reprint indian journal of economics and development

TRANSCRIPT

Print ISSN 2277-5412 Online ISSN 2322-0430

Volume 12 No. 2April-June, 2016

Indian Journal of Economics and Development

Society of Economics and Developmentwww.soed.in

2004

Reprint

Indian Journal of Economics and DevelopmentEditorial Board

Chief Editor

Dr. S.S. ChahalFormer Director, Techonology Marketing and IPR Cell, Punjab Agricultural University, Ludhiana(India)

EditorsDr. S.S. Chhina, Former Dean, Faculty of Agriculture, Khalsa College, AmritsarDr. P. Kataria, Punjab Agricultural University, Ludhiana (India)Dr. Shalini Sharma, Punjab Agricultural University, Ludhiana (India)Dr. Sanjay Kumar, Punjab Agricultural University, Ludhiana (India)

MembersDr. Inderpal Singh, Trade and Investment, Economic Policy and Strategy, NSW (Australia)Dr. Timothy J. Colwill, Research Economist, Agriculture and Agri-food Canada, Ottawa (Canada)

Dr. Ravinderpal Singh Gill, Agriculture and Agri-Food Canada, Ottawa (Canada)Dr. Richard Kwasi Bannor, Ministry of Food and Agriculture, Kasoa-GhanaDr. I.P. Singh, SK Rajasthan Agricultural University, Bikaner (India)

Dr. J.L. Sharma, Eternal University, Baru Sahib (India)

Dr. K.K. Datta, National Dairy Research Institute, Karnal (India)

Dr. A.K. Vasisht, Indian Agricultural Statistics Research Institute, New Delhi (India)

Dr. V.P. Luhach, CCS Haryana Agricultural University, Hisar (India)

Dr. M.K.Sekhon, Punjab Agricultural University, Ludhiana (India)

Dr. Y.C. Singh, Central Agricultural University, Manipur (India)Dr. Jasdev Singh, Punjab Agricultural University, Ludhiana (India)Dr. Seema Bathla, Jawaharlal Nehru University, New Delhi (India)

Dr. R.B.Hile, MPKV, Rahuri (India)Dr. Baljinder Kaur Sidana, Punjab Agricultural University, Ludhiana (India)

Dr. Naresh Singla, Central University of Punjab, Bathinda

Dr. Sadiq Mohammed Sanusi, Federal University of Technology, Minna (Nigeria)

Dr. Rohit Singla, Boston College, Fulton (USA)

Dr. Deepak Upadhya, Local Initiatives for Biodiversity, Research and Development, Pokhara, Kaski (Nepal)

Ms. Donata Ponsian Kemirembe, Division of Environment, Vice President’s Office, Dar es Salaam (Tanzania)

Print ISSN 2277-5412Online ISSN 2322-0430

Indian Journal of Economics and Development

Society of Economics and Developmentwww.soed.in

Indian Journal of Economics and DevelopmentVolume 12 (2) 2016

©Society of Economics and Development

Printed and Published by Dr. Parminder Kaur on the behalf of the Society of Economics andDevelopment

Email: [email protected]: www.soed.inJournal is available on www.indianjournals.com

Printed at PRINTVIZION1766/1, Street No. 2Maharaj NagarLudhiana-141004Phone: 0161-4612199Email: [email protected]

Indian Journal of Economics and Development(Journal of the Society of Economics and Development)

Volume 12 April-June, 2016 No. 2Contents

Review ArticleChallenges and prospects of convenience food in India: An overview 203

Shivani Verma and Ramandeep Singh

Research ArticlesDomestic water consumption pattern and its linkage with socio-economic variables: A case study ofLudhiana city

215

Jasdeep Kaur, A.S. Bhullar, and R.S. GhumanSweet potato in Nigeria: Trends and socio-economic characteristics of farmers in selected local governmentarea of Kano state

223

Isah Musa Ahmad, Makama S.A., and Babagana G.A.Socio-economic impact of enterprises adoption on self-help group households in Punjab 229

Nirbhai Singh, Sanjay Kumar, and Jasdev SinghRelationship between urbanisation and economic growth: A causality analysis for India 237

Laxmi NarayanCost and return structure of tomato growers under open field, low tunnel and poly house conditions 243

Gurhemdeep Singh, J.S.Sidhu, and Jasdev SinghComposition, intensity and competitiveness of agricultural trade between India and ASEAN 249

Renjini V.R. and Amit KarStructure of assets among households in rural Punjab: An empirical analysis 255

Sukhdev Singh, Jasdeep Singh Toor, and Balwinder SinghAgricultural resource and income inequality in Northern Rajasthan 265

Mada Melkamu and N.K SinghBSE SME equity financing platform: A study of index risk return paradoxn 273

Amanjot Singh and Parneet KaurLevel of income, expenditure behaviour and poverty among farming community in rural Bihar 283

Ghanshyam PandayEconomic evaluation of Badrigad Watershed, Uttarakhand 293

Subhash Chandra and K.P. RaverkarSocio-economics of herbal processing units in Himachal Pradesh 301

Sukhjinder Singh and Sharanjit Singh DhillonAnalysis of growth, distributional pattern and density of tractors in India with special reference to Punjab 307

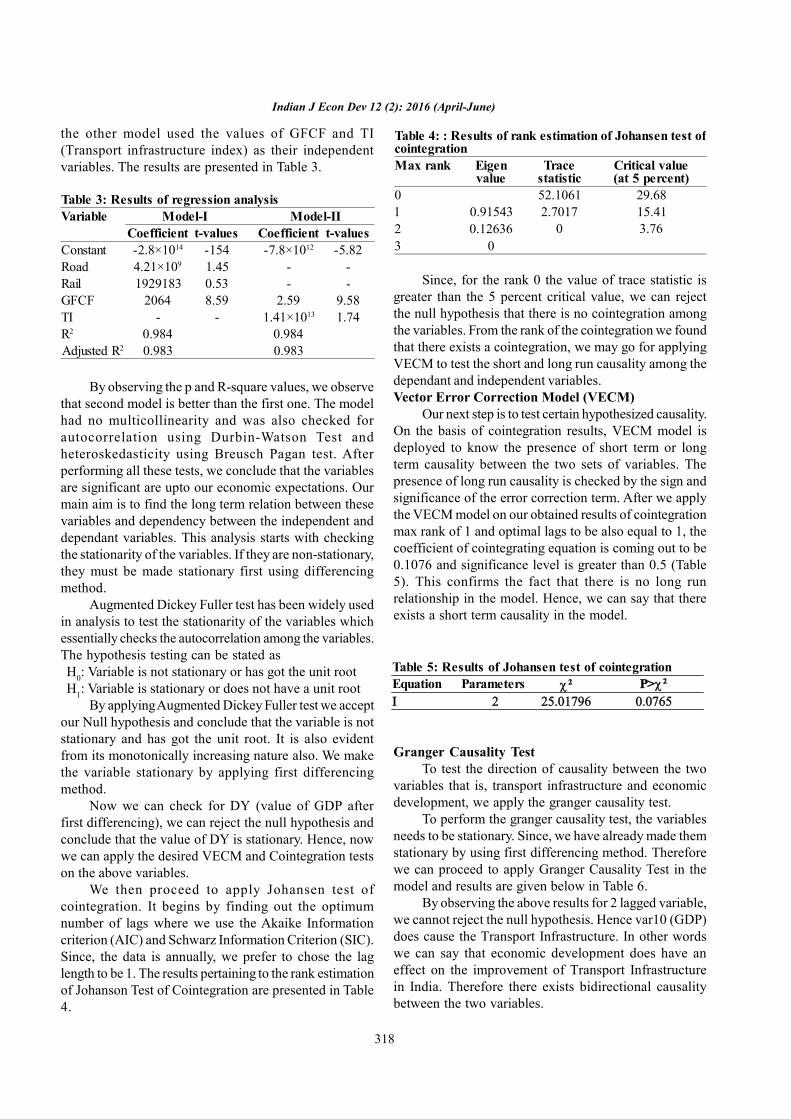

Vanusha Baregal and D.K.GroverInvestigating the relationship between transport infrastructure and economic growth: The case of India 315

Geet Kalra, Varun Chotia and Amit GoelSocio-economic factors affecting adoption behaviour of farmers for net-house vegetable cultivation inPunjab

321

Manjeet Kaur, M.K. Sekhon, Amrit Kaur Mahal, and Rakhi AroraAn empirical analysis of pilgrimage tourism in Jammu and Kashmir 327

Ruhi Refath Aara and Paramjeet Kaur Dhindhsa

Economic analysis of milk production among small holder dairy farmers in Punjab: A case study of Amritsardistrict

335

Kashish, Manjeet Kaur, M.K. Sekhon, and Vikrant DhawanHuman trafficking: A case of deceived aspiring emigrants in Punjab 341

