research investment idea 31 mar 2017 trent ltd. pcg... · pcg research private client group - pcg...

TRANSCRIPT

PCG RESEARCH INVESTMENT IDEA 31 Mar 2017

Trent Ltd.

Private Client Group - PCG RESEARCH P a g e | 1

Industry CMP Recommendation Add on Dips to band Target Time Horizon

Retail Rs 266 BUY Rs 235-266 Rs 305-350 3-4 Quarters

HDFC Scrip Code TRELTD

BSE Code 500251

NSE Code TRENT

Bloomberg TRENT

CMP as on 31 Mar 17 266

Equity Capital (Rs Cr) 33.23

Face Value (Rs) 1

Equity O/S (Cr) 33.23

Market Cap (Rs Cr) 8828

Book Value (Rs) 43.2

Avg. 52 Week Volumes

178927

52 Week High 270

52 Week Low 154

Shareholding Pattern (%)

Promoters 32.6

Institutions 41.9

Non Institutions 25.5

PCG Risk Rating* Yellow * Refer Rating explanation

Nisha Sankhala [email protected]

Trent Ltd owns and manages a number of retail chains in India. It primarily operates stores across three

formats: Westside, Star Bazaar and Landmark. A part of Tata Group, Trent was incorporated in 1998 and has

its headquarters in Mumbai.

Total of 95 Westside departmental stores are located in 58 cities offers menswear, women’s wear, kids’ wear,

footwear, cosmetics, perfumes and handbags, household furniture accessories, lingerie, and gifts. The

hypermarket business with Star Bazaar brand name provides staple foods, beverages, health and beauty

products, vegetables, fruits, dairy products, consumer electronics, and household items, at the most affordable

prices. In addition, Trent has also acquired 76% stake in Landmark, one of the largest books and music retail

chains in the country.

Currently stock is trading at 2x EV/Sales of FY19E and going forward we expect stock will trade at 2.3x and

2.6x EV/Sales, which brings the value of the stock at Rs 305 and 350. So we initiate Trent as a BUY at CMP

and add on decline at 235 for the targets of Rs 305 & 350 over the next 3-4 quarters.

INVESTMENT RATIONALE:

Favorable demographics, increasing urbanization, surge in discretionary spending, rising affluence amid

consumers, growing preference for branded products and higher aspirations are other factors which will drive

retail consumption in India.

GST will have a very positive impact going ahead on the retail sector. The implementation of GST would mean

an unhindered integration of goods and services transfer across the states. First of all, the procurement of

goods would become less cumbersome and this will open gates for vendors or suppliers to merge and have a

benefactor relation. The state boundary won’t be a hurdle anymore resulting in a low transportation cost and

better access. The simplified tax credits would mean fewer costs and profitable businesses.

Westside products are known for style and class amongst fashion conscious consumers. In recent years, the

chain has launched and refreshed a number of brands, available exclusively at Westside stores. Talking about

non-apparel businesses, Westside has brand like Footwear for Shoes Business, Studio west for fragrances,

Bath & Cosmetic business and Westside Home for Home Furnishing Industry.

Westside has slightly different business model format compared to peers. It has focused on Private labels and

In-house brand products for batter margins. Apparel contributes 80% of overall Westside revenues while the

overall 90% of the revenue comes from Private labels and In-house brand products. In-house brands offer

higher margins to retailers as they allow them to have complete control across the value chain. This also

enables them to give attractive discount offers to their customers.

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 2

Currently, Westside is operating through 95 stores across 58 Cities in India. Now Westside is planning to

accelerate expansion in the coming years by focusing broadly on two formats flagship stores - the prominent

full offer stores and the curated smaller stores in non-metros/ emerging micro-markets.

Average bill cycle of the company has seen 8% CAGR over FY12-16 and Walkins has increased from 20.36 mn

in FY12 to 25.15 mn in FY16 and going forward, we expect the trend to continue which would drive

performance of the company in the coming years.

RISK & CONCERNS:

Regulatory hurdles: Any regulatory change in the FDI policy will affect the growth of Hyper

City of Trent.

Highly price competitive business.

Threat form ever increasing trend of E-Commerce Business.

