report on sugar

TRANSCRIPT

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 1/16

Report onS urging sugar price in Pakistan

Presented To:

Prof. Kanwal Zahra

Group Members:

L1f09mbam2083

Due Date:

November29, 2010

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 2/16

Introduction:

Pakistan is the 5th largest country in the world in terms of area undersugar cane cultivation, 11th by production and 60th in; yield. Sugarcaneis the primary raw material for the production of sugar. Sinceindependence, the area under cultivation has increased more rapidly thanany other major crop. It is one of the major cash crops in Pakistancultivated over an area of around one million hectares.

The sugar industry in Pakistan is the 2nd largest agro based industrycomprising 81 sugar mills with annual crushing capacity of over 6.1million tones. Sugarcane farming and sugar manufacturing contributesignificantly to the national exchequer in the form of various taxes andlevies. Sugar manufacturing and its by-products have contributedsignificantly towards the foreign exchange resources through importsubstitution.

The sugar industry in Pakistan continued to deal with uncertainty in CY2009 due to decreasing sugar production and a lack of coordinatedgovernment policy.

Pakistan’s 2010/11 (Oct/Sept) total sugar production is forecast at 3.77MMT (Million Metric Tonnes), an increase of 10 percent over last year’sestimate. The increase is largely driven by higher prices and a strongdemand. Despite efforts to achieve self-sufficiency, Pakistan remains anet importer of sugar. In MY 2009/10 sugar imports are forecast at 1.03million tons and 700,000 tons in MY 2010/11. Sugar consumption in MY2009/10 is expected to decrease 50,000 tons due to limited sugarsupplies and price increases. Sugar consumption in 2010/11 is forecast at4.28 MMT.

SUGARCANEProduction:

Pakistan has the 5th largest sugarcane growing area in the world and isthe 15th biggest global producer of sugar. Sugarcane is grown on arounda million hectares and provides the raw material for Pakistan’s 84 sugarmills. The sugar industry is the country’s second largest agro-industryafter textiles. Besides its edible use, Pakistan also uses sugar to producealcohol for medicinal purposes, ethanol for fuel, chip board

manufacturing, etc.

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 3/16

In 2009/10, (Oct/Sept) Pakistan’s sugarcane production is estimated at47.8 MMT, down 2.2 million tons from last year’s estimate. The decreasein sugarcane area and lower production during the last couple of yearsare attributed to the non-transparent government sugar policies,

significant increase in minimum support prices for competing crops (e.g.wheat and rice), dwindling water resources, and higher input costs.

Internal disputes between Pakistan’s sugar growers and processors alsoplague the industry. Procurement practices used by sugar processorssuch as delaying the crushing season, buying cane at less than thesupport price, and withholding payments hurt the farmers’ profitability.On the other hand, sugar processors complain that farmers growunapproved varieties that produce low sucrose content resulting in lowersugar production and recovery rates. As a result of the fluctuations inquantity and quality of raw material, sugar mills have been required tooperate at 50 percent of their installed capacity. Furthermore, the lowersugarcane supplies have also forced most of the mills in cane producingareas to close 1-2 months earlier than normal.

