results of the initial analysis - entergy...

TRANSCRIPT

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

1

Results of the InitialAnalysis

EAI Technical ConferenceSeptember 23, 2010

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

2

Discussion Framework

PRIVILEGED AND CONFIDENTIALAttorney Client Privileged CommunicationAttorney Work Product

Understandingthe Drivers

Understandingthe Drivers

2013 & 2014Initial Results2013 & 2014

Initial Results

IndividualOperatingCompany

Drivers

IndividualOperatingCompany

Drivers

Gas PriceSensitivitiesGas Price

Sensitivities

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

3

The main difference in this initial analysis between CODA and theSystem Agreement revolves around the allocation of flexibleenergy costs

Flexible energy costs refer to the costs that correspond to the provision of flexibility forthe SystemFlexible energy costs are not unique to CODA -- they are as much a part of the SystemAgreement as they are of CODACODA and the System Agreement allocate flexible energy costs very differently

The System Agreement allocates flexible energy costs regardless of an OPCO’s“flex” position (i.e. if it has excess flexibility or is short flexibility)CODA allocates flexible energy costs based on an OPCO’s flex positionThe largest impact relates to different allocations of the flexible energy costs oflegacy gas/oil units as the cost of these unit are usually much higher than newergas and coal units -- i.e. $100/MWh versus $65-75/MWh

The following charts highlight how the CODA and System Agreement structures differ,using three portrayals that are indicative of circumstances faced by the OPCOs

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

4

The first depicts an OPCO with lower costs under CODAthan under the System Agreement

(i.e. $100/MWhflex energy

from legacy gas)

(i.e. $70/MWhenergy)

Under MSS-3, this OPCO is allocated flexible energy costs not because it needs flex-- it has excess flex -- but because it needs energyUnder CODA, the OPCO sells its excess flexible energy and buy its energy needs atthe hourly avoided cost

(i.e. $100/MWhflex energy

from legacy gas)

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

5

The second depicts an OPCO with higher costs under CODAthan under the System Agreement

This OPCO sells flexible energy under MSS-3 not because it has excess flex -- itneeds flex -- but because it has excess energyUnder CODA, the OPCO must buy its flex needs and then sell its excess energy atthe hourly avoided cost

(i.e. $100/MWhflex energy

from legacy gas)

(i.e. $100/MWhflex energy

from legacy gas)

(i.e. $70/MWhenergy)

