risk management using derivatives securities of derivatives are: options –put and call options,...

TRANSCRIPT

1

Risk Management

Using Derivatives

Securities

2

Definition of Derivatives

A derivative is a financial instrument whosevalue is derived from the price of a more basicasset called the underlying asset.

Examples of underlying assets: shares,commodities, currencies, credits, stock marketindices, weather temperatures, results of sportmatches or elections, etc.

Examples of derivatives are: Options – put andcall options, forwards, futures, and swaps

3

Derivative Markets

Derivative markets are markets for contractual instruments whose performance is determined by how another instrument or asset performs

– Cash market or spot market maximum delivery two

working days

– Forward markets related to forward and/or futures

contract

4

The Role of Derivative Markets

1. risk management hedging

Because derivative prices are related to the prices of the underlying spot market goods, they can be used to reduce or increase the risk of investing in the spot items

2. Price discovery

futures and forward markets are an important means of obtaining information about investors’ expectations of future prices

3. Operational advantages

Lower transaction cost, have greater liquidity than spot markets (futures & options), allow investors to sell short more easily

4. Market efficiency

5. Speculation

5

Types of Derivative Securities:

Options Contract

Forward Contract

Futures Contract

Swap

6

Derivatives Securities:OPTIONS CONTRACT

7

Definition of Options

Arrangement or agreement between the

seller and the buyer in which the buyer

has the right to buy (call option) or sell (put

option) an underlying assets at some time

in the future at a price stipulated at

present.

