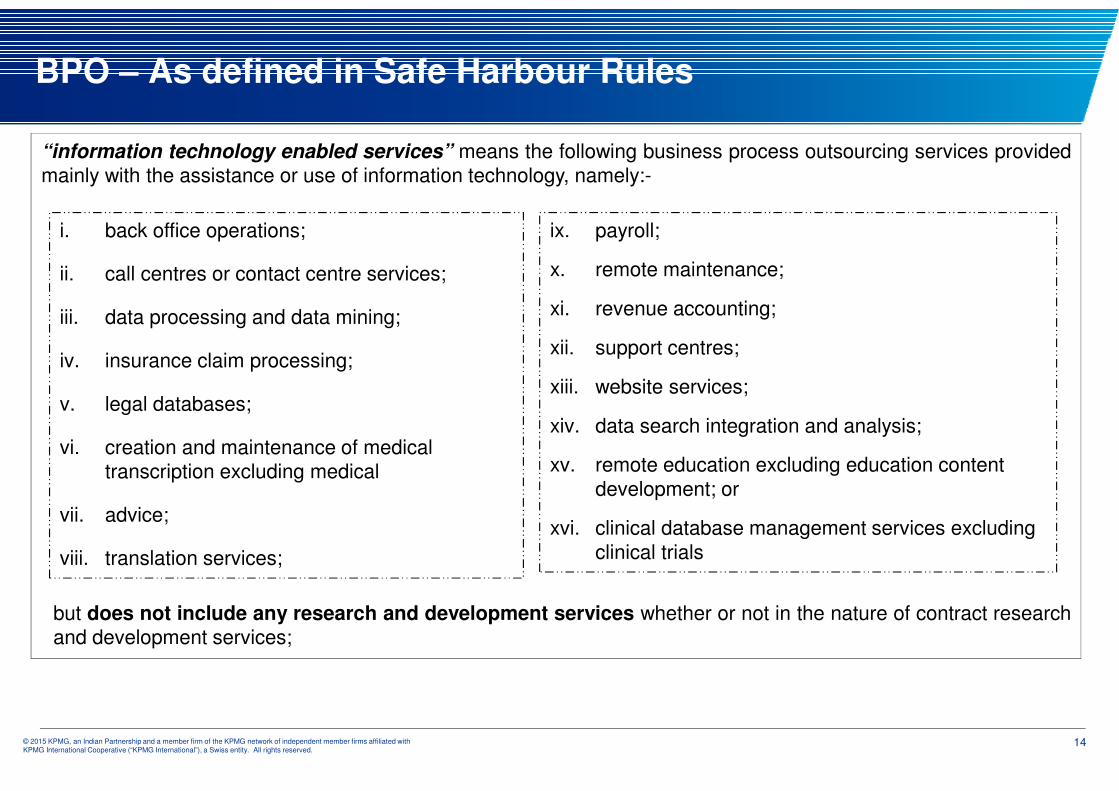

BPO – As defined in Safe Harbour Rules

“information technology enabled services” means the following business process outsourcing services providedmainly with the assistance or use of information technology, namely:-

but does not include any research and development services whether or not in the nature of contract researchand development services;

i. back office operations;

ii. call centres or contact centre services;

iii. data processing and data mining;

iv. insurance claim processing;

v. legal databases;

vi. creation and maintenance of medical transcription excluding medical

vii. advice;

viii. translation services;

ix. payroll;

x. remote maintenance;

xi. revenue accounting;

xii. support centres;

xiii. website services;

xiv. data search integration and analysis;

xv. remote education excluding education content

development; or

xvi. clinical database management services excluding

clinical trials

15© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

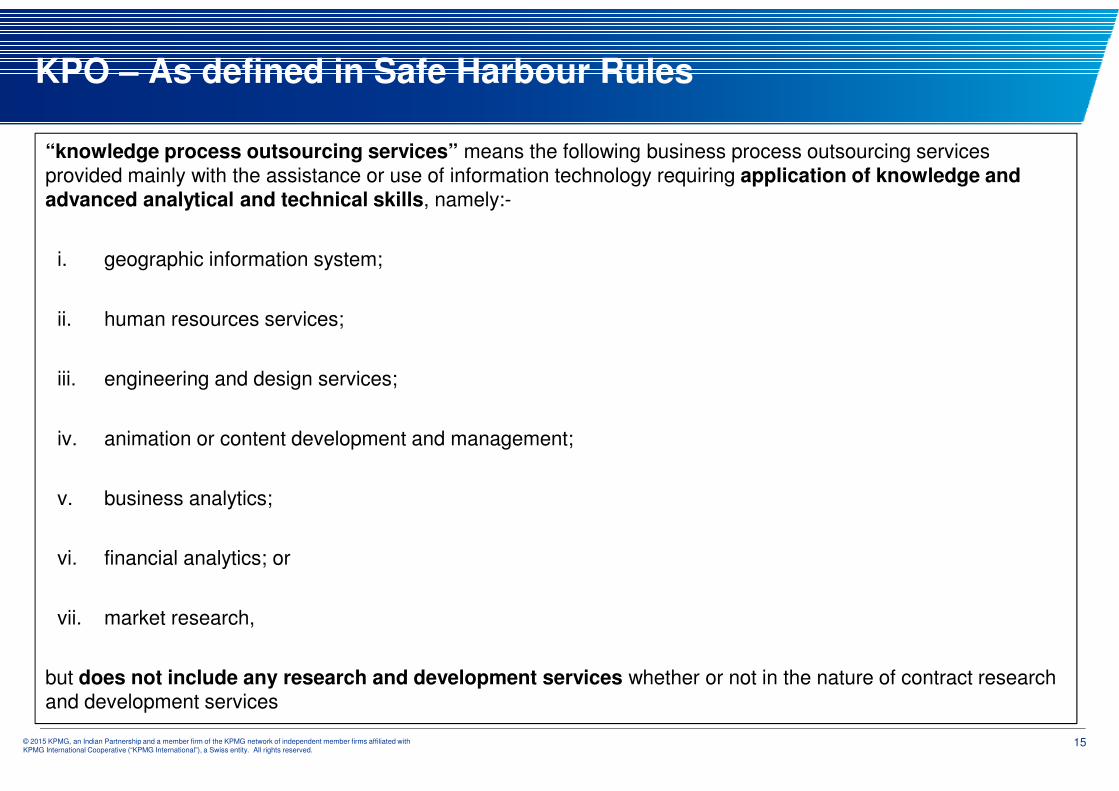

“knowledge process outsourcing services” means the following business process outsourcing services provided mainly with the assistance or use of information technology requiring application of knowledge and advanced analytical and technical skills, namely:-

i. geographic information system;

ii. human resources services;

iii. engineering and design services;

iv. animation or content development and management;

v. business analytics;

vi. financial analytics; or

vii. market research,

but does not include any research and development services whether or not in the nature of contract research and development services

KPO – As defined in Safe Harbour Rules

16© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Safe Harbour Rules (SHR) are effective from 18 Sep 2013:

• Different safe harbours (OP/OE) have been prescribed for KPO / IT-ITeS services

BPO vs. KPO – Safe Harbour Rules

Eligible International Transaction Safe Harbour ratios

ITeS, with insignificant risks OP/OE

o > 20 percent, if aggregate value of transactions < INR 500 crores

o > 22 percent, if aggregate value of such transactions > INR 500 crores

KPO services, with insignificant risks OP/OE > 25 percent

17© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Contract R&D v/s Entrepreneurial R&D

18© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Issue

Indian captive R&D service centres of MNEs typically remunerated on – Cost+ X%, or Hourly/ Man-day basis

