restructuring bulong debt_3

DESCRIPTION

Debt restructuring of BulongTRANSCRIPT

“Restructuring Bulong’s Project Debt”

Subject : INFIN-II

Guidance of Prof. Pramod

Submitted by Abhishek Shah, Kumar Abhishek

4/1/2013

Q1. Why did Bulong default in Jan 2000? Was it a result of a flawed strategy, poor

execution, or bad luck? Were any of the factors that caused them to default foreseeable?

Preston acquired Bulong from Resolute in July 1998 for A$319 million. Preston revenues in

1998 were A$ 231,000, consolidated assets of A$ 29 million. Preston funded the A$319 million

by borrowing A$260.5 million from Barclays in the form of Bridge loan, issuing A$39.9 million

equity to Resolute, assuming A$11.1 million in liabilities, and paying A$7.5 million of cash on a

deferred basis. At the time, the contracts had a negative net value on a mark-to-market basis of

A$33 million, a liability that Preston assumed from Resolute.

The projections made by Bulong assumed average nickel price of US$3.25, which was too

optimistic seeing the present conditions and London Metal Exchange’s spot and forward prices

of Nickel. Pricing of Nickel as per CRU assumptions were $2.03 and $2.07 for initial couple of

years which is about 62% less than what assumed by Preston. Also there was an exchange rate

risk.

Also Preston became a highly leveraged firm after the buyout. In 1998 Preston D/V value was

37.1% which soared to 83.3% in 1999. In 2000, Preston’s value of assets plunged by more than

200% from (in A$ 000) A$367,839 to A$ 115,100 creating a negative equity position for

Preston. Preston cash reserves were a mere A$2,233,000 in 1998. Bulong management had

assumed that commissioning would be completed in December 1998, but it started in March

1999 to be again stopped in August because certain valves were limiting throughput. The semi-

annual interest payments of A$ 18.3 million on the project bond that Preston had issued in

December 1998, were to commence on June15, 1999. The note issue had left BOP with cash

reserves of A$66 million, in June 1999. With this cash reserve Bulong could make both required

interest payment in 1999, but it failed to replenish the DSRA in Jan 2000, as between July 1999

till May 2000, Bulong faced operation problem and was not able to produce. The actual revenues

in 2000 were 155% less than what was forecasted. The revenues generated were not sufficient to

make payments to employees and suppliers.

The forecasts that Preston used were that of Resolute. Resolute’s forecast was of processing

600,000 tons of ore annually to produce 8000 tons of nickel and 670 tons of cobalt. Preston

(Exhibit-10) in its forecast kept the ore processes to be 600,000 tons but increased Nickel-output

sold to 9000 tons and Cobalt-output sold to 750 tons. The Bulong deposit averaged only 1 per

cent nickel, compared with grades of 3 per cent being mined at Kambalda at the time. Also

financial assumptions for (US$/lb) assumed by Preston were $3.30 for Nickel & $15-$25/lb for

Cobalt, whereas as per CRU Nickel prices were at $2.03/lb and $8.74-22.56/lb for Cobalt. Thus

we can say operating as well as financial forecasts done by Preston were very optimistic.

Thus we can say that operating side of Bulong bleached into the financial side and since the

financial side was also not robust enough Bulong defaulted in Jan 2000.

Bulong’s default in Jan 2000 was due to the failure of interest payment and the DSRA account

replenishing.

Let’s try to understand this default from the Operations as well as financial side.

Financial Side analysis:

- Bridge loan of A$260.5mn was taken during acquisition of Bulong by Preston

- Preston raised a bond of A$185mn to clear off the bridge loan debt

- In Yr. 2000, the borrowings from bond issue and other were used to clear of the

Bridge loan debt

- The interest on the bond to be paid for the 1st year was A$42.78mn

Let’s look at the below tables which highlights the Sources and Uses of fund:

