renewable asset risk management

TRANSCRIPT

Manuele Monti, Ph.D.GDF Suez Energia Italia Energy Management - Power & Risk Portfolio

Renewable asset risk management for fixed price offers

Presentation Title

Mercati energetici e metodi quantitativi: un ponte tra Università e Aziende

22-23 Maggio, Padova

E' vietata la riproduzione , e ridistribuzione sotto ogni forma, anche parziale, di immagini, testi o contenuti senza autorizzazione dell’autore e di GDF Suez Energia Italia S.p.A.Le indicazioni modellistiche, le conclusioni, i prodotti strutturati mostrati sono proprietà industriale di GDF Suez. I riferimenti allo sviluppo quantitativo, all’open innovation e alle reti di conoscenza rappresentano libera ed individuale espressione intellettuale dell’autore.Copyright all contenents reserved. For English conditions and disclaimer disclaimer please contactthe author.

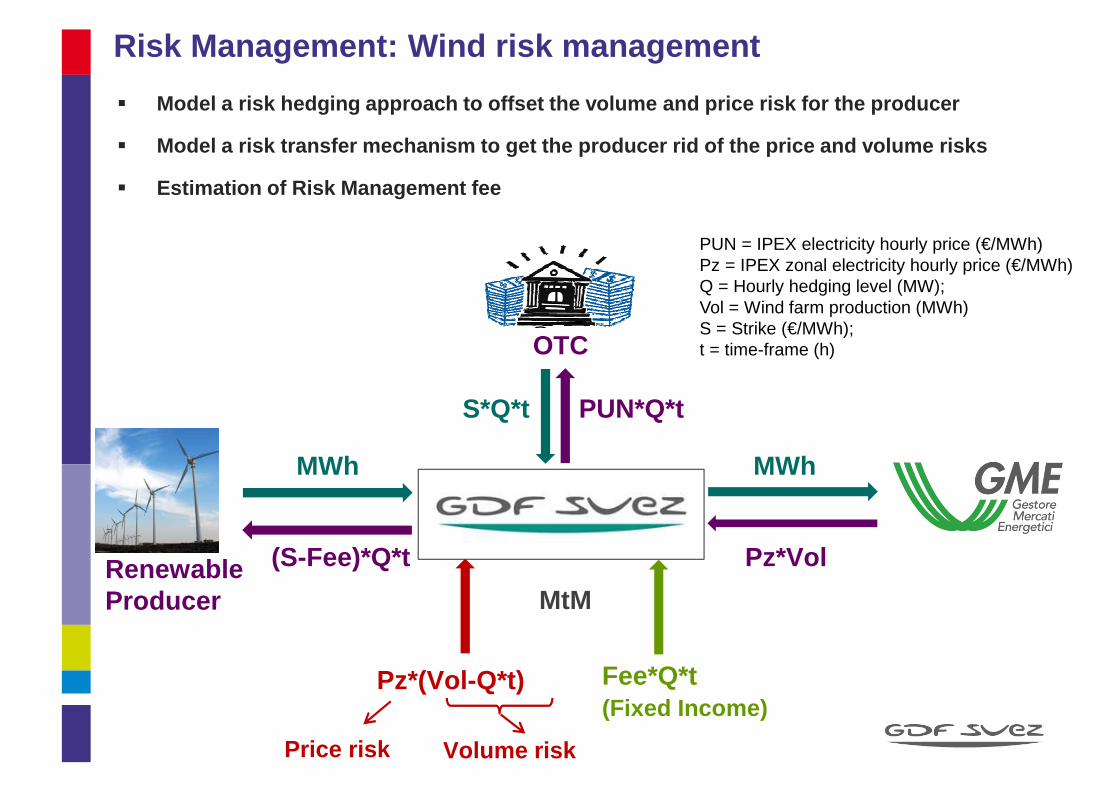

� Model a risk hedging approach to offset the volume and price risk for the producer

