results presentation 31 december 2018 andi case …...at 31 december balance sheet andi case and...

TRANSCRIPT

Results Presentation

31 December 2018

Andi Case and Jeff Woyda

11 March 2019

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20182

Agenda

1Financial results

2Markets

3Outlook

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20183

Financial results

Jeff WoydaChief Financial Officer and Chief Operating Officer

to 31 DecemberResults summary

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20184

2018

£m

2017

£m

Revenue 337.6 324.0

Underlying profit before taxation

(Before acquisition related costs)

45.3 50.2

Underlying earnings per share

(Before acquisition related costs)

105.2p 116.8p

to 31 DecemberResults summary

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20185

2018

£m

2017

£m

Revenue 337.6 324.0

Underlying profit before taxation

(Before acquisition related costs)

45.3 50.2

Acquisition related costs (2.4) (4.8)

Profit before taxation

(After acquisition related costs)

42.9 45.4

Underlying earnings per share

(Before acquisition related costs)

105.2p 116.8p

Revenue, profit and marginSegmental performance

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20186

Revenue

2018

£m

Revenue

2017

£m

Profit

2018

£m

Profit

2017

£m

Margin

2018

Margin

2017

Broking 251.7 238.9 44.0 43.9 17.5% 18.4%

Financial 46.1 52.0 8.0 10.1 17.4% 19.4%

Support 23.9 18.5 2.3 2.1 9.6% 11.4%

Research 15.9 14.6 5.0 4.8 31.4% 32.9%

to 31 December

*Assuming no further acquisitions, this should amount to a £1.7m in 2019

Acquisition related costs*

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20187

2018

£m

2017

£m

Cash and share-based payment charges 0.7 0.9

Loan note interest – 0.3

Amortisation – Platou 1.7 3.6

Total 2.4 4.8

at 31 DecemberBalance sheet

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20188

2015

£m

2016

£m

2017

£m

2018

£m

Tangible fixed assets 33.1 33.0 33.3 29.3

Intangible fixed assets (Software only) - - 1.5 5.4

Investments 1.9 4.1 4.9 4.8

35.0 37.1 39.7 39.5

Working capital (7.1) (15.1) (0.4) 17.5

Net available funds 91.6 98.4 79.1 73.4

84.5 83.3 78.7 90.9

Pensions (4.1) 2.3 12.3 14.0

Deferred tax 8.4 7.1 4.6 2.2

Loan notes (46.1) (23.6) – –

Net assets before intangibles 77.7 106.2 135.3 146.6

Intangibles (excl Software above) 263.2 300.5 288.1 288.0

Net assets 340.9 406.7 423.4 434.6

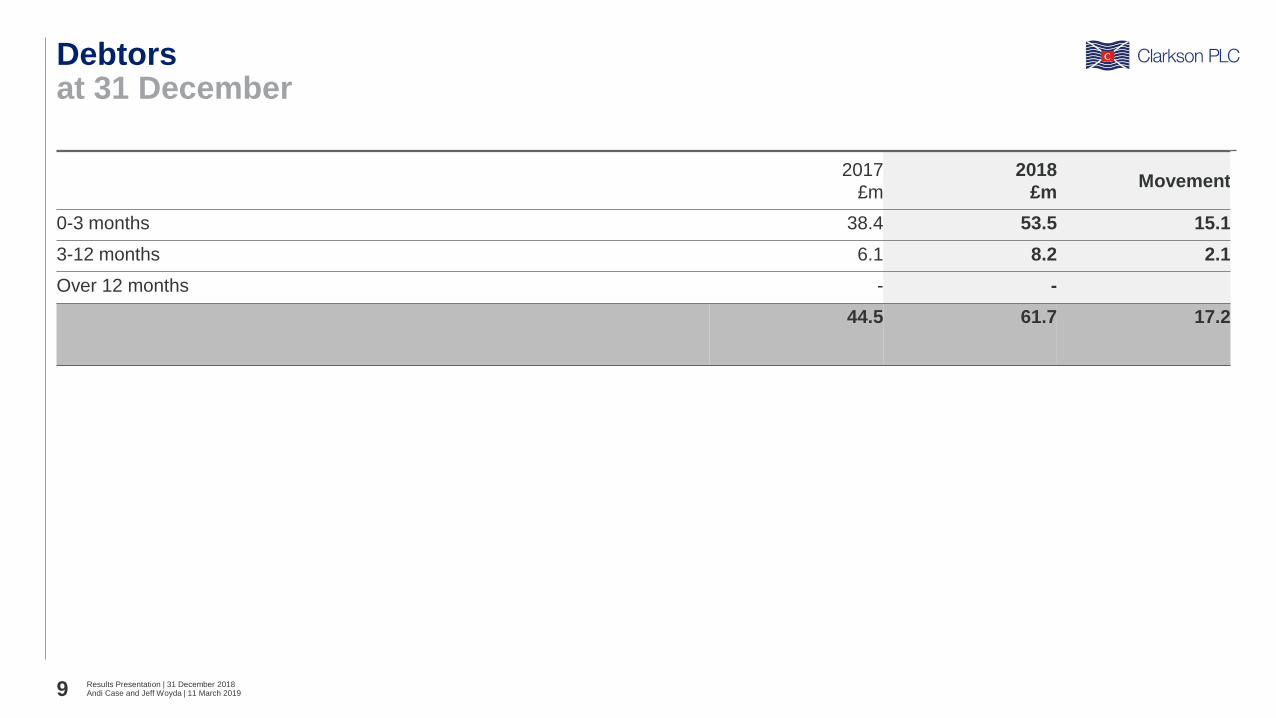

at 31 DecemberDebtors

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 20189

2017

£m

2018

£mMovement

0-3 months 38.4 53.5 15.1

3-12 months 6.1 8.2 2.1

Over 12 months - -

44.5 61.7 17.2

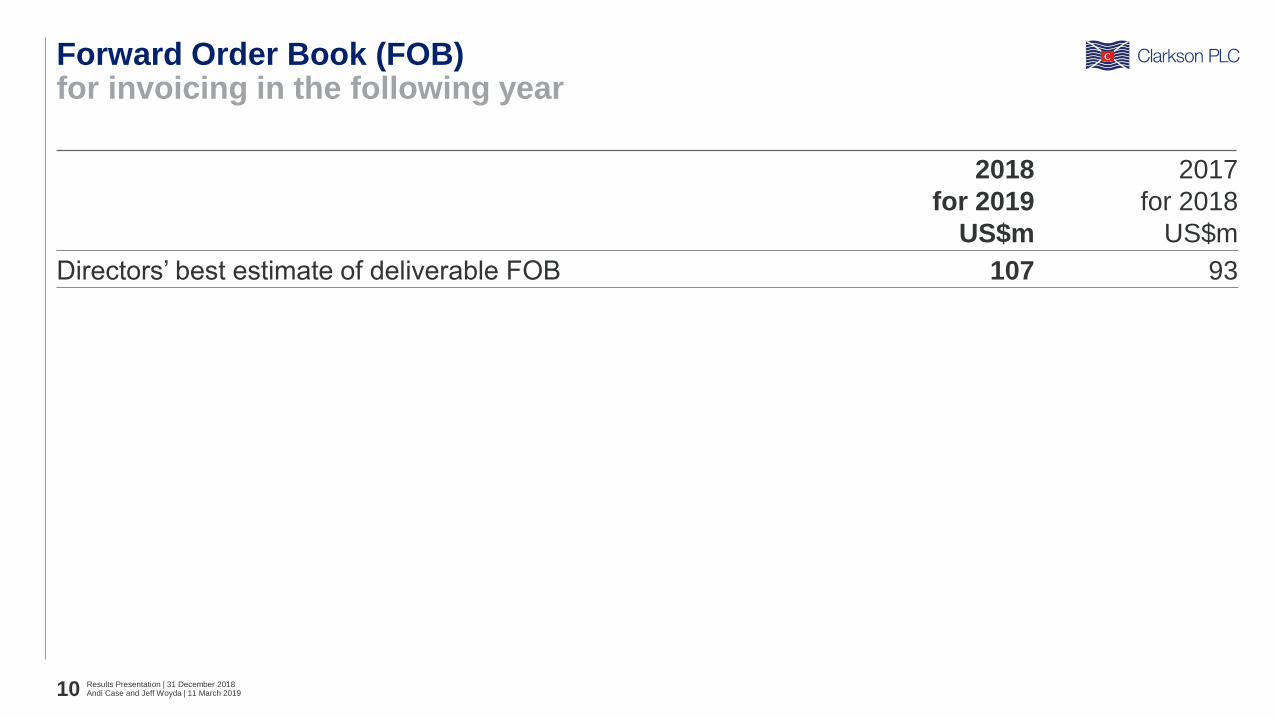

for invoicing in the following yearForward Order Book (FOB)

