report to the east williston school district board of

TRANSCRIPT

Report to the East Williston School District Board of Trustees and Administration from The East Williston Financial Advisory Committee

Delivered to the East Williston School District Board of Trustees

Dated April 11, 2018

Introduction

2

Introduce the Financial Advisory Committee

Discuss the the Tax Cap, Tax Levy and property taxes

Provide background context of the budget cost drivers

Assess the current environment for schools

Review growth trends & benchmarking

Review Student data

Discuss Capital needs & funding

Review a forecast & implications for long-term planning

Provide recommendations to the Board

3

Presentation Agenda

Advise the Board on strategies for delivering a high quality

education to students in a fiscally responsible manner

Maintain professional and absolute objectivity

Provide feedback, insight and analysis

Increase and facilitate transparency

Foster open lines of communication

4

Financial Advisory Committee

Role of the FAC

Ashish Chabria 20+ years banking, finance, accounting and strategy

Gaddy Cohen 20+ years accounting & finance, MBA/CPA

Alan Goldstein 30+ years finance & operations management, CPA

Larry Posner 25+ years financial & mgmt experience, MBA/CPA

Alvin Sarabanchong 20+ years finance, trading & operations management

5

FAC Committee Members

Comprised of volunteers with financial backgrounds

Recommended 2018-19 budget

Budget cost drivers and recent trends

Tax Cap and implications for future funding

Funding mechanisms for capital projects

Budget forecast

6

Focus of the FAC

Our current review focused on:

Background & Tax Cap

7

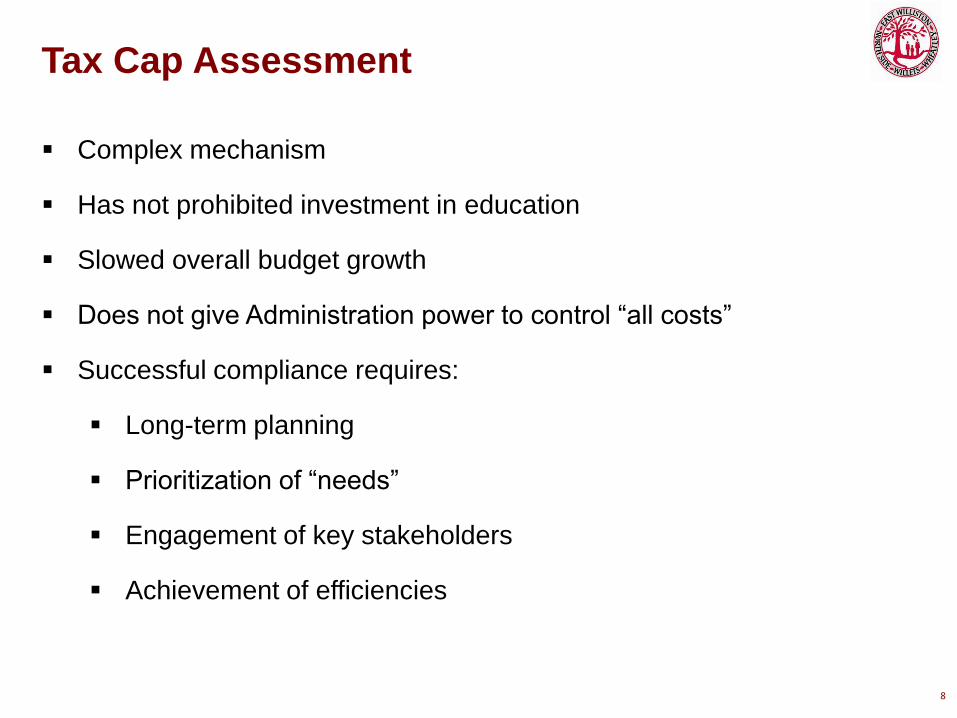

Complex mechanism

Has not prohibited investment in education

Slowed overall budget growth

Does not give Administration power to control “all costs”

Successful compliance requires:

Long-term planning

Prioritization of “needs”

Engagement of key stakeholders

Achievement of efficiencies

8

Tax Cap Assessment

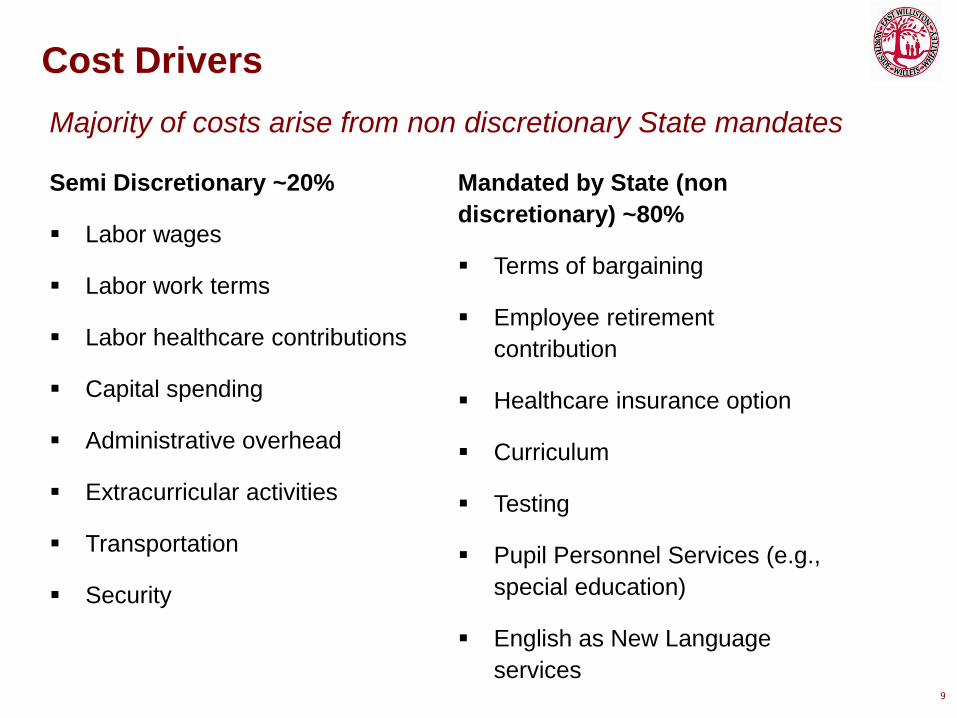

Semi Discretionary ~20%

Labor wages

Labor work terms

Labor healthcare contributions

Capital spending

Administrative overhead

Extracurricular activities

Transportation

Security

9

Cost Drivers

Mandated by State (non

discretionary) ~80%

Terms of bargaining

Employee retirement

contribution

Healthcare insurance option

Curriculum

Testing

Pupil Personnel Services (e.g.,

special education)

English as New Language

services

Majority of costs arise from non discretionary State mandates

School Environment

10

Higher state aid has helped levies stay low

LI public school districts ~2.6% increase 2018-19 year

Most Tax levies across Long Island are projected to rise 2-3%

All district’s proposed budgets are compliant with the Tax Cap

Disclosure on school budgets vary across district

Prioritization of resources / long-term planning

Student needs / achievement driving decisions

Tax cap compliance continues to require attention

Use of capital reserve funds becoming more prevalent

11

Current Environment for Schools

Budget developed to support priorities of the district

Continued implementation of the Strategic Priorities

Balance of:

Tax cap compliance

Investment to further student needs & achievement

Hedging for uncertainties in funding, compliance etc.