VIEW & VALUATION:

Favorable Indian Demographics, GST’s Favorable impact on whole Industry, Company’s expansion strategy and

continuously increasing Walkins & Avg. Bill Size puts Trent into sweet spot. Moreover, recent big listing of

DMart (One of the competitor) shows huge potential of the Retail Industry and this has led to re-rating of

Retail Sector. We believe Trent deserves higher multiple as being Tata Group Company, stable financials,

strong balance sheet as well as strong Brand pedigree.

Currently stock is trading at 2x EV/Sales of FY19 and going forward we expect stock will trade at EV/Sales of

2.3x and 2.6x which brings the value of the stock at Rs 305 and 350. Stock trades at ~19x EV/EBITDA and

based upon our target of Rs 350, we have implied ~25x EV/EBITDA on FY19E basis. So we initiate Trent a

strong BUY at CMP of Rs 266 and add on decline of 235 for the targets of Rs 305 & 350 for the period of 3-4

quarters.

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 3

BUSINESS BACKGROUND: The story began in 1998 when the Tata’s acquired Littlewoods a London based

retail chain by selling Lakme to Unilever. This acquisition was followed by the establishment of Trent Ltd.

With the headquarters in Mumbai it has presence in over 58 cities of India. Trent is a retail operations

company that owns and manages a number of retail chains in India. It primarily operates stores across three

formats: Westside, Star and Landmark.

Westside departmental stores: The Company has established 95 Westside departmental stores measuring

8000-34000 sq. ft. in floor space across 58 cities. The Westside stores have several departments to meet the

varied shopping needs of customers. These include menswear, women’s wear, kids’ wear, footwear,

cosmetics, perfumes and handbags, household furniture accessories, lingerie, and gifts.

Star Bazaar: Trent ventured into the hypermarket business in 2004 with Star Bazaar, providing an ample

assortment of products made available at the lowest prices. This store offers customers an eclectic array of

products that include staple foods, beverages, health and beauty products, vegetables, fruits, dairy products,

consumer electronics, and household items, at the most affordable prices. Star Bazaar also includes a large

range of fashionable in-house garments for men, women and children, exclusively available at the store.

Trent Hypermarket (THL) operates in a 50:50 JV between Trent Ltd & Tesco Plc UK.

Landmark: Trent has also acquired a 76% stake in Landmark, one of the largest books and music retail

chains in the country and began operations in 1987 with its first store in Chennai with a floor space of 5500

sqft.

ZARA: Zara is a leading global Spanish fashion apparel brand, focusing on customers at the premium end.

Trent operates Zara stores in a joint venture (JV) with the Inditex group of Spain with a shareholding of:

Inditex - 51% and Trent - 49%. Trent also has a JV with Inditex for the brand Massimo Dutti.

Trent History:

INVESTMENT RATIONALE:

1997 Tata sells

Lakme to Unilever &

acquires Littlewoods

1998 Launches first Westside

store in Bangalore

2004 Opens first Star Bazaar Store

in Ahmedabad

2005 Trent acquires

76% stake in Landmark

2014 Trent &

Tesco enter in a

50:50 JV for Trent Hypermarket Ltd

2008 Tesco enters India in

cash & carry business &

Ties-up with Star Bazaar

2009 Trent & Inditex form JV to bring Zara to India

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 4

Favorable Indian Demographics

India is a young nation with more than 50% of its population is in the working age group of 15-54 years. This

indicates significant influence wielded by this segment on consumption. The increasing desires to look good &

presentable, influenced by western culture and exposure to e-commerce and social media have boosted the

demand for more fashionable clothing and lifestyle products. Immense scope is seen for banners offering an

innovative product range to meet the aspirations of the brand conscious consumers with evolving

preferences.

Currently, 69% of India’s population lives in rural areas and this population contributes 54% to the total

retail consumption. Rapid urbanization in tier 2 and tier 3 cities is influencing the traction for organized retail

in these cities.

This has resulted in a surge in discretionary spending, which is expected to grow significantly from the

current 60% to ~72% of the overall spending by FY20E.

Market Size of Indian Retail Industry (US $ bn)

Source: BCG Retail 2020, HDFC sec Research

India - world’s youngest nation

Source: India Census 2011, HDFC sec Research

11 % CAGR

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 5

GST will be Game changer for the Retail Sector

GST will have a very positive impact going ahead on the retail sector. The implementation of GST would

mean an unhindered integration of goods and services transfer across the states. First of all, the

procurement of goods would become less cumbersome and this will open gates for vendors or suppliers to

merge and have a benefactor relation. The state boundary won’t be a hurdle anymore resulting in a low

transportation cost and better access. The simplified tax credits would mean fewer costs and profitable

businesses.