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201810

2018

for 2019

US$m

2017

for 2018

US$m

Directors’ best estimate of deliverable FOB 107 93

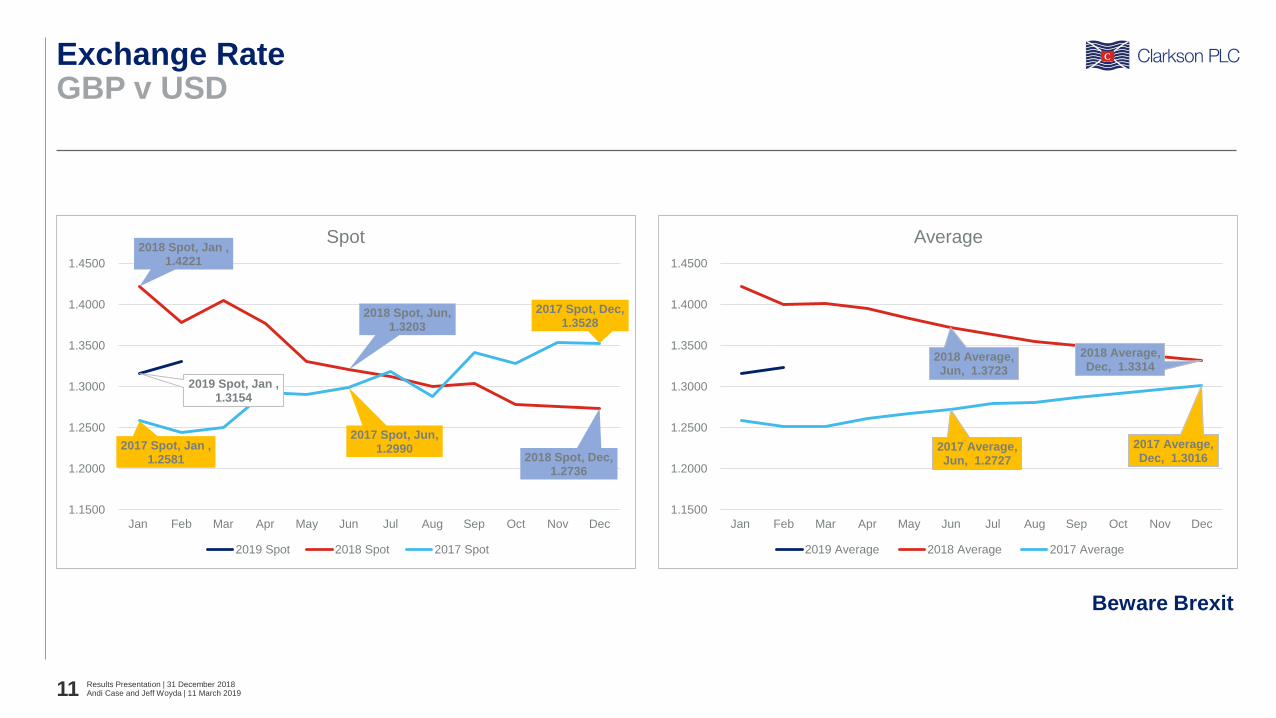

GBP v USDExchange Rate

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201811

2019 Spot, Jan , 1.3154

2018 Spot, Jan , 1.4221

2018 Spot, Jun, 1.3203

2018 Spot, Dec, 1.2736

2017 Spot, Jan , 1.2581

2017 Spot, Jun, 1.2990

2017 Spot, Dec, 1.3528

1.1500

1.2000

1.2500

1.3000

1.3500

1.4000

1.4500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Spot

2019 Spot 2018 Spot 2017 Spot

2018 Average, Jun, 1.3723

2018 Average, Dec, 1.3314

2017 Average, Jun, 1.2727

2017 Average, Dec, 1.3016

1.1500

1.2000

1.2500

1.3000

1.3500

1.4000

1.4500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Average

2019 Average 2018 Average 2017 Average

Beware Brexit

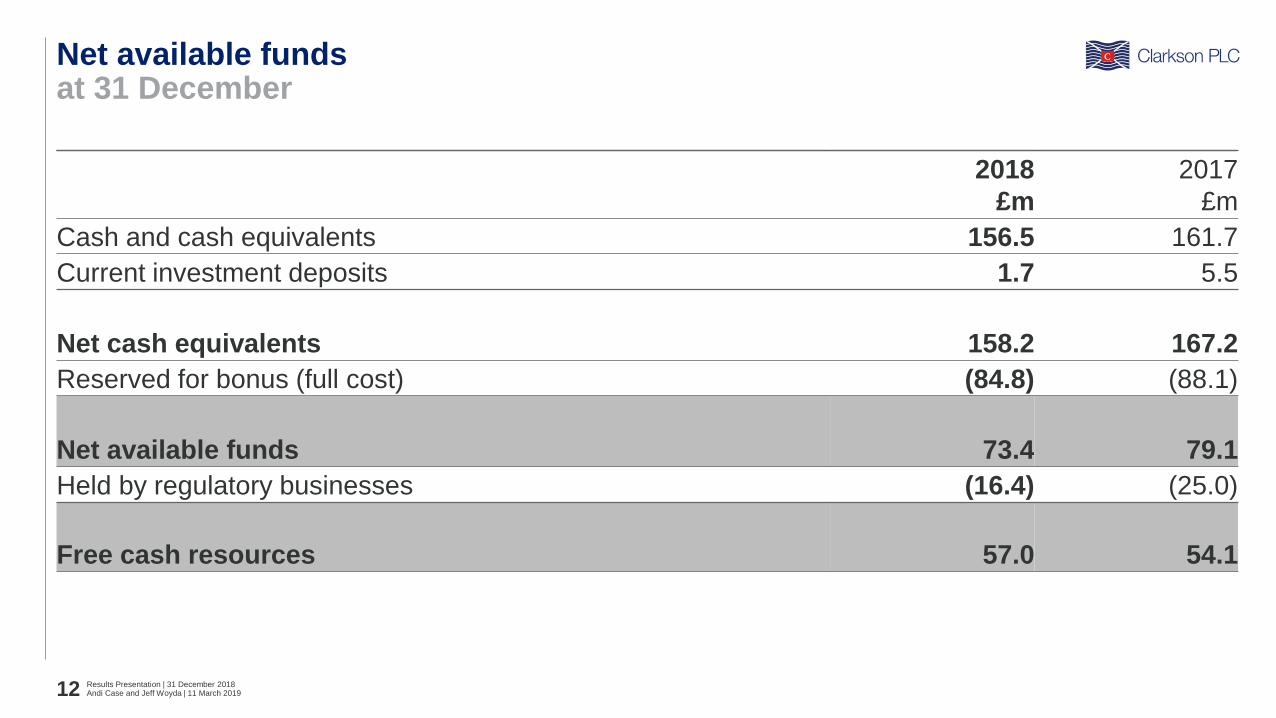

at 31 DecemberNet available funds

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201812

2018

£m

2017

£m

Cash and cash equivalents 156.5 161.7

Current investment deposits 1.7 5.5

Net cash equivalents 158.2 167.2

Reserved for bonus (full cost) (84.8) (88.1)

