renewable energy project financing: strategies for the deal

TRANSCRIPT

Presenting a live 90‐minute webinar with interactive Q&A

Renewable Energy Project Financing: Legal Strategies for Structuring the Deal

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, AUGUST 15, 2013

Today’s faculty features:

Edward W. Zaelke, Partner, Akin Gump Strauss Hauer & Feld, Los Angeles

Lloyd J. MacNeil, Partner, Akin Gump Strauss Hauer & Feld, Los Angeles

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-755-4350 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your locationattendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your participation by completing and submitting an Official Record of Attendance (CLE Form).

You may obtain your CLE form by going to the program page and selecting the appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For additional information about CLE credit processing, go to our website or call us at 1-800-926-7926 ext. 35.

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Renewable Energy – Project Financing: Legal Strategies for Structuring the DealStrategies for Structuring the DealPresented by: Edward Zaelke & Lloyd MacNeil

Strafford CLE WebinarAugust 15, 2013

© 2013 Akin Gump Strauss Hauer & Feld LLP

Introduction: Who are Ed Zaelke & Lloyd MacNeil?Introduction: Who are Ed Zaelke & Lloyd MacNeil?

Ed Zaelke is:● Co-chair, Akin Gump’s Global Project Finance Practice ● Named as one of California’s Top 100 Lawyers by The Daily Journal● Recognized by Chambers and Partners and numerous other publications for his

leading role in the renewables industryleading role in the renewables industry

Lloyd MacNeil is:● Partner, global project finance practice

Aki G t 125 li t i th blAkin Gump represents over 125 clients in the renewable energy sector including: Exelon, BrightSource, SunPower, First Wind, Terra-Gen Power, EverPower.

6

Today’s TalkToday s Talk

1. Why Are We Investing in Renewable Energy? 2 What Are Its Long-Term Prospects?2. What Are Its Long-Term Prospects?3. What Are the Key Legal and Business Elements of a Renewable Energy Deal?

7

Why Are We Investing in Renewable Energy?Why Are We Investing in Renewable Energy?

■ It’s good for the country (and the planet) I id i j b i i■ It provides energy security, job opportunities

■ It’s mainstream■ It’s growing■ It s growing■ It’s increasingly affordable

8

Good for the Country (and the planet)Good for the Country (and the planet)

In the U.S., over 40% of the Greenhouse-causing CO2 emissions come from the production of electricity:

Electricity Production 41%Production 41%

Transportation 33%

Industrial 15%

Residential 7%

Commercial 4%

9

U.S. CO2 Emissions Source: U.S. Environmental Protection Agency

March 2013

Good for the Country (and the planet)Good for the Country (and the planet)

And we produce electricity primarily from burning fossil fuels:p y p y g

Coal 42%

Natural Gas 25%

Nuclear 19%Nuclear 19%

Renewable Energy 13%13%

Other 1%

10

Source: US Energy Information Administration, Monthly Energy Review, March 2013

Renewable Energy has Entered the MainstreamRenewable Energy has Entered the Mainstream

11

The U S Wind Power MarketThe U.S. Wind Power Market

Nearly 1,300 MW of wind energy projects under construction at the end of the second quarter of 2013, with over 900 MW of new wind e d o t e seco d qua te o 0 3, t o e 900 o e dcapacity starting construction during the second quarter alone.

13,124 megawatts (MW) of electric generating capacity installed in 2012, leveraging $25 billion in private investment, and achieving over 0 , e e ag g $ 5 b o p a e es e , a d ac e g o e60,000 MW of cumulative wind capacity.

The U.S. wind industry has added over 35% of all new generating capacity over the past 5 years.p y p 5 y

Today, U.S. wind power capacity represents more than 20% of the world's installed wind power.

* S A i Wi d E

12

* Source: American Wind Energy Association (AWEA) 2012 Year End Report and AWEA Q2 2013 Market Update Report

U S has Ample Wind Resource to Meet DemandU.S. has Ample Wind Resource to Meet Demand

An All American R k St tR k St t

United States Wind Power Capacity (MW)