� Model a risk transfer mechanism to get the producer rid of the price and volume risks

� Estimation of Risk Management fee

MWh

(S-Fee)*Q*t

MWh

Pz*Vol

S*Q*t PUN*Q*t

RenewableProducer

OTC

PUN = IPEX electricity hourly price (€/MWh)Pz = IPEX zonal electricity hourly price (€/MWh)Q = Hourly hedging level (MW);Vol = Wind farm production (MWh)S = Strike (€/MWh);t = time-frame (h)

Pz*(Vol-Q*t) Fee*Q*t(Fixed Income)

Price risk Volume risk

MtM

Risk Management: Wind risk management

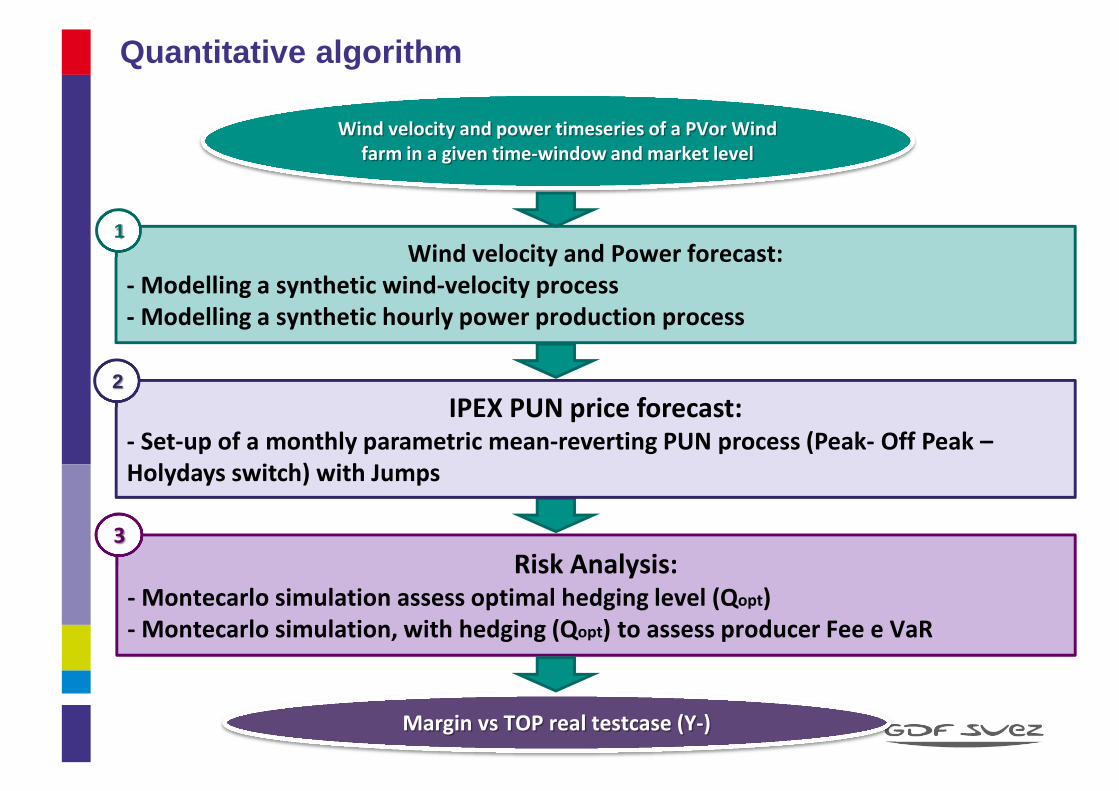

Margin vs TOP real testcase (Y-)

Wind velocity and power timeseries of a PVor Wind

farm in a given time-window and market level

Wind velocity and Power forecast:

- Modelling a synthetic wind-velocity process

- Modelling a synthetic hourly power production process

1

Risk Analysis:- Montecarlo simulation assess optimal hedging level (Qopt)