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

6

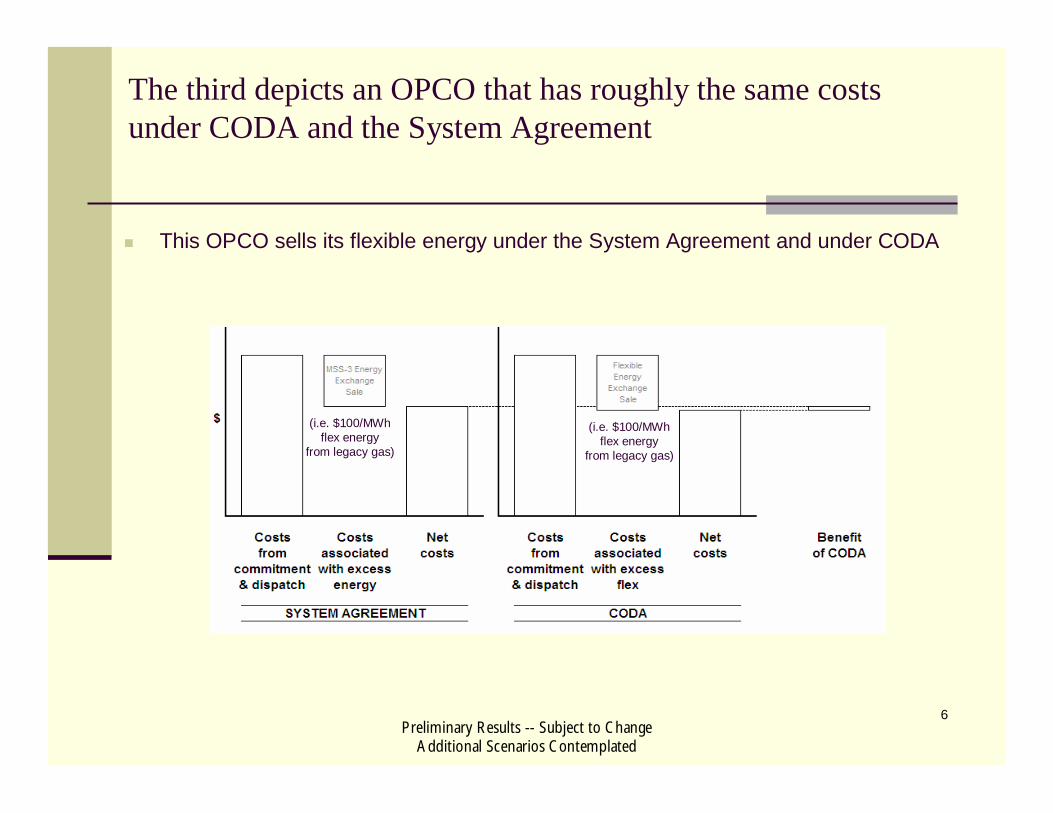

The third depicts an OPCO that has roughly the same costsunder CODA and the System Agreement

This OPCO sells its flexible energy under the System Agreement and under CODA

(i.e. $100/MWhflex energy

from legacy gas)

(i.e. $100/MWhflex energy

from legacy gas)

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

7

Discussion Framework

PRIVILEGED AND CONFIDENTIALAttorney Client Privileged CommunicationAttorney Work Product

Understandingthe Drivers

Understandingthe Drivers

2013 & 2014Initial Results2013 & 2014

Initial Results

IndividualOperatingCompany

Drivers

IndividualOperatingCompany

Drivers

Gas PriceSensitivitiesGas Price

Sensitivities

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

8

Summary of 2013 Initial Analysis: 6-Company CODA vsSystem Agreement

Comparison of 2013 Total Production Costs underCODA vs System Agreement

$39

$102

($37)($9)

($31)($53)

$12

-$100

-$50

$0

$50

$100

$150

EAI ELL EMI ENOI EGSL ETI System

$MM

• RPCE payments are not factored into the CODA results. Those are included in the appendix.

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

9

For 2013, the 6-Company CODA results in a shift of fuelcosts among the operating companies and produces non-fuelsavings

Breakdown of 2013 Production Cost Savings by Fueland Non-Fuel under CODA vs System Agreement

-$100

-$50

$0

$50

$100

$150

EAI ELL EMI ENOI EGSL ETI System

$MM

Fuel & Purch Pwr Non-Fuel

• RPCE payments are not factored into the CODA results. Those are included in the appendix.

