retailreimagined: thenewerafor customerexperience

TRANSCRIPT

Retail reimagined:The new era forcustomer experienceAugust 2020

2Periscope® byMcKinsey

In a matter of 90 days, we have vaulted forwardten years in United States e-commercepenetration.¹ Immersed almost exclusively in theimmediacy, convenience, availability, and safety ofdigital experiences for those twelve weeks,consumers reset their expectations andpreferences, and forced retailers to change theirtrajectory, priorities, and operating model.

Yet even as an economic downturn has putincreased pressure on retailers, this generation-shaping event has opened up entirely new frontsin the competition for customers. McKinseyresearch² has shown that in past recessions,companies that invest in and deliver superiorcustomer experience during a downturn emergefar stronger than their peers once the economyrebounds, producing shareholder returns threetimes larger than average.

To help retailers prioritize these efforts, Periscopeby McKinsey surveyed more than 2,500consumers in the United States, the UnitedKingdom, France, and Germany to understandhow consumer behavior is changing. We compiledthis research both prior to and during theshutdowns, looking at what changed and whattrends will likely stick in the next two months.Several core themes have become evident amongconsumers: a flight to online and omnichannel, ashock to loyalty, and convenience redefined withtechnology.

The key highlights of our findings appear in thefollowing pages.

¹ Aamer Baig, Bryce Hall, Paul Jenkins, Eric Lamarre, and Brian McCarthy, “The COVID-19 recovery will be digital: A plan for the first 90 days,”May 2020, McKinsey.com.

² Richard Dobbs, Tomas Karakolev, and Rishi Raj, “Preparing for the next downturn,” April 2007, McKinsey.com.

The COVID-19 pandemic isfirst and foremost a globalhumanitarian crisis that hasoverstretched health systems,challenged governments, andupended lives and livelihoods.

As the response and recovery to the pandemiccontinues, it has become clear that the crisis hasalso ushered in a new reality for consumers andretailers. The blow has been swift and vast,upending lives and livelihoods and upsettingeconomies. Some of the most dramatic effects havebeen to consumer behavior—how people buy, whatthey buy, and where they buy it.

In a matter of 90 days,we have vaulted forward

10yearsin consumer and businessdigital adoption

Executive Summary

USRespondents: 1,014

FranceRespondents: 512

GermanyRespondents: 527

UKRespondents: 504

46%

44%

32%

38%

During the last 2 months, when shopping for a specific category orproduct, have you switched from brands or retailers where youpreviously shopped?

Switching behavior

3Periscope® byMcKinsey

An end to ‘normal’ shopping decisions

40%of respondents said they triednew brands or made purchaseswith a new retailer

During the shutdown, with normal habits androutines knocked off course, consumers changedthe way they made purchasing decisions. In thefour countries we surveyed, 40 percent ofrespondents said they tried new brands or madepurchases with a new retailer. This was especiallyprevalent in the US, where 46 percent ofconsumers made a switch.

4Periscope® byMcKinsey

United States (n = 619)

Germany (n = 292)

United Kingdom (n = 314)

France (n = 317)

In a moment of great uncertainty, rather than sticking to familiarity andbrands they had used, consumers did the opposite.

Top 5 reasons for switching brands/retailers during shutdown, by country,% of respondents

Other answer choices included: special hours for high-risk groups. The importance of this choice remained below 20% across regions.

Offer lower prices

Offer relevant promotionsand messaging

Offer better price/value ratio

Offers ways to maintainsocial connections

Support employees

Donates to COVID-19relief efforts

Repurposing facilities

Communicates inpreferred channel

51 5246 48

27

1922

1521

14

45 4541

36

2126

21 1919 18

In a moment of great uncertainty, rather thansticking to familiarity and brands they had used,consumers did the opposite. This had a lot to dowith competitive pricing, what was in stock, andhow brands responded during this big moment. Forinstance, one of the biggest drivers for abandoningloyalty during the shutdown was items being out ofstock. Shoppers were also drawn to brands orretailers that supported their employees during thepandemic, such as by increasing their wages,giving extra sick leave, or paying employees for lostwages. In Germany and the US, consumers alsoswitched to brands and retailers that repurposed

their facilities to help slow the spread of the virusas well as those that led socially responsibleCOVID-19 initiatives. The North American apparelcompany Lululemon, for instance, responded to thecrisis by setting up a $2 million financial assistancefund for brand ambassadors who own a fitnessstudio. In the US, the Midwestern grocer Hy-Veepartnered with DoorDash to offer free grocerydeliveries to senior citizens, expectant mothers,and those considered at high risk for COVID-19.We see such purpose and branding fundamentalsas an increasingly important element for drivingfuture growth.