8

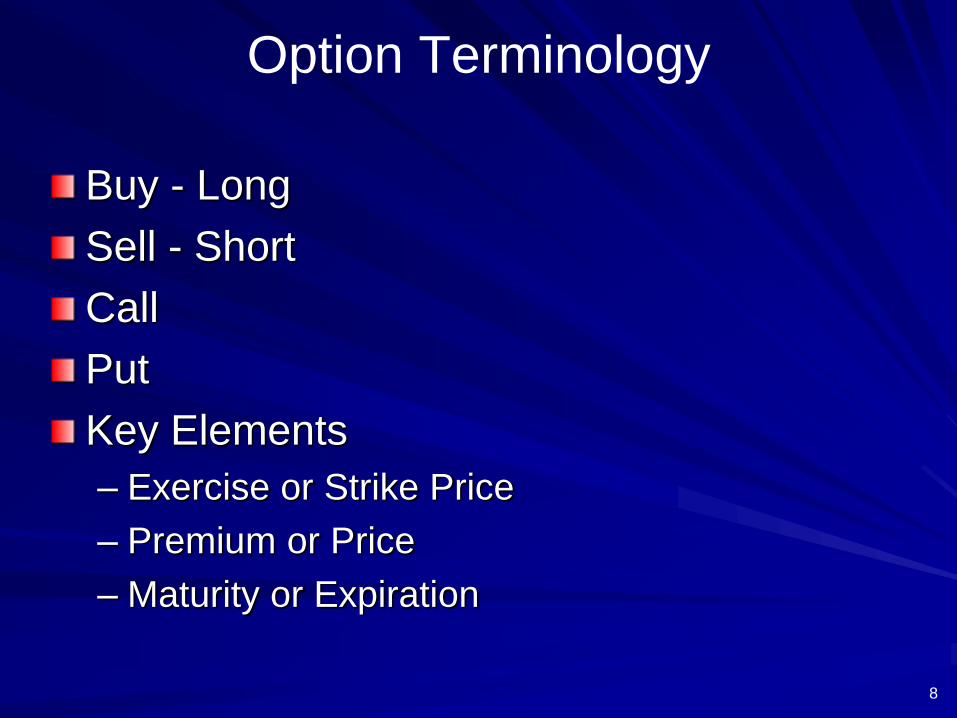

Option Terminology

Buy - Long

Sell - Short

Call

Put

Key Elements

– Exercise or Strike Price

– Premium or Price

– Maturity or Expiration

9

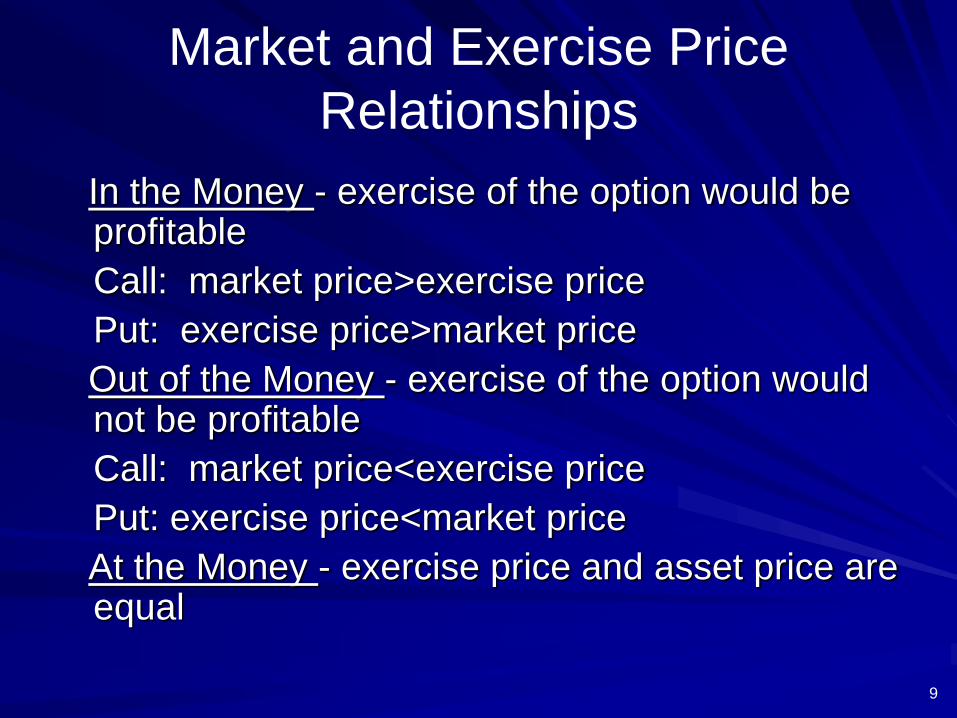

Market and Exercise Price

Relationships

In the Money - exercise of the option would be profitable

Call: market price>exercise price

Put: exercise price>market price

Out of the Money - exercise of the option would not be profitable

Call: market price<exercise price

Put: exercise price<market price

At the Money - exercise price and asset price are equal

10

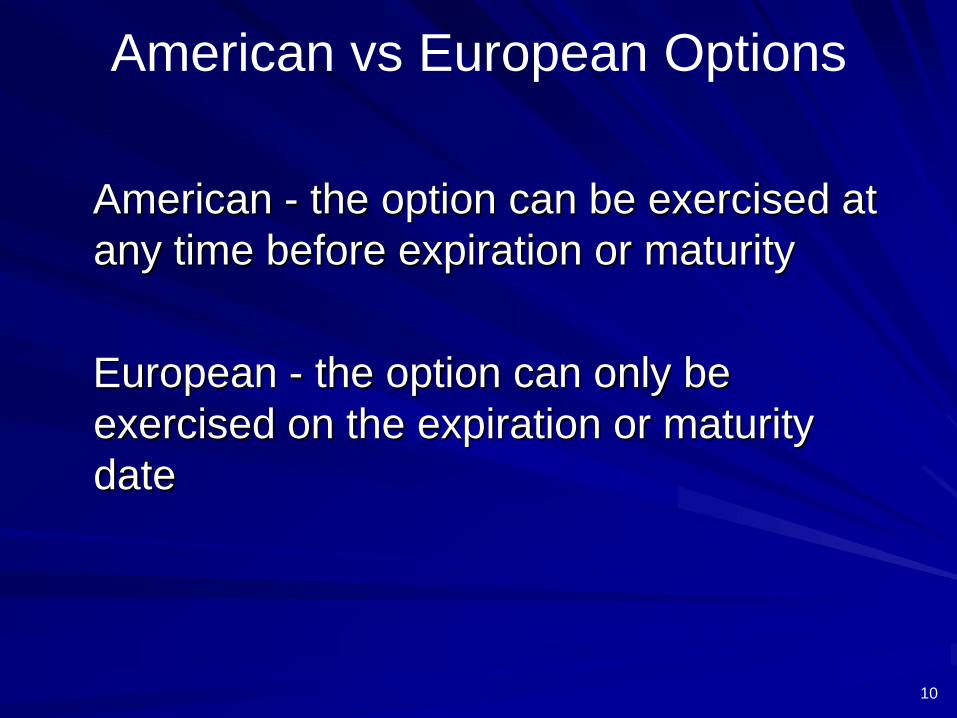

American vs European Options

American - the option can be exercised at

any time before expiration or maturity

European - the option can only be

