report on marine insurance premium 2002 and 2003 tore forsmo, managing director astrid seltmann,...

TRANSCRIPT

Report on Marine Insurance Premium 2002 and 2003

Tore Forsmo, Managing DirectorAstrid Seltmann, Analyst

The Central Union of Marine Underwriters, Oslo, Norway

Thanks also toFédération Française des Sociétés d’Assurances (FFSA) and the

International Underwriting Association of London (IUA)

IUMI 2004 Singapore IUMI 2004 Singapore Facts & Figures CommitteeFacts & Figures Committee

World Merchant Fleet by type of ship of 300gt and over

As at January 1st, 2004 – Number of ships in share of the World Reported Fleet, growth rate 1999-2004 (%) and average age

General cargo 35.6% (-4.03%)

Oil Tankers 19.1% (+7.61%)

Container ships 7.6% (+28.48%)

Passengers 10.0% (+9.51%)

Bulk carriers 15.1% (+2.66%)

Liquefied gas 2.9% (+10.48%)

Chemical tankers 3.3% (+1.37%)

Reefer ships 3.0% (-12.85%)

Ro-Ro cargo 3.0% (+8.16%)

Ore/Bulk/Oil 0.4% (-23.79%)

WORLD REPORTED FLEET Total number : 39,665 ships

increased by + 2.85% on the period Average age : 19.1 years

22.2 years

18.2 years

15.2 years

22.1 years

10.5 years

15.9 y

17.6 y

19.6

y

19.8

y

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Merchant Reported Fleet by type of ships 300gt and over

As at January 1st, 2004 – Deadweight and growth rate 1999-2004

840.355

90.214 12.107

317.827

20.835 8.791

289.510

80.259

6.758 8.171 5.883

+ 48.60%

+ 15.83%+ 18.61%

+ 11.93%

- 33.20%

- 5.71%- 9.65%

+ 9.95%+ 3.41%

+ 27.17%

+ 14.23%

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

Oil Tankers Chemicaltankers

Liquefiedgas

Bulk carriersOre/Bulk/Oil Containerships

Passengers Generalcargo

Reefer shipsRo-Ro cargo Total

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

million DWT in 2004 Growth rate 1999/ 2004

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Merchant Fleet of ships of 300gt and over

Evolution of the growth rates (GT, DWT, and Number of ships) between 1993 and 2004

39,665 ships + 14.2%

38,500 ships (+ 10.8%)

488,032 mGT (+ 18.8%)

570,325 m GT + 38.9%

743,611 mDWT (+ 12.2%)

840,355 m DWT + 26.8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Merchant Fleet by National and Foreign Flag

As at January 1st, 2004 – million DWT and number of ships

13,283 13,183 13,071 12,905 12,91612,646

12,22512,996

13,12113,342 13,305

13,840

0

100

200

300

400

500

600

700

800

900

1999 2000 2001 2002 2003 2004

million DWTNational Flag Foreign Flag

Ships of 1,000 GT and over

Total Units in the :

Reported Fleet

Not Reported Fleet

Total World Reported Fleet

25,508

3,700

26,179

3,371

26,192

3,524

26,247

3,686

26,221

4,174

26,486

4,117

29,208 29,550 29,716 29,933 30,395 30,603

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Merchant Fleet – Top Ten Countries by National (NF) and Foreign Flags (FF)

As at January 1st, 2004

0

20

40

60

80

100

120

Mill

ion

DW

T

0

5

10

15

20

25

30

35

Years

million DWT NF million DWT FF Average Age NF Average Age FF

Top Ten Countries Fleet Average Age : 15.1 years

Ships of 1,000 GT and over

Average Age FF : 13.9 years Average Age NF : 18.0 years

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

DWT-rank 2004 (2003)

Country of ManagementTotal fleet -

million DWT 2004

% share on the Total

World Fleet Reported in

2004

Growth rate 2003/2004

1(1) GREECE 156.4 20.1% + 5.0%2(2) JAPAN 109.5 14.0% + 6.1%3(3) NORWAY 50.8 6.5% -10.1%4(6) GERMANY 48.3 6.2% + 18.7%5(4) CHINA, PR of 45.6 5.8% + 6.8%6(5) USA 45.3 5.8% + 8.9%7(7) HONG-KONG 31.4 4.0% -16.5%8(8) KOREA, Rep.of 25.4 3.3% -0.8%9(10) SINGAPORE 23.0 2.9% + 20.4%10(9) TAIWAN 22.7 2.9% + 0.9%