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

10

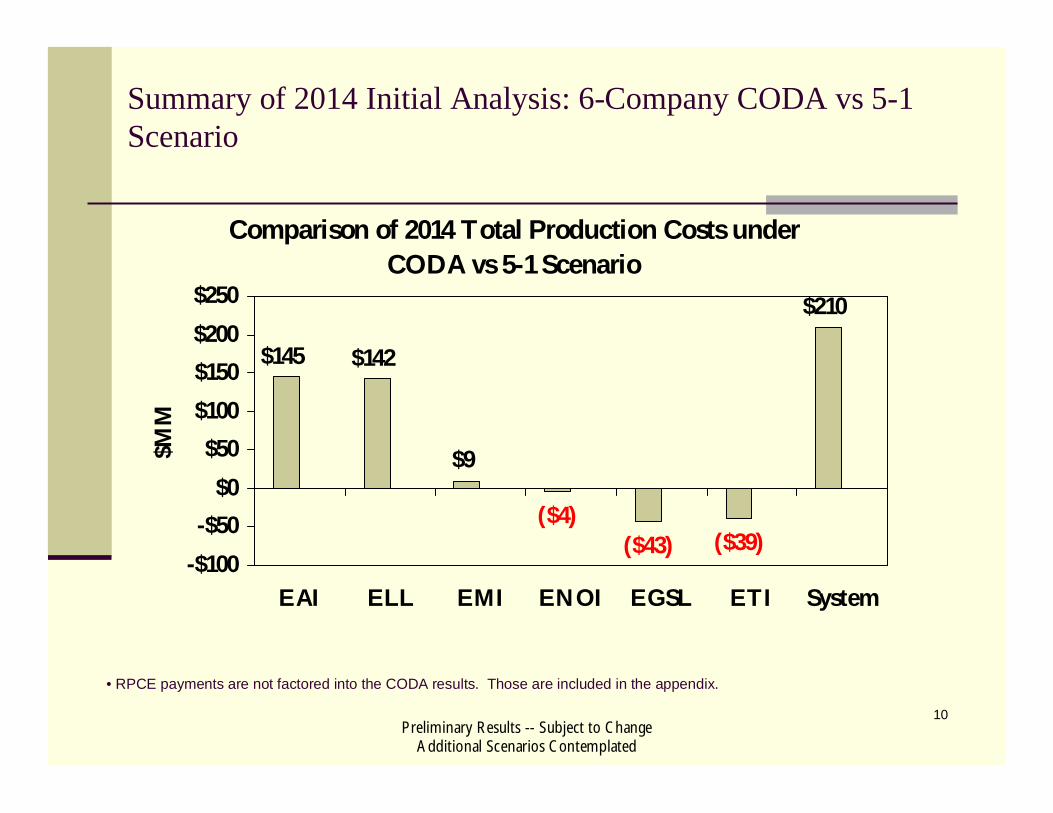

Summary of 2014 Initial Analysis: 6-Company CODA vs 5-1Scenario

Comparison of 2014 Total Production Costs underCODA vs 5-1 Scenario

($4)($43) ($39)

$9

$142$145

$210

-$100

-$50$0

$50

$100

$150

$200

$250

EAI ELL EMI ENOI EGSL ETI System

$MM

• RPCE payments are not factored into the CODA results. Those are included in the appendix.

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

11

Breakdown of 2014 Production Cost Savings by Fueland Non-Fuel under CODA vs 5-1 Scenario

-$100

-$50

$0

$50

$100

$150

EAI ELL EMI ENOI EGSL ETI System

$MM

Fuel & Purch Pwr Non-Fuel

For 2014, the 6-Company CODA produces both fuel and non-fuel savings for the combined companies

• RPCE payments are not factored into the CODA results. Those are included in the appendix.

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

12

Discussion Framework

PRIVILEGED AND CONFIDENTIALAttorney Client Privileged CommunicationAttorney Work Product

