renewable energy markets and the clean power plan (part...

TRANSCRIPT

Renewable Energy Markets and the

Clean Power Plan (Part I)

Thomas Vitolo, Synapse

David Wooley, Keyes, Fox & Wiedman

Ed Holt, Ed Holt & Associates

The Influence of Clean Power Plan Compliance Pathway Choice on Renewable Energy Construction

Renewable Energy Markets 2016

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved.

October 17, 2016

Dr. Thomas Vitolo

@TommyVitolo

3

Synapse Energy Economics

• Founded in 1996 by CEO Bruce Biewald

• Leader for public interest and government clients in providing rigorous analysis of the electric power sector

• Staff of 30 includes experts in energy and environmental economics and environmental compliance

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

The Clean Power Plan(abridged)

Clean Power Plan and Section 111(d)

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. 5

Who? Applies to existing fossil fuel-fired generators that were in operation or under construction by January 8, 2014 and that meet certain size and production requirements

What? Covered units must reduce emissions of carbon dioxide (CO2) by the amount determined by EPA to reflect the Best System of Emission Reductions (BSER) for the source category

When? Compliance targets must be met on average over an 8-year interim compliance period as well as in the final compliance year: 2030

Where? Applies to units in 47 states and several Tribal lands (Vermont and Washington D.C. have no covered units; Hawaii, Alaska, Puerto Rico, and Guam will be brought into the program when more data is available on the units in those states/territories)

Why? To reduce emissions of CO2 from the electricity sector in order to reduce the contribution to global climate change

Tommy Vitolo

6

Timeline for Compliance

• First date for compliance pushed back from 2020 to 2022

• Two additional years to complete final State Plans

• States still expected to demonstrate progress during an interim period

through 2029 and must meet the final compliance targets by 2030

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

EPA may extended

EPA holding these dates firm

CPP Compliance Options(abridged)

Two Forms of Compliance

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. 8

Rate-based

Compliance is determined on a pounds per megawatt hour basis at the unit level or on a state-wide weighted average basis

Mass-based

Compliance is determined on a total tons of CO2 emitted basis (EPA has done the translation from rate to mass for each state)

Tommy Vitolo

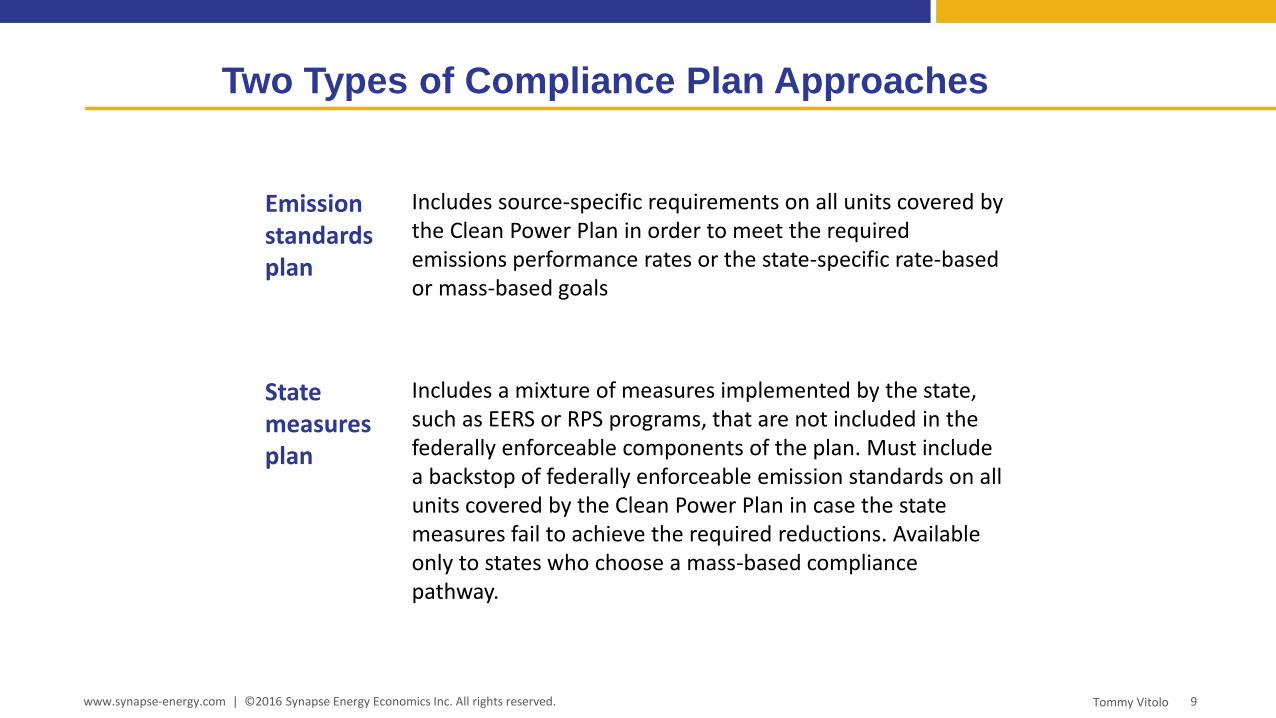

Two Types of Compliance Plan Approaches

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. 9

Emission standards plan

Includes source-specific requirements on all units covered by the Clean Power Plan in order to meet the required emissions performance rates or the state-specific rate-based or mass-based goals

Statemeasures plan

Includes a mixture of measures implemented by the state, such as EERS or RPS programs, that are not included in the federally enforceable components of the plan. Must include a backstop of federally enforceable emission standards on all units covered by the Clean Power Plan in case the state measures fail to achieve the required reductions. Available only to states who choose a mass-based compliance pathway.

Tommy Vitolo

Mo

del

Ru

les

10

Potential Compliance Pathways

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

11

Emission Trading for Compliance

• Emissions trading is a long-established mechanism for complying with environmental regulations

• Acid Rain program, Regional Haze, NOx Budget Trading program, CSAPR, CAIR, RGGI in the Northeast, AB 32 in California

• EPA provides a “panoply” of tools to facilitate the use of emissions trading programs in the Clean Power Plan

• Both of EPA’s proposed model rules (rate and mass) include emission budget trading programs

