rets presentation - home inspector's insurance & risk management

TRANSCRIPT

Home Inspector’s Insurance & Risk Management

Presented by:

Jerry Brunker, CPCU , ARM&

Brett Byland, ARM

RETS – Arlington TX, February 27, 2015

Learning Objectives - RETS Part 1 - Home Inspection Industry Overview

Liability of Home Inspectors Part 2 –Insurance

Types of Insurance Protection for Home Inspectors Tool Kit for Home Inspectors with Tips and Hints to

Reduce Liability Exposures Questions and Answers

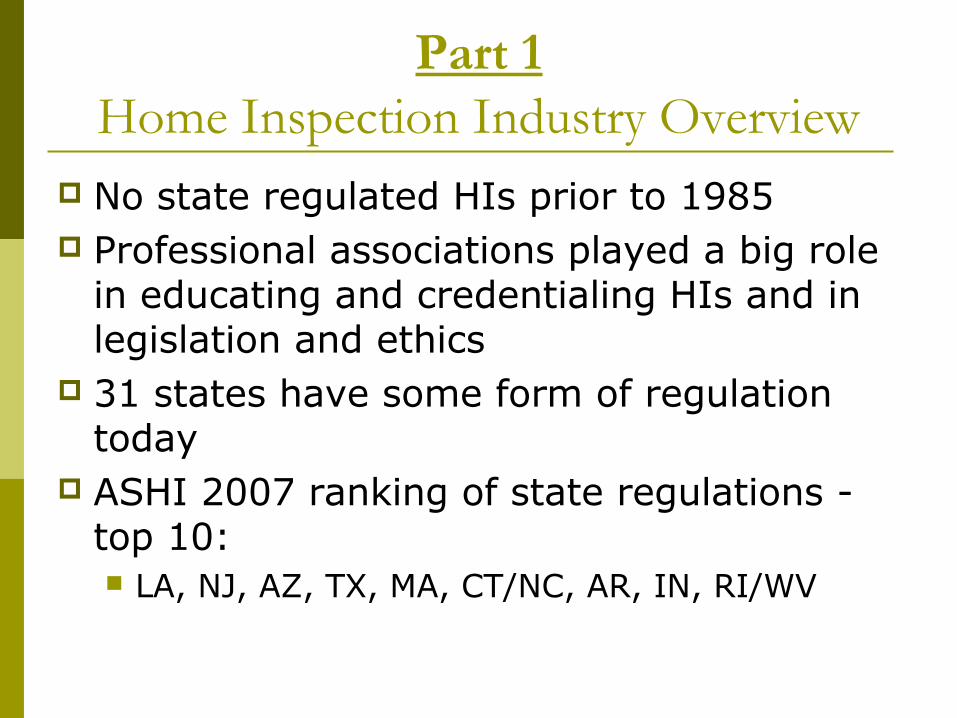

Part 1Home Inspection Industry Overview

No state regulated HIs prior to 1985 Professional associations played a big role

in educating and credentialing HIs and in legislation and ethics

31 states have some form of regulation today

ASHI 2007 ranking of state regulations - top 10: LA, NJ, AZ, TX, MA, CT/NC, AR, IN, RI/WV

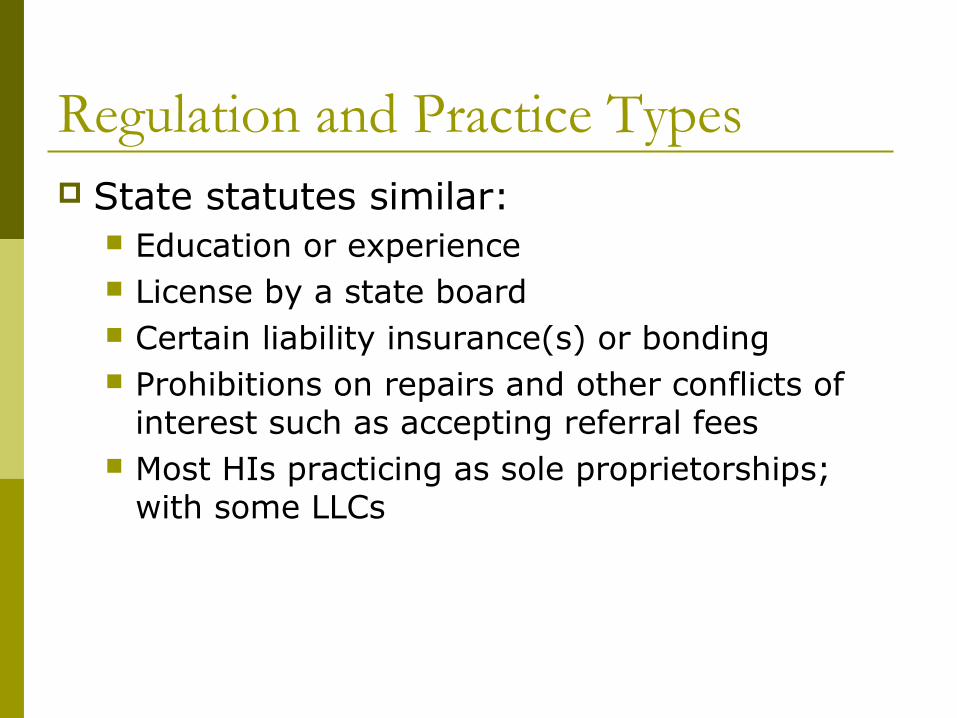

Regulation and Practice Types State statutes similar:

Education or experience License by a state board Certain liability insurance(s) or bonding Prohibitions on repairs and other conflicts of

interest such as accepting referral fees Most HIs practicing as sole proprietorships;

with some LLCs

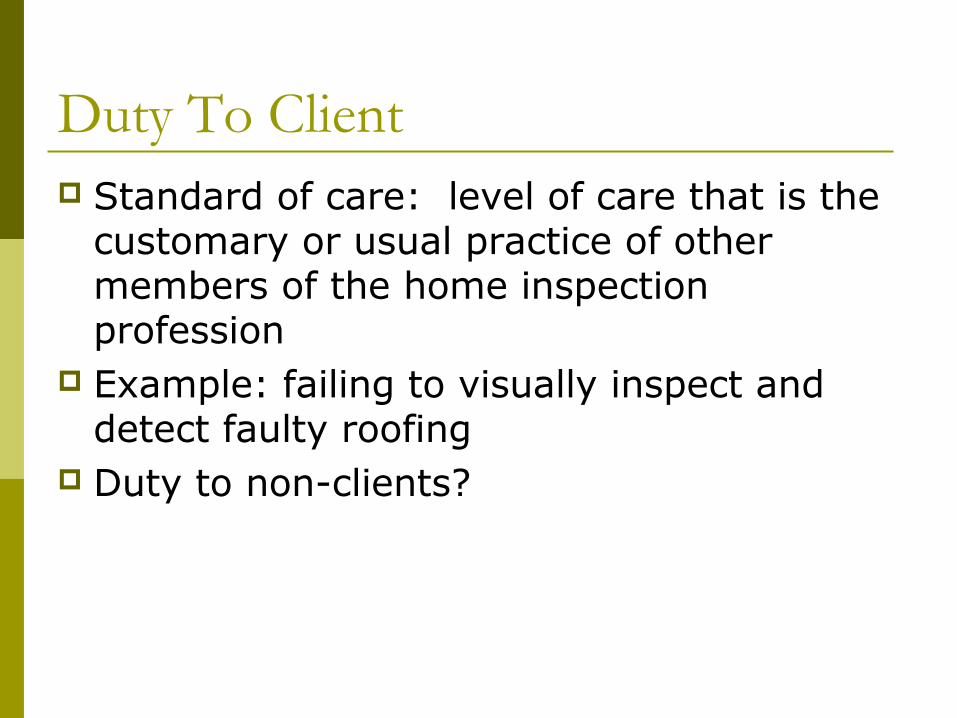

Duty To Client Standard of care: level of care that is the

customary or usual practice of other members of the home inspection profession

Example: failing to visually inspect and detect faulty roofing

Duty to non-clients?

Negligence Four key elements to a suit:

HI had a duty to the client Prove HI breached that duty Plaintiff must show they were injured Prove breach of duty was proximate cause of

the injury (was breach sufficiently responsible so that HI should be held accountable?)

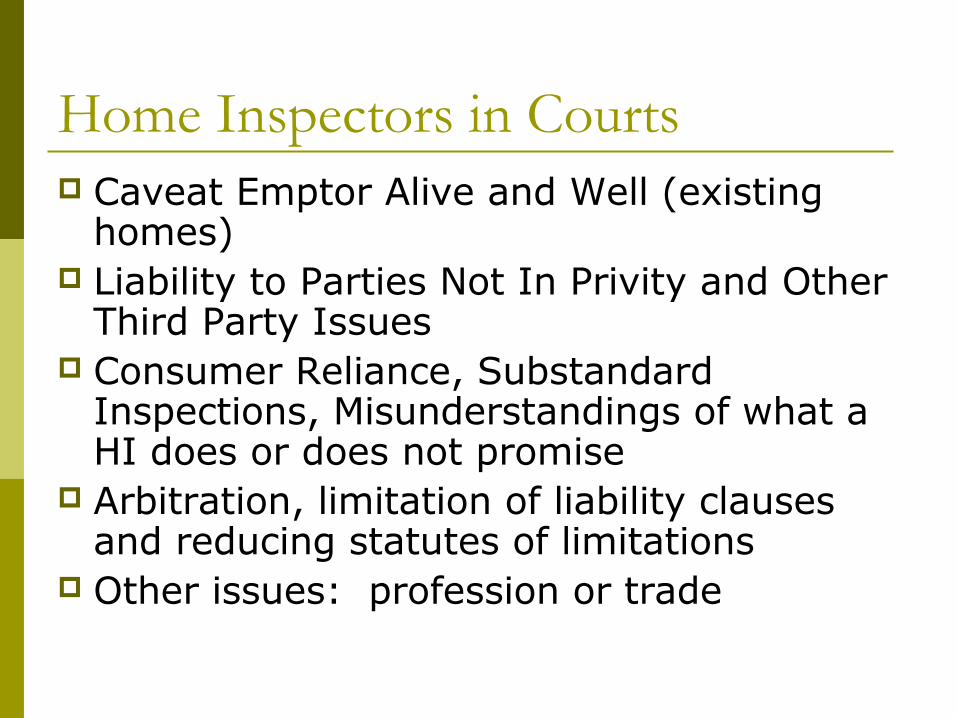

Home Inspectors in Courts Caveat Emptor Alive and Well (existing

homes) Liability to Parties Not In Privity and Other

Third Party Issues Consumer Reliance, Substandard

Inspections, Misunderstandings of what a HI does or does not promise

Arbitration, limitation of liability clauses and reducing statutes of limitations

