riding the nanotechnology wave - oxford instruments · pdf fileriding the nanotechnology wave...

TRANSCRIPT

The Business of Science®

Page 1 © Oxford Instruments 2013

Riding the

Nanotechnology Wave

13th February 2013

The Business of Science®

Page 2 © Oxford Instruments 2013

• General concepts, Nanotechnology and Tools – Jonathan Flint, Chief Executive

• Applying concepts to markets – Andy Matthews, Group Operations Director

• Accessing markets – Kevin Boyd, Group Finance Director

• Managing products and people – Ian Barkshire, Group Technical Director

• Summary and conclusions – Jonathan Flint, Chief Executive

Agenda

Page 3 © Oxford Instruments 2013

The Business of Science®

• Mathematics

This presentation may contain Science

Page 4 © Oxford Instruments 2013

The Business of Science®

• Mathematics

• Physics

This presentation may contain Science

Page 5 © Oxford Instruments 2013

The Business of Science®

• Mathematics

• Physics

• Chemistry

This presentation may contain Science

Page 6 © Oxford Instruments 2013

The Business of Science®

• Mathematics

• Physics

• Chemistry

• Quantum Mechanics

This presentation may contain Science

The Business of Science®

Page 7 © Oxford Instruments 2013

Mathematics

The Business of Science®

Page 8 © Oxford Instruments 2013

The $ per atom argument

The Business of Science®

Page 9 © Oxford Instruments 2013

Nanotechnology is a

mathematical certainty

The Business of Science®

Page 10 © Oxford Instruments 2013

• Surface area really matters

– Same volume of material

– 1 nm Nanoparticles have 10 million times the surface

area of a 1cm cube

Chemistry

Image courtesy of www.nano.gov/naonotech-101

The Business of Science®

Page 11 © Oxford Instruments 2013

Basic chemistry makes

Nanotechnology

inevitable

Page 12 © Oxford Instruments 2013

The Business of Science®

Moore’s Law

The Business of Science®

Page 13 © Oxford Instruments 2013

Physics makes

Nanotechnology a

certainty

Page 14 © Oxford Instruments 2013

The Business of Science®

Cooper’s Law

Page 15 © Oxford Instruments 2013

The Business of Science®

Haitz’s Law

The Business of Science®

Page 16 © Oxford Instruments 2013

The Quantum leap…

The Business of Science®

Page 17 © Oxford Instruments 2013

• Quantum Encryption

• Quantum Computing

The Quantum leap to Nanotechnology

The Business of Science®

Page 18 © Oxford Instruments 2013

Rose’s Law

The Business of Science®

Page 19 © Oxford Instruments 2013

Scientific principles make

Nanotechnology inevitable

Page 20 © Oxford Instruments 2013

The Business of Science®

How can you harvest

near term and long

term value from

Nanotechnology?

The Business of Science®

Page 21 © Oxford Instruments 2013

Sutter’s Fort

The Business of Science®

Page 22 © Oxford Instruments 2013

Samuel Brannan

The Business of Science®

Page 23 © Oxford Instruments 2013

John Sutter

The Business of Science®

Page 24 © Oxford Instruments 2013

Industrialise the process

Page 25 © Oxford Instruments 2013

The Business of Science®

Nanotechnology Tools

• NanoAnalysis Asylum Research Omniprobe

• NanoScience

• Omicron

• Plasma Technology

Industrial Products

• Industrial Analysis X-ray Fluorescence Optical Emission Spectroscopy Magnetic Resonance

• Industrial

Components Austin Superconducting Wire X-ray Technology

Service

• OiService CT& MR (3rd Party)

• NT & IP Service (OI products)

Our Businesses

Page 26 © Oxford Instruments 2013

The Business of Science®

• New Materials

Global Trends

Page 27 © Oxford Instruments 2013

The Business of Science®

• Environment

Global Trends

The Business of Science®

Page 28 © Oxford Instruments 2013

• New sources of energy

Global Trends

The Business of Science®

Page 29 © Oxford Instruments 2013

• High Tech Healthcare

Global Trends

0

500

1000

1500

2000

2500

2000 2010 2020 2030 2040 2050

Mill

ions

Year

World Population 60 and Over: 2000 - 2050

Source: Ageing societies – Sarah Harper (Hodder Arnold)

