report of the president's commission to study capital ... · iii the president’s commission...

TRANSCRIPT

WASHINGTON, D.C. FEBRUARY 1999

REPORTof thePRESIDENT’SCOMMISSIONto STUDYCAPITAL BUDGETING

Page

i

TABLE OF CONTENTS

Letter of Transmittal ................................................................................................................ iiiAcknowledgements .................................................................................................................... vPreface ........................................................................................................................................ 1Executive Summary .................................................................................................................. 3What is ‘‘Capital’’? ..................................................................................................................... 9Trends in Capital Spending ..................................................................................................... 13Budgeting Capital ..................................................................................................................... 17Do Current Budget Conventions Distort Decisions About Federal Capital Spending? ....... 25Recommendations ...................................................................................................................... 31Pros and Cons of a ‘‘Cap’’ on Capital Spending ...................................................................... 39A Capital Budget and Depreciation ......................................................................................... 43Other Versions of a Capital Budget ........................................................................................ 45Conclusion .................................................................................................................................. 45Endnotes .................................................................................................................................... 47Selected References and Bibliography ..................................................................................... 51Appendix A: Executive Order 13037: Commission to Study Capital Budgeting, and the

Amendments .......................................................................................................................... 53Appendix B: Commission Membership .................................................................................... 57Appendix C: List of Witnesses and Written Statements ....................................................... 59Appendix D: Outline of Material on the Website ................................................................... 61

GENERAL NOTES

This publication may be purchased from the U.S. Government Printing Office andits bookstores. An order form is included in this publication. The report is alsoavailable, with testimony and other supporting materials, on the Internet at:http://www.whitehouse.gov/pcscb.

Numerical detail in this document may not add to the totals because of rounding.

iii

The President’s Commissionto Study Capital Budgeting

Co-Chairs

Kathleen Brown

Jon S. Corzine

Members

Willard W. Brittain

Stanley E. Collender

Orin S. Kramer

Richard C. Leone

David A. Levy

James T. Lynn

Cynthia A. Metzler

Luis Nogales

Carol O’Cleireacain

Rudolph G. Penner

Steven L. Rattner

Robert M. Rubin

Herbert Stein

February 1, 1999

Honorable William J. ClintonThe PresidentThe White House1600 Pennsylvania Avenue, N.W.Washington, D.C. 20500-0001

Dear Mr. President:

We are hereby submitting the final report of the Commission to Study Capital Budgeting.

As you requested, we have concentrated on capital spending by the federal government. However, we haveconcluded that capital spending by all levels of government, as well as by the private sector, provides thenation with important long-term benefits.

Our research shows that the current budget process does not permit decision-makers in the executivebranch and Congress to pay sufficient attention to the long-run consequences of their decisions. Thisresults in inefficient allocation among capital expenditures and shortchanges the maintenance of existingassets.

In this report, we propose a series of recommendations that we believe would improve each of thecomponent parts of the budget process: setting priorities currently and for the long run, making budgetdecisions in the current year, reporting on those decisions, and subsequently evaluating them in order tomake improvements in future years. We do not propose, however, the current adoption of a formal capitalbudget, as defined and discussed in the report.

To implement the proposed recommendations, the executive branch and Congress must ensure that theappropriate information is made available to decision-makers and the public throughout the budgetprocess. As a result, policy makers will be both properly informed when deciding how to spend taxpayers’money, and held accountable by the public for those decisions.

This report reflects the views of commissioners from many different backgrounds. We reached ourconclusions after conducting nine hearings, at which more than thirty experts from the private and publicsectors presented their views. While the members of the commission endorse the recommendationspresented herein, individual members do not necessarily agree with all of the analysis or with each andevery word of the report.

The commission worked diligently to carry out your directions. We hope that our recommendations willhelp the Administration, future presidents, and the Congress in improving the budget process, especiallyas it relates to decisions about capital spending.

Respectfully,

Kathleen Brown, Co-Chair Jon S. Corzine, Co-Chair

v

ACKNOWLEDGEMENTS

The commission operated under the auspices of the U.S. Department of the Treasury. Assistingthe commission were staff members of the Office of Management and Budget and the Depart-ment of the Treasury, as well as individuals from organizations with which some of the commis-sioners are affiliated. The commission is grateful for all this support, and wants to acknowledgethe following people who made contributions to the overall effort and to this report:

Dick Emery, Executive Director to the commission (OMB)Robert E. Litan, writer of the report (The Brookings Institution)E. William Dinkelacker, Designated Federal Official (Department of the Treasury)

Barry Anderson (former Executive Director and formerly of OMB)Barbara Basser-Bigio (Goldman, Sachs & Co.)Bethann J. Beck (PricewaterhouseCoopers)Jesse Brackenbury (Levy Institute)Thomas J. Craren (PricewaterhouseCoopers)Philip R. Dame (OMB)Joshua Gotbaum (OMB)Lawrence W. Hush (OMB)Robert W. Kilpatrick (OMB)Sarah Lee (OMB)Patrick Locke (OMB)Rusty Moran (OMB)Jason Orlando (OMB)Justine Rodriguez (OMB)Arthur Stigile (OMB)

1

1 The full text of the initial order and subsequent amendmentsare shown in Appendix A. Other materials the commission exam-ined in carrying out its duties, including summaries and full ver-sions of the testimony the commission heard from a variety of ex-perts and interested parties, are posted on the website of the com-mission at: www.whitehouse.gov/pcscb.

2 The staff from the various organizations who provided assist-ance to the commission are listed in the Acknowledgements.

PREFACEBy Executive Order 13037, issued on March

3, 1997, the President of the United Statesestablished this Commission to Study CapitalBudgeting. The order directed the commissionto prepare a report discussing various aspectsof capital budgeting, including the budgetingof capital in other countries, state and localgovernments, and the private sector; theappropriate definition of capital; the roleof depreciation in capital budgeting; andthe effect of a capital budget on budgetarychoices, macroeconomic stability, and budg-etary discipline. 1

Since its formation, the commission hashad nine meetings, has heard testimony andreceived written submissions from many indi-viduals from the public and private sectors,

and has reviewed the relevant and voluminousprofessional literature. It has carried outits work on its own. The Administrationdid not provide any instructions concerningparticular results or suggestions that it wantedthe commission to explore or recommend.

This report is the product of the commis-sion’s hearings and of deliberations amongits members and associated staff. 2 The mem-bers of the commission endorse the rec-ommendations presented in the report, al-though individual commissioners may notagree with all of the analysis or with eachand every word. In some cases, the separateviews of certain commissioners on selectedsubjects are provided in footnotes to thereport (which are signified by alphabeticalletters; all other numbered notes after thispreface are found at the end of the report).

3

EXECUTIVE SUMMARYThe subject of capital budgeting—or indeed

public budgeting for any purpose—may appearto be of interest to only a special audience:government professionals ‘‘inside the Beltway’’and perhaps some analysts in the investmentcommunity. Nothing could be further fromthe truth.

The budget of any organization, privateor public, is a statement of both the resourcesto be made available to the organizationand the priorities of those who manageit. The budget that the President submitsto the Congress, which in fiscal year 1999covered expenditures of nearly $2 trillion,tells the American people how the administra-tion proposes to spend their taxes and, untilrecently, the proceeds of federal debt issuedto finance the shortfall between total expendi-tures and revenues. The budget is thusinherently a political document, but in thebest sense of the term. This is becauseit reflects the collective judgment of theindividuals in a democracy about how muchpublic funds are to be raised and howthey are to be used.

This commission has devoted its attentionto one particular kind of expenditure inthe federal budget: spending on ‘‘capital.’’Although this term has been defined invarious ways for different purposes, a commonelement among all of the definitions is thatcapital spending—whether undertaken by theprivate or public sector—is intended to gen-erate benefits over the long run.

In this report, we have concentrated oncapital spending by the federal governmentbecause it is our charge. But we cannotemphasize too strongly that capital spendingat all levels of government, as well asby the private sector, provides importantbenefits to the nation as a whole in significantpart because those benefits are deliveredover the long run. It is easy in the day-to-day battles over budget policy to forgetthat such spending helps determine the kindof society that we and our children willlive in—not just this year but many years

from now as well. We therefore encouragethis president and future presidents to helpeducate American citizens about the impor-tance of devoting current resources towardfuture needs—in the form of spending oncapital by both the private and public sectors.