Strong Financials Compared to Peers

Where Majority of the players in the industry have been posting losses or minor profits barring one or two

players, Trent has managed to do turn around (Since 2015) on the back of strong management. Recently

also Trent has appointed Mr. Venu Nair, managing director (MD) of Marks & Spencer Reliance, India, as the

new chief commercial officer. Since FY15, Company has started making profits and proved itself among its

peers.

The revenue of the company in FY16 stood at Rs. 2464 Cr compared to previous Rs. 2381 Cr. While the

EBITDA came in at Rs. 204 Cr with margin of ~9%. However, bottom line dipped 50% on the back of higher

Finance costs. It is to be noted that FY15 included one off gain of Rs 115cr, so adjusted to the same, FY16

profits is up as compared to FY15.

Going further we expect robust growth in the financials of Trent because of its aggressive store addition

strategy, and major focus on in house brands and shift from unorganized to organized segment. We expect

revenue to post 22% CAGR in FY16-19, margin to improve from 8.5% in FY16 to 11% in FY19. This will lead

to a stellar growth in PAT. Consolidated PAT of Trent is expected to reach Rs.239 Cr by FY19E from Rs. 65 Cr

in FY16.

Higher emphasis on small box format stores and improved financials would lead to superior revenue growth

for Trent. We expect return ratios RoE, RoCE to surge sharply from c.4.4% and 8.5% to 13.6%, 18.9%,

respectively in FY19E.

Average bill cycle of the company has seen 8% CAGR over FY12-16 and Walkins has increased from 20.36

mn in FY12 to 25.15 mn in FY16 and going forward, we expect the trend to continue which would drive

performance of the company in the coming years.

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 6

Attractive Brand Portfolio

Westside products are known for style and class amongst fashion conscious consumers. In recent years, the

chain has launched and refreshed a number of brands, available exclusively at Westside stores.

Over the years, Westside has been sharpening its focus on fast moving value fashion targeted towards

women. Industry, per se kids wear and women’s wear apparel segment are expected to outperform overall

apparel growth (Technopak Analysis). With the evolving trend of western wear Westside has private label

brands like Wardrobe, Gia, Lov, Sassy and Soda.

India’s ethnic wear is dominated by unorganized players. But now this trend is also changing and People are

choosing branded clothes. So Westside, through its in house brands like Zuba, Bombay Paisley, Westside Mix

and Match & Westside SKD has endeavored to capture this opportunity.

Talking about non-apparel businesses, Westside has brand like Footwear for Shoes Business, Studio west for

fragrances, Bath & Cosmetic business and Westside Home for Home Furnishing Industry.

The below are few of many brand at Trent’s Westside store.

Source: Company, HDFC sec Research

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 7

Private labels and In-house brand format Brings in Higher Margin

Westside has slightly different business model format compared to peers. It has focused on Private labels

and In-house brand products for batter margins. Apparel contributes 80% of overall Westside revenues while

the overall 90% of the revenue comes from Private labels and In-house brand products.

In-house brands offer higher margins to retailers as they allow them to have complete control across the

value chain right from designing merchandise, branding, sourcing, logistics, distribution, promotion, display,

fixing price points and retail margins. Where in the Private label brand they can get a pretty good discounts

from the retailers the procure product from. This also enables them to give attractive discount offers to their

customers.

Foot Print Expansion strategy will be a key growth driver for Westside

A team of in-house property experts helps in identifying strategic locations for new stores. They are

supported by a well-defined set of processes for analyzing the potential market and catchment. This

ecosystem of people and processes, helps the company in identifying the right store and making it profitable

in a relatively short span of time.

Currently, Westside is operating through 95 stores in 58 Cities of India. Now Westside is planning to

accelerate expansion in the coming years by focusing broadly on two formats flagship stores- the prominent

full offer stores and the curated smaller stores in non-metros/ emerging micro-markets.

Increasing reach of Westside

Source: Company, HDFC sec Research

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 8

Restructuring of Landmark will bring change

Landmark, which was primarily a music & books retail format, had been undergoing constant restructuring

due to increased threats from the internet, which resulted in a decline in book sales. The music segment was

especially impacted by free digital downloads, which further gained momentum through growth of smart

phones.