The Business of Science®

Page 30 © Oxford Instruments 2013

• Emerging markets

Global Trends

0

10

20

30

40

50

60

2010 2050

Constant 2000 USD, Tn

Growth of Emerging Markets vs Developing Markets

Developed Markets Emerging Markets

Source HSBC Calculations

The Business of Science®

Page 31 © Oxford Instruments 2013

• New Materials

• Environment

• New sources of energy

• High Tech Healthcare

• Emerging Markets

Company of the Future

The Business of Science®

Page 32 © Oxford Instruments 2013

The Business of Science®

Page 33 © Oxford Instruments 2013

Oxford Instruments

• Market:

• Model:

• Products:

Nanotechnology

Tools

Driven by Global Trends

The Business of Science®

Page 34 © Oxford Instruments 2013

Applying Concepts to Markets

Andy Matthews

Group Operations Director

The Business of Science®

Page 35 © Oxford Instruments 2013

Convergence of sciences

The Nanotechnology Revolution

Nano science

Nanotechnology

Bio Chem Phys

The Business of Science®

Page 36 © Oxford Instruments 2013

Convergence of sciences

The Nanotechnology Revolution

Nano science

Nanotechnology

Bio Chem Phys

Repeatable

Fabrication & Measurement

capability

The Business of Science®

Page 37 © Oxford Instruments 2013

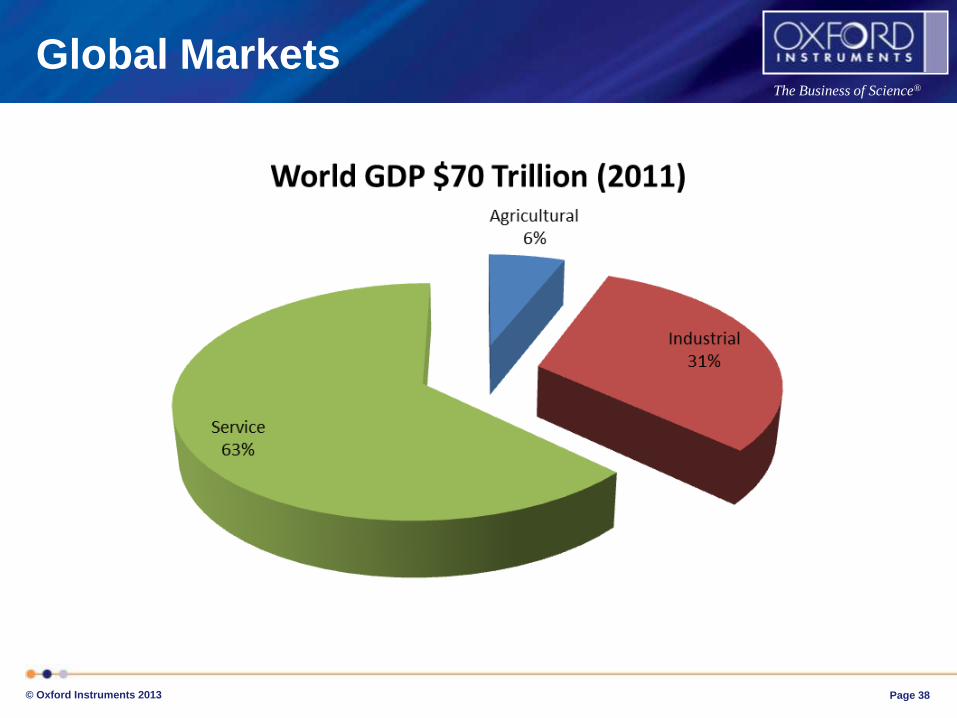

Global Markets

Convergence of sciences

The Nanotechnology Revolution

Bio Chem Phys

Repeatable

Fabrication & Measurement

capability

Nanotechnology

Nano science

Auto & Aviation

Metals Consumer Chemicals

Semi-con Pharma/

health

The Business of Science®

Page 38 © Oxford Instruments 2013

Global Markets

The Business of Science®

Page 39 © Oxford Instruments 2013

Nanotechnology Markets

Nanotechnology Enabled

Products

The Business of Science®

Page 40 © Oxford Instruments 2013

Nanotechnology Markets

Nanotechnology Enabled Products

Growing at 30%-40% CAGR

The Business of Science®

Page 41 © Oxford Instruments 2013

The Nanotechnology Revolution

Global Markets

Consumer

Semi-con

The Business of Science®

Page 42 © Oxford Instruments 2013

The Nanotechnology Revolution

Global Markets

Pharma/ health