Revenue‘s Allegations

Valuable & Unique IP generating work

undertaken in India

India R&D Centre becomes Economic

Owner of IP

IP transferred without adequate

compensation

Global Profits of MNE allocated to India on ratios such as R&D Head Count, etc

High mark up comparables selected by TPO without carrying out appropriate FAR as to whether Indian service provider does

actual R&D activities leading to development of unique IP or only acts as routine service provider

Prone to high litigation due to lack of clarity / subjective interpretation

19© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Favo

ura

ble

An

aly

sis

Unfavourable Analysis

R&D Activities in

India

Guidelines for identifying the

characterization

of R&D Centre

Foreign Entity

Performs Economically Significant Functions

Economically significant functions’ to include critical functions such as

conceptualization and design of the product and providing strategic direction and

framework

Provides funds/ capitalSignificant assets & intangibles

Strategic decisions for Core Functions & Monitoring on regular

basis

Economically Significant Risks

Legal & economic owner of resultant IP

Indian Entity

Performs work assigned by foreign entity

Receives remuneration for the services

performed

Operates under direct supervision and actual

control

No Economically Significant realised Risks

No ownership of resultant IP

Parameters

Funding/ Assets

Risk Profile

Outcome of Research

Functions

Supervision & Control

Entrepreneurial R&DContract R&D Cost Sharing Arrangements of R&D

Contract Research

Services

CBDT Circular – Administrative Guidance

Profit Split Method

(or other approach, if PSM not feasible)

Transactional Net Margin Method

Cost + X%

20© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Safe Harbour Rules – Definitions and Rates

Eligible International Transaction Safe Harbour ratios

Provisions of Software Development Services

OP/OE

o > 20 percent, if aggregate value of transactions < INR 500 crores

o > 22 percent, if aggregate value of such transactions > INR 500 crores

Software Development

� business application software and information system development using known methods and existing software tools

� support for existing systems

� converting or translating computer languages

� adding user functionality to application programmes

� debugging of systems

� adaptation of existing software

� preparation of user documentation

but does not include any R&D services whether or not in the nature of contract R&D services

21© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Safe Harbour Rules – Definitions and Rates

Eligible International Transaction Safe Harbour ratios

Specified contract R&D services, with insignificant risks, wholly or partly relating to software development

OP/OE ≥ 30 percent

Contract R&D services, with insignificant risks, wholly or partly relating to generic pharmaceutical drugs

OP/OE ≥ 29 percent

Contract R&D for Software Development

� R&D producing new theorems and algorithms in the field of theoretical computer science

� development of information technology at the level of operating systems, programming languages, data management, communications software and software development tools

� development of Internet technology

� research into methods of designing, developing, deploying or maintaining software

� software development that produces advances in generic approaches for capturing, transmitting, storing,

retrieving, manipulating or displaying information

� experimental development aimed at filling technology knowledge gaps as necessary to develop a software

programme or system

� R&D on software tools or technologies in specialised areas of computing (image processing, geographic data

presentation, character recognition, artificial intelligence and other areas)

� up-gradation of existing products where source code has been made available by the principal

22© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Location Savings

23© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

� What is Location Rent ?

� Incremental profit derived from LSA

� In highly competitive market, the competitors have access to the same LSA and therefore most of the benefits may pass on to consumers

� Accordingly, in a competitive market, the location rent may or may not ultimately exist even in presence of LSA

Location Specific Advantages and Location Rent

Existence and importance of other location-specific characteristics relevant to a particular location that may lead to some advantage for the firm

Location Specific Advantages (‘LSA’) Location Specific Disadvantages (‘LSDA’)

� Access and proximity to growing local / regional market;

� Large Customer Base with a higher spending capacity

� Market Premium;

� Advanced Infrastructure� Highly specialised local knowledge and

personnel

� Termination cost for the existing operations � Higher transportation cost if the new operation

is more distant from the market� Training costs of local employees

Location Savings = LSA - LSDA

What is Location Specific Advantages (LSA) ?

24© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Facts of the case

� Remuneration - Total OC plus arm’s length mark-up� MAM – TNMM� Approach and comparables accepted by TPO/DRP

� TPO/DRP contention - Location saving (LS) arises as manufacturing activity transferred from US/Europe (high cost) to India (low cost jurisdiction)

� Watson India ought to receive extra compensation on account of LS over and above the margins earned by the comparables

� LS - computed based on articles appearing in journal and websites

� Ad-hoc allocation of LS equally between both the entities

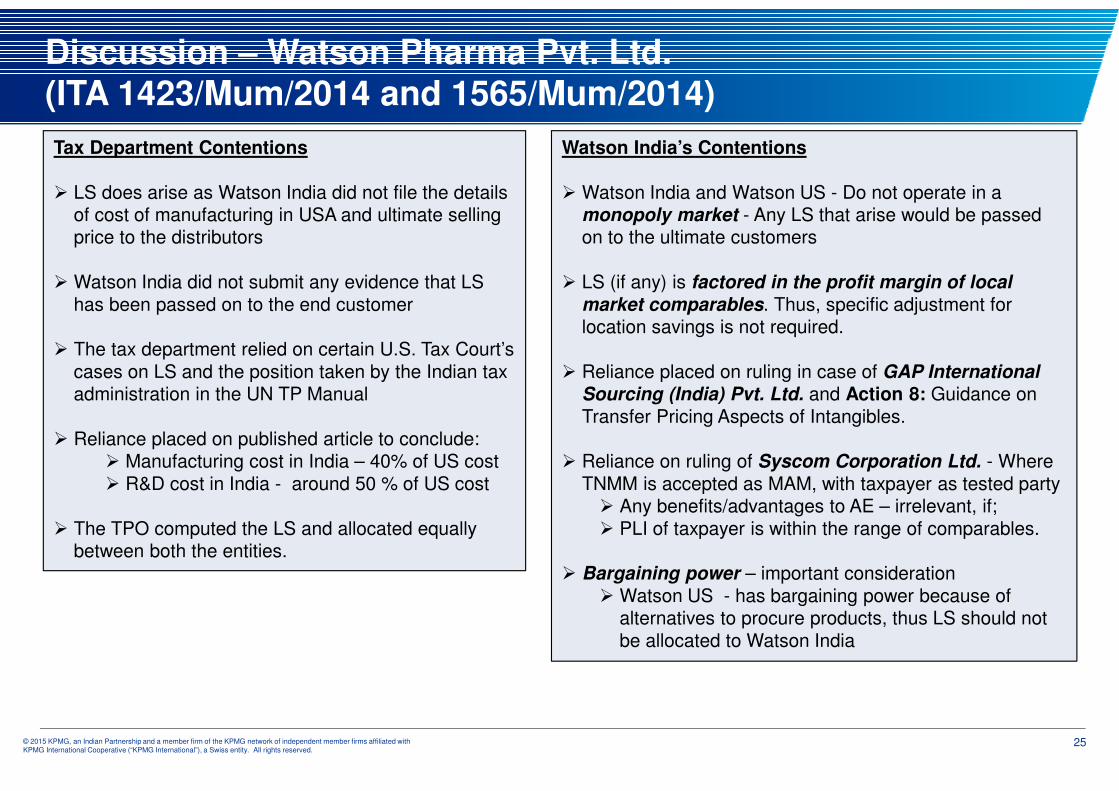

Discussion – Watson Pharma Pvt. Ltd. (ITA 1423/Mum/2014 and 1565/Mum/2014)

Watson Laboratories Inc. – Watson US

Watson Pharma Pvt. Ltd. – Watson India

Watson US

Watson India

Wholly

owned sub

India

US

Cont. mfg &

Cont R&D

25© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tax Department Contentions

� LS does arise as Watson India did not file the details of cost of manufacturing in USA and ultimate selling price to the distributors

� Watson India did not submit any evidence that LS

has been passed on to the end customer

� The tax department relied on certain U.S. Tax Court’s

cases on LS and the position taken by the Indian tax administration in the UN TP Manual

� Reliance placed on published article to conclude:� Manufacturing cost in India – 40% of US cost

� R&D cost in India - around 50 % of US cost

� The TPO computed the LS and allocated equally between both the entities.