Most firms in the private sector, as wellas many state and local governments, recog-nize the importance of capital expendituresby making decisions about them separatelyfrom decisions about how much to spendon annual operating expenses. By contrast,the federal government has never done this.

This commission has been directed to exam-ine whether this practice ought to bechanged—that is, whether the federal govern-ment should adopt a ‘‘capital budget’’—and,if not, what other steps, if any, shouldbe taken to improve the federal decision-making process as it relates to spendingon capital or ‘‘investment’’ expenditures.

Capital budgeting is a process that takesexplicit account of capital spending levels.In this report, we primarily examine versionsof a capital budget in which either: (1)the size of the deficit or surplus is madeto depend, in part or in whole, on theamount of expenditures defined as ‘‘capital,’’or (2) a single decision is made about howmuch to spend on ‘‘capital,’’ under somedefinition. A variation of the first definitionis what we label the ‘‘simplistic’’ versionof the capital budget, one in which capitalspending may be financed, in part or intotal, by borrowing. We treat the seconddefinition as the equivalent of imposing aseparate ‘‘cap’’ on expenditures defined tobe capital, or in the alternative, a processwhereby the depreciation of capital is explicitlytaken into account in the budget process.We briefly note in a concluding section thatthere are other, perhaps less formal, variationsof a capital budget that we do not extensivelyanalyze here.

The commission had its origins duringthe Congressional debate about whether toamend the Constitution to require the federal

4 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

a Comment of Commissioners Corzine, Kramer, Leone, Levy,O’Cleireacain, Rattner, and Rubin: We wish to register our strongopposition to any amendment to the Constitution that would man-date balanced federal budgets. The macroeconomic straightjacketimplied by such a change in the Constitution would cost the nationdearly in lost growth, unnecessary unemployment, and slow recov-ery from recessions. Indeed, were such an amendment to pass, itwould be essential that many spending items be exempted rou-tinely, while others be exempted under clearly defined cir-cumstances. Rather than simplify the budget process, it would thenbecome more confused and opaque. In addition, democratic govern-ance would suffer since the ability of Congress and the presidentto respond to public priorities would be unduly constrained.

Specifically, in a recession tax receipts fall and spending for suchitems as unemployment insurance rises. This imbalance offsets re-cessionary forces, thus speeding recovery. It is one of the reasonseconomic downturns have been less severe since World War II thanbefore. Indeed, the insistence on trying to balance the budget inthe early 1930s is generally considered to have deepened the GreatDepression. The counter-cyclical advantages of the current systemare not trivial. Giving them up may lead to real costs, particularlyamong working men and women: income lost when governmentcannot fight a recession is lost forever.

b Comment of Commissioners Lynn, Penner, and Stein: We donot favor adopting at this time a capital budget of any kind, wheth-er of the kind here labeled ‘‘simplistic’’ or any other known to us.We endorse the qualification ‘‘at this time’’ to allow for the possibil-ity that future developments in information, sophistication, anddiscipline in the budgetary process might recommend a differentcourse.

c Comment of Commissioners Corzine and Levy: These weak-nesses in the budget process may have macro as well as micro con-sequences. One of the aggregate effects of sub-optimal choices may,at times, be either an inadequate or an excessive level of capitalspending.

d Comment of Commissioners Corzine, Leone, and O’Cleireacain:We believe it is both possible and desirable to move towardclassifying the federal budget in two parts: as ‘‘capital,’’ in thesense of investment with long-term effects: and as ‘‘operating,’’such as consumption expenditures and transfer payments for thecurrent year. This approach, which is consistent with private sectororganizations’ practices, would enable the U.S. government to bet-ter understand, manage, and finance its commitments.

As is the custom at the state and local levels of government, acapital budget classification does not mean that the governmentwould lose its flexibility to manage during periods of fiscal con-straint/plenty. Nor does it mean that all capital expenditures mustbe financed from borrowed funds. Moreover, the definition of cap-ital, like other aspects of the current budget structure, could be re-fined and updated over time.

government to have a balanced budget everyyear. Nothing in this report should be con-strued as support for the balanced budgetamendment considered by the Senate in 1996. a

Nor does the commission endorse the adoptionof the simplistic version of the capital budget.Furthermore, a majority of the membersof the commission does not support, at thistime, adopting a budget procedure that wouldimpose a separate cap on capital spending. b

The reasons for reaching these conclusionsare spelled out in the body of the report.

At the same time, we have concludedfrom our study of existing practices andafter gathering evidence from a wide rangeof experts, that the existing federal budgetprocess—as it affects decision-making aboutcapital expenditures as well as other typesof spending—has significant weaknesses. In-sufficient attention is paid to the long-runconsequences of budget decisions. Capitalspending in particular is inefficiently allocatedamong projects. Moreover, the current processshortchanges the maintenance of existing as-sets. c

Accordingly, the commission urges the Con-gress and the executive branch to undertakea thorough examination of how the budgetprocess may be improved beyond addressingcapital-related needs. Toward this end, itmay be productive for both branches tocreate a new Commission on Budget Conceptsto aid them with this task.d

In the meantime, we believe there area series of constructive responses to theshortcomings we have identified, though theydo not include adopting any particular formof a capital budget as we have just definedthe term. These responses are aimed atimproving each of the component parts ofthe budget process: setting priorities currentlyand for the long run, making budget decisionsin the current year, reporting on those deci-sions, and subsequently evaluating them inorder to make improvements in future years.Key to achieving these improvements is ensur-ing that the appropriate information is madeavailable to decision-makers and the publicthroughout the process so that policy makers(1) are properly informed when deciding howto spend taxpayers’ money and (2) can beheld accountable by the public for thosedecisions.

The recommendations we summarize belowtake account of two important features offederal budgeting.

First, many government efforts have objec-tives, such as the management of foreignaffairs or the defense of the nation, thatcannot be readily measured in monetaryterms. In stark contrast, it is relativelyeasy to keep score in the private sector,where firms are often judged by a singlemetric, such as current profitability, return

5EXECUTIVE SUMMARY

e Comment of Commissioners Kramer, Leone, and O’Cleireacain:We believe the text over-emphasizes ‘‘theoretical’’ market disciplinewhen it comes to borrowing for capital by the states. Most states,as a simple matter of ‘‘capacity to pay,’’ could borrow much morethan they do. In fact, almost always, in the real world the actualconstraints are political (including referendum requirements) andpractical—demands for current revenues limit the amounts avail-able for debt service.

on equity, or the dollar value of their share-holders’ equity.

Second, borrowing is subject to less dis-cipline at the federal level than it is atlower levels of government. States and local-ities cannot ‘‘print money’’ to cover the debtsthey issue, whereas one arm of the federalgovernment—the Federal Reserve—has theability to ‘‘monetize’’ debt issued by theTreasury. A related difference is that federaldebt is viewed by the marketplace as prac-tically free of default risk, whereas statesand localities have a strong interest in main-taining high credit ratings, which constrainsborrowing at the state and local level. e

These considerations necessarily imply thatfederal budgeting rules should not simplyreplicate rules that may be used in theprivate sector or at the state and locallevels of government. But at the same time,because the existing federal budget processhas the weaknesses we have noted, certainimprovements are appropriate. We have con-centrated on suggestions for the executivebranch; however, as will become evident below,certain of these require the cooperation ofand concurrence by the Congress.

We also recognize the essential role ofthe American people as monitors, advocates,and parties whose interests ultimately areat stake during the budget process. Forthis reason it is important to increase thetransparency of that process—not only toenhance the quality of inputs to the Congressfrom the private sector and other levelsof government, but also to increase the federalgovernment’s accountability to the Americanpeople.