Net available funds 73.4 79.1

Held by regulatory businesses (16.4) (25.0)

Free cash resources 57.0 54.1

after bonusMovement in free cash resources

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201813

2.3 (22.5)

(14.6)

(8.3)

(6.7)

54.1

45.0

57.08.6

Free cashresources

Dec 17

Operating profit Depreciation Other Dividends Working capital Taxation Short termInvestments in

regulatedentities

CapitalisedSoftware

development

Capex Movement incash held by

regulatedentities

Free cashresources

Dec 18

5.2

(2.2)(3.9)

16 years of progressive dividendDividend history

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201814

6 79 10

1214

16 16 17 18 18 1921 22 22 23 24

911

16

22

24

2626 27

3032 33

37

3940

43

5051

1518

25

32

36

4042 43

4750 51

56

6062

65

7375

0

10

20

30

40

50

60

70

80

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Interim Final

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201815

Markets

Andi CaseChief Executive Officer

The Board

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201816

Chair

Bill ThomasChair (Independent Non-Executive)

Executive Directors

Andi CaseChief Executive Officer

Jeff WoydaChief Financial Officer and Chief Operating Officer

Peter M. AnkerPresident of Broking and Investment Banking

Non-Executive Directors

Peter BackhouseSenior Independent Non-Executive Director

Marie-Louise ClaytonIndependent Non-Executive Director

James Hughes-Hallett, CMGIndependent Non-Executive Director

Tim MillerIndependent Non-Executive Director

Birger NergaardIndependent Non-Executive Director

Company Secretary

Rachel SpencerCompany Secretary

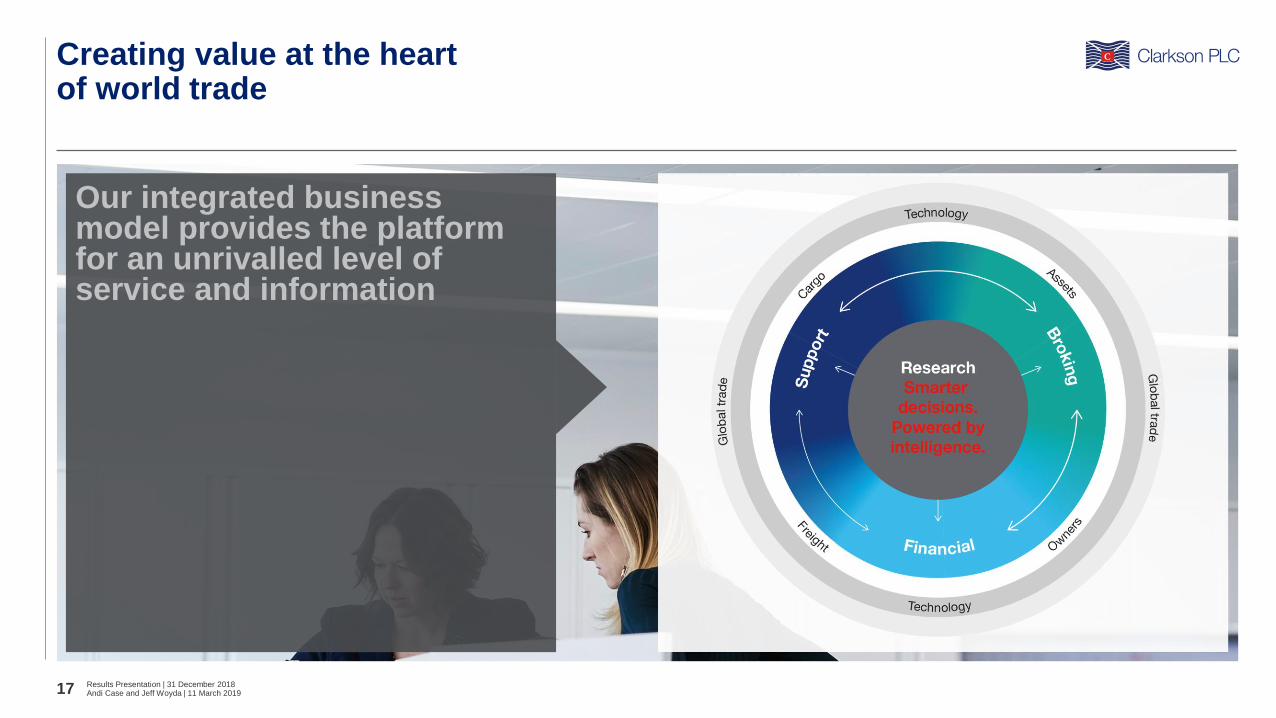

Creating value at the heart of world trade

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201817

Our integrated business model provides the platform for an unrivalled level of service and information

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201818

This is Smarter Shipping

TechnologyRebranded for the future

Technology

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201819

A collection of interoperable modules to enhance the end-to-end chartering process

INTELLIGENCE EXECUTION DOCUMENTATION MONITORING

Source: Clarksons/IMF

World Seaborne Trade vs. GDP

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201820

0

20

40

60

80

100

120

140

160

0

2

4

6

8

10

12

14

16

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29

GD

P C

urre

nt P

rices (T

N $

)

Wo

rld

Seab

orn

e T

rad

e (

BN

to

nn

es)

World Seaborne Trade Trade trend volume GDP Current Prices GDP trend volume Linear (World Seaborne Trade) Linear (GDP Current Prices)