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 4/16

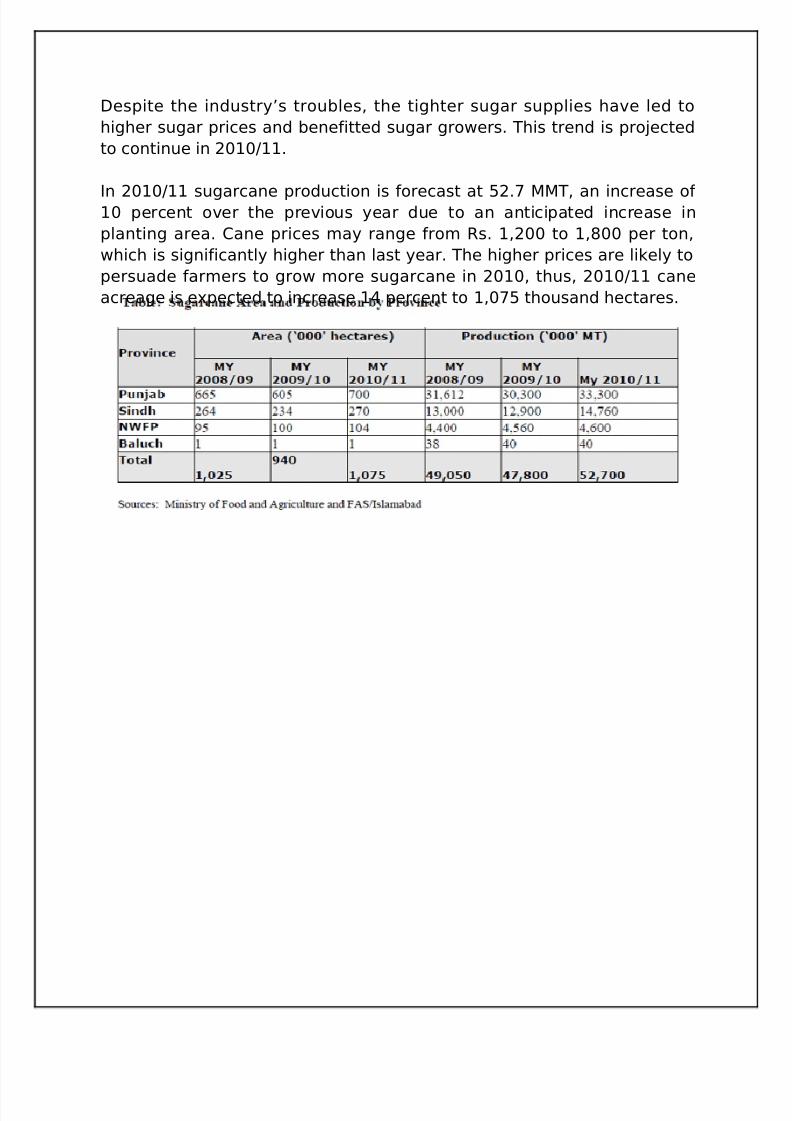

Despite the industry’s troubles, the tighter sugar supplies have led tohigher sugar prices and benefitted sugar growers. This trend is projectedto continue in 2010/11.

In 2010/11 sugarcane production is forecast at 52.7 MMT, an increase of 10 percent over the previous year due to an anticipated increase inplanting area. Cane prices may range from Rs. 1,200 to 1,800 per ton,which is significantly higher than last year. The higher prices are likely topersuade farmers to grow more sugarcane in 2010, thus, 2010/11 caneacreage is expected to increase 14 percent to 1,075 thousand hectares.