Understandingthe Drivers

Understandingthe Drivers

2013 & 2014Initial Results2013 & 2014

Initial Results

IndividualOperatingCompany

Drivers

IndividualOperatingCompany

Drivers

Gas PriceSensitivitiesGas Price

Sensitivities

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

13

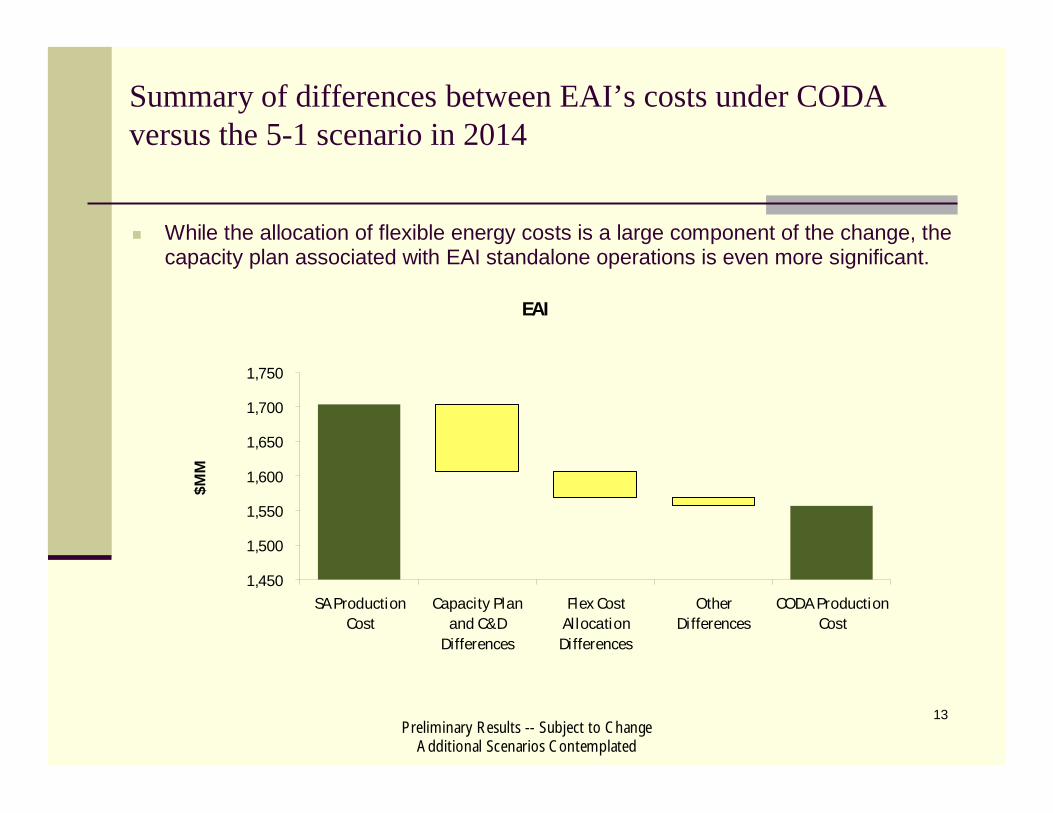

Summary of differences between EAI’s costs under CODAversus the 5-1 scenario in 2014

While the allocation of flexible energy costs is a large component of the change, thecapacity plan associated with EAI standalone operations is even more significant.

EAI

1,450

1,500

1,550

1,600

1,650

1,700

1,750

SA ProductionCost

Capacity Planand C&D

Differences

Flex CostAllocation

Differences

OtherDifferences

CODA ProductionCost

$MM

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

14

Summary of differences between ELL’s costs under CODAversus the 5-1 scenario in 2014

The largest impact relates to the allocation of flexible energy costs.