- Montecarlo simulation, with hedging (Qopt) to assess producer Fee e VaR

3

IPEX PUN price forecast:- Set-up of a monthly parametric mean-reverting PUN process (Peak- Off Peak –

Holydays switch) with Jumps

2

Quantitative algorithm

0 5 10 15 20 25 300

200

400

600

800Wind velocity (V)

[m/s]

Nsa

mpl

es

0 10 20 30 40 50 60 70

500

1000

1500Power output (Pout)

[MW]

V Cut-Off

λexp; kexp

Wind velocity and Power forecast:

- Modelling a synthetic wind-velocity process

- Modelling a synthetic hourly power production process

1

Wind modelization

From the experimentally revealed V/P

timeseries a Weibull distribution is

parametrized by the mean of a Maximum

Likelyhood method; ����λexp; kexp .

1a

The synthetic power process is obtained by

convolution of the wind process through

the wind-power curve. -10 0 10 20 30 40 50 60 70 800

200

400

600

800

1000

1200

1400

1600

[MW]

Oss

erva

zio

ni s

ul p

roce

sso

Potenza

Synthetic: power

Synthetic: wind

Experimental

A simulation of the synthetic velocity

distribution with given Weibull parameters

is thereafter obtained.

The farm wind velocity-energy production

curve is modelled by a polynomial

regression on the experimental power load

From the experimentally revealed V/P

timeseries a Weibull distribution is

parametrized by the mean of a Maximum

Likelyhood method; ����λexp; kexp .

1b

Wind asset modelization

1a

Wind velocity and Power forecast:

- Modelling a synthetic wind-velocity process

- Modelling a synthetic hourly power production process

1

PV power plant assessment

2 4 6 8 10 12 14 16 18 20 22 240

1

2

3

4

5

6

Hour

Pow

er [

MW

]

Jan

FebMar

Apr

May

JunJul

Aug

Sep

OctNov

Dic

A preliminary assessment on the PV plant average daily profile was performed for each month of the year, based on the historical data of the plant from May 2011 to Dec 2013.

The results are plotted in the figure above.

Plant data Description

Installed power [kW] 7775,48

Expected yearly prodction [kWh]10.574.000

Power module unit [W]255

Efficiency module [%]

Number of modules30492

Tilt [ ° ]30

Direction [ ° ]0

Surface [m2]150.000

Latitude40°22' 14''

Longitude18° 06' 07''

Total efficiency* [%]82

* This accounts for all the losses up to the immission point

PV power plant assessment

2 4 6 8 10 12 14 16 18 20 22 240

1

2

3

4

5Yearly average production PK hedge

hour

Pow

er [

MW

]

2 4 6 8 10 12 14 16 18 20 22 24-2

0

2

4

hour

Pow

er [

MW

]

Residual exposure

Production

Hedge

The idea is to hedge the expected production forecast profile with a standard OTC PK Calendar product, and bear the residual exposure in the EM portfolio.The deterministic production of a PV power plant determines a long position in the central hours (h 11-18) and a short position in the peripheral hours (8-11 and 18-21)

This residual short exposure matches the double peaks of the PUN prices (residual demand covered by conventional power generation). This generates a negative exposure in the EM portfolio (around 30% of the total production).