The company has taken major steps for the restructuring in Landmark business like significant reduction in

store, change of product mix etc. this will make this business more profitable one.

VIEW & VALUATION:

Favorable Indian Demographics, GST’s Favorable impact on whole Industry, Company’s expansion strategy

and continuously increasing Walk-ins & Avg. Bill size puts Trent into sweet spot. Moreover, recent listing of

DMart (Avenues supermarts) has led to re-rating of Retail Sector. We believe Trent deserves higher multiple

as being Tata Group Company, stable financials, strong balance sheet as well as strong Brand recall.

Currently stock is trading at 2x EV/Sales of FY19 and going forward we expect stock will trade at EV/Sales of

2.3x and 2.6x which brings the value of the stock at Rs 305 and 350. Stock trades at ~19x EV/EBITDA and

based upon our target of Rs 350, we have implied ~25x EV/EBITDA on FY19E basis. So we initiate Trent a

strong BUY at CMP and add on decline of 266 for the targets of Rs 305 & 350 for the period of 3-4 quarters.

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 9

Debt has been reduced significantly

Source: Company, HDFC sec Research

Tremendous growth in PAT

Source: Company, HDFC sec Research

Revenue to witness CAGR of 22% over FY16-19E

Source: Company, HDFC sec Research

InHouse Brands to drive Higher margin in the Business

Source: Company, HDFC sec Research

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 10

Average bill size in increasing trend

Source: Company, HDFC sec Research

Walkins (No. In Millions)

Source: Company, HDFC sec Research

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 11

Income Statement (Cr)

Year ending March FY15 FY16 FY17E FY18E FY19E

Net Revenue 2284 2397 2949 3547 4311

Other Income 97.2 66.2 91.4 110.4 128.9

Total Income 2381 2464 3040 3658 4440

Growth (%) -0.5 3.4 23.4 20.3 21.4

Operating Expenses 2212 2260 2760 3291 3968

EBITDA 169 203 280 366 471

Growth (%) 139.1 19.9 38.0 30.6 28.7

EBITDA Margin (%) 7.4 8.5 9.5 10.3 10.9

Depreciation 74 67 74 82 92

EBIT 95 136 206 284 380

Interest 11 36 37 36 38

Exceptional Items 115 3 0 0 0

PBT 200 103 169 249 341

Tax 70 40 54 80 109

RPAT 129 63 115 169 232

Growth (%) LP -51.2 82.3 46.8 37.2

EPS 3.9 1.9 3.5 5.1 7.0

Source: Company, HDFC sec Research

Balance Sheet (Cr)

(Rs Cr) FY15 FY16 FY17E FY18E FY19E

SOURCE OF FUNDS

Share Capital 33.2 33.2 33.2 33.2 33.2

Reserves 1388.7 1404.9 1481.8 1594.0 1758.2

Minority Interest 2.6 10.3 10.0 10.0 10.0

Shareholders' Funds 1422.0 1438.1 1515.0 1627.2 1791.5

Total Debt 112.5 87.5 110.5 122.5 128.5

Long Term Provisions & Others 62.7 51.3 60.0 70.0 80.0

Total Source of Funds 1599.8 1587.2 1695.5 1829.7 2010.0

APPLICATION OF FUNDS

Net Block 734.4 806.9 883.0 921.0 1029.4

Investment 681.7 700.8 712.1 737.1 802.6

Long Term Loans & Advances 160.9 100.3 111.5 124.3 139.0

Total Non Current Assets 1576.9 1608.0 1706.5 1782.4 1971.0

Current Investments 58.0 25.8 53.8 63.8 98.8

Inventories 329.9 355.3 428.2 505.4 617.7

Trade Receivables 17.7 19.0 24.2 29.2 35.4

Short term Loans & Advances 160.5 222.3 233.4 245.1 257.3

Cash & Equivalents 55.5 63.0 77.8 154.6 114.7

Other Current Assets 8.0 5.6 3.5 3.7 3.9

Total Current Assets 629.7 690.9 821.0 1001.7 1127.8

Short-Term Borrowings 4.4 4.0 10.0 11.0 12.1

Trade Payables 221.3 241.6 306.3 379.2 461.2

Other Current Liab & Provisions 257.1 451.1 496.2 535.8 578.7

Short-Term Provisions 124.1 15.0 19.5 28.3 36.8

Total Current Liabilities 606.8 711.7 831.9 954.4 1088.8

Net Current Assets 22.9 -20.7 -11.0 47.4 39.0

Total Application of Funds 1599.8 1587.2 1695.6 1829.8 2010.0

Source: Company, HDFC sec Research

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 12

Cash Flow (Rs Cr)