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 5/16

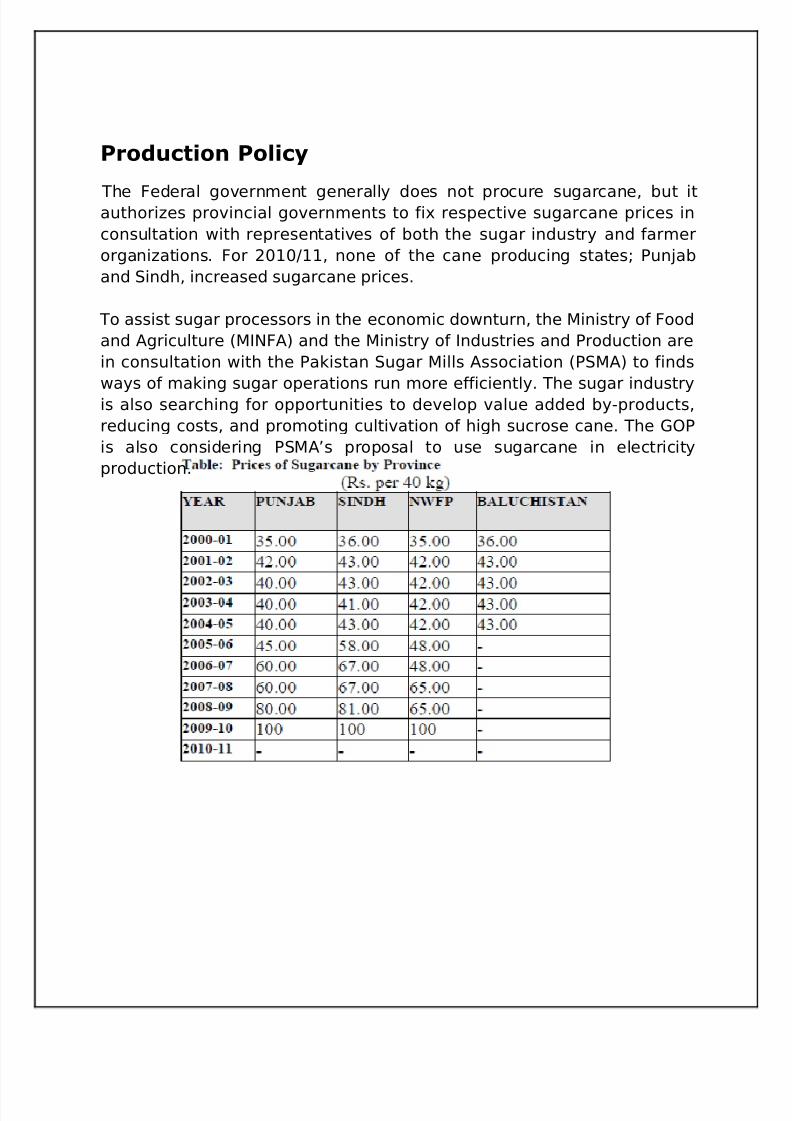

Production Policy

The Federal government generally does not procure sugarcane, but itauthorizes provincial governments to fix respective sugarcane prices inconsultation with representatives of both the sugar industry and farmerorganizations. For 2010/11, none of the cane producing states; Punjaband Sindh, increased sugarcane prices.

To assist sugar processors in the economic downturn, the Ministry of Foodand Agriculture (MINFA) and the Ministry of Industries and Production arein consultation with the Pakistan Sugar Mills Association (PSMA) to findsways of making sugar operations run more efficiently. The sugar industryis also searching for opportunities to develop value added by-products,reducing costs, and promoting cultivation of high sucrose cane. The GOPis also considering PSMA’s proposal to use sugarcane in electricityproduction.

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 6/16

SUGAR

Production

In 2010/11 refined sugar production is forecast at 3.75 MMT, primarilydue to anticipated increase in area under sugar cane crop. Pakistan’sdomestic consumption is expected to be 4.28 MMT. Domestic productionwill be supplemented through imports. For MY 2009/10, refined sugarproduction is estimated at 3.42 MMT (raw value) based on 80 percentcrushing and 8.9 percent recovery. The production decreased primarilydue to a smaller growing area, which is down 8 percent from the previousyear.

The MINFA and the PSMA have initiated a sugar crop development projectutilizing sugar beets. The provinces of Punjab and Sindh have alreadyconducted research in the cultivation of sugar beet with limited success.Industrial adoption and commercialization of sugar beet have been slowbecause it requires additional research as well as comprehensiveplanning on the part of government, industry and the farming community.In addition, the sugar industry is reluctant to promote sugar beetcultivation because the amount of time needed to process beets intosugar. The hot temperatures and processing delays could also easilydeteriorate the quality of the product. Beet processing requires more fuel,

making it costlier compared to cane processing. In order to promote thisinitiative, the GOP is considering tax holidays for companies that processsugar beets.

Consumption:

The 2010/11 sugar consumption is forecast at 4.28 MMT. Consumption estimatesfor MY 2009/10 is lowered to 4.2 million tons, 50,000 tons less than the earlierestimates due to relatively tight domestic supplies and higher prices.