Short

Short

Long

+

--

+LongShort

-Short

-

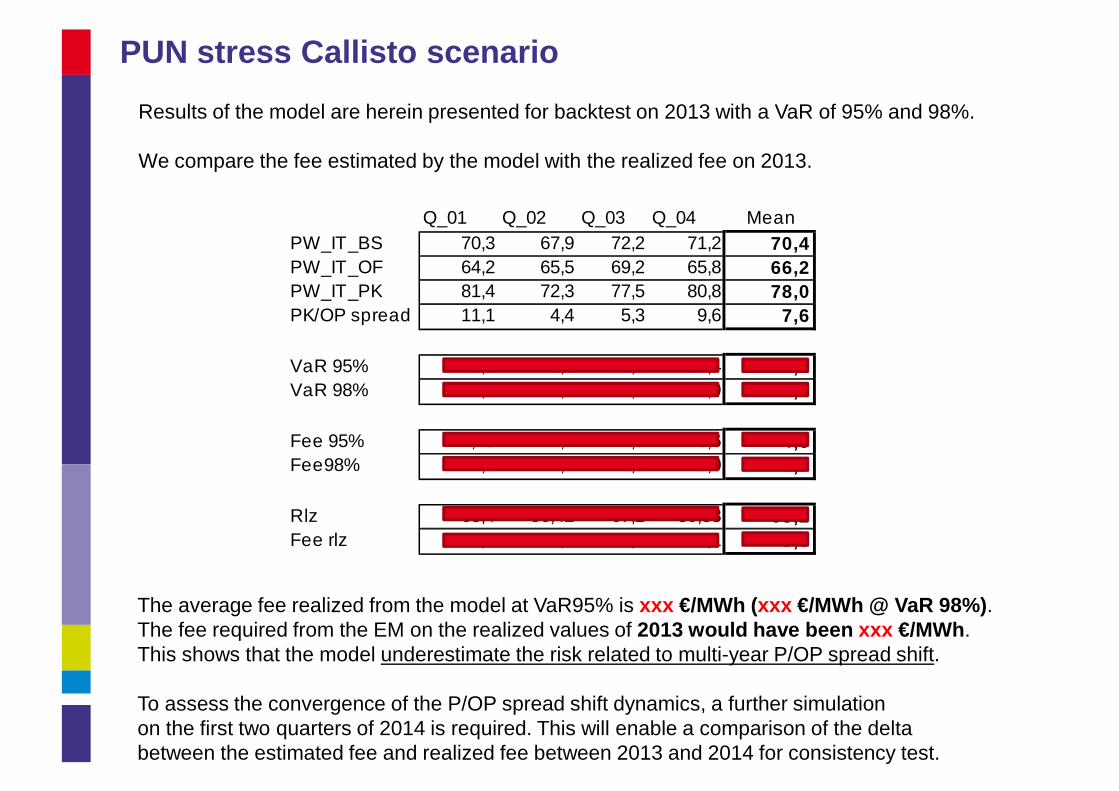

PUN stress Callisto scenario

0 1000 2000 3000 4000 5000 6000 7000 8000 90000

50

100

150

200

250

300

350

hour

Pric

e [€

/MW

h]

Product [€/MWh] Q_01 Q_02 Q_03 Q_04 Mean

PW_IT_BS 70,3 67,9 72,2 71,2 70,4

PW_IT_OF 64,2 65,5 69,2 65,8 66,2

PW_IT_PK 81,4 72,3 77,5 80,8 78,0

The power price scenario was stressed by using 1000 scenarios generated by Callisto tool:

• Reference date: 31/12/2012• Simulation window: 01/01/2013 –

31/12/2013• Hourly granularity

The scenarios generated match as an averagethe FWD quarterly prices, and the intraday hourly shape realized on the learning period of the model (01/01/2012 – 31/12/2012)

Multivariate Ornstein–Uhlenbeck process with Jumps:

= deterministic mean-reverting transition matrix

= unconditional expectation vector (based on historical and FWD screen prices)

= dispersion square matrix (namely scatter generator, historical prices only)

= vector of independent Wiener processes

= UOL multivariate processes vector

= Jump regimes vector (from seasonal statistics and hybrid physical market models)

IPEX PUN price forecast:- Set-up of a monthly parametric mean-reverting PUN process (Peak- Off Peak – Holydays switch) with Jumps

