retail industry tax update

TRANSCRIPT

© Grant Thornton LLP. All rights reserved.

CPE Credit is not available for viewing archived programs.Please visit http://www.grantthornton.com/events for upcoming programs.

Retail Industry Tax Update

Original Broadcast Date: October 2013

© Grant Thornton LLP. All rights reserved. 2

Giles SuttonPartnerState and Local TaxDallas, Texas

Presenters

Bill StickneyPartnerCorporate TaxPhiladelphia, Pa.

© Grant Thornton LLP. All rights reserved. 3

Guest presenters

Mark SullivanRetail Industry Practice Leader Chicago, Ill.

Jim WittmerRegional partnerStrategic Federal Tax ServicesPhiladelphia, Pa.

© Grant Thornton LLP. All rights reserved. 4

• Explain how the newly released repair regulations impact retailers

• Identify emerging trends retailers face, including multichannel retailing and global supply chain issues and explain related tax implications

• Identify valuable tax credits available to retailers • Explain which operational issues are the biggest

concern to retailers today

Retail Industry Tax UpdateLearning objectives

© Grant Thornton LLP. All rights reserved. 5

Retail Industry Tax UpdateAgenda

• Tax update for Retail• Federal legislative update• Repair Regs: What has changed?

© Grant Thornton LLP. All rights reserved. 6

Current Retail Operational Issues

• Current Operational Issues facing retailers– Multichannel issues– Global supply chain– Technology driven centralization– Cost rationalization

© Grant Thornton LLP. All rights reserved. 7

Current Operational Issues in Retail Multichannel Issues

• What's the issue?•28% growth in online sales in 2012 over 2011.

•Triple-digit year-over-year growth in sales through mobile and tablet devices.

•46% of U.S. consumers use their smartphones to check prices and reviews while shopping at retail stores, then nearly half buy a less expensive product elsewhere.

•Emergence of "omnichannel" retailing (a unified view of the brand in the marketplace).

© Grant Thornton LLP. All rights reserved. 8

Current Operational Issues in Retail Multichannel Issues (continued)

• Why is it important for retailers?

– Retailers can not grow or be competitive if they depend solely on in-store retailing.

– Brands get separated from the in-store experience. 90% of consumers trust peer recommendations through social media, only 14% trust ads.

– When physical stores, online/social media and mobile technologies work cohesively (omnichannel retailing), sales can skyrocket.

• How are retailers responding?

– Analytics solutions – Social media risk assessment– Integration: In-store, online and

mobile point of sale (POS) systems; controls for managing functions that overlap between online and in-store; policies for returns and responding to customer requests.