To facilitate the setting of prioritiesamong all programs, not just those involv-ing capital expenditures, the commissionrecommends:

Recommendation 1: Five-Year StrategicPlans.—Although federal agencies are now re-

quired (under the Government Performanceand Results Act) to prepare strategic plansevery three years and performance plans an-nually, this process should be improved in sev-eral respects:

• The strategic plans should (1) be preparedannually, (2) be integrated with the an-nual performance plans and the agencies’five-year budget projections that are nowsubmitted to the Office of Managementand Budget (OMB), and (3) be includedas an integral part of the budget justifica-tions sent to the Congress.

• The strategic plans of the agencies andtheir annual budgets should be tied to thelife-cycles of their capital assets.

• OMB should standardize the formats ofthese plans, in consultation with GAO andCBO, to make them more useful to policymakers.

• OMB should expand its efforts to evaluatethe plans and facilitate the Administra-tion’s use of them for government-wideplanning.

• Congress should take such plans into ac-count in deciding on annual agency appro-priations. It should also consider how itmight improve its own procedures so thatit can pay more attention both to thelonger-run implications of its current yeardecisions and to issues with longer-runconsequences. In undertaking this task,Congress might find it useful to take ad-vantage of the wide range of institutionalexpertise available to it, including re-sources within the Congressional BudgetOffice, the General Accounting Office, andthe Congressional Research Service.

Recommendation 2: Benefit-Cost Assess-ments.—There should be an ongoing effortwithin the federal government to analyze thebenefits and costs of all major government pro-grams (whether or not related to capital spend-ing), so that they can be adjusted, refashioned,or eliminated, as appropriate. OMB, the agen-cies, and the Congress (through GAO and CBOin particular) should be given the resourcesto carry out this important function.

6 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

f Comment of Commissioner Levy: I urge the Congress to ad-dress the lease-purchase problem as part of a special or com-prehensive amendment to the current budget process. I discuss thisissue in greater detail in a subsequent footnote (l).

To improve the process by which an-nual budget decisions are made, thecommission recommends:

Recommendation 3: Capital AcquisitionFunds.—To promote better planning andbudgeting of capital expenditures for federallyowned facilities, Congress and the executivebranch should experiment by adopting for oneor more agencies separate appropriations for‘‘capital acquisition funds’’ (CAFs). Budget au-thority would be lodged in the CAFs for feder-ally owned capital assets. The CAFs would‘‘rent out’’ their facilities to the various pro-grams within each agency, charging them theequivalent of debt service.

• CAFs would help ensure that individualprograms are assessed the cost of usingcapital assets.

• By spreading capital costs across entireagencies, CAFs would help smooth out thelumpiness in appropriations sometimes as-sociated with large capital projects.

• If the CAF experiment proves successful,the CAF approach should be adoptedthroughout the government.

Recommendation 4: Full Funding forCapital Projects.—All capital projects, or us-able segments thereof, should be fully fundedbefore the work begins. In this way, Congresscan fully evaluate their likely costs and bene-fits before appropriating funds for them.

Recommendation 5: Adhering to theScoring Rules for Leasing.—Existing rulesthat govern the scoring of leases should bestrictly followed by both agencies and the Con-gress. This will discourage the signing of short-term leases when it is cheaper over the longrun to construct or purchase a facility. f

Recommendation 6: Trust Fund Re-forms.—Although trust funds for highways,airports, and other uses insulate certain typesof spending from the balancing process thatis inherent in the rest of the budget, they canbe useful if the funds going into them trulyrepresent charges or fees for the use of thegovernment services they support. But this

purpose is fulfilled only if the monies raisedby earmarked taxes or fees to support infra-structure or other types of capital—averagedover some reasonable period, such as threeyears—are actually spent on the dedicateduses.

• To ensure that this is done, the President’sbudget should disclose the earmarkedtaxes or fees and spending of these variouscapital-related trust funds. This will allowpolicy makers to make informed decisionsabout whether to increase spending on theauthorized activities or reduce the chargesnow being assessed purportedly to financethose activities.

• State and local governments that are re-cipients of capital-related grants from thefederal government should be required tomaintain their capital—such as high-ways—as a condition to receiving any ad-ditional federal aid (unless those govern-ments can demonstrate that there is nolonger a need for the assets the federalgovernment initially supported).

Recommendation 7: Incentives for AssetManagement.—The executive branch and theCongress should experiment with incentives toencourage agencies to manage their assets effi-ciently. One possibility might be to allow, onan experimental basis, one or more agenciesto keep a limited portion of the revenues theyraise from selling or renting out existing as-sets.

Steps must be taken to improve themethods that are used to give the resultsof those decisions (and the programsthey support) to the public and policymakers. In particular:

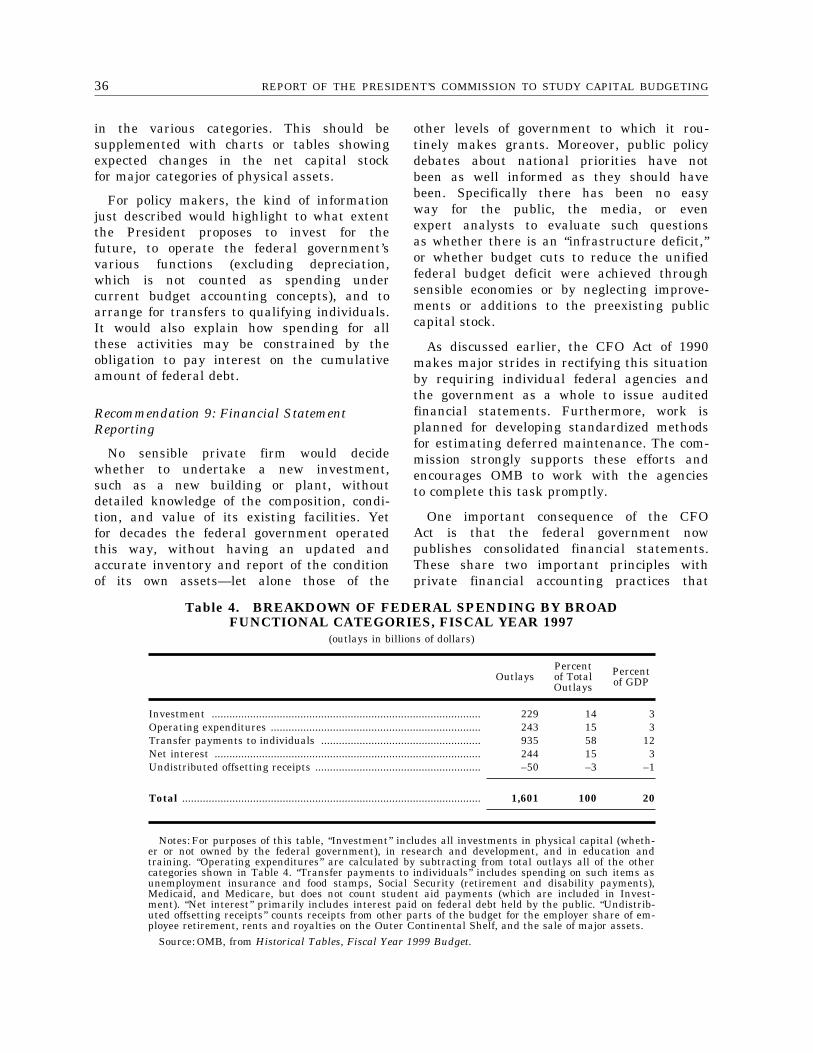

Recommendation 8: Clarification of theFederal Budget Presentation.—The Presi-dent’s annual budget should contain a break-down of proposed current and projected federalspending over the budget year and the subse-quent four years among the following cat-egories: investment, operating expenditures,transfers to individuals, and interest. Such abreakdown would make available to policymakers and the wider public the President’slong-run vision for federal spending. This in-formation might also encourage Congress to

7EXECUTIVE SUMMARY

g Comment of Commissioners Lynn, Penner, and Stein: We donot believe that this four-way classification of expenditures wouldbe helpful in making good budgetary decisions.

find ways of taking a longer-run view in itsannual budget deliberations. g

Recommendation 9: Financial StatementReporting.—Reporting on financial activitiesand asset positions of the federal governmentshould be enhanced in a number of ways tobetter inform the Congress and the publicabout the ways in which the federal govern-ment’s assets are being used and maintained:

• Federal agencies should be required toissue to policy makers and the public moredetailed information (both in print formand on their websites) about the composi-tion and condition of the federally ownedor managed capital assets under their con-trol. OMB should consolidate these re-ports, which should continue to be basedon independently developed accountingstandards, and report on them in sum-mary fashion in the annual budget.