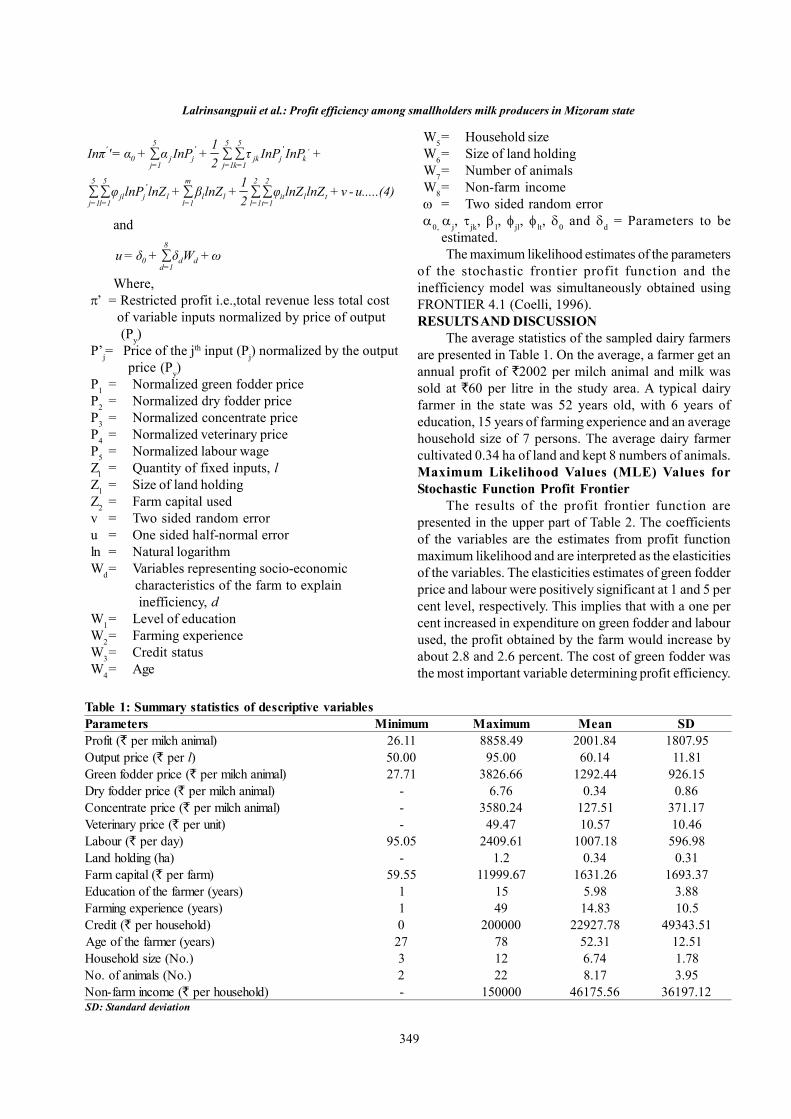

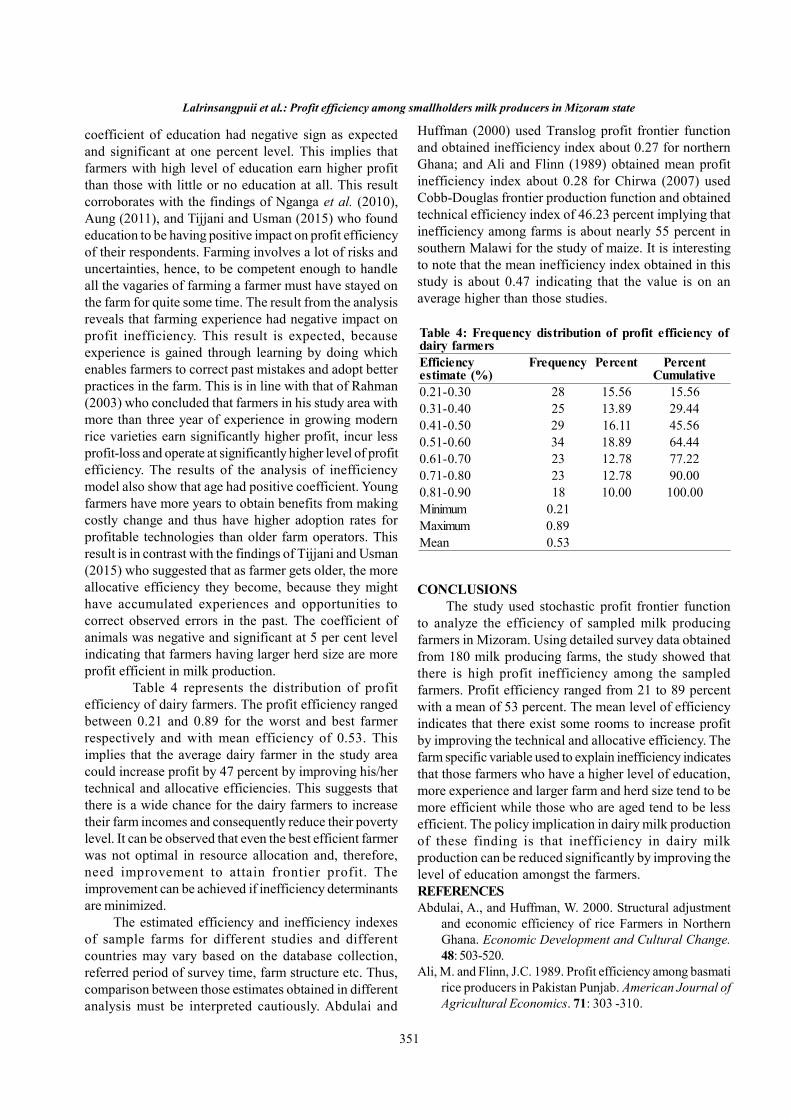

Shivani Sharma, Simran Kang Sidhu, and Shalini SharmaResearch NotesProfit efficiency among smallholders milk producers in Mizoram state 347

Lalrinsangpuii, R. Malhotra, and Laishram PriscillaEconomic analysis of milk production and marketed surplus in Chittorgarh district of Rajasthan 353

R.L. Bairwa, A.K. Chauhan, and Bulbul G.. NagraleEconomics and growth performance of chrysanthemumf flower in Tumkur district of Karnataka 359

Gunabhagya, S.S. Guledgudda, and B.C. RajurCotton cultivation in Punjab: An economic analysis 365

Shaminder Kumar and J. SachdevaEntrepreneurial behaviour of vegetable growers in Karnataka 369

N. Kumara, A. Nehal Farooquee, and P.V.K.SasidharDeterminants of participation of dairy farmers in dairy cooperative societies in Manipur 377

L. Priscilla, A.K. Chauhan, Lalrinsangpuii, and Bulbul G. NagraleProviding social security through public expenditure: An evidendce from India’s largest employment guaranteeprogramme

381

Paramita Saha and Soma DebnathEvaluation of vocational training programmes on mushroom cultivation 393

Dharminder Singh and K.B. SinghEconomics of farm business of selected small farmers in Akola district of Maharashtra 399

Aditi S. Ghevade, G.D.Rede, and G. B. Malthane

Abstracts (Ph.D./M.Phil./M.Sc. Theses) 405

.

INDEXING AND ABSTRACTING SOURCESIndian Journal of Economics and Development

Indexing and Abstracting Sources WebsiteAcademicKeys www.socialsciences.academickeys.comAdvanced Science Index www,journal-index.orgAcademic Resource Index (Research Bible) www.journalseeker.researchbib.comAmerican Economic Association (JEL) www.aeaweb.org

Centre for Agriculture and Biosciences www.cabi.orgInternational (CABI)Cite Factor www.citefactor.orgCrossref www.crossref.orgCNKI Scholar www.eng.scholar.cnki.netDirectory of Research Journals Indexing www.drji.orgDirectory of Science www.directorofscience.comDiva Enterprises Private Limited www.indianjournals.comEurasian Scientific Journal Index www.esjindex.orgGlobal Impact Factor (2015: 0.435) www.globalimpactfactor.com

Google Scholar www.scholar.google.co.inIndian Science and Research www.indianscience.inInfobase Index www.infobaseindex.comInstitute for Information Resources www.rjifactor.comInternational Impact Factor Services www.impactfactorservice.comInternational Society for Research Activity www.israjif.orgJIFACTOR www.jifactor.orgJ-Gate www.jgateplus.comNational Academy of Agricultural Sciences www.naasindia.orgNational Documentation Centre www.eskep.ekt.grScientific Indexing Services www.sindexs.org

Ulrichsweb Global Serials Directory www.ulrichsweb.serialssolutions.comWorldCat www.worldcat.orgYahoo Search www.in.search.yahoo.com

Society of Economics and DevelopmentObjectives

1. To promote awareness on the issues relating to economic development.2. To promote better social and ethical values to promote development.3. To promote economic prosperity and serve as a tool to create the consciousness for development.4. To conduct research and publish reports on economic issues.5. To organize seminars, symposia, workshops to discuss the economic problems.6. To offer consultancy, liaison and services as a facilitator.

Executive CommitteeFounder President

Dr. S.S. Chhina, Former Dean, Faculty of Agriculture, Khasla College, Amritsar

PresidentDr. M.S. Toor, Professor of Economics, PAU, Ludhiana

Vice PresidentsDr. D.K. Grover, Director, AERC, PAU, LudhianaDr. A.K. Chauhan, Principal Scientist (Dairy Economics), NDRI, KarnalDr. Simran K. Sidhu, Professor of Sociology, PAU, LudhianaDr. Pratibha Goyal, Professor of Business Management, PAU, LudhianaDr. Narinder Pal Singh, District Extension Specialist (FM), FASS (PAU), Amritsar

General SecretaryDr. Parminder Kaur, Professor of Economics, PAU, Ludhiana

Finance SecretaryDr. Mini Goyal, Professor of Economics, PAU, Ludhiana

Joint SecretaryMr. Taptej Singh, Research Fellow, Technology Marketing and IPR Cell, PAU, Ludhiana

MembersDr. Gian Singh, Professor of Economics, Punjabi University, PatialaDr. Deepak Shah, Professor, Gokhale Institute of Politics and Economics, Deccan Gymkhana, PuneDr. S.S. Burak, Professor, Maharana Pratap University of Agriculture and Technology, UdaipurDr. Ranjit Kumar, Professor, International Crops Research Institute for Semi-Arid Tropics, HyderabadDr. Varinder Kumar, Professor, CSK HP Krishi Vishvavidyalaya, PalampurDr. Prabhjot Kaur, Professor of Extension Education, PAU, LudhianaDr. Seema Sharma, Professor, PAU, LudhianaDr. J.M. Singh, Senior Agricultural Economist, PAU, LudhianaDr. M. Javed, Associate Professor of Statistics, PAU, LudhianaDr. Sukhmani Virk, Assistant Professor, PAU, LudhianaDr. Arjinder Kaur, Professor of Economics, PAU, LudhianaDr. Jatinder Sachdeva, Assistant Economist, PAU, LudhianaDr. H.S. Kingra, Farm Economist, PAU, LudhianaDr. Amanpreet Kaur, Research Scholar, PAU, LudhianaMs. Sadika Beri, Research Scholar, PAU, Ludhiana

Subscription RatesParticular Academics Students Institutional Processing fee

Annual Life Retired Annual Life Annual Per articleIndia (`) 600.00 4000.00 300.00 300.00 2000.00 2000.00 300.00Other countries ($) 25.00 250.00 - - - 250.00 10.00Membership should be paid by demand draft drawn in favour of Society of Economics and Development payable at Ludhiana andbe sent to the General Secretary, Society of Economics and Development, Department of Economics and Sociology, Punjab AgriculturalUniversity, Ludhiana-141004 (Punjab). Alternately, the membership fee can be deposited in Saving Bank Account No.29380100009412 (IFSC: BARB0PAULUD), Bank of Baroda, Punjab Agricultural University, Ludhiana.Log in http://soed.in/?page_id=3725 to remit membership fee via CCAvenue thruogh net banking, debit, or credit cards.Log in http://soed.in/?product=processing-fee to remit article process fee via CCAvenue thruogh net banking, debit, or creditcards.

203

www.soed.in

Challenges and Prospects of Convenience Food in India: AnOverviewShivani Verma* and Ramandeep Singh

School of Business Studies, Punjab Agricultural University, Ludhiana-141004

*Corresponding author’s email: [email protected]

Received: November 18, 2015 Accepted: April 10, 2016

Indian Journal of Economics and DevelopmentVolume 12 No. 2: 203-214

April-June, 2016DOI: 10.5958/2322-0430.2016.00127.X

ABSTRACTIn today’s scenario, convenience food industry is getting adapted to Indian type of requirements and is growing leaps andbounds in India. The present study throws light on convenience food along with categories, market size, opportunitiesand challenges of convenience food market in India. Convenience food is commercially prepared food designed for easeof consumption. Ready-to-eat (RTE) foods, Ready-to-use (RTU) foods and beverages are the three major categories ofconvenience food. In India, the convenience food industry, with a 90 percent contribution of RTE segment in 2013, hasbeen growing at a Compounded Annual Growth Rate (CAGR) of 15 percent from 2007 to 2013. The dairy productssegment constitutes about 35 percent of the total convenience food industry in India. Changing demographics of theIndian population, convenience and nutritional benefits are the opportunities that fuel the Indian convenience foodmarket. In addition, varied tastes, strong unorganized market, higher prices and poor infrastructure are the key challengesfor Indian convenience food industry.