7th Year of successful Tax Cap compliance

Tax payers will continue to receive state tax rebates

12

Current Environment for EWSD

Tax Levy

13

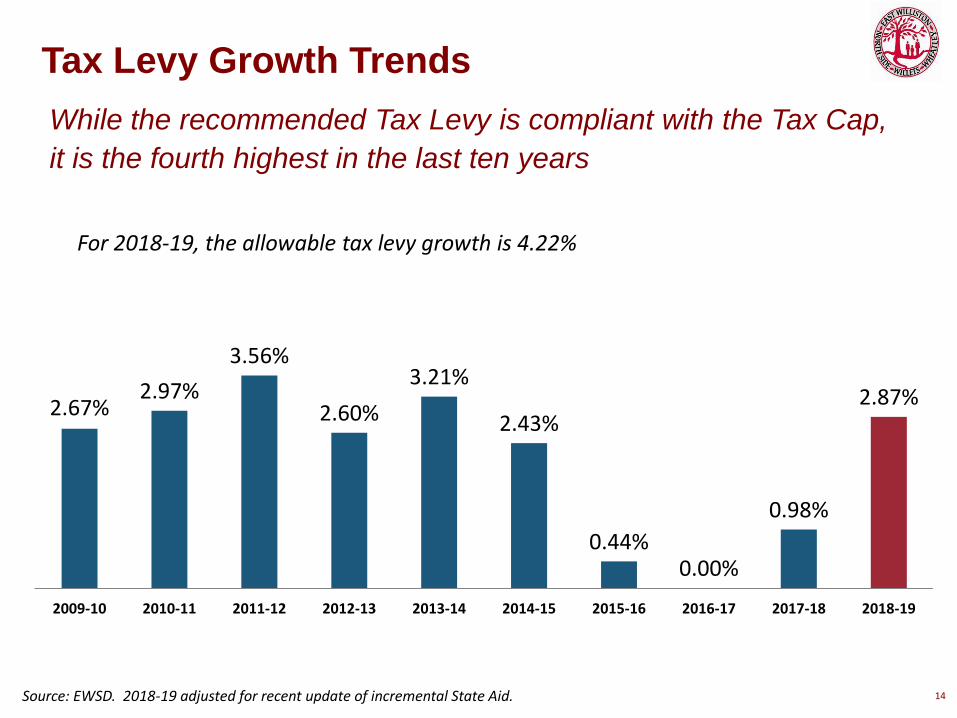

2.67% 2.97%

3.56%

2.60%

3.21%

2.43%

0.44% 0.00%

0.98%

2.87%

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

14

Tax Levy Growth Trends

While the recommended Tax Levy is compliant with the Tax Cap,

it is the fourth highest in the last ten years

Source: EWSD. 2018-19 adjusted for recent update of incremental State Aid.

For 2018-19, the allowable tax levy growth is 4.22%

15

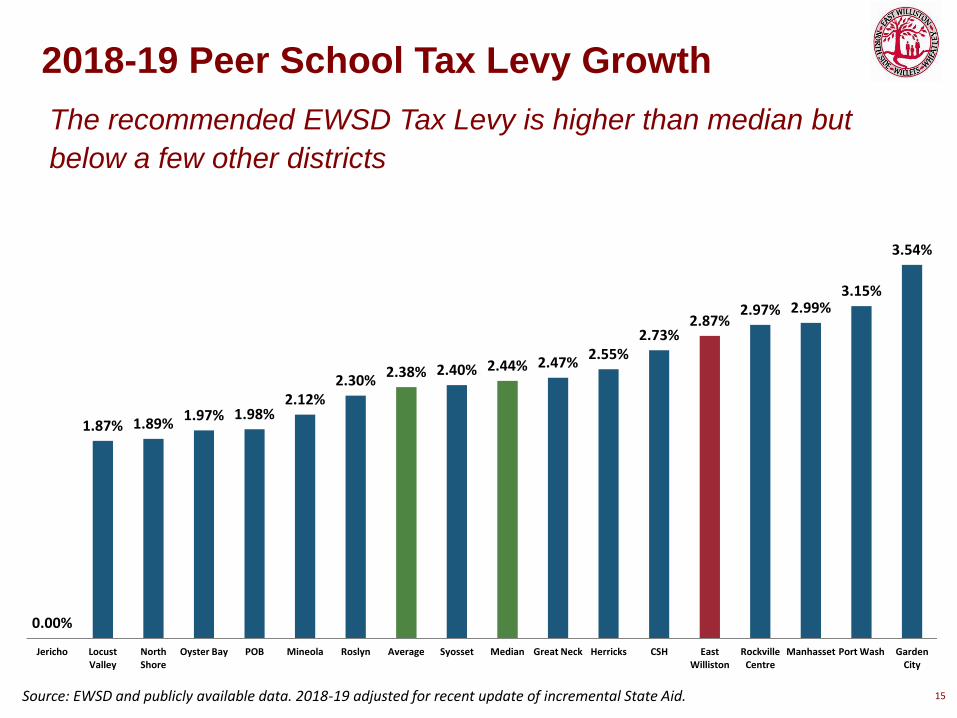

2018-19 Peer School Tax Levy Growth

The recommended EWSD Tax Levy is higher than median but

below a few other districts

0.00%

1.87% 1.89% 1.97% 1.98%

2.12% 2.30%

2.38% 2.40% 2.44% 2.47% 2.55%

2.73% 2.87%

2.97% 2.99% 3.15%

3.54%

Jericho Locust Valley

North Shore

Oyster Bay POB Mineola Roslyn Average Syosset Median Great Neck Herricks CSH East Williston

Rockville Centre

Manhasset Port Wash Garden City

Source: EWSD and publicly available data. 2018-19 adjusted for recent update of incremental State Aid.

16

Source of Funds for School Budget

Source: EWSD. $ in thousands. 2018-19 adjusted for recent update of incremental State Aid.