• There should be enough information in theconsolidated reports to provide Congressand the public with accurate benchmarksfor making appropriate comparisons bothin the current year and over time.

• The calculation of depreciation in variousgovernment reports should be standard-ized.

With more comprehensive, objective informa-tion on how the federal government as awhole, as well as individual agencies andprograms, have used resources, increased ordepleted assets, and undertaken new invest-ments, debates over critical national policieswould be better informed. Private corporationsreport audited financial results and assetand liability positions to investors. By thesame token, the federal government shouldmake available to the American people auditedfinancial statements and underlying detailthat go well beyond the information shownannually in the unified budget. Just ascorporate decision-makers have accurate ac-counting data to help them assess past per-formance and make decisions about the future,Congress and the public should also haveaccurate accounting on federal assets andinvestments.

Recommendation 10: Condition of Exist-ing Assets.—Work is planned at the federallevel for agencies to begin developing stand-ardized methods for estimating deferred main-tenance. The commission strongly supportsthese efforts and encourages OMB to workwith the agencies to complete this taskpromptly and to implement its results. In addi-tion, the federal government, working withstates and localities, should endeavor to reporton the condition of assets owned at these lowerlevels of government, or at least those thathave received federal support. In combinationwith the rest of the information provided inthe audited financial statements, data on de-ferred maintenance will enable policy makersto develop sound plans for maintaining exist-ing assets and spending on new ones wherethat is advisable.

Finally, steps should be taken to im-prove the process used in evaluatingthe impact of past budgetary decisions,so that policy makers can be in a positionto make improvements, if warranted.

Recommendation 11: Federal ‘‘ReportCard.’’—Under OMB guidance, agenciesshould assess the extent to which major invest-ment projects have produced returns in excessof some benchmark cost of capital, such asthe prevailing interest rate on long-term fed-eral debt, the average cost of capital expectedby private market investors, or some otherthreshold that OMB believes the public wouldfind useful. This federal ‘‘Report Card’’ couldbe included in the President’s annual budget.The commission recognizes that the projectsfor which it might be feasible to provide amonetary analysis may account for a relativelysmall fraction of total spending; nonetheless,it believes that over time advances in estimat-ing techniques may permit a larger fractionof total spending to be evaluated in this man-ner. Where benefits and costs cannot be ex-pressed in monetary terms, the evaluationsshould identify project objectives and assessoutcomes qualitatively.

The foregoing recommendations are summa-rized in the table on the following page.The columns in the table refer to threedifferent classes of capital, which are discussedin the body of the report: the federal govern-ment’s own assets (such as buildings in

8 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

which federal agencies are located), the federalgovernment’s investment in assets owned bystate and local governments (such as high-ways), and the federal government’s invest-ment in what we have labeled intangiblenational assets that are financed but notowned by the government (such as benefitsaccruing from federal expenditures on researchand development and or on education). Ourrecommendations are then classified both bythe stage of the budget process at whichthey are directed and by the types of capitalthat they are likely to affect. Because anumber of our recommendations are designedto improve decision-making with respect toone or more categories of capital, they arelisted in multiple columns.

While the primary responsibility for initiat-ing most of the foregoing recommendationsrests with the executive branch, in certaincases Congress also has an important role.

Indeed, virtually all of the recommendationsrequire active Congressional cooperation ifthey are to have a positive effect on thebudget process and budget decisions.

Although the commission as a whole doesnot endorse setting a separate cap on capitalspending, it nonetheless discussed the tech-nical details of such a change in budgetprocedure. The concluding section of thisreport contains our findings on these issues,outlines the key pros and cons of subjectingcapital spending to its own limit, analyzesproposals to reflect depreciation of capitalassets in the budget process, and brieflydescribes some alternative versions of a capitalbudget.

In sum, the federal budget process canbe and should be improved. The commissionbelieves the recommendations outlined in thisreport would help accomplish this objective.

Summary of Recommendations by Stage of the Budget Processand Type of Capital Affected

Federal Investment In:

Federal Assets State/Local Assets Intangible Assets

Strategy and Planning .......... Five-Year Plans Five-Year Plans Five-Year PlansBenefit-Cost Analysis Benefit-Cost Analysis Benefit-Cost Analysis

Decision-Making .................... CAFsFull FundingProper Lease ScoringTrust Fund Reforms Trust Fund ReformsInvestment Life-Cycle Plan-

ningStates/Localities Maintain

AssetsIncentives for Better Asset

Management

Reporting ................................ Improved Financial Report-ing

Improved Financial Report-ing

Improved Financial Report-ing

Audited Financials Audited Financials Audited FinancialsAsset Inventory Asset Inventory

Evaluation .............................. Report Card Report Card Report Card

9

h Comment of Commissioner Levy: A distinction must be madebetween practical and theoretical definitions. Defining investmentbased on its benefits (such as ‘‘increasing social welfare’’ or ‘‘in-creasing long-term growth’’) is useful in theoretical discussions, butno accounting is possible since we can never be sure which outlaysqualify. At the same time, practical definitions—such as those em-bodied in Generally Accepted Accounting Principles (GAAP)—al-ways have shortcomings, but still can be very useful. If we are toconsider using investment or capital in federal accounting andbudgeting, then we must resign ourselves to the use of practicaldefinitions. The definitions of the Federal Accounting StandardsAdvisory Board (FASAB) are a functioning example.

WHAT IS ‘‘CAPITAL’’?This commission has been charged with

examining capital budgeting in other coun-tries, states and local governments, and theprivate sector, and, in the process, withaddressing a number of questions about capitalbudgeting. It is only appropriate, therefore,to begin with the threshold issue: whatis ‘‘capital’’ (or its annualized counterpart,‘‘investment’’)?

The commission has not settled on, nordoes it endorse, a single definition of capital. 1

Instead, a series of distinctions between dif-ferent types of capital or ‘‘investment’’ spend-ing, both by governments and by firms inthe private sector, seem warranted for dif-ferent purposes (and different commissionersplace varying amounts of emphasis on alter-native definitions of capital).

One distinction relates to the functionsof capital. At its broadest level, any spendingthat yields benefits beyond the typical report-ing period (such as a year) should be consid-ered to be investment, and ‘‘capital’’ refersto the assets created by this spending. Sucha definition would encompass spending notonly on physical or fixed assets, such asstructures and equipment, but also on humanand a variety of intangible assets. ‘‘Humancapital’’ consists of the skills imparted toindividuals through training and educationthat enable them to increase their earningsnot just in a single year, but potentiallythroughout their lives. Intangible assets cancover a very broad class of items. In privatesector financial accounting, for example, intan-gibles are often measured by the expendituresrequired to gain patents, copyrights, trade-marks, or other intellectual property protec-tion. Certain types of public spending—includ-ing research and development (R&D), defense,nutrition, disease prevention, police protection,and drug treatment and prevention pro-grams—may also produce intangible assetsthat deliver, or are at least designed todeliver, benefits over years, if not lifetimes.

Broad definitions of investment or capitalcould be useful for several purposes. For

example, to the extent citizens and policymakers are interested in enhancing economicgrowth, the definition should count both pri-vate and public sector spending on buildings,equipment, research and development (includ-ing some defense-related R&D), and educationand training. An even broader definitionwould be justified if the goal were to measurecapital aimed at improving social welfare—one that included expenditures on nationaldefense and police to enhance security aswell as spending on childhood immunization,maternal health, nutrition, and substanceabuse, to improve the health and well-beingof citizens over many years. h

The accounting standards used in the pri-vate sector do not take such an expansiveapproach to the definition of capital. Generallyspeaking, they limit capital to physical andcertain intangible assets (such as investmentsin intellectual property). Similarly, the Na-tional Income and Product Accounts (NIPA)—the federal government’s statistical systemfor collecting and reporting data on overalleconomic activity—define capital to be spend-ing only on physical assets. 2 It is importantto keep in mind, however, that while theseaccounting standards may be conservative,they do not necessarily constrain the waymanagers think about spending that provideslonger-run benefits. For example, althoughprivate sector accounting standards defineemployee training expenditures as an expense,this spending typically generates longer-termbenefits to the firm (and to the employees).The fact that these expenditures are writtenoff during the course of a year does notstop managers or investors from considering

10 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

them as investments in the future well-being of the firm.