Watson India’s Contentions

� Watson India and Watson US - Do not operate in a monopoly market - Any LS that arise would be passed on to the ultimate customers

� LS (if any) is factored in the profit margin of local

market comparables. Thus, specific adjustment for location savings is not required.

� Reliance placed on ruling in case of GAP International Sourcing (India) Pvt. Ltd. and Action 8: Guidance on

Transfer Pricing Aspects of Intangibles.

� Reliance on ruling of Syscom Corporation Ltd. - Where

TNMM is accepted as MAM, with taxpayer as tested party � Any benefits/advantages to AE – irrelevant, if;

� PLI of taxpayer is within the range of comparables.

� Bargaining power – important consideration

� Watson US - has bargaining power because of alternatives to procure products, thus LS should not

be allocated to Watson India

Discussion – Watson Pharma Pvt. Ltd. (ITA 1423/Mum/2014 and 1565/Mum/2014)

26© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Tribunal Ruling

� Both the entities operate in competitive market and Watson India does not have exclusive access to the factors that may result in LSA.

� Rejected TPO reliance on UN TP Manual stating that Chapter 10 of UN TP Manual is the view of the Indian tax administration as the same is not binding on Appellate Authorities.

� Accepted reliance placed on Action 8: Guidance on Transfer Pricing Aspects of Intangibles which states that LS adjustment is not required where local market comparables are available. Further it also accepted

Watson India reliance on GAP International Sourcing (India) Pvt. Ltd

� As regards non-submission of details, Tribunal relied on Special Bench ruling of UCB India (P) Ltd. wherein it was held that with respect to requirements of Rule 10D(1)(f), ‘the maintenance of these records is procedural and non-maintenance of the same is not such that it would affect the determination of ALP…’

� The Tribunal deleted the adjustment made on account of LS by stating that TPO has based his computation on a method, which is not ascribed by the provisions of the Act. Further, the calculation of location saving made by the TPO is based on assumptions since it is based on articles published in different year as compared to year under consideration

“No adjustment on account of Location Savings is required when arm’s length price is determined on the basis of appropriate comparables”

Discussion – Watson Pharma Pvt. Ltd. (ITA 1423/Mum/2014 and 1565/Mum/2014)

27© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

TP Dispute Resolution Mechanism -Developments in APA and MAP

28© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

TP Dispute Resolution Mechanisms

Advance Pricing Agreement

Mutual Agreement Procedure

Mechanisms

29© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transfer Pricing - Winds of change !! … contd.

Source: Economic Times newspaper publication dated 21 May 2015

Govt. aims to sign 120 APAs by FY 15-16. 10 could be with US based middle ranked IT/ITES

cos. Bigger cos. like Google and Dell will come up later

APA officials reported to have sent their research papers on each of the 120 cases

stated above

Each position paper is a document of about 100 pages providing details about the dispute

and possible solutions

30© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

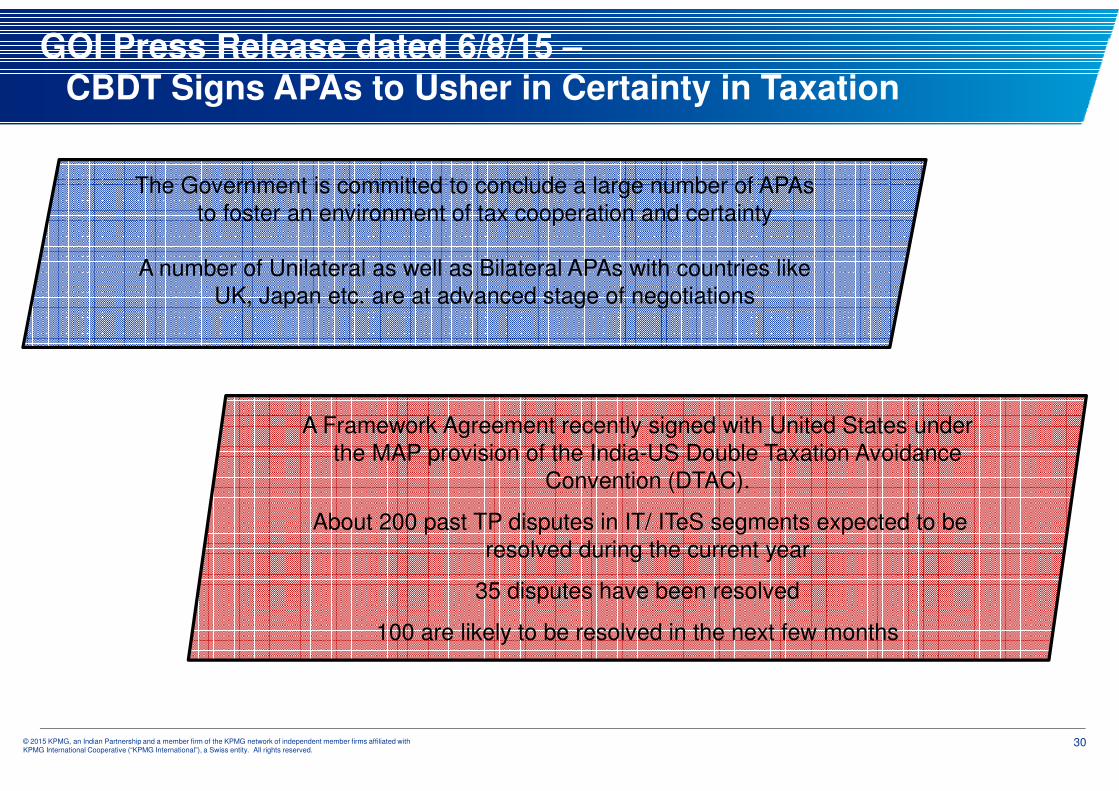

GOI Press Release dated 6/8/15 –CBDT Signs APAs to Usher in Certainty in Taxation

The Government is committed to conclude a large number of APAs

to foster an environment of tax cooperation and certainty

A number of Unilateral as well as Bilateral APAs with countries like

UK, Japan etc. are at advanced stage of negotiations

A Framework Agreement recently signed with United States under

the MAP provision of the India-US Double Taxation Avoidance

Convention (DTAC).