KeywordsConvenience food, ready-to-eat, ready-to-use, seasonings, beverages

JEL codesL66, M30, 047, P27, Q18, Q22

INTRODUCTIONIndia is the world’s second largest producer of food

next to China and has the potential of being the biggestwith the food and agricultural sector. The food processingsector mainly deals with the preservation of perishableproducts and utilization of by-products for other purposes(Verma, 2015). In India, the food processing industry ishighly fragmented and is dominated by the unorganizedsector. About 42 percent of the output comes from theunorganized sector, 25 percent from the organized sectorand the rest from small players. Though the unorganizedsegment varies across categories but approximately 75percent of the market is still in this segment (Rais et al.,2013). North India, comprising Punjab, Haryana andHimachal Pradesh, is fast emerging a hub of the foodprocessing industry, thanks to changing lifestyle of itspopulation, growing income of the middle class andsurplus production of fruits, vegetables and milk (Singhand Bansal, 2013).

India’s food processing industry has grownannually at 8.4 percent for the last five years, up to 2012-

13 (www.makeinindia.com). The total food productionin India is likely to double in the next 10 years with thecountry’s domestic food market has estimated to reachUS$ 258 billion by 2015 and US$ 344 billion by 2025(Singh et al., 2012). The Confederation of Indian Industry(CII) has estimated that the food processing sector hasthe potential of attracting US$ 33 billion of investment in10 years and generates employment of 9 million person-days (Anonymous, 2015a). During the last five yearsending 2011-12, employment in registered foodprocessing sector has been increasing at an AnnualAverage Growth Rate of 3.79 percent and unregisteredfood processing sector supports employment to 47.9 lakhworkers (Anonymous, 2014).

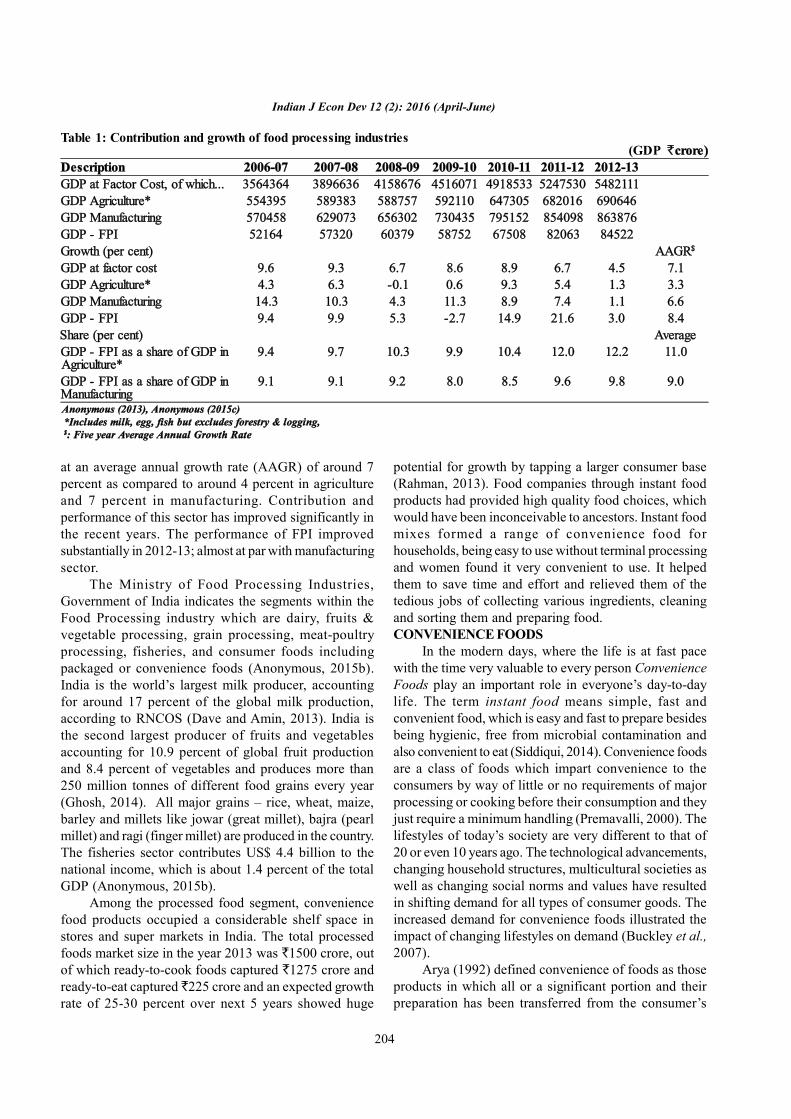

The perusal of Table 1 presented the contributionand growth of food processing industries (FPI). The foodprocessing sector forms an important segment of theIndian economy in terms of its contribution to GDP. Thesector contributed as much as 9.0 to 11.0 percent ofGDP in agriculture and manufacturing sector. During thelast 5 years ending 2012-13, FPI sector has been growing

204

Indian J Econ Dev 12 (2): 2016 (April-June)

at an average annual growth rate (AAGR) of around 7percent as compared to around 4 percent in agricultureand 7 percent in manufacturing. Contribution andperformance of this sector has improved significantly inthe recent years. The performance of FPI improvedsubstantially in 2012-13; almost at par with manufacturingsector.

The Ministry of Food Processing Industries,Government of India indicates the segments within theFood Processing industry which are dairy, fruits &vegetable processing, grain processing, meat-poultryprocessing, fisheries, and consumer foods includingpackaged or convenience foods (Anonymous, 2015b).India is the world’s largest milk producer, accountingfor around 17 percent of the global milk production,according to RNCOS (Dave and Amin, 2013). India isthe second largest producer of fruits and vegetablesaccounting for 10.9 percent of global fruit productionand 8.4 percent of vegetables and produces more than250 million tonnes of different food grains every year(Ghosh, 2014). All major grains – rice, wheat, maize,barley and millets like jowar (great millet), bajra (pearlmillet) and ragi (finger millet) are produced in the country.The fisheries sector contributes US$ 4.4 billion to thenational income, which is about 1.4 percent of the totalGDP (Anonymous, 2015b).

Among the processed food segment, conveniencefood products occupied a considerable shelf space instores and super markets in India. The total processedfoods market size in the year 2013 was `1500 crore, outof which ready-to-cook foods captured `1275 crore andready-to-eat captured `225 crore and an expected growthrate of 25-30 percent over next 5 years showed huge

potential for growth by tapping a larger consumer base(Rahman, 2013). Food companies through instant foodproducts had provided high quality food choices, whichwould have been inconceivable to ancestors. Instant foodmixes formed a range of convenience food forhouseholds, being easy to use without terminal processingand women found it very convenient to use. It helpedthem to save time and effort and relieved them of thetedious jobs of collecting various ingredients, cleaningand sorting them and preparing food.CONVENIENCE FOODS

In the modern days, where the life is at fast pacewith the time very valuable to every person ConvenienceFoods play an important role in everyone’s day-to-daylife. The term instant food means simple, fast andconvenient food, which is easy and fast to prepare besidesbeing hygienic, free from microbial contamination andalso convenient to eat (Siddiqui, 2014). Convenience foodsare a class of foods which impart convenience to theconsumers by way of little or no requirements of majorprocessing or cooking before their consumption and theyjust require a minimum handling (Premavalli, 2000). Thelifestyles of today’s society are very different to that of20 or even 10 years ago. The technological advancements,changing household structures, multicultural societies aswell as changing social norms and values have resultedin shifting demand for all types of consumer goods. Theincreased demand for convenience foods illustrated theimpact of changing lifestyles on demand (Buckley et al.,2007).

Arya (1992) defined convenience of foods as thoseproducts in which all or a significant portion and theirpreparation has been transferred from the consumer’s

Table 1: Contribution and growth of food processing industries(GDP `crore)

Description 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13GDP at Factor Cost, of which... 3564364 3896636 4158676 4516071 4918533 5247530 5482111GDP Agriculture* 554395 589383 588757 592110 647305 682016 690646GDP Manufacturing 570458 629073 656302 730435 795152 854098 863876GDP - FPI 52164 57320 60379 58752 67508 82063 84522Growth (per cent) AAGR$

GDP at factor cost 9.6 9.3 6.7 8.6 8.9 6.7 4.5 7.1GDP Agriculture* 4.3 6.3 -0.1 0.6 9.3 5.4 1.3 3.3GDP Manufacturing 14.3 10.3 4.3 11.3 8.9 7.4 1.1 6.6GDP - FPI 9.4 9.9 5.3 -2.7 14.9 21.6 3.0 8.4Share (per cent) AverageGDP - FPI as a share of GDP inAgriculture*

9.4 9.7 10.3 9.9 10.4 12.0 12.2 11.0

GDP - FPI as a share of GDP inManufacturing

9.1 9.1 9.2 8.0 8.5 9.6 9.8 9.0

Anonymous (2013), Anonymous (2015c) *Includes milk, egg, fish but excludes forestry & logging,

$: Five year Average Annual Growth Rate

205

Verma and Singh: Challenges and prospects of convenience food in India: An overview

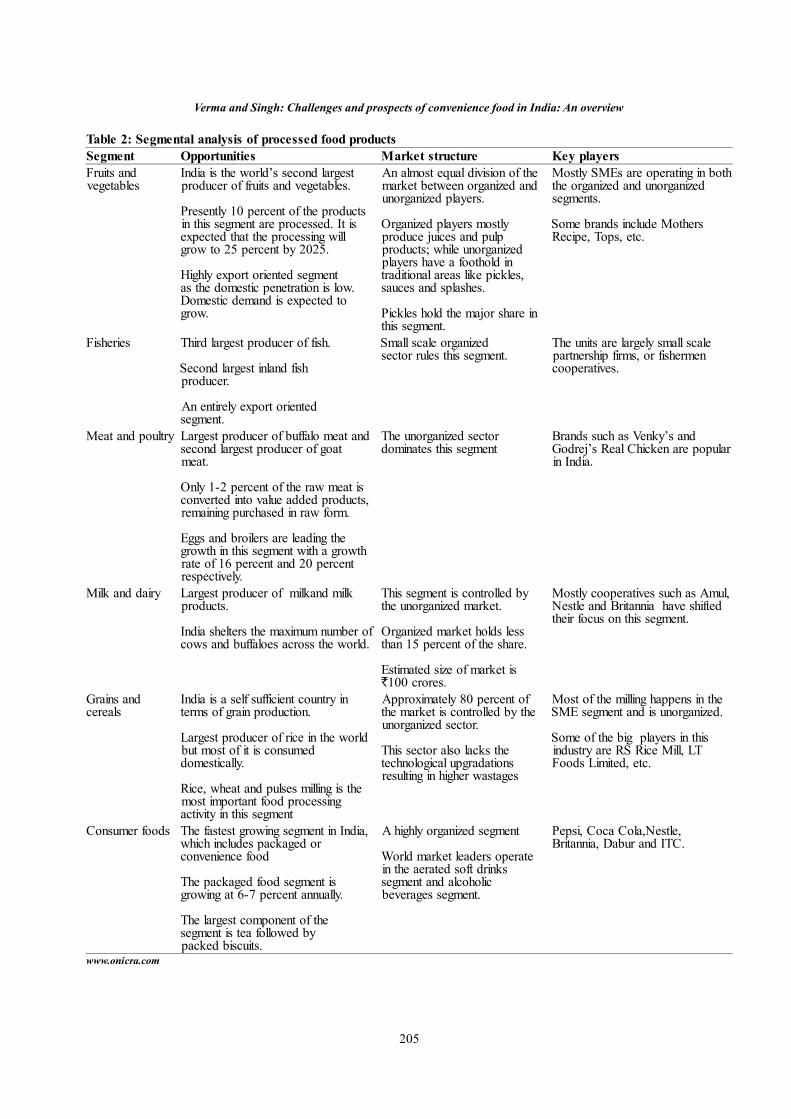

Table 2: Segmental analysis of processed food productsSegment Opportunities Market structure Key playersFruits andvegetables

India is the world’s second largestproducer of fruits and vegetables.