Diff 99-98 % Diff 00-99 %

Sources

Sources

Acc Payable $ 14,341 3% Acc Payable $ 40,293 5%

ST Borrowings $ 43,643 9% ST Borrowings $ 321,653 38%

Provisons $ 2,867 1% Other $ 123,992 15%

Other $ - 0% Share Capital $ 1,562 0%

Acc Payable $ 3,143 1% Cash $ 20,618 2%

LT Borrowings $ 279,964 57% Receivables $ 4,124 0%

Provisons $ 69,514 14% Inventories $ 1,799 0%

Share Capital $ 73,750 15% Other $ 3,722 0%

Receivables $ - 0%

Investments $ 268 0%

Total $ 487,222 PPE $ 252,739 30%

Exploration $ 33,729 4%

Uses

Other $ 44,451 5%

Cash $ 19,209 4% Total $ 848,950

Receivables $ 5,201 1% Uses

Inventories $ 10,741 2% Provisons $ 2,278 0%

Other $ 6,608 1% Acc Payable $ 1,045 0%

Receivables $ - 0% LT Borrowings $ 279,964 33%

Investments $ 159 0% Provisons $ 66,883 8%

PPE $ 367,582 75% Reserves $ 1,562 0%

Exploration $ 7,095 1% Accumulated Losses $ 497,219 59%

Other $ 46,805 10%

Reserves $ 525 0%

Accumulated Losses $ 23,295 5%

Total $ 487,220 $ 848,951

From the above table we can easily identify that the ST borrowings (i.e. Bond issued + other

borrowings) A$321.653mn were used to pay back the LT borrowing (i.e. Bridge loan) of

A$279.964mn (A$260.5 + interest accrued). So the majority of source of fund in Yr.2000 was

used to pay the borrowings.

Now consider the interest to be paid for the bond issued (US$185 mn); in below table –

A$ A$ A$ A$ A$ A$

Yr Sr. No Bond Issue 1st half 2nd half Interest at 1st half Interest at 2nd half Total interest

2000 1 291.85 277.26 262.67 17.33 16.42 33.75

2001 2 262.67 248.08 233.48 15.50 14.59 30.10

2002 3 233.48 218.89 204.30 13.68 12.77 26.45

2003 4 204.30 189.70 175.11 11.86 10.94 22.80

2004 5 175.11 160.52 145.93 10.03 9.12 19.15

2005 6 145.93 131.33 116.74 8.21 7.30 15.50

2006 7 116.74 102.15 87.56 6.38 5.47 11.86

2007 8 87.56 72.96 58.37 4.56 3.65 8.21

2008 9 58.37 43.78 29.19 2.74 1.82 4.56

2009 10 29.19 14.59 0.00 0.91 0.00 0.91

The 1st year interest payment is of A$ 33.75mn

Considering the operations side now we try to find whether the revenue generated was enough to

facilitate the interest amount;

From the Exhibit 5 of the case, the Operating Revenue in year 2000 is A$ 62.259mn; which on

deduction of expenses becomes A$ - 33.51mn! (Ref: Exhibit 5). This clearly shows that the Op.

rev of A$ 62.59mn cannot clear the interest payment of A$ 33.75mn

To meet the interest payment of A$ 33.75mn, an operating revenue of at least A$ 129.52mn is

required – which as per the revenue projection (Exhibit 9) should be A$ 159.022mn.

Also, if we try to adjust the interest rates to meet the revenue generated; still as the Op. Exp. are

so huge that the interest payment would not be made.

Now let’s consider the Business side analysis

Business Side analysis:

The main objective of Preston to acquire Bulong was to utilize Bulong’s operation cash flow in developing

Marlborough mine and also, to utilize the expertise at Bulong for Marlborough.

But, without having detailed examination on profitability/break even of mine – they directly considered it as a rare

opportunity!

Let’s examine the Break even analysis, based on the Exhibit 5, 10 & 11; we can conclude that the BEP production

volume in 2000 were very high than the existing production! (Please refer below table)

Op Exp 51427.7 A$ (000)

Co rev 7416.8 A$ (000)

Ni rev 44010.9 A$ (000)

BEP Ni prod 9602.2 ton

Act Ni prod 4006.4 ton From the above table; the BEP Ni production required is 9602.2ton against current production of 4006.4ton! Almost

140% reduction!

Now suppose we consider that the above situation was for that particular year 2000 only. So we try to find when it

will achieve BEP considering average production and average prices. Please find the below table showing average

production required per month and its relative expenses and revenue generated.