About 200 past TP disputes in IT/ ITeS segments expected to be

resolved during the current year

35 disputes have been resolved

100 are likely to be resolved in the next few months

31© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Advance Pricing Agreement (‘APA’)

32© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

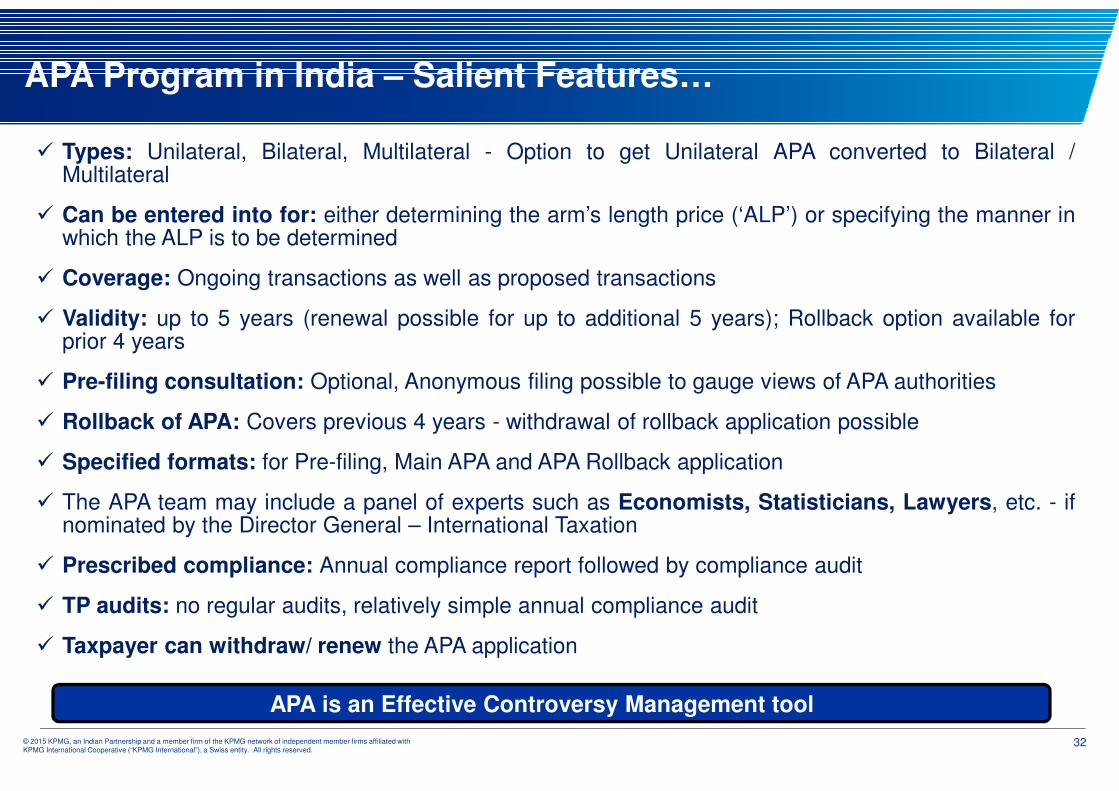

APA Program in India – Salient Features…

� Types: Unilateral, Bilateral, Multilateral - Option to get Unilateral APA converted to Bilateral /Multilateral

� Can be entered into for: either determining the arm’s length price (‘ALP’) or specifying the manner inwhich the ALP is to be determined

� Coverage: Ongoing transactions as well as proposed transactions

� Validity: up to 5 years (renewal possible for up to additional 5 years); Rollback option available forprior 4 years

� Pre-filing consultation: Optional, Anonymous filing possible to gauge views of APA authorities

� Rollback of APA: Covers previous 4 years - withdrawal of rollback application possible

� Specified formats: for Pre-filing, Main APA and APA Rollback application

� The APA team may include a panel of experts such as Economists, Statisticians, Lawyers, etc. - ifnominated by the Director General – International Taxation

� Prescribed compliance: Annual compliance report followed by compliance audit

� TP audits: no regular audits, relatively simple annual compliance audit

� Taxpayer can withdraw/ renew the APA application

APA is an Effective Controversy Management tool

33© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Approach of APA authorities

� Pragmatic and fact-cognizant approach; cordial and non-intrusive

� Focus is on in-depth understanding of the business and the nature of the services rendered byIndian entity in the overall supply chain

� Strong emphasis on establishing and mutually agreeing on detailed analyses to mitigate

subjectivity by field officers

� Flexible and open-minded to fair suggestions regarding the potential practical challenges in

implementation of proposed terms in agreements

� Fair progress on ground also on Bilateral APA discussions

34© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Finance Minister’s proposal to

strengthen the tax administrative set-up for quick disposal of

APAs(ET dated 27.02.15)

� APA is applicable for 5 futureyears and rollback for 4 previous

years.

� “Rollback” - Application ofnegotiated position under an

executed APA to prior years

� Potential effect on prior open

years in litigation.

� Renewal of APA for further 5years

� Reduced documentation burden

Certainty for14 years of

potential TP disputes

APA

(For 5 Future Years)

APA Rollback

(For 4 Previous Open Years)

FY 2015-16

FY 2012-13

FY 2013-14

FY 2014-15

FY 2016-17

FY 2017-18

FY 2018-19

FY 2019-20

Rollback

agreements could

have persuasive

value for prior years

in litigation

Renewal of APA

(For 5 Future Years)

FY 2020-21

APA as an option – Why?

35© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Transfer Pricing – Recent Developments

36© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Key Recent Developments - Areas of discussion

1

2

OECD/G20 BEPS Releases – Final reports on various Action Plans (05 October 2015)

3

Introduction of Range and multiple-year analysis – 2015 - India aligning to international best practices

Guidance on implementation of Transfer Pricing Provisions (Instruction No. 15)

37© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Introduction of Range and multiple-year analysis - 2015India aligning to international best practices(CBDT Notification dated 19 October 2015)

38© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• The OECD advocates the usage of Inter-Quartile Range (“IQR”)

• The IQR is the range from the 25th to the 75th percentile of the results derived from the uncontrolled comparables.

• TP Adjustments usually done to the median

• The concept of IQR has been adopted by majority of the countries having transfer pricing regulations including Austria, Australia, China, Denmark, Finland, France, Germany,

Indonesia, Israel, Italy, Japan, Korea, Mexico, Netherlands, Poland, Portugal, Romania, Singapore, South Africa, Sweden, Taiwan, Thailand, United Kingdom and USA amongst others

Use o

f M

ult

iple

year

data

• The OECD strongly recommends the usage of multiple years’ data for the purposes of comparability analyses. As it provides useful insights in understanding long term arrangements, business and product cycles

• Globally, almost all counties use multiple year data, generally (a) two out of three years; or (b) three out of five years.

• Multiple year data usually used along with the use of multiple year averages to arrive at a reliable Arm’s length range

• Multiple year data is used for comparables while comparing the single year of tested party. Some countries even accept multiple year analysis for both the tested party as well as the comparables.

Global Best PracticesA

rm’s

Len

gth

Ran

ge

39© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Circular No.12 of 2001 dated 23rd August, 2001 stated:

“The Assessing Officer (AO) shall not make any adjustment to the arm’s length price determined by the taxpayer, if such price is up to 5 per cent less or up to 5 per cent more than the price determined by the AO…”

Finance Bill 2002

“With a view to allow a degree of flexibility in adopting an arm’s length price, …………. a price which differs from

the arithmetical mean by an amount not exceeding five per cent of such mean may be taken to be the arm’s length price, at the option of the assessee.”