Tax Levy accounts for substantial majority of funds for budget

Growth Rate

2017-18 2018-19 5-Year 1-Year

Property Tax Levy 52,956 54,473 1.3% 2.9%

Non-tax Revenue 4,791 4,816 10.9% 0.5%

Appropriated Fund Balance 544 544 0.0% 0.0%

Total Funds Avail for Budget 58,290 59,833 1.9% 2.6%

% of Total Budget

Property Tax Levy 90.8% 91.0%

Non-tax Revenue 8.2% 8.0%

Appropriated Fund Balance 0.9% 0.9%

17

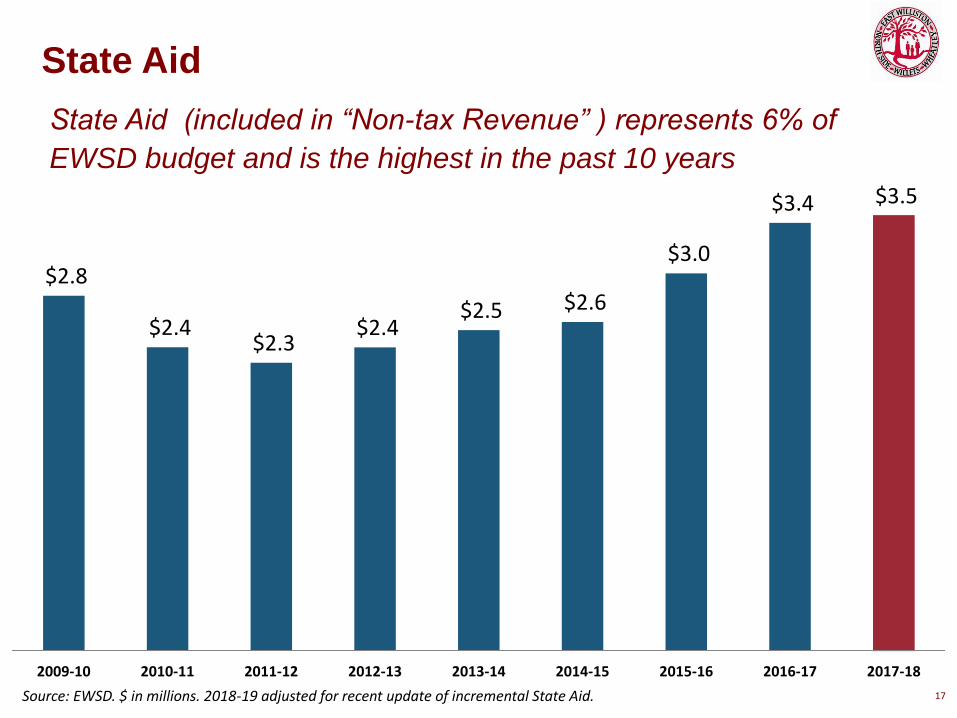

State Aid

State Aid (included in “Non-tax Revenue” ) represents 6% of

EWSD budget and is the highest in the past 10 years

$2.8

$2.4 $2.3

$2.4 $2.5 $2.6

$3.0

$3.4 $3.5

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

Source: EWSD. $ in millions. 2018-19 adjusted for recent update of incremental State Aid.

18

Tax Levy Growth & Your Taxes

EWSD sets tax levy, Nassau County determines how to get it

Source: Per Nassau County tax assessment bills. Assessed value is a number correlated to the property values in EWSD; it is not the FMV of properties.

Last year, 0.98% EWSD tax levy increase and assessed value

decrease resulted in 2.36% actual tax rate increase

Tax Year

Nassau

County

Assessed

Value

Nassau

County Tax

Rate/$100

YoY Nassu

County Tax

Rate

Change

EWSD Levy

Change

2011/2012 8,033,194 661.636

2012/2013 7,156,120 769.984 16.38% 2.60%

2013/2014 6,934,485 822.905 6.87% 3.21%

2014/2015 6,793,492 863.471 4.93% 2.43%

2015/2016 6,552,808 897.035 3.89% 1.85%

2016/2017 6,240,460 930.999 3.79% 0.00%

2017/2018 6,138,412 952.962 2.36% 0.98%

Change 2017-18/2011-12 -23.6% 44.0%

Budget

19

20

Budget Growth

The recommended budget will increase 2.65% to $59.8

$49.3 $50.5 $51.4 $52.7 $54.4 $55.7 $56.7 $57.5 $58.3 $59.8

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Source: EWSD. $ in millions. 2018-19 excludes potential one-time spending for additional security measures.

21

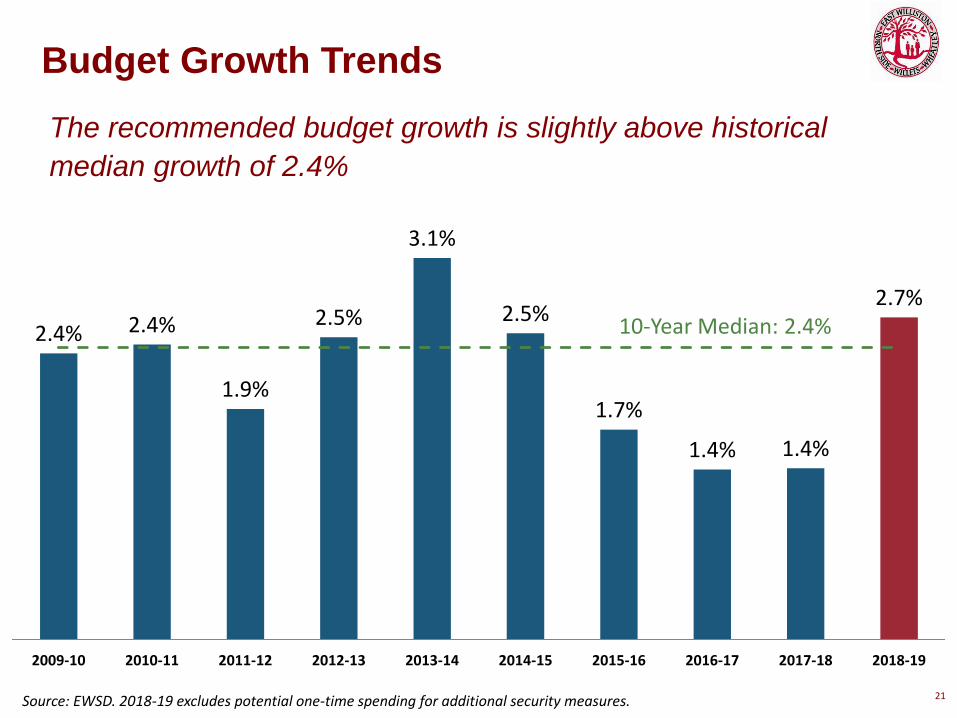

Budget Growth Trends

The recommended budget growth is slightly above historical

median growth of 2.4%

2.4% 2.4%

1.9%

2.5%

3.1%

2.5%

1.7%

1.4% 1.4%

2.7%

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Source: EWSD. 2018-19 excludes potential one-time spending for additional security measures.