• Trading options limited by compliance pathway

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

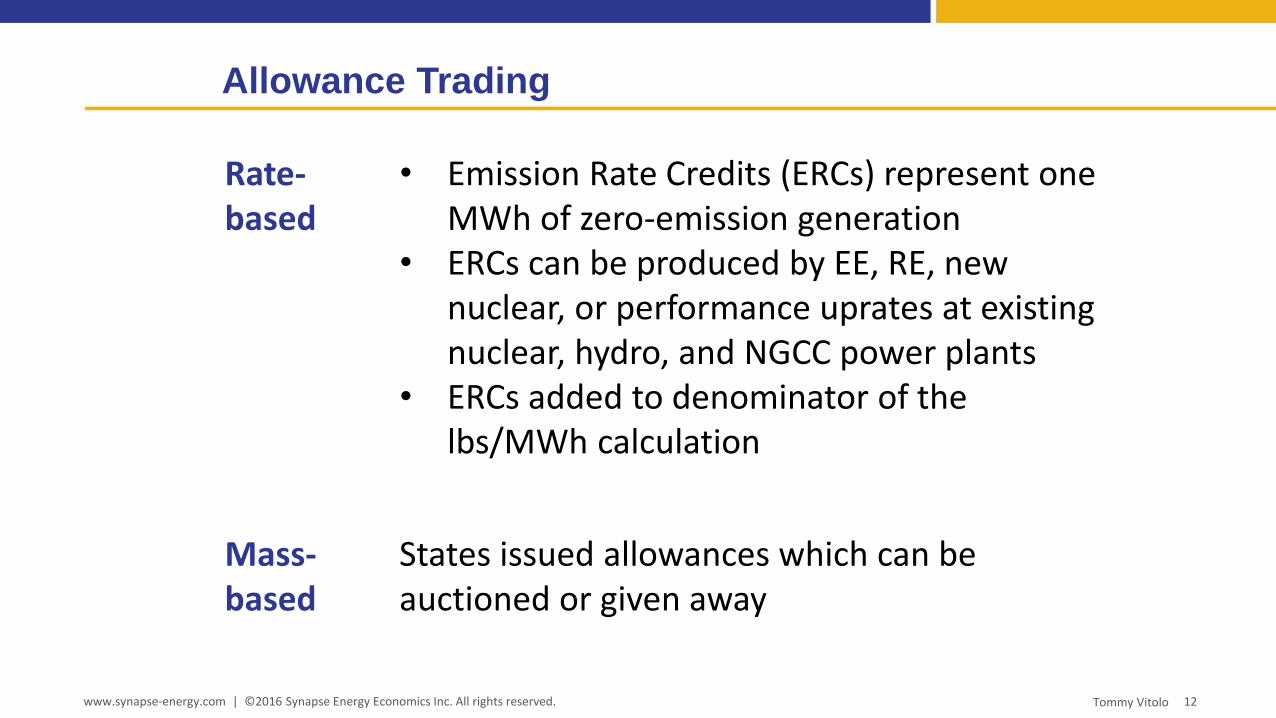

Allowance Trading

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. 12

Rate-based

• Emission Rate Credits (ERCs) represent one MWh of zero-emission generation

• ERCs can be produced by EE, RE, new nuclear, or performance uprates at existing nuclear, hydro, and NGCC power plants

• ERCs added to denominator of the lbs/MWh calculation

Mass-based

States issued allowances which can be auctioned or given away

Tommy Vitolo

13

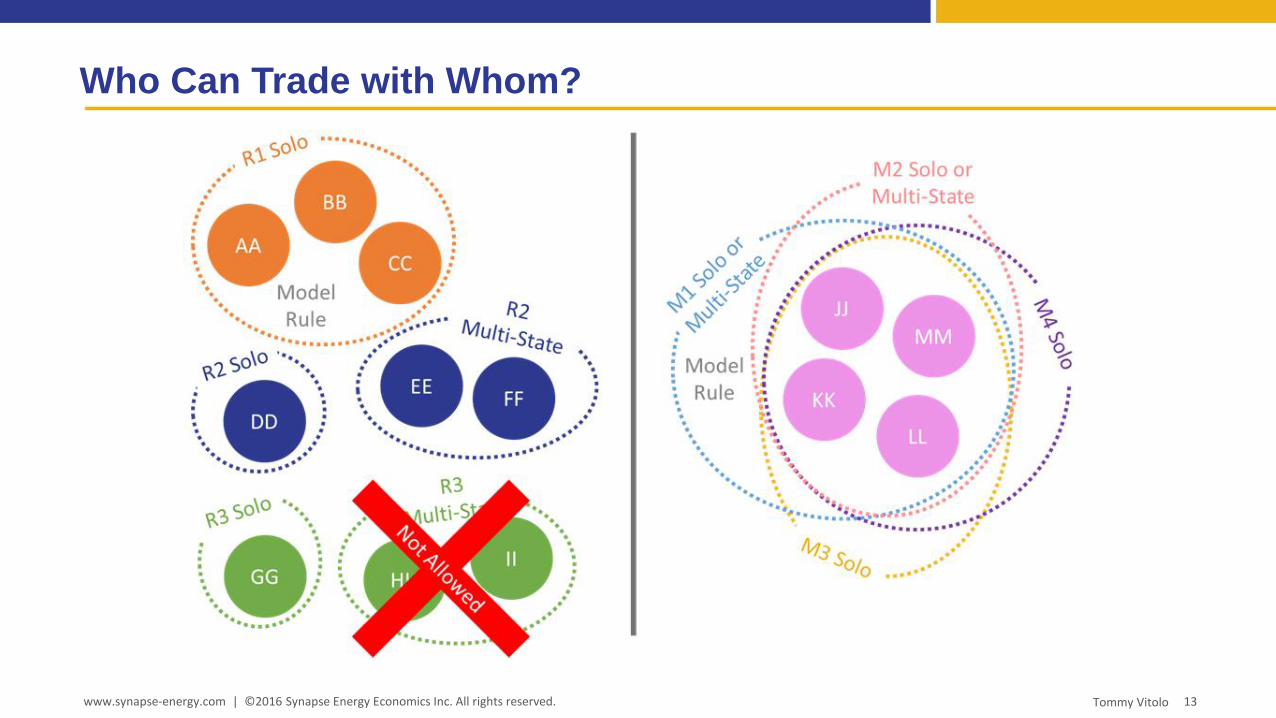

Who Can Trade with Whom?