Economic growth remains supportive of seaborne tradeGlobal Macroeconomic Indicators

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201821

44

46

48

50

52

54

56

58

60

62

Jan-1

2

Ma

y-1

2

Sep-1

2

Jan-1

3

Ma

y-1

3

Sep-1

3

Jan-1

4

Ma

y-1

4

Sep-1

4

Jan-1

5

Ma

y-1

5

Sep-1

5

Jan-1

6

Ma

y-1

6

Sep-1

6

Jan-1

7

Ma

y-1

7

Sep-1

7

Jan-1

8

Ma

y-1

8

Sep-1

8

Jan-1

9

Co

ntr

acti

on

| E

xp

an

sio

n

US Japan Eurozone China

Global Manufacturing PMI’s

Source: IMF, HSBC, Markit, Caixin, Refinitiv

-6

-4

-2

0

2

4

6

8

10

12

14

16

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19 e

% c

han

ge (

year

on

year)

World GDP US GDP Eurozone China GDP India GDP

GDP Growth

Manufacturing activity in emerging economies is expandingEmerging Asian Economies Potential

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201822

Source: HSBC, Markit, Caixin, Refinitiv

Selected Emerging Economies Manufacturing PMI’s Energy Use Per Capita Vs GDP Per Capita Steel Use Per Capita

44

46

48

50

52

54

56

58

Jan-1

4

Ma

y-1

4

Sep-1

4

Jan-1

5

Ma

y-1

5

Sep-1

5

Jan-1

6

Ma

y-1

6

Sep-1

6

Jan-1

7

Ma

y-1

7

Sep-1

7

Jan-1

8

Ma

y-1

8

Sep-1

8

Jan-1

9

Co

ntr

acti

on

| E

xp

an

sio

n

India Indonesia Vietnam

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

South

Kore

a

Japa

n

Ch

ina

Ma

laysia

US

A

Tha

iland

Vie

tnam

India

Indon

esia

Sri L

anka

Myan

ma

r

Pakis

tan

Bang

lad

esh

Kg

fin

ish

ed

ste

el

pro

du

cts

per

year

per

cap

ita

China

India

United States

Vietnam

Philippines

Indonesia

EU

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

- 10 20 30 40 50 60 70

Oil e

qu

ivale

nt

per

cap

ita (

kg

)

GDP per capita (thousand USD)

Creating inefficiencies in seaborne trade US-China Trade Dispute

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201823

• Tariffs compromising world

economic growth

• Uncertainty leading to reduced

investment and slower

demand growth

• Strong dollar impacting

demand for commodities

• Risk of escalation and

retaliatory tariffs

• Accelerated production /

hoarding ahead of tariff

implementation

• Dislocation of trades creating

inefficiencies and tightening

supply / demand balances

• U.S. energy exports continue to

increase but a resolution

generates additional upside

• Increase in China’s import of

energy products increases

overall tonne-mile demand

Source: Clarksons Research. Data as of 1st January 2019. Retrospective changes to number of orders may occur due to late reporting and other factors.

Global Newbuilding Orders at Historic Low…

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201824

480 545411

550

795

546667

1,378

1,196 1,145

2,256

2,909

1,872

582

1,840

1,043

706

2,054

1,342

1,152

242

787708

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

No. Ships

Orders representative of vessels

over 20,000 dwt

Source: Clarksons Research. Data as of 1st January 2019. Retrospective changes to number of orders may occur due to late reporting and other factors.

…Reflected In Number Of Yards With An Orderbook Of At Least One Vessel >20,000 dwt

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201825

47 49 50 5361

70 72 71 7685

101

151

208

235 232240

224

181

158 152 151138

120107

65 61 63 58 4645 49 47 47

48

54

64

71

7163 56

52

40

3831 33

33

29

20

0

50

100

150

200

250

300

350

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

No. Yards

Rest of World

China - Japan - Korea

2009: 306 yards

1996-2019: Yards with at least 1 ship

on order at year start.

January 2019:

127 yards

Source: Clarksons

Orderbook as % of Fleet

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201826

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Dry Bulk (Dwt) Containerships (TEU) Deep Sea Tankers (Dwt) Specialised Products (Dwt)

LNG Carriers (Cu. M.) LPG Carriers (Cu. M.) Global Fleet – All Vessel Types (% based on no. of Vessels – Right Axis)

Demand Growth

(BN Tonne-Miles*, % Chg 2018–2020)

Data Source: Clarksons. *LNG and Oil Tanker Demand Growth account for fleet productivity and floating storage developments as well as tonne-miles, and are measured in cbm/dwt demand respectively. Container Demand Growth basis TEU-

miles, adjusted to account for fleet productivity changes; container utilization adjusted for estimated changes in capacity idle or out of service.