exercised on the expiration or maturity

date

11

Different Types of Options

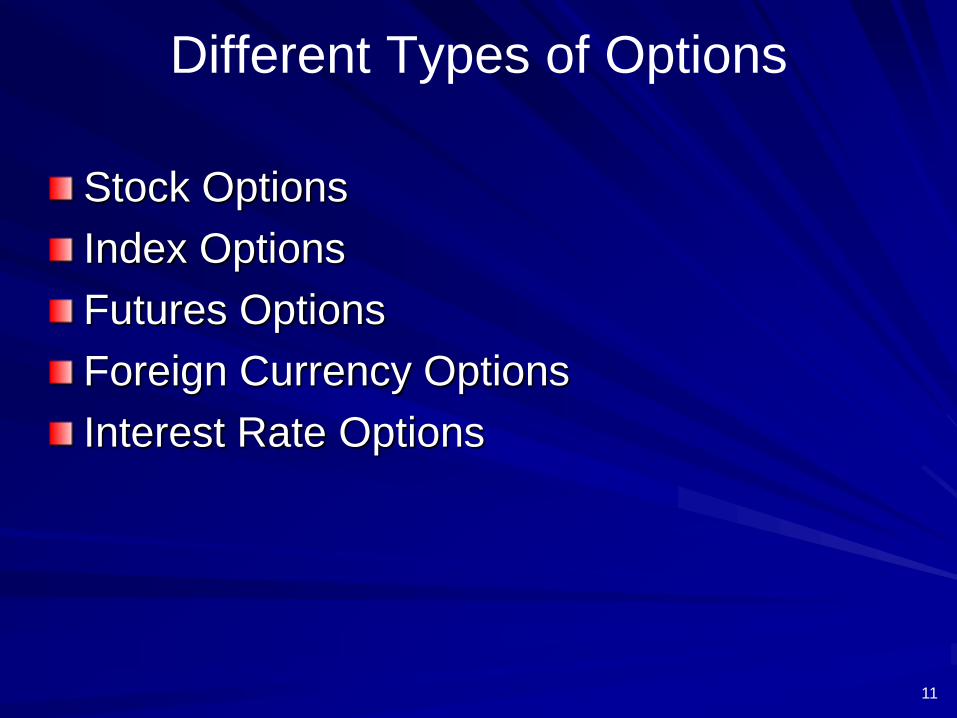

Stock Options

Index Options

Futures Options

Foreign Currency Options

Interest Rate Options

12

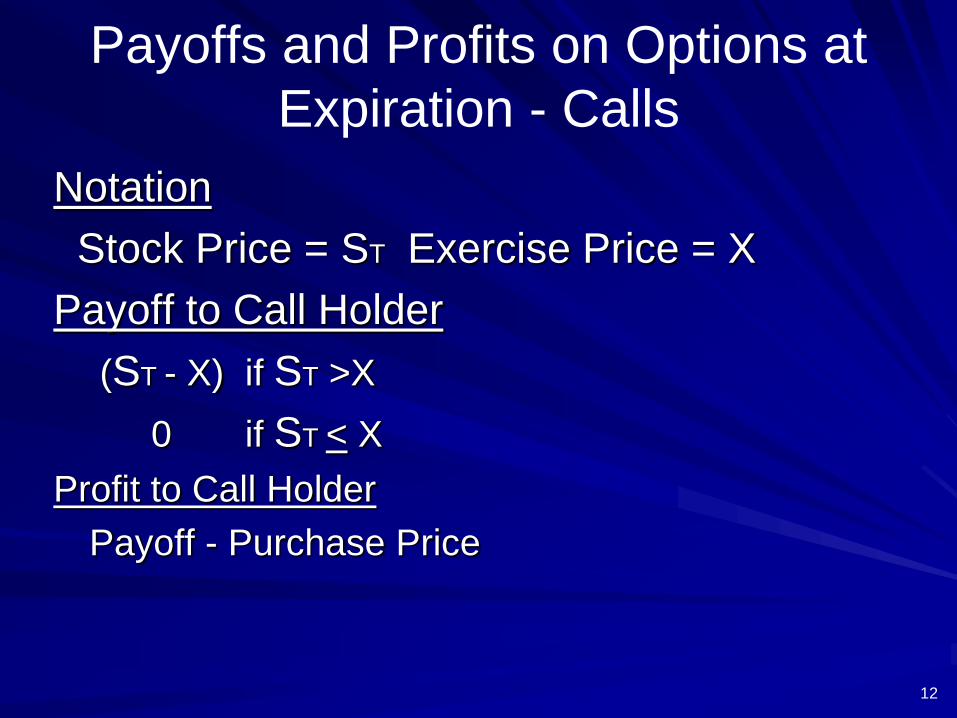

Payoffs and Profits on Options at

Expiration - Calls

Notation

Stock Price = ST Exercise Price = X

Payoff to Call Holder

(ST - X) if ST >X

0 if ST < X

Profit to Call Holder

Payoff - Purchase Price

13

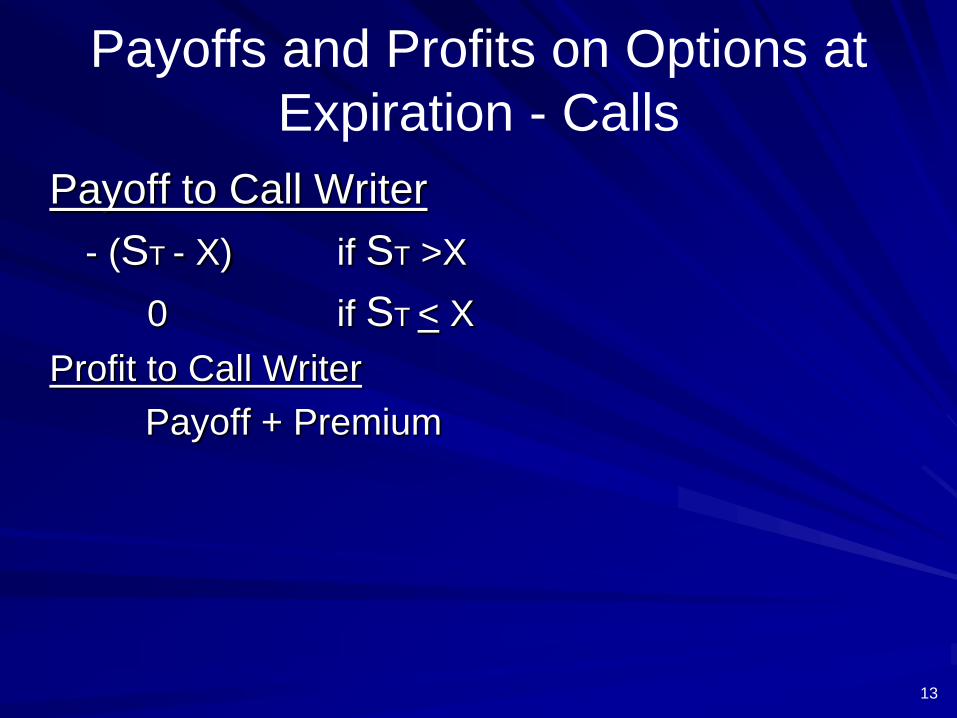

Payoffs and Profits on Options at

Expiration - Calls

Payoff to Call Writer

- (ST - X) if ST >X

0 if ST < X

Profit to Call Writer

Payoff + Premium

14

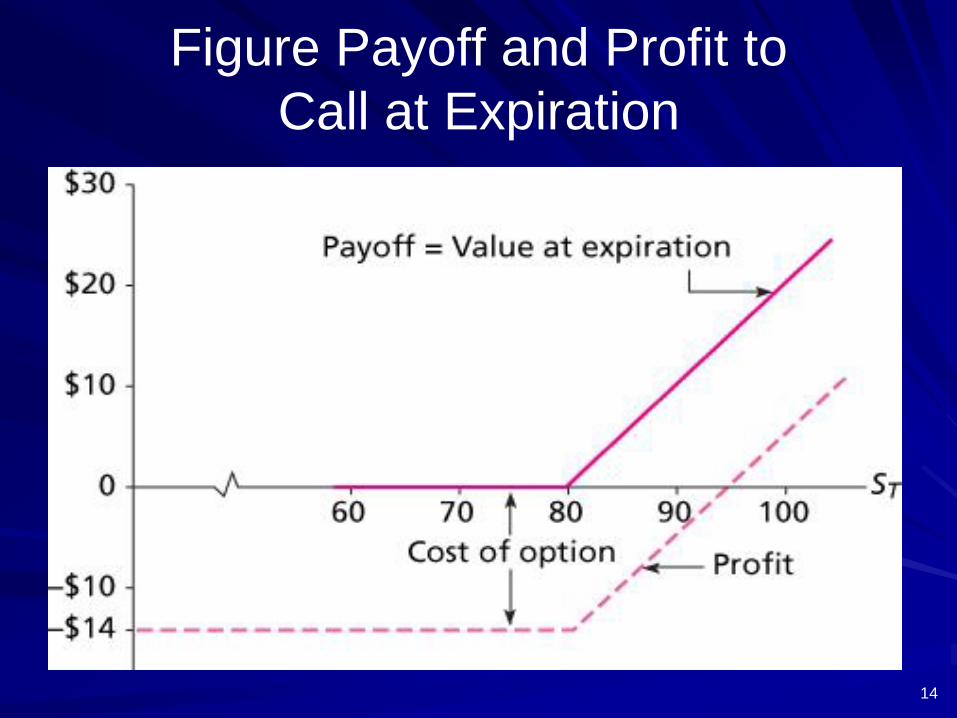

Figure Payoff and Profit to

Call at Expiration

15

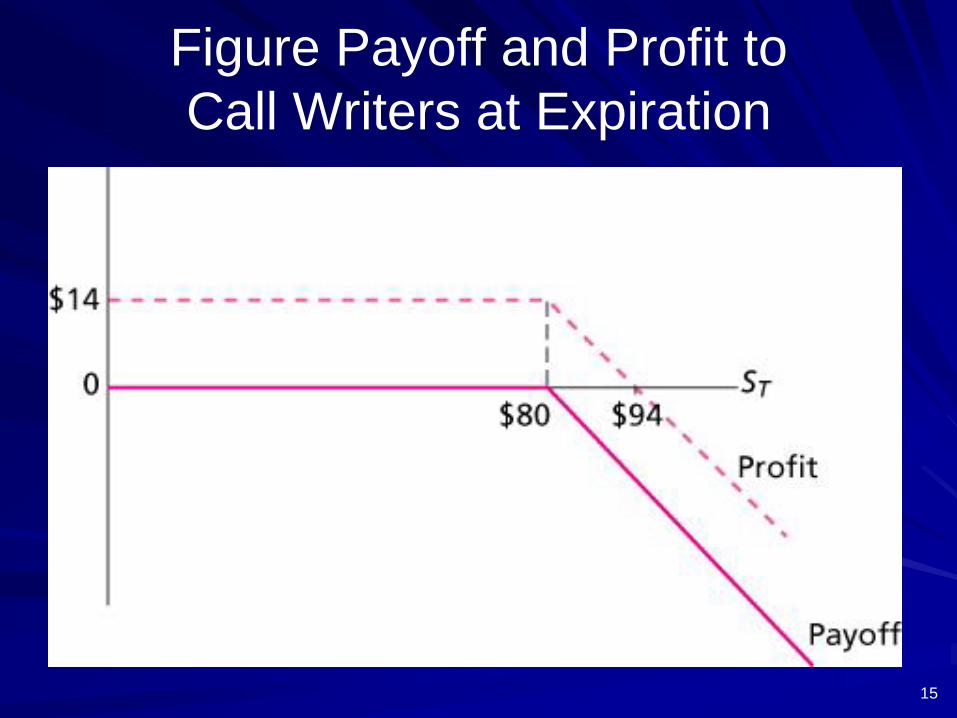