Presently 10 percent of the productsin this segment are processed. It isexpected that the processing willgrow to 25 percent by 2025.

Highly export oriented segmentas the domestic penetration is low.Domestic demand is expected togrow.

An almost equal division of themarket between organized andunorganized players.

Organized players mostlyproduce juices and pulpproducts; while unorganizedplayers have a foothold intraditional areas like pickles,sauces and splashes.

Pickles hold the major share inthis segment.

Mostly SMEs are operating in boththe organized and unorganizedsegments.

Some brands include MothersRecipe, Tops, etc.

Fisheries Third largest producer of fish.

Second largest inland fishproducer.

An entirely export orientedsegment.

Small scale organizedsector rules this segment.

The units are largely small scalepartnership firms, or fishermencooperatives.

Meat and poultry Largest producer of buffalo meat andsecond largest producer of goatmeat.

Only 1-2 percent of the raw meat isconverted into value added products,remaining purchased in raw form.

Eggs and broilers are leading thegrowth in this segment with a growthrate of 16 percent and 20 percentrespectively.

The unorganized sectordominates this segment

Brands such as Venky’s andGodrej’s Real Chicken are popularin India.

Milk and dairy Largest producer of milkand milkproducts.

India shelters the maximum number ofcows and buffaloes across the world.

This segment is controlled bythe unorganized market.

Organized market holds lessthan 15 percent of the share.

Estimated size of market is`100 crores.

Mostly cooperatives such as Amul,Nestle and Britannia have shiftedtheir focus on this segment.

Grains andcereals

India is a self sufficient country interms of grain production.

Largest producer of rice in the worldbut most of it is consumeddomestically.

Rice, wheat and pulses milling is themost important food processingactivity in this segment

Approximately 80 percent ofthe market is controlled by theunorganized sector.

This sector also lacks thetechnological upgradationsresulting in higher wastages

Most of the milling happens in theSME segment and is unorganized.

Some of the big players in thisindustry are RS Rice Mill, LTFoods Limited, etc.

Consumer foods The fastest growing segment in India,which includes packaged orconvenience food

The packaged food segment isgrowing at 6-7 percent annually.

The largest component of thesegment is tea followed bypacked biscuits.

A highly organized segment

World market leaders operatein the aerated soft drinkssegment and alcoholicbeverages segment.

Pepsi, Coca Cola,Nestle,Britannia, Dabur and ITC.

www.onicra.com

206

Indian J Econ Dev 12 (2): 2016 (April-June)

kitchen to the processing plant. He observed that all overthe world during the last two decades, the conveniencefood market had witnessed breath taking changes inquality and quantity of products available and thepackaging technology employed for their processing.Convenience food minimizes the working time but it doesnot save us from consuming high preservatives, extrasodium and hydrogenated fats. The study conducted byBanerjee et al. (2013) aimed to identify the factorsresponsible for awareness towards convenience foodamong women from Raipur city. Their study revealedthat 72 percent working and 94 percent non-workingwomen knew that consumption of convenience foodmight lead to obesity and cancer like diseases. Dealingwith convenience were difficult since multiplecharacteristics could contribute to the convenienceattribute of food products for example, preparationmethod and time, preservation, packaging and addedculinary skills were all characteristics which contributedto the convenience attribute of food products (Harris andShiptsova, 2007).

Priya and Mathew (2014) studied martialdissimilarities towards the consumption of conveniencefood. Their results showed that there was a significantdifference between married and unmarried respondentson the product attributes and sensory attributes and itwas observed that the behavioural, packing, healthconsequence factors of married and unmarried were notsignificantly different. Capps et al. (1985) analyzedconvenience foods based on the degree of processing oradded features and used three classifications ofconvenience food: 1) basic convenience foods, productswhere the processing was more related to preservationrather than to ease of preparation (foods with a single orlimited number of ingredients and foods with time orenergy inputs but not culinary expertise built in); 2)complex convenience foods, which encompassed multi-ingredient prepared mixtures and foods which have highlevels of time saving and energy inputs as well as culinaryexpertise built into the products; and 3) manufacturedconvenience foods, which deal with foods which haveno home-prepared counterparts. They also created a non-convenience food class composed of fresh (unprocessed)foods and home-produced, home-frozen home-cannedor home-preserved food items.

Ryan et al. (2002) revealed differences towardsconvenience orientation between six established consumersegments in the Irish population. The established groupsincluded: hedonistic food consumers (28 percent),conservative food consumers (21 percent), extremelyuninvolved food consumers (16 percent), enthusiasticfood consumers (14 percent), moderate food consumers(13 percent) and adventurous food consumers (8 percent).

It was found that the hedonistic, extremely uninvolvedand adventurous food consumers were the mostconvenience oriented out of the six groups, displayingthat differences were present between the groups’convenience-orientation. Olsen et al. (2007) investigatedcultural differences between five European countries inthe meaning of convenience orientation and the relationshipbetween convenience, attitudes and fish consumption. Itwas found that actual levels of convenience orientationdiffered from country to country. A study completed byMarquis (2005) confirmed the importance of conveniencein determining food choice among young, single adultsliving in residence halls. It was found that conveniencewas the most important food choice factor, while price,pleasure, health and concern about weight followed after.Similarly, Marquis and Manceau (2007) determined thatconvenience played a big role in determining food choicesof single men living in apartments in Montreal.

Botonaki et al. (2007) applied the model ofconvenience orientation in order to examine consumerbehaviour in the context of convenience food usage. Theirempirical results indicated that socio-demographiccharacteristics affect behaviour both directly andindirectly through perceived time resources andconvenience orientation towards meal preparation andclearing up. Even though traditionally convenience hasbeen examined in the context of strategies used by theconsumer to reduce time pressures, time is not the onlydimension involved in the consumption of conveniencefoods. Pearson et al. (1985) used preparation time as thefocal point to classify convenience foods, but alsoconsidered the use of the food in the household meal.The first component part of the categorization was adetailed system consisting of 14 categories. Those 14categories were then represented by a condensed three-category form consisting of no preparation, somepreparation and considerable preparation. Darian andCohen (1995) proposed two dimensions of convenience.The first one concerned the type of convenience, whichcould be saving time, physical energy and mental energy.The second dimension referred to the stage of the mealprocess that convenience was obtained.

The demand for convenience food has been fuelledby increased female participation in the workforce(Somogyi, 1990, Stafford and Wills, 1979). Warde (1999)emphasized that many people were constrained to eatwhat they called convenience foods as a provisionalresponse to intransigent problems of scheduling everydaylife. It was maintained that convenience food was requiredbecause people were too often in the wrong place; theimpulse to time-shifting aroused from the compulsion toplan ever more complex time-space paths in everydaylife. Brown and Mcenally (1993) suggested that it was

207

Verma and Singh: Challenges and prospects of convenience food in India: An overview

important to consider convenience at all stages in theprocess of food consumption and to determine theproportionate importance that consumers attached to timeand energy used in acquisition, consumption and disposal.Candel (2001) emphasized that there was a mental effortcomponent associated with convenience and in thecontext of meal preparation that related to the extent towhich the individual enjoyed the activity of preparingmeals. Studies have been conducted by manyresearchers, academicians, professionals and practitionerson convenience food yet there is tremendous room forresearch involving convenience foods. The present studyaimed at in-depth review of work related to changingscenario of food processing with reference toconvenience food in India.WHY CONVENIENCE FOODS?

Convenience food is gaining acceptance primarilyfrom Indian youth and is becoming part of day to day life(Srinivasan and Shende, 2015). With higher disposableincome, consumers today demand for quality and healthyfood that is offered as per their convenience and changingneeds (Jayadevan, 2012). The quality of convenience foodranges from the least expensive to the highest qualitygourmet items. Some of the economic advantages ofconvenience foods as perceived by Linstrom and Seigle(1976) are labour-saving equipment, time saving methodand reduced labour costs. With proper planning andmanagement, convenience items may reduce purchasingtime, storage facilities and food costs. Hales (2003) foundthat about 90 percent of Americans purchasedconvenience foods and nearly 25 percent used more timesaving convenience foods today than in 2001.Convenience foods require more freezer space but lesspreparation area. Faced with rising food prices, increasingwages and a lack of skilled personnel, the food serviceindustry can reduce some costs and increase efficiencyby using convenience foods. As a result of the widevariety of convenience foods, the operator can offercustomers special diet foods, such as those low incholesterol, salt, carbohydrates, or high in protein.CLASSIFICATION OF CONVENIENCE FOODS

Types of convenience foods can vary by countryand geographic region. Some convenience foods havereceived criticism due to concerns about nutritionalcontent and how its packaging may increase solid wastein landfills. Convenience foods are broadly classified intothree major categories:Ready-to-Eat (RTE) Foods: Ready-to-eat (RTE) foodsare foods intended to be consumed as they are. Thesefoods do not require additional cooking and are usuallystored in refrigeration or at room temperature (Muktawatand Varma, 2013). Goyal and Singh (2007) have exploredthat the young Indian consumer had passion for visiting

RTE outlets for fun and change but the consumeracceptability for RTE in the future would be decided onlyby the quality of food and customer service. The RTEmarket in India is expected to expand to reach 2,900crore by 2015, according to an analysis done by TataStrategic Management Group (Vijayabaskar andSundaram, 2012). In India, the convenience food industry,with a 90 percent contribution of ready-to-eat segmentin 2013 has been growing at a Compounded AnnualGrowth Rate (CAGR) of 15 percent from 2007 to 2013(Kulkarni, 2014). The consumers’ demand for RTE foodis showing consistent growth due to its convenient natureat a reasonable price and also the appeal of RTE food fortexture (Senthil et al., 2015).Ready-to-Use (RTU) Foods: Ready-to-use Foods (RTU)are highly fortified, oil-based nutrient dense pastesspecifically designed for the treatment ofmalnutrition. Patel et al. (2005) suggested thatsupplementary feeding with ready-to-use therapeutic foodpromotes better growth in children at risk of malnutritionthan the standard fortified cereal/legume-blended food.RTU foods are made from varying combinations of grains,pulses and seeds, milk powder, sugar, oil, vitamins andminerals. These foods need some preparations likecooking, frying, reconstitution, dilution etc. beforeconsumption. As they are oil-based, bacteria cannot growin ready-to-use foods which can be stored safely for upto one year without the need for refrigeration. In aresource poor setting, these products are literally life-savers (www.validnutrition.org). Thakur et al. (2013)compared the efficacy of locally-prepared ready-to-usetherapeutic food (LRUTF) and locally-prepared F100 dietin promoting weight-gain in children with severe acutemalnutrition during rehabilitation phase in hospital. Theyobserved that LRUTF promoted more rapid weight-gainwhen compared with F100 in patients with severe acutemalnutrition during rehabilitation phase.Beverages: Beverages are potable drinks which havethirst-quenching, refreshing, stimulating and nourishingqualities and they are specifically prepared for humanconsumption. Wolf et al. (2008) have demonstrated thatbeverages containing sugar, high fructose corn syrup(HFCS) or alcohol are handled differently by the bodythan when sugar or HFCS are incorporated in solidfoods. Increased sugar-sweetened beverages intake isassociated with weight gain and obesity (Malik et al.,2006). Beverages are broadly classified into alcoholicbeverages and non-alcoholic beverages. An alcoholicbeverage is a drink containing ethanol, commonly knownas alcohol. Current trends suggested increasinginvolvement of the alcoholic beverage industry in scientificresearch in ways that go beyond investigating the productsafety and consumer marketing (Babor, 2009). Non-

208

Indian J Econ Dev 12 (2): 2016 (April-June)

alcoholic beverage is a beverage that contains no alcohol.Such drinks are generally drunk for refreshment, or toquench people’s thirst. India is the third largest marketof alcoholic beverages.The beverages were estimated atUS$ 155 million out of which fruit juices and fruit-baseddrinks constituted US$ 60 million (Chetty, 2012).