2

Electricity price PUN modelization

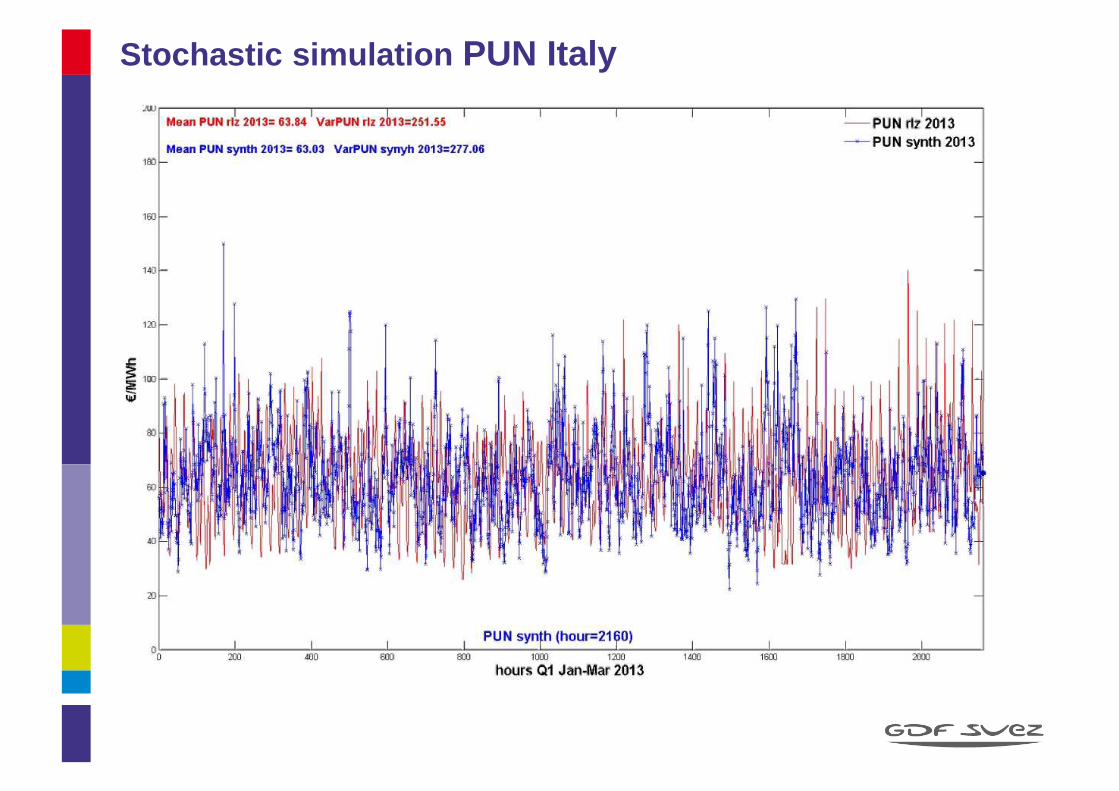

Stochastic simulation PUN Italy

Stochastic simulation PUN Italy

PUN stress Callisto scenario

Q_01 Q_02 Q_03 Q_04 MeanPW_IT_BS 70,3 67,9 72,2 71,2 70,4PW_IT_OF 64,2 65,5 69,2 65,8 66,2PW_IT_PK 81,4 72,3 77,5 80,8 78,0PK/OP spread 11,1 4,4 5,3 9,6 7,6

VaR 95% 70,2 70,6 72,5 81,4 73,7VaR 98% 69,8 70,2 72,2 80,9 73,3

Fee 95% 11,25 1,7 4,9 -0,6 4,3Fee98% 11,6 2,1 5,3 0,0 4,7

Rlz 68,4 56,42 67,2 80,88 68,2Fee rlz 13,0 15,9 10,3 -0,1 9,8

Results of the model are herein presented for backtest on 2013 with a VaR of 95% and 98%.

We compare the fee estimated by the model with the realized fee on 2013.