The Business of Science®

Page 43 © Oxford Instruments 2013

The Nanotechnology Revolution

Global Markets

Auto & Aviation

Metals Chemicals

The Business of Science®

Page 44 © Oxford Instruments 2013

Global Markets

Convergence of sciences

The Nanotechnology Revolution

Bio Chem Phys

Repeatable

Fabrication & Measurement

capability

Nanotechnology

Nano science

Auto & Aviation

Metals Consumer Chemicals

Semi-con Pharma/

health

The Business of Science®

Page 45 © Oxford Instruments 2013

Governments’ funding of

Nanotechnology

Source: Cientifica ltd. 2011

20% growth in funding in next 3 years

The Business of Science®

Page 46 © Oxford Instruments 2013

US Government Nanotechnology Funding

Source: NNI (Nano.Gov Web Site)

The Business of Science®

Page 47 © Oxford Instruments 2013

Nanotechnology Market

• Nanotechnology market = $17 billion

• Growing at 10% -15% CAGR

• Nanotools market = $4 billion

The Business of Science®

Page 48 © Oxford Instruments 2013

• Nanotechnology enabled product – High efficiency solar cells currently in development

• Nanotechnology – Thin film 10nm Al2O3 layer used to improve efficiency

• Nanotool – FlexAl ALD tool from Plasma Technology

Nanotechnology Example

The Business of Science®

Page 49 © Oxford Instruments 2013

World Nanotechnology Market

World GDP ≈ $70 trillion

World Industry GDP ≈ $22 trillion Nano-enabled products ≈ $1 trillion

Nano products ≈ $17 billion

NanoTools ≈ $4 billion

The Business of Science®

Page 50 © Oxford Instruments 2013

Accessing markets

Kevin Boyd

Group Finance Director

The Business of Science®

Page 51 © Oxford Instruments 2013

World Nanotechnology Market

World GDP ≈ $70 trillion

World Industry GDP ≈ $22 trillion Nano-enabled products ≈ $1 trillion

Nano products ≈ $17 billion

NanoTools ≈ $4 billion

The Business of Science®

Page 52 © Oxford Instruments 2013

• What fraction of the market is addressed by our products?

(Product coverage)

• What fraction of the customers can we reach?

(market Presence)

• What fraction of the customers choose us over the

competition?

(Hit rate)