2000 2001 2002 Avg/mnth

Ni ton/mnth 364 529 544 479

Rev(A$)/mnth 1669 2279 2455 2135

Co ton/mnth 19 34 33 29

Rev(A$)/mnth 674 1061 849 862

Op exp(A$)/mnth 4675 6832 6735 6081 The above table is summarized as below:

Total Avg Ton Total Avg Rev Total Avg OpExp

Existing 508 2996 6081

Additional 523 3085 0

Required 1031 6081 6081

The above table tells us the whole story on the required production to meet BEP. Bulong will have to mine on a n

average of 1031ton of Ni+Co per month, i.e. around 12000ton per year!! Which when compared with their

projections too, it doesn’t match throughout the period.

Now suppose say, they will rise their commodity prices and recover the break even; but the markets won’t allow this

too! As the prices of Ni and Co is falling y-o-y.

Based on above analysis we can say that the strategy to go for Bulong itself was a flawed! And

they were bound to default with the flawed strategy backed by weak operations and a bleeding

financial side.

Q2. How did Preston try to resolve the default? Why has it been difficult to restructure the

debt?

- Preston tried to resolve the default by taking working capital loan of A$30mn from

Barclays

- Also, looked towards restructuring by issuing equity of A$75mn and considered a JV

proposal with Australian firm Anaconda Nickel Ltd.

If we try to restructure by issuing more equity; say A$ 75mn, then the new structure would look

as below:

Yr. 2000 Restructure

d= $ 375,296 $ 300,296

plus A$75mn e= $ 102,137 $ 177,137

v= $ 477,433 $ 477,433

d/v= 78.61% 62.9%

e/v= 21.4% 37.1%

Debt break up

Bond $291,853 $ 233,529

Borrowings $83,443 $ 66,767

Total $375,296 $ 300,296

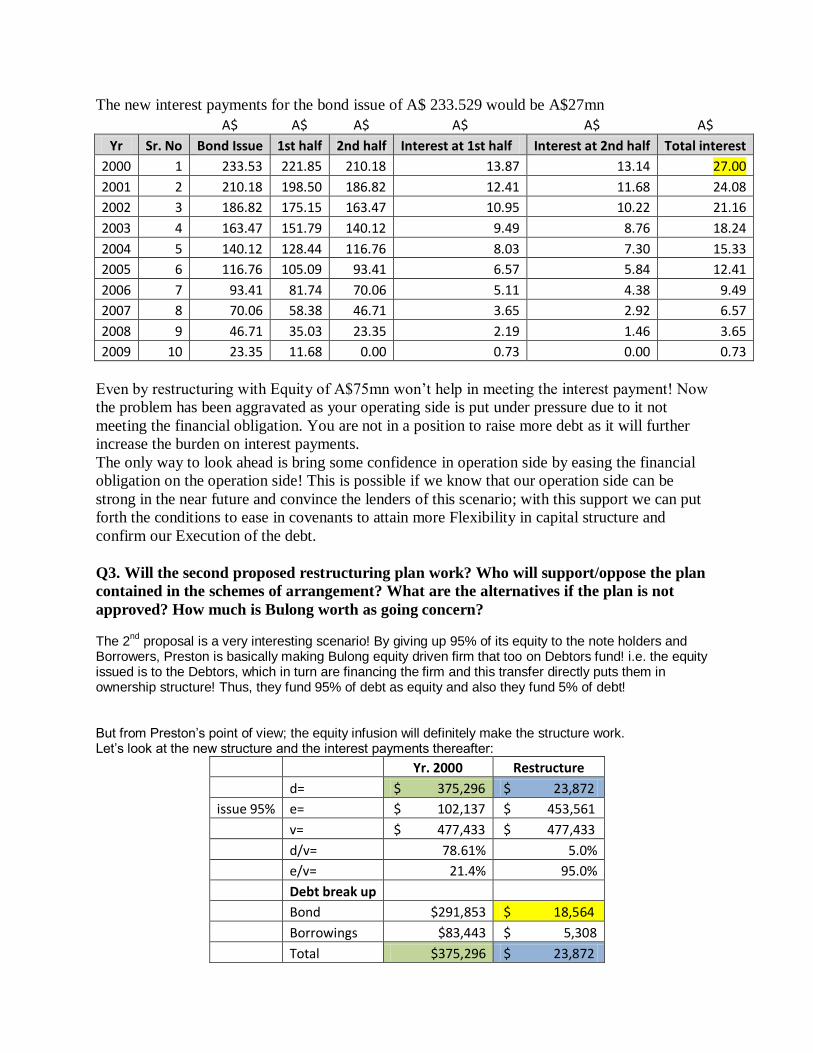

The new interest payments for the bond issue of A$ 233.529 would be A$27mn

A$ A$ A$ A$ A$ A$

Yr Sr. No Bond Issue 1st half 2nd half Interest at 1st half Interest at 2nd half Total interest