Although limited sugar supplies and the steady increase in prices have affectedhousehold sugar consumption, overall sugar consumption remains the same dueto growing demand by the processed food sector (soft drinks, fruit drinks, dairy,confectionary, traditional sweets etc). Bulk consumers such as bakeries, makersof candy and local sweets, and soft drink manufacturers account for about 60percent of the total sugar demand.

Pakistan’s sugar industry continued to deal with uncertainty in CY 2009 due todecreasing sugar production and a lack of coordinated government policy.Despite the Economic Coordination Committee of the Cabinet’s (ECC’s) February2009 decision to import 200,000 metric tons of sugar, the Trading Corporation of Pakistan (TCP -government entity responsible for importing and exportingcommodities) was still unable to arrange timely imports. As a result of the

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 7/16

government’s inability to deal with the supply situation, the Pakistan SupremeCourt intervened to stabilize sugar prices. Despite the Supreme Court’sintervention, however, sugar prices continued to rise due to the tighter supplies.Sugar prices have been on the rise since May 2008 and reached record levels inDecember 2009. The current sugar retail price is around $803 per ton, about 60percent higher than last year’s level. Prices are expected to hover around Rs.60in the remaining part of the year due to anticipated better sugar supplies in theinternational market. The future stability of retail prices will depend upon timelyimports and prevailing prices in the international market.

Trade:

In 2010/11 sugarimports are forecastat 700,000 MT, andMY 2009/10 sugarimports areestimated at1,030,000 MT. On

January 2010, theECC decided toimport 1.25 milliontons of refined sugarfrom theinternational market.Accordingly, the GOPauthorized the TCP to import 500,000 MT for government stocks and theremaining 750,000 MT for the private sector before June 2010.

The ECC also decided that the private sector import would be exemptedfrom sales taxes and other duties to ensure that landing cost of imported

sugar will range around Rs.50 per Kg and retail price at Rs.55. The ECC

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 8/16

also decided to scrap the 16 percent General Sales Tax (GST) in order tostem the rise of sugar prices.