5Periscope® byMcKinsey

New e-commerce experience expectations

As expected, e-commerce spending experienceda major boost during the shutdowns even asoverall spending went down. In the United States,it was up more than 30 percent from thebeginning of March through mid-April, comparedto the same period the previous year.³ In all fourcountries surveyed, we observed higher shoppingactivity in several categories during shutdown.Categories with the biggest uptick were apparel(in the United States and United Kingdom),children’s products (United States, UnitedKingdom, Germany), beauty (United States), andgrocery (United States).

Some pre-crisis shopping features continued to beimportant, such as free delivery and returns as wellas fast delivery (one or two days). But a number ofother attributes skyrocketed in importance duringthe crisis. The need for informative productdescriptions and clear product images at a timewhen consumers couldn’t see, feel, or test productsin a store ranked as one of the top three factors for a

great online browsing experience in all the countrieswe surveyed, increasing in importance by 12 to 23percentage points, from pre- to post-shutdown.

Quick website loading also became critical. Asmillions of consumers started spending so much oftheir lives online, they became even less tolerant ofsites or apps that were slow to load or unresponsive.Post shutdown, the importance of this factor rosebetween ten to 15 percentage points, with UnitedKingdom shoppers being the least tolerant ofslow sites.

As brands vie for consumer attention in increasinglycompetitive digital environments, it is moreimportant than ever to build real engagement withcustomers and offer real value. Nike China, forexample, activated its digital community by offeringvirtual workouts and saw an 80 percent increase inweekly active users of its app.

³ Market research firm Rakuten Intelligence

6Periscope® byMcKinsey

Cleardescriptionand images

47

70

23pp

Works fast/loads quickly

42

57

15pp

Productreviews

33

52

18pp

Visuallyappealing

24

33

9pp

Easy tonavigate

4145

3pp

Easy tonavigate

40

49

10pp

Productreviews

39 42

3pp

Works fast/loadsquickly

29

41

12pp

Cleardescriptionand images

38

51

13pp

Easy tonavigate

43 42

-2pp

Cleardescriptionand images

43

56

13pp

Works fast/loadsquickly

39

53

15pp

Visuallyappealing

17

30

13pp

Productreviews

4145

4pp

Cleardescriptionand images

45

57

12pp

Productreviews

3743

6pp

Works fast/loadsquickly

32

43

10pp

Availability/stock issues

N/A

37

N/A

Availability/stock issues

N/A

30

N/A

Easy tonavigate

35

54

19pp

Great online browsing experience

USRespondents: 922

GermanyRespondents: 464

UKRespondents: 478

FranceRespondents: 459

1st run: Think about browsing/researching products in the online stores or mobile apps in the last3 months. In your opinion, which factors create a great online browsing experience?

2nd run: Think about browsing/researching products in the online commerce sites in the last 2 months.In your opinion, which factors create a great online browsing experience?

Other answer choices included: customer service phone/email, recognize me as returning user, productrecommendations, consistent across channels, product videos, virtual sampling/testing, other. Theimportance of these choices remained below 20% across regions.