Link to Oxford Instruments

PPH Analysis

The Business of Science®

Page 53 © Oxford Instruments 2013

How we determine market share

The Business of Science®

Page 54 © Oxford Instruments 2013

Market Share

Market Share = 72% x 50% x 50% = 18%

The Business of Science®

Page 55 © Oxford Instruments 2013

• Increase R&D

spend

• Add technologies

through acquisitions

Nanotechnology Tools Sector PPH

- Product Coverage

0

5

10

15

20

25

30

2005/6 2006/7 2007/8 2008/9 2009/10 2010/11 2011/12

£M

The Business of Science®

Page 56 © Oxford Instruments 2013

• Increase direct presence

in BRIC

• Acquire distribution and

offer more Service

• Presence growth in

BRIC for acquisitions

Nanotechnology Tools Sector PPH

- Presence

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2009 2010 2011 2012

£M

BRIC revenues

The Business of Science®

Page 57 © Oxford Instruments 2013

• Brand recognition value

• Recruit and retain best people

• Better, faster, more efficient internal

processes and controls

• Better integrated marcomms

• Better selling processes and CRM

• Improve customer satisfaction score

Nanotechnology Tools Sector PPH

- Hit Rate

The Business of Science®

Page 58 © Oxford Instruments 2013

100%

17%

71%

55%

7%

0%

20%

40%

60%

80%

100%

120%

Market Product Coverage

Presence Hit Rate Market Share

Nanotechnology Tools Sector PPH

The Business of Science®

Page 59 © Oxford Instruments 2013

Total Market

$4bn

Acquisition

Targets

Product Product Product Product

Presence Presence Presence Presence

Hit Rate Hit Rate Hit Rate Hit Rate

Plasma Tech

Market

Omicron

Market Hopper

NanoScience

Market NanoAnalysis

Market

Organic Growth

Strategy

R&D Plan

Sales Plan

Ops Plan

M&A

Strategy

Target

Selection

From Market to Strategy

NS NA

PT ON

Addressed Market

The Business of Science®

Page 60 © Oxford Instruments 2013

Techniques totalling $4.0bn

Market segmentation

The Business of Science®

Page 61 © Oxford Instruments 2013

Group Techniques into Clusters

Experimental equipment, $300M

Imaging, $1,600M

Characterisation, $600M

Nano-mechanics, $70M

Nano-structures, $1,100M

Nano-particles, $240M

0

10

20

30

40

50

60

70

80

90

100

Nu

mb

er

of

co

mp

an

ies

pa

rtic

ipa

tin

g

Market proximity

The Business of Science®

Page 62 © Oxford Instruments 2013

Market Concentration

OI

OI

OI

OI

OI

Co. 8

Co. 8 Co. 8

Co.8

Co. 7

Co. 7

Co. 7

Co. 6

Co. 5

Co. 5

Co. 5

Co. 4

Co. 3

Co. 3

Co. 3 Co. 2

Co. 2

Co. 2

Co. 1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

experimental equipment

characterisation imaging nanomechanics nano structures/films particles

Sh

are

of

Clu

ste

r

The Business of Science®

Page 63 © Oxford Instruments 2013

Product Coverage

Characterisation Experimental

equipment Imaging Nano-structures Nano-mechanics Nano-particles

EBSD WDS EDS Technique C1 Technique C2 Technique C3 Technique C4 Technique C5 Technique C6 Technique C7 Technique C8 Technique C9

Cryogenics >1k ULT <1k Systems (MPHS/PMPS) Magnet Instrumentation (experiment control) Technique EE1 Technique EE2 Technique EE3

Technique I1 Technique I2 Technique I3 Technique I4 Technique I5 Technique I6 Technique I7 Technique I8

CVD PECVD PVD ALD RIE Technique NS1 Technique NS2 Technique NS3 Technique NS4 Technique NS5 Technique NS6 Technique NS7 Technique NS8

Technique NM1 Technique NM2 Technique NM3 Technique NM4 Technique NM5 Technique NM6 Technique NM7

Particle analysis Technique NP1 Technique NP2

Existing

The Business of Science®

Page 64 © Oxford Instruments 2013

Product Coverage

Omicron

Characterisation Experimental

equipment Imaging Nano-structures Nano-mechanics Nano-particles

EBSD WDS EDS XPS Auger Technique C3 Technique C4 Technique C5 Technique C6 Technique C7 Technique C8 Technique C9

Cryogenics >1k ULT <1k Systems (MPHS/PMPS) Magnet Instrumentation (experiment control) UHV Technique EE2 Technique EE3

SPM - UHV Technique I2 Technique I3 Technique I4 Technique I5 Technique I6 Technique I7 Technique I8

CVD PECVD PVD ALD RIE MBE Technique NS2 Technique NS3 Technique NS4 Technique NS5 Technique NS6 Technique NS7 Technique NS8

Technique NM1 Technique NM2 Technique NM3 Technique NM4 Technique NM5 Technique NM6 Technique NM7

Particle analysis Technique NP1 Technique NP2

Existing

The Business of Science®

Page 65 © Oxford Instruments 2013

Product Coverage

Omniprobe

Characterisation Experimental

equipment Imaging Nano-structures Nano-mechanics Nano-particles

EBSD WDS EDS XPS Auger Technique C3 Technique C4 Technique C5 Technique C6 Technique C7 Technique C8 Technique C9