A second distinction relates to who ownscapital: specifically, whether it is owned pri-vately or publicly (and if publicly, by federal,state, or local governments). Individuals andfirms reap most of the benefits from thespending on capital they undertake; however,the public benefits when government is mak-ing the expenditures. For example, governmentspending to educate each generation of citizensbenefits the entire public by ensuring thatthe population continues to be literate, cog-nizant of the benefits of our system ofgovernment, and able to work in an ever-changing economic environment. Similarly,when the government spends money on thenation’s defense or finances basic scientificresearch, the benefits accrue to all citizens.Appropriately enough, economists call invest-ments that confer benefits on a wide classof parties ‘‘public goods’’ because no privateperson or firm can capture all of theirbenefits. Identifying and funding those pro-grams that produce returns to society wellabove the cost of capital is especially importantfor enhancing economic growth.

These points highlight the different criteriathat are used to decide whether to addto private and public capital. In the privatesector, capital spending decisions are madebased primarily on how they affect sharehold-ers, and are evaluated predominantly in mone-tary terms. In the public sector, decisionsabout capital take into account the impacton the public at large and rest on bothmonetary and non-monetary considerations.

A third distinction is between federal govern-ment capital and national capital. Federalgovernment capital, as we use the term,refers only to those assets the governmentowns, such as federal buildings or federalmilitary hardware. National capital is a broad-er term, including all government spendingaimed at delivering long-term benefits toany portion of the nation, whether or notit is owned by the federal government. So,for example, using the broad functional defini-tion of capital discussed above, national capitalwould include spending at all levels of govern-ment on roads and other physical assets,research and development, and education and

training, among other items. At the federallevel, what OMB labels as ‘‘federal investmentoutlays,’’ illustrated in Table 1, representsfederally financed national capital regardlessof who owns it. 3 As the table shows, nearlyhalf of the federal government’s investmentoutlays in fiscal year 1997 were devotedto physical capital, about one-third to researchand development, and the balance to educationand training—roughly the same proportionsthat were prevalent during the earlier partof the decade. 4

Federal government capital, in contrast,can be defined as including only assets ownedby the federal government, so it can beaccounted for in a fashion similar to theway capital is measured in the private sector.For example, OMB’s Capital ProgrammingGuide, which provides guidance to federalagencies on capital planning, procurement,and management, defines ‘‘federal capital’’to include land, structures, equipment, andintellectual property (including software) be-longing to the federal government that hasan estimated useful life of at least twoyears. Consistent with this definition, Table2 illustrates how the federal governmentprovided almost $66 billion of budget authorityfor fiscal year 1997 on ‘‘major capital acquisi-tions’’: government buildings, information tech-nology, and ‘‘other items’’ (weapons systemsin the case of the Department of Defense,and facilities and equipment for other agen-cies). The table shows that the major partof the federally owned investment was fordefense-related purposes.

This distinction between ‘‘national’’ and ‘‘gov-ernment’’ capital is of more than academicinterest. As discussed below, the governmentof New Zealand has adopted a separatecapital budget but only for government capital.In contrast, the General Accounting Officehas suggested defining a budget target thatis a variation of national capital: publicinvestments that promise ‘‘to raise the privatesector’s long-run productivity,’’ which wouldinclude spending on infrastructure, non-de-fense R&D, education and training, and somedefense activities, but would specifically ex-clude what GAO calls ‘‘federal capital,’’ suchas government-owned buildings, weapon sys-tems, and land [GAO, 1993].

11WHAT IS ‘‘CAPITAL’’?

Table 1. FEDERAL INVESTMENT OUTLAYS,FISCAL YEAR 1997

(billions of dollars)

Outlays Percentof total

Physical capital:Direct federal defense ..................................................................... $52.4 23%Direct federal nondefense ............................................................... 19.7 9%Grants to state and local governments ......................................... 41.5 18%

Subtotal, physical capital ........................................................... 113.6 50%

Research and development:Defense ............................................................................................ 40.2 18%Nondefense ...................................................................................... 30.9 14%

Subtotal, research and development .......................................... 71.1 31%

Education and training:Grants to state and local governments ......................................... 25.0 11%Direct federal ................................................................................... 19.0 8%

Subtotal, education and training ................................................... 44.0 19%

Total, federal investment outlays ........................................ 228.8 100%

Source: OMB, Analytical Perspectives, Fiscal Year 1999, p. 125.

Table 2. MAJOR FEDERAL CAPITALACQUISITIONS, FISCAL YEAR 1997

(budget authority, in billions of dollars)

Construction and rehabilitation:Defense military construction and family housing 4.2Corps of Engineers ................................................... 1.6General Services Administration ............................ 1.4Department of Energy .............................................. 1.2Department of the Interior ...................................... 1.0Other agencies .......................................................... 5.6

Subtotal, construction and rehabilitation ........... 15.1

Major equipment:Department of Defense ............................................ 42.8Department of Transportation ................................ 2.2NASA ......................................................................... 0.6Department of the Treasury .................................... 0.3Other agencies .......................................................... 4.4

Subtotal, major equipment ................................... 50.3

Purchases of land and structures ............................... 0.3

Total, major acquisitions ........................................ 65.7

Source: OMB, Analytical Perspectives, Fiscal Year 1999, p. 135.

12 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

A fourth definitional distinction is betweencapital created by (1) direct government spend-ing and (2) public and private capital spendinginduced by government policies. The advantageof confining any definition to direct spendingis that measurement is relatively easy. None-theless, if the objective is to measure theimpact of overall government policy on na-tional capital (narrowly or broadly defined),then a definition based only on the govern-ment’s direct expenditures is too limited.A full accounting would also require inclusionof capital spending at the state and locallevels and by the private sector that maybe brought about by such policies as federaldeficit reduction (through lower interest rates),and targeted tax incentives, as well as regu-latory mandates such as those requiring orinducing expenditures on pollution controlor occupational safety. 5 Granted, such inducedspending may be very important; however,the operational problem with adding inducedexpenditures is that they cannot be directlymeasured, but instead must be estimated,using economic models or survey responses.

The different definitions underscore theproposition that ‘‘capital’’ is not a single,uniform concept, but one that varies accordingto why the term is being used. Indeed,this is one reason that most members ofthe commission are opposed to recommendingthat a separate capital budget using onesingle definition of capital be adopted fordecision-making purposes. Nonetheless, defini-tional issues should not stand in the wayof illuminating the consequences of choosingamong different government programs, wheth-er or not they are labeled as capital. Norshould debate over definitions distract atten-tion from (1) the need to improve planningand evaluation for whatever expenditures pol-icy makers may choose to label as capital,or, (2) in the case of federal capital inparticular, the need to identify the assetsthe government has and report them ina coherent way.

Finally, one important characteristic ofmuch (but not all) capital spending is thatits value declines over time. Buildings and

machines wear out. Patents and copyrightshave limited lives. Even the value of basiceducation and training may decline in aworld of continuing technological change,which requires many workers to upgradetheir skills constantly to maintain their earn-ings.

Accounting standards in the private sector,as well as the concepts reflected in theNational Income and Product Accounts, takeaccount of the declining value of capitalitems by requiring property and plant andequipment (but not land) to be ‘‘depreciated’’or ‘‘amortized’’ over their ‘‘useful lives.’’ Theannual amounts of depreciation or amortiza-tion represent expenses that, along with sala-ries, supplies, rent, taxes, and other expenseitems, are deducted from annual revenueto determine profits each year. 6 A numberof different methods for depreciation andamortization are in use, ranging from the‘‘straight-line’’ method (that computes the an-nual deduction simply by dividing the originalcapital investment by the years of usefullife) to various forms of ‘‘accelerated deprecia-tion’’ (that deduct more in the early yearsof an asset’s useful life and less in lateryears). Businesses may also use depreciationmethods for financial accounting purposesthat are different from those they use tocompute their income tax liability.