An All American Resource

Rank123

State

North DakotaTexasKansas

Rank123

State

North DakotaTexasKansas3

4567

KansasSouth DakotaMontanaNebraskaWyoming

34567

KansasSouth DakotaMontanaNebraskaWyoming7

89

1011

WyomingOklahomaMinnesotaIowaColorado

789

1011

WyomingOklahomaMinnesotaIowaColorado11

12131415

ColoradoNew MexicoIdahoMichiganNew York

1112131415

ColoradoNew MexicoIdahoMichiganNew YorkG ’ O L d P i l GW

~

13

151617

New YorkIllinoisCalifornia

151617

New YorkIllinoisCalifornia

Germany’ s On-Land Potential ˜ 100 GWNorth Dakota’ s Potential > 400 GW

The U S Solar Power MarketThe U.S. Solar Power Market

14

The U S Solar MarketThe U.S. Solar Market

The U.S. leads globally with the largest number of solar installations.The U S installed 723 megawatts (MW) of solar energy in Q1 2013The U.S. installed 723 megawatts (MW) of solar energy in Q1 2013,

which accounted for over 48 percent of all new electric capacity installed in the U.S. last quarter. Overall, these installations represent the best first quarter of any given year for the industry.s qua e o a y g e yea o e dus y

3,300 MW of solar capacity installed in 2012. The U.S. now has over 7,700 MW of installed solar electric capacity, enough to power more than 1.2 million average American households.g

The utility scale and commercial segments drove the U.S. market in 2012, with 1,800 MW and 1,000 MW respectively, of installed capacity. Eleven states had 50 MW or more of utility-scale installations.y

Residential Solar is poised for explosive growth. The average price of a solar panel has declined by 60% since 2011.Top states for solar energy generation are California, Arizona, New

Jersey, and Nevada. 15* Source: Solar Energy Industry Association

The U.S. Geothermal Market

Geothermal power generates electricity from heat stored in the earthfrom heat stored in the earth.

Twenty-seven plants came online between 2006 and 2012 in seven Western states, bringing the total installed capacity in the U.S. to 3.38 GW.

Today, geothermal power plants are currently online in eight states: Alaskacurrently online in eight states: Alaska, California, Hawaii, Idaho, Nevada, Oregon, Utah, and Wyoming.

Additionally, 175 geothermal projects y, g p jare currently in development, which could add ≈2,500 MW to U.S. installed capacity in the next decade or so.

* Source: Geothermal Energy Association May 2013

16

What is Driving the Growth?What is Driving the Growth?

The demand for electricity continues to increaseGlobal energy demand projected to grow at 2.7% per annumU.S. demand growth has been flat since financial crash/recession

17

What is Driving the Growth?What is Driving the Growth?

Environmental and other domestic concerns are driving public policyp yGovernment support is active due to public concern over

climate change and job growth.Renewable power is a viable part of national energy policy as aRenewable power is a viable part of national energy policy as a

hedge against fossil fuel price volatility and contribution to energy diversity.

The federal government adopted subsidies and tax benefits toThe federal government adopted subsidies and tax benefits to incent the development of renewable energy resources.

Several state governments adopted renewable energy portfolio standards.standards.

But, historically low natural gas prices are impacting policy choices.

18

What is Driving the Growth?What is Driving the Growth?

Tax incentives 60% - 65% of the cost of renewable energy projects is “paid” by tax incentives 60% - 65% of the cost of renewable energy projects is paid by tax incentives Financial and legal engineering is essential to extract or monetize the tax

incentives● PTC (Production Tax Credit)● PTC (Production Tax Credit)

- 10 year credit period- $23 per MWh- Available for wind and geothermal but not solar- Projects must “begin construction” prior to December 31, 2013Projects must begin construction prior to December 31, 2013

● ITC (Investment Tax Credit)- One-time tax credit of 30% of eligible cost basis - Historically available for solar; recently available for PTC eligible technologies (ARRA)

MACRS (M difi d A l t d C t R S t )● MACRS (Modified Accelerated Cost-Recovery System)- Established 5 year class life for depreciation of eligible costs for wind, solar and geothermal

● Bonus Depreciation - 50% first-year bonus depreciation for projects placed in service before January 1, 2014

19

What is Driving the Growth?What is Driving the Growth? State RPS Programs - As of January 2013, 30 States and the District of Columbia have enforceable RPS or other mandated renewable capacity

li ipolicies.

20

* Source: U.S. Energy Information Administration

Key Elements of a Renewable Energy Transaction

21

Key Elements of a Renewable Energy TransactionKey Elements of a Renewable Energy Transaction

Renewable energy transactions involve elements common to most other transactionselements common to most other transactions

that involve the conversion of natural resources to commercial uses.