Year ending March FY15 FY16 FY17E FY18E FY19E

Reported PBT 199.5 103.4 169.3 248.6 341.2

Non-operating & EO items 219.8 -83.3 -91.4 -110.4 -128.9

Interest Expenses 10.7 35.6 37.1 35.6 38.4

Depreciation 74.3 67.5 73.9 82.0 91.6

Working Capital Change 258.5 51.2 2.9 18.5 -31.6

Tax Paid -70.1 -40.3 -54.2 -79.6 -109.2

OPERATING CASH FLOW ( a ) 692.8 134.1 137.7 194.7 201.5

Capex -13.8 -140.0 -150.0 -120.0 -200.0

Free Cash Flow 678.9 -6.0 -12.3 74.7 1.5

Investments -440.7 41.3 -20.2 -37.9 -80.2

Non-operating income 97.2 66.2 91.4 110.4 128.9

INVESTING CASH FLOW ( b ) -357.4 -32.5 -78.8 -47.5 -151.3

Debt Issuance / (Repaid) -297.9 -36.4 31.7 22.0 16.0

Interest Expenses -10.7 -35.6 -37.1 -35.6 -38.4

FCFE 370.3 -77.9 -17.7 61.1 -20.8

Share Capital Issuance 0.0 7.7 -0.3 0.0 0.0

Dividend -33.2 -29.9 -38.2 -56.8 -67.8

FINANCING CASH FLOW ( c ) -341.8 -94.1 -44.0 -70.4 -90.2

NET CASH FLOW (a+b+c) -6.4 7.4 14.9 76.8 -39.9

Closing Cash 55.5 62.9 77.8 154.6 114.7

Source: Company, HDFC sec Research

Key Ratio %

FY15 FY16 FY17E FY18E FY19E

Profitability

EBITDA Margin 7.4 8.5 9.5 10.3 10.9

EBIT Margin 4.2 5.7 7.0 8.0 8.8

APAT Margin 5.7 2.6 3.9 4.8 5.4

RoE 10.7 4.4 7.8 10.8 13.6

RoCE 5.9 8.5 12.2 15.5 18.9

Solvency Ratio

Net Debt/EBITDA (x) 2.0 1.3 -4.0 -23.2 -15.5

D/E 0.1 0.1 0.1 0.1 0.1

Interest Coverage 8.9 3.8 5.6 8.0 9.9

PER SHARE DATA

EPS 3.9 1.9 3.5 5.1 7.0

CEPS 6.1 3.9 5.7 7.6 9.7

BV 42.8 43.3 45.6 49.0 53.9

Dividend 1.0 0.9 1.0 1.5 1.8

Turnover Ratios (days)

Debtor days 2.8 2.9 3.0 3.0 3.0

Inventory days 54.8 52.2 53.0 52.0 52.3

Creditors days 60.8 66.8 68.0 70.0 71.0

Working capital days -3.1 -11.8 -12.0 -15.0 -15.7

VALUATION (x)