SEASONINGS, KEY TO TASTY CONVENIENCEFOODS

The key to tasty and appetizing convenience foodsis the seasonings added to them. Seasoning is acomprehensive term applied to aromatic ingredients thatimprove the flavor of food products. These arecompounds, containing one or more spices, or spiceextractives, which when added to a food during itsmanufacturing, preparation or before it is served, enhancethe natural flavor of the food and increase its acceptanceby consumers (Farrell, 1998). Despite the limited use ofspices and seasonings in food, their impact on foodprocessed, stored or packaged is immense. If used in theright quantity, it is beneficial to health but then excessuse may result in harmful effects (Gadegbeku et al.,2014). Spices, herbs and dried vegetable seasonings arecurrently treated with ionizing radiation to eliminatemicrobial contamination (Khan and Abrahem, 2010).Proper seasoning is an art. With a little patience this art iseasy to learn and adapt. There are no hard-and-fast rulesfor the use of seasoning; however Thorner (1973) gavethree basic practices that should be followed: (1) underseason, rather than over season, because it is difficult toreduce the seasoning level without injuring the product;(2) experiment with various seasonings and becomefamiliar with the seasonings that are available; (3) useonly fresh, high-quality seasonings.MARKET SIZE OF CONVENIENCE FOODINDUSTRY IN INDIA

The total value of Indian food processing industrywas around US$12 billion in 2012 and was expected tobe around US$194 billion by 2015. According to theAgricultural & Processed Food Products ExportDevelopment Authority (APEDA), India’s agricultural andprocessed food exports stood at US$18.65 billion duringApril 2012-March 2013, which was US$13.22 billion lastyear. The Indian food processing sector employed over10 million people with total investment of US$24.04 billiongrown at 20 percent per annum in the last five years(Kulkarni, 2014). Demand for convenience foodsproducts in India remains need-based. Hence, productssuch as dairy and oil which form part of the daily stapledominate the total convenience food consumption.

Major players in the convenience food sector areNestle, Parle Agro, Britannia, Cadbury, MTR, KwalityDairy and ITC-Agro. The demand for convenience food

has increased manifold in past 2 years, according to asurvey conducted by Associated Chambers of Commerceand Industry of India (ASSOCHAM). The surveyindicated annual growth of about 40-60 percent between2011 and the end of 2015 for the convenience and ready-to-eat food segments. Growing at a compounded annualgrowth rate (CAGR) of about 15 to 20 percent annually,the Indian convenience food industry is likely to touch$30 billion by 2015 from the current level of $15 billionincluding snack foods, ready-to-eat foods, healthy andfunctional foods (Thomas and Pant, 2012).

THE RISE OF THE CONVENIENCE FOOD MARKETIN INDIA

Our ways of cooking have changed since morehouseholds are experiencing drastic change in eatinghabits and meals need to be prepared as quickly andconveniently as possible in order to keep up with the paceof life. There are various reasons which have graduallyresulted in the rise of convenience food in the country.These are:Pre-packaged Items: This is where convenience foodhas begun to fill the gap. More and more people now aredependent on convenience food as well as pre-packageditems to help them facilitate their day to day activity. Theconvenience food products are often sold in portioncontrolled, single serve packaging designed for portability.Then there are some packaged mixes which require somepreparation and cooking either in the oven or on the stovetop. Nutrition labelling on food products has emerged asa prominent policy tool for promoting healthy eating(Cowburn and Stockley, 2005). Therefore, nutrition labelson pre-packaged foods are among the most prominentsources of information (Campos et al., 2011) althoughingredients and health claims may be perceived as moreimportant (Reid and Hendricks, 1993).On-The-Go Lifestyle: The food-related lifestyledeterminants have been identified as important whenconsidering the convenience food purchasing patterns (DeBoer et al., 2004). Convenience foods are perceived toinvolve a lower degree of planning and preparation (Bogueand Sorenson, 2001). On-the-go lifestyles have emergedas a result of several factors, longer working hours, longercommuting times and a wider range of leisure activities,thus a family is less inclined to spend what valuable timeit has on preparing food. The main consequence of thishas been a greater reliance on ready-prepared foods inthe evening. Gofton (1995) suggested that in dual-incomehouseholds the family is often served convenience foodswhen parents are too tired and/or do not have enoughtime to prepare a home cooked meal.Mall Culture or Supermarkets: The supermarkets arecreating an environment of impulsive buying where most

209

of the convenience foods packed in their full splendourand tagged with hot offers lure the customers to try them.The entry of global supermarket chains into developingcountries has been an important factor behind theexpansion of the supermarket network and the increasedpresence of supermarkets in food markets (Arda, 2006).Emergence of mall culture has led to increase incompetition in the food retail supermarket industry(Mohan, 2013). Large-scale food manufacturers haveincreased their importance in the food system assupermarkets and have similar and indeed related impactsupstream in the food system’ (Reardon and Berdegué,2002).Packaging: One of the main reasons for the growth ofconvenience food is the packaging that comes with itand it serves a very important role to market conveniencefood products and improves their usefulness (Onyebuchi,2013). The packaging systems are now being designedkeeping environmental aspects in mind and there are eco-friendly packaging materials in the market that arerecyclable and biodegradable. McDaniel and Baker (1977)speculated that the consumers perceived a higher qualityof product in the more expensive packaging and they arewilling to sacrifice the ease of opening in order to obtaina higher quality. Further, packaging systems are designedkeeping storage aspects in mind and therefore we havezipper pack in the market, which is re-closable afteropening up the pack. There are also composite containerswith foil lining to keep the product fresh inside, whichcan replace conventional tin containers in the market.OPPORTUNITIES FOR THE CONVENIENCE FOODMARKET IN INDIA

Convenience food is a concept that is prevalent inthe developed world since long, while its inception intothe Indian market has been recent. According to Chadhaet al. (2010), the opportunities that fuel the Indianconvenience food market are:Changing Demographics of the Indian Population:The Indian population is younger, more urban, with greaterdisposable income and high purchasing power parity(PPP). Blaylock (1999) showed that a rise in incomehad a positive effect on food choice. Urban consumersare typically busier and more affluent, thus more willingto pay for convenience. The main impact of urbanizationhas created a growing demand for convenient products.Ready meals thus saw a strong 18 percent growth in2008 over the previous year, with these products regardedas a convenient alternative to cooking from scratch.Packaged soup also benefited, with dehydrated soupgrowing by 21 percent in current value terms, whileinstant noodles became an increasingly popular snack ormeal component, with sales thus growing by 24 percent.Veenma et al. (1995) assessed the significance of psycho-

social, demographic and life-style factors using acovariance structure model. Their results indicated thatthe most important determinants of convenience foodusage were nutritional knowledge, socio-economic status,marital status, employment status and stage in the familylife cycle.Convenience: It is evident that convenience plays aprominent role in the food choices of today’s customers.Wales (2009) suggested that food products offering lessconvenience are deemed to be less preferable toconsumers. The growing presence of drive-thruwindows, microwave dinners, take-out meals, homedelivery for groceries and internet shopping, alldemonstrate the importance of convenience in determiningfood choices (Jaeger and Cardello, 2007). Jaeger andMieselman (2004) investigated the construct of food-related convenience itself, looking over each stage of themeal preparation process. Scholderer and Grunert (2004)discovered that convenience includes dimensions of bothtime and effort saving. Verlegh and Candel (1999)investigated the situational influence as another dimensionof food related convenience and found that ‘socialsituations’ impacted the intention of consumers’consumption of convenience foods. Berry et al. (2002)indicated that convenience consumption has beenoperationalized by the use of convenience foods (frozenexpensive entrees, ready-to-eat cold cereal) and timesaving durables (microwave oven, dishwasher andfreezer).Nutritional and Health Benefits: The concept thatcertain foods can promote health by aiding in theprevention or treatment of disease, is increasingly gainingacceptance within the public arena and the scientificcommunity (Winter and Rodriguez, 1997). According tothe research conducted by Weaver et al. (2014), nutritionscientists, public health professionals, agriculturaleconomists, food scientists and other professionalsdedicated to meet the food and nutritional needs of peoplearound the globe recognized that fresh, local foods couldnot meet all nutritional requirements. Birch (1999) hasonly a rudimentary understanding of factors that promotethe development of food preferences consistent withhealthy diets and optimal nutrition. According to Dixonet al. (2006), consumers were being encouraged toembrace convenient food solutions, while also beingconcerned about the nutritional qualities of foods. Manyfood producers communicated that their products werepart of a healthy diet or claimed that they provided specifichealth benefits to inform the consumer through nutrientlabels and front-of-package labeling (McGuire, 2012).EMERGING NEW CATEGORIES OF CONVENIENCEFOOD IN INDIA

According to Agrawal, 2011, the emerging new

Verma and Singh: Challenges and prospects of convenience food in India: An overview

210

Indian J Econ Dev 12 (2): 2016 (April-June)

categories and the future of convenience food in Indiaare:Value-added Dairy Products: The dairy productssegment constitutes about 35 percent of the totalconvenience food industry in India. The main growthdrivers in this segment are curd, ghee and ice creams.Dairy product demand is anticipated to grow in the nextfive years by some 15-20 percent. Abdulla (2014) saidthat cheese and yoghurt offered a very good opportunityespecially when consumers had become more willing tospend on value-added dairy products. The IndianGovernment has been focusing on the dairy industry toothrough policy support with major supportive initiativeslike: In the sector of dairy processing, 51 percent offoreign equity participation is permitted. A recent reportby CARE Ratings said that the significant transformationtook place in the Indian demographic space which led toheightened consumer interest in Value-added DairyProducts. According to estimates, the share of Value-added Dairy Products in the milk and milk derivativessegment was growing at about 25 percent every yearand it was expected this pace would be maintained till2019-2020 (Das, 2014).Health-focused Snack Foods: Snack foods have beena long-time favorite in the Indian diet and now packagedand branded variants of namkeen, sweets and wafershave become the natural solution to the culinary cravingsinduced by the modern Indian lifestyle (Wanduragala,2012). Brown and Oqden (2004) compared the modellingand control theories of parental influence on children’seating attitudes and behaviour with a focus on snackfoods. His results showed that children whose parentsindicated greater attempts to control their child’s dietsreported higher intakes of both healthy and unhealthy snackfoods.