Some state and local governments accountfor the declining value of their debt-financedcapital assets by including in their annualbudgets the annual debt service on the bondsthey issued to finance the investments. Debtservice includes interest and the annualamount of the principal of the bond thatis paid off (similar to amortization of principalon a mortgage that individuals may takeout to finance their homes) or put intoa ‘‘sinking fund’’ that is eventually usedto pay off the bonds when they mature.The amortization component of the debt serv-ice charge is analogous to depreciation, butwith a time profile that is the oppositeof accelerated depreciation—much larger de-ductions in the later years than in theearlier years.

13

1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995

-10

-5

0

5

10

15

20

NET CAPITAL SPENDING ON PHYSICAL ASSETS

FIGURE 1

Federal Government

Private

State and Local

As a Percentage of GDP

TRENDS IN CAPITAL SPENDINGTwo important distinctions are useful to

keep in mind when considering trends incapital spending:

• The amount of capital spending in anygiven year is defined as ‘‘investment.’’ Thisis different from the total amount of theexisting capital ‘‘stock,’’ which is the cumu-lative total of all previous investmentminus cumulative depreciation.

• Investment, in turn, is often measured intwo ways: as either the ‘‘gross’’ amountof spending on capital items or the ‘‘net’’investment, which is the gross figureminus annual depreciation. Many analystsconcerned with the contribution of capitalto economic output pay more attention tothe net figures than the gross figures.

Figure 1 depicts trends in net spendingon physical assets alone, as a share ofGDP, by the private sector, state and localgovernments, and the federal government. 7

Since World War II, the shares of suchnet spending in GDP have been reasonablystable—more so in the public sector thanthe private sector—with private investmentsubstantially exceeding public investment.Meanwhile, within the government sector,since 1950 net investment at the state andlocal level has consistently outpaced federalspending. It is important to note, however,that about one-quarter of state and localinfrastructure spending is financed by federalgrants, and much of the rest has beensubsidized by the federal tax exemption onmunicipal and state debt.

14 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

-4

-2

0

2

4

6

8

RATE OF NONFARM PRODUCTIVITY GROWTH

FIGURE 2

Annual Percent Change

1948 1953 1958 1963 1968 1973 1978 1983 1988 19931997

Average(1948-1973)

Average(1974-1997)

One reason that public investment hasbeen of special interest to economists, busi-ness, and policy makers is its impact oneconomic output. In particular, some econo-mists have argued that the decline in thepublic investment-to-GDP ratio shown in Fig-ure 1 has contributed significantly to theslowdown in long-term growth from the firsthalf of the post-World War II era to thesecond. 8 As shown in Figure 2, althoughit has picked up in recent years, over thepast 25 years the annual rate of productivitygrowth in the United States, which determinesthe growth in average living standards, hasbeen substantially below that of the 1948–73period, which some have characterized asa ‘‘golden age.’’ Figure 3 suggests that theslowdowns in public spending and productivitygrowth have occurred more or less aroundthe same time.

The claim that the first slowdown (ininfrastructure spending) ‘‘caused’’ the otherone (in productivity growth) has proven tobe highly controversial, however. Among other

things, various economists have claimed thatthe causation runs the other way: that is,(1) public capital spending has slowed becauseeconomic growth has slowed; (2) the publiccapital buildup in the 1950s and 1960s waslargely associated with once-in-a-generationevents—the construction of the interstate high-way system and the construction of schoolsfor the baby boom generation—that couldnot have been expected to be repeated afterthey were completed; and (3) the statisticalestimates used to prove that the slowergrowth in capital spending caused the slow-down in productivity growth are highly sen-sitive to the time period examined. 9 Moreover,as already shown in Figure 1, public sectorinvestment in physical assets is considerablysmaller in magnitude than private sectorinvestment, which has also decreased relativeto GDP during the same period in whichpublic investment has declined. Both of thesefacts raise the question of whether andwhy public capital spending in particularshould be singled out as being primarily

15TRENDS IN CAPITAL SPENDING

1948 1952 1956 1960 1964 1968 1972 1976 1980 1984 1988 1992 1996

-2

0

2

4

6

8

10

Per

cent

age

of G

DP

-3

-2

-1

0

1

2

3

4

5

6

7

8

Ann

ual P

erce

nt C

hang

e

NONFARM PRODUCTIVITY GROWTH AND PUBLIC INVESTMENT

Nonfarm Productivity GrowthAnnual Percent Change

Net Public Capital Spending on Physical Assets as a Percentage of GDP

FIGURE 3

responsible for the trends in productivitygrowth.

There’s no need to resolve the debateover what has caused the slowdown in meas-ured productivity growth over the past 25years to conclude that all types of capital(fixed assets, human capital, and intangibles),whether owned by the private or publicsectors, remain important to economic growth.Economic theory has long pointed to thatconclusion. The challenge for decision-makersin both the private and public sectors isto undertake those investments that realisti-cally promise returns that exceed the costof financing the investments; otherwise, scarceresources will be wasted.

Some observers have attempted to drawpolicy implications for the United Statesby comparing the intensity of investmentactivity here (both public and private), aswell as rates of return on investment, withsimilar figures for other industrialized coun-tries. Such comparisons, however, do notprovide a standard for judging the appropriate-

ness of the amount of total investment inthis country, and still less for judging theamount of investment spending by the federalgovernment.

In any event, several points should bemade about those comparisons. First, thoughby conventional measurements the UnitedStates invests a smaller share of its GDPthan other advanced countries do, that isnot true (1) if investment is defined morebroadly to include expenditures on education,research and development, consumer durablesand defense capital, and (2) if the relativeprice of investment goods and other outputis correctly calculated [Kirova and Lipsey,1998]. Second, comparing investment/GDP ra-tios may not be as illuminating as comparingrates of return on capital. When this isdone, the United States typically comes outon top of other countries. Third, significantdifferences in definitions and demographicconditions make comparisons of public invest-ment particularly complicated across coun-tries. 10

17

BUDGETING CAPITALThe executive order directs the commission

to report specifically on capital budgetingpractices used in the private sector, by stateand local governments and in other countries,and then to explain the relevance of thosepractices for budget decisions made by thefederal government.

By definition, a budget is a constraintbecause it implies the existence of a finiteamount of resources that can be allocatedamong alternative uses. But what is it thatlimits the amount of available money? Thevastly different answers to this question forprivate firms, state and local governments,and the federal government help shed lighton the extent to which capital budgetingpractices followed elsewhere are suitable forthe federal budget.

Capital Budgeting in the Private Sector

The American economy is populated byover twenty million businesses, large andsmall, which surely have different ways ofbudgeting capital expenditures. Nonetheless,certain conventions have become standardizedthrough custom and repetition, as well asthrough formal professional practice. As aresult, it is possible to describe a stylizedprocess that many firms, typically largerpublicly held corporations, use to analyzetheir capital spending options, to choose amongthem, and then to account for those choices.To help understand these conventions, itis useful to refer to three basic financialstatements that are found in the annualreports of publicly held companies: the balancesheet, the income statement, and the state-ment of cash flows.