ELL

2,650

2,700

2,750

2,800

2,850

2,900

SA ProductionCost

Capacity Planand C&D

Differences

Flex CostAllocationDifferences

Other Differences CODA ProductionCost

$MM

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

15

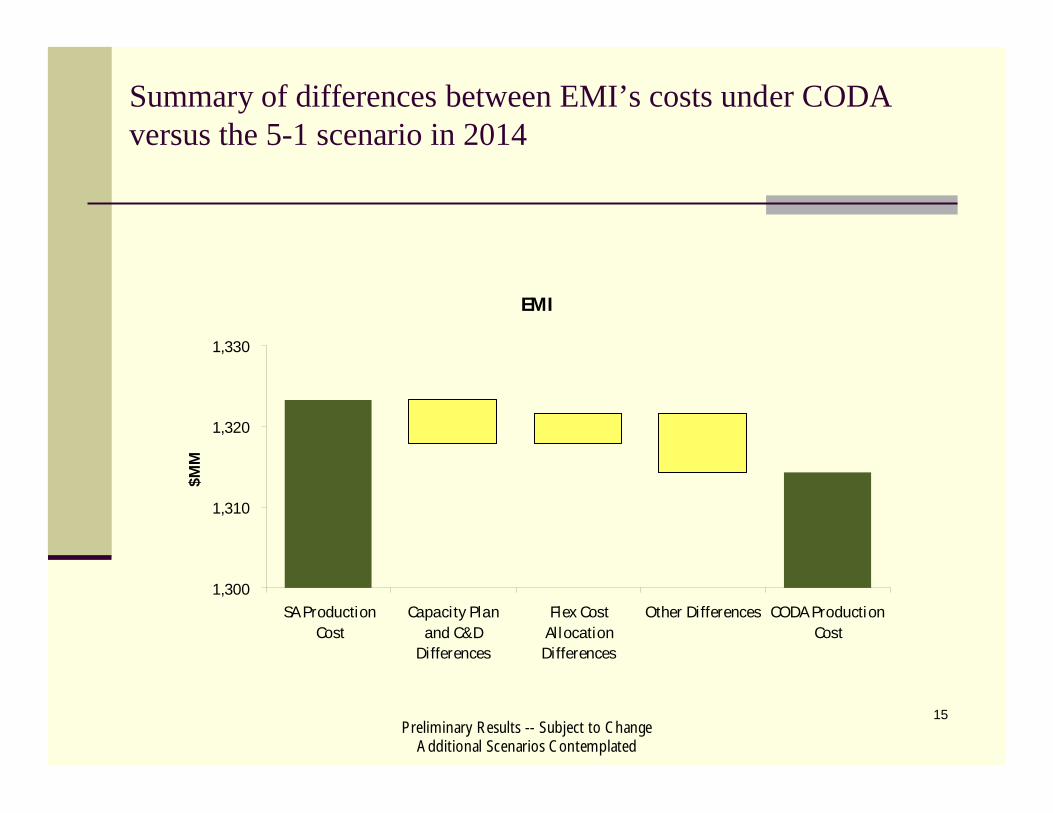

Summary of differences between EMI’s costs under CODAversus the 5-1 scenario in 2014

EMI

1,300

1,310

1,320

1,330

SA ProductionCost

Capacity Planand C&D

Differences

Flex CostAllocation

Differences

Other Differences CODA ProductionCost

$MM

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

16

Summary of differences between EGSL’s costs under CODAversus the 5-1 scenario in 2014

The largest impact relates to the allocation of flexible energy costs.

EGSL

1,740

1,760

1,780

1,800

1,820

1,840

1,860

SA ProductionCost

Capacity Plan andC&D Differences

Flex CostAllocation

Differences

Other Differences CODA ProductionCost

$MM

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

17

Summary of differences between ENOI’s costs under CODAversus the 5-1 scenario in 2014

The largest impact relates to the allocation of flexible energy costs.

370

380

390

400

SA ProductionCost

Capacity Plan andC&D Differences

Flex CostAllocation

Differences

Other Differences CODA ProductionCost

$MM

ENOI

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

18

Summary of differences between ETI’s costs under CODAversus the 5-1 scenario in 2014

The largest impact relates to the allocation of flexible energy costs.

ETI

1,670

1,680

1,690

1,700

1,710

1,720

1,730

1,740

1,750

1,760

SA ProductionCost

Capacity Planand C&D

Differences

Flex CostAllocation

Differences

Other Differences CODA ProductionCost

$MM

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

19

Discussion Framework

PRIVILEGED AND CONFIDENTIALAttorney Client Privileged CommunicationAttorney Work Product