10-Year Median: 2.4%

22

Proposed 2018-19 Peer Group Budget

The recommended EWSD budget increase is in line with peers,

and only slightly above Median

0.00%

1.70% 1.82%

2.00% 2.01%

2.33% 2.35%

2.59% 2.59% 2.65% 2.65% 2.80% 2.85% 2.90%

3.95%

Jericho Garden City Locust Valley North Shore Great Neck Average Oyster Bay Median Manhasset Herricks East Williston Roslyn Port Wash Syosset Rockville Centre

Source: EWSD and publicly available data. No data available yet for CSH, Mineola and POB school districts. East Williston excludes potential one-time spending for additional security measures.

23

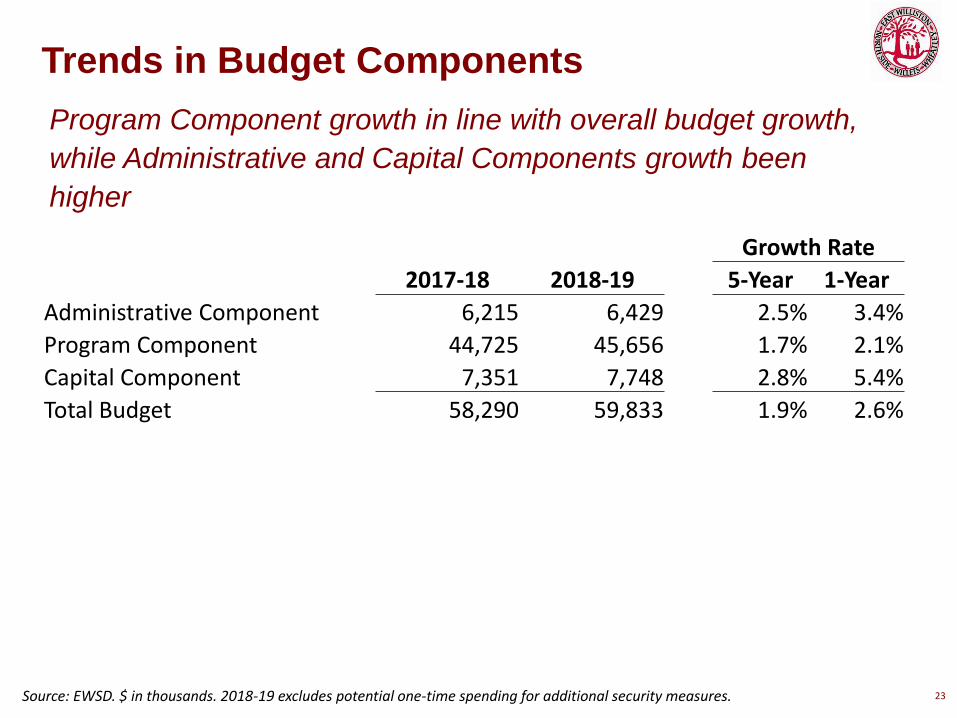

Trends in Budget Components

Source: EWSD. $ in thousands. 2018-19 excludes potential one-time spending for additional security measures.

Program Component growth in line with overall budget growth,

while Administrative and Capital Components growth been

higher

Growth Rate

2017-18 2018-19 5-Year 1-Year

Administrative Component 6,215 6,429 2.5% 3.4%

Program Component 44,725 45,656 1.7% 2.1%

Capital Component 7,351 7,748 2.8% 5.4%

Total Budget 58,290 59,833 1.9% 2.6%

24

Budget vs Actual Spending

Current year Budget vs Actual (expensed and encumbered)

spending is relatively tight with only $1,170 difference (or 98% of

budget)

Source: EWSD. $ in thousands. 2018-19 excludes potential one-time spending for additional security measures..

Expensed & Growth Rate

Budget Encumbered Budget Budget to Budget to

2017-18 2017-18 Difference 2018-19 Budget Exp. & Enc.

58,290 57,120 1,170 59,833 2.65% 4.75%

25

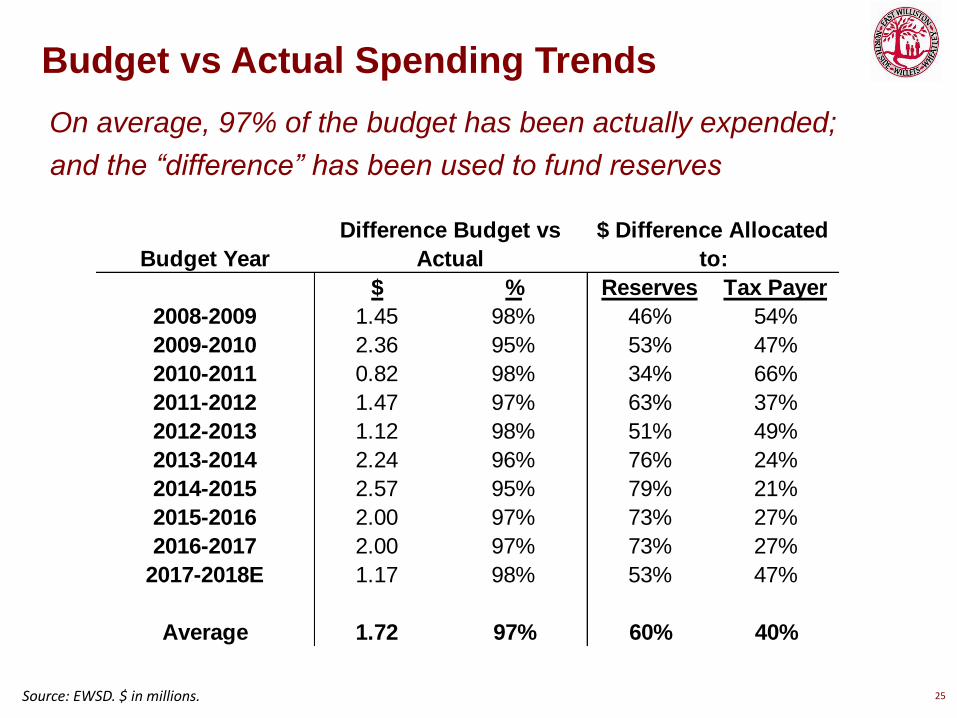

Budget vs Actual Spending Trends

On average, 97% of the budget has been actually expended;

and the “difference” has been used to fund reserves

Source: EWSD. $ in millions.