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

CPP Compliance Pathway Implications on RE Construction

15

USA Wind and Solar w/ & w/out CPP

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

0

100

200

300

400

500

600

700

800

900

2016 2018 2020 2022 2024 2026 2028 2030 2032 2034 2036 2038 2040

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

AEO 2016 Reference

AEO 2016 No CPP

16

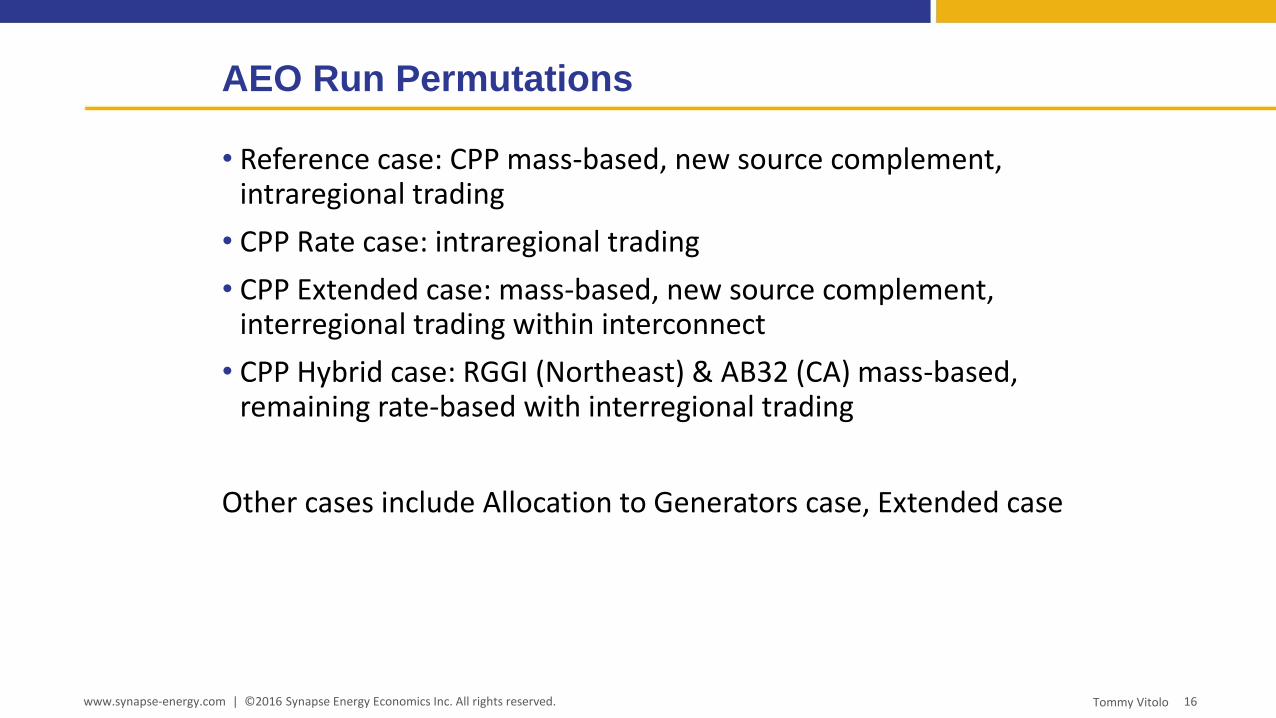

• Reference case: CPP mass-based, new source complement, intraregional trading

• CPP Rate case: intraregional trading

• CPP Extended case: mass-based, new source complement, interregional trading within interconnect

• CPP Hybrid case: RGGI (Northeast) & AB32 (CA) mass-based, remaining rate-based with interregional trading

Other cases include Allocation to Generators case, Extended case

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

AEO Run Permutations

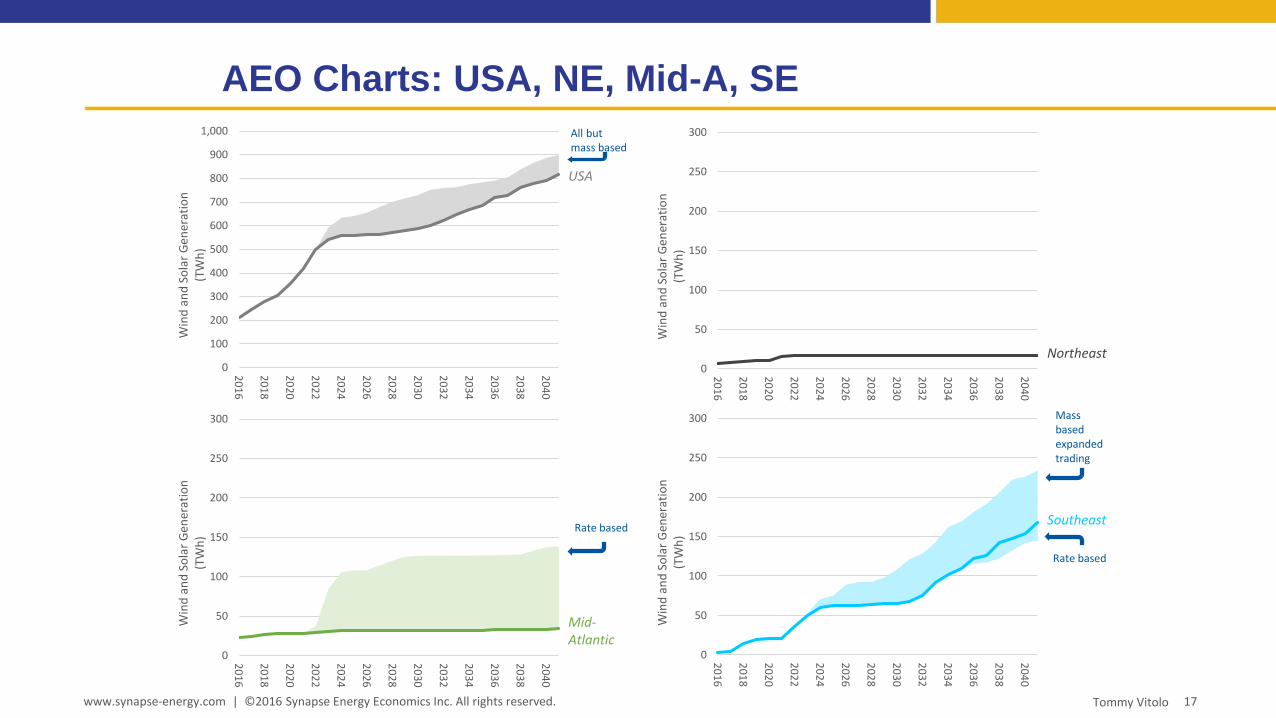

17www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

AEO Charts: USA, NE, Mid-A, SE

0

100

200

300

400

500

600

700

800

900

1,000

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

USA

All but mass based

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

Northeast

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

Mid-Atlantic

Rate based

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

Southeast

Mass based expanded trading

Rate based

18www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

AEO Charts: West, Upper MW, TX, Lower MW

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

Upper Midwest

Rate based

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

West

Rate based

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

Lower Midwest

0

50

100

150

200

250

300

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

20

40

Win

d a

nd

So

lar

Gen

erat

ion

(T

Wh

)