558.4 71.6%Others countries 221.3 28.4% + 4.2%

779.7

832.2 4,117 ships for 52.5 million dwt

not reported

WORLD MERCHANT FLEET - THE TOP TEN COUNTRIES OF MANAGEMENT As at January 1st, 2004 – Rank in 2004 (in 2003) and million DWT

Total Top Ten Countries of Management

Total World Merchant Fleet by Country of Management

Total World Merchant Fleet (including fleets for which the Country of Management is unknown)

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

Orderbook Evolution by type of ship

90.5 95.8 112.7 113.3 115.6

77.4

51.5

5.0

32.7

6.0

0

20

40

60

80

100

120

140

160

180

1998 1999 2000 2001 2002 2003

Tankers >=1,000dwt Bulk Carriers >=10,000dwt LNG/LPG Carriers

Container Vessels >=5,000dwt Others (of which Passenger Vessels >=1000grt)

Total million DWT : 171.2

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

Deliveries in 2003 by Country of Shipbuilder

Million DWT and number of ships

45.6

19.6

18.0

3.0

0.8

0.8

0.6

2.8

49.6

19.4

20.7

3.6

1.1

0.6

1.0

6.8

54.6 (1,051)

20.4 (329)

22.4 (230)

5.7 (145)

1 (51)

0.4 (12)

1.1 (13)

3.6 (271)

0 10 20 30 40 50 60

TOTAL

Japan

S.Korea

China, PR of

Germany

Poland

Taiwan

Others countriesEnd 2003

End 2002

End 2001

DELIVERIES by Region : ASIA : 750 ships (71.4% share)

EUROPE : 265 ships (25.2% share)Others : 36 ships

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Seaborne Trade Volume Development 1993-2003 (in million tonnes)

Growth rate in 2003

+ 4.1%

+ 6.8%

+ 3.2%

+ 4.4%

900

1,100

1,300

1,500

1,700

1,900

2,100

2,300

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003(*)

Maj

or tr

ades

4,000

4,500

5,000

5,500

6,000

6,500

Total W

orld Trade

Crude oil and oil products The 4 main Dry Bulk Cargoes (Iron Ore, Coal, Grain, Bauxite/Alumina)Other Cargoes Total World Trade (*) estimates

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Market Price Indices for Selected Commodities

Annual Average (1993-2003) – Average in 2004 as at end of May (*)

134.6

125.8

114.7

0

30

60

90

120

150

180

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 (*)

Grain Non ferrous metal Agricultural raw material

Index 2000 = 100

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

World Market Price Indices for Selected Commodities

Annual Average (1993-2003) – Average in 2004 as at end of May (*)

161.2

190.2

117.5

0

20

40

60

80

100

120

140

160

180

200

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 (*)

Iron ore, scrap metals Coal Crude oil

Index 2000 = 100

Source: Indicators issued from various sources such as ISL Bremen for World fleet and trading figures (as at May 2004) and Clarkson Research Studies for shipbuilding and scrapped vessels (as at June 2004).

Report on marine insurance premiums 2002 and 2003

• By end of August 2003, 46 of 56 members reported their country’s marine premium figures for accounting years 2002 and 2003.

• Reported figures represent approx. 97% of the total marine premium written by all IUMI members in 2002 and 2003.

• Total premium for 2002 is therefore estimated to reach approx. USD 13.3 billion and for 2003 approx. USD 15.3 billion (excluding P&I from mutual P&I Clubs).

World Merchant Fleet and Global Marine Hull & Liability Premium

Index of evolution, vessels > 100 GT, 1995 = 100%

Source: Indicators for World Fleet from ISL Bremen

0%

25%

50%

75%

100%

125%

150%

1995

1996

1997

1998

1999

2000

2001

2002

2003

No. Ships

Gross tonnage

Global Marine Hull &Liab. Premium

World Seaborne Trade Volume and Global Cargo Premium

Index of evolution, 1995 = 100%

Source: Indicators for World Trade Volume from ISL Bremen

50%

75%

100%

125%

150%

1995

1996

1997

1998

1999

2000

2001

2002

2003

Total World TradeVolume

Global CargoPremium

Global premiums reported 1998 to 2003 (accounting years)

0 2000 4000 6000 8000 10000 12000 14000 16000

USD (millions)

Total

Offshore / Energy

Marine Liability

Transport / Cargo

Global Hull 20032002200120001999

Reported Increase

2002->2003

15.2%

15.4%

15.0%

12.5%

15.0%

A major part of the 15 % increase is due to a weakening of US$ against major European and Asian currencies and thus not a real global volume increase!