Other issues: profession or trade

Liability To Parties Not In Privity Other defendants with the HI: sellers, real estate

agents and lenders Attempts to limit circulation of written reports

and to limit liability to party in privity Like other professionals with written reports,

courts have expanded liability beyond client identified in contract

Use disclaimer language and express language aimed at listing agent and seller

Potential exposure to seller for devaluation of property

Consumer Reliance Out options on contract if inspection uncovers

significant problems (buyer) “As is” imposes duty on buyer to thoroughly

inspect – can be fatal to a subsequent claim for fraud, fraudulent suppression or negligence

Buyer should not expect to hold HI liable when HI’s recommendations for further investigations are ignored

Whether sellers or real estate salespersons present during the inspection

Buyers must understand limited nature of inspections (visual snapshot @ accessible places)

ASHI Definition of Home Inspection A visual analysis for the purposes of providing a

professional opinion of the condition of a building and its carports and garages, any reasonably accessible installed components and the operation of the building systems, including the controls normally operated by the owner, for the following components of a residential building of four units or fewer: heating system, electrical system, cooling system, plumbing system, structural components, foundation, roof covering, exterior and interior components and site aspects as they affect the building.

Substandard Inspections Most common claim is negligence and not

fraud HIs performing beyond mere negligence

may be liable for mental anguish and violations of DTPA (Guilbeau v Anderson 841 S.W.2d517 (Tex.App. 1992)

Limitation of Liability and Imposition of Mandatory Arbitration Mixed success in most jurisdictions Enforceability of arbitration has not gone

well – not many cases – cost of arbitration greater than the fee limitation

Limitation of liability clauses – present them early and in a conspicuous fashion (Head v U.S. Inspect DFW, Inc.) (limitation of liability clause was set apart; enclosed in a box and separately initialed by client)

Shrinking Statutes of Limitation Statutes of limitations for torts and contracts –

bar action after the injury or discovery of a deficiency

In Pitts v Watkins HI went 0-3. MS Supreme Court found arbitration was unconscionable (HI could go to court but consumer forced to arbitrate)

Limitation of liability unconscionable with $265 fee limitation but negligence caused damages of $30,000-$40,000

Three year statute of limitation shrunk to one year from date of inspection – further evidence of overreaching, oppressive, unconscionable

Other Issues Suing the individual or corporate entity Texas unique with the Real Estate

Inspection Recovery Fund ($12,500 per transaction/$30,000 aggregate per inspector)

Texas Loser Pays Statute

Part 2Insurance Overview

New TREC Laws Bonds

What is Professional Liability? Non-Admitted vs Admitted Markets What is General Liability? Other Insurances WDI Inspections Tips and Hints to Reduce Liability

Exposures

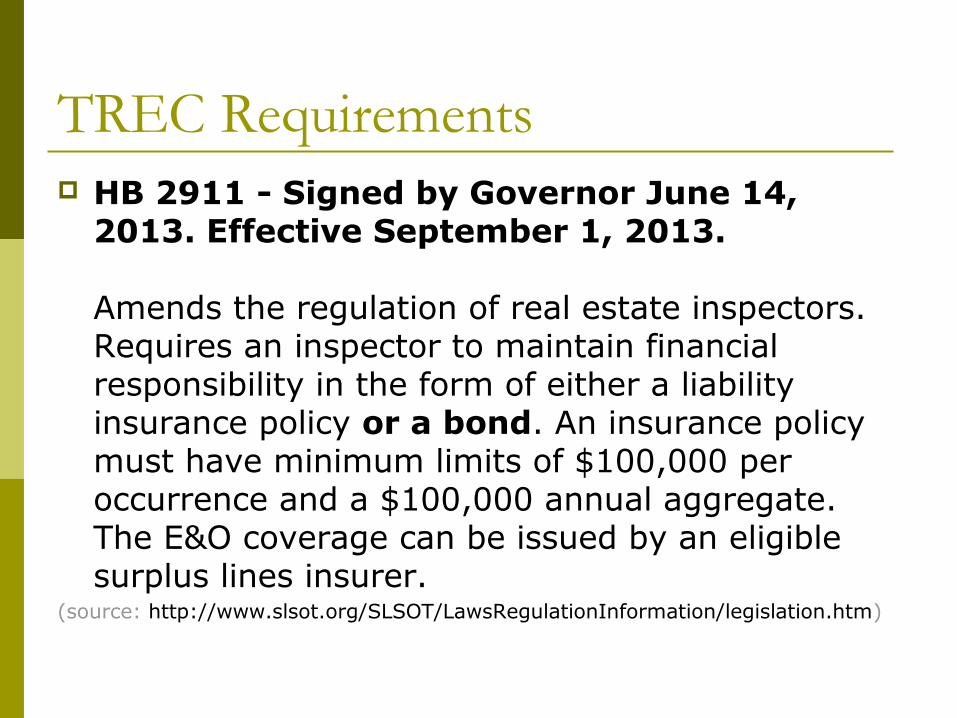

TREC Requirements HB 2911 - Signed by Governor June 14,

2013. Effective September 1, 2013.

Amends the regulation of real estate inspectors. Requires an inspector to maintain financial responsibility in the form of either a liability insurance policy or a bond. An insurance policy must have minimum limits of $100,000 per occurrence and a $100,000 annual aggregate. The E&O coverage can be issued by an eligible surplus lines insurer.