The average fee realized from the model at VaR95% is xxx €/MWh (xxx €/MWh @ VaR 98%).The fee required from the EM on the realized values of 2013 would have been xxx €/MWh.This shows that the model underestimate the risk related to multi-year P/OP spread shift.

To assess the convergence of the P/OP spread shift dynamics, a further simulationon the first two quarters of 2014 is required. This will enable a comparison of the deltabetween the estimated fee and realized fee between 2013 and 2014 for consistency test.

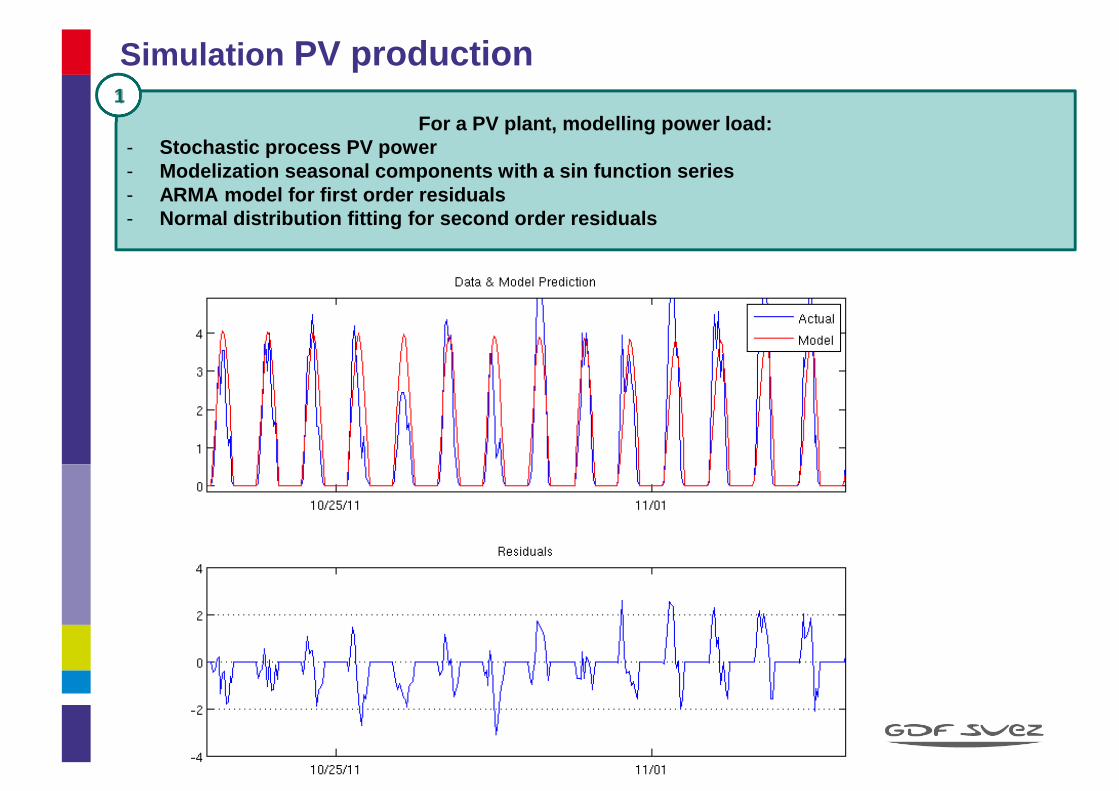

Simulation PV production

For a PV plant, modelling power load:- Stochastic process PV power- Modelization seasonal components with a sin function ser ies- ARMA model for first order residuals- Normal distribution fitting for second order residuals

1

For a PV plant, modelling power load:- Stochastic process PV power- Modelization seasonal components with a sin function ser ies- ARMA model for first order residuals- Normal distribution fitting for second order residuals