© Grant Thornton LLP. All rights reserved. 9

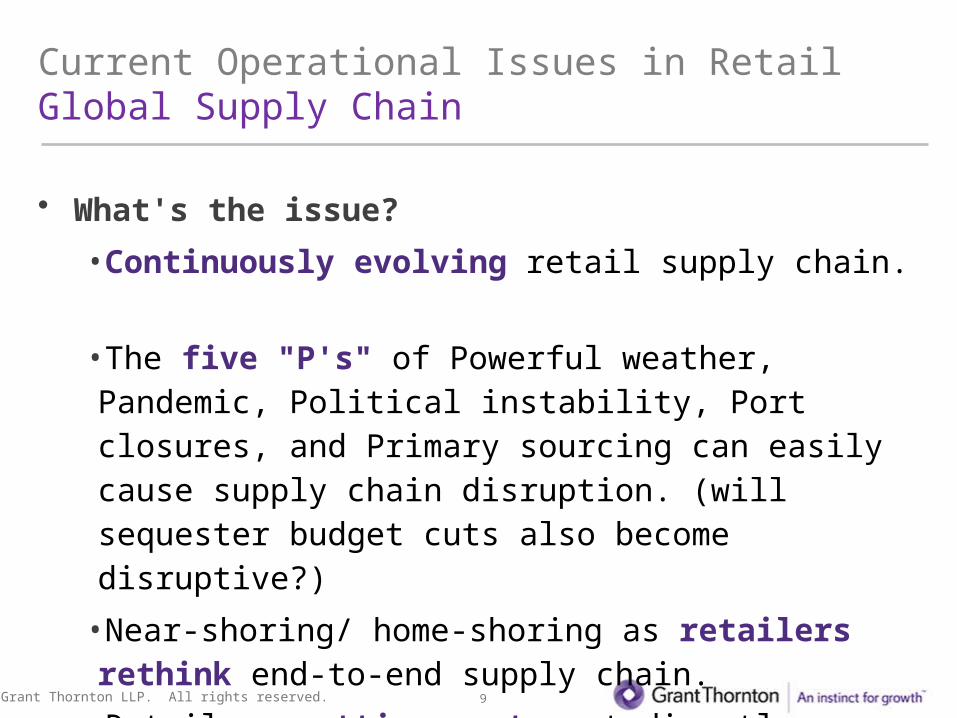

Current Operational Issues in Retail Global Supply Chain

• What's the issue?

•Continuously evolving retail supply chain.

•The five "P's" of Powerful weather, Pandemic, Political instability, Port closures, and Primary sourcing can easily cause supply chain disruption. (will sequester budget cuts also become disruptive?)

•Near-shoring/ home-shoring as retailers rethink end-to-end supply chain.

•Retailers cutting costs not directly related to the customer experience, especially in the supply chain.

© Grant Thornton LLP. All rights reserved. 10

Current Operational Issues in Retail Global Supply Chain (continued)

• Why is it important for retailers?

– Supply chain fraud and theft of intellectual property in a global supply chain.

– Smooth operations , especially when costs are being cut .

– Adapting to multichannel retailing.

• How our retailers responding?– Risk management – financial,

operational, compliance (California Transparency in Supply Chain Act, Conflict Minerals, etc.)

– Forensic, Investigative and Dispute services

– IT selection and implementation -- solutions to manage supply chain risks (data security, supply chain disruptions/business continuity, inventory management)

– Tax transfer pricing

© Grant Thornton LLP. All rights reserved. 11

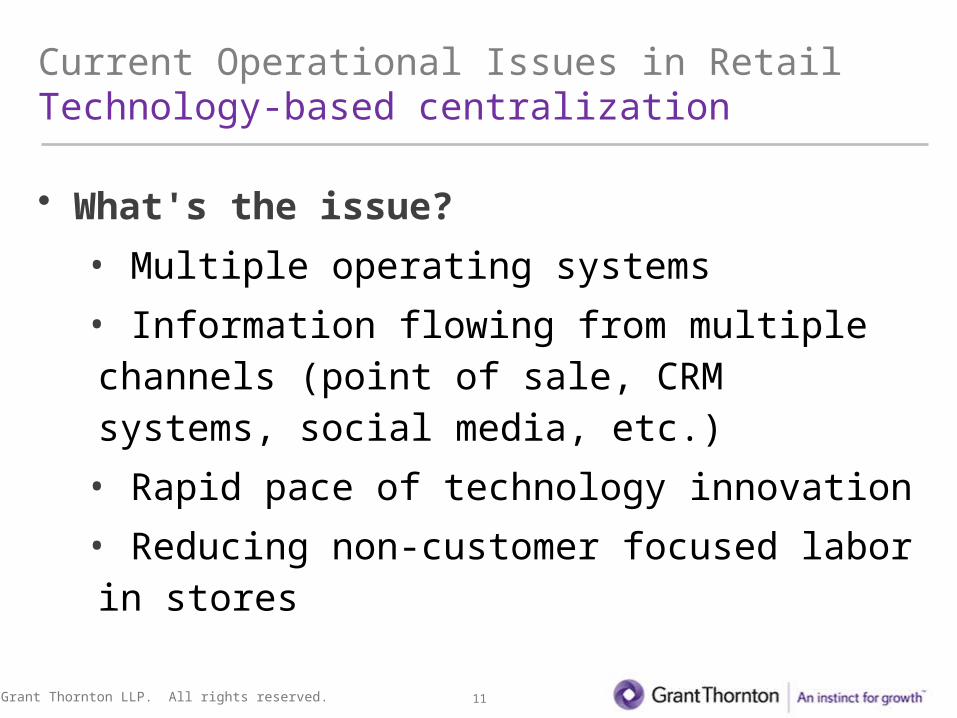

Current Operational Issues in Retail Technology-based centralization

• What's the issue?

• Multiple operating systems

• Information flowing from multiple channels (point of sale, CRM systems, social media, etc.)