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 9/16

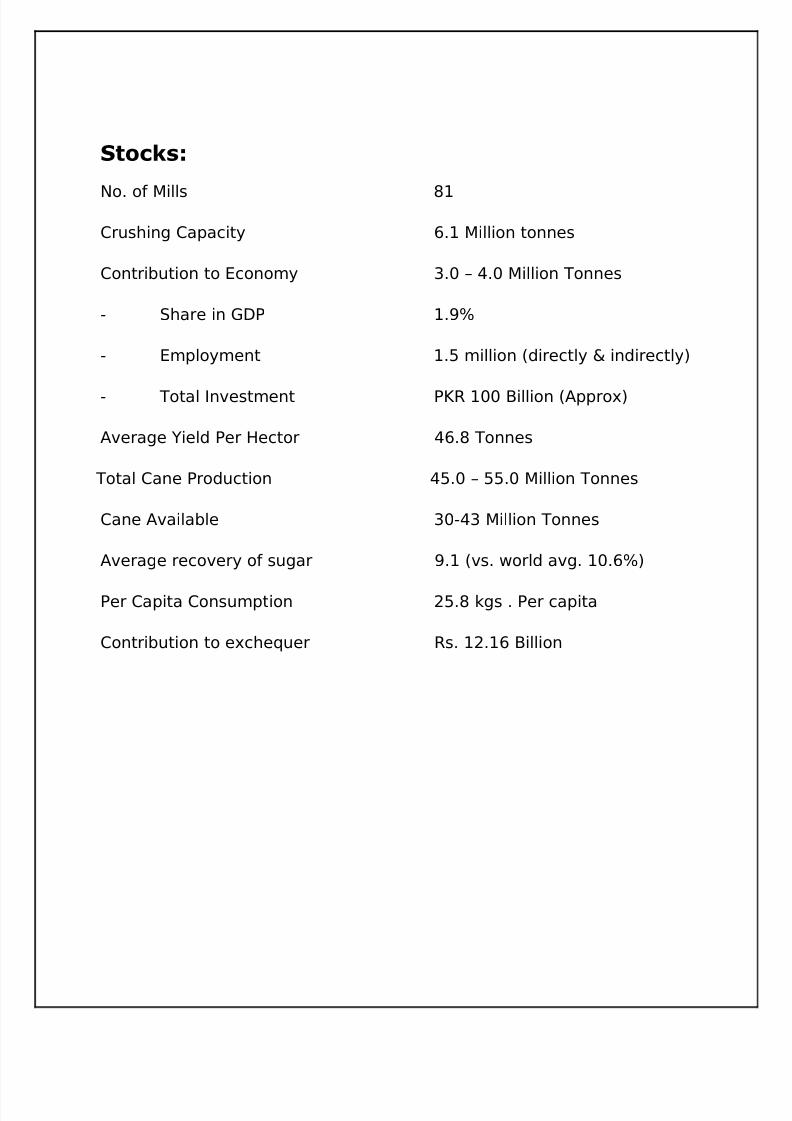

Stocks:

No. of Mills 81

Crushing Capacity 6.1 Million tonnes

Contribution to Economy 3.0 – 4.0 Million Tonnes

- Share in GDP 1.9%

- Employment 1.5 million (directly & indirectly)

- Total Investment PKR 100 Billion (Approx)

Average Yield Per Hector 46.8 Tonnes

Total Cane Production 45.0 – 55.0 Million Tonnes

Cane Available 30-43 Million Tonnes

Average recovery of sugar 9.1 (vs. world avg. 10.6%)