Ever increasing health consciousness gives a widermarket for snack foods which are health focused innature. Many of the large existing companies like ITCFoods, Parle Agro and Frito Lay, have considered thisfact and focused on this segment by targeting customersby offering a product line in health focused segment.Mclntyre and Baid (2009) analyzed that many adultsshowed some concerns about specific diet and healthrelated aspects of many snack products and would liketo be tempted by healthier versions. With the boostingdemand for healthy foods, this segment will witness ahuge share in snack food industry.Frozen Ready-to-eat Segment: The availability of frozenfoods in the Indian market has brought about great changein the life-style of the people of India. Among the differentreasons for the popularity of frozen foods in India, theimproving standard of living of the middle-income groupedpeople in India has also contributed towards the

development of companies in the frozen food industry inIndia (Raghu and Radha, 2013). As the penetration oforganized retail has improved, it is expected that therewill be a significant rise in the frozen ready-to-eat segment.Due to lack of cold chain facility, frozen food productswere wasted but with improved supply chain quality, theopportunities would be many (Rathore et al., 2010). It isexpected that freezer space will be doubled in the coming4-5 years, increasing the accessibility of frozen productsin the Indian market. The growth of this market will beaided by the entrance of enormous multinationalcompanies such as McCain, Tyson Foods, etc.Non-vegetarian Processed Foods: Presently, In Indiamajority of non-vegetarian products that are sold are inraw form which is unhygienic. Given the increasing needfor convenience and increasing health consciousness,considerable development in the category of nonvegetarian food is anticipated. The increasing penetrationof supermarkets/hypermarkets and improvement in coldchain infrastructure will significantly aid the growth ofthis segment. The Indian convenience food segment isnow at a very budding stage. Changes on the generalmarket, affecting demand and supply side such asincreasing urbanization, need for convenience, healthconsciousness, increased penetration of organized retailand entry of international players are key drivers that willresult in significant growth in the market.CHALLENGES FOR THE CONVENIENCE FOODINDUSTRY IN INDIA

Despite the strong growth, various regulatory andinfrastructural issues inhibit the growth of the Indianconvenience food industry. The main challenge is to retainthe nutritional value, aroma, flavour and texture of foods,and presenting them in near natural form with addedconveniences. Convenience foods need to be offered tothe consumer in hygienic and attractive packaging and atlow incremental costs (Harchekar, 2008). Key challengesfor the Indian convenience food industry are:Varied tastes and preferences: India is a country of aunique culture and has its own tastes and preferenceswhich again differ from region to region. Hence, it is achallenge for manufacturers to customise their productportfolio to local tastes and preferences rather than justbringing in global products into India.Strong unorganised market: All the key sectors of thefood industry face a stiff challenge from the unorganisedmarket. Success of the unorganised market is largely dueto easy accessibility and cheaper prices of products.Higher prices: Although convenience food products aretraditionally higher than the unorganised food market,increase in raw materials has led to further price rise inthe convenience food products.Poor infrastructure: Many categories in the convenience

211

food industry such as ready-to-eat products and frozenfood require strong infrastructural support such as coldchains and warehouses and dedicated logistic supply chainwhich is still not available in greater part of the country.CONCLUSIONS

The study revealed that the food-processing industryis significant for India’s development because it hasimportant link and synergy with industry and agriculture,the two main support of the economy. It widely comprisesof the various segments viz. fruits and vegetables, milkand milk products, poultry, packaged or convenience foodetc. Convenience foods are identified as those that arefully or partially prepared foods in which a significantamount of preparation time, culinary skills, or energyinputs have been transferred from the home kitchen tothe food processor and distributor. Convenience food isthe result of modern technological advances in the fieldof food processing, preservation techniques and theinvention of various new food additives. Its products arealways available, ready to use and properly stored butthey often contain a lot of fat and their energy content isalso very high. There is a greater demand for RTE foodsegments and the major attraction for these products isconvenience, availability and less time consumption tocook.

Ready-to-use products are free from bacteria andsafer than fresh goods, the shelf-life is longer, modernproduction techniques and preservation methods minimizethe nutritional loss of pre-cooked food products. Inregards to the dimensions of convenience, conveniencehas been defined to include aspects of both time and effortsaving - effort consisting of both physical and mentaleffort. As the customers are educated in present era theyfocus on consuming hygienic and healthy food products.Convenience foods contribute to both food security(ensuring that sufficient food is available) and nutritionsecurity (ensuring that food quality meets human nutrientneeds). The changing lifestyles and culture continue todrive the demand for convenience foods. Despite thestrong growth, various infrastructural issues and logisticsupply chain inhibit the growth of the Indian conveniencefood industry. The results of this study seem to be ofparticular interest not only for food product marketers,but also for food policy makers to understand the role ofconvenience food in India.REFERENCESAbdulla, H. 2014. Dairy in India: How to win over Indian

consumer. Culled from www.just-food.com/management-briefing/how-to-win-over-the-indian-consumer_id127988.aspx

Agrawal, N. 2011. Marketing strategies by packaged foodcompanies in India. M.Sc. Thesis, submitted to AstonBusiness School, England.

Anonymous. 2013. State of Indian Agriculture. Departmentof Agriculture and Cooperation, Ministry of Agriculture,Government of India, New Delhi.

Anonymous, 2014. Annual Report. Ministry of FoodProcessing Industries, Government of India, New Delhi.

Anonymous. 2015a. Importance of food processing sectorin India-A CII and Rabo equity report. Confederationof Indian Industry, New Delhi.

Anonymous. 2015b. A brief report on food processing sectorin India. Corporate Catalyst India, New Delhi.

Anonymous. 2015c. Data bank on economic parameters ofthe food processing sector. Ministry of Food ProcessingIndustries, Government of India, New Delhi.

Arda, M. 2006. Food retailing, supermarkets and foodsecurity: Highlights from Latin America. UNU- WorldInstitute for Development Economics Research. 107 (9):1-19.

Arya, S. S. 1992. Convenience foods- Emerging scenario.Indian Food Industry. 11 (4): 31-42.

Babor, T.F. 2009. Alcohol research and the alcoholic beverageindustry: Issues, concerns and conflicts of interest.Addiction.104 (1): 34-47.

Banerjee, S., Joglekar, A., and Kundle, S. 2013. Consumerawareness about convenience food among working andnon-working women. International Journal of ScientificResearch. 2 (10): 1-4.

Berry, L.L., Seiders, K., and Grewal, D. 2002. Understandingservice convenience. Journal of Marketing. 66 (4): 1-17.

Birch, L.L. 1999. Development of food preferences. AnnualReview of Nutrition. 19:41-62.

Blaylock, J. 1999. Economics, food choice and nutrition. FoodPolicy. 24 (2-3): 269-286.

Bogue, J. and Sorenson, D. 2001. An exploratory study ofconsumers’ attitude towards health-enhancing foods.Culled from www.ucc.ie

Botonaki, A., Natos, D., and Mattas, K. 2007. Exploringconvenience food consumption through a structuralequation model. In: Mediterranean Conference of Agro-Food Social Scientists, Spain: 1-18.

Brown, L.G. and Mcenally, M.R. 1993. Convenience:Definition, structure and application. Journal ofMarketing Management. 2 (2): 47-56.

Brown, R. and Oqden, J. 2004. Children’s eating attitudesand behaviour: a study of the modelling and controltheories of parental influence. Health EducationResearch. 19 (3): 261-271.

Buckley, M., Cowan, C., and McCarthy, M. 2007. Theconvenience food market in Great Britain: Conveniencefood lifestyle (CFL) segments. Appetite. 49 (3): 600-617.

Campos, S., Doxey, J., and Hammond, D. 2011. Nutrition labelson pre-packaged foods: A systematic review. PublicHealth Nutrition. 14 (8): 1496-1506.

Candel, M.J.J.M. 2001. Consumers’ convenience orientationtowards meal preparation: Conceptualization and

Verma and Singh: Challenges and prospects of convenience food in India: An overview

212

Indian J Econ Dev 12 (2): 2016 (April-June)

measurement. Appetite. 36 (1): 15-28.Capps, O., Tedford, J.R., and Havelicek, J. 1985. Household

demand for convenience and non-convenience foods.American Journal of Agricultural Economics. 67 (4):862-869.

Chadha, R., Bhatiani, R., and Dutta, S. M. 2010. Opportunitiesin the packaged food market in India. Technopakperspective. 3: 83-89.

Chetty, P. 2012. Major segments in India’s food processingsector. Culled from www.projectguru.in/publications/major-segments-in-indias-food-processing-sector/

Cowburn, G. and Stockley, L. 2005. Consumer understandingand use of nutrition labeling: A systematic review. PublicHealth Nutrition. 8 (1): 21-28.

Darian, J.C. and Cohen, J. 1995. Segmenting by consumertime shortage. Journal of Consumer Marketing. 12 (1):32-44.

Das, S. 2014. Dairies focus on value-added products for futuregrowth. Culled from http://www.business-standard.com/article/markets/dairies-focus-on-value-added-products-for-future-growth-114071900690_1.html

Dave, R. and Amin, A. 2013. Indian processed food: Recenttrends and future prospects. International Journal ofResearch in Business Management. 1 (1): 11-18.

De Boer, M., McCarthy, M., Cowan, C., and Ryan, I. 2004.The influence of lifestyle characteristics and beliefsabout convenience food on the demand for conveniencefoods in Irish market. Food Quality and Preference. 15:155-165.

Dixon, J.M., Hinde, S.J., and Banwell, C.L. 2006. Obesity,convenience and phood. British Food Journal. 108 (8):634-645.

Farrell, K.T. 1998. Spices, Condiments, and Seasonings.Aspen Publishers, Inc., New York

Gadegbeku, C., Tuffour, M.F., Katsekpor, P., and Atsu, B.2014. Herbs, spices, seasonings and condiments usedby food vendors in Madina, ACCRA. CaribbeanJournal of Science and Technology. 2: 589-602.

Ghosh, N. 2014. An assessment of the extent of foodprocessing in various food sub-sectors. Culled fromwww.iegindia.org/ardl/2014-11-n-1.pdf

Gofton, L. 1995. Food choice and the consumer. BlackieAcademic and Professional, Glasgow, United Kingdom.

Goyal, A. and Singh, N.P. 2007. Consumer perception aboutready-to-eat in India: An exploratory study. British FoodJournal. 109 (2): 182-195.

Hales, D. 2003. What (and who) is really cooking at yourhouse. Culled from http://www.utexas.edu/courses/stross/ant393b_files/ARTICLES/americaeats.htm

Harchekar, N. 2008. Indian processed food industry-Opportunities Galore. Culled fromwww.way2wealth.com/reports/RR150420084.PDF

Harris, J.M. and Shiptsova, R. 2007. Consumer demand forconvenience foods: Demographics and expenditures.Journal of Food Distribution Research. 38 (3): 22-36.