• Rapid pace of technology innovation

• Reducing non-customer focused labor in stores

© Grant Thornton LLP. All rights reserved. 12

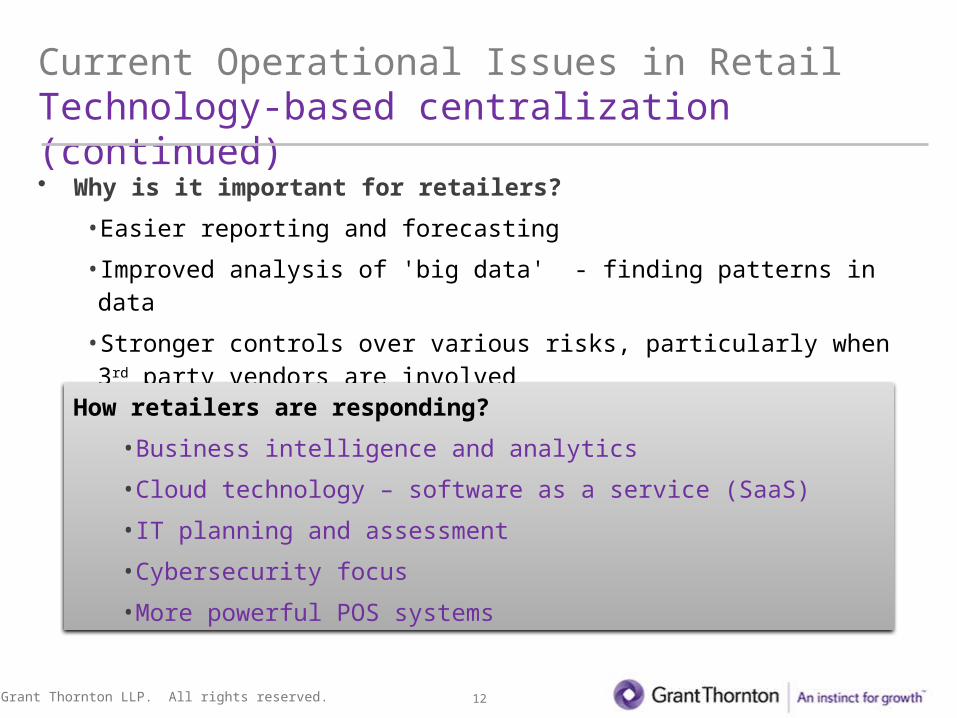

Current Operational Issues in Retail Technology-based centralization (continued)

• Why is it important for retailers?

•Easier reporting and forecasting

•Improved analysis of 'big data' - finding patterns in data

•Stronger controls over various risks, particularly when 3rd party vendors are involved

How retailers are responding?

•Business intelligence and analytics

•Cloud technology – software as a service (SaaS)