Per Capita Consumption 25.8 kgs . Per capita

Contribution to exchequer Rs. 12.16 Billion

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 10/16

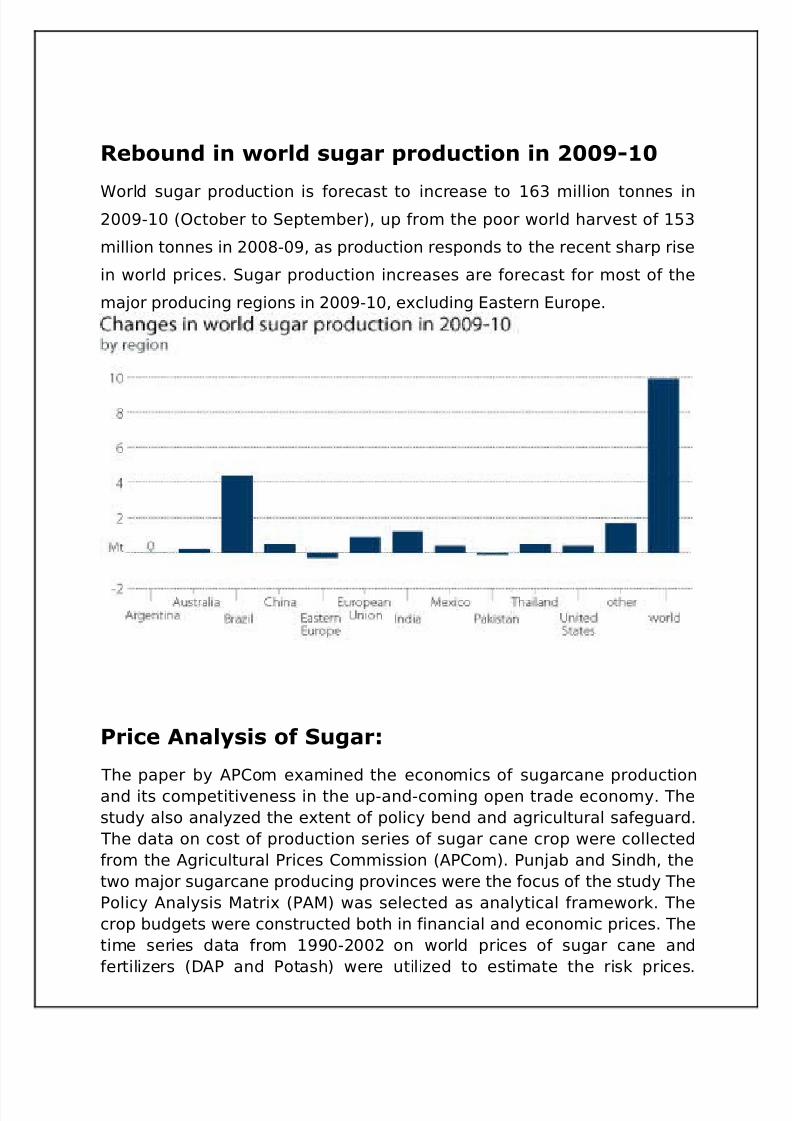

Rebound in world sugar production in 2009-10

World sugar production is forecast to increase to 163 million tonnes in2009-10 (October to September), up from the poor world harvest of 153

million tonnes in 2008-09, as production responds to the recent sharp rise

in world prices. Sugar production increases are forecast for most of the

major producing regions in 2009-10, excluding Eastern Europe.

Price Analysis of Sugar:

The paper by APCom examined the economics of sugarcane productionand its competitiveness in the up-and-coming open trade economy. Thestudy also analyzed the extent of policy bend and agricultural safeguard.

The data on cost of production series of sugar cane crop were collectedfrom the Agricultural Prices Commission (APCom). Punjab and Sindh, thetwo major sugarcane producing provinces were the focus of the study ThePolicy Analysis Matrix (PAM) was selected as analytical framework. Thecrop budgets were constructed both in financial and economic prices. Thetime series data from 1990-2002 on world prices of sugar cane andfertilizers (DAP and Potash) were utilized to estimate the risk prices.