22

Bringing Natural Resources to MarketBringing Natural Resources to Market

Capital

A Market in which To Sell the Resource

Capital

A Method of Conversion to Final Product

Transportation to Market

A Method of Extraction or Capture

A Method of Conversion to Final Product

Ownership of Resource

Government Permission to Extract or Capture Resource

23

Ownership of Resource

Land Control

Local Permits/Compliance with Federal & State Environmental Laws

Renewable Energy Technology

Plant Construction

Transmission

Power Sales

Finance and Monetization of Tax Incentives

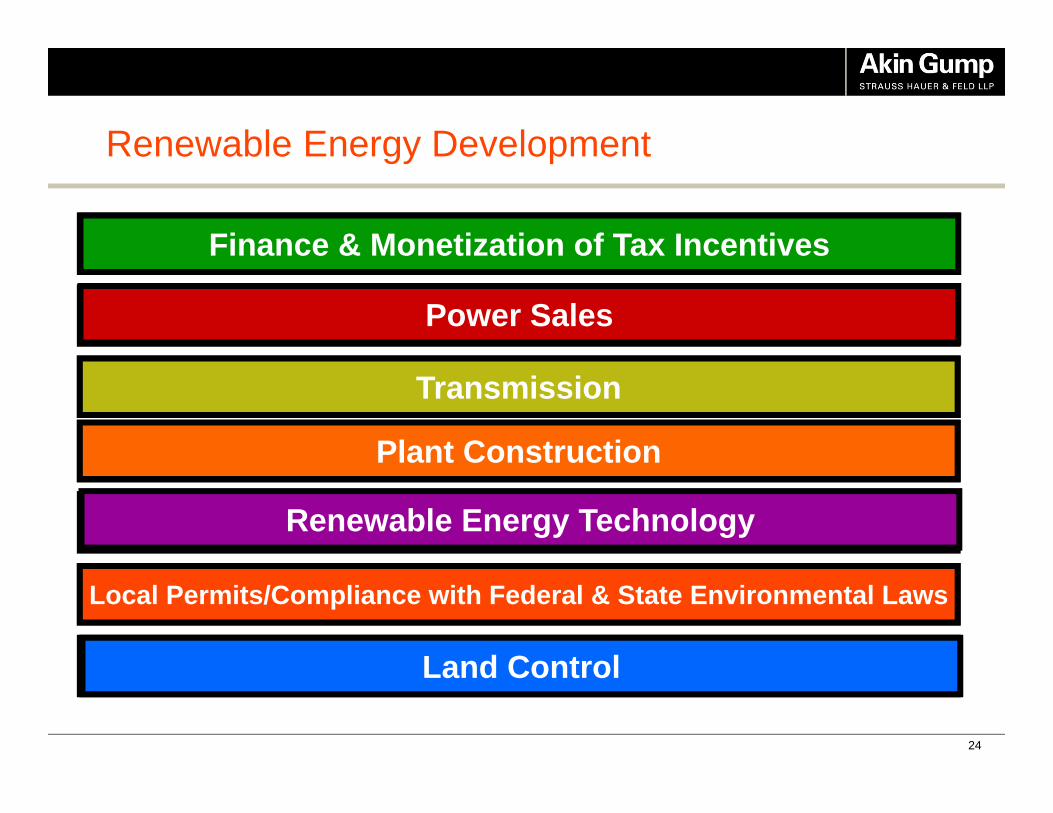

Renewable Energy Development

24

Land Control

Renewable Energy Technology

Plant Construction

Transmission

Power Sales

Finance & Monetization of Tax Incentives

Local Permits/Compliance with Federal & State Environmental Laws

Legal StrategiesLegal Strategies

Land Control

Purchasing Options, Leases, Easements and Rights of Way● Private Land

Land Control

● BLM Land● Tribal Lands● Forest Services Lands and other federal land● State Land● Seabeds

25

Legal StrategiesLegal Strategies

Land Control (Cont’d)

Land Control● Can be in the form of easements or leases● Easements in gross not allowed in all states● Term must match/exceed financing term

Recurring IssuesRecurring Issues● Set backs● Access rights● Liens on the fee interest● Liens on the fee interest

26

Legal StrategiesLegal Strategies

Local Permits/Compliance with Federal & State Environmental Laws

Public PolicyLand Use (State and Local)

Local Permits/Compliance with Federal & State Environmental Laws

Land Use (State and Local)Neighbor Issues● View, Noise, Radar Interference

FAA/Milit O flFAA/Military OverflyAvian IssuesEndangered SpeciesScenic Issues

27

Legal StrategiesLegal Strategies

Renewable Energy Technology

Patents, Intellectual Property, Manufacturing and Commercial Transactions

Renewable Energy Technology

a sac o s● Development vs. Commercialization● Clean Tech ● Equipment Supply Agreements● Equipment Supply Agreements