•IT planning and assessment

•Cybersecurity focus

•More powerful POS systems

© Grant Thornton LLP. All rights reserved. 13

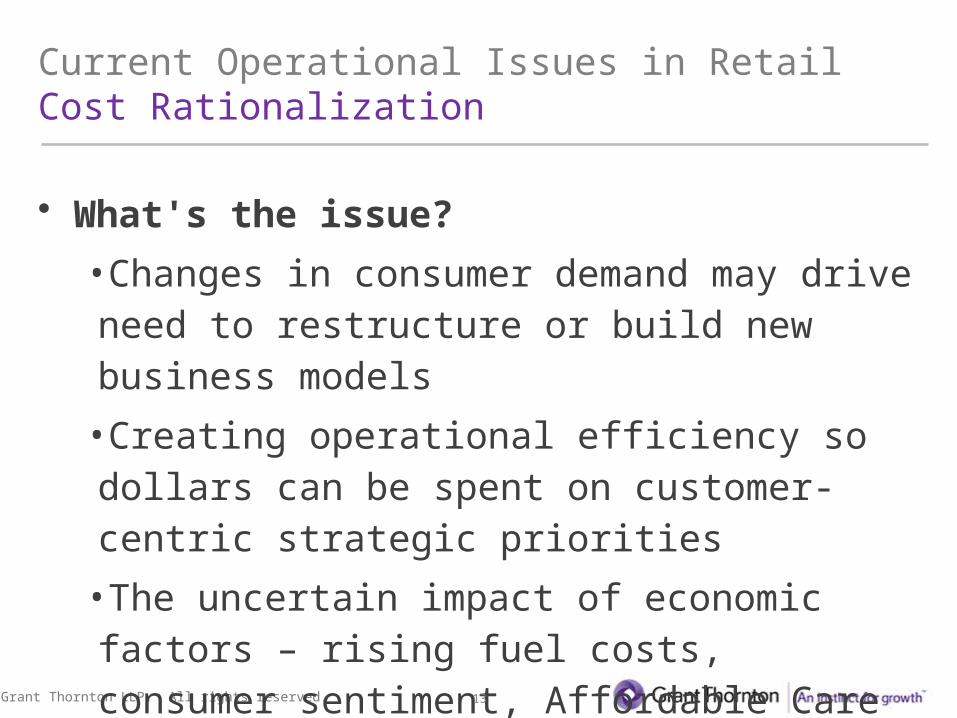

Current Operational Issues in Retail Cost Rationalization

• What's the issue?

•Changes in consumer demand may drive need to restructure or build new business models

•Creating operational efficiency so dollars can be spent on customer-centric strategic priorities

•The uncertain impact of economic factors – rising fuel costs, consumer sentiment, Affordable Care Act and other regulatory factors, etc.

© Grant Thornton LLP. All rights reserved. 14

Current Operational Issues in Retail Cost Rationalization (Cont.)

• Why is it important for retailers?

•Reducing costs without losing competitive edge or marketplace differentiation

•Need to invest in technology that will propel the company into the future

•Slow growth forecast for 2013

How are retailers responding?

•IT planning and assessment, cloud technology – software as a service(SaaS)

•Focus on financing arrangements/securitizing receivables to lower borrowing costs

•Restructuring to reduce tax costs

•Seeking performance improvement

•Effectively dealing with health care reform

© Grant Thornton LLP. All rights reserved. 15

Retail – State Tax Issues

– Sales tax systems and POS changes

– Outsourcing– C&I and purchased credits– Gross receipts taxes– Sales tax procurement

structures & cloud computing

– Sales taxation of services– Entity rationalization– Leverage Planning– NOL Utilization– Group Reporting Issues

© Grant Thornton LLP. All rights reserved. 16

Current Retail SALT Issues Procurement Structures & Cloud Computing

• Retailers are a large consumers of software and cloud-type products– It helps to manage IT costs

• Identifying tax issues and solutions around such transactions are, and will be, important to the retail community

• Procurement structures can often help – the objective:– Owning the tax determinations pertaining to cloud

purchases

© Grant Thornton LLP. All rights reserved. 17

Current Retail SALT Issues Entity Rationalization

• Entity simplification• Supply chain orientation• Off-shore planning• Unitary determinations

– Instant unity (for M&A transactions)– Treatment of foreign source income– 80/20– Water's-edge elections

© Grant Thornton LLP. All rights reserved. 18

Current Retail SALT Issues Complexity of Tax Regimes Impacting Retailers

• Extra-Jurisdictional reaches (Chicago/Illinois)• Sales tax holidays• Bag taxes• Food stamp transactions• Gross receipts taxes

– State (CAT, B&O, Delaware, TX Margins)– Local (San Francisco, Philadelphia, BPOL)– Local sales taxes (origin vs destination sourcing)

• Reduction in collection allowances• Transaction taxes should be transparent, fair, easy to administer

and understandable!

© Grant Thornton LLP. All rights reserved. 19

Current Retail SALT Issues The Changing Face of Nexus

• What is the current nexus standard?– Known nexus standards

• Physical presence (Quill)• Agency nexus• Bright line nexus• "Amazon" agency + bright-line nexus

– New "click-through" nexus regimes in 2013: KS, ME, IA and MO• KS law broadens the "agency" type relations the will create nexus for a remote

seller including another person (including unrelated 3rd parties) that uses trademarks, trade names, or service marks in the state similar to those used by the retailer

– Public contracting laws (KS and IA) – a retailer selling to state agencies, must register as must their retail affiliates must registers for sales and use tax

– Remote seller notice requirement (KY) – Unitary nexus (WV) effectively expanding the definition of "retailer engaging in

business in this state" to certain related members of a unitary group

© Grant Thornton LLP. All rights reserved. 20

Current Retail SALT Issues The Changing Face of Nexus

• Gift cards– What if they really don't know where the gift cards are

going (due the use of 3rd part distributors)– Do gift cards create physical presence nexus?

• Big box, specialty, e-commerce– What is fairness?