Texas

19

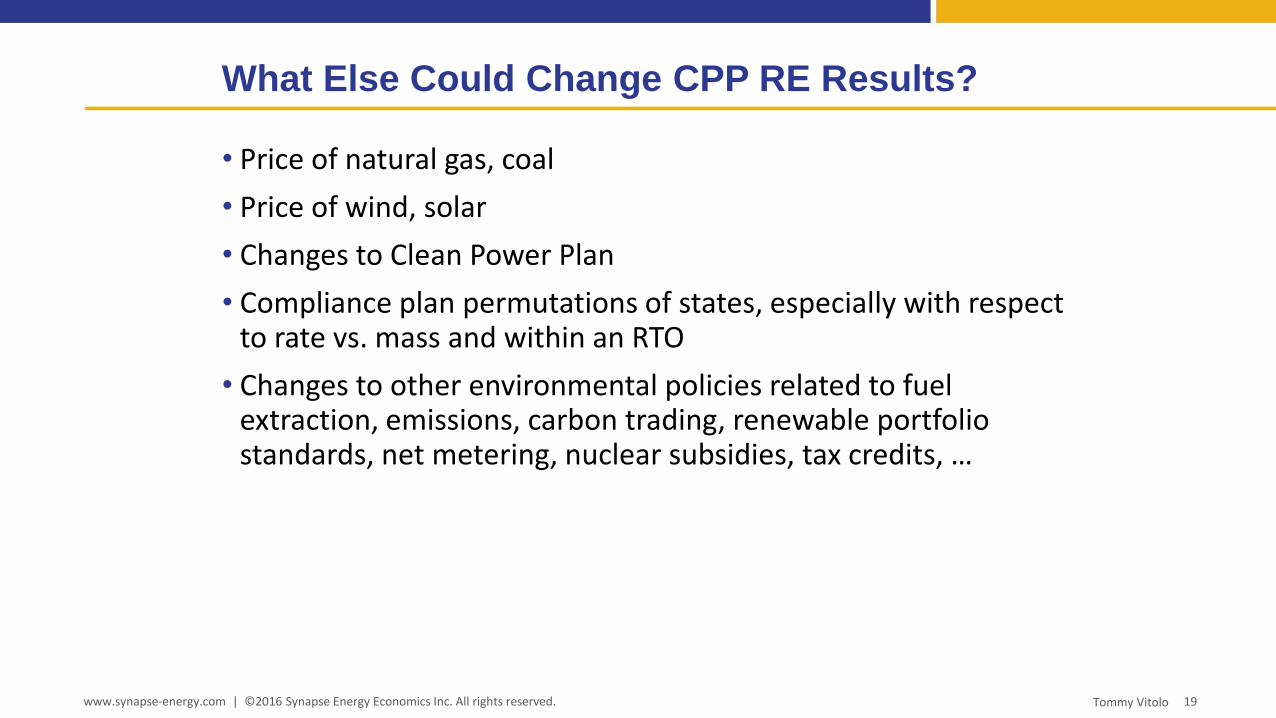

• Price of natural gas, coal

• Price of wind, solar

• Changes to Clean Power Plan

• Compliance plan permutations of states, especially with respect to rate vs. mass and within an RTO

• Changes to other environmental policies related to fuel extraction, emissions, carbon trading, renewable portfolio standards, net metering, nuclear subsidies, tax credits, …

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

What Else Could Change CPP RE Results?

Let’s talk.

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. 20Tommy Vitolo

Dr. Tommy Vitolo

617.453.7036

@TommyVitolo

21

Related Media

• Jackson, S., Santen, N., and Biewald, B. “Overview of the Final Clean Power Plan.” For the National

Association of State Utility Consumer Advocates. August 25, 2015.

• Jackson, S. “Overview of the Clean Power Plan.” 2015 Clean Power Plan Summit of Southeastern

Advocates. September 23, 2015. http://www.synapse-energy.com/sites/default/files/Overview-

of-CPP-for-Southeast-Advocates.pdf

• Energy Information Administration. “Annual Energy Outlook 2016.” July 2016.

http://www.eia.gov/forecasts/aeo/

• M. J. Bradley & Associates. “EPA’s Clean Power Plan Summary of IPM Modeling Results.” March 4,

2016. http://www.mjbradley.com/sites/default/files/MJBA_CPP_IPM_Summary.pdf

• PJM Interconnection. “EPA’s Final Clean Power Plan Compliance Pathways Economic and Reliability

Analysis.” September 1, 2016. http://www.pjm.com/~/media/documents/reports/20160901-cpp-

compliance-assessment.ashx

• MISO Policy & Economic Studies Department. “MISO’s Analysis of EPA’s Final Clean Power Plan

Study Report DRAFT.” May 2016.

https://www.misoenergy.org/Library/Repository/Meeting%20Material/Stakeholder/PAC/2016/20

160518/20160518%20PAC%20Item%2002a%20DRAFT%20MISO%20Analysis%20of%20EPA%20Fin

al%20Clean%20Power%20Plan%20Study%20Report.pdf

www.synapse-energy.com | ©2016 Synapse Energy Economics Inc. All rights reserved. Tommy Vitolo

Renewable Energy Markets and the

Clean Power Plan (Part I)

Thomas Vitolo, Synapse

David Wooley, Keyes, Fox & Wiedman

Ed Holt, Ed Holt & Associates

Federal Carbon Pollution Standards & Renewables

David WooleyKeyes & Fox LLP

Oakland, CA

Renewable Energy Markets

Conference

San Francisco

October 17, 2016

Clean Air Act – Clean Power Plan (CPP)

• CPP is, potentially, very good for RE

• It is likely to be up-held in court

• Likely to be succeeded by stronger standards

• But, CPP will not automatically help RE –Advocacy needed now Engage with states to influence implementation

• RE companies need to structure operations in order to access CPP compliance market revenue

Ways CPP Can Help RE

• Increased Utility RE Procurement

• Emission Reduction Credit (ERC) & Allowance awards/trading

• State Allowance Auction Proceeds

• Increased wholesale & retail electric prices

• Helps secure RE policy supports (RPS, NEM)

• CEIP early action credits for wind and solar 2020-2022

We are not there yet

• Financial benefits, over long term, are potentially large

• RE investors will not automatically get a financial reward for lowering CO2 emissions

• Action needed now to secure them

“Allowance allocation may be the single-most important decision states will make ....”

States Will Make Key Decisions

• States will design compliance – in concert with– Air Quality Regulators, Utility Commissions, Utilities– And you

• Poorly designed state plan could:– RATE-BASED: Exclude renewables from ERC eligibilit– MASS BASED:

• Limit award of allowances to utility owned RE systems• Adversely affect existing voluntary RE markets• Deprive Corporate RE buyers of sustainablity claims and green

marketing

– Disqualify behind-the-meter RE from compliance market– Compliance plans that rely exclusively on coal-to-gas shift