Budget Year

$ % Reserves Tax Payer

2008-2009 1.45 98% 46% 54%

2009-2010 2.36 95% 53% 47%

2010-2011 0.82 98% 34% 66%

2011-2012 1.47 97% 63% 37%

2012-2013 1.12 98% 51% 49%

2013-2014 2.24 96% 76% 24%

2014-2015 2.57 95% 79% 21%

2015-2016 2.00 97% 73% 27%

2016-2017 2.00 97% 73% 27%

2017-2018E 1.17 98% 53% 47%

Average 1.72 97% 60% 40%

Difference Budget vs

Actual

$ Difference Allocated

to:

Budget Cost Drivers

26

27

Budget Growth Drivers

Employee Benefits and Transportation have increased

substantially

Source: EWSD. $ in thousands. 2018-19 excludes potential one-time spending for additional security measures.

Growth Rate

2017-18 2018-19 5-Year 1-Year

Salaries & Salary Related Taxes 34,452 35,352 2.5% 2.6%

All Employee Benefits 10,724 11,309 0.9% 5.5%

Contract Transportation (incl. BOCES) 1,756 1,986 1.9% 13.1%

Special Education (non salary) 2,649 2,396 -0.7% -9.6%

Debt Service (Bonds, TANs, EPC) 1,859 1,868 -4.0% 0.5%

Technology Equipment & Support 1,116 1,076 5.2% -3.6%

All Other 5,734 5,848 3.3% 2.0%

Total Budget 58,290 59,833 1.9% 2.6%

28

Budget Growth, Total Salaries Growth and

Contract Wage Growth

While Contract Wage Growth has hovered around 1%, Budget

Growth and Total Salaries Growth have been higher

2.5%

3.1%

2.5%

1.7% 1.4% 1.4%

2.6%

2.2%

-1.2%

0.6%

2.9%

4.0%

2.7%

2.1%

1.3% 1.6% 1.7%

1.0% 0.6% 0.7%

2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Budget Total Salaries Contract Wage

Source: EWSD.

No contract yet for 2018-19 period

29

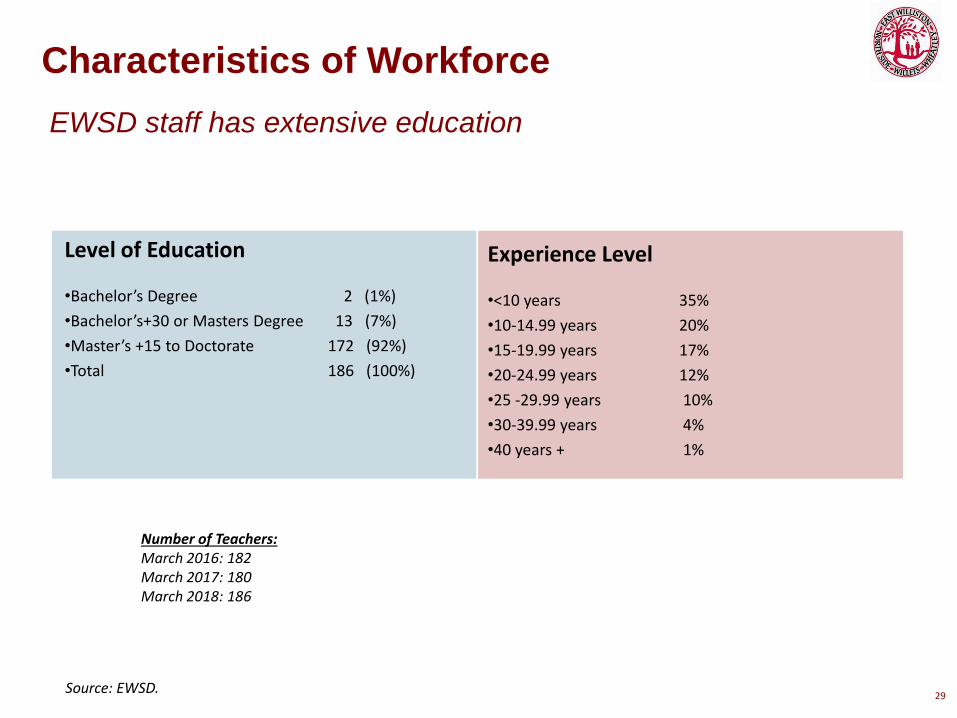

Characteristics of Workforce

EWSD staff has extensive education

Source: EWSD.

Level of Education

•Bachelor’s Degree 2 (1%)

•Bachelor’s+30 or Masters Degree 13 (7%)

•Master’s +15 to Doctorate 172 (92%)

•Total 186 (100%)

Experience Level

•<10 years 35%

•10-14.99 years 20%

•15-19.99 years 17%

•20-24.99 years 12%

•25 -29.99 years 10%

•30-39.99 years 4%

•40 years + 1%

Number of Teachers: March 2016: 182 March 2017: 180 March 2018: 186

30

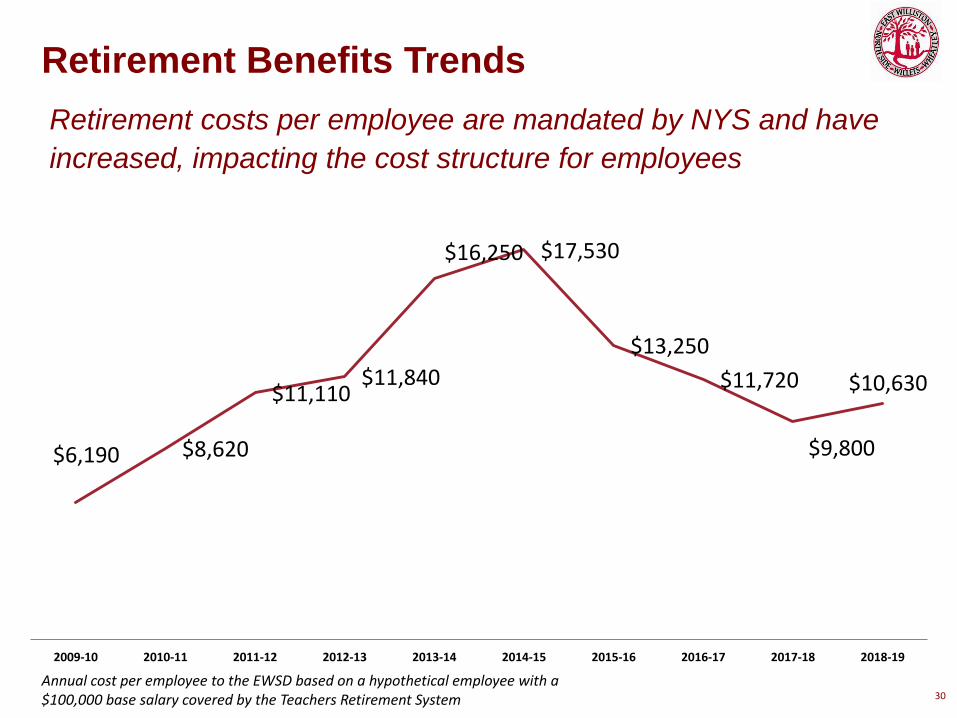

Retirement Benefits Trends

Retirement costs per employee are mandated by NYS and have

increased, impacting the cost structure for employees

Annual cost per employee to the EWSD based on a hypothetical employee with a $100,000 base salary covered by the Teachers Retirement System