The balance sheet provides a financial snap-shot at a single point in time, usuallyat the end of a reporting year, of thefirm’s assets (on one side) and liabilitiesand net worth (on the other). The twosides add to the same total. Assets are‘‘financed,’’ as it were, by borrowing (liabilities)and shareholders’ contributions (paid-in capitaland retained earnings). Broadly speaking,three categories of assets are reported on

the balance sheet: short-term assets (suchas cash, marketable securities, receivables,and inventories), fixed assets (structures andequipment) minus any cumulative deprecia-tion, and intangible assets minus any cumu-lative amortization. Using the nomenclatureof this report, capital for private firms consistsof fixed assets and, under some definitions,intangible assets as well. 11 It is worth notingthat private sector accounting has been stand-ardized in Generally Accepted AccountingPrinciples (GAAP), which are used to preparefinancial statements. 12 The Financial Account-ing Standards Board, an independent bodyof experts, is responsible for seeing thatthe principles embodied in GAAP are main-tained, updated, and applied in a fair andreasonable manner. 13

The income statement is an accountingof revenues and expenses over a certaintime frame, typically a year, with the dif-ference representing the firm’s profit or loss.Because businesses exist to generate profits,spending decisions by private companies—including whether and how much to investin capital projects—are judged predominantlyby their likely impact on profitability. Invest-ments in capital projects by definition aredesigned to deliver benefits over the longrun, so capital spending does not appearon the income statement. Instead, the depre-ciation or amortization of existing capitalrecorded on the balance sheet shows upon the income statement as an expensethat reduces reported profits.

Where, then, might spending on capitalshow up? The typical place is on the statementof cash flows. This statement combines infor-mation on where a firm gets its moneyand where it spends it during the courseof a year: on operating activities, intereston any outstanding debt, and the full costof capital projects.

How do firms decide how much capitalspending to undertake, and of their manypossible options, which projects to pursue?

18 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

Here, again, practices surely vary. But certainfacts and conventions are widely understood.

First, most firms cannot spend withoutlimits: they are constrained by their cashon hand, revenue likely to be realized inthe short run, and how much additionalcash they might be able to raise by sellingexisting assets, borrowing, or selling newequity. 14 In turn, creditors and investorsdecide whether to provide funds, if theyare requested, and on what terms basedon the firm’s ability to repay its debts(in the case of borrowings) and generateprofits (in the case of equity sales). Inshort, firms in the private sector are subjectto market discipline.

Second, it is standard practice in privateindustry for firms to assess their capitalprojects by estimating their ‘‘net presentvalue.’’ Net present value (NPV) is calculatedby projecting the future cash flows the invest-ment is likely to generate (such as rentalsfrom a building or cost savings from investingin new equipment or machinery), ‘‘discounting’’the future cash flows by the ‘‘time valueof money,’’ taking appropriate account ofthe risk of investment, and then subtractingthe initial cost of the endeavor. Future cashflows are discounted because a dollar todayis worth more than a dollar to be receivedin two, three, or several years hence (sincethe dollar today can be invested in a financialinstrument and earn a rate of interest).

According to standard practice, it makeseconomic sense to undertake a capital projectonly if its NPV is positive (the discountedreturns are greater than the project’s cost),and even then a firm may decide not toproceed. 15 For example, if the discount rateis 10 percent, a project costing $1 millionbut projected to generate net revenues of$200,000 annually for ten years, would havea NPV of $229,000. But if annual net revenuesare projected to be only $100,000 over thesame time period, the project should notbe pursued because its NPV is a negative$386,000 (which doesn’t even cover theproject’s cost).

Passing the NPV test, however, does notmean that a project will be authorized. Afirm may have many potential projects thatlook promising when judged by their NPVs;

however, it might not pursue all of thembecause it may have strategic objectives thatcannot be readily quantified which limit therange of investments it can undertake. Thefirm may also be reluctant for other reasonsto seek outside financing (preferring to under-take only those projects that can be financedwith cash on hand), or to limit its borrowingor sale of equity.

Third, regardless of which of these ap-proaches (or others) private firms may employto decide how much capital investment toundertake and which projects to pursue,all of them ultimately measure the probablesuccess of the projects by a single metric—the likely effect on future financial perform-ance. Moreover, the process of evaluatingthese undertakings is different from thatof deciding whether to make certain expendi-tures for operating purposes (the expensesnecessary to keep the business running ona day-to-day basis). These decisions do notrequire long-run projections of impacts ordiscounting into the future, although tech-niques such as calculating NPVs are oftenused to decide whether to terminate existinglines of activity. Accordingly, operating budg-ets are often prepared and overseen in theprivate sector through a process that isseparate from the capital budget (althoughboth processes are often linked by an overallmanagement plan). 16

Finally, a firm’s decision to undertake oneor more capital projects is not necessarilylinked with a decision about how to financethose projects. Some firms, averse or unableto take on additional debt, may financeall, most, or part of their capital projectswith cash on hand; others may borrow;and still others may sell equity. But justbecause capital spending may require a sepa-rate decision and budget, it need not befinanced to any degree with additional debt.

Capital Budgeting by State and LocalGovernments

Just as there is no single capital budgetingpractice prevalent in the private sector, theapproach to capital budgets also varies amongstate and local governments. Nonetheless,some general tendencies are worth noting. 17

19BUDGETING CAPITAL

First, most state governments maintaina capital budget separate from the operatingbudget. However, states differ substantiallyin how they define capital, the degree towhich capital is separate in the governor’sproposed budget and in the legislature’s budg-et, and the means by which they financecapital expenditures. 18

Second, whether or not states budget capitalspending separately from other expenditures,most states have long-range capital plans,ranging from three to ten years, with fiveyears being the most frequent planning hori-zon. The spending figures in these planstend not to be as detailed as the figuresincluded in the annual budgets.

Third, available survey evidence indicatesthat the states most satisfied with theircapital budgeting process use some methodof keeping their legislatures regularly in-formed about capital needs. Some state legisla-tures also have a separate committee chargedwith overseeing all or most capital projectsand their financing.

Fourth, unlike the private sector, wheredifferent capital projects can be judged bythe common standard of impact on profit-ability, governments are responsible for avariety of functions, including police protec-tion, health care, and education, whose bene-fits generally cannot be reduced to dollarsand cents. This is a common situation sharedby all levels of government. Nonetheless,governments must set priorities in decidinghow to spend tax revenues and any borrowedfunds.

How do state governments set prioritiesin deciding on their capital expenditures?Although some do it project-by-project, orcase-by-case, most states have formal mecha-nisms, either in statute or by practice, forsetting priorities. Many states that take thisapproach set priorities on a functional basis,allocating expenditures for higher education,transportation, aiding local governments, orprotecting natural resources. Others have stat-utes that give priorities to certain activities,such as health and safety.

Fifth, contrary to popular belief, state gov-ernments do not always finance their capitalprojects by borrowing. To the contrary, states

often dip into general revenues to pay forcapital items, although the extent to whichthey are allowed or choose to do so varies.Other major sources of revenue for statecapital spending include excise taxes (suchas taxes on gasoline) or grants from thefederal government. In addition, while debtservice—interest and repayment of principal—typically shows up in state operating budgets,no state budget includes charges for deprecia-tion. 19 Many states impose user fees onintended beneficiaries of capital projects inorder to help service the debt issued tofinance them.

Finally, most states have either constitu-tional or statutory limits (often with referen-dum requirements) on the amount of debtthey may issue. State borrowing is alsodisciplined by the market. Rating agenciesdetermine the ratings they give to a state’sbonds, which strongly influence the interestrate at which those bonds can be marketed.These ratings are set in significant partby measuring the amount of state debt out-standing against the economic output gen-erated in the state. Higher interest ratesdue to adverse ratings can force states tolimit their borrowing.

As a broad generalization, local governmentsfollow procedures and conventions similarto those outlined for state governments.

Current Budgeting by the FederalGovernment

It may be surprising to some that through-out much of American history, the federalgovernment had no central budget. Untilthe Budget and Accounting Act of 1921,which created the Bureau of the Budget,each individual agency submitted a budgetto Congress. Since 1921, the Bureau of theBudget (now OMB) has coordinated the prepa-ration and submission of a Presidential budgetfor the entire executive branch. The Presidentis required to submit the budget for thecoming fiscal year by the first Monday inFebruary. This gives Congress eight monthsto enact the legislation that will continuethe operation of most government operationsand programs. If the necessary appropriationslaws have not been enacted by October 1,temporary ‘‘continuing resolutions’’ usually

20 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

provide funds until full-year appropriationsare enacted.

Although the Congress considers the Presi-dent’s budget proposals, it usually does notactually pass a law setting forth a budget(although, as discussed below, the ‘‘budgetresolution’’ passed by Congress establishesa framework for later Congressional consider-ation of different pieces of the budget). Instead,it enacts thirteen separate appropriations billsfor the approximately one-third of all federalspending that is deemed to be ‘‘discretionary.’’The thirteen appropriations bills are developedfor full Congressional consideration by thesame number of subcommittees of the Appro-priations Committees of each chamber.