Figure Payoff and Profit to

Call Writers at Expiration

16

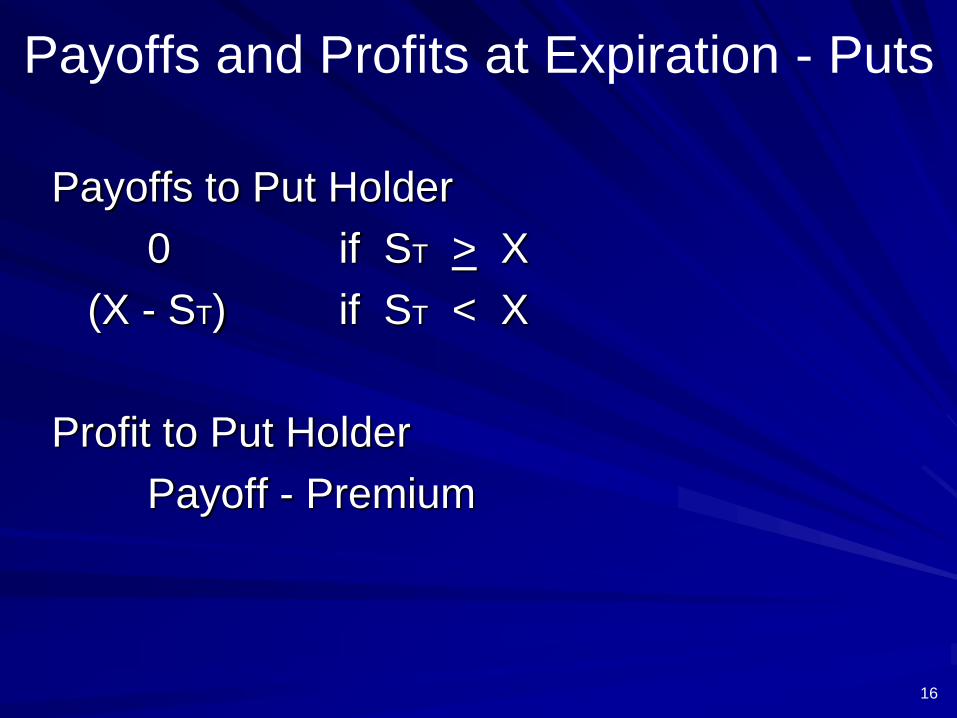

Payoffs and Profits at Expiration - Puts

Payoffs to Put Holder

0 if ST > X

(X - ST) if ST < X

Profit to Put Holder

Payoff - Premium

17

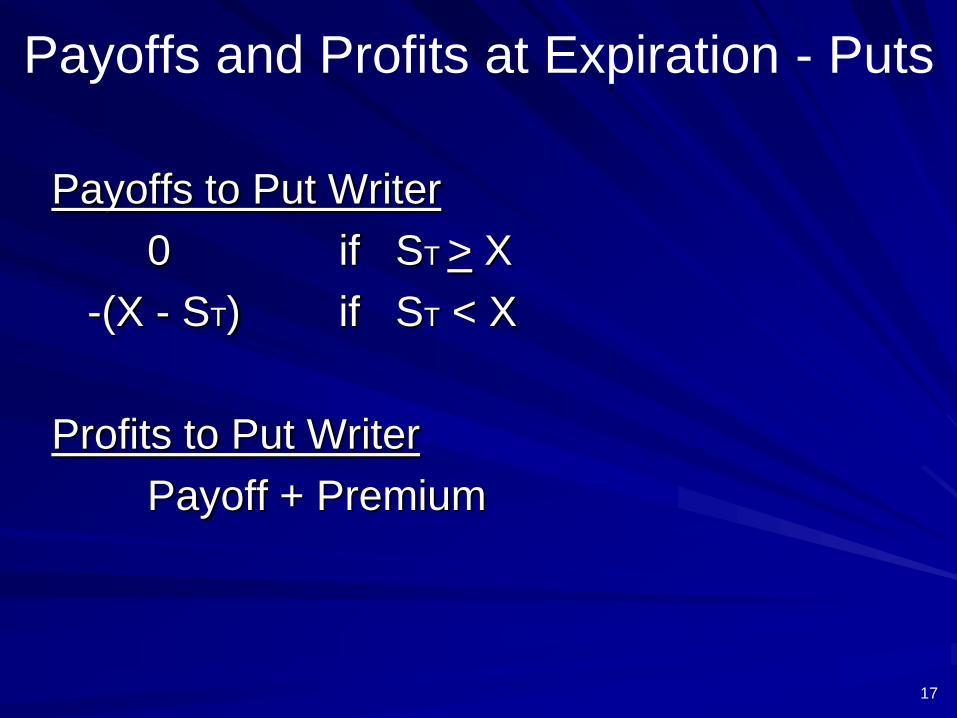

Payoffs and Profits at Expiration - Puts

Payoffs to Put Writer

0 if ST > X

-(X - ST) if ST < X

Profits to Put Writer

Payoff + Premium

18

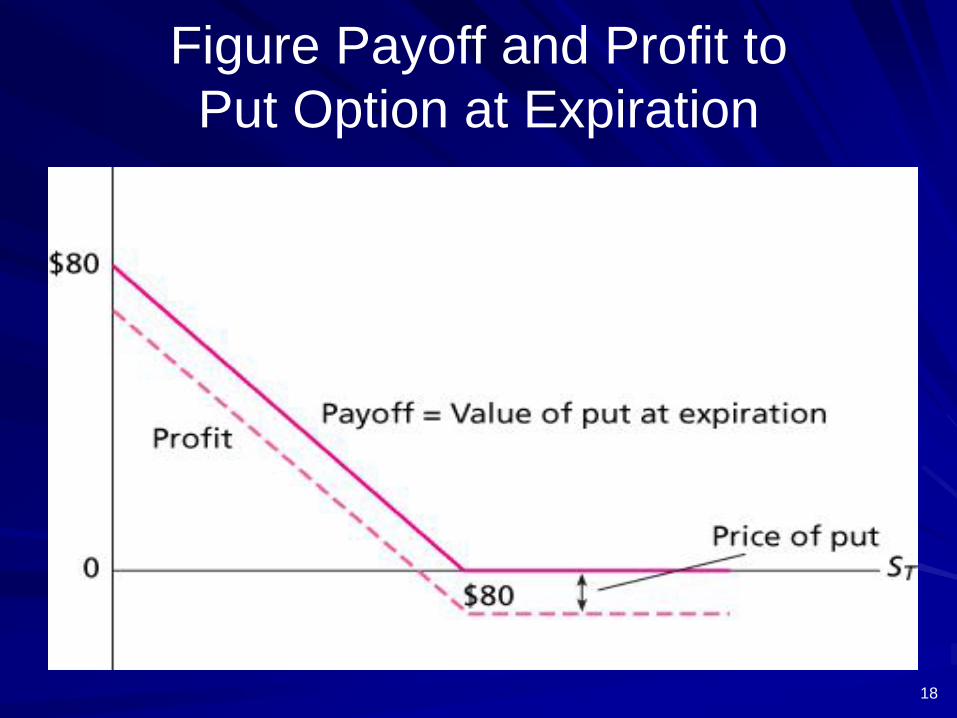

Figure Payoff and Profit to

Put Option at Expiration

19

Optionlike Securities

Callable Bonds

Convertible Securities

Warrants

Collateralized Loans

Levered Equity and Risky Debt

20

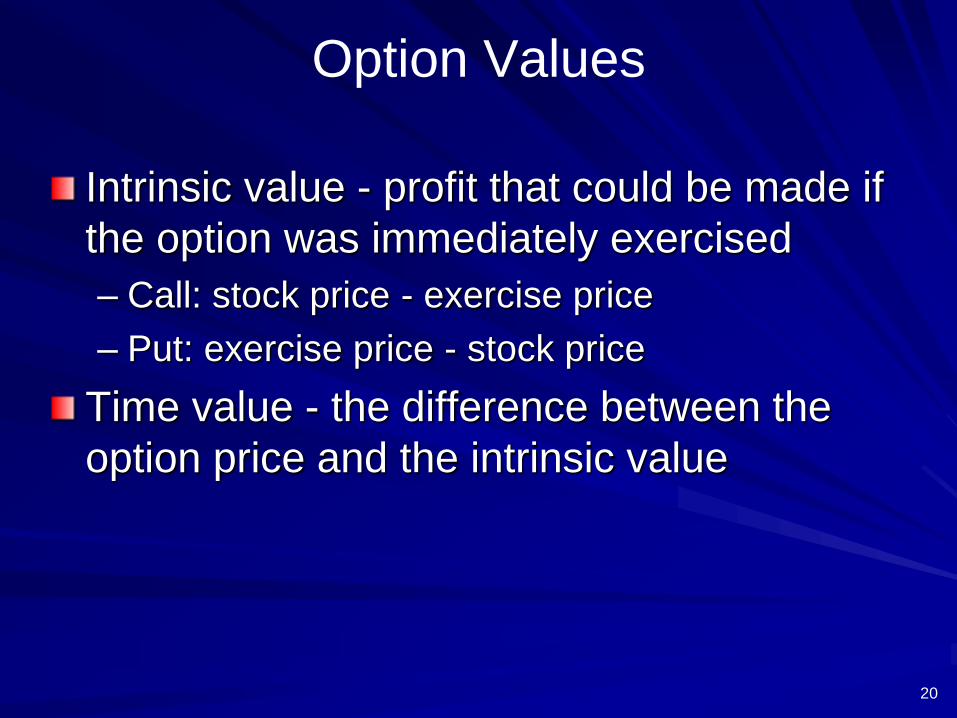

Option Values

Intrinsic value - profit that could be made if