could drop ERC and Allowance values to zero

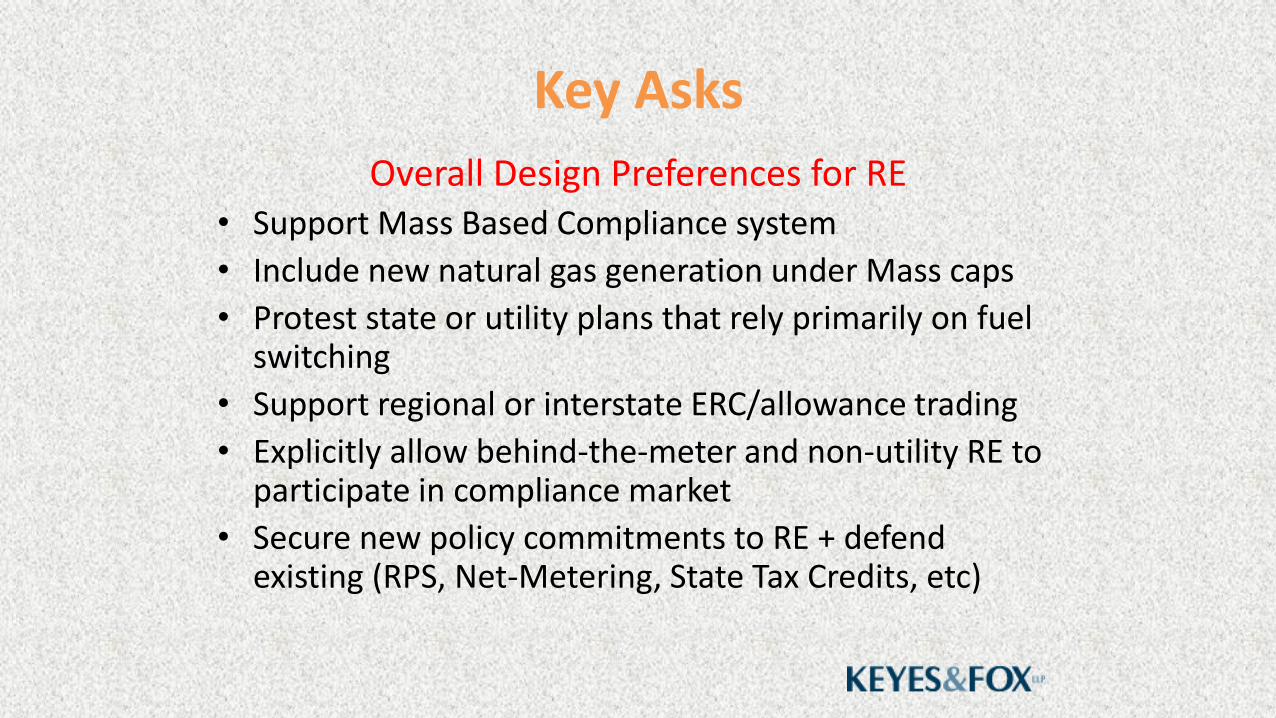

Key Asks

Overall Design Preferences for RE• Support Mass Based Compliance system

• Include new natural gas generation under Mass caps

• Protest state or utility plans that rely primarily on fuel switching

• Support regional or interstate ERC/allowance trading

• Explicitly allow behind-the-meter and non-utility RE to participate in compliance market

• Secure new policy commitments to RE + defend existing (RPS, Net-Metering, State Tax Credits, etc)

Key AsksRate-based Plans

• Make RE Eligible for ERCs

– “A state may … restrict the definition of eligible resource by allowing only some of the technologies identified by EPA to generate ERCs”

• Clear, easy-to-follow, mechanisms to award ERCs

• ERC Tracking System

• Mechanisms to qualify of Independent Verifiers

• Participate in CEIP Early reductions program

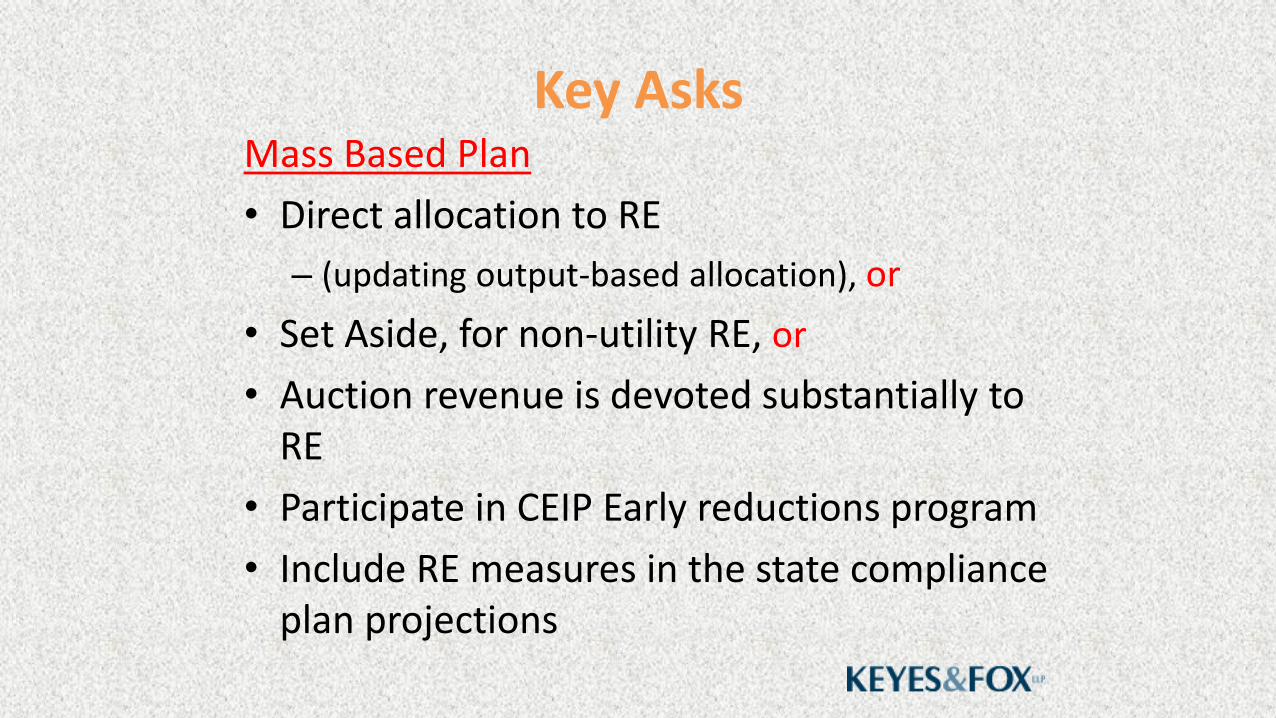

Key AsksMass Based Plan

• Direct allocation to RE

– (updating output-based allocation), or

• Set Aside, for non-utility RE, or

• Auction revenue is devoted substantially to RE

• Participate in CEIP Early reductions program

• Include RE measures in the state compliance plan projections

What’s it Worth?Too Early to Tell

Near Term 2022-2025

• In some states – $0/ton/mWh

• In many states – $1-5/ton

– $.4 to $4/mWh

• Potentially more in states that restrict interstate trading & have steep emission reduction target

Long Term 2025-2030

• Expect allowances to trade between $5 and $20 a ton

– ERCs $1 to $15/mWh

• Potentially higher if CPP is tightened

– Could occur before 2030

– Likely after 2030

Principle Advocacy Venues

• State air quality regulators - Allow utility-scale and behind-the meter RE to count