Sector Fundamentals Outlook Comparison

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201827

8%

7%

14%

9%

16%

11%

0% 5% 10% 15% 20%

Containers

Dry Bulk

Crude & Products

Chemicals

LNG

LPG & Ammonia

Fleet Growth

(% Chg 2018–2020)

7%

6%

5%

4%

17%

8%

0% 5% 10% 15% 20%

Containers

Dry Bulk

Crude & Products

Chemicals

LNG

LPG & Ammonia

7%

6%

8%

6%

19%

11%

0% 5% 10% 15% 20%

Containers

Dry Bulk

Crude & Products

Chemicals

LNG

LPG & Ammonia

Fleet Growth

(% Chg 2016–2018)

Data Source: Clarksons/TEX/Asiasis/Refinitiv

Upward Pressure on Newbuilding Prices

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201828

0

50

100

150

200

250

300

350

0

20

40

60

80

100

120

140

160

180

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Jan-1

6

Jan-1

7

Jan-1

8

Jan-1

9

Ind

ex

MM

$

VLCC NB Price (LH-axis) 100 Billion Won in US$ (LH-Axis) Korean Steel Price Index (RH-axis)

• Newbuilding prices have increased

from 2017’s low point

• Cost pressures supporting rise in

prices

• Shipyard consolidation continuing

• Environmental regulations and new

technology likely to add to costs

Impact of the IMO 2020 Sulphur Cap on Bunker Fuels

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201829

Fleet Supply

• Reduction in active fleet size due to scrubber retrofitting

• Re-positioning of the fleet in order to prepare for compliance

• Potential early retirement of older vessels due to higher bunker fuel costs

Vessel Demand

• Potential speed restraint due to higher bunker costs, leading to increased

vessel requirements

• Anticipated increase in demand for tankers due to higher refinery runs,

changes to oil trade patterns and floating storage

Market Impact

Expected tightening of supply

/ demand balances across

most market sectors

Source: Clarksons. Based on individually identified vessels only. *% of all vessels for Cruise / Passenger and Ro-Ro.

Installation of Scrubbers

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201830

0

100

200

300

400

500

600

700

800

900

1000

Bulk Carrier Cruise/Passenger Containership Gas Carrier Ro-Ro Tanker Others

Num

ber

of

vessels

Existing vessels with scrubbers fitted Existing vessels due to be retrofitted Vessels due to be delivered with scrubbers fitted

• Heavy investment in scrubbers

predominantly in larger vessels

• $2.5 million – $5.0 million price range for

equipment and installation on larger

vessels (tankers and dry bulk) and $5.0

million - $7.0 million for large

containerships.

• Off-hire time for retrofitting vessels in key

market sectors disrupting fleet utilisation.

4% 7% 1% 1%9%

% of fleet per sector >20,000 dwt that is retrofitting scrubbers*

0.2% 1%

The regulatory timeline continues to accelerate

Source: Clarksons Research, January 2019

Environmental Regulation

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201831

2019 2020 2021 2022 2023 2024 2025 - - - - - - 2030 - - - - - - 2050

ECAs SOx NOx GHG / EEDI Green Recycling Ballast Water Current position

EU MRV

certification in

effect

Lower EEDI ref.

line (Phase 3)

Lower EEDI

ref. line

(Phase 2)

North Sea & Baltic

Sea NOx ECAs in

effect

50% GHG

Reduction Target

IMO DCS reporting

period begins

EU SRR

enters into

force

40% CO2 Intensity

Reduction Target

IMO 2020

0.5% Global

Sulphur Limit

IMO BWM

Convention requires

retrofitting of vessels

Immediate loss of export volumes

Source: Clarksons/GTIS

Vale Iron Ore Disaster: Lost volumes and replacement capacity

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201832

World Iron Ore Supply 2019(f) vs 2018

873 882 905

920

384 396 396 411

275 253 263 263

200

250

300

350

400

450

500

550

600

650

700

750

800

850

900

950

2017 2018(f) 2019(f) 2020(f)

Millio

n T

on

nes

Australia Brazil Other

27.6

41.0

0.0

23.0

23.0

20.0

4.7

4.2

1.6

1.4

0.7

0.3

-3.6

-8.9

1.2

1.0

-14 -9 -4 1 6 11 16 21 26 31 36 41 46

Total

Total

Brazil

Brazil

Australia

Australia

Canada

Canada

South Africa

South Africa

Chile/Peru

Chile/Peru

Iran

Iran

Sweden/Norway/Finland

Sweden/Norway/Finland

Y-O-Y Million Tonnes

Post-Vale incidentPre-Vale incident

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

Jan-1

5

Jul-1

5

Jan-1

6

Jul-1

6

Jan-1

7

Jul-1

7

Jan-1

8

Jul-1

8

Millio

n b

pd

China Japan South KoreaTaiwan India EUSouth Africa

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Jan-1

5

Jul-1

5

Jan-1

6

Jul-1

6

Jan-1

7

Jul-1

7

Jan-1

8

Jul-1

8

Millio

n b

pd

North America China Europe India

Venezuelan Crude Exports to Key Areas Iranian Crude Exports to Asia and EU

• Venezuelan exports expected to fall,

particularly to the U.S., adding to OPEC

cuts. However disruption may lead to some

longer-haul VLCC voyages.

• Iranian exports believed to have increased

in early 2019 due to specific waivers.

• Further reductions in Iranian exports from

Q2 2019 may lead to increased spot market

shipments from other countries.

Source: GTIS/Clarksons. Trade data based on reported imports into receiving countries. Not all receiving countries provide import data e.g. no data available for imports of Iranian crude oil into Turkey.