$6,190 $8,620

$11,110 $11,840

$16,250 $17,530

$13,250

$11,720

$9,800

$10,630

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

31

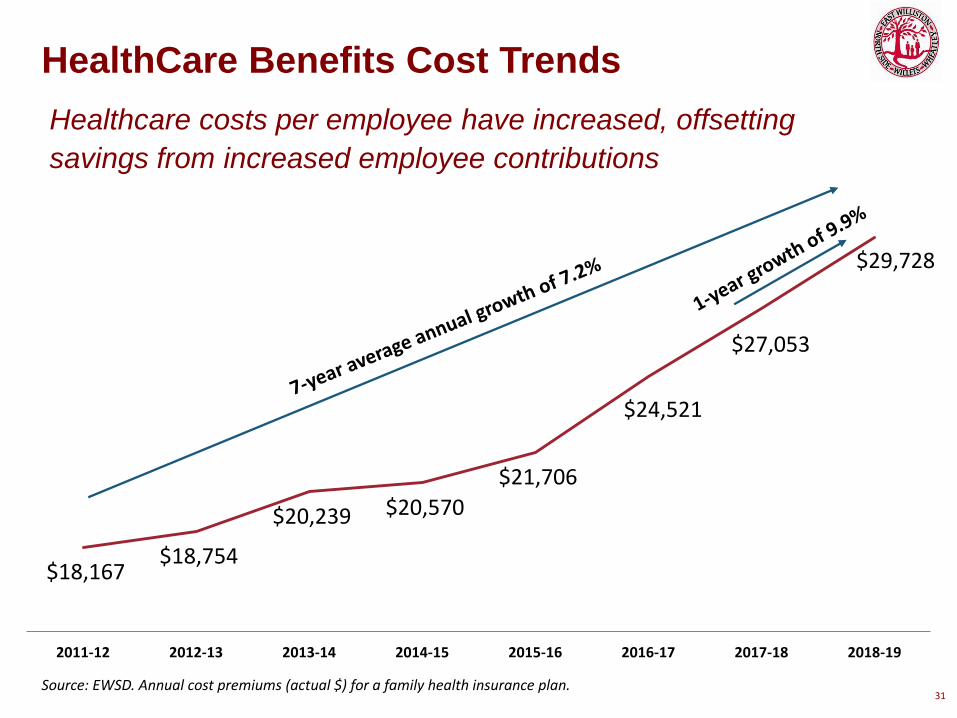

HealthCare Benefits Cost Trends

Healthcare costs per employee have increased, offsetting

savings from increased employee contributions

Source: EWSD. Annual cost premiums (actual $) for a family health insurance plan.

$18,167 $18,754

$20,239 $20,570

$21,706

$24,521

$27,053

$29,728

2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

32

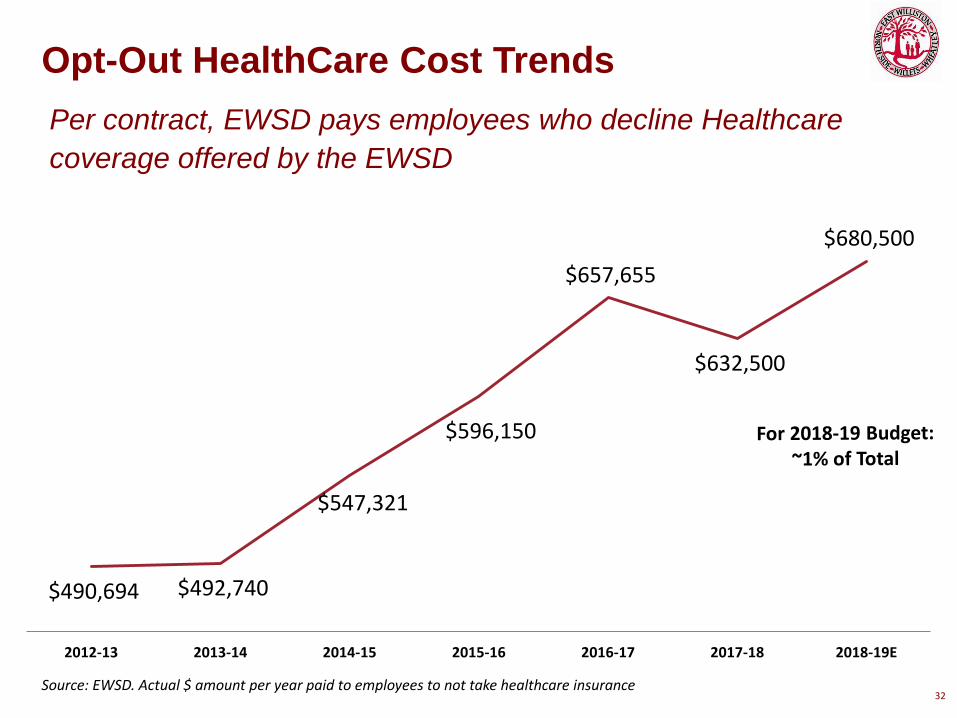

Opt-Out HealthCare Cost Trends

Per contract, EWSD pays employees who decline Healthcare

coverage offered by the EWSD

Source: EWSD. Actual $ amount per year paid to employees to not take healthcare insurance