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 11/16

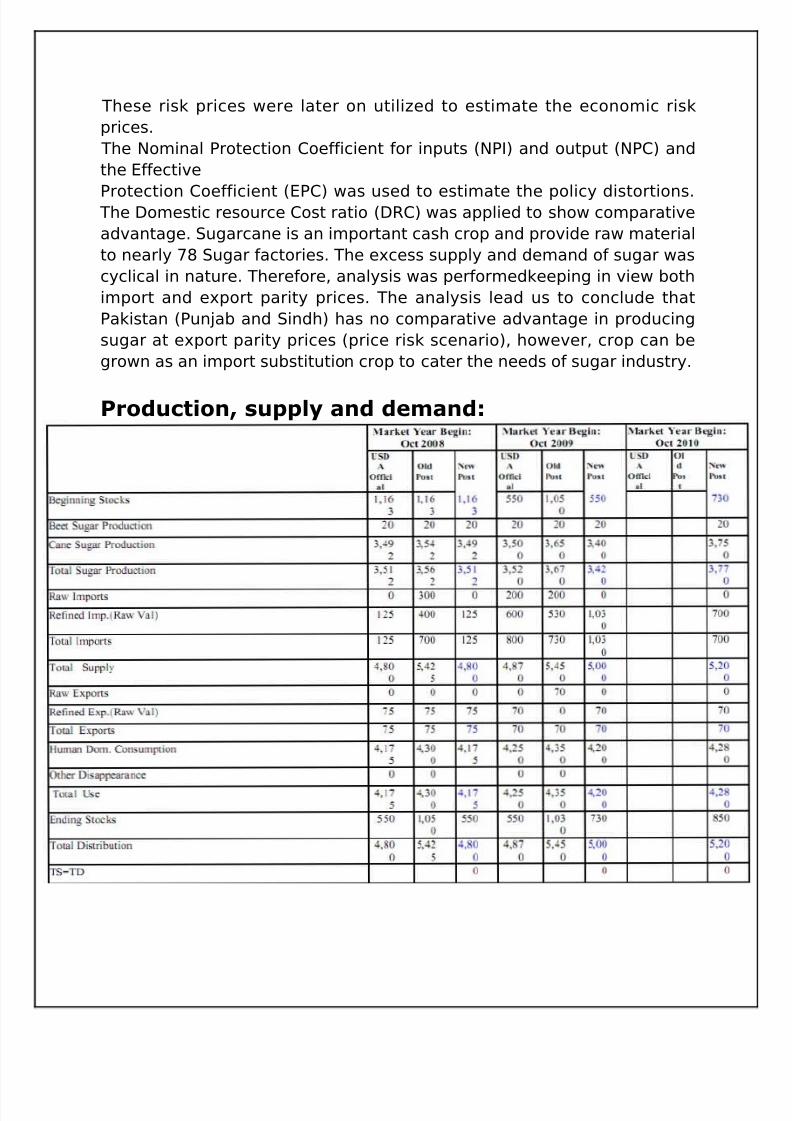

These risk prices were later on utilized to estimate the economic riskprices.

The Nominal Protection Coefficient for inputs (NPI) and output (NPC) andthe Effective

Protection Coefficient (EPC) was used to estimate the policy distortions. The Domestic resource Cost ratio (DRC) was applied to show comparativeadvantage. Sugarcane is an important cash crop and provide raw materialto nearly 78 Sugar factories. The excess supply and demand of sugar wascyclical in nature. Therefore, analysis was performedkeeping in view bothimport and export parity prices. The analysis lead us to conclude thatPakistan (Punjab and Sindh) has no comparative advantage in producingsugar at export parity prices (price risk scenario), however, crop can begrown as an import substitution crop to cater the needs of sugar industry.

Production, supply and demand:

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 12/16

Supply and Demand Graph (2007-2010)

Yearly Price Graph (Nov. 2006 till Nov. 2010)

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 13/16

Factors affecting Sugar price:

✔ Creating artificial shortage by hoarding✔ Price manipulation tactics✔ Price in the international market✔ Involvement of Politicians✔ Failure of government regulatory control✔ Lack of research and development programs✔ Lower national yield as compared to international yield ratio✔ Decrease in value of Pakistani Rupee✔ Lack of strategic planning by government

Forecast for 2011:Pakistan has revised a forecast of 2010/11 sugar production to 3.7 milliontonnes, up by about 500,000 tonnes from an earlier estimate, despite flooddamage to the sugarcane crop, officials said on Friday.

The government had earlier expected up to 3.2 million tonnes of sugar from thecrop, after the country's worst floods washed away nearly 10.5 million tonnes of sugarcane.

But after recent surveys of the flood-hit areas in the main sugar-growingprovinces of Punjab and Sindh, government and industry officials told a meetingon Thursday that yield would be higher in areas where there were rains but nofloods.

"Although floods damaged the crop, because of excessive rains we areexpecting a healthy crop and up to 20 percent increase in yield per acre," JavedKayani, chairman Pakistan Sugar Mills Association (PSMA), told Reuters.

"Our estimate is that we should be able to produce about 3.7 million tonnes of sugar from the crop."

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 14/16

Some of the sugar mills in Pakistan:

Abdullah Sugar Mills Ltd Kamalia Sugar Mills Ltd

Adam Sugar Mills Ltd Kashmir Sugar Mills Ltd

Ashraf Sugar Mills Ltd Kohinoor Sugar Mills Ltd

Baba Farid Sugar Mills Ltd Layyah Sugar Mills Ltd

Brother Sugar Mills Ltd National Sugar Mills Ltd

Channar Sugar Mills Ltd Noon Sugar Mills Ltd

Chaudhry Sugar Mills Ltd Pattki Sugar Mills LtdCrescent Sugar Mills Ltd CSK (Phalia) Sugar Mills

Fatima Sugar Mills Ltd Punjab Sugar Mills Ltd

Fauji Sugar Mills Ltd Ramzan Sugar Mills Ltd

Fecto Sugar Mills Ltd Shahtaj Sugar Mills Ltd

Gojra Samundri Sugar Mills Ltd Shakarganj Mills Ltd

Hamza Sugar Mills Ltd Tandlianwala Sugar MillsHaseeb Waqas Sugar Mills Yousaf Sugar Mills Ltd