Finance Act, 2002 More than one price determined by Most appropriate method (MAM) – Arithmetic mean (AM) to

be considered as ALP. Variation of 5% from such AM allowed at the option of the assessee

Variation of 5% allowed from the transfer price (as against erstwhile ALP) (w.e.f. 1 October, 2009)

• Variation of 3% (instead of erstwhile 5%) allowed from the transfer price

• 1% for wholesale traders

Introduction of range concept and use of multiple year data allowed

Arm’s Length Price (ALP) – Changes over the years

Finance Act, 2009

Finance Act, 2012

Finance Act, 2014

(w.e.f. FY 2012-13

onwards)

Multiple year data - Rule 10B(4) envisaged use of data for the relevant financial

year (FY) & two years preceding the relevant FY, subject to certain conditions

40© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

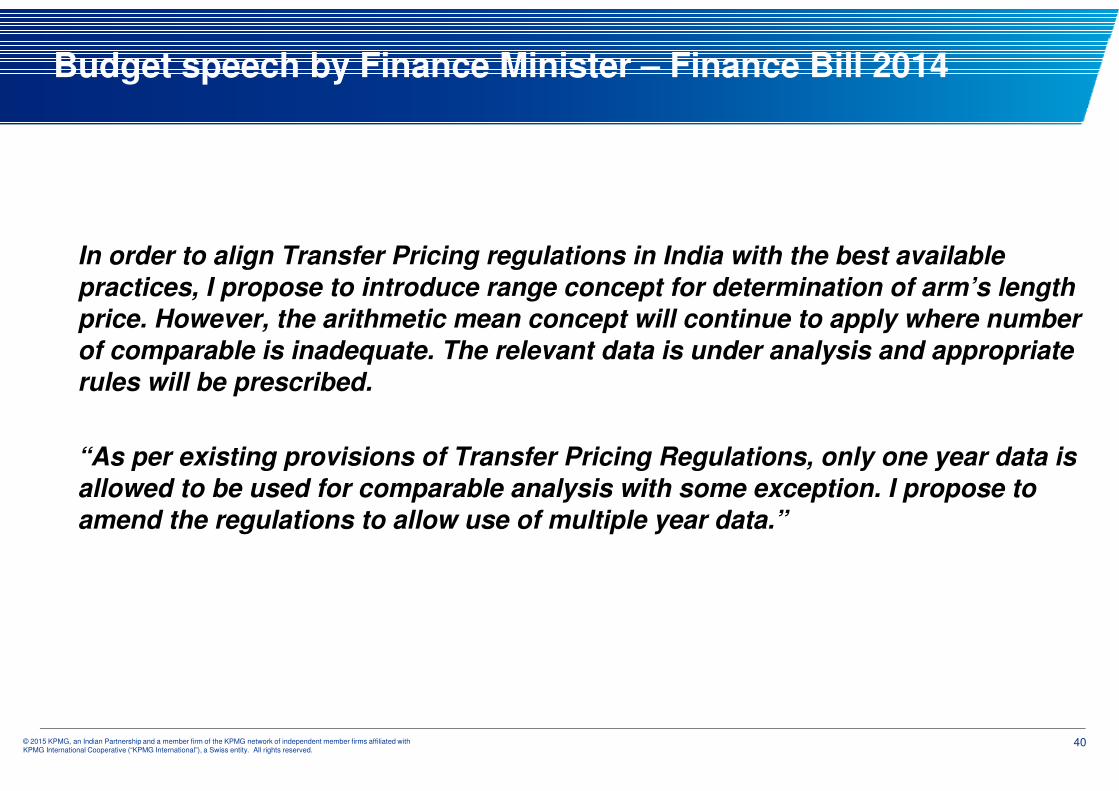

In order to align Transfer Pricing regulations in India with the best available

practices, I propose to introduce range concept for determination of arm’s length

price. However, the arithmetic mean concept will continue to apply where number

of comparable is inadequate. The relevant data is under analysis and appropriate

rules will be prescribed.

“As per existing provisions of Transfer Pricing Regulations, only one year data is

allowed to be used for comparable analysis with some exception. I propose to

amend the regulations to allow use of multiple year data.”

Budget speech by Finance Minister – Finance Bill 2014

41© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• The term ‘financial year’ replaced by the term ‘Current Year’ - to avoid disputes arising from the use of the term ‘financial year’.

• Multiple year data to be used only for those international transactions or Specified Domestic Transactions (SDTs), entered into on or after 1 April 2014.

• Applicable only in case the most appropriate method (MAM) used for determination of ALP is Transactional Net

Margin Method (TNMM), Resale Price Method (RPM) or Cost Plus Method (CPLM)

• Comparability to be conducted based on:

‒ Data relating to the Current Year

‒ Data relating to the financial year immediately preceding the Current Year, if the data relating to the Current Year is not available at the time of furnishing the return of income

• If the Current Year data becomes available, during assessment proceedings, the same to be considered irrespective of the fact that such Current Year data was not available at the time of furnishing of return of income.

Need to rationalize with contemporaneous

data requirements under Rule 10D(4)

Use of Multiple Year data

42© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Multiple year analysis does not apply if MAM used is Comparable Uncontrolled Price Method (CUP), Profit Split

Method (PSM) or ‘Other’ Method

Use of Multiple Year data…contd.

• Enterprises may not be considered as comparables, if they have not undertaken comparable uncontrolled transaction in the Current Year.

‒ even if, such an enterprise had undertaken comparable uncontrolled transaction in either or both of the financial years immediately preceding the Current Year.

43© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

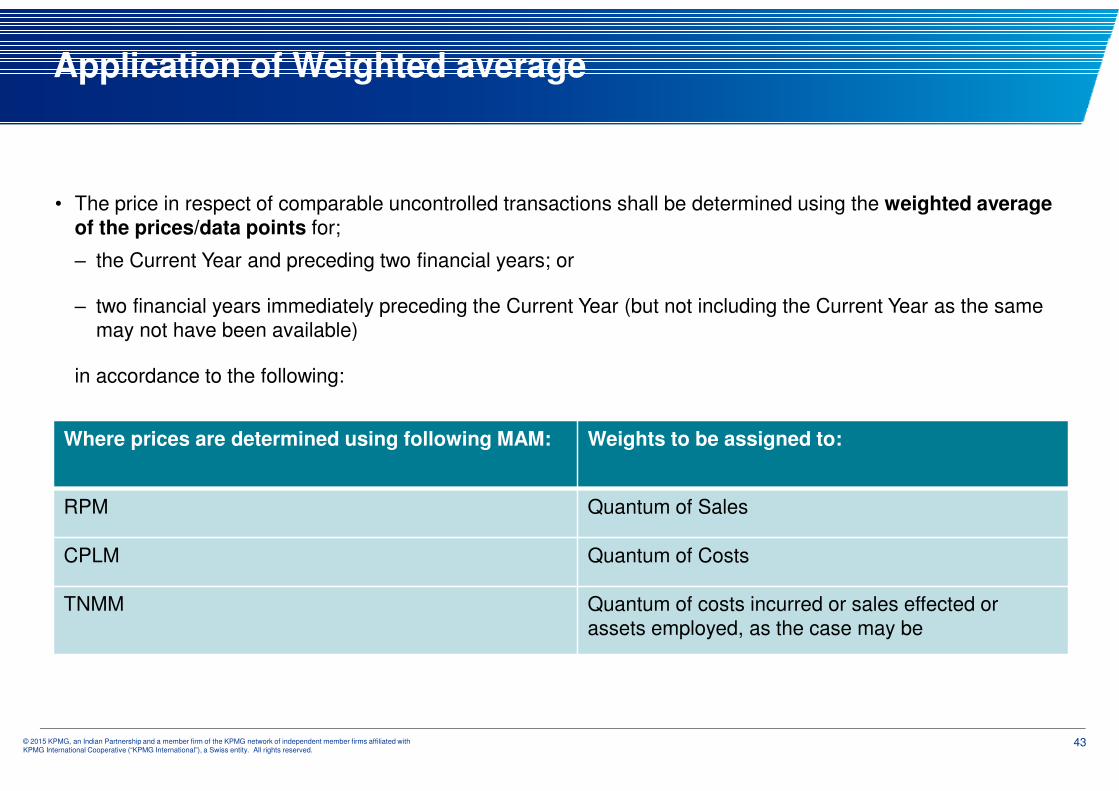

• The price in respect of comparable uncontrolled transactions shall be determined using the weighted average of the prices/data points for;