the option was immediately exercised

– Call: stock price - exercise price

– Put: exercise price - stock price

Time value - the difference between the

option price and the intrinsic value

21

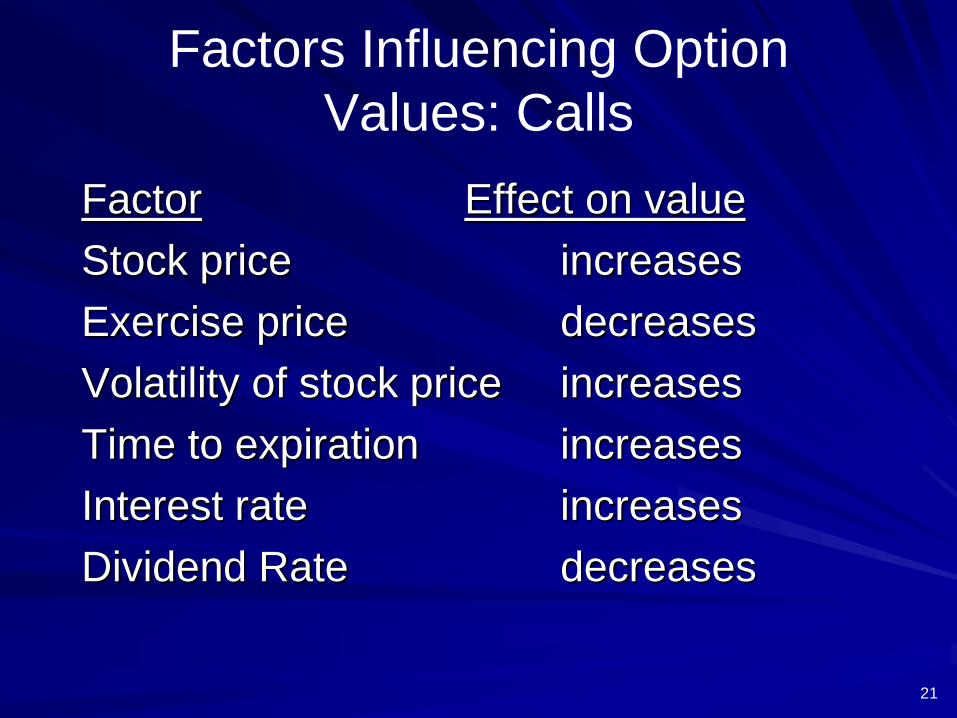

Factors Influencing Option

Values: Calls

Factor Effect on value

Stock price increases

Exercise price decreases

Volatility of stock price increases

Time to expiration increases

Interest rate increases

Dividend Rate decreases

22

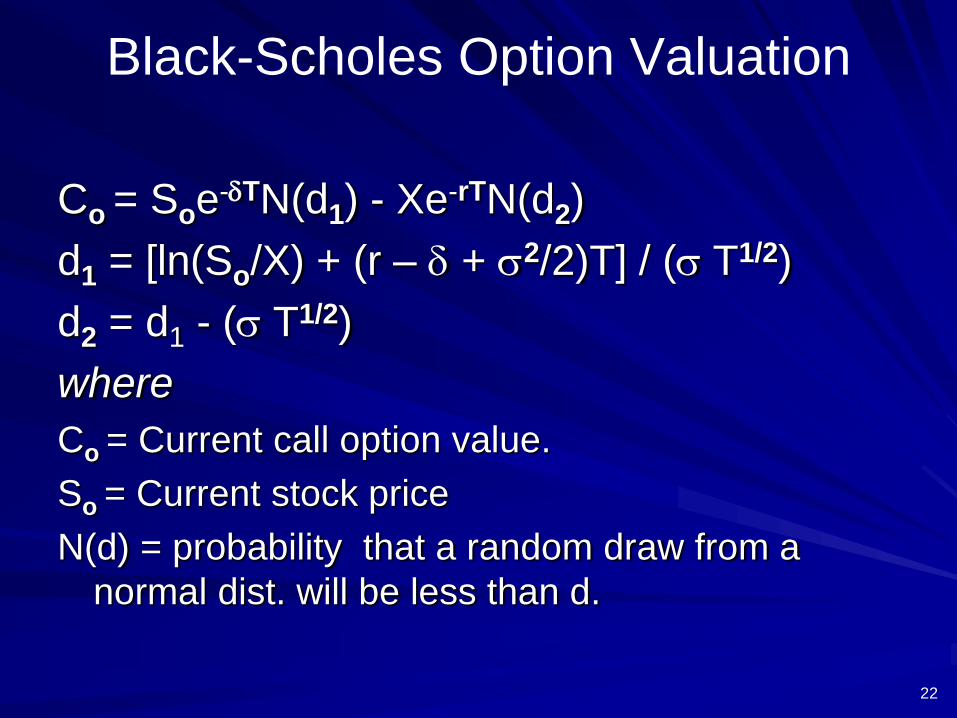

Black-Scholes Option Valuation

Co = Soe-dTN(d1) - Xe-rTN(d2)

d1 = [ln(So/X) + (r – d + s2/2)T] / (s T1/2)

d2 = d1 - (s T1/2)

where

Co = Current call option value.

So = Current stock price

N(d) = probability that a random draw from a

normal dist. will be less than d.