Estimate of increase 2002->2003 without exchange rate impact

9%

3%

9%

7%

6%

Index of evolution of Exchange rates between US$ and selected currencies

(as of December each year)

Source: Norges Bank Exchange Rates Statistics

60%

70%

80%

90%

100%

110%

120%

130%

1999 2000 2001 2002 2003

EUR

GBP

JPY

NOK

Market Shares 2003

2.1%11.6%

24.5%

61.9%

EuropeAsia/PacificNorth AmericaRest of World

Europe : Albania, Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Romania, Russia, Slovenia, Spain, Sweden, Switzerland, Turkey, Ukraine, United Kingdom (IUA + Lloyds)Asia/Pacific : Australia, China, Hong Kong, India, Indonesia, Japan, North Korea, South Korea, Malaysia, New Zealand, Pakistan, SingaporeNorth America : Bermuda, Canada, USARest of the World : Congo, Egypt, Israel, Ivory Coast, Kenya, Lebanon, Mexico, Morocco, Nigeria, South Africa,Tunisia, United Arab Emirates

Countries in italics did not report for 2003

Report on marine insurance premiums - by economic areas

(USD Millions)

0

2000

4000

6000

8000

10000

1997 1998 1999 2000 2001 2002 2003

Accounting Year

Europe

Asia/Pacific

NorthAmerica

Rest of theWorld

A major part of the increase in European volume is due to a weakening of the US$ against European currencies and thus not a real volume increase.

Global Marine Premium 1992 - 2003 (USD Million), as reported

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Accounting Year

Dotted lines show estimated increase without exchange rate impact.

Total

Cargo

Hull

EnergyLiability

0

200

400

600

800

1000

1200

1400

Accounting Year

FranceItalyJapanNorwaySpainUK (ILU/IUA)UK (Lloyd's)USA

Global Hull Premium - Major Markets 1992 - 2003 (USD Million)

Global Cargo Premium - Major Markets 1992 - 2003 (USD Million)

0

500

1000

1500

2000

2500

Accounting Year

Belgium

China

France

Germany

Italy

Japan

Netherlands

Spain

Sweden

Switzerland

UK (ILU/IUA)

UK (Lloyd's)

USA

MARINE MUTUAL MARKET SECTORGross Calls (Premium) – Operational location

0

200

400

600

800

1000

1200

1400

1998 1999 2000 2001 2002 2003

Accounting Year

Japan

Norway

Sweden

UK

US

Per accounting year – USD Million

Source: Standard & Poors Marine Mutual Report 2004

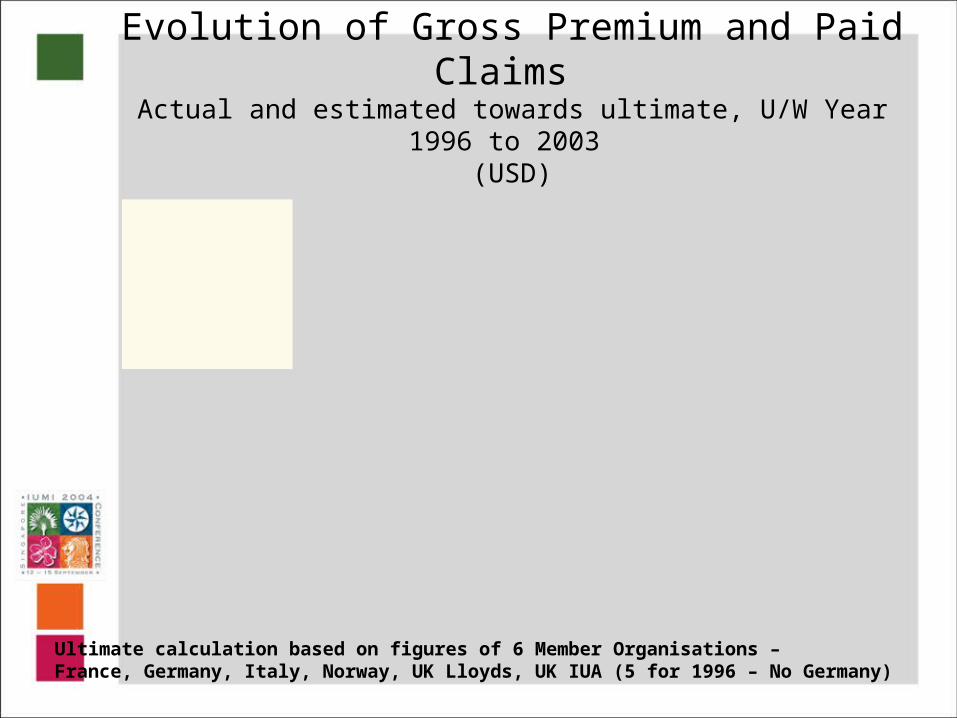

Ultimate calculation based on figures of 6 Member Organisations – France, Germany, Italy, Norway, UK Lloyds, UK IUA (5 for 1996 – No Germany)