Geopolitical Developments Affecting Oil Trade

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201833

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201834

Financial Division

Global full service investment bank for our core industriesClarksons Platou Securities

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201835

Global full service investment bank for our three core industries – Shipping, Oil Services, and Metals & Mining

Investment banking arm of the Clarksons Group

Fully licensed in Norway and EEA alongside a strong

track record of capital markets activity in US/Canada

Global coverage from five dedicated offices in Europe

and North America

Clarksons Platou Securities covers “cargo and its

journey”

− Shipping

− Oil Services

− Metals & Mining

43% market sharein shipping ECM globally

2013-2018

41% market sharein offshore drilling ECM globally

2010-2018

Joint book-running manager in

USD 1.9bnsecondary offering of GLNG (NASDAQ)

shares for the Fredriksen Group (2014)

USD 20.7bn equity capital raised since 2010

Sole advisor to Transocean in USD 3.4bn

acquisition of Songa Offshore,

one of the largest

rig M&As globally

Sole financial advisor to both parties in

USD 328m

acquisitionof Songa Bulk by Star Bulk

Participated in

3x coal IPOsAnd

2x term loans

USD 17.3bn debt capital raised since 2010

Joint Bookrunner in

USD 350m senior

secured bond issue for Nemaska Lithium in May 2018

Participated in

AUD 774mIPO of Coronado Resources, the largest

coal IPO in Australia

Seamless execution leading to repeat business

Clarksons Platou Securities

Andi Case and Jeff Woyda | 11 March 2019

Results Presentation | 31 December 201836

2,705

2,205

1,674

1,440

1,100

604

487

478

105

Go

lar

LN

GB

orr

Drilli

ng

Scorp

ioB

ulk

ers

Scorp

ioT

ankers

Sh

elf

Dri

llin

gN

em

aska

Lith

ium

DH

TH

old

ings

Navio

sG

rou

pS

tand

ard

Dri

llin

g

Joint Lead Manager

Jun 2014

USD 683m

Equity Offering

Joint Lead Manager

Sept 2014

USD 1,872m

Equity Offering

Joint Lead Manager

Nov 2016

USD 150m

Equity Offering

Joint Lead Manager

Dec 2016

USD 155m Equity

Offering

Joint Lead Manager

Mar 2017

USD 800m Equity

Offering

Joint Lead Manager

Oct 2017

USD 650m Equity

Offering

Joint Lead Manager

Mar 2018

USD 250m Equity

Offering

Joint Lead Manager

May 2018

USD 350m

Convertible Bond

Sole Manager

Jun 2013

USD 250mm

Equity Offering

Sole Manager

Sep 2013

USD 300m

Equity Offering

Sole Manager

Oct 2013

USD 300m

Equity Offering

Joint Lead Manager

Dec 2013

USD 350m

IPO

Placement Agent

Nov 2014

USD 150m

Equity Offering

Joint Lead Manager

Jun 2015

USD 200m

Equity Offering

Sole Bookrunner

Mar 2016

USD 63m

Equity Offering

Sole Bookrunner

Jun 2016

USD 61m

Equity Offering

Sole Manager

Jan 2013

USD 230m

Equity Offering

Sole Manager

Mar 2013

USD 235m

Equity Offering

Sole Manager

May 2013

USD 300m

Equity Offering

Joint Lead Manager

Aug 2013

USD 219m

Equity Offering

Joint Lead Manager

Apr 2015

USD 140m

Equity Offering

Sole Bookrunner

Nov 2017

USD 90m

Equity Offering

Senior Manager

Oct 2018

USD 227m

Equity Offering

Co-Manager

Feb 2018

USD 600m

Bond Offering

Co-Manager

Jun 2018

USD 300m

Bond Offering

Joint Bookrunner

Jun 2018

USD 225m

IPO

Sole Manager

Nov 2013

USD 110m

Equity Offering

Joint Lead Manager

Jan 2014

USD 227m

Equity Offering

Joint Lead Manager

Sept 2014

USD 150m

Equity Offering

Sole Manager

Feb 2013

USD 101m

Equity Offering

Sole Manager

May 2013

USD 120m

Equity Offering

Sole Manager

Sept 2013

USD 100m

Equity Offering

Joint Lead Manager

Feb 2014

USD 58m

Equity Offering

Sole Bookrunner

Aug 2017

USD 50m

Equity Offering

Joint Bookrunner

Nov 2017

USD 50m

Equity Offering

Sole Manager

Dec 2016

NOK 275m

Equity Offering

Sole Manager

Jan 2017

NOK 100m

Equity Offering

Sole Manager

Jan 2017

NOK 198m

Equity Offering

Sole Manager

Nov 2017

NOK 200m

Equity Offering

Sole Manager

Mar 2018

NOK 100m

Equity Offering

Figures in

USDm

Sole Selling Agent

Jun 2017

USD 39m

Equity Offering

Sole Selling Agent

May 2018

USD 215m

Equity Offering

Joint Lead Manager

Jun 2018

USD 350m

Bond Offering

29 x ECM, DCM, CB, M&A and restructuring transactions completed in 2018Clarksons Platou Securities