23

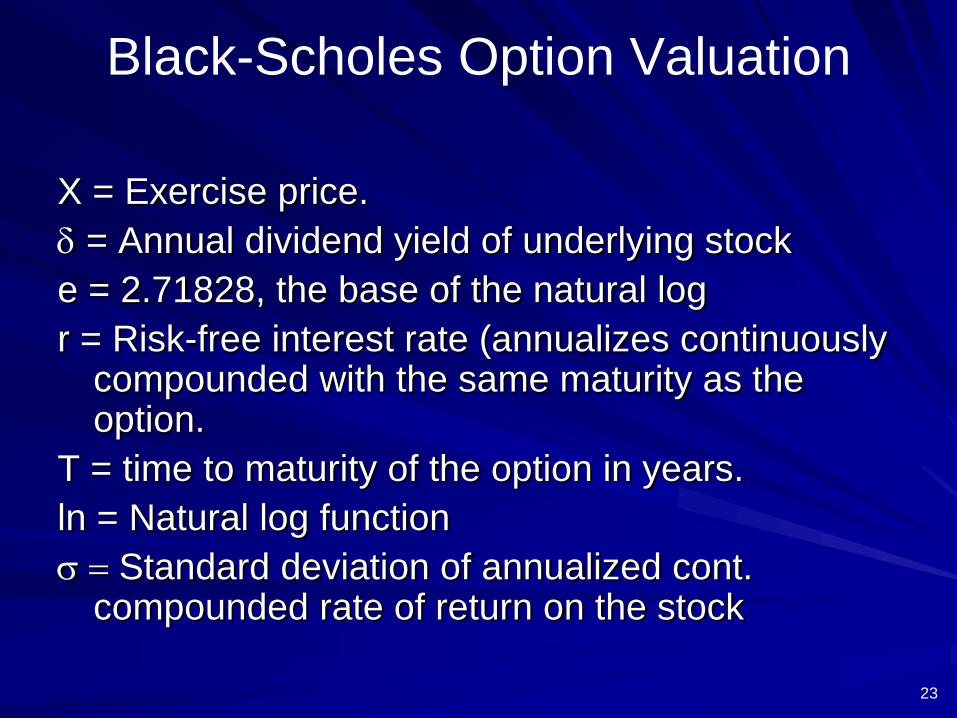

Black-Scholes Option Valuation

X = Exercise price.

d = Annual dividend yield of underlying stock

e = 2.71828, the base of the natural log

r = Risk-free interest rate (annualizes continuously compounded with the same maturity as the option.

T = time to maturity of the option in years.

ln = Natural log function

s = Standard deviation of annualized cont. compounded rate of return on the stock

24

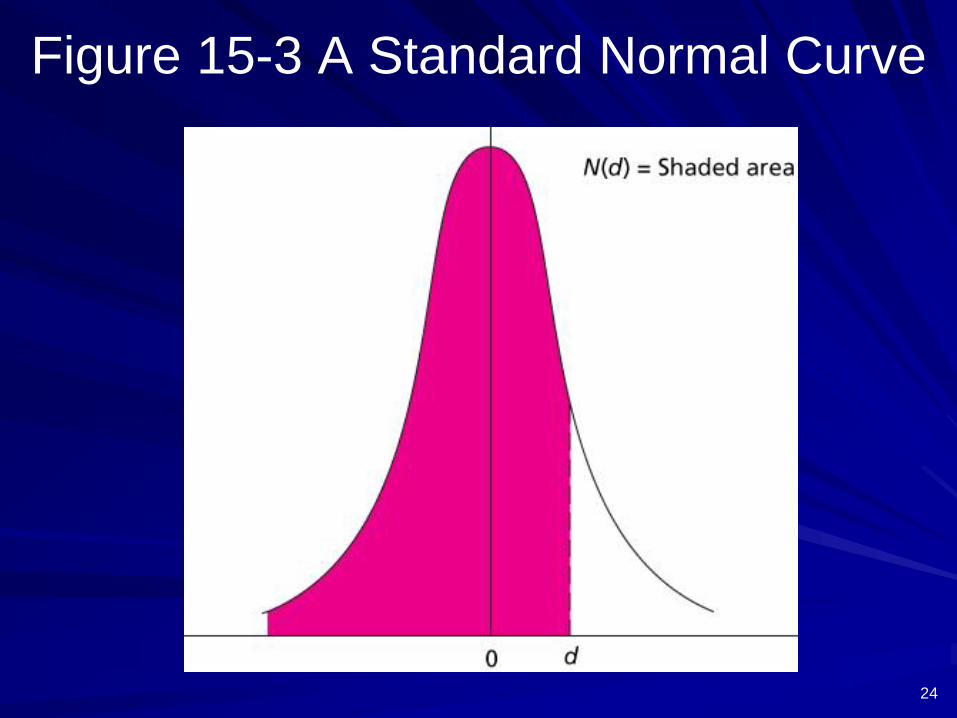

Figure 15-3 A Standard Normal Curve

25

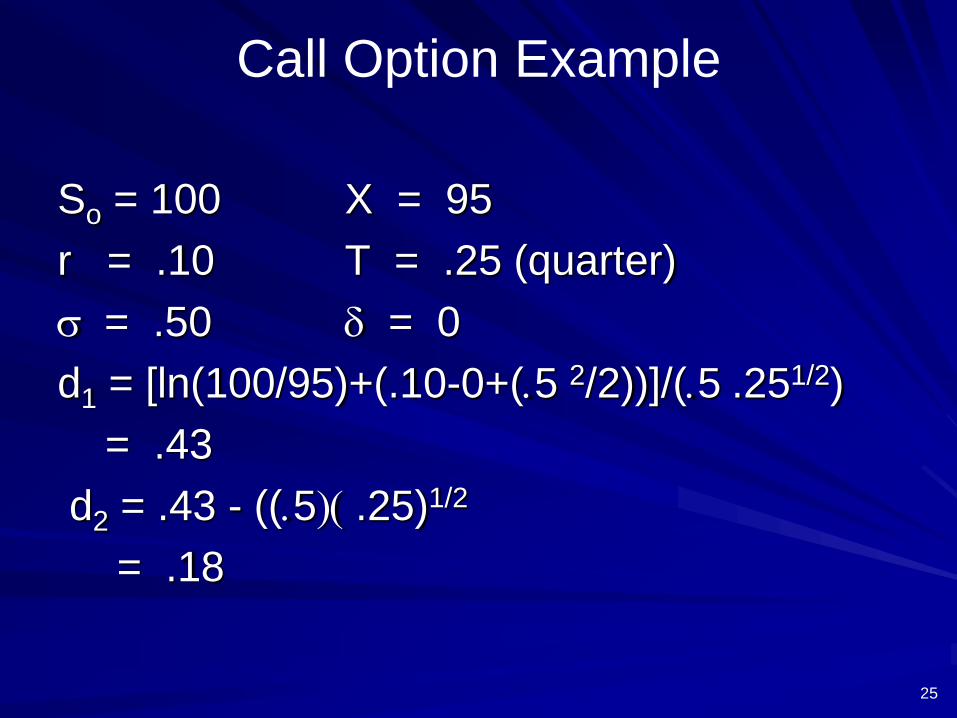

Call Option Example

So = 100 X = 95

r = .10 T = .25 (quarter)

s = .50 d = 0

d1 = [ln(100/95)+(.10-0+(.5 2/2))]/(.5 .251/2)