‒ the Current Year and preceding two financial years; or

‒ two financial years immediately preceding the Current Year (but not including the Current Year as the same may not have been available)

in accordance to the following:

Where prices are determined using following MAM: Weights to be assigned to:

RPM Quantum of Sales

CPLM Quantum of Costs

TNMM Quantum of costs incurred or sales effected or assets employed, as the case may be

Application of Weighted average

44© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

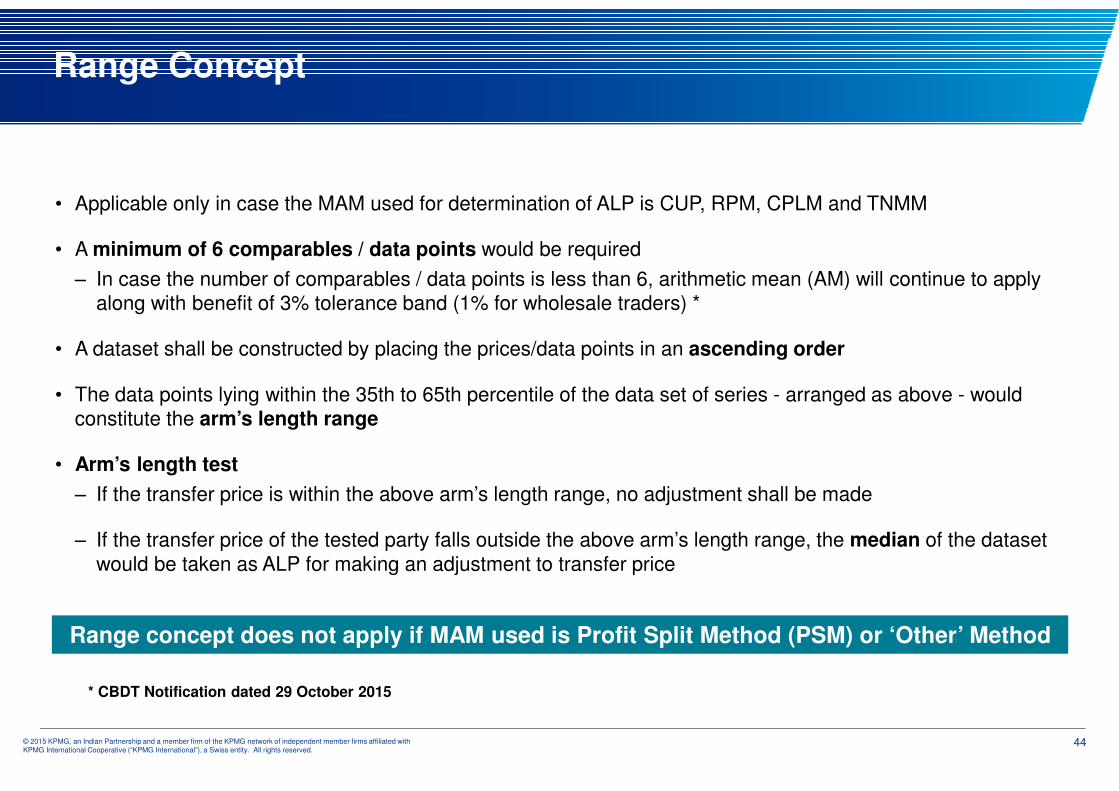

• Applicable only in case the MAM used for determination of ALP is CUP, RPM, CPLM and TNMM

• A minimum of 6 comparables / data points would be required

‒ In case the number of comparables / data points is less than 6, arithmetic mean (AM) will continue to apply along with benefit of 3% tolerance band (1% for wholesale traders) *

• A dataset shall be constructed by placing the prices/data points in an ascending order

• The data points lying within the 35th to 65th percentile of the data set of series - arranged as above - would constitute the arm’s length range

• Arm’s length test

‒ If the transfer price is within the above arm’s length range, no adjustment shall be made

‒ If the transfer price of the tested party falls outside the above arm’s length range, the median of the dataset

would be taken as ALP for making an adjustment to transfer price

Range concept does not apply if MAM used is Profit Split Method (PSM) or ‘Other’ Method

Range Concept

* CBDT Notification dated 29 October 2015

45© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

MethodsApplicability of

Multiple year data Range Concept

CUP � �

CPLM � �

RPM � �

PSM � �

TNMM � �

Other Method � �

Applicability of Range and Multiple year data

46© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Guidance on implementation of Transfer Pricing Provisions (CBDT Instruction No. 15 dated 16 October

2015)

47© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Reference to the Transfer Pricing Officer (TPO)

‒ If there is an income or potentiality of an income arising and/or being affected , the Assessing officer (AO) to record his satisfaction in the following 3 situations before proceeding to determine the ALP or making a reference to the TPO,

o Accountants Report (AR) has not been filed by the taxpayer

o AR has been filed but international transaction(s) has not been reported

o Taxpayer has made qualifying remarks in the AR – regarding impact on income of taxpayer

‒ Quantum on transactions not to be a criteria for referring cases to TPOs – risk parameters to be considered

• Procedural requirements

‒ Taxpayer objection to applicability of TP provisions should be considered and specifically dealt with by the AO, before making a reference to the TPO

‒ AO to provide an opportunity of hearing to the taxpayer

‒ TPO’s - Additional/Joint CIT to be assigned not more than 50 cases

• TPOs to maintain database in prescribed format providing details / information about the assessment outcome e.g. Transfer Price and MAM declared by the taxpayer and determined by the TPO

• The above guidance would be applicable mainly in case of International Transactions and to SDTs till such time separate guidance is issued for SDTs

Key highlights

48© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

OECD/G20 BEPS Releases - Final reports on various Action Plans (05 October 2015)

49© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

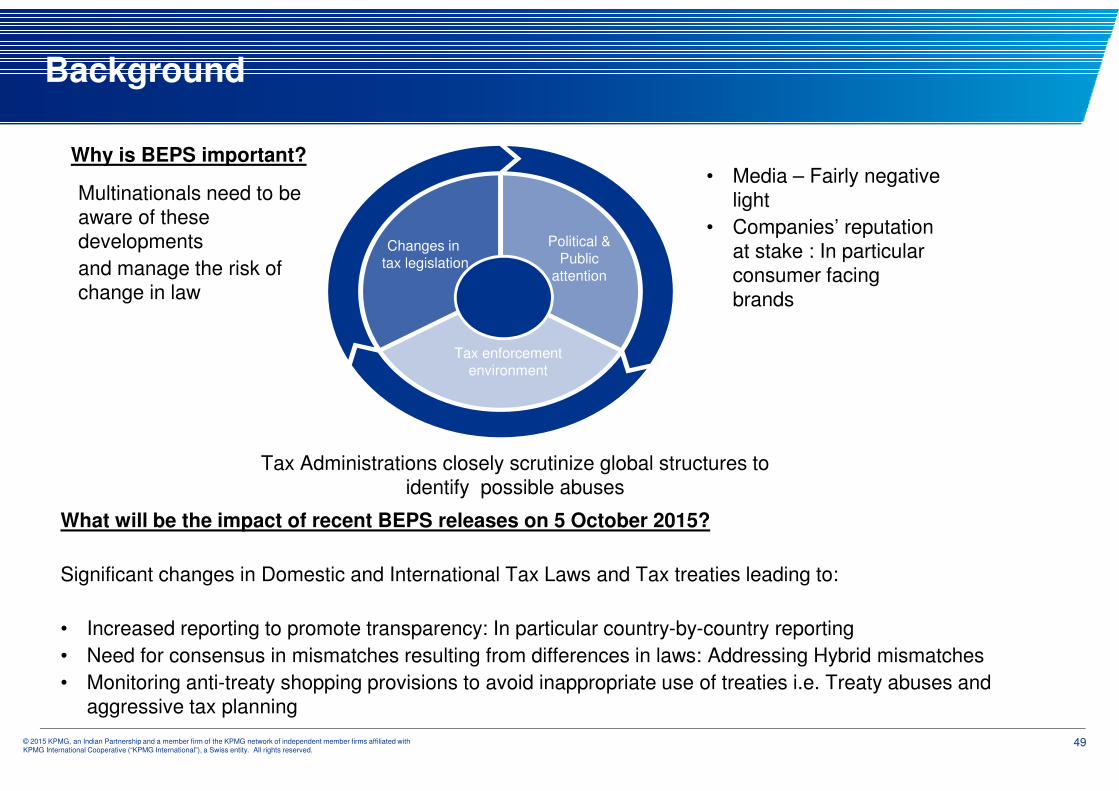

Background

Political &

Public

attention

Changes in

tax legislation

Tax enforcement

environment

• Media – Fairly negative light

• Companies’ reputation at stake : In particular consumer facing

brands

Tax Administrations closely scrutinize global structures to identify possible abuses

Multinationals need to be aware of these developments

and manage the risk of change in law

What will be the impact of recent BEPS releases on 5 October 2015?

Significant changes in Domestic and International Tax Laws and Tax treaties leading to:

• Increased reporting to promote transparency: In particular country-by-country reporting

• Need for consensus in mismatches resulting from differences in laws: Addressing Hybrid mismatches

• Monitoring anti-treaty shopping provisions to avoid inappropriate use of treaties i.e. Treaty abuses and aggressive tax planning

Why is BEPS important?

50© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Key Considerations – India's involvement

• Global revenue losses from BEPS are up to USD 240 billion annually - BEPS proposals expected to address this tax gap.

• India has been an active participant and endorses the BEPS proposals

• Challenges for taxpayers and Indian Revenue authorities (IRA)

o MNCs required to fundamentally rethink their tax strategies and prepare for more disclosure requirements

to align with BEPS proposals, and

o IRA required to create a balance between attracting MNCs to invest and shift business operations to their jurisdiction vis-à-vis the need to prevent erosion of tax base

• IRA to study and analyze BEPS recommendations and likely to make legislative or administrative amendments effective fiscal year beginning April 01, 2016

• Indian Competent Authority stated - Indian Government expects that Indian Corporates should be aware of BEPS and proposed changes that may happen and therefore, ignorance may not be a valid excuse –Grandfathering of previous tax structures may not happen

• On 8 October 2015, G20 Finance Ministers endorsed the final package of BEPS and have forwarded the same to the G20 Heads of State for consideration in their meeting in November 2015

• Development of a multilateral instrument (MLI) is key to amend several DTAA’s and India is supporting the same. Framework for the MLI expected by December 2016

• No retrospective changes will be made in domestic laws with respect to implementation of BEPS Actions

Source1. www.taxsutra.com

2. Nov 2014 Minutes of Tax officers offsite organized by Ministry of Finance and CII

51© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

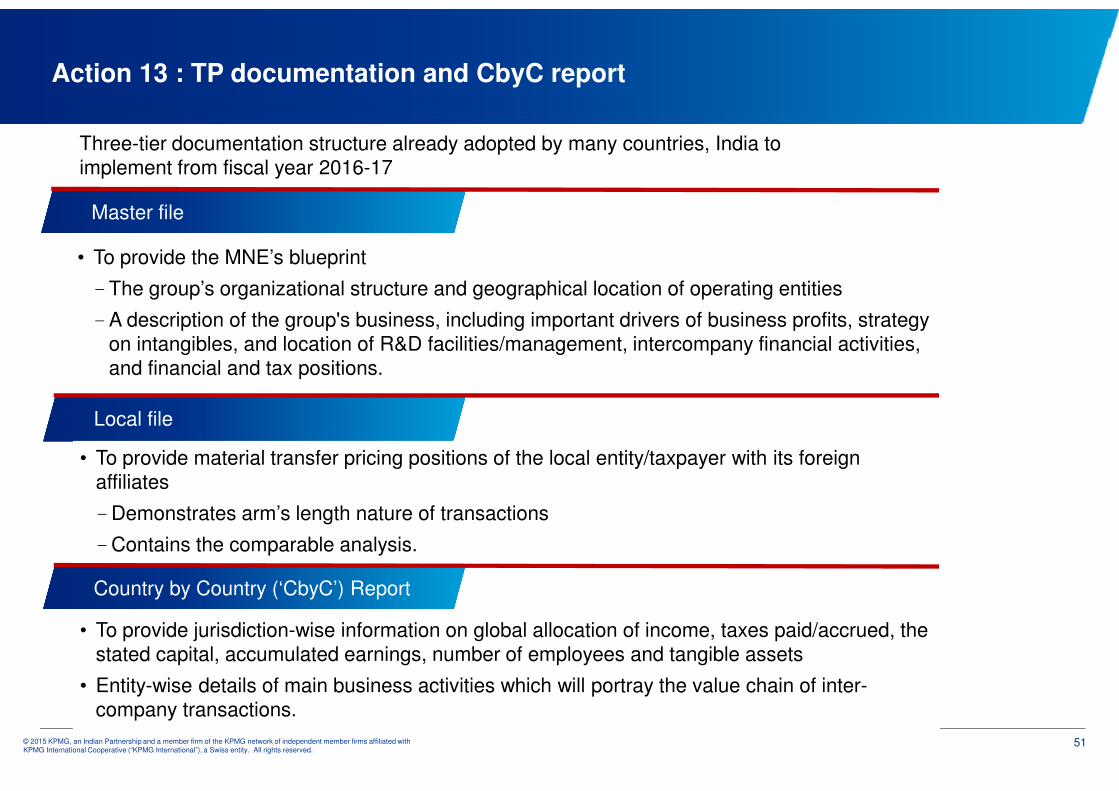

Master file

• To provide the MNE’s blueprint

–The group’s organizational structure and geographical location of operating entities

–A description of the group's business, including important drivers of business profits, strategy on intangibles, and location of R&D facilities/management, intercompany financial activities, and financial and tax positions.

Country by Country (‘CbyC’) Report

• To provide jurisdiction-wise information on global allocation of income, taxes paid/accrued, the stated capital, accumulated earnings, number of employees and tangible assets

• Entity-wise details of main business activities which will portray the value chain of inter-company transactions.

Local file

• To provide material transfer pricing positions of the local entity/taxpayer with its foreign affiliates

–Demonstrates arm’s length nature of transactions

–Contains the comparable analysis.