P/E 68.3 140.4 76.8 52.3 38.1

P/BV 6.2 6.1 5.8 5.4 4.9

EV/EBITDA 52.3 43.6 31.6 24.2 18.8

EV / Revenues 3.9 3.7 3.0 2.5 2.1

Dividend Yield (%) 0.4 0.3 0.4 0.6 0.7

Source: Company, HDFC sec Research

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 13

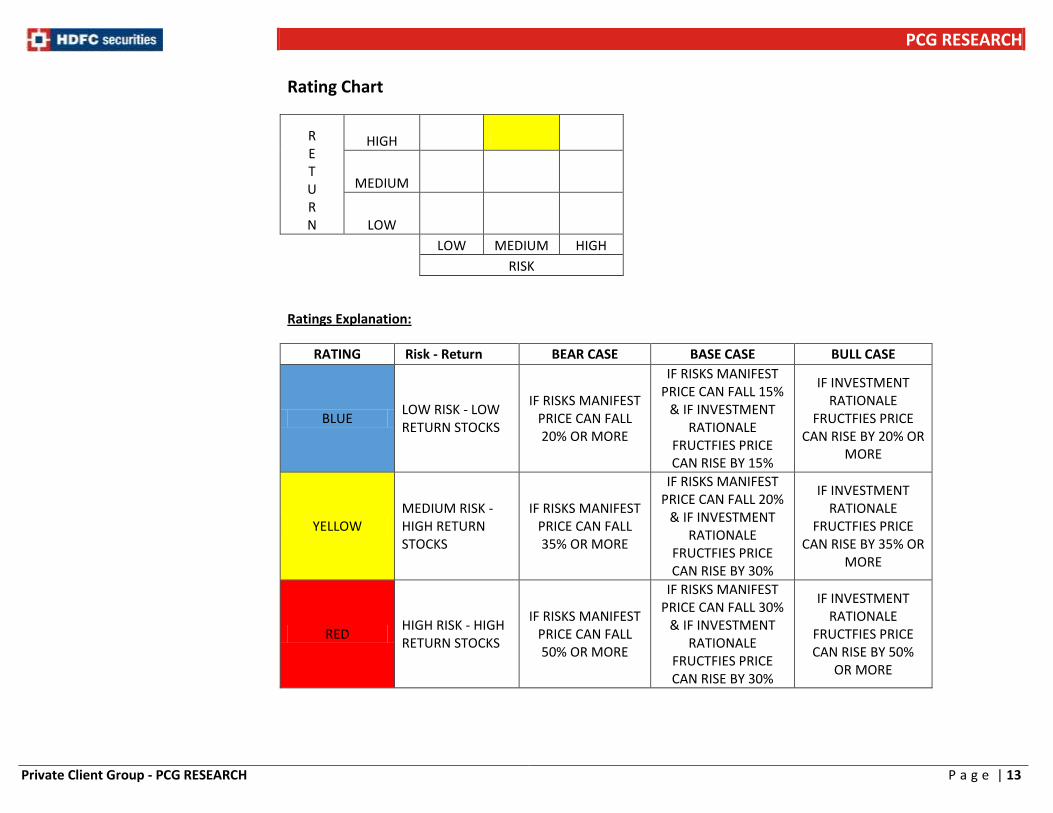

Rating Chart

R E T U R N

HIGH

MEDIUM

LOW

LOW MEDIUM HIGH

RISK

Ratings Explanation:

RATING Risk - Return BEAR CASE BASE CASE BULL CASE

BLUE LOW RISK - LOW RETURN STOCKS

IF RISKS MANIFEST PRICE CAN FALL 20% OR MORE

IF RISKS MANIFEST PRICE CAN FALL 15%

& IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 15%

IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 20% OR

MORE

YELLOW MEDIUM RISK - HIGH RETURN STOCKS

IF RISKS MANIFEST PRICE CAN FALL 35% OR MORE

IF RISKS MANIFEST PRICE CAN FALL 20%

& IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 30%

IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 35% OR

MORE

RED HIGH RISK - HIGH RETURN STOCKS

IF RISKS MANIFEST PRICE CAN FALL 50% OR MORE

IF RISKS MANIFEST PRICE CAN FALL 30%

& IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 30%

IF INVESTMENT RATIONALE

FRUCTFIES PRICE CAN RISE BY 50%

OR MORE

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 14

Rating Definition:

Buy: Stock is expected to gain by 10% or more in the next 1 Year. Sell: Stock is expected to decline by 10% or more in the next 1 Year.

PCG RESEARCH

Private Client Group - PCG RESEARCH P a g e | 15

I, Nisha Sankhala, MBA, author and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or her relative or HDFC Securities Ltd. or its associate does not have material conflict of interest. Any holding in stock – NO Disclaimer: This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HDFC Securities Ltd or its affiliates to any registration or licensing requirement within such jurisdiction. If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HDFC Securities Ltd . Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HDFC Securities Ltd may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments. HDFC Securities and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. HDFC Securities Ltd, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. HDFC Securities Ltd and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report. HDFC Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. HDFC Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business. HDFC Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HDFC Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HDFC Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the Subject Company or third party in connection with the Research Report. HDFC Securities Ltd. is a SEBI Registered Research Analyst having registration no. INH000002475 HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042

HDFC securities Limited, 4th Floor, Above HDFC Bank, Astral Tower, Nr. Mithakali 6 Road, Navrangpura, Ahmedabad-380009, Gujarat.

Website: www.hdfcsec.com Email: [email protected]