- Delivery Obligations - Warranties

28

Legal StrategiesLegal Strategies

Renewable Energy Technology (Cont’d) Technology Issues ● “Proven” technology (‘100 turbine’ rule for wind)

Renewable Energy Technology (Cont d)

● Supportable by IE report● Creditworthy warranty

- Often backstopped by L/C or other securityConcern over bankruptcy of panel manufacturers- Concern over bankruptcy of panel manufacturers

● Warranty terms shortening for wind- Warranty covers defects, availability, power curve, sound, IP

● Micrositing and ambient conditions can be criticalMicrositing and ambient conditions can be critical ● Federal export/import duties ● Deliverability

- Timing of deliveries - Liquidated damages- Security deposits

29

Legal StrategiesLegal Strategies

Plant ConstructionEPC Contracts vs. Construction Contracts● Cost of EPC Wraps

Ti i f l ti● Timing of completion● Cost overrun guaranties ● Creditworthiness of EPC or BOP Contractor● Retainage L/Cs and performance bonds● Retainage, L/Cs and performance bonds

Operation and Maintenance Contracts● OEM provided vs. third party provided● Term and Price● Term and Price● Cost should be supported by IE report● Guaranties and warranties

30

Legal StrategiesLegal Strategies

Transmission

Interconnection and Transmission RightsT i i U d C t t

Transmission

Transmission Upgrade ContractsTiming IssuesCostCostFirst in Time vs. ClustersPrivate Transmission OpportunitiesShared Facilities - Tenancies in Common

31

Legal StrategiesLegal Strategies

Power SalesOfftake/Hedging Contracts (Electricity, RECs)● Term (financing term is usually 1-2 years shorter than PPA term, at best)

C dit th t t i ti l f f bl fi t● Creditworthy counterparty is essential for favorable finance terms● Default triggers

- Project performance based covenants and milestones should trigger LDs, not termination

● Allocation of transmission constraint/curtailment risk- Economic curtailment problematic

● “As-available” delivery vs. fully contracted deliverability● Pricing fixed or escalating ● RECs retained or sold● May need to address intercreditor issues (debt, tax equity)● Merchant projects far less attractive for finance parties

32

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)Current Renewable Energy Financing Market Who is lending?

( )

● European Banks● Life Insurance Companies● Some U.S. Banks● Private Equity ● Debt is readily available for quality projects

Continued Emphasis on “Quality” Projects● Brand-name sponsors● Proven technology● Creditworthy, well-structured offtakers

C ti fi i d l ti● Conservative financing model assumptions

33

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)Tax Equity Market● Market continues to grow for ITC/PTC deals

M tl i i fi i l i tit ti d fit bl i f th il

( )

● Mostly insurance companies, financial institutions and profitable companies from the oil, technology and utility sectors (22 players according to last JP Morgan count)

● Returns beginning to soften

34

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)Typical Project Finance Structure for Renewable Energy in the U.S.

Tax Equity DebtProject Equity

• Direct equity

• Project developer

• Private equity investor

•Sale–leaseback

• Partnership flip

• Construction Loan

• Term Loan

• Bridge LoanPrivate equity investor

Project Company (Borrower)

• Mezzanine, etc.

PPA EPCSupply Contract and Warranties

O&M Agreement

Utility/Offtaker Contractor Equipment S l

Service P id

35

Utility/Offtaker Contractor Supply Provider

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)Typical Project Finance Structure ● Project company borrower – SPV or holding company of multiple SPVs (LLC or LP)

■ Sometimes bankruptcy remote (investment grade projects)

( )

■ Sometimes bankruptcy remote (investment grade projects)

Limited or no recourse to sponsor● Exception: tax liability (i.e. recapture)

Security for Lenders● All assets of project company (including contract rights)● Pledge of ownership interests in project company

Disbursement Waterfall ● All revenues of project company collected in collateral account and disbursed in

specified order of priority: expenses, debt, equity

36

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)

Tax Equity Investors Project Developer

Typical Partnership Flip-Structure

Tax Equity Investors Project Developer

Revenue: 99% Pre-Flip; Capital

Development

Revenue: 1% Pre Flip;

ITC, PTC, Depreciation, MACRS: 99%

99% Pre-Flip; 5% Post-Flip

Revenue: 1% Pre-Flip;95% Post-Flip

Project Utility/OfftakerPPA

Electricity

37

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)Tax Equity Structure: Flip Partnership● Tax investor can use ITC or PTC

T i t i i t t t ft t t

( )