Percentage point change values may have -/+1pp error because of rounding

1st run – early March 2020

2nd run – early June 2020

7Periscope® byMcKinsey

58 55

Freedelivery

and return

-3pp

Range ofpaymentoptions

4538

-7pp

Fastdelivery

4130

-11pp

Seamlesspurchase/checkout

N/A

27

N/A

No-questions-asked return

policy

N/A

39

N/A

62 60

Freedelivery

and return

-3pp

45 49

Fastdelivery

3pp

39 38

Loyaltycard offers

-1pp

28 27

Fastcheckout

-2pp

23 25

Abilityto savebasket

2pp

Great online purchasing experience

Freedelivery

and return

67 65

-2pp

Freedelivery

and return

63 62

-1pp

Fastdelivery

38 41

3pp

Fastdelivery

4148

6pp

Loyaltycard offers

3728

-9pp

Fastcheckout

3427

-6pp

No-questions-asked return

policy

N/A

25

N/A

Loyaltycard offers

3428

-6pp

Seamlesspurchase/checkout

N/A

27

N/A

Range ofpaymentoptions

28 24

-4pp

USRespondents: 922

GermanyRespondents: 461

UKRespondents: 478

FranceRespondents: 459

1st & 2nd run: Think about purchasing products in online stores or via mobile apps.What makes a great online buying experience?

Other answer choices included: range of delivery options, contactless delivery option, subscription optionthat automates checkout, other. The importance of these choices remained below 25% across regions.

Percentage point change values may have -/+1pp error because of rounding

1st run – early March 2020

2nd run – early June 2020

8Periscope® byMcKinsey

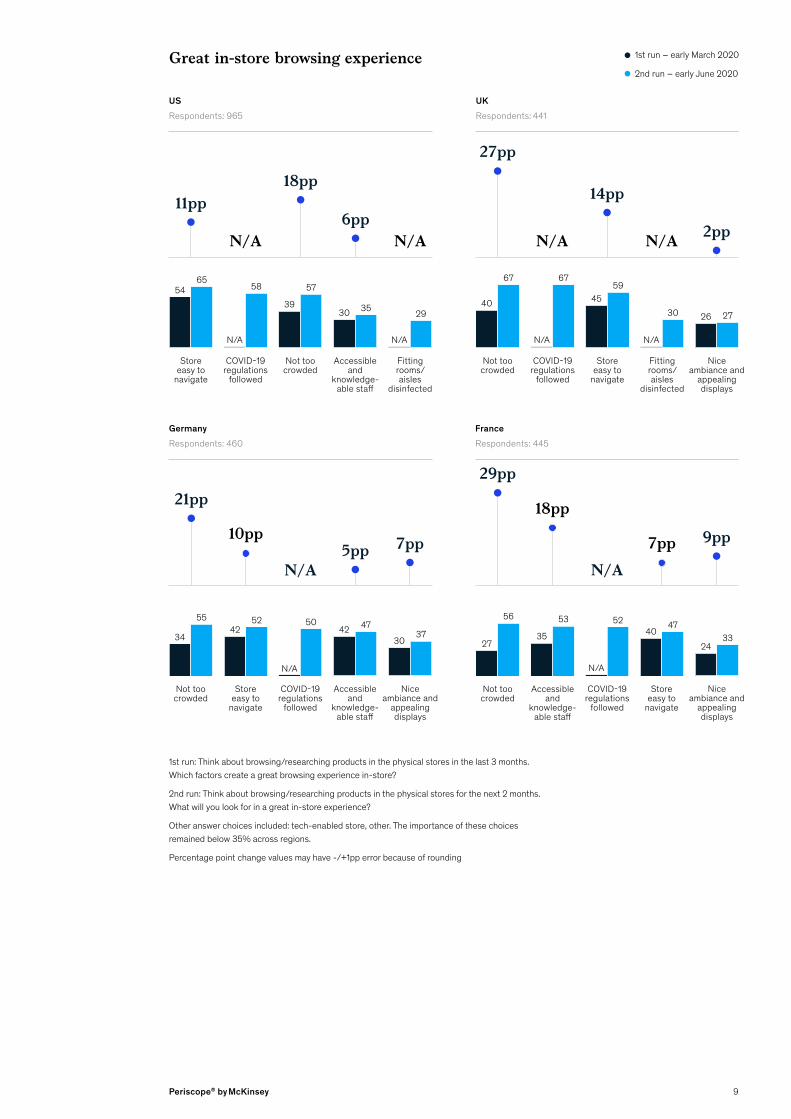

Safety and convenience critical forin-store experience

Amid the trauma and uncertainty of the COVID-19crisis, many people have entirely new concernsabout safety and hygiene. At least 50 percent ofour survey respondents said they want stores tofollow guidelines that will help keep shoppers andemployees safe, such as the installation ofplexiglass at the checkout and the use of masksand availability of hand sanitizers.