• Big box - cutting deals with states (credits) and local jurisdictions (incentives)

• Specialty – (de minimis credits)• E-commerce /small business (just liabilities?)

© Grant Thornton LLP. All rights reserved. 21

Retail Industry Tax Update WebcastAgenda

• Tax update for Retail• Federal legislative update• Repair Regs: What has changed?

© Grant Thornton LLP. All rights reserved. 22

Federal Legislative Update

• Section 336(e) Regulations Issued• IRS Guidance Issued after Supreme Court Strikes Down

DOMA• Other Items You May Have Missed

22

© Grant Thornton LLP. All rights reserved.

Federal Legislative Update – Section 336(e) Regs.

23

What is the effect of a Sec. 336(e) election?

Who makes the election?

What is the effective date of the regulations?

See T.D. 9619 for details.

© Grant Thornton LLP. All rights reserved. 24

Federal Legislative Update – IRS Issues DOMA Guidance

The Supreme Court held that section 3 of the

Defense of Marriage Act (DOMA) was unconstitutional.

What are the implications?

What did the IRS recently decide?

What should or can employers do?

© Grant Thornton LLP. All rights reserved. 25

Federal Legislative Updates – Items You May Have Missed

25

What happened?

• IRS will no longer issue Section 355 comfort letters• Deduction denied for costs associated with stock

offering• IRS cuts refundable corporate AMT credit

© Grant Thornton LLP. All rights reserved. 26

Retail: Current Federal IssuesFederal Tax Credits

• Certain federal tax credits are applicable and very attractive to retailers, such as:– R&D– IRC Sec. 45B (Restaurant retail)– IRC Sec. 49O (limited

applicability)

© Grant Thornton LLP. All rights reserved. 27

Retail: Current Federal IssuesRetail M&A Issues

• There is a fair amount of retail M&A going on– Buying concepts out of distressed position– Buying assets– Buying smaller innovative e-commerce plays

• Tax planning opportunities– Transaction cost analysis– Post acquisition integration– Attribute analysis

27

© Grant Thornton LLP. All rights reserved. 28

Retail Industry Tax Update WebcastAgenda

• Tax update for Retail• Federal legislative update• Repair Regs: What has changed?

© Grant Thornton LLP. All rights reserved.

What was issued?

• Final regulations under 162 and 263(a)

– Amounts paid to acquire, produce, or improve tangible property

• Re-proposed regulations under 168

– General asset accounts and disposition of depreciable property

• IRS and Treasury expect to finalize these regulations in 2014

© Grant Thornton LLP. All rights reserved.

Repair regulations: What has changed?Agenda

• Improvements to tangible property

• Dispositions

• De Minimis

• Materials and supplies

• Effective dates

© Grant Thornton LLP. All rights reserved.

A TP must generally capitalize an amount that IMPROVES a unit of property ("UOP") if the amount:

(1) Is for a betterment;

(2) Restores the UOP; or

(3) Adapts the UOP to a new or different use.

Improvements to propertyGeneral rule

© Grant Thornton LLP. All rights reserved.