$490,694 $492,740

$547,321

$596,150

$657,655

$632,500

$680,500

2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19E

33

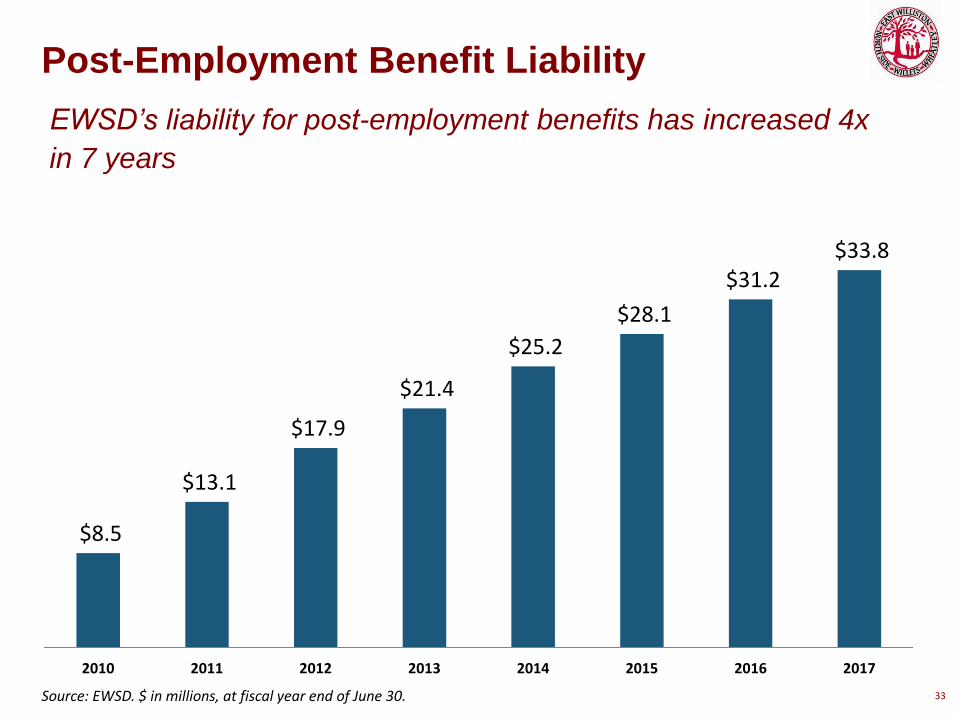

Post-Employment Benefit Liability

EWSD’s liability for post-employment benefits has increased 4x

in 7 years

Source: EWSD. $ in millions, at fiscal year end of June 30.

$8.5

$13.1

$17.9

$21.4

$25.2

$28.1

$31.2 $33.8

2010 2011 2012 2013 2014 2015 2016 2017

34

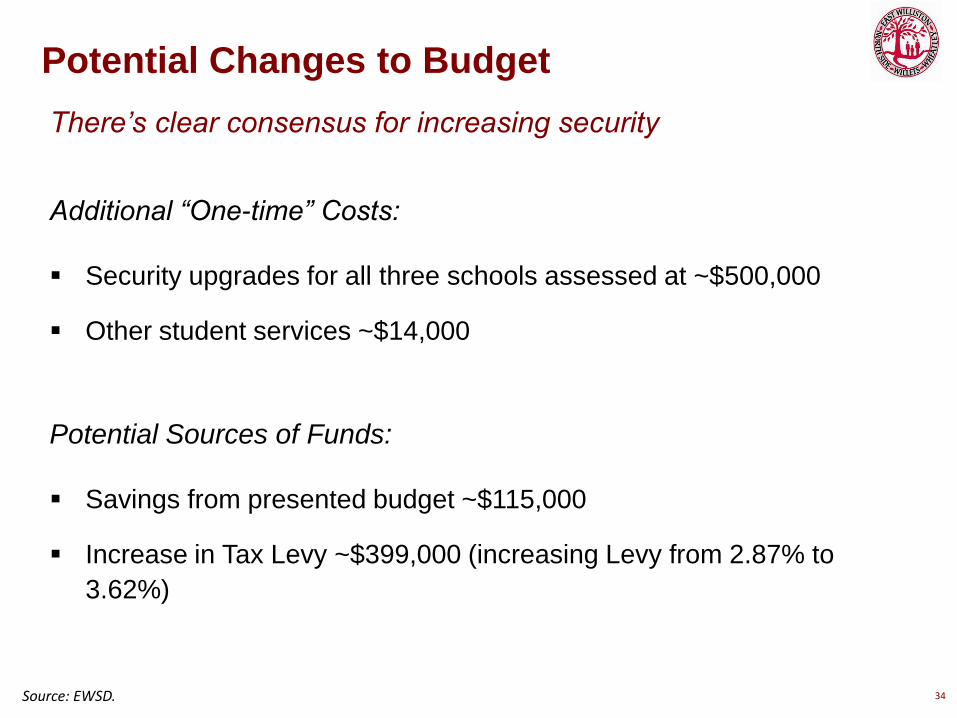

Potential Changes to Budget

There’s clear consensus for increasing security

Source: EWSD.

Additional “One-time” Costs:

Security upgrades for all three schools assessed at ~$500,000

Other student services ~$14,000

Potential Sources of Funds:

Savings from presented budget ~$115,000

Increase in Tax Levy ~$399,000 (increasing Levy from 2.87% to

3.62%)

Student Data

35

36

Student Enrollment

After multiple years of decline, enrollment has been growing

1,810

1,807

1,767

1,736 1,753 1,731

1,716 1,683

1,734

1,722

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

2017-18 and Prior Periods is Actual # 2018-19 is Projected #

Source: EWSD.

37

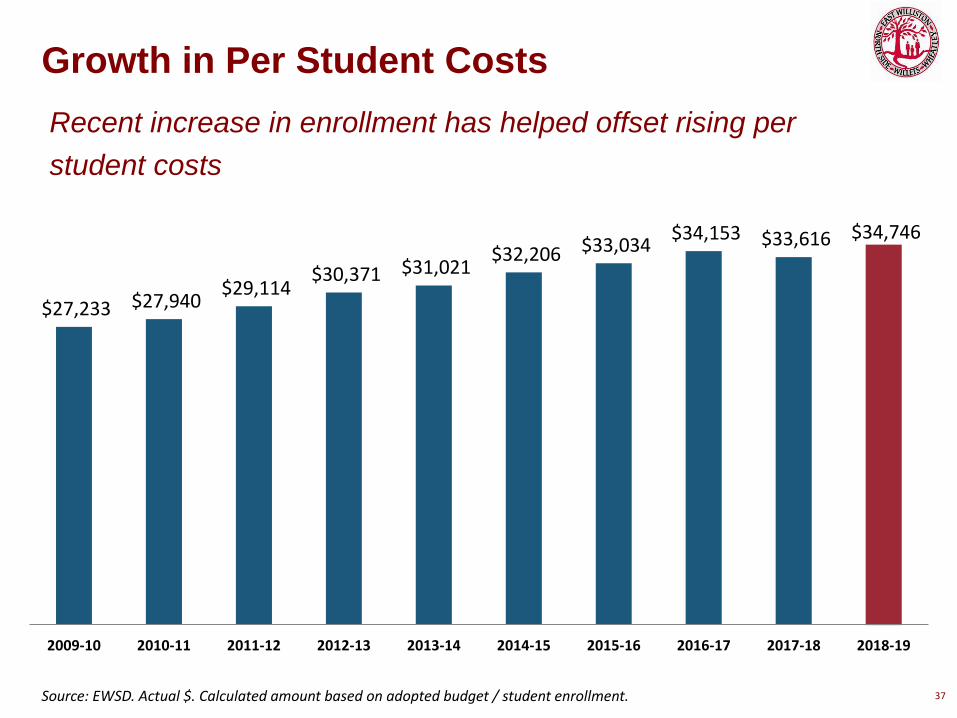

Growth in Per Student Costs

Recent increase in enrollment has helped offset rising per

student costs

$27,233 $27,940 $29,114

$30,371 $31,021 $32,206 $33,034

$34,153 $33,616 $34,746

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19

Source: EWSD. Actual $. Calculated amount based on adopted budget / student enrollment.