Most importantly, consumers noted theimportance of finding what they’re looking for.Organized and easy-to-navigate stores are evenmore appealing as many people seek to spend aslittle time as possible mingling with others inpublic spaces. The significance of this rose inevery country by seven to 14 percentage points inJune, as compared to March.

Also more valuable is the ability to do self-checkout. The appeal of this contactless means ofpurchasing rose between two and 12 percentagepoints in every country, with United Kingdomconsumers registering the highest increase.

In at least one way, stores still have a leg up overonline purchasing. Consumers in all four countriesrated social interactions with a helpful andknowledgeable staff as a top-three feature forbrowsing and making purchases in stores. In theUnited States, its importance rose ten percentagepoints for checkout and six percentage points forbrowsing following the crisis.

At least

50%of our survey respondents said theywant stores to follow guidelines thatwill help keep both shoppers andemployees safe

9Periscope® byMcKinsey

4252

Storeeasy tonavigate

10pp

4047

Storeeasy tonavigate

7pp

34

55

Not toocrowded

21pp

35

53

Accessibleand

knowledge-able staff

18pp

27

56

Not toocrowded

29pp

Great in-store browsing experience

Storeeasy tonavigate

5465

11pp

Storeeasy tonavigate

4559

14pp

Niceambiance andappealingdisplays

26 27

2pp

Niceambiance andappealingdisplays

3037

7pp

Niceambiance andappealingdisplays

2433

9pp

Not toocrowded

39

57

18pp

Accessibleand

knowledge-able staff

30 35

6pp

Accessibleand

knowledge-able staff

42 47

5pp

Not toocrowded

40

67

27pp

COVID-19regulationsfollowed

N/A

58

N/A

Fittingrooms/aisles

disinfected

N/A

29

N/A

COVID-19regulationsfollowed

N/A

50

N/A

COVID-19regulationsfollowed

N/A

52

N/A

COVID-19regulationsfollowed

N/A

67

N/A

Fittingrooms/aisles

disinfected

N/A

30

N/A

USRespondents: 965

GermanyRespondents: 460

UKRespondents: 441

FranceRespondents: 445

1st run – early March 2020

2nd run – early June 2020

1st run: Think about browsing/researching products in the physical stores in the last 3 months.Which factors create a great browsing experience in-store?

2nd run: Think about browsing/researching products in the physical stores for the next 2 months.What will you look for in a great in-store experience?

Other answer choices included: tech-enabled store, other. The importance of these choicesremained below 35% across regions.

Percentage point change values may have -/+1pp error because of rounding

10Periscope® byMcKinsey

64 63

Friendlystaff at

checkout

-1pp

6151

Fastcheckout

-10pp

43 44

Fastcheckout

1pp

6856

Rewardsand

discountsfor loyalty

-12pp

54 55

Friendlystaff at

checkout

1pp

Great in-store purchasing experience

Fastcheckout

59 58

-1pp

COVID-19regulationsfollowed

N/A

57

N/A

COVID-19regulationsfollowed

N/A

58

N/A

COVID-19regulationsfollowed

N/A

61

N/A

COVID-19regulationsfollowed

N/A

65

N/A

Fastcheckout

51 55

4pp

Friendlystaff at

checkout

3747

10pp

Self-checkout

3846

8pp

Self-checkout

18 20

2pp

Self-checkout

1926

7pp

Self-checkout

2941

12pp

Rewardsand

discountsfor loyalty

5142

-8pp

Rewardsand

discountsfor loyalty

37 35

-2pp

Rewardsand

discountsfor loyalty

5238

-14pp

Friendlystaff at

checkout

5043

-7pp

USRespondents: 965

GermanyRespondents: 441

UKRespondents: 460

FranceRespondents: 449

1st run: Now think about purchasing products in physical store. What makes a great buyingexperience in-store?

2nd run: Think about purchasing products in physical store. What are you looking for in yourbuying experience in-store?

Other answer choices included: pay with mobile, pausing cash payments, other. The importanceof these choices remained below 20% across regions.