(source: http://www.slsot.org/SLSOT/LawsRegulationInformation/legislation.htm)

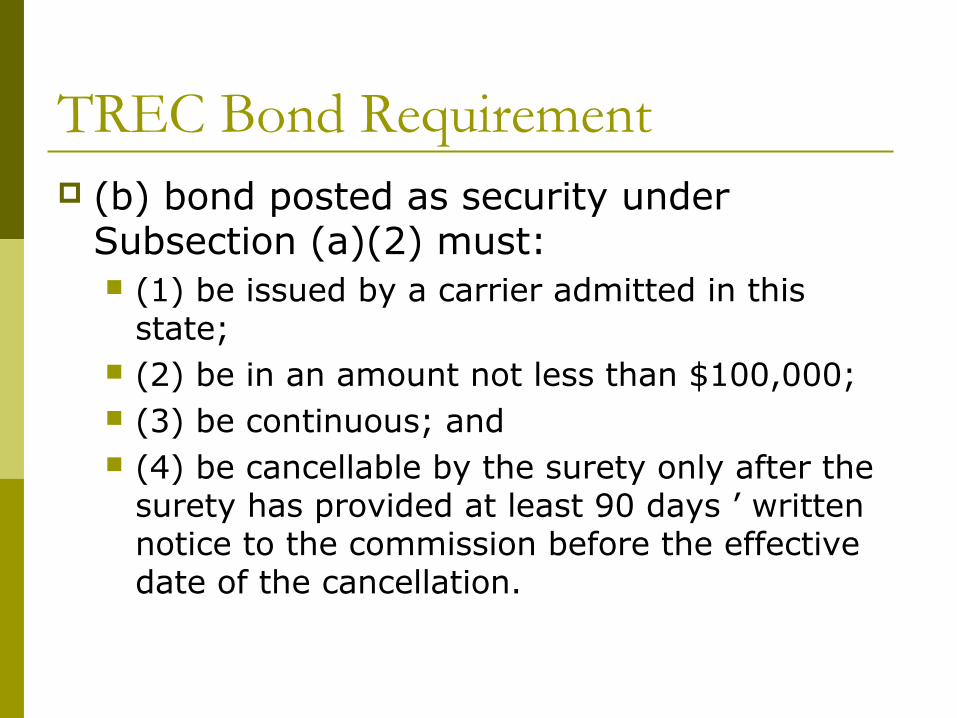

TREC Bond Requirement (b) bond posted as security under

Subsection (a)(2) must: (1) be issued by a carrier admitted in this

state; (2) be in an amount not less than $100,000; (3) be continuous; and (4) be cancellable by the surety only after the

surety has provided at least 90 days ’ written notice to the commission before the effective date of the cancellation.

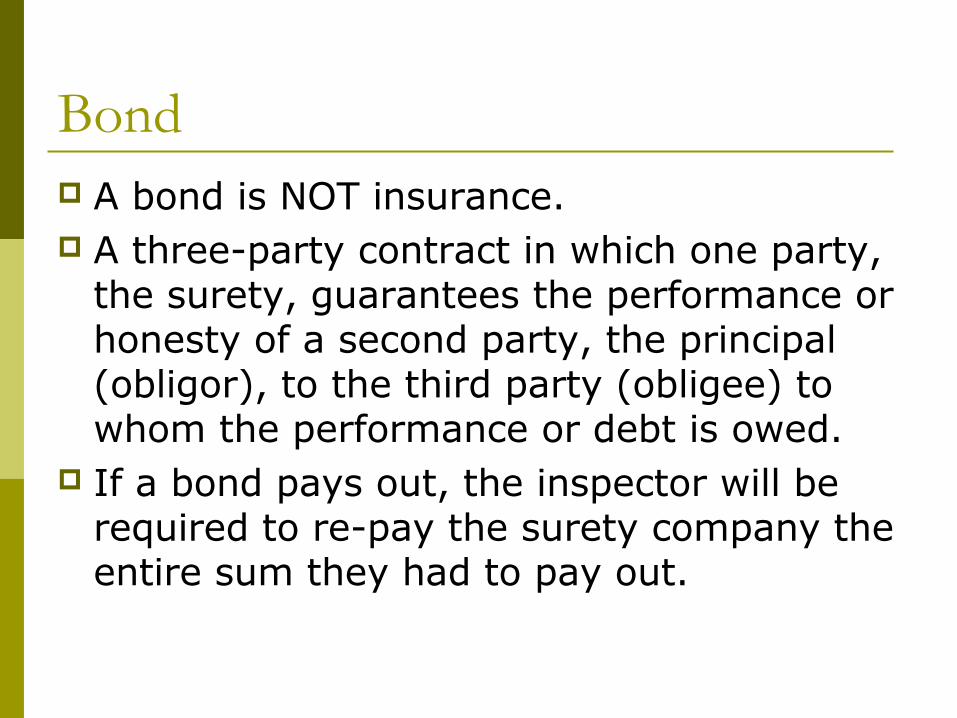

Bond A bond is NOT insurance. A three-party contract in which one party,

the surety, guarantees the performance or honesty of a second party, the principal (obligor), to the third party (obligee) to whom the performance or debt is owed.