Three-tier documentation structure already adopted by many countries, India to implement from fiscal year 2016-17

Action 13 : TP documentation and CbyC report

52© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

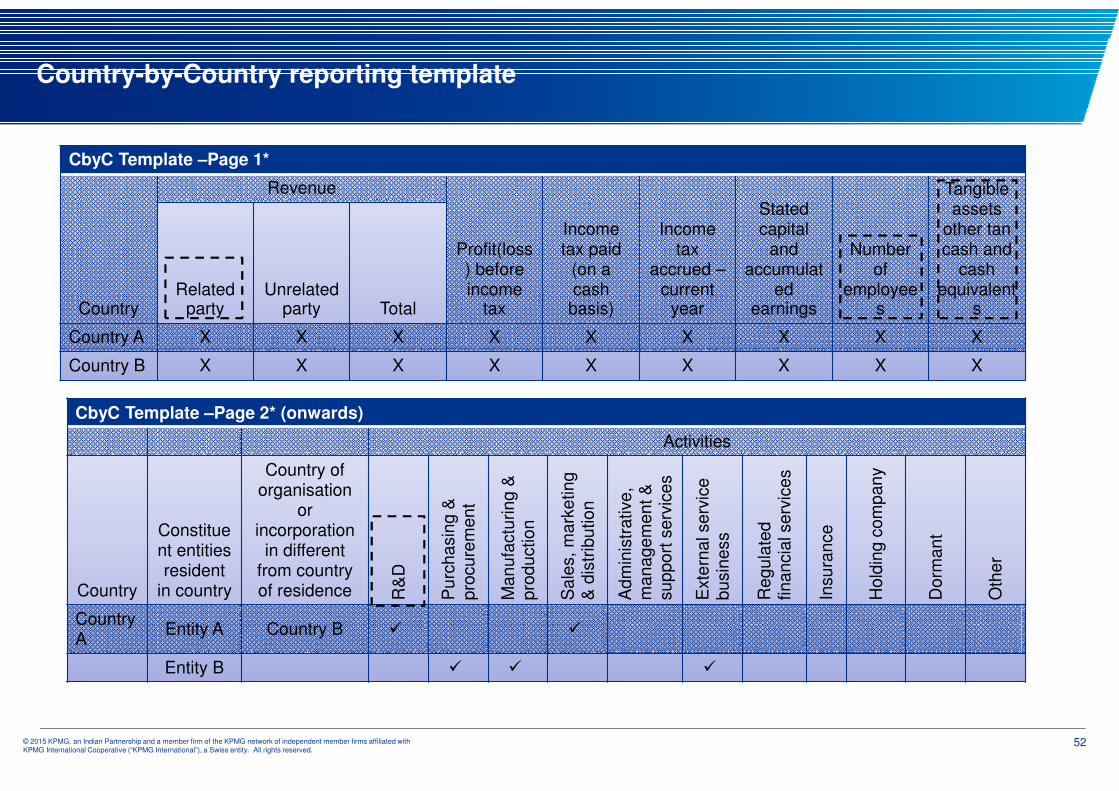

CbyC Template –Page 1*

Country

Revenue

Profit(loss) before income

tax

Income tax paid

(on a cash basis)

Income tax

accrued –current

year

Stated capital

and accumulat

ed earnings

Number of

employees

Tangible assets

other tan cash and

cash equivalent

sRelated

partyUnrelated

party Total

Country A X X X X X X X X X

Country B X X X X X X X X X

CbyC Template –Page 2* (onwards)

Activities

Country

Constituent entities resident

in country

Country of organisation

or incorporation

in different from country of residence R

&D

Purc

hasin

g &

pro

cure

ment

Manufa

ctu

ring &

pro

duction

Sale

s, m

ark

eting

& d

istr

ibution

Adm

inis

trative,

managem

ent &

support

serv

ices

Exte

rnal serv

ice

busin

ess

Regula

ted

financia

l serv

ices

Insura

nce

Hold

ing c

om

pany

Dorm

ant

Oth

er

Country A

Entity A Country B � �

Entity B � � �

Country-by-Country reporting template

53© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Action 13 – India Perspective

India Perspective

• CbyC report - contains summary data by jurisdiction including revenue, income, taxes, and indicators of

economic activity.

- Required to be filed by MNE groups with annual consolidated group revenue of more than €750 million

(approx. INR 5000 crores);

- Effective from MNE’s fiscal year beginning on or after January 1, 2016 in all countries;

- Automatic exchange of information between countries

• Indian MNEs and other MNEs operating in India required to have a TP documentation strategy in place - make

sure that the three elements consistently explain the group’s business model.

• Profits in all jurisdictions to align with operations

• India will seek to introduce the CbyC reporting requirements by fiscal year 2016-17

54© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Action 8 – 10 - Aligning Transfer Pricing Outcomes with Value Creation

Intangibles

• Legal ownership of an intangible does not by itself provide a right to all (or indeed any) of the return generated from its exploitation. Instead those returns accrue to the entities which carry out DEMPE functions -development, enhancement, management, protection and exploitation -in relation to that intangible

Risk Re-characterization & Special Measures

• Emphasis on the need to accurately delineate a transaction so that the actual conduct of parties will replace contractual arrangements. Transactions can be disregarded for TP purposes where they lack commercial

rationality

• Contractual allocations of risk to be respected only when they are supported by actual decision-making i.e. exercising control over these risks coupled with financial capacity to assume such risks

• ‘Cash boxes’ entitled only to risk-free returns to the extent of their capital contributions, if only providing funding without performing significant activities and without having de-facto control on associated risks

Other high risk transactions

• Safe harbour cost plus margin of 5% for low value adding services recommended, with a simplified benefits test.

• In Cost Contribution Arrangements, contributions would be based on value i.e. arm’s length price of the contributions and not the costs.

55© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

• Highly litigated issues – Marketing Intangibles, Intra-group services , Location savings, R&D arrangements

• Concept of Economic ownership vis-à-vis Legal ownership

• Indian Revenue Authorities (IRA) - scrutinizing issues like risk return profile and profit allocations based on

economic activity, locational savings etc. Therefore amendments in line with BEPS recommendations expected

in local tax regulations.

• Subjectivity of issues like characterization and degree of economic activities and resulting allocation of profits

may dampen foreign investments

• Taxpayers to proactively re-evaluate their legal and contractual structures and ensure that they are aligned to

the actual business operations in various jurisdictions.

Action 8 – 10 – India Perspective

Robust FAR analysis and Documentation is the key

56© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Way forward

57© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Way Forward – Taxpayer’s Perspective

Be Proactive – not reactive - Manage Dispute Resolution effectively

Adopt Coordinated and centralized approach.

Involve operational teams in tax and TP planning and documentation process

Holistic solutions – not fragmented responses

Global awareness and vision – not myopic

Harmonize TP documentation with other regulatory requirements

58© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Way Forward : India Changing its Approach

� Objective of the Indian Government / Finance Ministry to reduce Transfer Pricing Litigation

� More focus and pragmatic approach on dispute resolution mechanisms like APA & MAP

� Adopting international best practices like use of multiple years, range concept, other method, etc. for determining arm’s length price

� Judicial precedents on Transfer Pricing building by the day including on vexed issues

like Location Savings, Marketing Intangibles

� The choice of the appropriate / mix of dispute resolution mechanisms - APA / MAP / Litigation – is the key

59© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Glossary

Abbr. Description

KPO Knowledge Process Outsourcing

BPO Business Process Outsourcing

OP Operating Profit

OE Operating Expense

TPO Transfer Pricing officer

ITA Indian Tax Authorities

FAR Functions, Assets and Risk

IT Information Technology

ITES Information Technology Enabled Services

the Act Income Tax Act, 1961

SHR Safe Harbour Rules

TP Transfer Pricing

AE Associated Enterprise

MAP Mutual Agreement Procedure

CBDT Central Board of Direct Taxes

Abbr. Description

R&D Research & Development

OECD Organization for Economic Co-operation and Development

MNE Multinational Enterprise

IP Intellectual Property

DRP Dispute Resolution Panel

MAM Most Appropriate Method

TNMM Transactional Net Margin Method

PLI Profit Level Indicator

APA Advance Pricing Agreement

BEPS Base Erosion and Profit Shifting

60© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Questions & Answers

Questions

&

Answers

61© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with

KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

61

Thank You !

Thank You