Jaeger, S.R. and Cardello, A.V. 2007. A construct analysis ofmeal convenience applied to military foods. Appetite.49 (1): 231-239.

Jaeger, S.R. and Meiselman, H.L. 2004. Perceptions of mealconvenience: The case of at home evening meals.Appetite. 42 (3): 317-325.

Jayadevan, G.R. 2012. Ethics and marketing of processedfoods in India. Abhinav National Journal of Researchin Commerce & Management. 1 (12): 8-15.

Khan, A. and Abrahem, M. 2010. Effect of irradiation on qualityof spices. International Food Research Journal. 17 (4):825-836.

Kulkarni, S. 2014. CAGR of convenience food market 15%and tetra pack preferred packaged material. Culled fromwww.fnbnews.com.

Linstrom, H.R. and Seigle, N. 1976. Convenience foods forthe hotel, restaurant and institutional market: Theprocessor’s view. National Economic Analysis Division,Economic Research Service, U.S. Department ofAgriculture, Washington, D.C.

Malik, V.S., Schulze, M.B., and Hu, F.B. 2006. Intake of sugar-sweetened beverages and weight gain: a systematicreview. The American Journal of Clinical Nutrition. 84(2): 274-288.

Marquis, M. 2005. Exploring convenience orientation as afood motivation for college students living in residencehalls. International Journal of Consumer Studies. 29(1): 55-63.

Marquis, M. and Manceau, M. 2007. Individual factorsdetermining the food behaviours of single men living inapartments in Montreal as revealed by photographs andinterviews. Journal of Youth Studies. 10 (3): 305-316.

McDaniel, C. and Baker, R.C. 1977. Convenience foodpackaging and the perception of product quality. Journalof Marketing. 41 (4): 57-58.

McGuire, S. 2012. Front-of-Package Nutrition Rating Systemsand Symbols: Promoting Healthier Choices. TheNational Academies Press, Washington, DC, USA.

Mclntyre, C. and Baid, A. 2009. Indulgent snack experienceattributes and healthy choice alternatives. British FoodJournal. 111 (5): 486-497.

Mohan, R. 2013. To identify the factors impacting customersatisfaction in food retail supermarkets. InternationalJournal of Research and Development- A ManagementReview. 2 (2): 51-54.

Muktawat, P. and Varma, N. 2013. Impact of ready to eat foodtaken by single living male and female. InternationalJournal of Scientific and Research Publications. 3 (11):1-3.

Olsen, S., Scholderer, J., Brunsø, K., and Verbeke, W. 2007.Exploring the relationship between convenience and fishconsumption: A cross-cultural study. Appetite. 49 (1):84-91.

Onyebuchi, N.J. 2013. Production, Characterization andshelf-life studies of Irvingia Gabonensis based ‘Ready-

213

to-prepare soup’. M.Sc. Thesis, submitted to Universityof Ibadan, Nigeria.

Patel, M.P., Sandige, H.L., Ndekha, M.J., Briend, A., Ashorn,P., and Manary, M.J. 2005. Supplemental feeding withready-to-use therapeutic food in Malawian children atrisk of malnutrition. Journal of Health, Population andNutrition. 23 (4): 351-357.

Pearson, J.M., Capps, O., Gassman, C., and Axelton, J. 1985.Degree-of-readiness classification system for foods:Development, testing and use. Journal of ConsumerStudies and Home Economics. 4: 249-255.

Premavalli, K.S. 2000. Convenience foods for defence forcesbased on traditional Indian foods. Defence ScienceJournal. 50 (4): 361-369.

Priya, G.B.S. and Mathew, A. 2014. A study on martialdissimilarity towards processed convenience food.ZENITH International Journal of MultidisciplinaryResearch. 4 (12): 222-232.

Raghu, G. and Radha, S. 2013. The market potential of frozenfood products in Bangalore. Social Science ResearchNetwork. (9): 1-29.

Rahman, T. 2013. RTE and RTC foods-A new era in theprocessed food industry with special reference to MTR.International Journal of Management and SocialSciences Research. 2 (5): 63-67.

Rais, M., Acharya, S., and Sharma, N. 2013. Food processingindustry in India: S&T capability, skills and employmentopportunities. Journal of Food Processing &Technology. 4 (9): 2-13.

Rathore, J., Sharma, A., and Saxena, K. 2010. Cold chaininfrastructure for frozen food: A weak link in Indian retailsector. The IUP Journal of Supply Chain Management.7 (1&2): 90-103.

Reardon, T. and Berdegué, J. 2002. The rapid rise ofsupermarkets in Latin America: Challenges andopportunities for development. Development PolicyReview. 20 (4): 371-388.

Reid, D.J. and Hendricks, S. 1993. Consumer awareness ofnutrition information on food package labels. Journalof Canadian Dietetic Association. 54 (3): 127-131.

Ryan, I., Cowan, C., McCarthy, M., and O’Sullivan, C. 2002.Food-related lifestyle segments in Ireland with aconvenience orientation. Journal of International Food& Agribusiness Marketing. 14 (4): 29-47.

Scholderer, J. and Grunert, K.G. 2004. Consumers, food andconvenience: The long way from resource constraintsto actual consumption patterns. Journal of EconomicPsychology. 26 (1): 105-128.

Senthil, A., Kumar, B.S., and Pathak, A. 2015. Comparativequality evaluation of commercial extruded snacks.Wudpecker Journal of Food Technology. 3 (1): 1-11.

Siddiqui, A. 2014. Study to evaluate the preferences ofworking women and housewives towards packaged andnon packaged food. Abhinav National Journal ofResearch in Commerce & Management. 3 (6): 1-6.

Singh, H. and Bansal, M. 2013. Major problems and prospectsof food processing industry in Punjab. InternationalJournal of Management Excellence. 1 (1): 7-12.

Singh, S.P., Tegegne, F., and Ekenem, E. 2012. The foodprocessing industry in India: Challenges andopportunities. Journal of Food Distribution Research.43 (1): 81-89.

Somogyi, J.C. 1990. Convenience foods and the consumer-Current questions and controversies. NutritionalAdaptation to New Lifestyles. 45: 104-107.

Srinivasan, S. and Shende, K.M. 2015. A study on the benefitsof convenience foods to working women. ATITHYA: AJournal of Hospitality. 1 (1): 43-50.

Stafford, T.H. and Wills, J.W. 1979. Consumer demandincreasing for convenience in food products. NationalFood Review. 13: 15-17.

Thakur, G.S., Singh, H.P., and Patel, C. 2013. Locally-preparedready-to-use therapeutic food for children with severeacute malnutrition: A controlled trial. Indian Pediatrics.50 (3): 295-299.

Thomas, T. and Pant, S. 2012. Rise of convenience food-Impact on the industry. Culled from http://www.fnbnews.com.

Thorner, M.E. 1973. Convenience and Fast food handbook.The AVI Publishing Company, Inc., Westport,Connecticut

Veenma, K.S., Kistemaker, C., Lowik, M.R.H., Hulshof,K.F.A.M., Steerneman, A.G.M., and Wedel, M. 1995.Socio-demographic, psycho-social and life-style factorsaffecting consumption of convenience food. EuropeanAdvances in Consumer Research. 2: 149-156.

Verlegh, P.W.J. and Candel, M.J.J.M. 1999. The consumptionof convenience foods: Reference groups and eatingsituations. Food quality and preference. 10 (6): 457-464.

Verma, S. 2015. Role of agro-industries for sustainableagricultural development in India. Indian Journal ofEconomics and Development. 11 (1): 277-284.

Vijayabaskar, M. and Sundaram, N. 2012. A market study onkey determinants of ready-to-eat/cook products withrespect to Tier-1 cities in southern India. InternationalJournal of Multidisciplinary Research. 2 (6): 168-180.

Wales, M.E. 2009. Understanding the role of convenience inconsumer food choices: A review article. Studies byUndergraduate Researchers at Guelph. 2 (2): 40-48.

Wanduragala, G. 2012. Strategies for success in India’s snackfood market. Culled from http://kanvic.com.

Warde, A. 1999. Convenience food: Space and timing. BritishFood Journal. 101 (7): 518-527.

Weaver, C.M., Dwyer, J., Fulgoni, V.L., King, J.C., Leveille,G.A., MacDonald, R.S., Ordovas, J., and Schnakenberg,D. 2014. Processed foods: Contributions to nutrition.The American Journal of Clinical Nutrition. 99 (6):1525-1542.

Winter, K. and Rodriguez, G. 1997. Consumers’ views on

Verma and Singh: Challenges and prospects of convenience food in India: An overview

214

Indian J Econ Dev 12 (2): 2016 (April-June)

nutrition and public health. Proceedings of the NutritionSociety. 56 (3): 879-888.

Wolf, A., Bray, G.A. and Popkin, B.M. 2008. A short history ofbeverages and how our body treats them. ObesityReviews. 9 (2): 151-164.

Webliographywww.makeinindia.comwww.onicra.comwww.validnutrition.org

215

Indian Journal of Economics and DevelopmentVolume 12 No.2: 216-222

April-June, 2016DOI: 10.5958/2322-0430.2016.00128.1

www.soed.in

Domestic Water Consumption Pattern and its Linkage withSocio-economic Variables: A Case Study of Ludhiana City

Jasdeep Kaur1*, A.S. Bhullar2, and R.S. Ghuman3

1Kamla Lohtia Sanatan Dharam College, Daresi, Ludhiana- 1410082Economics Program, University of Northern British Columbia, BC, Canada3Nehru SAIL Chair Professor, CRRID, Chandigarh-160019

*Corresponding author’s email: [email protected]

Received: January 07, 2016 Accepted: May 08, 2016

ABSTRACTThe consumption of water depends on the life style of the population, work and working conditions, climate, culture andfood habits etc. The per household and per capita water consumption in the selected households of the Ludhiana cityshowed that high income groups consume more water than the low income and slum households. The relationshipbetween demographic and socio-economic variables like education, occupation and household income and waterconsumption was positive. The paper reviews the domestic water consumption pattern and its linkage with socio-economicvariables in Ludhiana city.

KeywordsDeficiency, education, income, , occupation, water consumption

JEL CodesI25, P46, Q25, R21

INTRODUCTIONWater, the basic need of life, is likely to surpass the

scarcity of many other commodities during the twenty-first century. It will be a great challenge to meet increaseddemand for water due to increasing population, economicgrowth and technological changes. The opportunities toenhance the supply of potable water are becomingincreasingly limited (Marothia, 2003). The supply isshrinking year by year due to over exploitation, pollutionand inefficient water use methods and policies. This ismore so in the developing countries due to uncheckedpopulation growth, interest groups competition andconflict (Ballabh, 2003), expansion of economic activities(Biswas, 1993 and Narayanamoorthy, 2003) along withlack of institutional framework and policies for watermanagement. It is certain that coming generations haveto confront, among other things, demographic transitionof population, geographical shift of population,technological advancement, growing globalization,degradation of the environment and the emergence ofwater scarcity.