– Be a stakeholder early in the decision making

– Comment on state implementation plans design

• State utility commissions – resource planning

• Governors’ offices

• Engage utilities on compliance planning

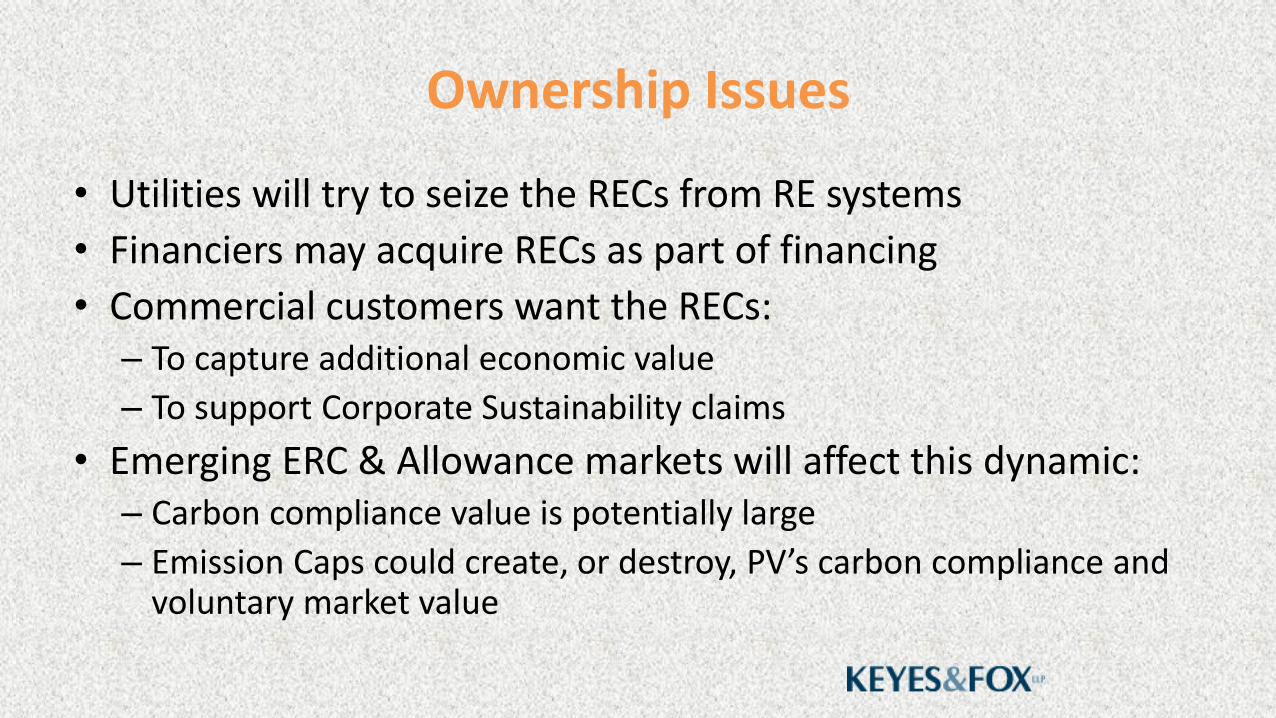

Ownership Issues

• Utilities will try to seize the RECs from RE systems

• Financiers may acquire RECs as part of financing

• Commercial customers want the RECs:– To capture additional economic value

– To support Corporate Sustainability claims

• Emerging ERC & Allowance markets will affect this dynamic:– Carbon compliance value is potentially large

– Emission Caps could create, or destroy, PV’s carbon compliance and voluntary market value

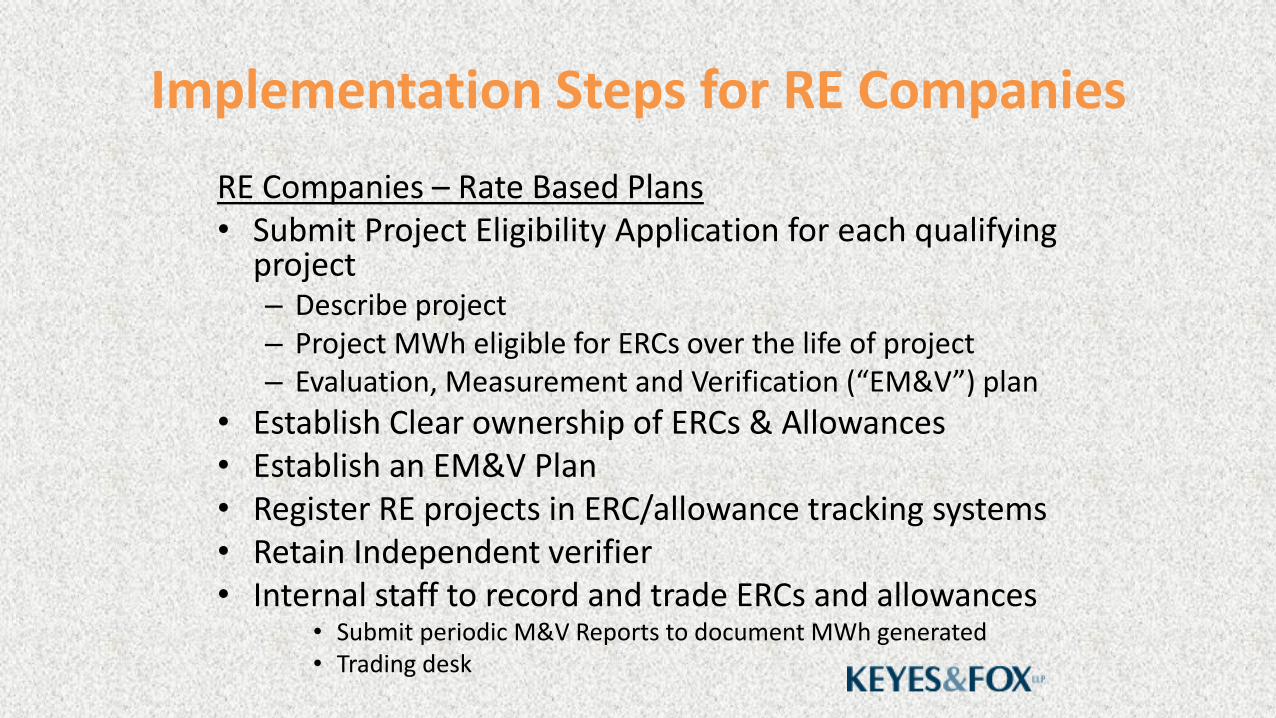

Implementation Steps for RE Companies

RE Companies – Rate Based Plans• Submit Project Eligibility Application for each qualifying

project– Describe project– Project MWh eligible for ERCs over the life of project– Evaluation, Measurement and Verification (“EM&V”) plan

• Establish Clear ownership of ERCs & Allowances• Establish an EM&V Plan• Register RE projects in ERC/allowance tracking systems • Retain Independent verifier• Internal staff to record and trade ERCs and allowances

• Submit periodic M&V Reports to document MWh generated • Trading desk

Conclusion• Renewables can significantly reduce carbon

pollution in the electric sector • Carbon Pollution Standards could help expand RE

if the rules are properly designed to:– Allow solar to count toward carbon emission

reduction compliance– Preserve private property rights to carbon reduction

attributes of solar generation

• Renewable industry must– Be heard on the state implementation plans, and – Set up internal mechanism to manage ERCs and

allowances.

Keyes&FoxDistributed Generation Law

• Interconnection• Net Metering • Permitting• Contracts• Transmission• Rate Design • Utility Regulation• Storage & Demand

Response• Emission & Renewable

Energy Credits

DAVID WOOLEY436 14th Street

Oakland, CA 94706415-271-1135 cell

Renewable Energy Credit Registries

• REC Registries exist throughout US

• Could be used to preserve private property rights & ERC/Allowance value

• Increase confidence in RE as CO2 control measure

Renewable Energy Markets and the

Clean Power Plan (Part I)

Thomas Vitolo, Synapse

David Wooley, Keyes, Fox & Wiedman

Ed Holt, Ed Holt & Associates

The Clean Power Plan and Voluntary Renewable Energy Claims

Renewable Energy Markets

San Francisco

17 October 2016

28 Headland Road

Harpswell, ME 04079

Tel. 207.798.4588

Outline

Interactions between VRE and the CPP

VRE and rate-based plans

Buyer’s perspective

VRE and mass-based plans

Buyer’s perspective

Ed Holt & Associates, Inc.