= .43

d2 = .43 - ((.5)( .25)1/2

= .18

26

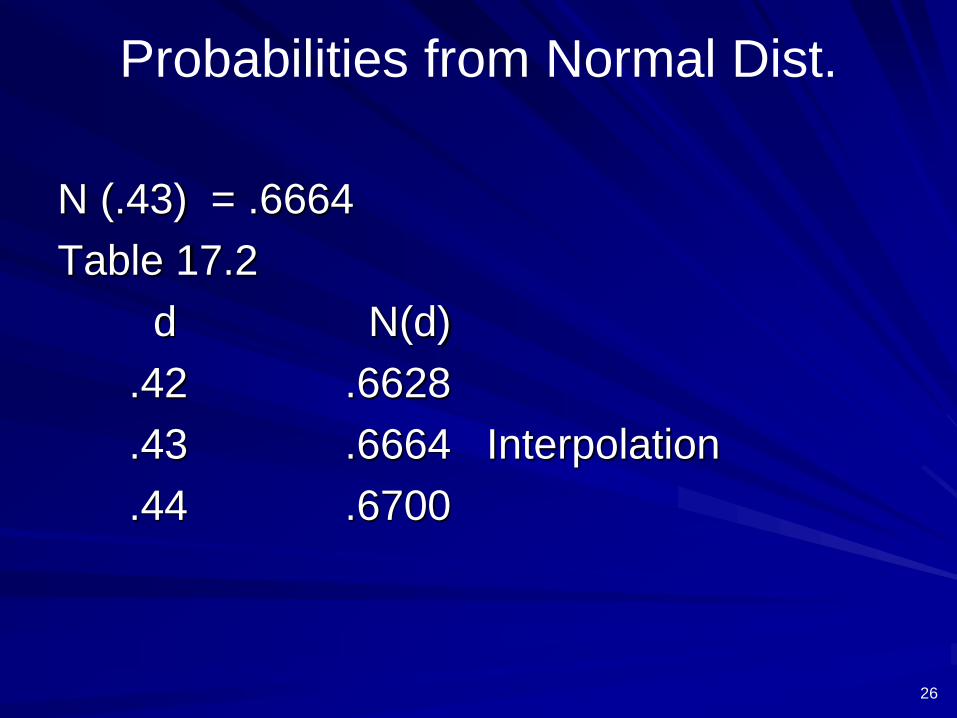

Probabilities from Normal Dist.

N (.43) = .6664

Table 17.2

d N(d)

.42 .6628

.43 .6664 Interpolation

.44 .6700

27

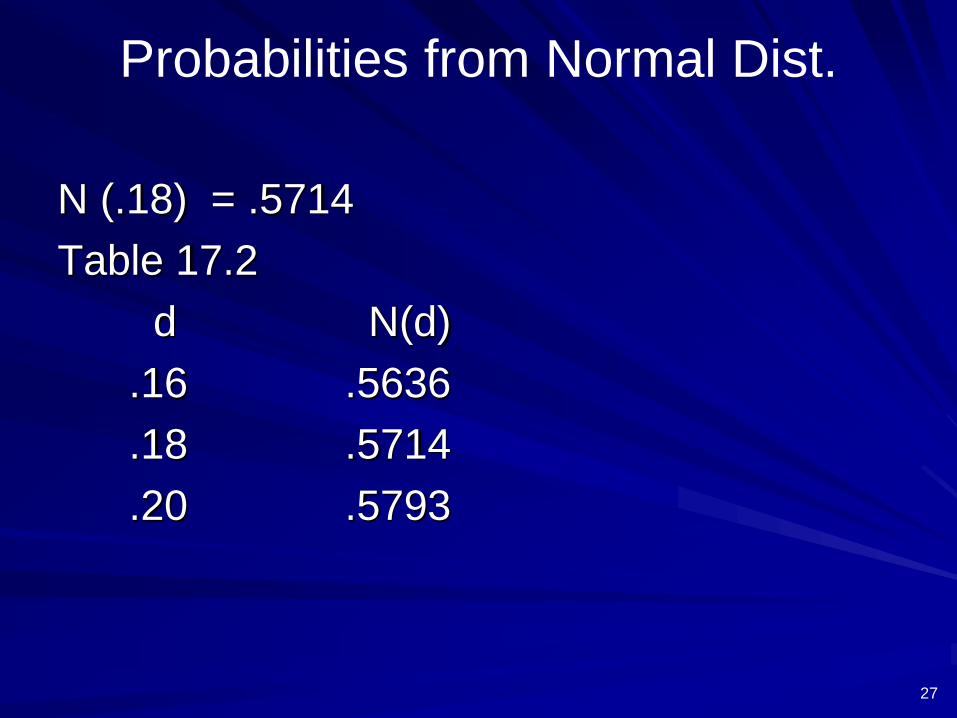

Probabilities from Normal Dist.

N (.18) = .5714

Table 17.2

d N(d)

.16 .5636

.18 .5714

.20 .5793

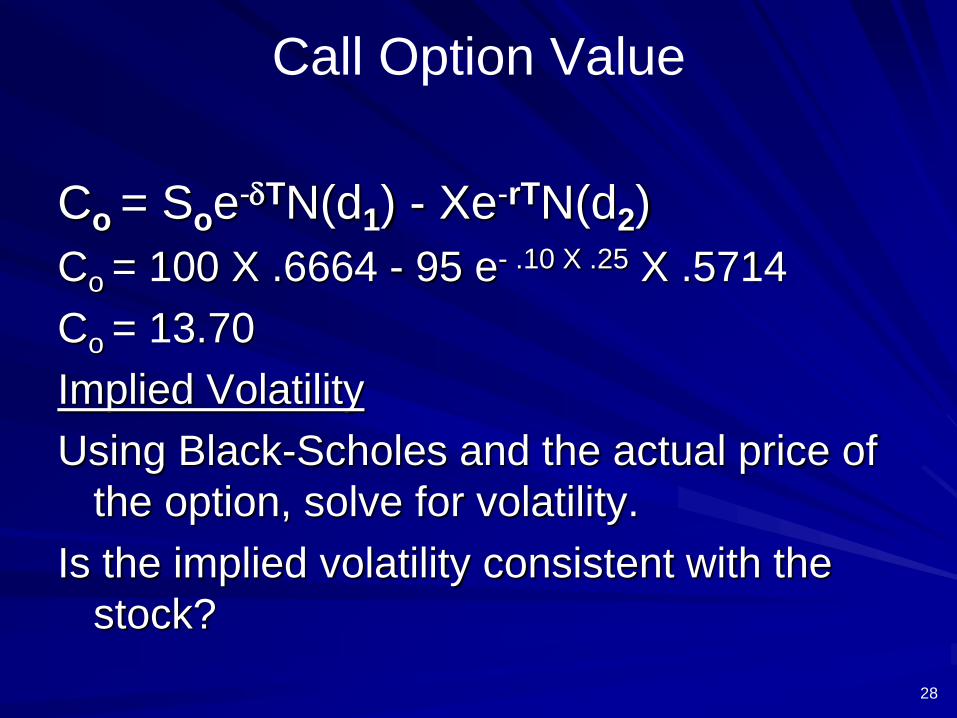

28

Call Option Value

Co = Soe-dTN(d1) - Xe-rTN(d2)

Co = 100 X .6664 - 95 e- .10 X .25 X .5714

Co = 13.70

Implied Volatility

Using Black-Scholes and the actual price of

the option, solve for volatility.

Is the implied volatility consistent with the

stock?