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201837

Joint Lead Manager

USD 11m Equity

Private Placement

Joint Lead Manager

NOK 500m Senior

Unsecured Bond Issue

Sole Selling Agent

CAD 280m Equity

Offering

Sole Advisor

USD 21m Sale- and

Leaseback

Financial Advisor

USD 10m Equity

Private Placement and

USD 65m Stream

Sole Advisor

USD 65m Private

Secured Loan Facility

Joint Lead Manager

NOK 520m Equity

Private Placement

Sole Manager

USD 32m Equity

Private Placement

Joint Bookrunner

USD 550m

Term Loan B

Sole Manager

Listing on Oslo Stock

Exchange

Joint Lead Manager

USD 350m Senior

Convertible Bond

Joint Lead Manager

USD 250m Equity

Private Placement

Joint Lead Manager

AUD 774m IPO

Listing on ASX

Joint Bookrunner

USD 225m IPO

Listing on OSE

Sole Advisor

USD 328m (EV)

acquisition of Songa

Bulk

Sole Manager

NOK 100m Equity

Offering

Senior Manager

USD 330m

Public Offering of

Common Shares

Financial Advisor

Spin-off from Grindrod

Limited and listing on

NASDAQ

Joint Lead Manager

USD 350m Senior

Secured Callable Bond

Financial Advisor

51% acquisition of

Island Offshore Subsea

Sole Manager

USD 45m Equity

Private Placement

Co-Manager

USD 300m Tack-on

Senior Notes Issue

Underwriter

CAD 8m Equity Private

Placement

Co-Manager

USD 600m Senior

Notes Issue

Sole Advisor

Southern Cross

Group’s disposal of UP

Offshore

Sole Selling Agent

CAD 9m

Equity Offering

Sole Financial Advisor

USD 5m Private

Placement and Change

of Control

Joint Lead Manager

NOK 40m

Rights Issue

Joint Bookrunner

USD 350m senior

secured 1st lien notes

UP Offshore

Avenir LNG

Songa Bulk

• Clarksons Platou Securities completed 29x transactions

during the course of 2018

• Working for 25x unique clients, generating both new and

repeat business across our core sectors of Shipping, Oil

Services and Metals & Mining

• Full service offering with ECM, DCM, CB, M&A and

restructuring transactions completed during the year

Why 2018 was a challenging year - MacroClarksons Platou Securities

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201838

S&P, FTSE & OSE 2018 development Commentary

• Turbulent year for the global stock market driven by

― All-time-high valuations prompting fears of correction

― Weaker Chinese economic growth

― Fear of higher interest rates

― Trade war tensions

― Uncertain outcome of Brexit

• Implementation of stricter regulatory policies such as MiFID II and GDPR

― Resulted in pressure on CPS commissions/research payments

• Brent crude oil price ended down 24% in 2018YE compared to 2017YE, at USD 50.57/bbl compared to USD 66.73/bbl, effecting our core markets

• However, markets have shown signs of recovery 2019YTD

0

5

10

15

20

25

30

35

40

80

85

90

95

100

105

110

115

120

VIX

vo

lati

lity

ind

ex

Equ

ity

ind

ice

s (r

eb

ase

d)

Volatility (VIX) S&P 500 OSEBX FTSE 100

2018YE

Why 2018 was a challenging year - MicroClarksons Platou Securities

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201839

Companies trading significantly below NAV

• Challenging equity market with peers trading significantly below NAV

• Limited equity market activity, other than in distressed situations

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

Weighted Average Tankers Weighted Average DRY

Completed 36 projects in the shipping and real estate space during 2018

Total transaction value of USD 1,7 billion

Raised USD 250 million in equity for new projects

Corporate management on 52 vessels and 42 properties (total of 360 000 sqm)

Established Clarksons Platou Real Estate Investment Management with its first

NOK 500 million (USD 61 million) fund

Continued strong transaction flowClarksons Platou Project Finance

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201840

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201841

Outlook

Financial Outlook

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201842

Tailwinds vs Headwinds

Forward

order book

$ 107m

+$14m

Finance

requirement

strong

amongst

clients

IMO 2020

• Scrubber

fitting

• Regulatory

uncertainty

• Voyage

dislocation

Demand

growth

2018

11.9bn tonnes

2008

8.6bn tonnes

Supply side

challenged

• Lack of

finance

• Rates

• Shipyards

Progressive

dividend

policy in

16th year

Cash

generative

and debt

free

US-China

trade war

Vale NAV to

Market Cap

SEC closureSanctionsExchange

rate

volatility

Dec 1.2736

Feb 1.3301

Venezuela

Headwinds…?

Tailwinds

Thank You

ClarksonsCommodity QuaySt. Katharine DocksLondonUnited KingdomE1W 1BFwww.clarksons.com

The material and the information (including, without limitation, any future rates and/or forward looking predictions) contained herein (together,

the "Information") are provided by Clarkson PLC (Clarksons) for general guide.

The Information is provided on ‘as is’ and ‘as available’ basis. Clarksons and all its Group companies make no representations or warranties of

any kind, express or implied about the completeness, accuracy, reliability, suitability or availability with respect to the Information. Any reliance

placed on such Information is therefore strictly at the recipient's own risk and no responsibility is accepted for any loss or damage howsoever

arising. Please note that future rates and/or forward looking predictions are for illustration purposes only and given without guarantee; the

ultimate outcome may be different.

This Information is not for reproduction or distribution without Clarksons’ prior written consent. Especially, the Information is not to be used in

any document for the purposes of raising finance whether by way of debt or equity. All intellectual property rights are fully reserved by

Clarksons, its Group companies and/or its licensors.

This disclaimer shall be governed by and construed in accordance with English law.

Commodity Quay, St. Katharine Docks, London, UK, E1W 1BF

Clarkson PLCDisclaimer

Andi Case and Jeff Woyda | 11 March 2019Results Presentation | 31 December 201844