If a bond pays out, the inspector will be required to re-pay the surety company the entire sum they had to pay out.

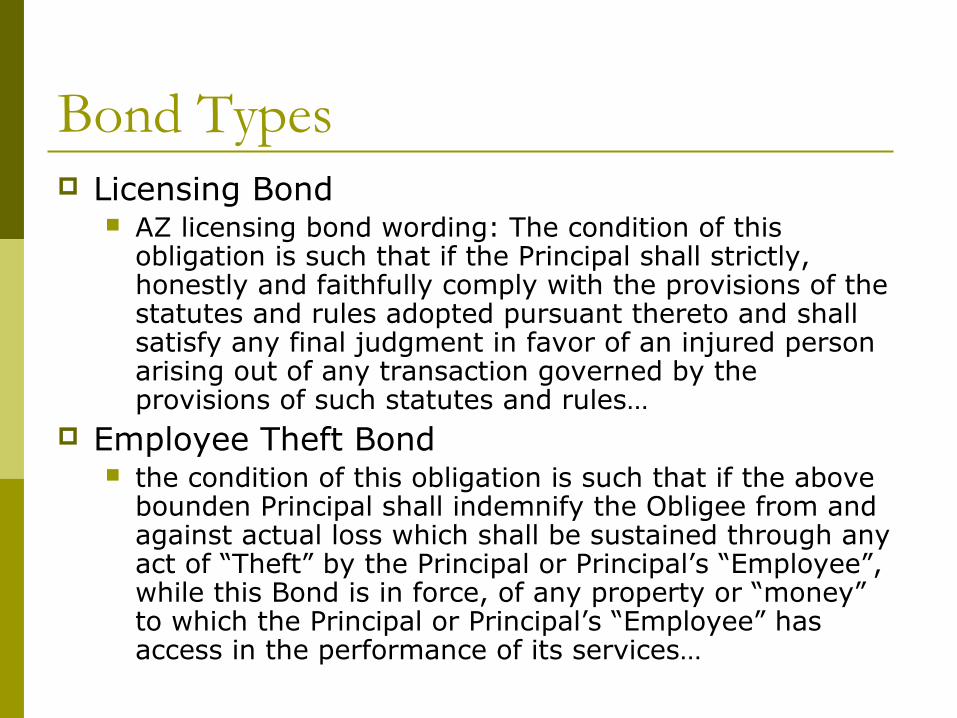

Bond Types Licensing Bond

AZ licensing bond wording: The condition of this obligation is such that if the Principal shall strictly, honestly and faithfully comply with the provisions of the statutes and rules adopted pursuant thereto and shall satisfy any final judgment in favor of an injured person arising out of any transaction governed by the provisions of such statutes and rules…

Employee Theft Bond the condition of this obligation is such that if the above

bounden Principal shall indemnify the Obligee from and against actual loss which shall be sustained through any act of “Theft” by the Principal or Principal’s “Employee”, while this Bond is in force, of any property or “money” to which the Principal or Principal’s “Employee” has access in the performance of its services…

Professional Liability Also referred to as Errors & Omissions or

E&O Coverage intended for claims that might

arise from the rendering or failure to render professional services

Professional Liability Claim Examples Failure to note bad electrical wiring

Professional Liability Claim Examples Client claims that the roof damage was

not noted on the inspection report. Weather might restrict inspecting certain areas

of the house. In this situation, be sure to make a clear notation of areas you are not able to inspect and the reasons why.

Duty to Defend Claims might arise from false or frivolous

allegations causing a business to incur defense costs. Within the scope of a policy's coverage, the insurance provider of a professional liability policy would have a duty to defend, within the policy limits.