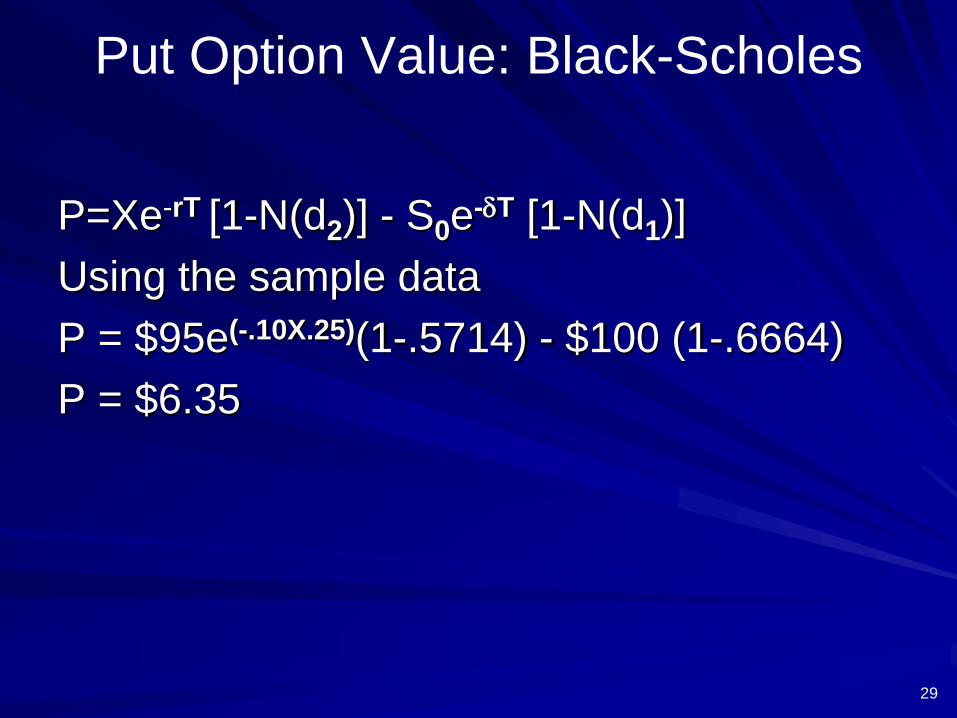

29

Put Option Value: Black-Scholes

P=Xe-rT [1-N(d2)] - S0e-dT [1-N(d1)]

Using the sample data

P = $95e(-.10X.25)(1-.5714) - $100 (1-.6664)

P = $6.35

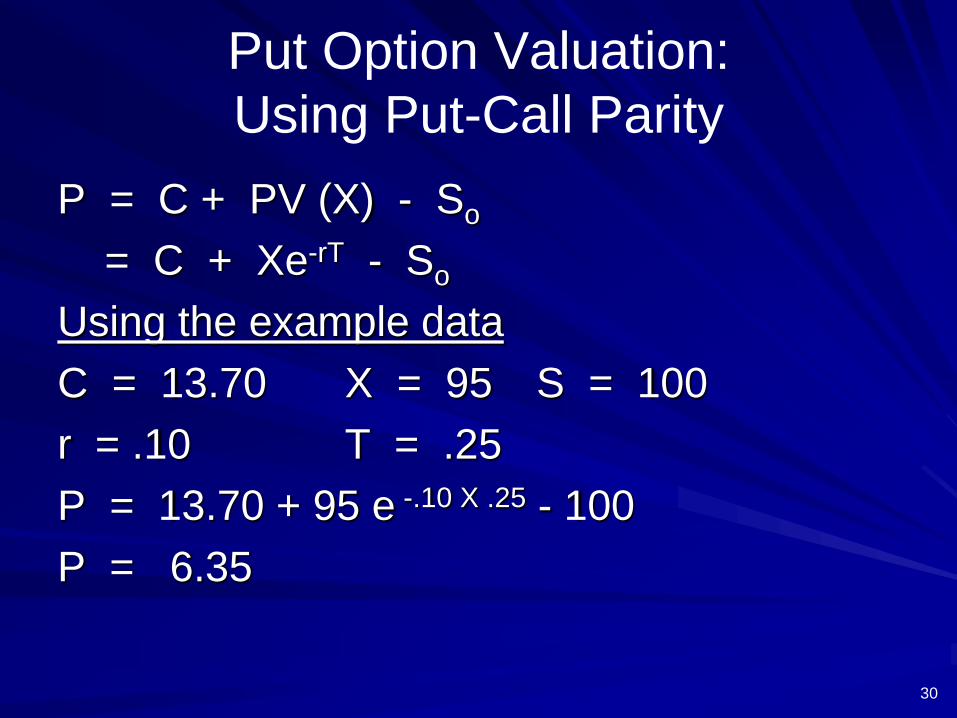

30

Put Option Valuation:

Using Put-Call Parity

P = C + PV (X) - So

= C + Xe-rT - So

Using the example data

C = 13.70 X = 95 S = 100

r = .10 T = .25

P = 13.70 + 95 e -.10 X .25 - 100

P = 6.35

31

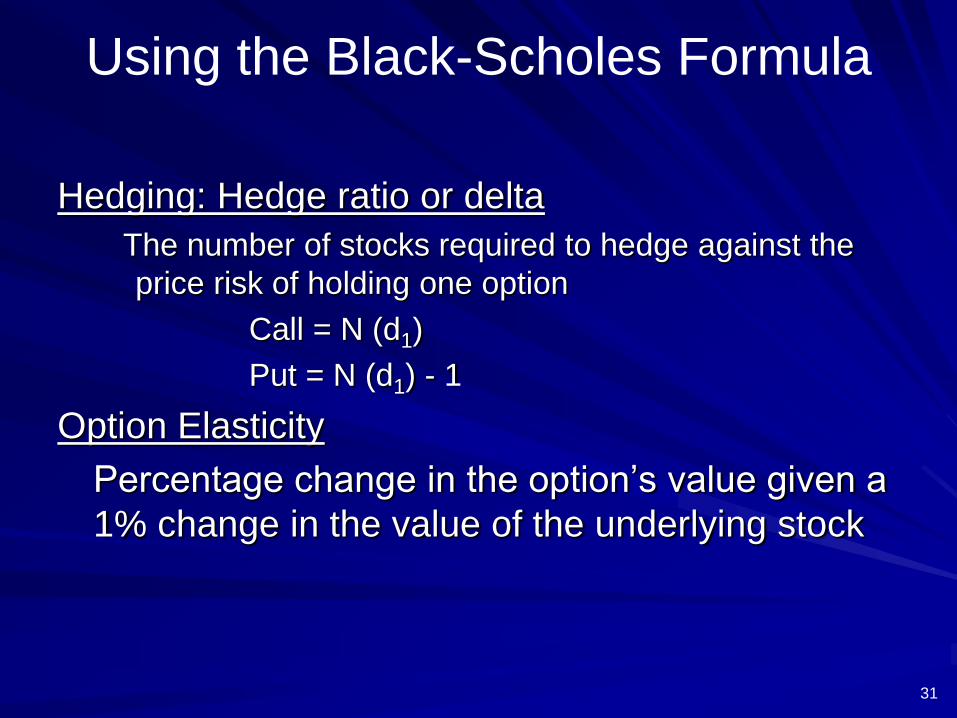

Using the Black-Scholes Formula

Hedging: Hedge ratio or delta

The number of stocks required to hedge against the

price risk of holding one option

Call = N (d1)

Put = N (d1) - 1

Option Elasticity

Percentage change in the option’s value given a

1% change in the value of the underlying stock