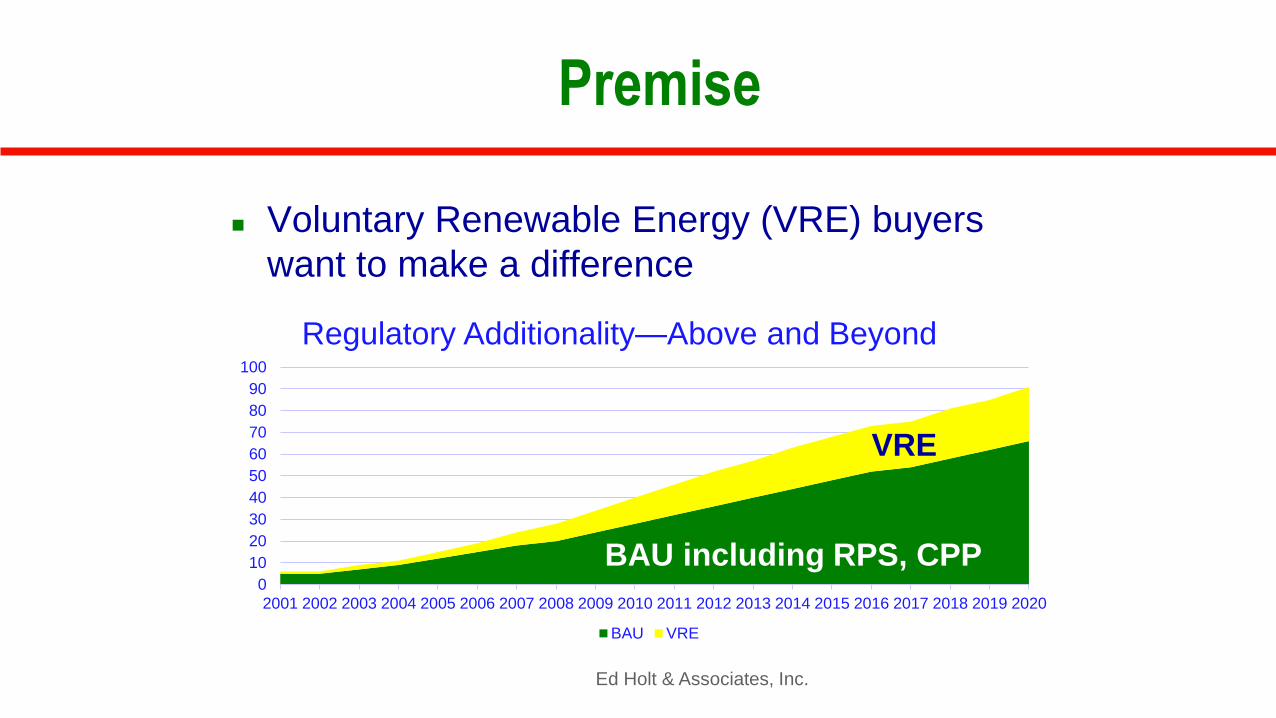

Premise

Voluntary Renewable Energy (VRE) buyers

want to make a difference

Ed Holt & Associates, Inc.

0

10

20

30

40

50

60

70

80

90

100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Regulatory Additionality—Above and Beyond

BAU VRE

BAU including RPS, CPP

VRE

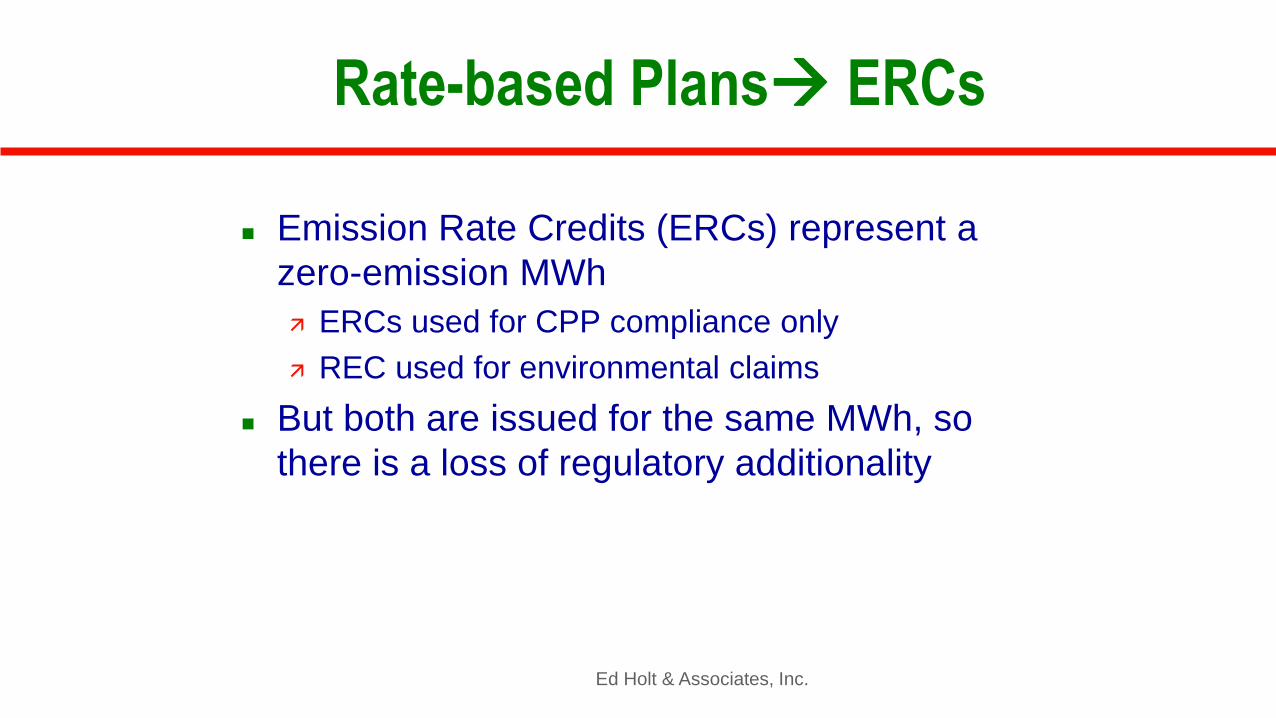

Rate-based Plans ERCs

Emission Rate Credits (ERCs) represent a

zero-emission MWh

ERCs used for CPP compliance only

REC used for environmental claims

But both are issued for the same MWh, so

there is a loss of regulatory additionality

Ed Holt & Associates, Inc.

Ed Holt & Associates, Inc.

Not All RE Will Be Issued ERCs

All generation

certificates

RECs

ERCs: RE, EE,

nuclear, EGU

efficiency, gas

for coal

substitution

RE ERCs from

new capacity

post-2012

Although overlapping,

REC and ERCs still

separate instruments

Generators must

apply for ERCs

Buy around the ERC eligibility RE that began construction pre-2013*

RE generated 2013-2021 (no ERCs issued**)

Buy from generators that don’t apply for ERCs Accompanied by attestation that no ERCs were issued

for the energy produced

Buy (and retire) ERCs to match renewable energy purchases PPA or virtual PPA could specify the purchase of both

RECs and ERCs

Ed Holt & Associates, Inc.