Capital

38

Budget

Capital Reserve Fund

Bonds/Debt

39

Capital Projects

EWSD has funded capital projects in the following three ways:

40

Budgeted Capital Projects

EWSD has continued to increase funding for capital projects in

the budget

$170,000 $150,000 $150,000

$225,510

$525,510 $525,510 $573,550

$626,000

$800,040 $800,040

2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 2018-19 Source: EWSD.

Key Benefits

Avoids interest and other costs typically associated with issuing bonds

Overall lowers the cost of the capital projects (timing + costs)

Shortens the time to deploy capital, improving efficiency

Should alleviate the need to issue debt again

41

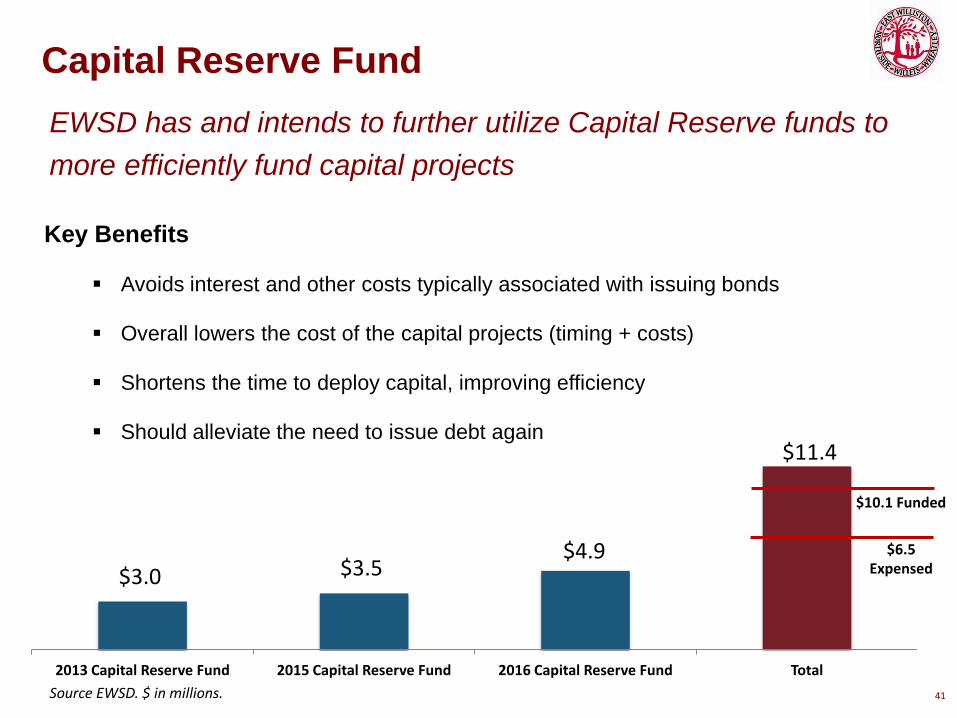

Capital Reserve Fund

EWSD has and intends to further utilize Capital Reserve funds to

more efficiently fund capital projects

$3.0 $3.5 $4.9

$11.4

2013 Capital Reserve Fund 2015 Capital Reserve Fund 2016 Capital Reserve Fund Total

Source EWSD. $ in millions.

$10.1 Funded

$6.5 Expensed

42

Trend in Debt

EWSD’s debt burden has decreased

$13.8 $14.4 $15.5

$17.9

$16.4

$14.7

$13.0

$11.3

$9.4 $8.9

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018E

Source EWSD. $ in millions, at fiscal year end of June 30. Includes bonds payable plus energy performance contract payable.

FAC Recommendations

43

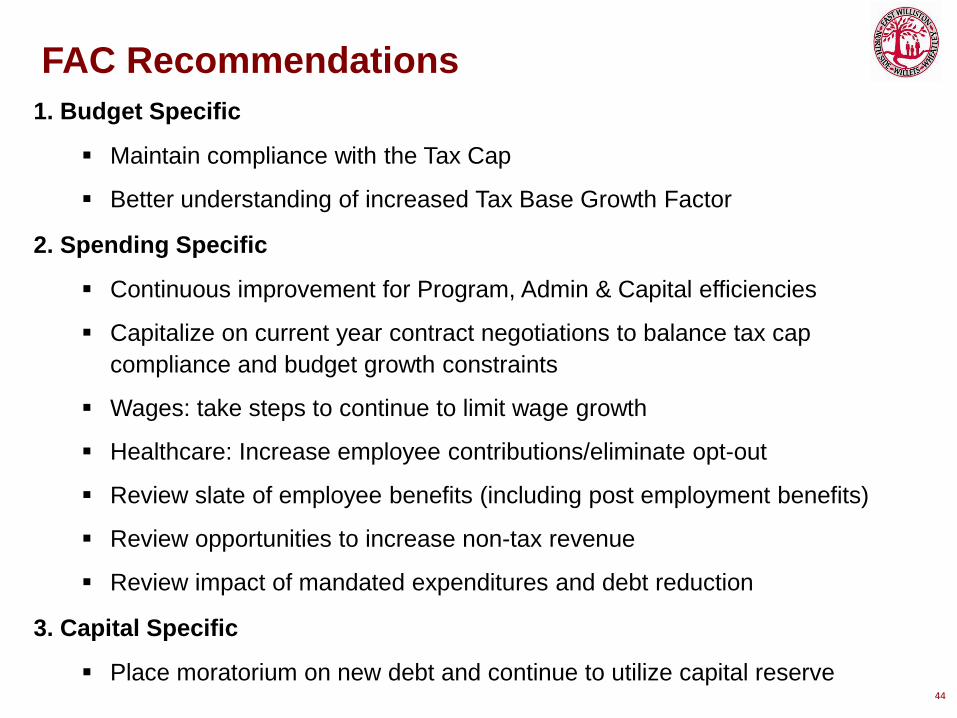

1. Budget Specific

Maintain compliance with the Tax Cap

Better understanding of increased Tax Base Growth Factor

2. Spending Specific

Continuous improvement for Program, Admin & Capital efficiencies

Capitalize on current year contract negotiations to balance tax cap

compliance and budget growth constraints

Wages: take steps to continue to limit wage growth

Healthcare: Increase employee contributions/eliminate opt-out

Review slate of employee benefits (including post employment benefits)

Review opportunities to increase non-tax revenue

Review impact of mandated expenditures and debt reduction

3. Capital Specific

Place moratorium on new debt and continue to utilize capital reserve 44

FAC Recommendations

45

Thank You

The FAC wishes to thank the Administration, members of the

Board, interested parties and members of the community for

their input and efforts.