The quantity of water consumed in most of the

Indian cities is not determined by the demand but thesupply. People attempt to adjust to the quantity as well asquality of water supplied. A majority of households inmajor cities in India depend on the municipal water supplyfor their daily needs (Anonymous, 2010).

There are lots of asymmetries in the household waterconsumption. The water consumption varies acrosslocalities, household sizes, income and occupationalcategories, demographic profiles etc. These variations inthe water consumption, by and large, are the sum totalof activity-wise water use differentials.

This paper endeavors to examine the domestic waterconsumption pattern in Ludhiana city of Punjab. Thepaper has been divided into five sections. Section I dealswith the database and methodology of the study. The perday water consumption norms suggested in various plandocuments and by other organizations have been enlistedin the Section II. In Section III, an effort has been madeto examine the locality-wise, activity-wise and season-wise per household and per capita water consumption.Section IV deals with the relationship between the socio-economic and demographic variables. The summary and

216

Indian J Econ Dev 12 (2): 2016 (April-June)

conclusions have been presented in the last section.DATABASEAND METHODOLOGY

This paper is mainly based on primary data collectedthrough a survey of the households by personal interviewmethod. To examine the pattern of water consumption,cross sectional data from 360 households was collectedthrough a questionnaire. The data pertains to the year2009-10. The different localities of Ludhiana city werecategorized into six income clusters1 as following:1. Very High Income Group (VHIG) areas with well-

planned localities and buildings and the plot size morethan 400 square yards.

2. High Income Group (HIG) areas with well-plannedlocalities and buildings and the plot size varyingbetween 250 to 400 square yards.

3. Middle Income Group (MIG) areas with well-plannedlocalities and buildings and the plot size varyingbetween 125 to 250 square yards.

4. Low Income Group (LIG) areas with well-plannedlocalities and buildings and the plot size less than 125square yards.

5. Mixed areas2

6. Slum areasIn this way, a number of clusters falling under each

income group were identified. Four localities from eachincome cluster were selected and from each locality 15respondents were interviewed. Thus the total number ofhouseholds surveyed from each cluster was 60. In thisway, the total sample included 360 households from 6income clusters. From the selected households the dataregarding plot size, household income, occupationstructure, and education level of the head of the householdwere collected and analyzed so as to examine therelationship of these variables with water consumption.

The data were collected through a structured scheduleby recall method and the target respondents werehousewives. The volume of vessels in which householdsstore water was assessed and the number of vessels ofwater used in different activities like bathing, clotheswashing, utensil cleaning, house cleaning, watering thelawn and pots etc. were estimated. The quantity of watercontained in the vessels was assessed by physicallymeasuring the quantity of water contained in a vessel. Apilot survey of ten houses using different kind of vessels

was conducted for this purpose. In this way, the averagesize of the vessel was assessed and this average wasused to work out the quantity of water used for differentactivities. The average size of the vessel was 9.73 liters.

Where running tap or piped water was used in someactivities, the duration for which the tap was used wasestimated and the quantity of water delivered per minutefrom the tap was measured. The quantity of water usedin flushing toilet was measured by volume of bucket usedand flush tank capacity.RESULTSAND DISCUSSIONWater Requirement Norms and Standards

A number of factors like climate, culture, food habits,work, and working conditions, level and type ofdevelopment and physiology determine the requirementof water. The World Health Organization (WHO, 2003)classifies the supply and access to water in four servicecategories. These categories are:i. No Access (Water available below 5 lpcd)ii. Basic Access (Avg. app. 20 lpcd)iii. Intermediate Access (Avg. app. 50 lpcd)iv. Optimal Access (Avg. app. 100-200 lpcd)

The National Commission on Urbanization (1988)recommended that a per capita water supply of 90-100liters per day is needed to lead a hygienic existence andemphasized that this level of water supply must be ensuredto all citizens.

As per the Bureau of Indian Standards, IS: 1172-1993 a minimum water supply of 200 liters per capitaper day (lpcd) should be provided for domesticconsumption in cities with full flushing systems. IS: 1172-1993 also mentions that the amount of water supplymay be reduced to 135 lpcd for the LIG and theeconomically weaker sections of the society and in smalltowns.

The Ninth Plan (1997-2002) had advocated therequirement of water in urban areas as 125 lpcd in citieswith planned sewerage systems; 70 lpcd in cities withoutplanned sewerage systems; 40 lpcd for those collectingwater from public stand posts.

However, in the tenth plan (2002-2007), the citieswith planned sewerage systems were classified into twogroups based on population that is, metropolitan or megacities and non-metropolitan cities. In the former, therecommended water supply level was 150 lpcd, and inthe latter it was 135 lpcd (Anonymous, 1997-2002).

Twelfth Plan (2012-17) has set the objective toprovide 40 lpcd piped drinking water supply to 50 percentof rural population and 50 percent Gram Panchayats willachieve Nirmal Gram Status by the end of the TwelfthFive Year Plan.

Notwithstanding the IS: 1172-1993 and the five yearplan recommendations, almost every municipal

1 In a similar study Shaban and Sharma (2007) has classifiedthe households on the basis of type of houses i.e. HIG, LIG,MIG, Mixed and others etc. Broadly, the classification ofShaban and Sharma has been adopted in the study butlittle changes have been made according to the localsituation of the study area.2 Mixed areas represent where unplanned localities andbuildings within MC limits and the plot sizes varied.

217

Kaur et al.: Domestic water consumption pattern and its linkage with socio-economic variables

corporation/ municipality has defined the requirement ofwater in its own way. One agrees that industrial andcommercial development of towns and cities may differhence the amount of water required will also vary, butthe requirement for domestic use seems unlikely to varyso much. The Municipal Corporation of Greater Mumbaiadvocates 135 lpcd as the domestic requirement of water,Delhi Development Authority considers 225 lpcd as thewater required for domestic use and MunicipalCorporation Ludhiana advocates 220 lpcd for variousdomestic water related activities. This wide variation inrecommendations/ prescriptions for domestic use ofwater seems inexplicable, particularly when these megacities have well- developed sewerage/flushing systems.Domestic Consumption of Water

The main sources of water supply are MC/IT,supplemented with submersible pumps and hand pumps.Water requirements of 82.67 percent of the VHIGhouseholds was made up by Municipal Corporation (MC)and Improvement Trust (IT) while the other 17.33 percentrespondents of VHIG also having personal submersiblepumps while 13.33 percent of HIG and only 4 percent ofmixed areas use submersible pump as the other sourceof water (Table 1). Only 10 and 6 percent respondentsrespectively from LIG and mixed class use hand pumpsto supplement their water requirement. None of thehouseholds except above income class use hand pumpsfor their water requirement. So, therefore, MC/IT emergedas the major source of water supply to the residents ofurban Ludhiana.

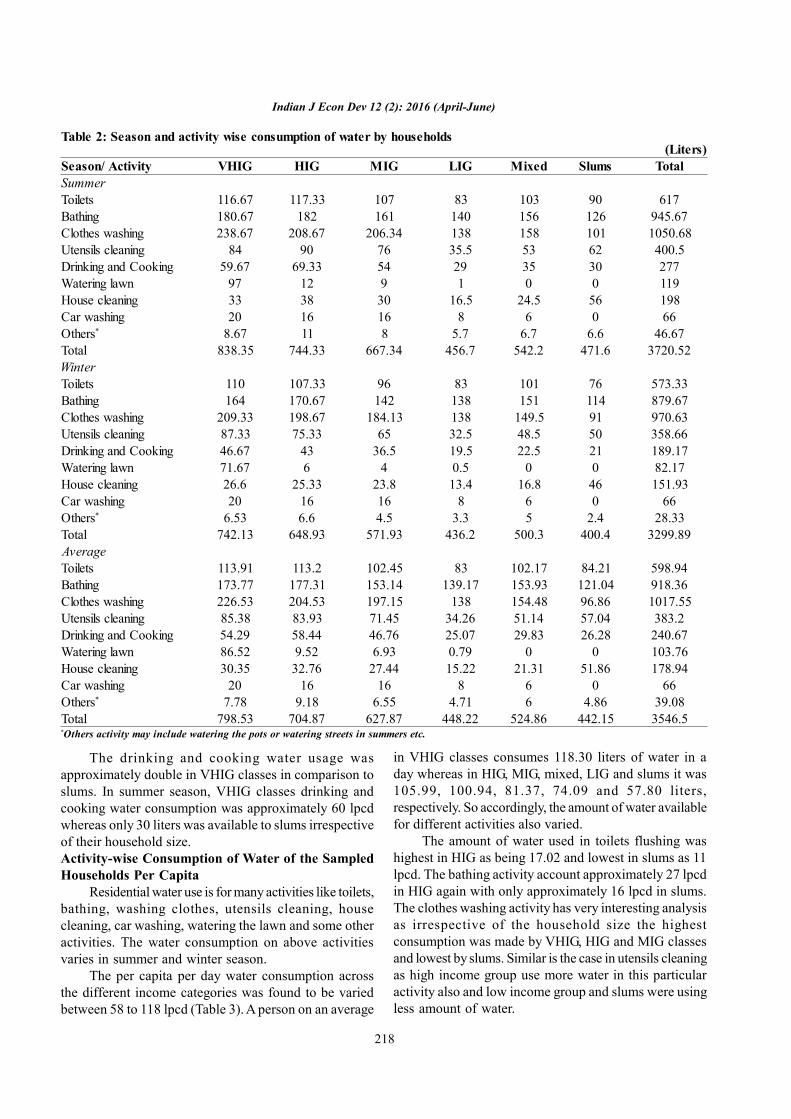

cleaning, drinking and cooking, watering the garden,washing car and house cleaning are dependent on wateravailability. Residential water use is influenced by severalfactors, including climate, household income, price,fashion and conservation awareness programmes(Kennedy, 1984).

Since the consumption of water varies acrossseasons, so the seasonal fluctuations of household wateruse were recorded in the survey. Summer (April toOctober) and winter (November to March) seasons wereused in the study to know the water consumption patternsof the households in Ludhiana city. In India, mainlysummer and winter are prevalent in most of the states.Punjab also has two seasons (summer and winter). Thewater use is higher during summers than winters. Waterconsumption also varies by the type of dwelling unit.

At household level, average daily water consumptionduring the year for VHIG, HIG, MIG, LIG, mixed andslums was 798.55, 704.87, 627.87, 448.22, 524.86, and442.15 liters respectively (Table 2). Thus, average dailywater consumption shows that if we move from higherincome classes to lower income classes and then to slumsthe consumption goes on decreasing. The highestconsumption was on clothes washing followed by bathing,toilets and utensils cleaning. The car washing and wateringthe lawn by various household categories was very lessas compared to other activities. Some categories likemixed and slums do not have cars and area under lawnso the consumption was at zero level in these categories.

There were considerable differences in the waterusage in summer and winter months. The totalconsumption of water in various activities in summerswas 838.35 liters in VHIG, 744.33 liters in HIG, 667.34liters in MIG, 456.70 in LIG, 542.20 liters in mixed and471.60 liters in slum houses. Water consumption in winterwas 742.13, 648.93, 571.93, 436.20, 500.30, and 400.40liters in VHIG, HIG, MIG, LIG, mixed and slums,respectively (Table 2).