Insurer’s duty to defend is broader than the duty to pay

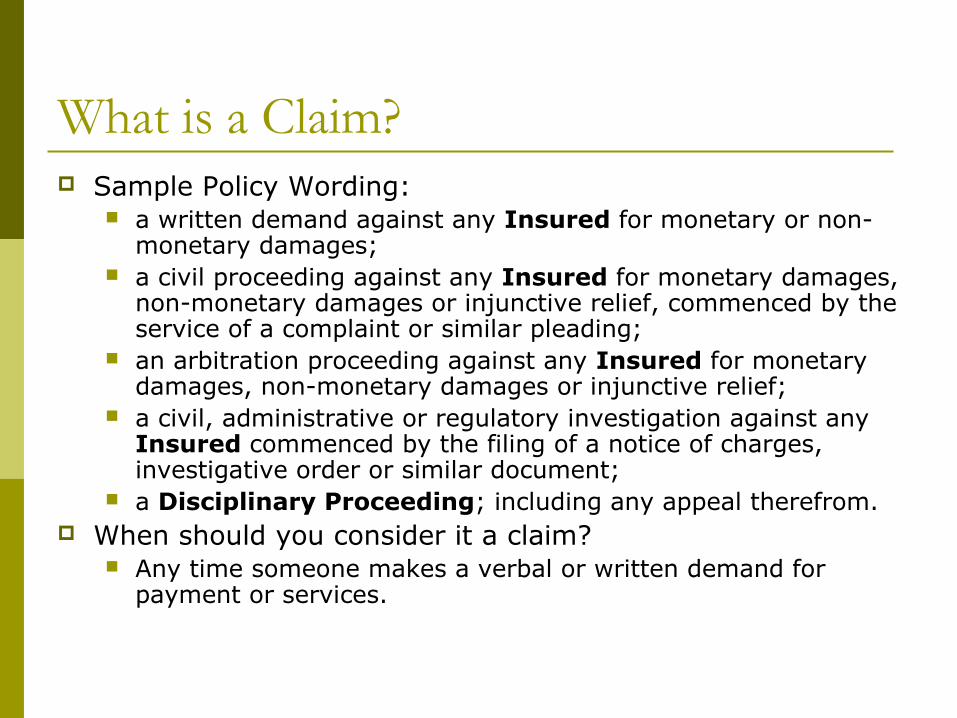

What is a Claim? Sample Policy Wording:

a written demand against any Insured for monetary or non-monetary damages;

a civil proceeding against any Insured for monetary damages, non-monetary damages or injunctive relief, commenced by the service of a complaint or similar pleading;

an arbitration proceeding against any Insured for monetary damages, non-monetary damages or injunctive relief;

a civil, administrative or regulatory investigation against any Insured commenced by the filing of a notice of charges, investigative order or similar document;

a Disciplinary Proceeding; including any appeal therefrom. When should you consider it a claim?

Any time someone makes a verbal or written demand for payment or services.

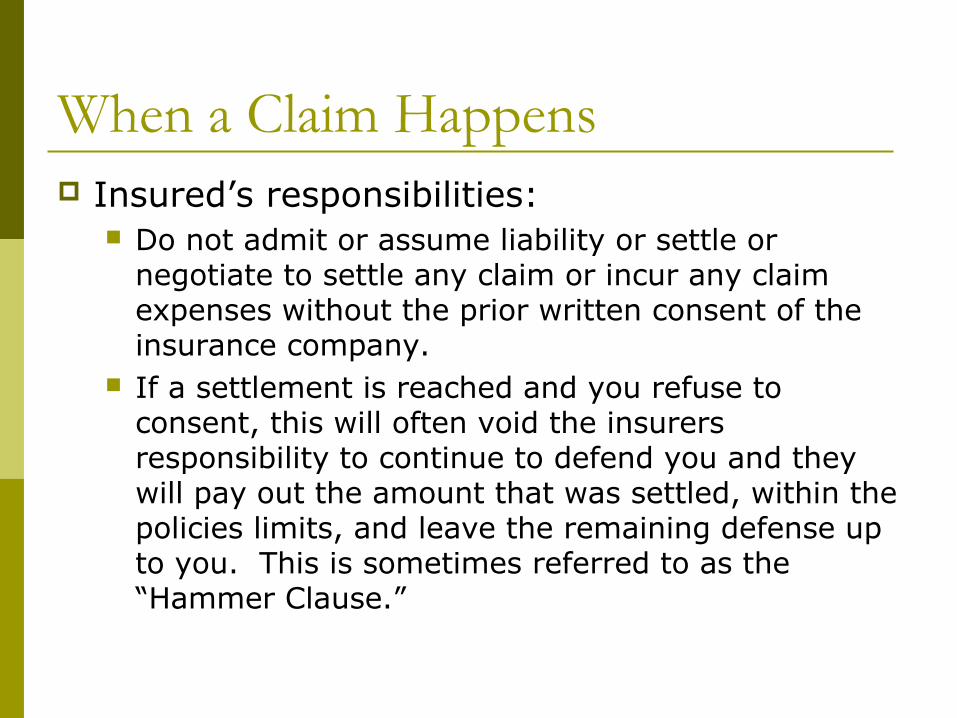

When a Claim Happens Insured’s responsibilities:

Do not admit or assume liability or settle or negotiate to settle any claim or incur any claim expenses without the prior written consent of the insurance company.

If a settlement is reached and you refuse to consent, this will often void the insurers responsibility to continue to defend you and they will pay out the amount that was settled, within the policies limits, and leave the remaining defense up to you. This is sometimes referred to as the “Hammer Clause.”