Percentage point change values may have -/+1pp error because of rounding

1st run – early March 2020

2nd run – early June 2020

11Periscope® byMcKinsey

Limited in-store technologyfeatures available

The flight to digital and increased customerexpectations in stores have created newchallenges for how retailers serve their customers.To respond, retailers will need to utilize innovativein-store technologies that give shoppers a newlevel of convenience, a more personalizedexperience, and a greater integration of the offlineand online environments. This integration includestechnologies such as contactless paymentsystems, digital screens that offer in-storeshoppers certain features of online shopping, andaugmented reality (AR) systems for trying onclothing or testing products.

Unfortunately, many retailers have yet to progressvery far on this ambition. In the first run of oursurvey, more than 35 percent reported zeroexposure to any of the in-store technologies weasked about. Here are some of the most visibleand widespread among those with any visibleadoption at all:

— Mobile payments: The ability to pay with asmartphone is the most well-known in-storetechnology among consumers, yet retailers arenot doing a great job at encouragingcustomers to adopt it. Only 23 percentreported using or noticing it. Post-shutdown,consumer appetite for seeing or using thiscontactless form of payment in stores grew by13 percentage points in the United States andthe United Kingdom, and nine percentagepoints in Germany.

— Mobile preorders: The convenience andspeed of ordering digitally and then picking upat or just outside the store took on new appealduring the shutdown. In June, attractiveness ofthis option increased by 13 percentage pointsin the United States and the United Kingdomand eight percentage points among Frenchconsumers, as compared to March.

— Digital screen browsing. Kiosks or apps thatenable shoppers to easily browse products orcategories or customize products, or thatfeature navigation tools to help shoppers movethrough the store quickly, are also among thetechnologies most noticed or used by shoppers.

Key considerations

Amajority of shoppers said theyhaven’t encountered even the mosttalked-about or basic in-storetechnologies, and more than

35%reported zero exposure to any option

12Periscope® byMcKinsey

USRespondents: 1,027 Percentage point change

Percentage point change

Percentage point changeGermanyRespondents: 492

UKRespondents: 502

Interest in omnichannel technologies 1st run – early March 2020

2nd run – early June 2020

Mobile payments

Mobile app orders

Apps to scan barcodes

Self-identification at terminal

Digital screens to navigate

Digital screens for browsing

Digital shelf labels for info

AR to try on product

AR for product info

Location recognition

Mobile app orders

Mobile payments

Self-identification at terminal

Digital screens for browsing

Digital screens to navigate

Apps to scan barcodes

Digital shelf labels for info

Using an app to text customer service

Cashierless payment

Digital screens customization

Mobile payments

Self-identification at terminal

Apps to scan barcodes

Mobile app orders

Digital screens to navigate

Digital shelf labels for info

13pp

13pp

N/A

-1pp

N/A

-3pp

-2pp

1pp

1pp

3pp

13pp

13pp

1pp

-4pp

N/A

N/A

-3pp

N/A

5pp

0

13pp

3pp

N/A

2pp

N/A

-4pp

3017

1615

3420

2916

2816

1615

2815

2118

25

1613

2423

20

2526

1923

1917

22

17

18

2023

17

2021

1518

14

138

1313

13Periscope® byMcKinsey

Percentage point change

Percentage point change

GermanyRespondents: 492

FranceRespondents: 492

1sr run: Which of these did you find most helpful? Please select up to three.

2nd run: Which of the following communication/experience at retailers would you like to see/use in the near future?

Other answer choices included: tech-enabled sales personnel, biometric sensors for authentication. The importanceof these choices remained below 10% across regions.