Cryogenics >1k ULT <1k Systems (MPHS/PMPS) Magnet Instrumentation (experiment control) UHV Technique EE2 Technique EE3

SPM - UHV Technique I2 Technique I3 Technique I4 Technique I5 Technique I6 Technique I7 Technique I8

CVD PECVD PVD ALD RIE MBE Technique NS2 Technique NS3 Technique NS4 Technique NS5 Technique NS6 Technique NS7 Technique NS8

Nanomanipulators Technique NM2 Technique NM3 Technique NM4 Technique NM5 Technique NM6 Technique NM7

Particle analysis Technique NP1 Technique NP2

Omicron

Existing

The Business of Science®

Page 66 © Oxford Instruments 2013

Product Coverage

Asylum

Characterisation Experimental

equipment Imaging Nano-structures Nano-mechanics Nano-particles

EBSD WDS EDS XPS Auger Technique C3 Technique C4 Technique C5 Technique C6 Technique C7 Technique C8 Technique C9

Cryogenics >1k ULT <1k Systems (MPHS/PMPS) Magnet Instrumentation (experiment control) UHV Technique EE2 Technique EE3

SPM - UHV SPM - ambient Technique I3 Technique I4 Technique I5 Technique I6 Technique I7 Technique I8

CVD PECVD PVD ALD RIE MBE Technique NS2 Technique NS3 Technique NS4 Technique NS5 Technique NS6 Technique NS7 Technique NS8

Nanomanipulators NanoIndentation Technique NM3 Technique NM4 Technique NM5 Technique NM6 Technique NM7

Particle analysis Technique NP1 Technique NP2

Omniprobe

Omicron

Existing

The Business of Science®

Page 67 © Oxford Instruments 2013

Regular Reviews

Synergistic

targets Regular

Contact Negotiation

Due diligence

100 day plan

Contract Integration

Criteria: • Expand product coverage

• Leverage the brand

• Synergies in markets

• Technology proximity

• Cultural proximity

• Growth potential

• Margin potential in line with 14³

or better

• Geographical proximity

Criteria: • Shareholders ready

to sell

• Doable

• Can agree on price

Criteria: • Letter of intent

Criteria: • No deal breakers

• Acceptable contract

• Board approval

• Agreed 100 day plan

c.100

businesses

The M&A Funnel

The Business of Science®

Page 68 © Oxford Instruments 2013

Managing products, channels and

people

Ian Barkshire

Group Technical Director

The Business of Science®

Page 69 © Oxford Instruments 2013

Customers

& Markets

Market Intimacy & Voice of Customer

Select Product

Developments

Focused Product Development

Product

Launch & Customer

Support

Continuous Development Cycle

The Business of Science®

Page 70 © Oxford Instruments 2013

‘ICEBURG’ of

Available

Information

Superficial

Information

dig

dig

dig

NEEDS

summarise

dig

dig

dig

Market

Trends

summarise

Market Intimacy – Voice of Customer

• Exploration process

• Customer Interviews & Observations

• Global, Territory & Market Sector focus

The Business of Science®

Page 71 © Oxford Instruments 2013

Making NPI more effective

Planning Delivery Embed Execution

• FIVE Stage Gate Development Process

• Management Board sign off

• Audited process

The Business of Science®

Page 72 © Oxford Instruments 2013

Making NPI more effective

• FIVE Stage Gate Development Process

• Management Board sign off

• Audited process

Planning Delivery Embed Execution

The Business of Science®

Page 73 © Oxford Instruments 2013

Making NPI more effective

• FIVE Stage Gate Development Process

• Management Board sign off

• Audited process

Planning Delivery Execution

0

20

40

60

80

100

120

I F D L V

Cost

Flexibility

%

Gate

Embed

The Business of Science®

Page 74 © Oxford Instruments 2013

Making NPI more effective

0

20

40

60

80

100

120

I F D L V

Cost

Flexibility

%

Gate

• FIVE Stage Gate Development Process

• Management Board sign off

• Audited process

Planning Delivery Embed Execution

The Business of Science®

Page 75 © Oxford Instruments 2013

Making NPI more effective

• FIVE Stage Gate Development Process

• Management Board sign off

• Audited process

44% Vitality Index

Planning Delivery Embed Execution

The Business of Science®

Page 76 © Oxford Instruments 2013

SIZE Matters - Taking Analysis from hours to minutes

A real success story

150mm2

Aug 2012

The Business of Science®

Page 77 © Oxford Instruments 2013

What else Matters to Customers?