Marine Hull – Evolution of Gross Premium and Paid Claims Actual and estimated towards ultimate, U/W Year 1996 to 2003

(USD)

end of 1996 1997 1998 1999 2000 2001 2002 2003 ultimate0

500

1000

1500

2000

2500

3000

1996 underwriting year

end of 1997 1998 1999 2000 2001 2002 2003 2004 ultimate0

500

1000

1500

2000

2500

3000

1997 underwriting year

end of 1998 1999 2000 2001 2002 2003 2004 2005 ultimate0

500

1000

1500

2000

2500

3000

1998 underwriting year

2000 underwriting year

end of 2000 2001 2002 2003 2004 2005 2006 2007 ultimate0

500

1000

1500

2000

2500

3000

USD

end of 1999 2000 2001 2002 2003 2004 2005 2006 ultimate0

500

1000

1500

2000

2500

3000

1999 underwriting yearUSD USD

USD

USD

2000 underwriting year

end of 2002 2003 2004 2005 2006 2007 2008 2009 ultimate0

500

1000

1500

2000

2500

3000

USD 2002 underwriting year

end of 2001 2002 2002 2004 2005 2006 2007 2008 ultimate0

500

1000

1500

2000

2500

3000

USD 2001 underwriting year

end of 2003 2004 2005 2006 2007 2008 2009 2010 ultimate0

500

1000

1500

2000

2500

3000

USD 2003 underwriting year

Blue line = Gross Premium; Red line = Paid Claims

0%

20%

40%

60%

80%

100%

120%

140%

12 24 36 48 60 72 84 96

Ultim

ate

1996

1997

1998

1999

2000

2001

2002

70%

2003

Ultimate calculation based on figures of 6 Member Organisations: France, Germany, Italy, Norway, UK Lloyds, UK IUA (5 for 1996 – No Germany)

Marine Hull – Evolution of Gross Loss Ratio, actual and estimated towards ultimate

U/W Year 1996 to 2003 Assuming a

30% expense ratio

(acquisition and

management expenses),

technical break even is

achieved when the gross loss ratio does not exceed 70%

1999

1998

2000/ 2002

1997 / 20012003

1996

Transport / Cargo – Evolution of Gross Premium and Paid Claims

Actual and estimated towards ultimate, U/W Year 1996 to 2003 (USD)

Totals of 7 Member Organisations – Belgium, France, Germany, Italy, Netherlands, UK Lloyds, UK IUA (6 for 1996 – no Germany)

Blue line = Gross premiumRed line = Paid claims

Blue line = Gross premiumRed line = Paid claims

end of 1996 1997 1998 1999 2000 2001 2002 2003 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

1996 underwriting year

end of 1997 1998 1999 2000 2001 2002 2003 2004 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

1997 underwriting year

end of 1998 1999 2000 2001 2002 2003 2004 2005 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

1998 underwriting yearUSD USD USD

end of 1999 2000 2001 2002 2003 2004 2005 2006 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

1999 underwriting yearUSD

end of 2000 2001 2002 2003 2004 2005 2006 2007 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

USD 2000 underwriting year 2001 underwriting year

end of 2001 2002 2003 2004 2005 2006 2007 2008 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

USD 2001 underwriting year

end of 2002 2003 2004 2005 2006 2007 2008 2009 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

USD 2002 underwriting year

end of 2003 2004 2005 2006 2007 2008 2009 2010 ultimate0

500

1000

1500

2000

2500

3000

3500

4000

USD 2003 underwriting year

Blue line = Gross Premium; Red line = Paid Claims

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

12 24 36 48 60 72 84 96

Ultim

ate

1996

1997

1998

1999

2000

2001

2002

70%

2003

Ultimate calculation based on totals of 7 Member Organisations – Belgium, France, Germany, Italy, Netherlands, UK Lloyds, UK IUA (6 for 1996 – no Germany)

Transport/Cargo – Evolution of Gross Loss Ratio, actual and estimated towards ultimate

U/W Year 1996 to 2003 Assuming a

30% expense ratio

(acquisition and

management expenses),

technical break even is

achieved when the gross loss ratio does not exceed 70%

0%

20%

40%

60%

80%

100%

120%

140%

1996 1997 1998 1999 2000 2001 2002 2003

Marine Hull

Cargo/Transport

Marine Hull and Cargo/TransportGross Ultimate Loss Ratio

U/W Year 1996 to 2003 Assuming a

30% expense ratio

(acquisition and

management expenses),

technical break even is

achieved when the gross loss ratio does not exceed 70%