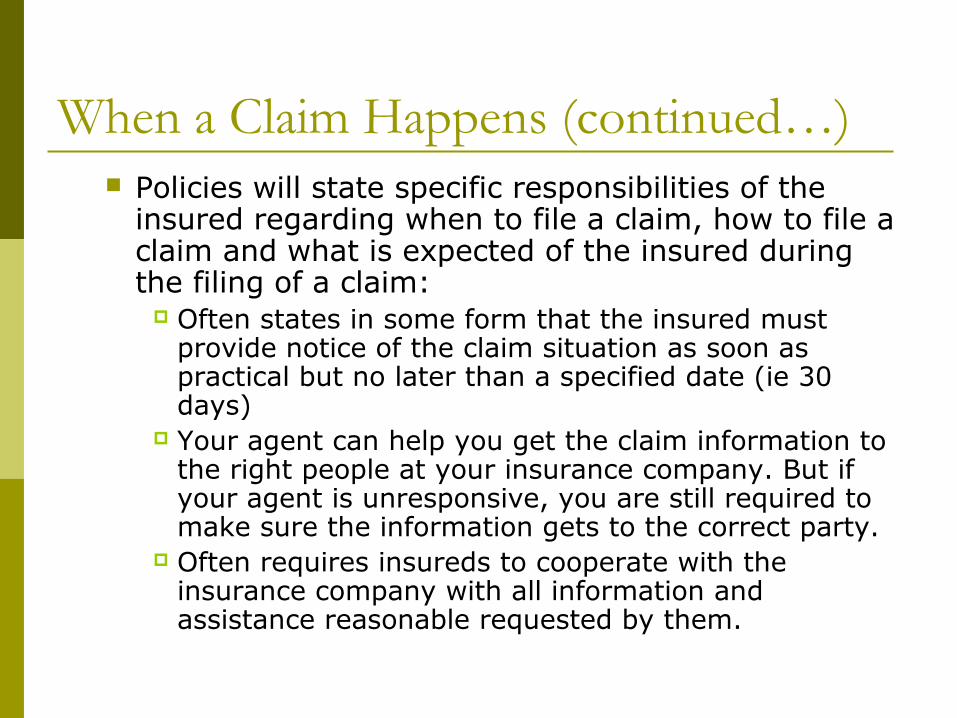

When a Claim Happens (continued…) Policies will state specific responsibilities of the

insured regarding when to file a claim, how to file a claim and what is expected of the insured during the filing of a claim:

Often states in some form that the insured must provide notice of the claim situation as soon as practical but no later than a specified date (ie 30 days)

Your agent can help you get the claim information to the right people at your insurance company. But if your agent is unresponsive, you are still required to make sure the information gets to the correct party.

Often requires insureds to cooperate with the insurance company with all information and assistance reasonable requested by them.

Disciplinary Proceeding Limit Some policies provide coverage in the

event that a disciplinary hearing causes you to incur actual loss of earnings. Often an aggregate limit that is in addition to

the policy limit Not subject to the deductible.

Each Claim/Aggregate LIMITS An each claim limit is the limit a policy can pay

out for any one claim situation. An aggregate limit is the total amount that a

policy can pay for the duration of a policy period. For example, a policy with limits of $100,000 each claim

$100,000 aggregate has a claim that pays out $50,000 and in that same policy period a second claim is filed resulting in $50,000 paid out. In this example, the policy's aggregate limit of $100,000 would be exhausted and no more coverage would exist for the remainder of the policy period.

Defense costs included within limits of liability

Retroactive date Also referred to as prior acts date Found in Claims Made policies This is the earliest date from which a currently in

force claims made policy will provide coverage for wrongful acts committed after the retroactive date. If a policy with a 09/01/12-13 policy period has a

retroactive date of 09/01/1998, coverage would be provided for claims arising from wrongful acts that took place on or after 09/01/1998 and prior to 09/01/2013.

Extended Reporting Period (ERP) Coverage afforded under a claims made

professional liability policy only applies to claims made and reported during the policy period. Coverage ceases to exist as of the expiration, cancellation or non-renewal date.

An extended reporting period (ERP) is coverage that can be purchased for an additional set amount of years in order to continue to provide coverage for inspections that were previously done between your expiring policy’s retroactive date and the expiration date of your last policy. Must be purchased within a certain time from the

expiration of your policy. Options vary by carrier Fully Earned Premiums (cannot be financed)

Contingent bodily injury/property damage Provides bodily injury and property

damage coverage to professional liability claims.

Without this coverage, bodily injury and property damages that arise out of your rendering or failure to render professional services are excluded.

Additional Coverage Options Standard home inspector’s professional liability

policies cover standard visual inspections. Specialized areas and areas that require testing often need to be added:

WDI/Pest Inspections Radon Testing Carbon Monoxide Testing Mold Inspections Septic Systems Inspections Pool/Spa Inspections Lead Inspections Code Compliance EIFS/Stucco

It is important to remember that just because you do not perform a certain type of inspection, such as carbon monoxide, does not mean someone can not sue you for it.

Options Some provide the option of ala carte

coverages. Others provide package coverage options. Independent Agents work with different

markets and are able to help you understand the differences between the different options.

Admitted/Non-Admitted Markets An admitted insurer is licensed within that state to sell

insurance. The state provides financial support if the insurer were to become financially insolvent.

A non-admitted insurer is not licensed and must have a state specified surplus lines tax paid on top of the premiums and fees. They must be approved by the states department of insurance as a non-admitted insurer. This state guaranty support would not be provided with a non-

admitted insurer that became financially insolvent. (Note: Chose an A- or higher AM Best financially rated insurer).

One of the reasons an insurer might choose to operate on a non-admitted basis is because the admitted insurers are required to file with the state’s department of insurance every change to their policies. Thus, non-admitted insurers have more flexibility to make necessary changes to their policies as the need arises.

Commercial General Liability (CGL) General liability provides protection for

claims that might arise out of premises, operations, products and completed operations resulting in bodily injury and/or property damage to a third party. Or claims may arise from specific personal injury offenses such as libel or slander or advertising injury.

Premises General Liability Bodily Injury and Property Damage

coverage only during the performance of a home inspection.

Some insurance companies have the option to add this coverage to a professional liability policy.

General Liability Claim Example During an inspection you would logically leave

your ladder propped against the house while inspecting the roof. If a gust of wind were to knock a ladder over, causing it to land atop the neighbor's head, the resulting bodily injury might land you in a general liability claim.

While walking through an attic during an inspection you might put your foot through the ceiling causing property damage that could result in a general liability claim.

Each Occurrence Limit Commonly commercial general liability

insurance is written on an occurrence policy form.