Thermal Stability

Throughput

Resolution

The Business of Science®

Page 78 © Oxford Instruments 2013

+

Finding & Riding the Waves

The Business of Science®

Page 79 © Oxford Instruments 2013

Finding & Riding the Waves

HB LED

The Business of Science®

Page 80 © Oxford Instruments 2013

Finding & Riding the Waves

HB LED

Quantum Computing

The Business of Science®

Page 81 © Oxford Instruments 2013

Finding & Riding the Waves

HB LED

Graphene

Quantum Computing

The Business of Science®

Page 82 © Oxford Instruments 2013

Product Styling reinforces our brand

The Business of Science®

Page 83 © Oxford Instruments 2013

Managing the people who make it happen

Outstanding Personal

Performance

Clear, inspiring strategy

Challenging work

Performance culture

Customer intimacy

Personal Recognition

Intelligent Dialogue

Technical Career Path

Ethical Values

The Business of Science®

Page 84 © Oxford Instruments 2013

Innovative Teamwork

The Business of Science®

Page 85 © Oxford Instruments 2013

Employee Engagement

• Understanding the strategy

• Emotional commitment

73%

35-40%

Benchmark

point

Oxford Instruments

The Business of Science®

Page 86 © Oxford Instruments 2013

Efficiencies

80.0

100.0

120.0

140.0

160.0

180.0

200.0

2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

£'0

00

Sales/employee

The Business of Science®

Page 87 © Oxford Instruments 2013

Managing & Integrating acquisitions

• Culture Advantage

• Engaging with Creative Staff

• Leverage ‘Value’ from proven OI processes

• Create new OI Champions

The Business of Science®

Page 88 © Oxford Instruments 2013

Summary and

Conclusions

Jonathan Flint

Chief Executive

The Business of Science®

Page 89 © Oxford Instruments 2013

• Nanotechnology is the place to be

• Broad exposure to Nanotechnology via Tools model

• Total Nanotechnology

• Tools market of $4bn

• PPH model drives detailed strategy

• Opportunity-rich, diverse market space

• People and processes to deliver growth

Summary

The Business of Science®

Page 90 © Oxford Instruments 2013

• This presentation concentrated on our

Nanotechnology Tools Sector

• Industrial Products Sector provides the opportunity

for industrialisation of Nanotech

• Service Sector provides stable, recurring revenues

to support R&D

Oxford Instruments Sectors

The Business of Science®

Page 91 © Oxford Instruments 2013

• 14 cubed target reaffirmed

• Strategic momentum for the medium and

long term, driven by successive

technology waves

• New strategic plan to be announced in

June 2014

Conclusions

The Business of Science®

Page 92 © Oxford Instruments 2013

Disclaimer

This presentation is prepared for and addressed to authorised persons within the meaning of the Financial Services and

Markets Act 2000 (FSMA). The information contained in this presentation is not for publication, distribution or reproduction,

in whole or in part, to any persons outside the jurisdiction of this Act. The Company, its Directors, employees, agents or

advisers do not accept or assume responsibility to any other person to whom this presentation is shown or into whose

hands it may come and any such responsibility or liability is expressly disclaimed.

Statements contained in this presentation are based on the knowledge and information available to the Company's

Directors at the date it was prepared and therefore the facts stated and views expressed may change after that date. By

their nature, any statements concerning the risks and uncertainties facing the Company in this presentation involve

uncertainty since future events and circumstances can cause results and developments to differ materially from those

anticipated. To the extent that this presentation contains any statement dealing with any time after the date of its

preparation such statement is merely predictive and speculative as it relates to events and circumstances which are yet to

occur. The Company undertakes no obligation to update these forward-looking statements.

The information in this presentation shall not constitute or be deemed to constitute any offer or invitation to invest in or

otherwise deal in shares or other securities of Oxford Instruments plc.

All information in the presentation is the property of Oxford Instruments plc.