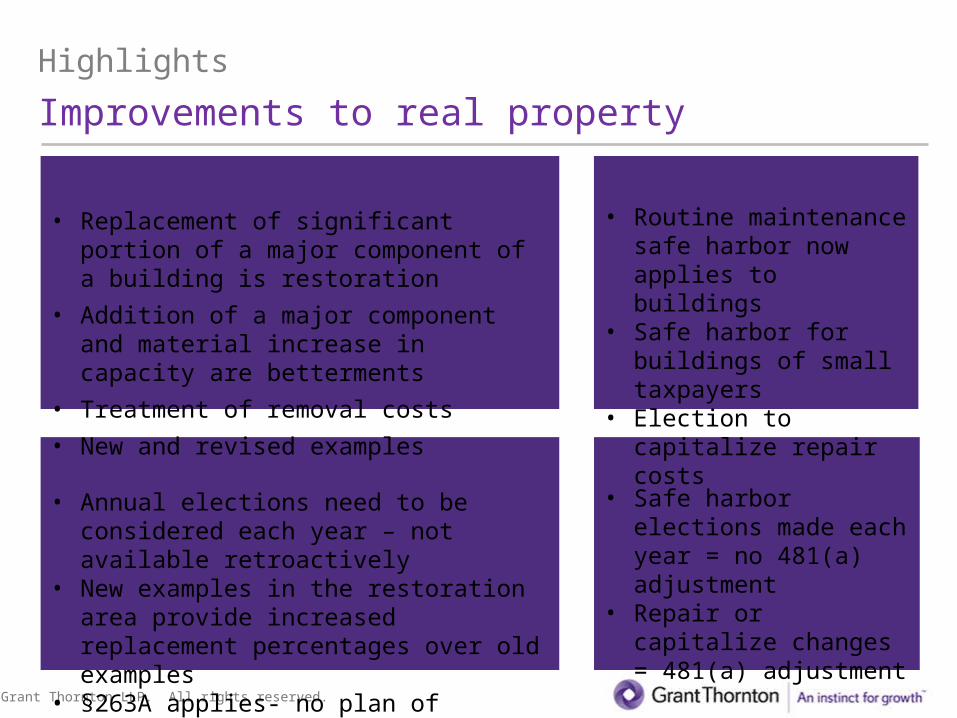

Highlights

Improvements to real property

Issues and opportunities• Annual elections need to be considered

each year – not available retroactively• New examples in the restoration area

provide increased replacement percentages over old examples

• §263A applies- no plan of rehabilitation

What's the effect?• Safe harbor elections

made each year = no 481(a) adjustment

• Repair or capitalize changes = 481(a) adjustment

New elections• Routine maintenance

safe harbor now applies to buildings

• Safe harbor for buildings of small taxpayers

• Election to capitalize repair costs

Significant changes• Replacement of significant portion of a

major component of a building is restoration

• Addition of a major component and material increase in capacity are betterments

• Treatment of removal costs

• New and revised examples

© Grant Thornton LLP. All rights reserved.

Highlights

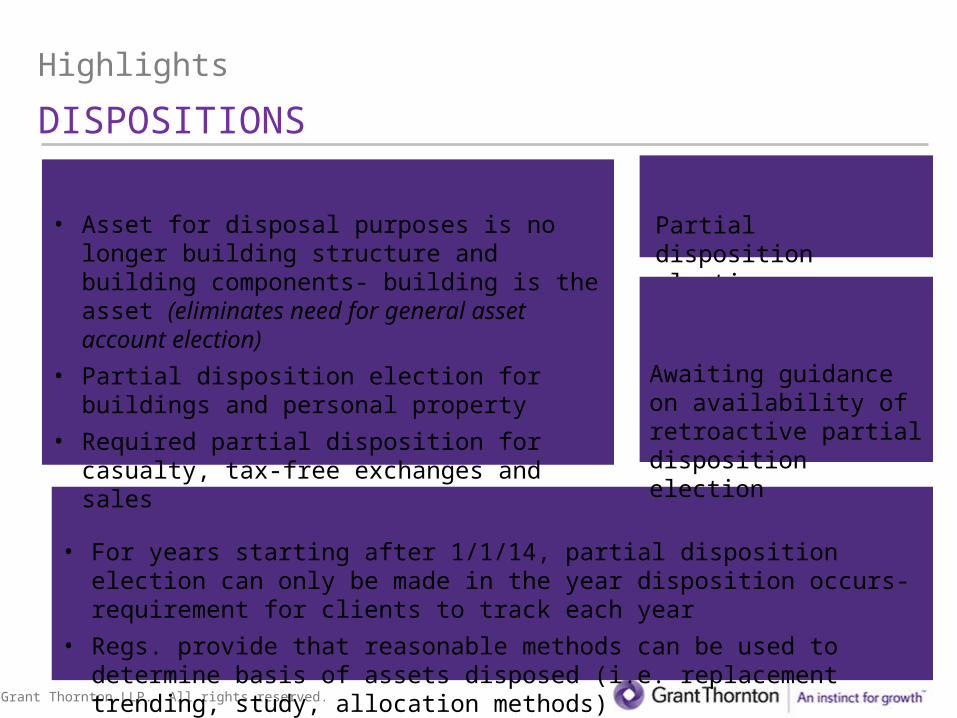

DISPOSITIONS

Issues and opportunities• For years starting after 1/1/14, partial disposition election can only be made in

the year disposition occurs- requirement for clients to track each year

• Regs. provide that reasonable methods can be used to determine basis of assets disposed (i.e. replacement trending, study, allocation methods)

New elections

Partial disposition election

What's the effect?