1

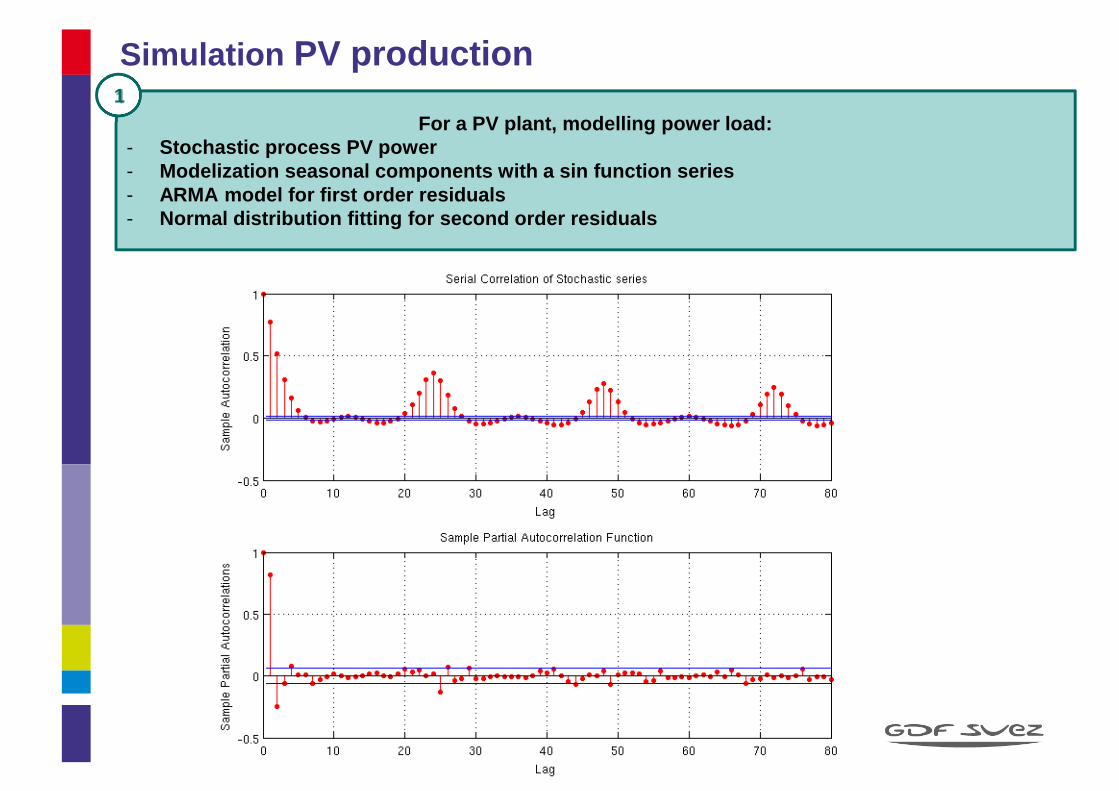

Simulation PV production

For a PV plant, modelling power load:- Stochastic process PV power- Modelization seasonal components with a sin function ser ies- ARMA model for first order residuals- Normal distribution fitting for second order residuals