Understandingthe Drivers

Understandingthe Drivers

2013 & 2014Initial Results2013 & 2014

Initial Results

IndividualOperatingCompany

Drivers

IndividualOperatingCompany

Drivers

Gas PriceSensitivitiesGas Price

Sensitivities

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

20

Key forecasts based on 2010 Business Plan

Low Reference High

Gas Price ($/MMBtu) $5.30 $7.37 $9.18

Market Price ($/MWh) $60 $71 $77

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

21

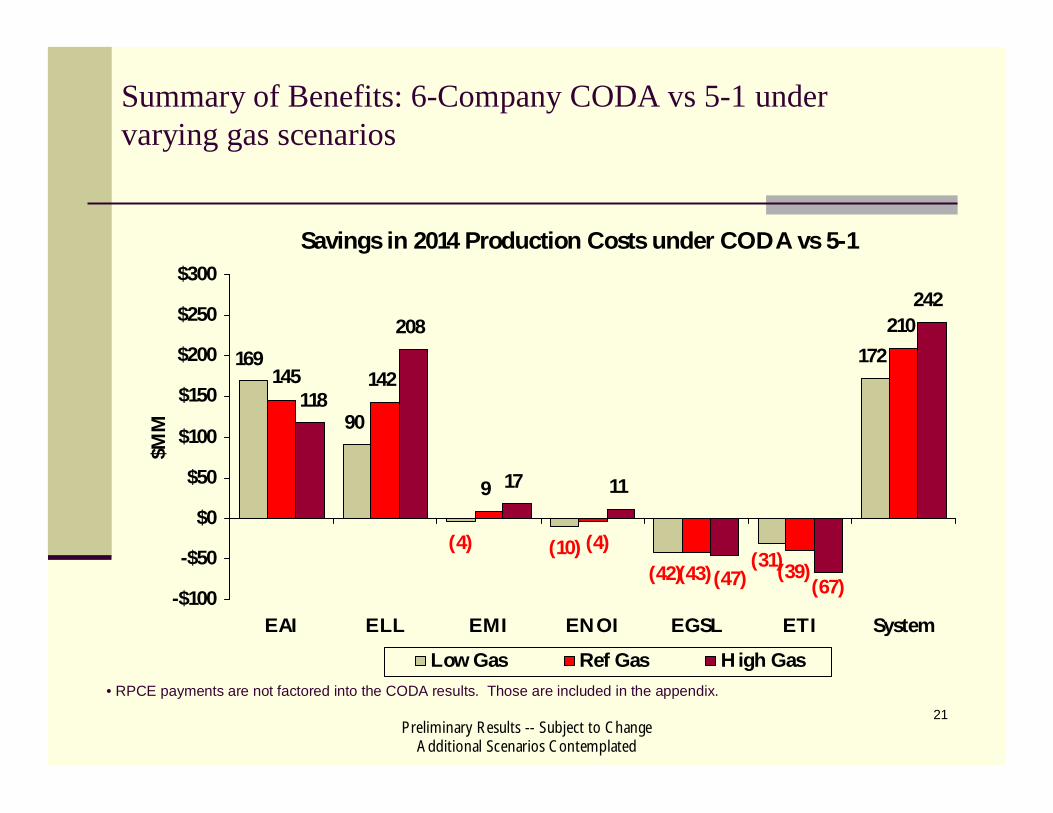

Summary of Benefits: 6-Company CODA vs 5-1 undervarying gas scenarios

Savings in 2014 Production Costs under CODA vs 5-1

90

(4) (10)

172142

9

210208

17 11

242

(42)(31)

169

(39)(43)(4)

145

(67)(47)

118

-$100

-$50

$0

$50

$100

$150

$200

$250

$300

EAI ELL EMI ENOI EGSL ETI System

$MM

Low Gas Ref Gas High Gas• RPCE payments are not factored into the CODA results. Those are included in the appendix.