An each occurrence limit provides coverage for claims that arise out of damage or injury that took place during the policy period, regardless of when the claim is made. Defense costs in addition to limits of liability

Home Builders Requiring CGL We are seeing an increase in the amount

of home builders requiring home inspectors to carry CGL.

Typical requirements: Minimum Limits of $500,000

Possible future requirements: Listed as Additional Insured Provide Waiver of Subrogation

Additional Insureds/Referral Agent Additional Insured coverage extends your

coverage to a client/vendor. Typically only added to General Liability coverage. It is

not typically provided on E&O policies. Referral Agent specifically applies to business

associates, such as real estate agents, that might refer business to you. It provides them protection on your E&O policy that is similar to additional insured coverage. Some policies automatically include. Some can add this coverage for additional premium.

Waiver of Subrogation Subrogation is when an insurance company seeks

reimbursement from a third party that they deemed responsible for the incurred claim costs.

Providing a client/vendor a waiver of subrogation voids the insurance company’s right to subrogate against a third party. Some policies automatically include with a requirement

that you must have a written contract requiring you to provide this to a client/vendor prior to the loss.

Some policies require you to name the third party and might charge an additional premium.

Certificates of Insurance ACORD Certificates TREC Certificate WDI Certificate - (Texas Department Of

Agriculture)

Business Owners Policy (BOP) A general liability and property package

policy Can add in the following coverages:

Inland Marine Business Personal Property (BPP) 3rd Party Data Breach Hired/Non-Owned Auto

Property Coverages Inland Marine Coverage – Insurance for

portable property (i.e.: ladders, thermal imaging camera, smart phones, etc.)

Business Personal Property (BPP) Coverage – Insurance for stationary property at covered location. (i.e.: computers, office art work, desks, printers, etc.)

3rd Party Data Breach Coverage for lost and stolen sensitive

digital data of clients and vendors. (i.e.: credit card numbers, bank account numbers, etc.)

Hired/Non-Owned Auto Hired: Refers to autos the named insured leases,

hires, rents, or borrows. (does not include autos the named insured leases, hires, rents, or borrows from any of it’s employee’s)

Non-Owned: Refers to an auto that is used in connection with the named insured's business but that is not owned, leased, hired, rented, or borrowed by the named insured. As used in the business auto policy (BAP), the term specifically applies to vehicles owned by employees and used for company business.

(source: www.irmi.com)

WDI Inspectors Texas Department of Agriculture requires General

Liability. $200,000 for bodily injury and property damage

coverage with a minimum total annual aggregate of $300,000 for all occurrences limits

Care custody and control endorsement Pesticide applicator endorsement

Carriers provide coverage Some provide certificate if waiver is signed stating there

are no pest applications performed. Some provide the coverage as required by the state, but

exclude coverage for the home inspections.

Workers’ Compensation (Not CGL) Workers’ Compensation provides several benefits if an

inspector is injured on the job. Income benefits - (other than impairment income benefits)

replace a portion of any wages you lose because of a work-related injury or illness. Income benefits include temporary income benefits (TIBs); impairment income benefits (IIBs); supplemental income benefits (SIBs); and lifetime income benefits (LIBs).

Medical benefits - benefits pay necessary medical care to treat your work-related injury or illness.

Burial benefits pay for some of the deceased employee's funeral expenses to the person who paid the funeral expenses.

Death benefits replace a portion of lost family income for eligible family members of employees killed on the job.

(source: http://www.tdi.texas.gov/wc/employee/benefits.html)

Home Inspector Risk Management You have the option to turn away potential clients. Use signs to keep others from using your equipment,

following you in crawl spaces or up a ladder. Take as many pictures as you can. Use standard & consistent wording. Quote the SOPs on your report. Write down what you are missing/what you could not access. State how it LOOKS, not how it IS. Go over entire document with client. Always get a signed agreement. Save everything.

(Source: http://riskpro.us/wordpress/reduce-your-risk-of-a-home-inspector-lawsuit-part-1/)

Avoid a Lawsuit Refunding a home inspection is often

verbiage found in most inspection agreements to resolve a dispute about the performance of the home inspection.

If you are able to settle the matter by refunding the inspection fee, be sure and obtain a general release form.

Inspection Agreement Some insurance companies require you

have a signed agreement for coverage to even apply.

Underwriters strongly recommend always having the agreement signed because they have been able to avoid lawsuits from groundless claims by using the signed agreement and inspection report.

Include clauses where necessary Include all the areas that are necessary to

properly protect yourself, you should not be concerned about the inconvenience your client might feel by having to read several pages.

Always have it signed Programs like DocuSign can be used in

situations where the client is not available to sign the agreement in person.

Some insurance companies require you have a signed agreement for coverage to even apply.

Inspection Agreement

Conclusion New TREC requirements Coverage Features In Professional Liability Coverage Features In General Liability Other Possible Coverage options for HIs Tips and Hints to reduce your risk

Check out our blogs – www.riskpro.us/blog Questions?

Follow us Online Facebook: RISKPRO Insurance Agency, LLC Twitter: RISKPROInsAgy LinkedIn: RISKPRO Insurance Agency, LLC Blog: www.riskpro.us/blog Email: [email protected]

This presentation can be found online at:http://www.slideshare.net/GeraldBrunker/home-inspectors-insurance-risk-management-45195435