Awaiting guidance on availability of retroactive partial disposition election

Significant changes• Asset for disposal purposes is no longer building

structure and building components- building is the asset (eliminates need for general asset account election)

• Partial disposition election for buildings and personal property

• Required partial disposition for casualty, tax-free exchanges and sales

© Grant Thornton LLP. All rights reserved.

Highlights

DE MINIMIS

Issues and opportunities• Election must be made each year- statement attached to return• Taxpayers without audited financial statements can now take advantage of

a de minimis deduction• Written accounting policy must be in place on first day of taxable year to

which election applies• Amounts not subject to de minimis must meet clear reflection or capitalize

New elections

De Minimis safe harbor

What's the effect?Only applies to amounts incurred in the year adopted: no retroactive adjustment

Significant changes• No ceiling limit or tracking requirement• Safe harbor based on invoice/item price:

– TP w/AFS = $5,000– TP w/o AFS = $500

• Includes transaction costs and other costs of acquisition (i.e. labor and OH)

• If elected, applies to all materials and supplies

© Grant Thornton LLP. All rights reserved.

Highlights

MATERIALS AND SUPPLIES

Issues and opportunities• Clear definition of materials and supplies

• Can elect to deduct under de minimis, applies to all eligible materials and supplies

New elections

Election to capitalize now only applies to rotable, temporary or emergency spare parts

What's the effect?

Final regulations only apply to amounts incurred on or after 1/1/14, unless early adopt.

No retroactive adjustment

Significant changes

• Definition now includes property with acquisition or production cost of $200 or less (increased from $100)

• Definition of emergency spare parts

© Grant Thornton LLP. All rights reserved.

Transitional rules

• Revenue procedures expected to be issued late October or November

• Expected to provide for late partial disposition election for 2012, 2013, and 2014 tax years

• Will provide guidance on changes made under the temporary regulations

© Grant Thornton LLP. All rights reserved.

Effective dates

• Final and re-proposed regulations effective for years beginning on or after January 1, 2014

• TP may choose to apply the final, reproposed, temporary or any combination thereof for 2012 and 2013

• Transitional relief for elections in 2012 and 2013

© Grant Thornton LLP. All rights reserved. 38

Comments?Questions?

38

© Grant Thornton LLP. All rights reserved. 39

ContactInformation

Giles SuttonPartnerState and Local [email protected]

Bill StickneyPartnerCorporate [email protected]

Mark SullivanRetail Industry Practice Leader [email protected]

Jim WittmerRegional partnerStrategic Federal Tax [email protected]

© Grant Thornton LLP. All rights reserved.

The foregoing slides and any materials accompanying them are educational materials prepared by Grant Thornton LLP and are not intended as advice directed at any particular party or to a client-specific fact pattern. The information contained in this presentation provides background information about certain legal and accounting issues and should not be regarded as rendering legal or accounting advice to any person or entity. As such, the information is not privileged and does not create an attorney-client relationship or accountant-client relationship with you. You should not act, or refrain from acting, based upon any information so provided. In addition, the information contained in this presentation is not specific to any particular case or situation and may not reflect the most current legal developments, verdicts, or settlements.

You may contact us or an independent tax advisor to discuss the potential application of these issues to your particular situation. In the event that you have questions about and want to seek legal or professional advice concerning your particular situation in light of the matters discussed in the presentation, please contact us so that we can discuss the necessary steps to form a professional-client relationship if that is warranted. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein.

© 2013 Grant Thornton LLP, the U.S. member firm of Grant Thornton International. All rights reserved. Printed in the U.S.A. This material is the work of Grant Thornton LLP, the U.S. member firm of Grant Thornton International, Ltd.

* * * * * * * * * * * * * * * * * * * * * *IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the U.S. Internal Revenue Service, we inform you that any U.S. federal tax advice contained in this PowerPoint is not intended or written to be used, and cannot be used, for the purpose of (a) avoiding penalties under the U.S. Internal Revenue Code or (b) promoting, marketing or recommending to another party any transaction or matter addressed herein.

* * * * * * * * * * * * * * * * * * * * * *

Disclaimer

© Grant Thornton LLP. All rights reserved.

Thank you for viewing this presentation.

Visit us online at:

www.GrantThornton.com

twitter.com/GrantThorntonUS

linkd.in/GrantThorntonUS