The other two-thirds of the budget coversso-called ‘‘mandatory spending,’’ which ismainly for entitlement programs such asSocial Security, Medicare, Medicaid, and un-employment insurance. Mandatory spendingcontinues at levels regulated by standinglaws unless Congress enacts legislation tochange them (for example, by changing abenefit formula). The same is true of taxreceipts. Congress assigns responsibility forlegislation governing mandatory spending andreceipts to the authorizing (rather than appro-priations) committees.

Until the Congressional Budget Act of 1974,Congress had no procedures for coordinatinglegislation governing appropriations, manda-tory spending, and revenues into an overallfiscal policy. Instead, a fiscal policy simplyemerged as the sum of all of the enactedbills. The 1974 Act aimed at bringing moreorder to the budget process by creatingseparate budget committees in both the Houseand the Senate, and the Congressional BudgetOffice (the congressional counterpart to OMB),which provides information to Congress aboutthe costs and effects of legislation. In addition,the Act requires Congress first to decidewhat the projected budget surplus or deficitshould be and then to be guided by thatdecision in enacting spending and revenuebills.

More specifically, the 1974 Act calls forCongress to adopt each year a ‘‘budget resolu-tion’’ that sets a ceiling on total outlaysand a floor on total receipts. The resolution,which is not presented to the President

because it is technically not a law, alsoallocates ‘‘budget authority’’ and ‘‘outlays,’’by functional categories, to the appropriationscommittees (for discretionary spending) andthe authorizing committees (for mandatoryspending). The appropriations committees, inturn, further allocate budget authority amongtheir thirteen subcommittees, which mustreport bills back to the full committee consist-ent with those allocations. The resolutionmay also direct authorizing committees toachieve a specified amount of savings byreducing mandatory spending or increasingreceipts. Finally, the 1974 Act establishedparliamentary rules (‘‘super-majority’’ votingrequirements in the Senate) to stop billsthat violate the budget resolution.

The distinction between ‘‘budget authority’’and ‘‘outlays’’ is fundamental to understandingthe way budget decisions are actually made.Congress grants budget authority (BA), ena-bling agencies to incur obligations. Thoseobligations, in turn, require outlays (actualcash payments). Capital expenditures andoperating expenses typically have very dif-ferent ‘‘outlay rates.’’ Capital projects areoften completed over several years, so theoutlays for them are spread out over someperiod of time. In contrast, the outlays forsuch things as salaries of government workers,repairs, and maintenance, along with pay-ments under the various entitlement pro-grams, typically coincide with the amountof BA for the same year.

The Budget Enforcement Act of 1990 addedfurther requirements to the budget processfor fiscal years 1991–95. The BEA has beenextended twice so that its requirements nowapply (with amendments) through fiscal year2002:

• The BEA divided all discretionary spend-ing, of which capital spending is a part,into categories and imposed statutory lim-its or ‘‘caps’’ on each category (on bothBA and outlays). The categories changefrom year to year, but currently consistof defense, non-defense, violent crime re-duction, highways, and mass transit. Theseparate caps for defense and non-defenseare replaced after fiscal year 1999 by a‘‘discretionary spending’’ category, whilethe other categories remain intact. The

21BUDGETING CAPITAL

violent crime reduction category expiresafter fiscal year 2000, leaving the discre-tionary, highways, and mass transit cat-egories. Increases in taxes do not increasespending allowed by the caps (althoughthe BEA rules allow discretionary spend-ing to be offset by fees charged for goodsand services when the fees are authorizedin appropriations acts). The caps were in-tended to restrain the growth of spending,whether or not additional tax revenues formore spending could be found.

• The BEA contained ‘‘pay-as-you-go’’(PAYGO) provisions to ensure that the cu-mulative impact of changes in legislationaffecting mandatory spending or receiptsdo not increase the deficit. In other words,any increases in mandatory benefits mustbe financed either by cuts in other manda-tory spending or by increased revenue. Be-cause most capital expenditures are dis-cretionary, the PAYGO rules seldom applyto capital spending.

The federal budget contains several typesof funds. The ‘‘general fund’’ is the broadestand includes income and some excise taxreceipts. It also includes proceeds of generalborrowing, on the revenue side of the budget;on the expense side, it includes nationaldefense, interest on the federal debt, operatingexpenses of most federal agencies, and somecapital expenditures (broadly defined) on R&D,education, and infrastructure and other phys-ical capital spending. ‘‘Special funds’’ areearmarked for specific purposes; while theyare not designated by law as ‘‘trust funds,’’they do not differ from them in substance. 20

Most special funds are financed by userfees. ‘‘Trust funds’’ also have dedicated uses,and are financed by user fees or taxes;when their surpluses are borrowed, the fundsreceive interest. A few of the best-knowntrust funds are those for Social Security,Medicare, and highways (although there areabout 150 such trust funds in total). 21

Although each of the trust funds is tech-nically distinct, they are reported on a com-bined basis in a ‘‘unified budget,’’ a conceptadopted in January 1968 (for the FY 1969Budget). The unified budget provides thebottom-line impact of all federal spendingand taxing on the economy by indicating—

through the cash deficit or surplus—the im-pact on credit markets.

The unified budget also consolidates bothoperating and capital expenditures, whichmeans that the federal government does nothave a separate budget for capital expendi-tures. The receipts and outlays shown inthe unified budget are similar to a cashflow statement in the private sector, whichalso provides a comprehensive accounting ofincome and spending.

There have been several efforts since WorldWar II to address the question of whetherbudget procedures should be changed to pro-vide for separate consideration of capitaland operating expenditures. 22 For example,a capital budget was incorporated in theTaft-Radcliffe amendment to the EmploymentAct of 1945, which was passed by the Senatebut rejected in the House. The 1949 HooverCommission did not recommend a separatecapital budget, but it did suggest that thegovernment publish budget estimates for cur-rent operating expenditures and capital out-lays separately under each major functionor activity in the budget.

There were periodic attempts in Congressduring the subsequent two decades to adopta capital budget, but these were often opposedby the executive branch and never resultedin legislation. The capital budget was firmlyrejected in 1967 by the President’s Commissionon Budget Concepts, as it was in previousstudies by the American Institute of CertifiedPublic Accountants and the U.S. Chamberof Commerce. Interest in the idea returnedin the 1980s with the apparent approvalof Comptroller General Charles Bowsher andthe suggestion by President Reagan in 1986that the idea be studied. Interest in capitalbudgeting surfaced again during Congressionaldeliberations in 1995–96 over the proposedBalanced Budget Amendment (BBA) to theConstitution. Some of the proponents of theBBA wanted the amendment applied onlyto operating expenses of the federal govern-ment, excluding some defined capital thatcould be financed by government debt.

The federal budget process today continuesto budget operating and capital expenditurestogether. 23 During the course of its delibera-tions, the commission heard several expla-

22 REPORT OF THE PRESIDENT’S COMMISSION TO STUDY CAPITAL BUDGETING

nations of why this is the case (althoughnot all commissioners agree with each ofthem).

First, for reasons already discussed, federalpolicy makers have not been able to agreeon a single definition of capital or investmentin the public sector. While a technical analysisthat accompanies the budget (today it isknown as Analytical Perspectives) has useda stable definition of investment for manyyears, the use of the term investment inthe budget to describe policy proposals haschanged with the political priorities of dif-ferent administrations. 24 Given the changingpriorities of the Congress and different admin-istrations through time, it is not surprisingthat no single definition of public capitalhas emerged.

Second, capital is one of a number ofinputs (along with materials and labor) thatthe federal government uses to deliver itsservices (directly or through state and locallevels of government) to the public. Thepublic, in turn, judges the government notby the inputs it uses, but by the amountand perceived quality of the output it delivers.On this view, budget decisions should focuson the goals to be achieved (such as providingeducation or securing the national defense),and not on the mix between capital andother inputs judged necessary to achievethem.