1

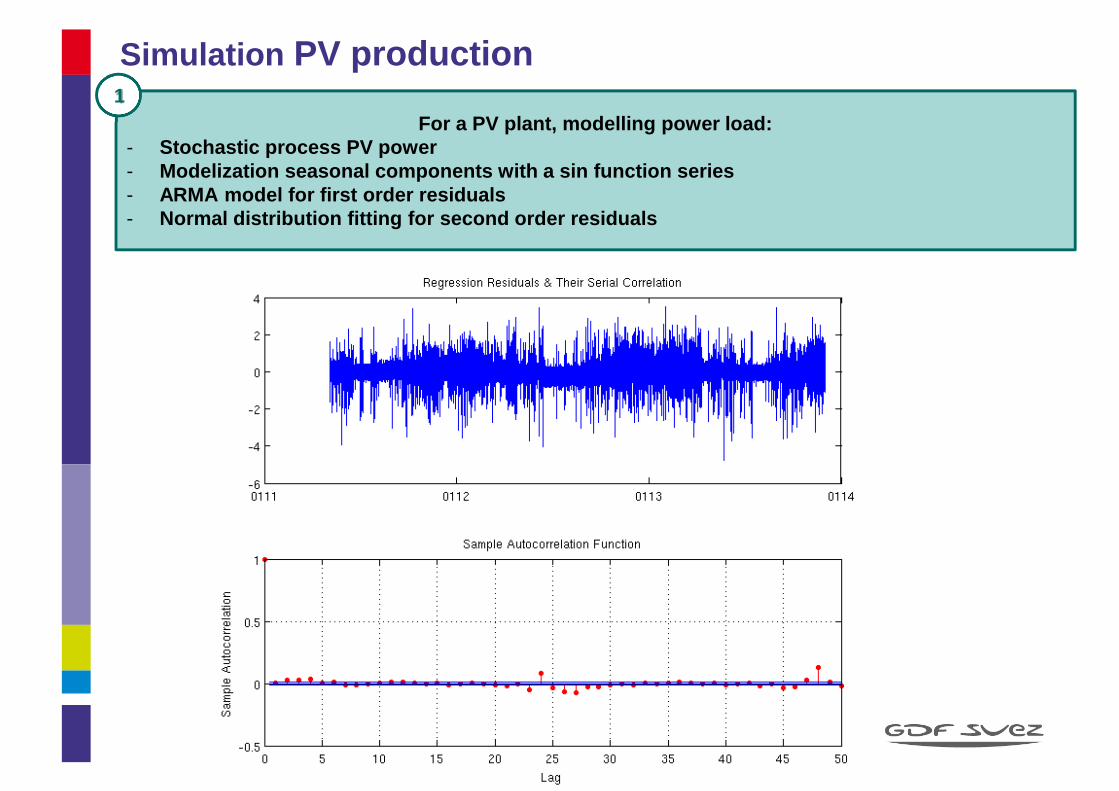

Simulation PV production

For a PV plant, modelling power load:- Stochastic process PV power- Modelization seasonal components with a sin function ser ies- ARMA model for first order residuals- Normal distribution fitting for second order residuals

1

Simulation PV production

17.2 17.4 17.6 17.8 18 18.2 18.4 18.60

50

100

150

200

250

300

350

400

450

500

MW

N o

bse

rva

tion

s M

on

teca

rlo (

out

of 4

000

pro

cess

es)

Psynth

mean

mean rlz 2010 ≈≈≈≈ 17.9 MW ≈≈≈≈ Q

opt

Pmean ~ Q

Risk Analysis:- Montecarlo simulation assess optimal hedging level (Qopt)

- Montecarlo simulation, with hedging (Qopt) to assess producer Fee e VaR

3

A first MC run generates the wind velocity

and power processes. The frequency

distribution determinates the optimal

hedging level Qopt.

3a

MC simulation for production

Risk Analysis:- Montecarlo simulation assess optimal hedging level (Qopt)

- Montecarlo simulation, with hedging (Qopt) to assess producer Fee e VaR

-3 -2.5 -2 -1.5 -1 -0.5 0 0.5 1 1.5 2 2.5 30

50

100

150

200

250

300

350

400

450

500

€/MWh

N o

bse

rva

tions

Mon

teca

rlo (

out o

f 40

00

pro

cess

es)

Exposure Delta

mean rlz 2010 ≈≈≈≈ -0.28 €/MWh

95%confidence

95%confidence

fee @ 1.5 €/MWh

A second MC run generates the exposure

to PUN of the residual production

above/behind Qopt

The producer fee is at 95% confidence.

VaR 95% ~ Fee

A first MC run generates the wind velocity

and power processes. The frequency

distribution determinates the optimal

hedging level Qopt.

3

MC simulation for residual exposure VaR

3a

3b