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

22

Appendix

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

23

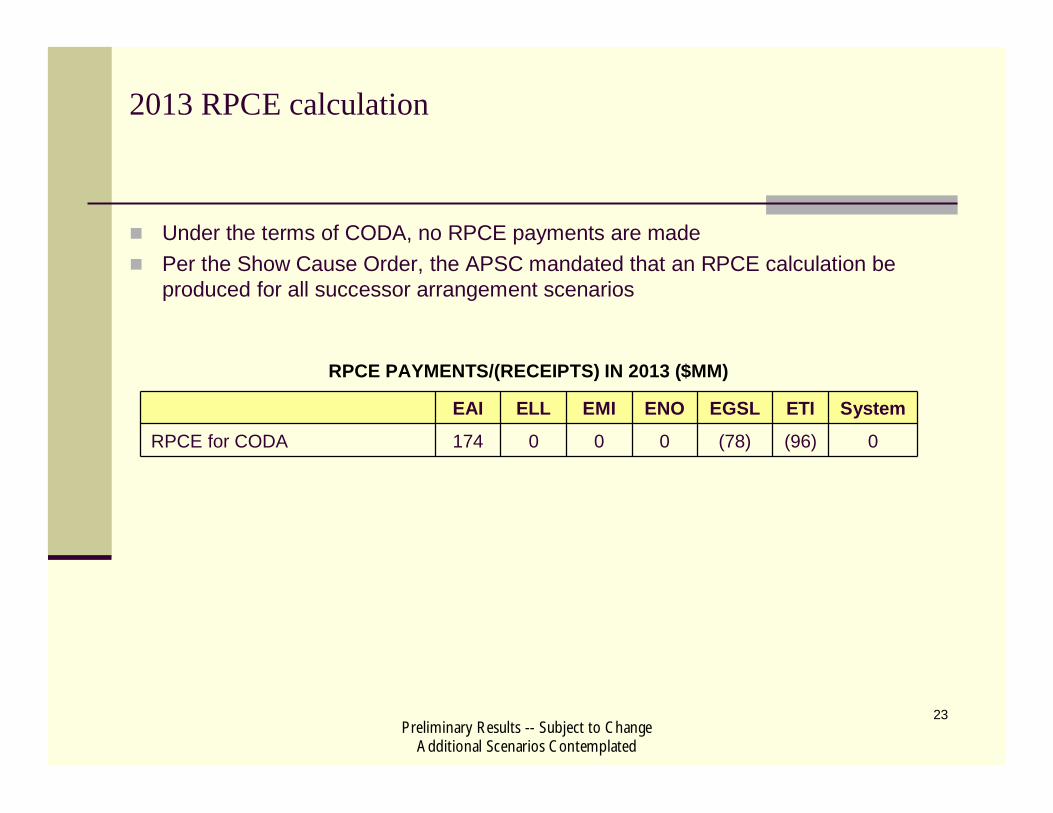

2013 RPCE calculation

RPCE PAYMENTS/(RECEIPTS) IN 2013 ($MM)

EAI ELL EMI ENO EGSL ETI System

RPCE for CODA 174 0 0 0 (78) (96) 0

Under the terms of CODA, no RPCE payments are madePer the Show Cause Order, the APSC mandated that an RPCE calculation beproduced for all successor arrangement scenarios

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

24

2014 RPCE calculation

RPCE PAYMENTS/(RECEIPTS) IN 2014 ($MM)

EAI ELL EMI ENO EGSL ETI System

RPCE for CODA 141 0 (1) 0 (54) (86) 0

Under the terms of CODA, no RPCE payments are madePer the Show Cause Order, the APSC mandated that an RPCE calculation beproduced for all successor arrangement scenarios

Preliminary Results -- Subject to ChangeAdditional Scenarios Contemplated

25

2014 RPCE calculation – Gas Price Scenarios

RPCE PAYMENTS/(RECEIPTS) UNDER GAS PRICE SCENARIOS ($MM)

EAI ELL EMI ENO EGSL ETI System

RPCE for CODA – Low Gas 15 0 0 0 0 (15) 0

RPCE for CODA – High Gas 227 0 (8) 0 (91) (128) 0