Percentage point change values may have -/+1pp error because of rounding

Mobile app orders

Mobile payments

Self-identification at terminal

Digital screens for browsing

Digital screens to navigate

Apps to scan barcodes

Digital shelf labels for info

Using an app to text customer service

Cashierless payment

Digital screens customization

Mobile payments

Self-identification at terminal

Apps to scan barcodes

Mobile app orders

Digital screens to navigate

Digital shelf labels for info

Digital screens for browsing

AR to try on product

AR for product info

Cashierless payment

Mobile payments

Mobile app orders

Digital shelf labels for info

AR to try on product

Apps to scan barcodes

Self-identification at terminal

AR for product info

Using an app to text customer service

Digital screens to navigate

Digital screens customization

13pp

13pp

1pp

-4pp

N/A

N/A

-3pp

N/A

5pp

0

13pp

3pp

N/A

2pp

N/A

-4pp

-6pp

-2pp

-4pp

N/A

9pp

8pp

-8pp

3pp

N/A

-4pp

1pp

N/A

N/A

-3pp

2916

2213

2118

2113

20

2128

1917

2017

18

14

18

1620

1721

1313

1622

1617

1418

12

1716

14

1316

14Periscope® byMcKinsey

While disruption and fierce competition is certainly nothing newfor retailers, the pace and intensity of coronavirus-related changeis unprecedented. As retail leaders plot how they will bounce

back, they also need to lookbeyond the immediatechallenges and issues. Now isthe time to engage in criticallong-term planning to quicklyrecover revenue⁴ and acceleratefuture⁵ growth.

⁴ Brian Gregg, Eric Hazan, Rock Khanna, Aimee Kim, Jesko Perrey, and Dennis Spillecke,“Rapid revenue recovery: A road map for post-COVID-19 growth” May 2020, McKinsey.com.

⁵ Arun Arora, Peter Dahlström, Eric Hazan, Hamza Khan, and Rock Khanna, “Reimaginingmarketing in the next normal,” July 2020, McKinsey.com.

15Periscope® byMcKinsey

Delivering on omnichannel ambitions

This is a real moment not only of changingloyalties and a shifting leaderboard, but anopportunity to really connect with consumers innew ways as they reformulate their habits anddecision journeys.

In the short term, companies need a completeunderstanding of which new, COVID-19-era habitswill stick and which won’t, and for what segments.The surge in online shopping, for instance, is likelyto spur a sustained increase in buy online/pickupin-store options—roughly half of consumers whoused this option during the shutdown say theyintend to keep using it. To prepare for thisdemand, retailers will need to redirectmerchandise to specific stores, reallocateinventory between offline and online, orexperiment with “gray” or “dark” stores that maymimic actual stores but are used mainly forfulfillment and may never see consumers directly.It is yet another omnichannel concept that hasaccelerated during the pandemic.⁶ For example,during the shutdown, Levi’s used some of its

closed stores in the United States and the UnitedKingdom to fulfill online orders, helping boostdelivery efficiency and prevent overcrowding in itse-commerce fulfillment centers.

A critical component for delivering a greatomnichannel experience is being able to deliverhyperlocal and personalized experiences—both instore and online. This requires a deep andgranular understanding of the customer and theirdecision journey—from zip code to zip code, andcategory by category—to quickly identify andpredict where demand is going to surge or not. Asconsumers navigate new routines, retailers andbrands have a unique opportunity to meet thisdemand with the right targeting, messaging,content, and customer promise. During theshutdown, between 12 and 21 percent of surveyrespondents said they switched to brands thatsent them relevant messages or promotions intheir preferred channel.

⁶ Manik Aryapadi, Ashutosh Dekhne, Wolfgang Fleischer, Claudia Graf, and Tim Lange, “Supply chain of the future: Key principles in buildingan omnichannel distribution network,” January 2020, McKinsey.com.

16Periscope® byMcKinsey

Rebooting loyalty online

With customers eager to try other brands andstores, this is a once-in-a-generation chance forretailers to recapture and win back customers. It’snow more important than ever that digitalexperiences be truly “zero friction,” deliveringconsistently on attributes consumers care mostabout: free and fast delivery and returns, clear anddetailed product descriptions and images, andquick page loading.

To create dynamic loyalty programs, companiesneed to develop an underlying consumer-loyaltystrategy that transcends the “earn and burn”discount programs of the past. The use of loyaltyprograms has been stuck around 50 percent foryears. The evolution to next-generation programsis essential for boosting customer engagement.Programs that balance monetary rewards withexperiential offerings designed to makeconsumers feel special and recognized (such asexclusive events, early access, unique discoveries)can provide real value and appeal to a consumer’shead and heart. To keep loyal customers engagedduring a period of minimal air travel, AlaskaAirlines created an email campaign for its loyalcustomers that offered extra miles through a “buynow, fly later” promotion.