● Tax investor sizes investment to an after-tax return● If choosing ITC, tax investor must be in partnership before asset placed-in-service● Once tax investor return achieved, 95% of benefits “flip” back to sponsor● Sponsor generally has post-flip purchase option● Sponsor generally has post flip purchase option● Recapture on change in control or cessation/change of operations

Tax Investor Receives Tax Benefits and Cash (99%)● Sponsor typically receives initial cash until return of capital● Sponsor typically receives initial cash until return of capital ● Tax basis reduced by 50% of ITC, if used

38

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)

Project Developer

Typical Sale-Leaseback Structure

Sale and leaseback

DevelopmentRent

Tax LessorUtility/Offtaker Project

Collateral

Equipment Sale

PTC, ITC, Bonus

PPA

ElectricityPTC, ITC, Bonus Depreciation, MACRS

39

Legal StrategiesLegal Strategies

Finance and Monetization of Tax Incentives (cont’d)Tax Equity Structure: ITC Sale-Leaseback Structure (no PTCs)● Tax investor (lessor)/sponsor(lessee)

T b fit tili d ffi i tl b t l id l/ h ti i

( )

● Tax benefits utilized more efficiently, but larger residual/purchase option price■ Can be effected up to 3 months after placed-in-service■ Sponsor retains upside during lease term ■ ITC based upon FMV (instead of sponsor cost)

Traditional “true lease” rules apply● Maximum lease term not to exceed 80% of useful life● Maximum PV of rentals not to exceed 90% of FMV● Minimum residual of 20%● Residual and early buy-outs at actual or projected FMV

40

Case StudyCase Study

3,000 MW wind project in California● 20 Landowners (private and public)● 20 Landowners (private and public)● Permits required from one county and federal government

- Legal Challenges E i t l C- Environmental Concerns

● Wind turbines provided by General Electric and Vestas● Construction includes shared facilities with adjacent wind farms● California Transmission Market● Power Sales to Utilities in California● $6 billion financing in multiple phases● $6 billion financing in multiple phases■ First phase ($400 million) involved 8 banks and tax equity investors■ Phases II-V ($1.2 Billion) involved 10 banks and tax equity investors

and a capital markets issuep

41

Edward W Zaelke Partner Los AngelesEdward W. Zaelke, Partner, Los Angeles

Edward Zaelke co-chairs Akin Gump’s global project finance practice. Mr. Zaelke focuses his practice on project development and finance, with a particular emphasis on representing companies engaged in the development, financing and operation of wind power, solar power and other alternative energy projects. His clients include many of the top renewable energy developers and investors in the United States.

Practice & BackgroundMr Zaelke’s experience extends to all elements of alternative energy development andMr. Zaelke s experience extends to all elements of alternative energy development and finance, including equity and debt financing, merger and acquisition transactions, equipment purchase and sale agreements, power purchase agreements, siting and other real property issues, governmental approvals and construction and EPC contracts.

Mr. Zaelke is the former president of the American Wind Energy Association (AWEA) and

Co-chair, Global Project [email protected] p gy ( )

has been a board member of AWEA since 2002. He is also a founding board member of the American Wind Energy Foundation and the chair of the AWEA Conference and Education Committee. He has been named as one of California’s Top 100 Lawyers for each of the past 3 consecutive years by the San Francisco and Los Angeles Daily Journal, and is recognized by Chambers and Partners and numerous other publications for his leading role in the

Areas of Practice:•Global Project Finance•Corporate•Climate Change•Energy

renewables industry.gy

•Mergers and Acquisitions•Real Estate and Finance

EducationJ.D. University of California at Los Angeles School of

42

at Los Angeles School of Law, 1983B.S. California State University Long Beach, 1980

Lloyd J MacNeil Partner Los AngelesLloyd J. MacNeil, Partner, Los Angeles

Lloyd J. MacNeil is a member of the firm’s global project finance practice, focusing on project development, project financing and mergers and acquisitions in the energy and infrastructure sector, with a particular emphasis on renewable energy.

Practice & BackgroundMr. MacNeil has worked for developers, sponsors, lenders and investors on a variety of renewable and nonrenewable energy project developments, financings and acquisitions.He is a frequent speaker at industry conferences and contributor to renewable energyHe is a frequent speaker at industry conferences and contributor to renewable energy publications. Prior to joining Akin Gump, Mr. MacNeil was a partner at another large, international law firm.Partner, Global Project

Areas of Practice:•Global Project Finance•Corporate•Climate Change•Energygy•Mergers and Acquisitions

EducationJ.D. Dalhousie University School of Law 1994

43

School of Law, 1994B.S. Dalhousie University, 1990