2000 1 233.53 221.85 210.18 13.87 13.14 27.00

2001 2 210.18 198.50 186.82 12.41 11.68 24.08

2002 3 186.82 175.15 163.47 10.95 10.22 21.16

2003 4 163.47 151.79 140.12 9.49 8.76 18.24

2004 5 140.12 128.44 116.76 8.03 7.30 15.33

2005 6 116.76 105.09 93.41 6.57 5.84 12.41

2006 7 93.41 81.74 70.06 5.11 4.38 9.49

2007 8 70.06 58.38 46.71 3.65 2.92 6.57

2008 9 46.71 35.03 23.35 2.19 1.46 3.65

2009 10 23.35 11.68 0.00 0.73 0.00 0.73

Even by restructuring with Equity of A$75mn won’t help in meeting the interest payment! Now

the problem has been aggravated as your operating side is put under pressure due to it not

meeting the financial obligation. You are not in a position to raise more debt as it will further

increase the burden on interest payments.

The only way to look ahead is bring some confidence in operation side by easing the financial

obligation on the operation side! This is possible if we know that our operation side can be

strong in the near future and convince the lenders of this scenario; with this support we can put

forth the conditions to ease in covenants to attain more Flexibility in capital structure and

confirm our Execution of the debt.

Q3. Will the second proposed restructuring plan work? Who will support/oppose the plan

contained in the schemes of arrangement? What are the alternatives if the plan is not

approved? How much is Bulong worth as going concern? The 2

nd proposal is a very interesting scenario! By giving up 95% of its equity to the note holders and

Borrowers, Preston is basically making Bulong equity driven firm that too on Debtors fund! i.e. the equity issued is to the Debtors, which in turn are financing the firm and this transfer directly puts them in ownership structure! Thus, they fund 95% of debt as equity and also they fund 5% of debt! But from Preston’s point of view; the equity infusion will definitely make the structure work. Let’s look at the new structure and the interest payments thereafter:

Yr. 2000 Restructure

d= $ 375,296 $ 23,872

issue 95% e= $ 102,137 $ 453,561

v= $ 477,433 $ 477,433

d/v= 78.61% 5.0%

e/v= 21.4% 95.0%

Debt break up

Bond $291,853 $ 18,564

Borrowings $83,443 $ 5,308

Total $375,296 $ 23,872

A$ A$ A$ A$ A$ A$

Yr Sr. No Bond Issue 1st half 2nd half Interest at 1st half Interest at 2nd half Total interest

2000 1 18.56 17.64 16.71 1.10 1.04 2.15

2001 2 16.71 15.78 14.85 0.99 0.93 1.91

2002 3 14.85 13.92 12.99 0.87 0.81 1.68

2003 4 12.99 12.07 11.14 0.75 0.70 1.45

2004 5 11.14 10.21 9.28 0.64 0.58 1.22

2005 6 9.28 8.35 7.43 0.52 0.46 0.99

2006 7 7.43 6.50 5.57 0.41 0.35 0.75

2007 8 5.57 4.64 3.71 0.29 0.23 0.52

2008 9 3.71 2.78 1.86 0.17 0.12 0.29

2009 10 1.86 0.93 0.00 0.06 0.00 0.06 The new bond issue would be of only A$18.56mn incurring an interest payment of A$2.15mn which is very much feasible to cover from operations! This structure will basically make the debtors to be the equity holders! There are chances of them (i.e. note holders and Barclays’) to resist against this; as they would be facing the whole risk of Bulong while Preston would be enjoying its Marlborough mines! But looking at the scenario, this option looks the best. As once the assets start generating revenue, the note holders and Barclays are in full position to sell off the assets and recover their funds. If the restructuring fails then it will ultimately lead to the liquidation of the Company, which again has its costs. Thus looking at the scenario the restructuring is best for both Preston as well as Barclays.

--x--