Some brands will want to go even further andpursue partnerships with other consumer brandsto develop a joint loyalty ecosystem around aunifying customer value proposition. Footwearretailer DSW, for example, partnered with grocerychain Hy-Vee to sell shoes at the grocer’sextensive network of locations, giving the footwearretailer additional customers and Hy-Vee anopportunity for incremental sales. In Paris, Frenchretailer Carrefour partnered with Uber Eats to offergrocery delivery to customers in the region.

12-21%of survey respondents said theyswitched to brands that sent themrelevant messages or promotions intheir preferred channel

17Periscope® byMcKinsey

Reimagining the in-store experience

Now that most stores are open for business again,how do you make people really want to shop inthem? To start, every retailer needs a clear andcomprehensive plan for addressing concernsabout safety and hygiene, which aren’t going awayanytime soon. This means enabling safe physicaldistancing, sanitizing surfaces and products, andcommunicating proactively, clearly, andempathetically. Retailers will need to strike adelicate balance between enabling the socialinteractions that shoppers find valuable and beingresponsive to heightened concerns aboutpersonal health. Widespread adoption of mobiletechnologies for contactless payment and quickstore navigation will help in creating a morehygienic and convenient shopping experience.

Beyond the current crisis concerns, retailersshould consider adopting the right technology tomake stores more compelling and useful. Thiscould mean giving sales associates digital devicesand tools to enable them to better help customersfind what they need, offering shoppers productrecommendations on the next product to buy, ormaking phones and mobile apps a useful part ofthe shopping experience.

Such technology not only provides next-levelcustomer experience; it also gives retailers accessto valuable data that can feed into personalizationalgorithms or be used to optimize prices andpromotions. Stores can also optimize theirexperience not just for consumers, but for thegrowing number of online order pickers, forexample by featuring “fast zones” of popularonline items at the front of the store. Yet this storeof the future can’t wait until tomorrow. Retailersshould consider moving quickly to startreinventing the customer experience now.

Consumers have been wrestling with uncertainty through theCOVID-19 crisis. But their expectations for their retailexperience—both online and in-store—continue to be high.Retailers that can adapt quickly enough will be well positionedwhen the recovery comes.

18Periscope® byMcKinsey

About our surveys

In early March, Periscope by McKinsey fieldedconsumer surveys across the United States, theUnited Kingdom, Germany, and France with morethan 2,500 consumers to understand what theyvalue most in digital and in-store experiences, aswell as among the retail technologies that tie thetwo together. To see the impact of COVID-19 on

consumer preferences and behavior, the surveywas repeated in mid-June. The surveys wereconducted online in local languages. In eachcountry, results are sampled and weighted for arepresentative balance of the consuming class,based on variables including age andsocioeconomic status.

About Periscope®by McKinsey

Founded in 2007, the Periscope by McKinseyplatform combines world-leading intellectualproperty, prescriptive analytics, and cloud-basedtools with expert support and training. It is a uniquecombination that drives revenue growth, both nowand into the future. The platform offers a suite ofMarketing & Sales solutions that accelerate andsustain commercial transformation for businesses.Periscope leverages its world-leading IP (especiallyfrom McKinsey but also from other partners) andbest-in-class technology to enable transparencyinto big data, actionable insights, and new ways ofworking that drive lasting performanceimprovement and a sustainable two to seven

Contributors: Brian Elliott, Sajal Kohli, Kelsey Robinson, and Jamie Wilkie

percent increase in return on sales (ROS). With atruly global reach, the portfolio of solutionscomprises Insight Solutions, Marketing Solutions,Customer Experience Solutions, CategorySolutions, Pricing Solutions, Performance Solutions,and Sales Solutions. These are complemented byongoing client service and custom capability-building programs.

To learn more about how Periscope’ssolutions and experts are helping businessescontinually drive better performance, visitMcKinsey.com/Periscope or contact us [email protected].

Kelly UngermanDrives transformations forsales and marketingorganizations by findinglong-term potential.

Brian RuwadiAdvises large-scaleperformancetransformations thatdrives growth.

Eric HazanBrings extensiveknowledge of strategicmarketing and digitaltransformations.

Lars FiedlerBrings innovativemarketing solutions andstrategies to companiesacross B2C sectors.

The authors