Hunza Sugar Mills Chishtia Sugar Mills Ltd

Husein Sugar Mills Ltd Gunj Buksh Sugar mill

Indus Sugar Mills Pahrianwali Sugar Mills Ltd

Ittefaq Sugar Mills Ltd Sheikhoo Sugar Mills Ltd

JDW Sugar Mills Ltd United Sugar Mills Ltd

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 15/16

Conclusion and Recommendations:

Sugar cane crop is an important cash crop of Pakistan and is grown onarea of more than on million hectares. It provides raw material to 77sugar factories besides indigenous “brown Sugar” cottage industry(APcom, 2003). The sugarcane crop is beset with many problems: oneabysmally low yield leading to yearly fluctuation in production, andsecondly monopolistic exploitation of sugar cane growers by the powerfulsugar syndicate. The sugar cane highly water consumptive crop, thuslosing comparative advantage id water scarce scenario. Therefore, it isimportant to look at the economics of sugar cane production in the WTOregimes.

The DRC (at import parity prices) was 0.59, 0.52 and 0.57 for Punjab,Sindh and Pakistan respectively and remained almost same up to fifthyear. Thus, Pakistan will have comparative advantage in sugar caneproduction as an import substitution crop (import parity prices) in thefuture.

The DRC (at export parity prices was 1.51, 1.10 and 1.19 for Punjab,Sindh and Pakistanrespectively. This showed that in the future, Punjab would have nocomparative advantage in sugar cane production at export parity prices.In conclusion, Pakistan sholud grow sugarcane only to maintain self sufficiency level as it will be cheaper in domestic market than to invest onimport of sugar cane. It will not be feasible for country to grow for exportpurposes. On the other hand, the country should increase sugar caneproductivity per unit of resource use especially scarce irrigation water.

Recommendations: The sugar industry must spearhead the research and development effortsso as to meet its raw material requirements and to control the prices of sugar which increases continuously The specific recommendations are:

1. The marketing of the produce, raw material as well as end product, hasemerged a key issue requiring serious attention of the government. Themarket imperfections must be removed through marketing efficiency andinstitutionalization of market intelligence.

2. The recurring water shortage is posing a serious challenge to the largescale cultivation of sugarcane being highly water consumptive crop. It isin the interest of industry and farmers to curtail its area but promote the

8/8/2019 Report on Sugar

http://slidepdf.com/reader/full/report-on-sugar 16/16

cultivation of improved varieties with rational use of inputs and improvedcrop management. The sugarcane is highly water consumptive crop. Thepresent flat rate system is allocatively neutral leading to misallocation of this scarce resource. Therefore, the water pricing of is imperative for its

rational use.

3. The vertical integration rather than horizontal expansion of the sugarindustry is the need of the hour. The value added products e.g. spirits,yeast, acetic acid, citric acid, glucose etc., must be produced .Thedevelopment of these products would help reduce the cost of sugar whichremains the principal produce.

References:

[1] APCom (Agricultural Prices Commission).2002. “Support Price Policy”.Reports on Sugarcane. Agricultural Prices Commission, Islamabad.[2] APCom (Agricultural Prices Commission). 2003. “Support Price Policy”.Reports on Sugarcane, Agricultural Prices Commission, Islamabad.[3] Alpine, R.W.L. and J.Pickett.1993.”Agricultur, Liberalization and

Economic Growth in Ghanaand Cote D’ivoire, 1960-1990. OECD Development Center, Paris[4] Appleyard, D. R. 1987. “Report On Comparative Advantage”.Agricultural Prices Commission(APCom series No.61) Islamabad[5] Chishti, A.F. and W. Malik. 2001. “WTO’s Trade Liberalization,Agriculture Growth andPoverty Alleviation in Pakistan”. The Pakistan Development Review 40:4part II 1035-1052[6] Food and Agriculture Organization of United Nations 1997. “Theimpact of trade liberalization

on production of agricultural commodities and related fertilizer use to2000.”