* May be limited by Green-e vintage eligibility

** Exception for CEIP 2020-2021

What Can a Buyer Do About It?

Ed Holt & Associates, Inc.

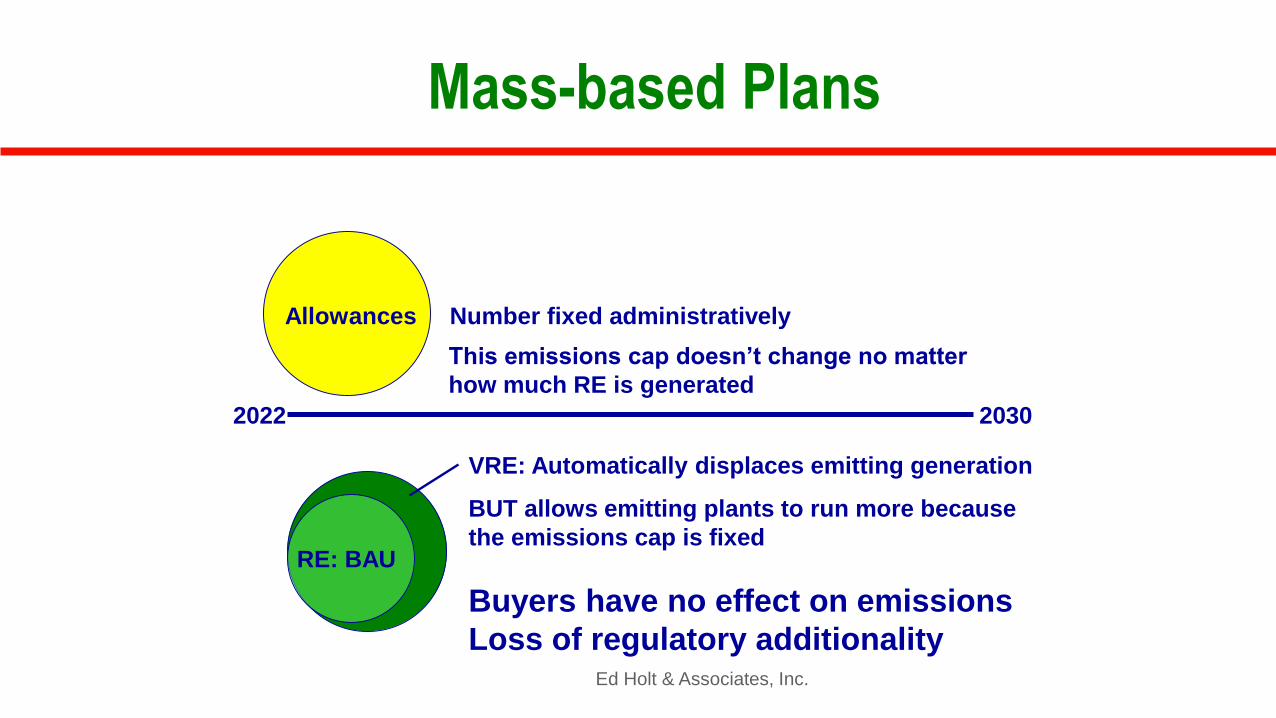

Mass-based Plans

2022 2030

Allowances Number fixed administratively

RE: BAU

VRE: Automatically displaces emitting generation

This emissions cap doesn’t change no matter

how much RE is generated

BUT allows emitting plants to run more because

the emissions cap is fixed

Buyers have no effect on emissions

Loss of regulatory additionality

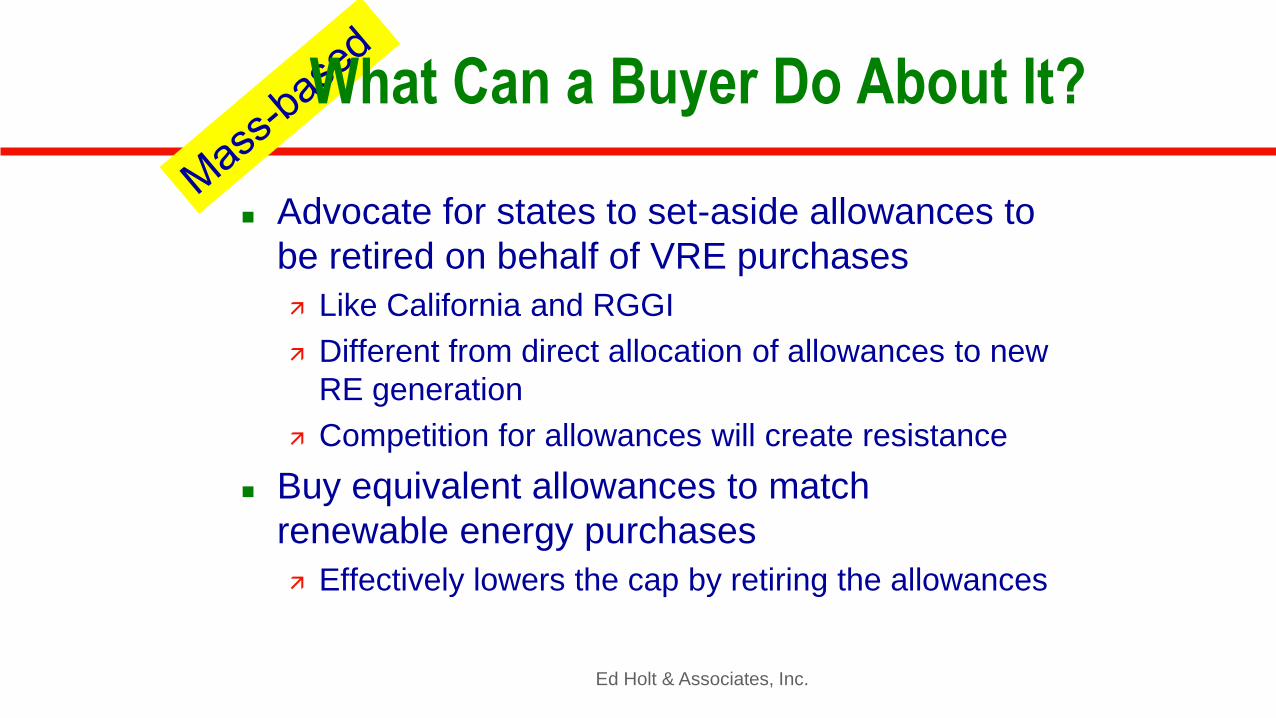

Advocate for states to set-aside allowances to

be retired on behalf of VRE purchases

Like California and RGGI

Different from direct allocation of allowances to new

RE generation

Competition for allowances will create resistance

Buy equivalent allowances to match

renewable energy purchases

Effectively lowers the cap by retiring the allowances

Ed Holt & Associates, Inc.

What Can a Buyer Do About It?

Thank you!

Questions?